Sample Category Title

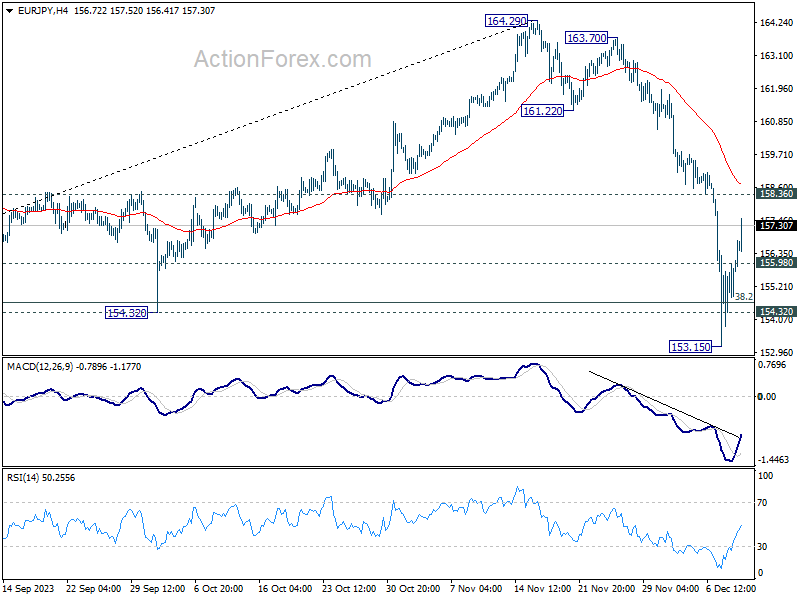

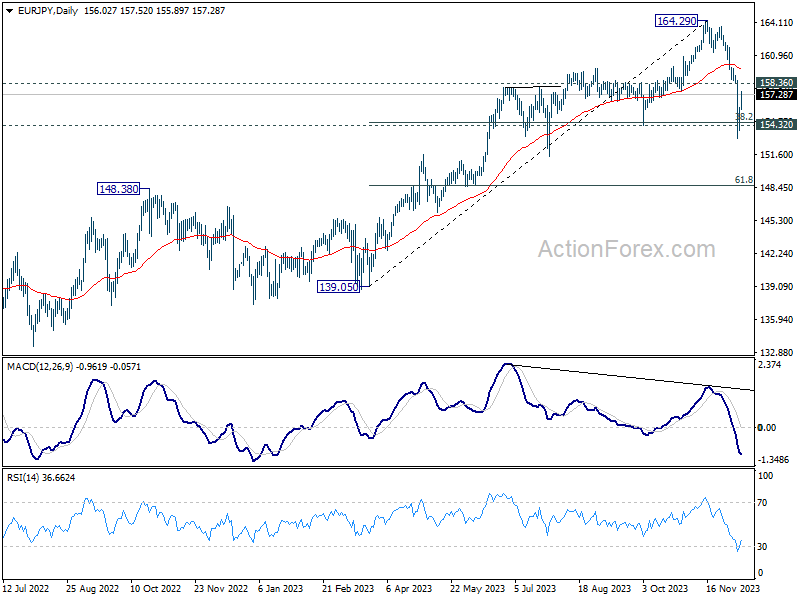

EUR/JPY Daily Outlook

Daily Pivots: (S1) 154.54; (P) 155.32; (R1) 156.76; More..

EUR/JPY's recovery from 153.15 extends higher today but outlook is unchanged. Upside should be limited below 158.36 minor resistance to bring another fall. On the downside, below 155.98 will turn bias to the downside for retesting 153.15. Break of 153.15 and sustained trading below 38.2% retracement of 139.05 to 164.29 at 154.64 will target 61.8% retracement at 148.69 next.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

