Sample Category Title

Fed’s Mester suggests another rate hike needed

Cleveland Fed President Loretta Mester acknowledged in a speech yesterday the robust state of the economy with a cautious stance on inflation and interest rates. She signaled the possibility of another rate hike this year.

"I suspect we may well need to raise the fed funds rate once more this year and then hold it there for some time," she said.

However, Mester also underscored the contingent nature of future monetary policy decisions, stating, "whether the fed funds rate needs to go higher than its current level and for how long policy needs to remain restrictive will depend on how the economy evolves relative to the outlook."

Inflation, according to Mester, continues to pose a significant challenge. She plainly remarked that inflation remains "too high". Though she expects some easing of price pressures, she cautioned that "the risks to the inflation forecast remain tilted to the upside."

On a positive note, Mester expressed optimism about the broader economic picture. "The economy is on a good path," she observed. Delving into labor market dynamics, she pointed out that while conditions remain robust, the disparity between labor demand and supply is shrinking, indicating that "firms are finding it easier to find the workers they need."

Fed’s Barr eyes restrictive policy duration over rate height

Fed Vice Chair Michael Barr advocated for a cautious approach to monetary policy adjustments during his speech yesterday. While discussions surrounding interest rate hikes are paramount, Barr's concern is primarily anchored on the duration for which these elevated rates should be maintained.

Speaking on the current tightening cycle, Barr highlighted the progress made and expressed that it's a juncture where meticulous decision-making is essential. He stated, "Given how far we have come, we are now at a point where we can proceed carefully as we determine the extent of monetary policy restriction that is needed."

Perhaps most notably, he reframed the ongoing debate on rate adjustments by remarking, "The most important question at this point is not whether an additional rate increase is needed this year or not, but rather how long we will need to hold rates at a sufficiently restrictive level." This perspective places a clear emphasis on policy duration, suggesting a prolonged period of elevated rates may be more impactful than further substantial hikes in the near term.

On the economy, Barr's baseline is for real GDP growth to "moderate to somewhat below its potential rate over the next year" as restrictive monetary policy and tighter financial conditions restrain economic activity." He anticipates this deceleration in growth to be concomitant with "some further softening in the labor market".

EURUSD Found Sellers At The Equal Legs Area

Hello fellow traders. In this technical blog we’re going to take a quick look at the Elliott Wave charts of EURUSD, published in members area of the website. As our members know the pair is showing incomplete bearish sequences in the cycle from the July 18th peak targeting 1.0435-1.0318 area. Consequently, we recommended members to avoid buying at this stage and calling for the further decline. Recently EURUSD made a pull back that has found sellers right at the equal legs area.

