Sample Category Title

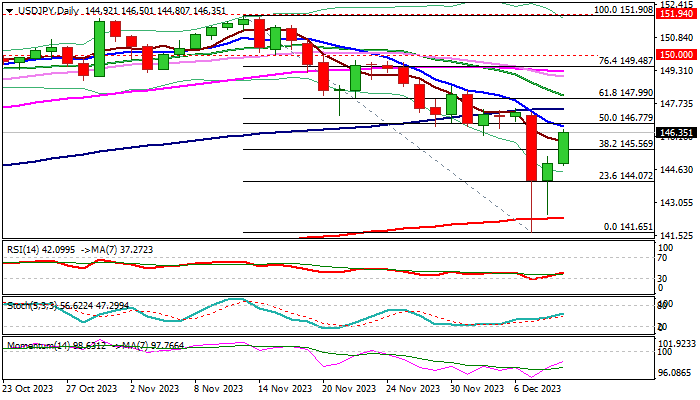

USD/JPY: Extends Advance on Fresh Dovish Comments from BoJ

Bounce from last Thursday’s multi-month low and a bear-trap, extends into second consecutive day and accelerates on Monday.

The dollar benefited from stronger than expected US jobs data in November, which shifted the view about rate cuts in 2024, while BoJ softened the narrative about start of tightening its ultra-loose policy, by comments that there is a little need to end negative rates in December.

Fresh extension higher broke above pivotal Fibo barrier at 145.56 (38.2% of 151.90/141.65), close above which would add to bullish near-term outlook.

Bulls pressure next pivots at 146.70 zone (10DMA/50% retracement) which guards key 148.00 zone (Fibo 61.8%/20DMA/daily cloud base).

Daily studies are improving, as strong downside rejection and bear-trap under 200DMA, underpin the action, though 14-d momentum is still in negative territory and MA’s are predominantly in bearish configuration, keeping in play risk of recovery stall.

Daily close above 145.56 Fibo level (reverted to support) is needed to keep near-term bias with bulls.

Res: 146.70; 147.00; 147.51; 148.00.

Sup: 145.56; 144.80; 144.07; 142.37.

Sunset Market Commentary

Markets

The Japanese yen last week grabbed a lot of market attention over speeches by the Bank of Japan’s number 1 (governor Ueda) and shared number 2 (deputy governor Himino). Both fanned speculation over an imminent (ie December 19) policy shift, lifting Japanese yields and with it the yen. The currency hijacked the spotlights again today. A scoop by Bloomberg triggers sharp JPY underperformance with USD/JPY bouncing from <145 to 146.35 currently. EUR/JPY recoups much of last week’s losses to trade at 157.48. Compared to the intraday low (JPY high) seen last Thursday (in the wake of the Himino-Ueda comments), the pairs trade respectively 4.7 and 4.2 yen higher. The financial news agency citing people familiar with the matter reported that the Bank of Japan sees little need to rush policy normalization, which could have included ending the negative rate (-0.1%) experiment later this month. The people said the potential cost of waiting for more information, amongst others evidence of higher wage growth, wasn’t very high and thus worth it. We take note of today’s report but add that it has the BoJ’s modus operandi written all over it. In December last year as well as this summer, the BoJ did exactly the same: downplaying any speculation so that markets expected nothing before coming up with something after all and enjoy the benefit of market moves being exacerbated through liquidity-thinned circumstances. Moves in markets outside Japan are contained and there’s nothing strange about that given the jampacked eco calendar this week. It kicks off with US CPI numbers tomorrow ahead of the Fed on Wednesday. The ECB and Bank of England (and the Norges Bank and Swiss National Bank) meet on Thursday. PMI business confidence indicators for Japan over Europe and the UK to the US are due on Friday. US yields today add a few basis points, building on Friday’s gains and extending a recent recovery. German bunds outperform with the long end easing about 3 bps. The dollar trades flat against the euro and sterling ekes out a gain vs both of them. EUR/GBP is testing support again at the 0.8557 level. This reference was tested multiple times last week and is the last hurdle before EUR/GBP returning to the YtD low of 0.8492.