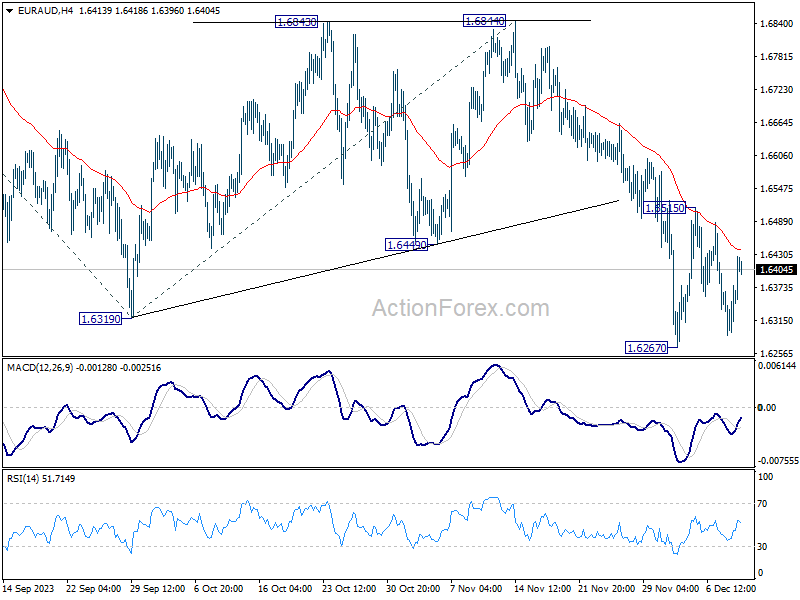

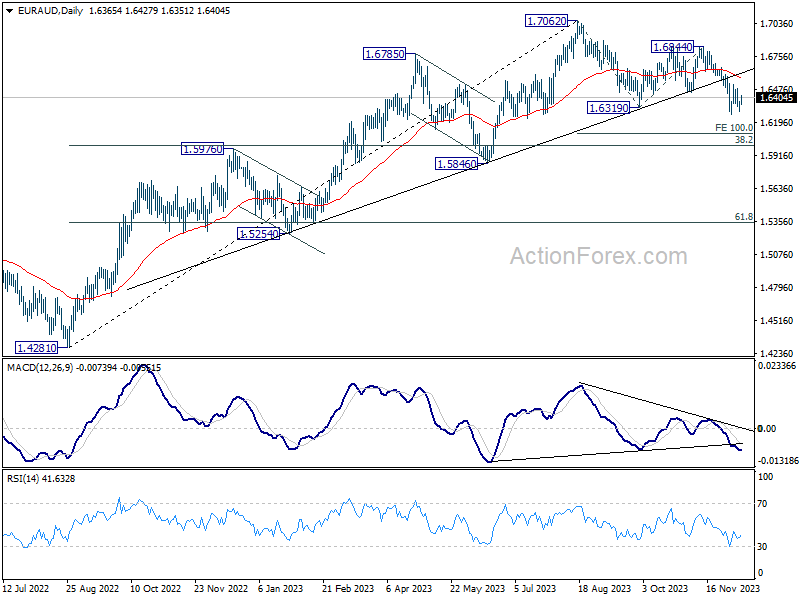

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6305; (P) 1.6342; (R1) 1.6392; More...

Intraday bias in EUR/AUD remains neutral for the moment, as consolidation from 1.6267 is extending. Outlook will stay bearish as long as 1.6515 resistance holds. On the downside, break of 1.6267 will resume the whole decline from 1.7062 to 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106 next. However, break of 1.6515 resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.7062 medium term top is seen as correcting the whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound on first attempt. But risk will stay on the downside as long as 1.6844 resistance holds. Sustained break of 1.6000 would bring further fall to 61.8% retracement at 1.5343.

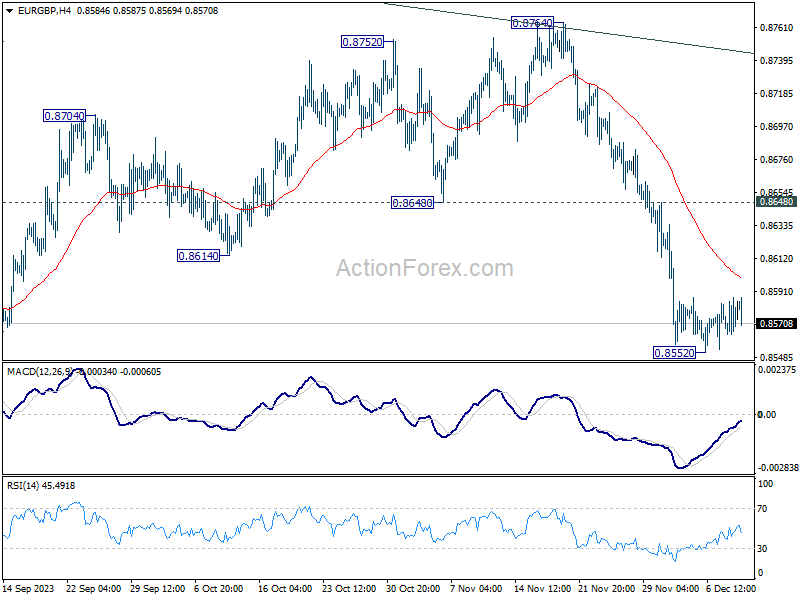

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8564; (P) 0.8577; (R1) 0.8589; More....