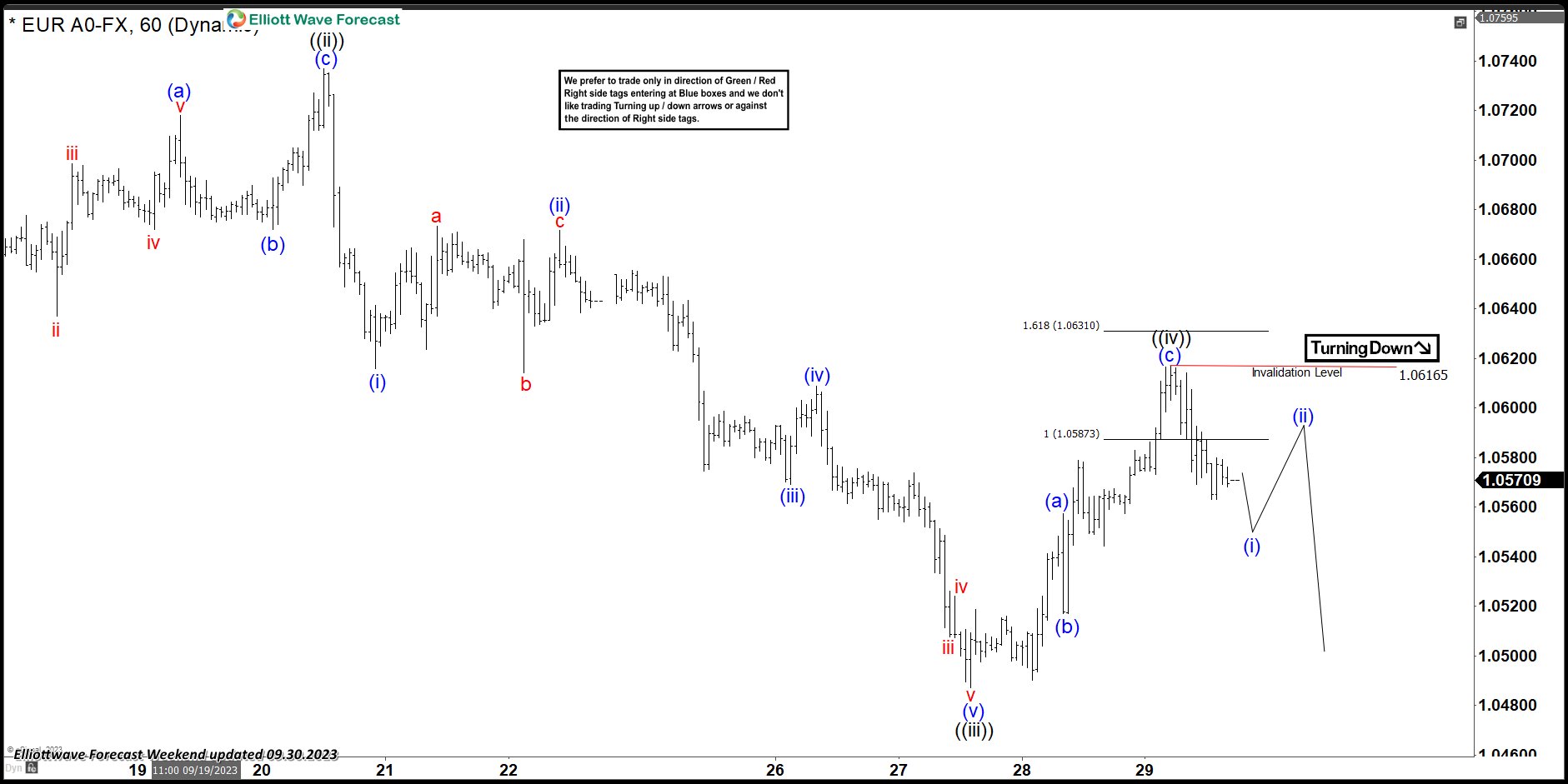

EURUSD H1 Weekend Update 09.30.2023

EURUSD has given us 3 waves bounce in wave ((iv)) recovery. The pair has made clear 3 waves up and reached equal legs area at 1.05873-1.06310. Sellers appeared as expected and we can already see reaction from the equal legs area. Correction is counted completed at 1.06165 peak as Elliott Wave Zig Zag Pattern.

EURUSD H1 Weekend Update 10.02.2023

The price kept 1.06165 peak intact and we got further separation lower. As far as the price stays below 1.06174 high, we expect the pair to keep trading lower in wave ((v)) , targeting 1.0458-1.0409 area. We would like to see break of 09/28 low to confirm extension down toward mentioned zone.

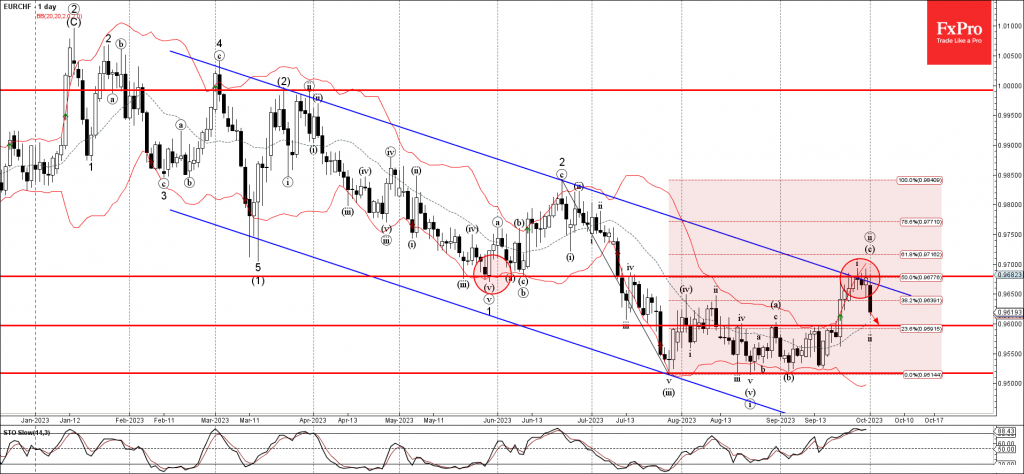

EURCHF Wave Analysis

- EURCHF reversed from resistance level 0.9680

- Likely to fall to support level 0.9600

EURCHF currency pair recently reversed down from the key resistance level 0.9680 (former strong support from May) intersecting with the upper daily Bollinger Band and the 50% Fibonacci correction of the downward impulse from June.