News & Views

November Norway CPI today provided the final input for the Norges Bank’s (NB) final policy decision this year on Thursday. Inflation was very volatile over the previous months with a substantial downside surprise in September and a big upside surprise in October. November came in slightly lower than consensus. Headline inflation rose 0.5% M/M and 4.8% Y/Y (was 1.0% and 4.0% in October). Core inflation decreased 0.2% M/M bringing the Y/Y-measure to 5.8% (from 6.0%). The rise in headline inflation was mainly driven by a 3.4% M/M rise in prices for housing, water, electricity gas and other fuels. Clothing and footwear rose 2.8% M/M. Furnishings, household equipment, and routine maintenance (-1.7%), recreation and culture (-0.9% M/M) and communications (-0.4% M/M) slowed inflation. Both headline and core inflation were below the NB September forecast of respectively 5.4% and 6.1%. The NB back then kept an additional interest rate hike on the table (4.25% currently), depending on the data. The weak krone was a concern at time of the November meeting. Since then, the NOK rebound was limited given the overall easing of monetary conditions due to lower LT yields in the US and EMU. The krone today weakened from EUR/NOK 11.75 to currently 11.795.

Inflation in the Czech Republic in November rose 0.1% M/M easing the Y/Y-measure to 7.3% Y/Y down from 8.5%. Prices of electricity were .6% M/M higher and natural gas 0.7%. Clothing and footwear rose (1.0%). Prices for transport and health dropped 1.1% and 1.4% M/M. Goods prices remained unchanged M/M while services still increased 0.2% M/M. The Czech national bank in its autumn report forecasted November CPI slightly slower at 7.1%. According to the CNB this was due to a less pronounced slowdown in the Y/Y growth in administered prices. By contrast, core inflation slowed slightly more markedly than forecasted (3.9% vs 4.0% expected). Annual food price inflation also slowed significantly further (-0.4% M/M and 1.7% Y/Y down from 3.5%). The CNB concludes that the strength and broad nature of the disinflationary trend is illustrated by low month-on-month price growth in recent months. The CNB sees inflation averaging 2.7% in Q1 2024. The market still isn’t sure whether today’s numbers will be enough for the CNB to start its cutting cycle in December. CZK today trades marginally stronger at EUR/CZK 24.36.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0722; (P) 1.0762; (R1) 1.0799; More...

Further decline remains in favor in EUR/USD despite loss of downside momentum. Sustained trading below 55 D EMA (now at 1.0770) will extend the fall from 1.1016 short term top to retest 1.0447 support. However, on the upside, above 1.0816 minor resistance will turn intraday bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

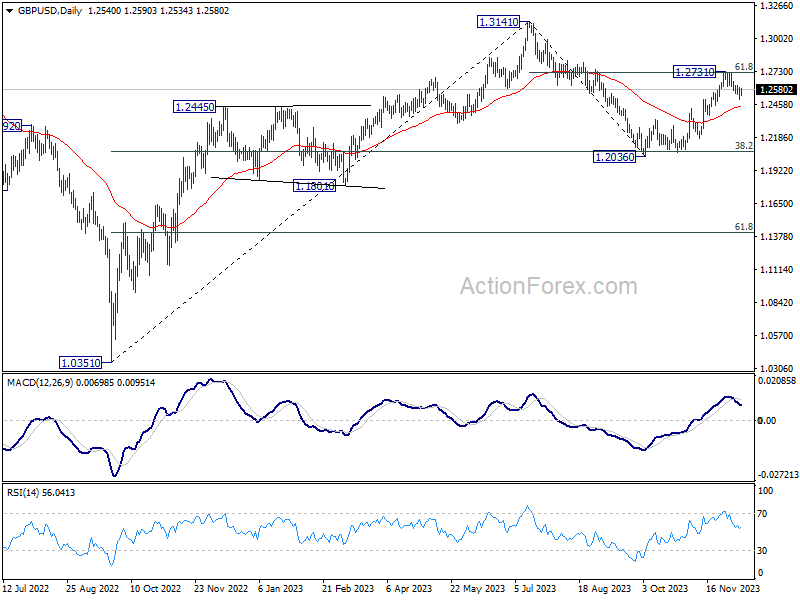

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2500; (P) 1.2551; (R1) 1.2600; More...

Further decline remains mildly in favor in GBP/USD despite today's recovery. Fall fall 1.2731 short term top would extend to 55 D EMA (now at 1.2445). Sustained break there will bring retest of 1.2036 low. However, firm break of 1.2611 will turn bias back to the upside for retesting 1.2731 resistance.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, that could still extend through 1.2731. But upside should be limited by 1.3141 o bring the third leg of the pattern. Meanwhile, sustained trading below 55 EMA will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again, and possibly below.