Intraday bias in EUR/GBP remains neutral as consolidation from 0.8552 is extending. IN case of another recovery, upside should be limited below 0.8648 support turned resistance to bring another decline. Below 0.8552 will target 0.8491 low first. Firm break there will resume larger down trend.

In the bigger picture, current development suggests that down trend from 0.9267 (2022 high) is still in progress. This decline is seen as the third leg of the pattern from 0.9499 (2020 high). Break of 0.8201 will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969. In any case, outlook will stay bearish as long as 0.8764 resistance holds.

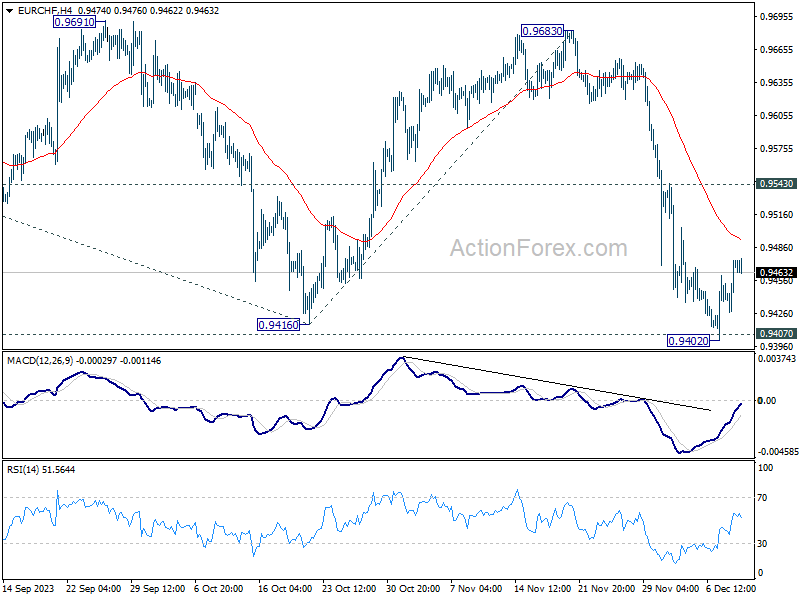

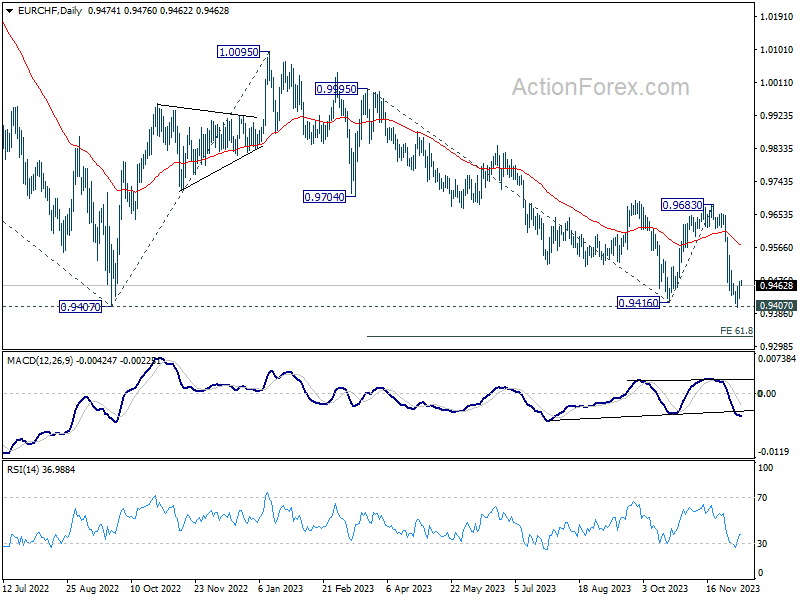

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9443; (P) 0.9459; (R1) 0.9490; More...