The resistance level 0.9680 was strengthened by the resistance trendline of the daily down channel from February.

Given the clear daily downtrend, EURCHF can be expected to fall further toward the next support level 0.9600 (former resistance from August).

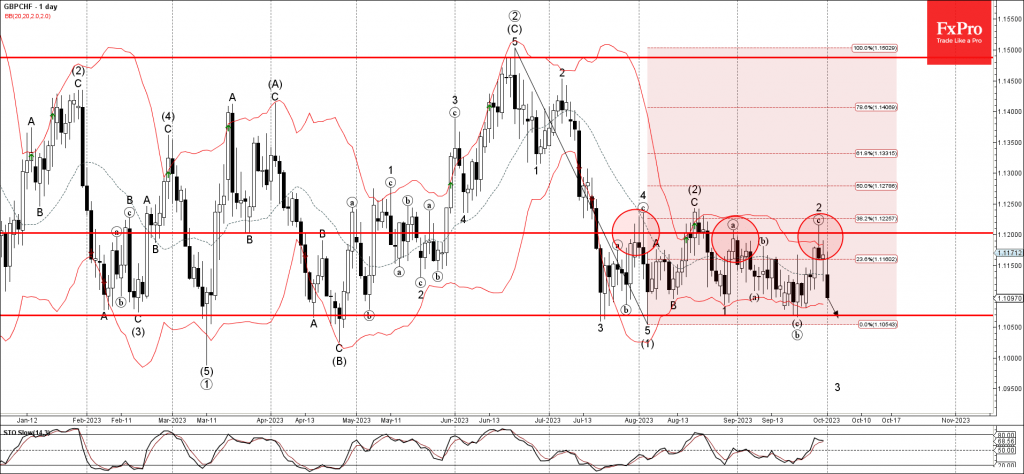

GBPCHF Wave Analysis

- GBPCHF reversed from resistance level 1.1200

- Likely to fall to support level 1.1070

GBPCHF currency pair earlier reversed down from the key resistance level 1.1200 (which has been reversing the pair from July) intersecting with the upper weekly Bollinger Band and the 38.2% Fibonacci correction of the downward impulse (1) from June.

The downward reversal from the resistance level 1.1200 started the active short-term impulse wave 3.

Given the strength of the Swiss franc inflows, GBPCHF can be expected to fall further toward the next support level 1.1070 (which has been reversing the pair from April).

Brent Crude – Volatile Start for Oil Ahead of OPEC+ Meeting

- PMIs continue to point to a weakness in demand

- OPEC+ holds the key to crude oil prices

- Lost momentum ahead of recent decline

It’s been a volatile start to the week for oil, with prices initially rising before falling negative to trade almost 2% lower on the day.

We’ve had a vast selection of PMIs to bear in mind today, as well as speculation around the OPEC+ decision on Wednesday and, of course, the US averted a government shutdown.

I’m not sure all of this is a net negative for oil, per se, but it was trading at very high levels prior to this and had already started to lose momentum so perhaps what we’re seeing is a case of profit-taking. Especially given the proximity to the OPEC+ meeting on Wednesday.

BCOUSD Daily

The recent decline in BCOUSD came following a rally and new high that failed to be backed up by stronger momentum and now it appears to have potentially moved into a corrective phase.

A divergence often isn’t followed by such a sudden corrective move and this may also quickly reverse higher again but the moves over the last few days are not small.

The price is now testing last week’s lows and a break below may point to further declines, with support in the $88-$90 region potentially key.

Ultimately, though, the OPEC+ decision on Wednesday may dictate the direction of travel.

DAX – PMIs Paint a Bleak Picture for Manufacturing But China Offers Hope

- Manufacturing remains in trouble

- China seeing some growth but unconvincing

- Bearish confirmation for DE30 index

Manufacturing PMIs released throughout the day have made for pretty miserable reading and even those in China barely registered any growth after a lengthy period of contraction.

The Chinese data did offer some cause for hope at least, despite ultimately barely sitting in growth territory. The trajectory is positive and boosted by targeted stimulus measures that are seemingly working. External demand remains a problem but a bump in domestic demand is promising.