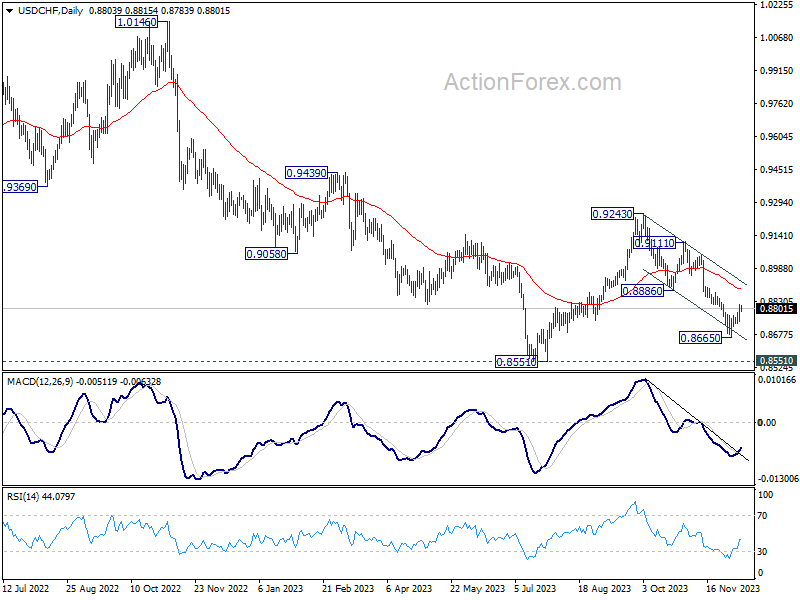

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8754; (P) 0.8788; (R1) 0.8834; More....

USD/CHF's rebound from 0.8665 short term bottom is still in progress. Intraday bias stays on the upside for 0.8886 support turned resistance first. Decisive break there will indicate that whole fall from 0.9243 has completed, and bring stronger rally to 0.9111 resistance next. On the downside, below 0.8727 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243 and above.