Intraday bias in EUR/CHF remains neutral for the moment and some consolidations would be seen above 0.9402 first. Further fall is expected as long as 0.9543 resistance holds. On the downside, decisive break of 0.9407 will confirm larger down trend resumption.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Firm break of 0.9407 (2022 low) will resume long term down trend. Next target will be 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

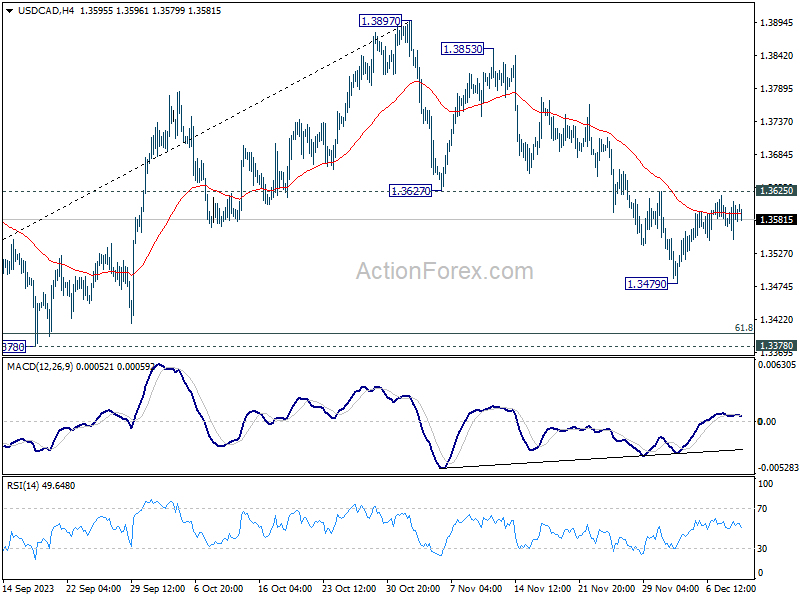

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3552; (P) 1.3581; (R1) 1.3611; More...

Intraday bias in USD/CAD remains neutral for the moment. On the downside, below 1.3479 will resume the corrective fall from 1.3897. But downside should be contained by 1.3378 support, which is close to 61.8% retracement of 1.3091 to 1.3897 at 1.3399, to bring rebound. On the upside, break of 1.3625 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rise.

In the bigger picture, rise from 1.3091 is seen as the fifth leg of the whole rise from 1.2005 (2021 low). Further rally is expected as long as 1.3378 support holds, to 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. However, decisive break of 1.3378 will dampen this view and bring deeper fall back to 1.3091 instead.