The sector in Europe is looking particularly grim with demand remaining extremely weak, backlogs falling and layoffs expected to accelerate over the months ahead. That’s unless we can see a rebound in activity which is looking very unlikely at this stage with the global economy struggling for any positive momentum against the backdrop of high interest rates.

The PMIs from the US were a little better, particularly the ISM reading which significantly beat expectations but even here, it remains below 50 and therefore in contraction territory. With interest rates set to remain “higher for longer”, things aren’t likely to dramatically improve for the sector.

A very bearish signal for the DAX

The DE30 turned lower again today after staging a mild recovery in recent sessions and the move could reinforce bearish views on the index.

Source – OANDA on Trading View

The reason is that the move lower came after a retest of the 200/233-day simple moving average band, following the breakout last week. The rotation lower now could be viewed as confirmation of the breakout and therefore a bearish signal.

The next potential area of support could be seen around 15,000 where prior support and resistance falls around the bottom of the descending channel.

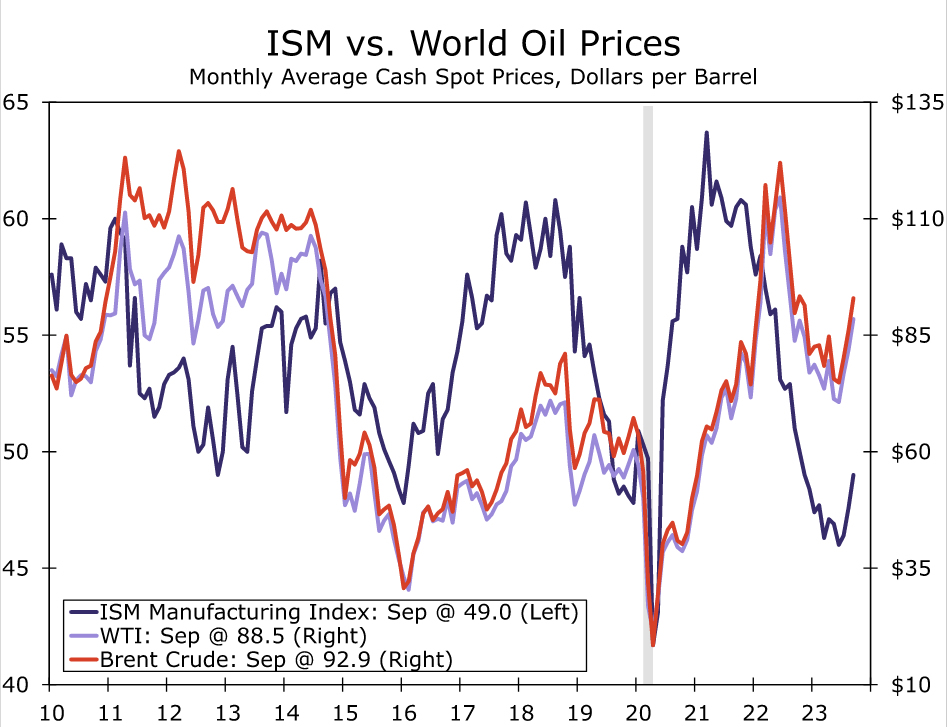

Manufacturing Reprieve: 11-Month High Still Pretty Low for ISM

Summary

Manufacturing activity contracted at the slowest pace in nearly a year according to the September ISM. Recent data signal some relief in the sector, while higher oil prices point to potential upside risk ahead.