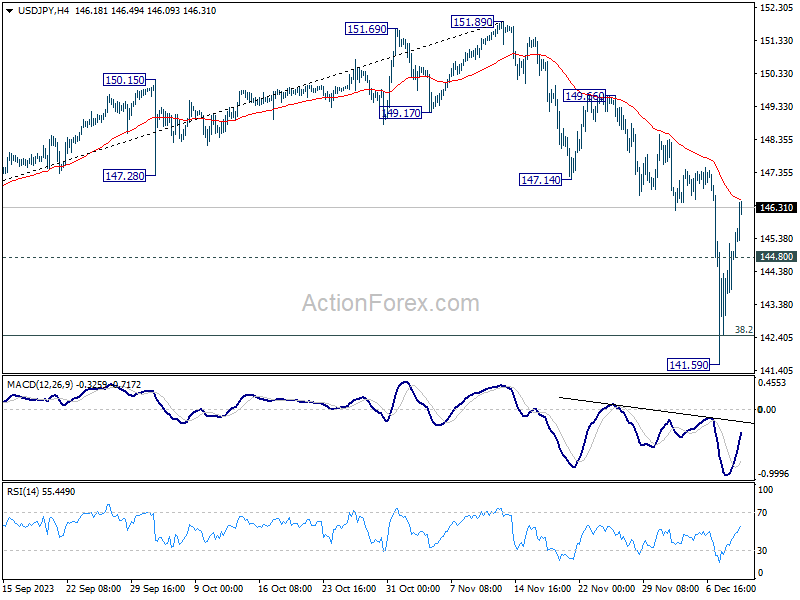

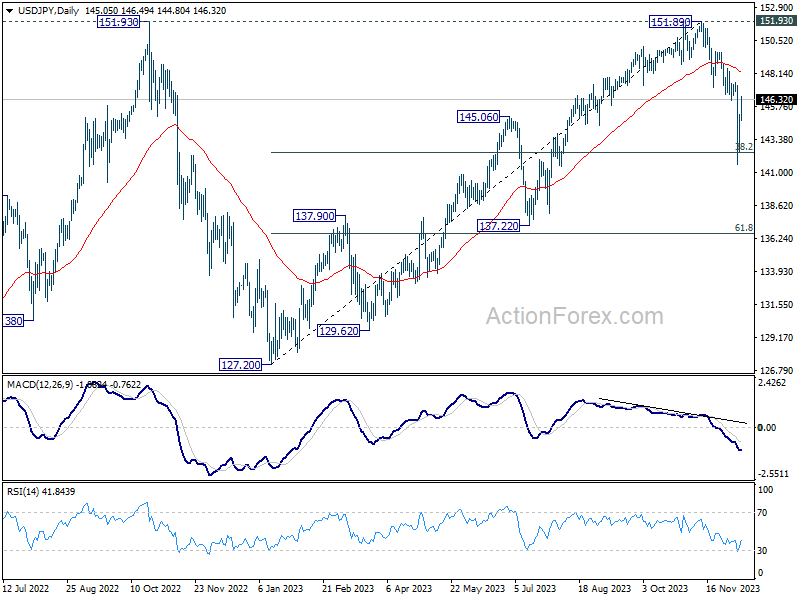

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.18; (P) 144.20; (R1) 145.89; More...

While USD/JPY's rebound from 141.59 is strong, outlook is unchanged for the moment. Upside should be limited be 147.14 support turned resistance. On the downside, below 144.80 minor support will turn bias to the downside for retesting 141.59. Break of 141.59 and sustained trading below 142.45 fibonacci level will pave the way to next fibonacci level at 136.63. However, firm break 147.14 will dampen the bearish view, and bring stronger rally to 149.56 resistance and above.

In the bigger picture, current fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. This will now remain the favored as long as 147.14 support turned resistance holds.

Yen Pullback Persists as Sterling and Dollar Gain Ahead of Crucial Events

Yen's near-term pullback has notably accelerated today. Some reports surfaced suggesting that the BoJ is not poised to abandon its negative rate policy anytime soon, with the earliest potential shift expected no sooner than April meeting. This stance isn't fundamentally new, as BoJ has consistently indicated that it requires time to assess Spring's wage negotiations before considering any policy changes. Additionally, the timing of the new economic projections aligns with April meeting, making it an opportune moment for the bank to explain any significant policy shifts. Despite this, the resilience seen in 10-year JGB yields indicates that traders are still hopeful for a minor policy adjustment, particularly concerning the yield curve control, later this month.

In other developments, British Pound is currently leading as the strongest currency for the day, followed by Canadian Dollar and then US Dollar. The Pound faces several critical economic releases, including tomorrow's UK job data and Wednesday's GDP figures, before BoE rate decision on Thursday. Meanwhile, Dollar is gearing up for tomorrow's CPI release, followed by FOMC rate decision and new economic projections on Wednesday. These upcoming releases suggest a significant week ahead for these currencies, with potential for notable market movements.

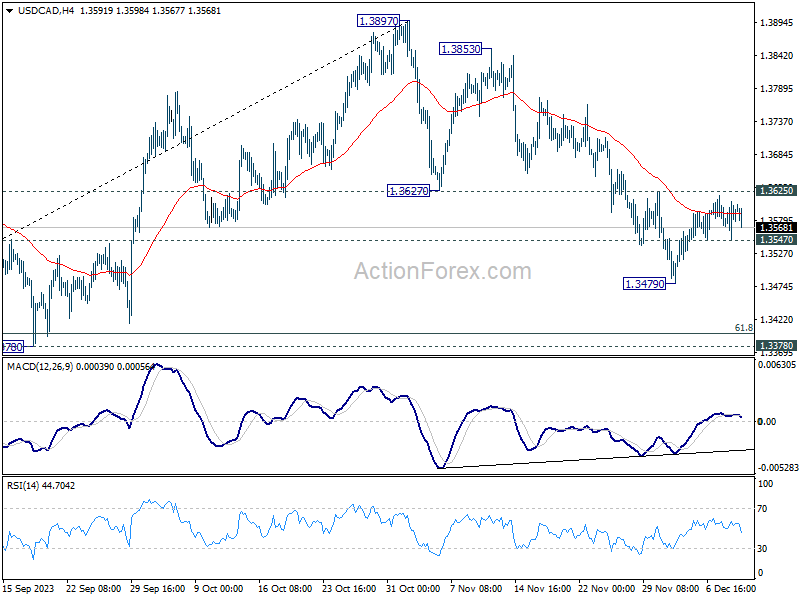

Technically, USD/CAD continued to lose upside momentum just ahead of 1.3625 support. Focus could be back to 1.3547 minor support in the next 24 hours. Break there will indicate rejection by 1.3625 resistance, and the fall from 1.3897 is in progress for another leg through 1.3479 towards 1.3378 support. Let's see how it goes.