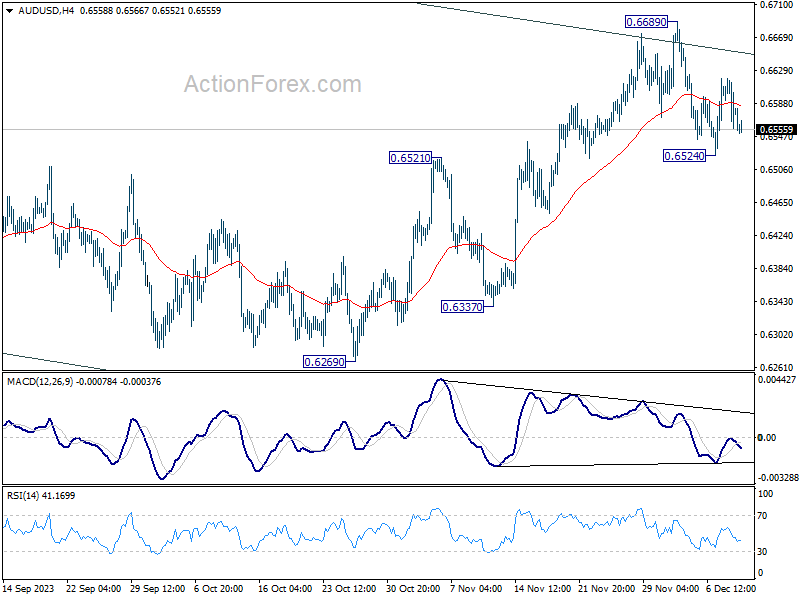

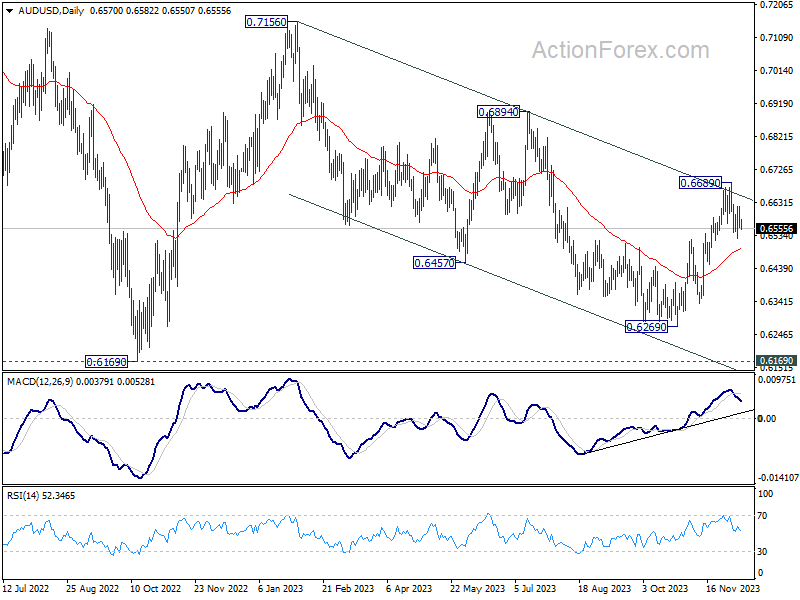

AUD/USD Daily Report

Daily Pivots: (S1) 0.6551; (P) 0.6585; (R1) 0.6613; More...

Intraday bias in AUD/USD remains neutral for the moment. Risk will stay on the downside as long as 0.6689 resistance holds. Break of 0.6524 will resume the fall from 0.6689 short term top to 55 D EMA (now at 0.6496). Nevertheless, firm break of 0.6689 will resume the rise from 0.6269 instead.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern, with fall from 0.7156 as the second leg. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