Some Reprieve in Manufacturing

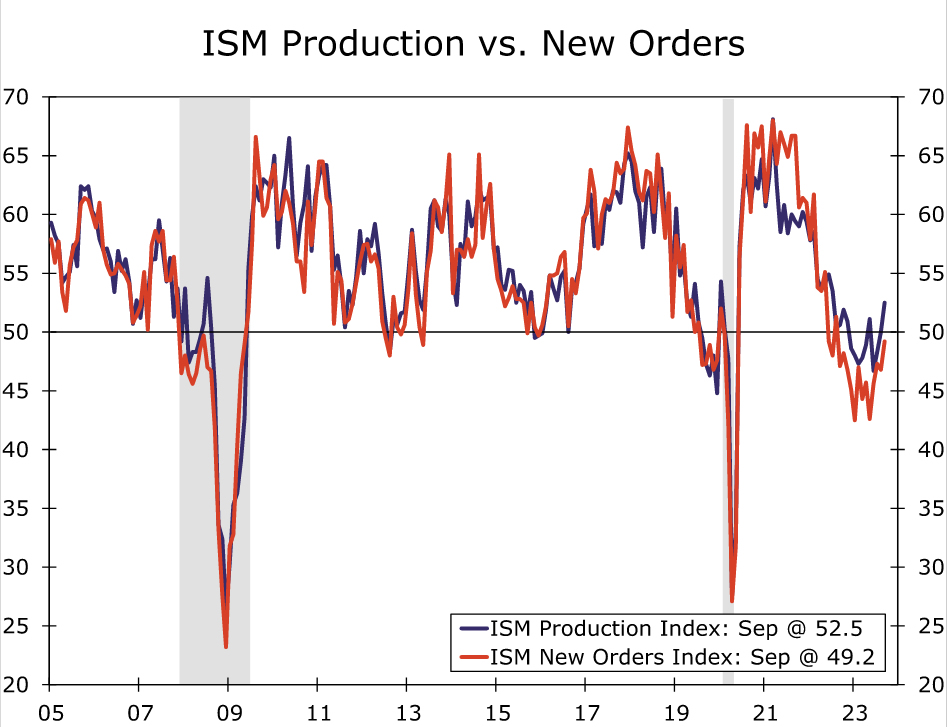

The recent read on the manufacturing sector is that activity is seeing somewhat of a reprieve though it remains weak. This is the message from today's ISM. The overall manufacturing index rose for the third straight month, but at 49.0 in September still signals activity is contracting—even if it's at a slower pace (chart). That said, even though 50 marks the traditional threshold for economic expansion, for manufacturing any reading above 48.7 is typically associated with expansion.

Most of the underlying measures moved in the right direction. Production and new orders pushed higher, with current production in expansion territory (52.5) for the second consecutive month (chart). New orders remained in contraction, but at 49.2 the index reached the highest in just over a year. Manufacturers also expanded head count last month. The employment index rose to 51.2 in September after contracting for three months. While labor prospects look to have improved last month, the release noted continued slowdown. Specifically the release referenced, "In September, attrition remained the primary source of head-count reductions, but hiring freezes were more prevalent". When the full Employment Situation report is released on Friday, we expect to see a continued slowdown in hiring. Order backlog slipped further into contraction and prices paid fell by the most of any component, dropping 4.6 points to 43.8.

The Undeniable Impact of Oil Prices

Last month we highlighted the gap between the Manufacturing and the Services ISM. One of the main factors that can contribute to a divergence between these measures is the price of a barrel of oil (chart). There was a period in the midst of the prior expansion that highlighted this relationship. Between 2014 and 2016, oil prices went through a slow-motion collapse going from north of $100/barrel in the summer of 2014 to a low of about $26/barrel in February 2016. In the same period, the ISM manufacturing index went from readings of north of 55 in the summer of 2014 to a mid-cycle low of 47.6 in January 2016.

High oil prices may present headwinds for some parts of the economy and not every manufacturer celebrates higher prices for crude, but on balance high oil prices are associated with brisk activity in manufacturing. Of the larger industries covered in the ISM, only two were in expansion in September: food, beverage & tobacco products and petroleum & coal products. Yet, higher oil prices tend to bring increased investment and activity to places beyond the petroleum industry. Activity in the energy business requires pipes, machinery and metal products, and when we look at the industries that reported order growth in September, the fingerprints of these industries were all over place: miscellaneous manufacturing, primary metals, fabricated metal products and nonmetallic mineral products all reported a growing order book in September

Fed’s Bowman flags energy as potential setback to disinflation progress; advocates more hike

Fed Michelle Bowman has made her hawkish stance clear on the pressing issue of inflation that continues to grip the US economy. In a speech today, Bowman emphasized the persistence of inflationary pressures, signaling the need for a more restrictive monetary policy to anchor inflation back to the Fed's 2% target.

"Inflation continues to be too high, and I expect it will likely be appropriate for the Committee to raise rates further and hold them at a restrictive level for some time to return inflation to our 2 percent goal in a timely way," Bowman stated.

Bowman pointed to the latest inflation reading based on the PCE index, noting a rise in overall inflation driven, in part, by escalating oil prices. "I see a continued risk that high energy prices could reverse some of the progress we have seen on inflation in recent months," she warned.

Also, Bowman cited the Summary of Economic Projections released during the September FOMC meeting, where "the median participant expects inflation to stay above 2 percent at least until the end of 2025." This expectation of prolonged inflationary pressures aligns with Bowman's perspective that "further policy tightening" will be instrumental in steering inflation back towards target.