In Europe, at the time of writing, FTSE is down -0.50%. DAX is up 0.10%. CAC is up 0.39%. Germany 10-year yield is down -0.016 at 2.264. UK 10-year yield is up 0.025 at 4.066. Earlier in Asia, Nikkei rose 1.50%. Hong Kong HSI fell -0.81%. China Shanghai SSE rose 0.74%. Singapore Strait Times fell -0.66%. Japan 10-year JGB yield rose 0.0052 to 0.779.

Q3 next year marked for SNB's first rate cut, economists predict

SNB is widely anticipated to maintain its key policy rate at 1.75%. However, the focus of market analysts and economists has shifted to speculating the timing of potential policy loosening. Recent polls conducted by Reuters and Bloomberg revealed a consensus among economists that SNB would only start cutting interest rates in Q3 next year.

The Reuters poll, conducted between December 5-11, gathered responses from 31 economists, all of whom unanimously agreed that SNB would hold the rate at 1.75% in the upcoming meeting. A substantial majority, approximately 70% (or 21 out of 31), predicted that SNB would maintain this rate until at least the third quarter of next year. Furthermore, a notable minority of 45% (or 13 out of 29) economists foresee the first rate cut by being pushed back to December 2024 or even later.

In comparison, a separate Reuters poll last week focusing on ECB revealed that around 57% of economists expect the ECB to implement at least one rate cut by the end of June. This comparison highlights expectations that SNB could starting cutting rates after ECB.

Additionally, a Bloomberg poll conducted from December 1-7 forecasts SNB initiate an interest rate cut in September next year. This would be followed by two more reductions of 25 bps each, anticipated in December 2024 and March 2025.