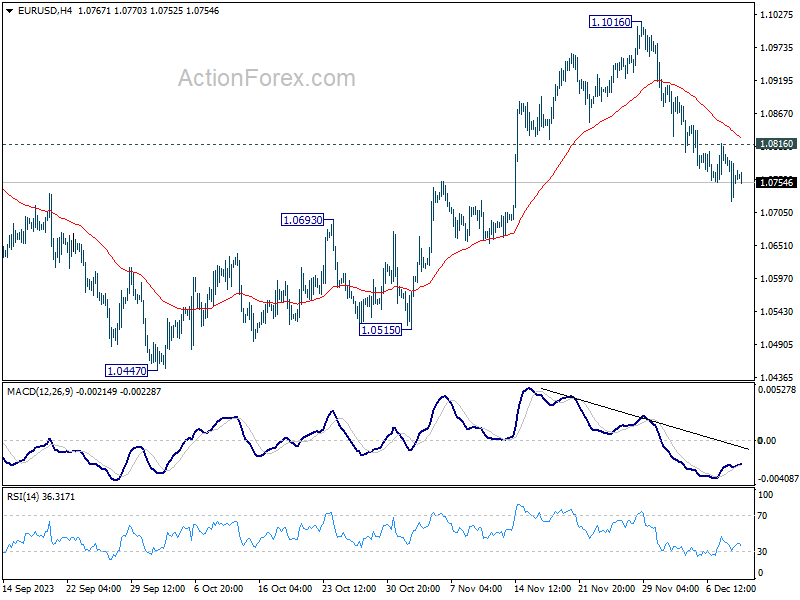

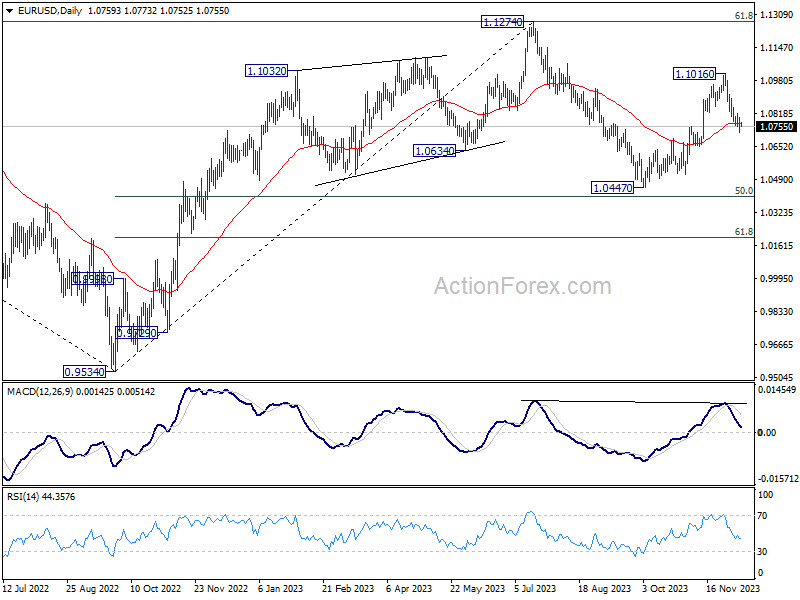

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0722; (P) 1.0762; (R1) 1.0799; More...

Intraday bias in EUR/USD remains mildly on the downside for the moment. Sustained trading below 55 D EMA (now at 1.0770) will extend the fall from 1.1016 short term top to retest 1.0447 support. On the upside, above 1.0816 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

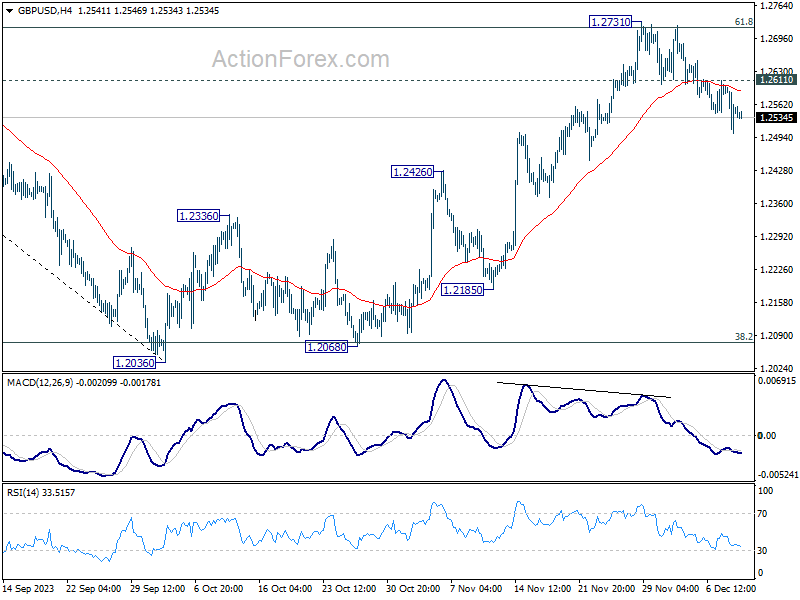

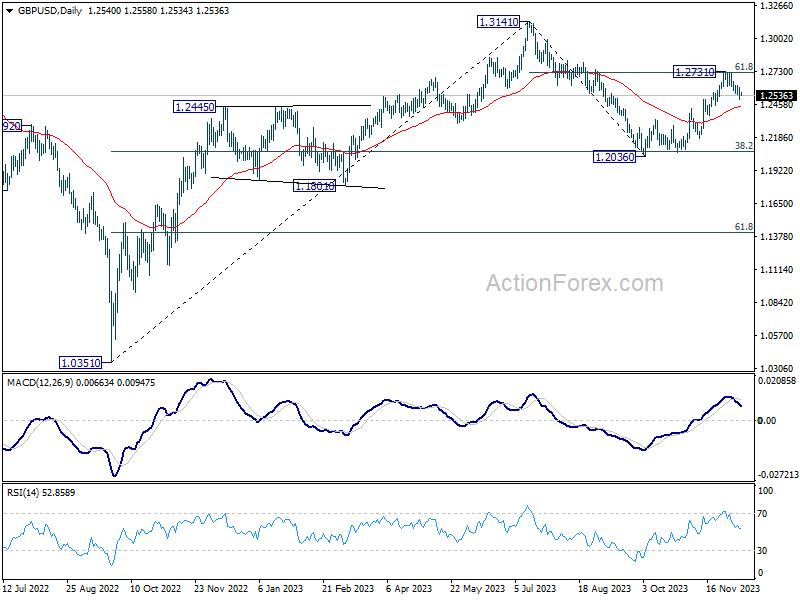

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2500; (P) 1.2551; (R1) 1.2600; More...