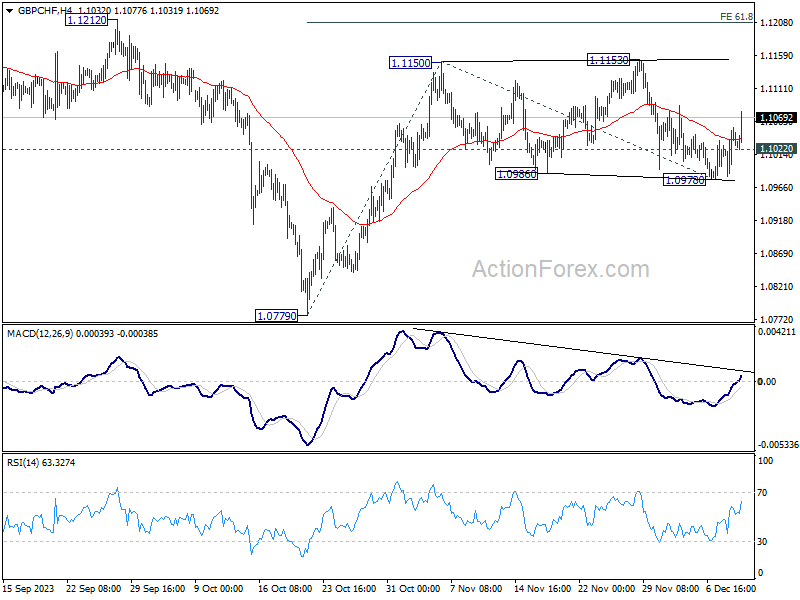

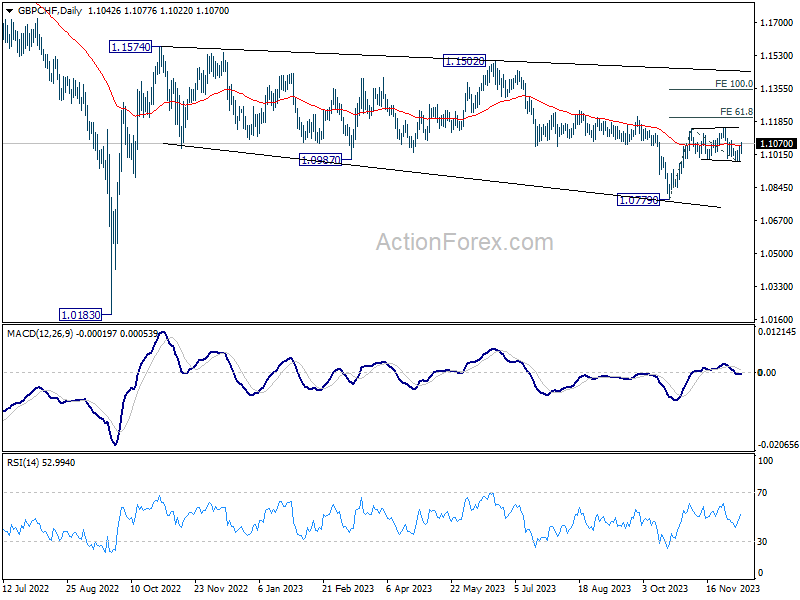

GBP/CHF rebounds, eyes 1.115 resistance

GBP/CHF stands as one of the focuses this week, particularly in light of the upcoming monetary policy decisions by both BoE and SNB. Market consensus widely anticipates that both central banks will maintain their current interest rates.

GBP/CHF's rebound from 1.0978 extends higher today. The development suggests that fall from 1.1153 has completed at 1.0978 already. More importantly, corrective pattern from 1.1150 might has completed with three waves down to 1.0978 too.

Further rise is now in favor as long as 1.1022 minor support hold. Decisive break of 1.1153 resistance will confirm resumption of whole rise from 1.0779. GBP/CHF should then target 61.8% projection of 1.0779 to 1.1150 from 1.0978 at 1.1199, or even further to 100% projection at 1.1341.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.18; (P) 144.20; (R1) 145.89; More...

While USD/JPY's rebound from 141.59 is strong, outlook is unchanged for the moment. Upside should be limited be 147.14 support turned resistance. On the downside, below 144.80 minor support will turn bias to the downside for retesting 141.59. Break of 141.59 and sustained trading below 142.45 fibonacci level will pave the way to next fibonacci level at 136.63. However, firm break 147.14 will dampen the bearish view, and bring stronger rally to 149.56 resistance and above.

In the bigger picture, current fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. This will now remain the favored as long as 147.14 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | 5.7 | 5.6 | 5.4 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 2.30% | 2.50% | 2.40% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | -13.60% | -20.60% |

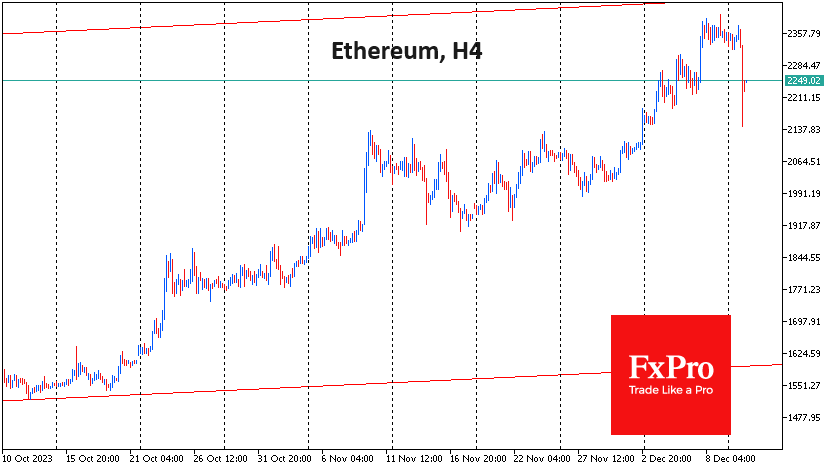

The Flash Sell-off in Crypto?

Market Picture

A wave of profit-taking hit the cryptocurrency market on Monday morning. It seems that the failure of cryptocurrencies to rise over the weekend caused players to pull stop orders very close to market prices, and we saw a massive exit from long positions in low liquidity before the regular session in Asia. Strong demand for risk assets in traditional markets suggests that the market will try to get back on its previous growth track.

Bitcoin started the day at $43.8K, soon fell to $40.7K, and then stabilised at $42.1K, losing 4% since the start of the day. This quick reload did not break the bullish trend. In our view, it will remain in force if Bitcoin manages to hold above $40K.