Intraday bias in GBP/USD remains mildly on the downside at this point. Fall from 1.2731 short term top is in progress for 55 D EMA (now at 1.2445). Sustained break there will bring retest of 1.2036 low. On the upside, above 1.2611 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, that could still extend through 1.2731. But upside should be limited by 1.3141 o bring the third leg of the pattern. Meanwhile, sustained trading below 55 EMA will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again, and possibly below.

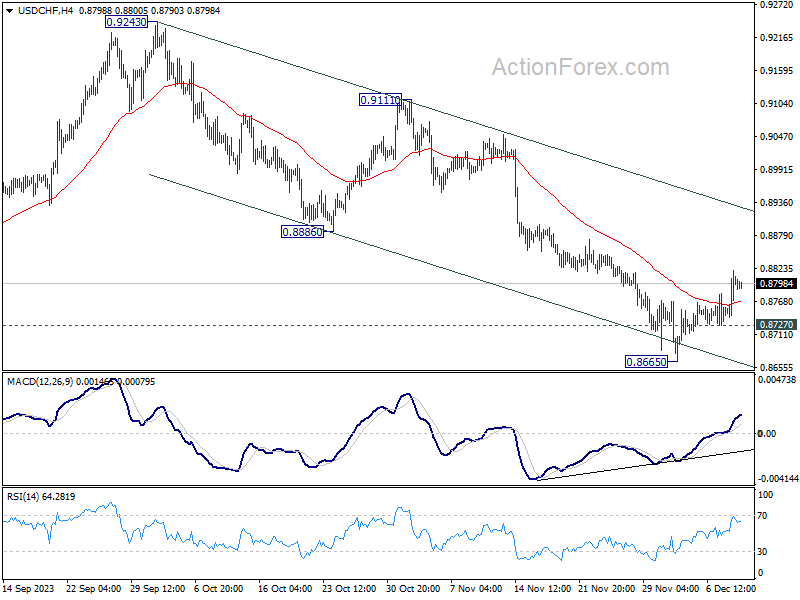

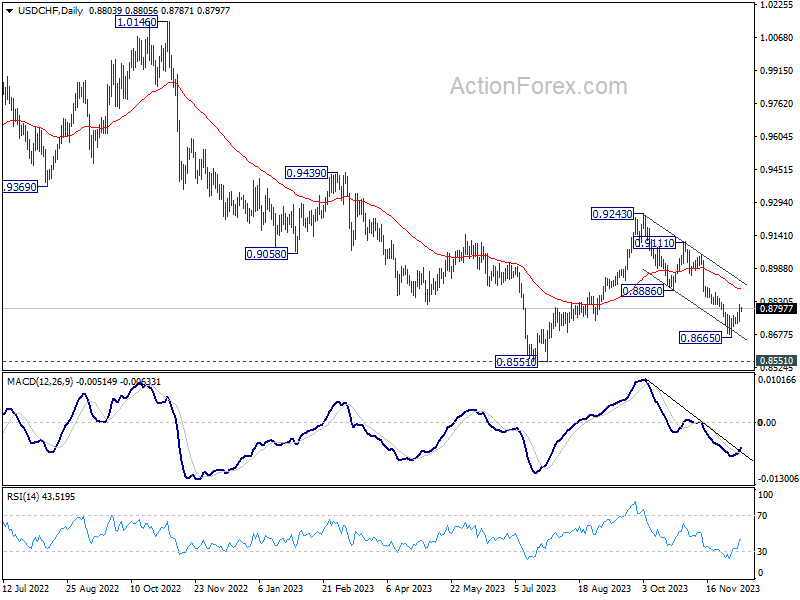

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8754; (P) 0.8788; (R1) 0.8834; More....

Intraday bias in USD/CHF stays on the upside at this point. rebound from 0.8665 short term bottom is in progress for 0.8886 support turned resistance first. Decisive break there will indicate that whole fall from 0.9243 has completed, and bring stronger rally to 0.9111 resistance next. On the downside, below 0.8727 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243 and above.