The sudden sell-off proved even harder for altcoins. At one point, Ethereum was losing over 9%, XRP was losing over 10%, Solana collapsed by 13%, and Cardano lost 14%. The largest altcoins have already recovered about half of those losses. The sell-off attracted buyers who were waiting for lower prices to enter the market, and the market gave them that chance.

News Background

Spot bitcoin ETFs could raise more than $2.4bn as early as the first quarter of 2024, according to asset management firm VanEck. Bitcoin is expected to take away a significant market share from gold. The inflow of funds may reach $40.4bn in two years.

Bitcoin will hit a new all-time high in the fourth quarter of 2024, potentially driven by ‘political events and regulatory changes following the U.S. presidential election’, VanEck predicts.

A new Glassnode report notes significant fund flows on cryptocurrency exchanges, which could suggest institutional investors are preparing for spot ETFs.

Société Générale, one of France’s largest banks, plans to become the first traditional financial institution to list its stablecoin on a cryptocurrency exchange.

CoinGecko estimates that more than half of the world’s countries have already legalised cryptocurrencies in some form. The best example is Europe, where 39 out of 41 countries have already legalised cryptocurrencies.

Authorities in El Salvador announced the launch of an emigration programme that will offer residency permits and a chance to obtain citizenship for crypto investments of $1m in Bitcoin or USDT.

GBP/CHF rebounds, eyes 1.115 resistance

GBP/CHF stands as one of the focuses this week, particularly in light of the upcoming monetary policy decisions by both BoE and SNB. Market consensus widely anticipates that both central banks will maintain their current interest rates.

GBP/CHF's rebound from 1.0978 extends higher today. The development suggests that fall from 1.1153 has completed at 1.0978 already. More importantly, corrective pattern from 1.1150 might has completed with three waves down to 1.0978 too.

Further rise is now in favor as long as 1.1022 minor support hold. Decisive break of 1.1153 resistance will confirm resumption of whole rise from 1.0779. GBP/CHF should then target 61.8% projection of 1.0779 to 1.1150 from 1.0978 at 1.1199, or even further to 100% projection at 1.1341.

GBP/USD – Pound Edges Higher ahead of UK Job Data

- UK to release employment report on Tuesday

- US nonfarm employment payrolls beats forecast and rise to 199,000

The British pound is showing little movement at the start of the week. In Monday’s European session, GBP/USD is trading at 1.2576, up 0.22%.

It’s a busy week for UK releases which could translate into volatility from the British pound. The UK releases employment data on Tuesday, GDP on Wednesday, followed by the Bank of England rate decision on Thursday.

BoE eyes employment report

The UK employment report will be closely watched by the BoE, which is expected to hold the cash rate at 5.25% for a third straight time. The UK labour market has remained strong despite the BoE’s aggressive tightening and high wage growth continues to drive inflation. The unemployment rate is expected to tick higher from 4.2% to 4.3% while wages including bonuses are expected to ease to 7.7%, down from 7.9%.

BoE Governor Bailey had a hawkish message for the markets last week, saying that interest rates could remain at current levels for “an extended period” in order to bring inflation back down to the 2% target. Inflation has been falling sharply, but the current clip of 4.9% remains much higher than the target and the BoE doesn’t want to encourage talk of a rate hike, which could ease financial conditions and push inflation higher. The markets, however, have priced in rate cuts in mid-2024.

US nonfarm payrolls dampens rate-cut expectations

Friday’s US nonfarm payrolls came in at 199 thousand in November, above the market consensus of 180,000 and higher than the October gain of 150,000. Unemployment dropped from 3.9% to 3.7% and average hourly earnings rose to 0.4% m/m, up from 0.2% in October and above the market consensus of 0.3%. The strong data points to a resilient labour market despite signs that the economy is cooling down, and has reduced fears of recession.

The markets are still expecting four or five rate cuts in 2024, pointing to a deep disconnect with the Fed, which is insisting that hikes remain on the table. The strong nonfarm payroll report is a reminder to the markets that the US labour market remains strong, even if there are clear signs that the economy is cooling down. Tuesday’s inflation report will be closely watched, as a stronger-than-expected reading would likely force the markets to temper expectations about rate hikes in 2024.

GBP/USD Technical

- GBP/USD is putting pressure on resistance at 1.2592, followed by 1.2682

- 1.2484 and 1.2369 are the next support levels