Markets Look Forward to Tomorrow’s US November CPI

Markets

Data on Friday suggested that the US economy remains resilient. For now, there is no reason for the Fed to support demand. The labour market in November added 199k jobs, up from 150k in October (35k downward revision of the previous two months). Data from the consumer survey were very strong. The unemployment rate declined from 3.9% to 3.7%, as job growth outpaced a strong rise in the labour force. Average hourly earnings at 0.4% M/M and 4.0% y/y stayed solid. Later, consumer confidence of the U. of Michigan even painted a ‘perfect world scenario’. Sentiment jumped sharply from 61.3 to 69.4, both by a better assessment of consumers’ current situation and expectations. At the same time, consumers see inflation easing. Expectations for the next 12 months tumbled from 4.5% to 3.1%. Expectations for 5-10-y eased from 3.2% tot 2.8%. This should comfort the Fed. Still, the data overall was strong enough for markets not further frontload aggressive Fed easing next year. US yields rose between 12.6 bps (2-y) and 4.8 bps (30-y). Markets scaled back bets for a March Fed rate cut < 50% (from 70% before the release). The price pattern on US yield markets was copied in Europe with German yields rebounding between 9.7 bps (2-y) and 6.6 bps (30-y) yield. The hope on a soft landing kept equities well bid with the US indices testing the 2023 top levels (S&P 500 + 0.41%). The Eurostoxx 50 even closed at a post-corona top (+1.1%). The dollar jumped upon the payrolls’ release, but with no follow-through gains. DXY (close 104.01) failed to take out first resistance at 104.23/56. EUR/USD spiked near 1.0725, but managed to limit the damage (close 1.0763). The raise in US/core yields also blocked recent ascent of the yen. USD/JPY closed at 144.95 off an intraday low near 142.5 in Asia.

This morning, Asian equities mostly trade in green. Japan outperforms. Chinese markets are a bit in doubt as price data point to persistent deflation (cfr infra). Today, the eco calendar is empty. Markets look forward to tomorrow’s US November CPI inflation ahead of several central bank decisions, including the Fed (Wednesday), the ECB and the BoE (Thursday). In case of a soft US CPI, we look out if recent lows in yields hold. With respect to the Fed and ECB meetings dots/projections are key. We assume markets will see more than 50 bps expected Fed cuts by end 2024 as ‘confirming’ recent positioning. Question also is how much the ECB will lower its expected path for 2024 and 2025 inflation. A softening of both the Fed and ECB stance might bring the EUR/USD cross rate more in balance. In this scenario, the EUR/USD 1.065 area gradually might provide some support.

News & Views

Chinese deflation intensified in November with CPI dropping from -0.2% to -0.5% y/y, the lowest in exactly three years. The unexpected worsening came amid slumping pork prices, which carry a big weight in the index. Other categories dragging the figure lower were transport and communication. Core inflation (ex-food and energy), remained positive, though barely, at 0.6%. 0.4% services inflation underscores ongoing weak (domestic) demand as well as the need to support it both fiscally and monetary. Factory inflation (PPI) ventured deeper in deflation territory with a further decline from -2.6% to -3%. The index has been under water since October 2022. The numbers continue to cast a shadow over the Chinese economy, triggering local equity underperformance. The CSI 300 opened 1.5% lower but pared losses to 0.5% in dealings afterwards. USD/CNY trades stronger at 7.185 vs a 7.17 on Friday.

Rating agency Fitch downgraded Slovakia’s credit rating from A to A- with a stable outlook. Key reason for the decision are deteriorating public finances. Fitch estimates debt by 2025 to rise to 62.1%, exceeding the pandemic high of 61.1% of GDP in 2021 and to remain on an upward path (65.5% by 2027). The fiscal deficit is expected to widen to 6% this year from 2% in 2022. Fitch estimates fiscal deficits of 6% in 2024 and 6.5% in 2025. This compares to peer medians of 2.6% and 2% respectively. Adding to the decision are Slovakia’s weakening governance as well as structural challenges, including a heavy reliance on the automotive industry and decreasing labour productivity. The still solid A- rating stems from Slovakia’s eurozone membership that “underpins a relatively stable and credible macro-economic framework and steady EU capital inflows, as well as a competitive export sector and stable foreign direct investment.” Growth is seen picking up from 1.3% in 2023 to 2.3% and 2.8% in 2024 and 2025. Inflation over that time span is seen declining from an average of 11.1% to 5% and 3.1%. Slovakia’s external accounts improved faster than expected, allowing for a rapid narrowing of the CA deficit to just 0.5% in 2023-2025 vs 8.1% in 2022.