Sample Category Title

ECB’s Lane: There is still work to be done

ECB's Chief Economist Philip Lane voiced his ongoing concerns regarding the elevated inflation levels in the Eurozone during a conference. Despite a drop in inflation in September to its lowest in two years, Lane emphasized the need for continued efforts to steer price increases back towards the 2% target.

Lane stated, "Price increases are still well above 2%, we are not at the inflation target yet and therefore there is still work to be done in terms of bringing inflation down."

While wage inflation is anticipated to decline, Lane cautioned that this process would be gradual, as "it's going to take months, it will take time". Lane's focus appears to be more on services inflation data. "I think we will be looking at services inflation data for quite a while," he shared

One key area of focus for the ECB is the unpredictable nature of energy prices. "We don't expect the current low gas price to be maintained, we do expect to see gas prices go up from where they are now," he said. "Energy has been such a volatile component, it's going to be very important to us to keep an eye on energy in the coming months and years."

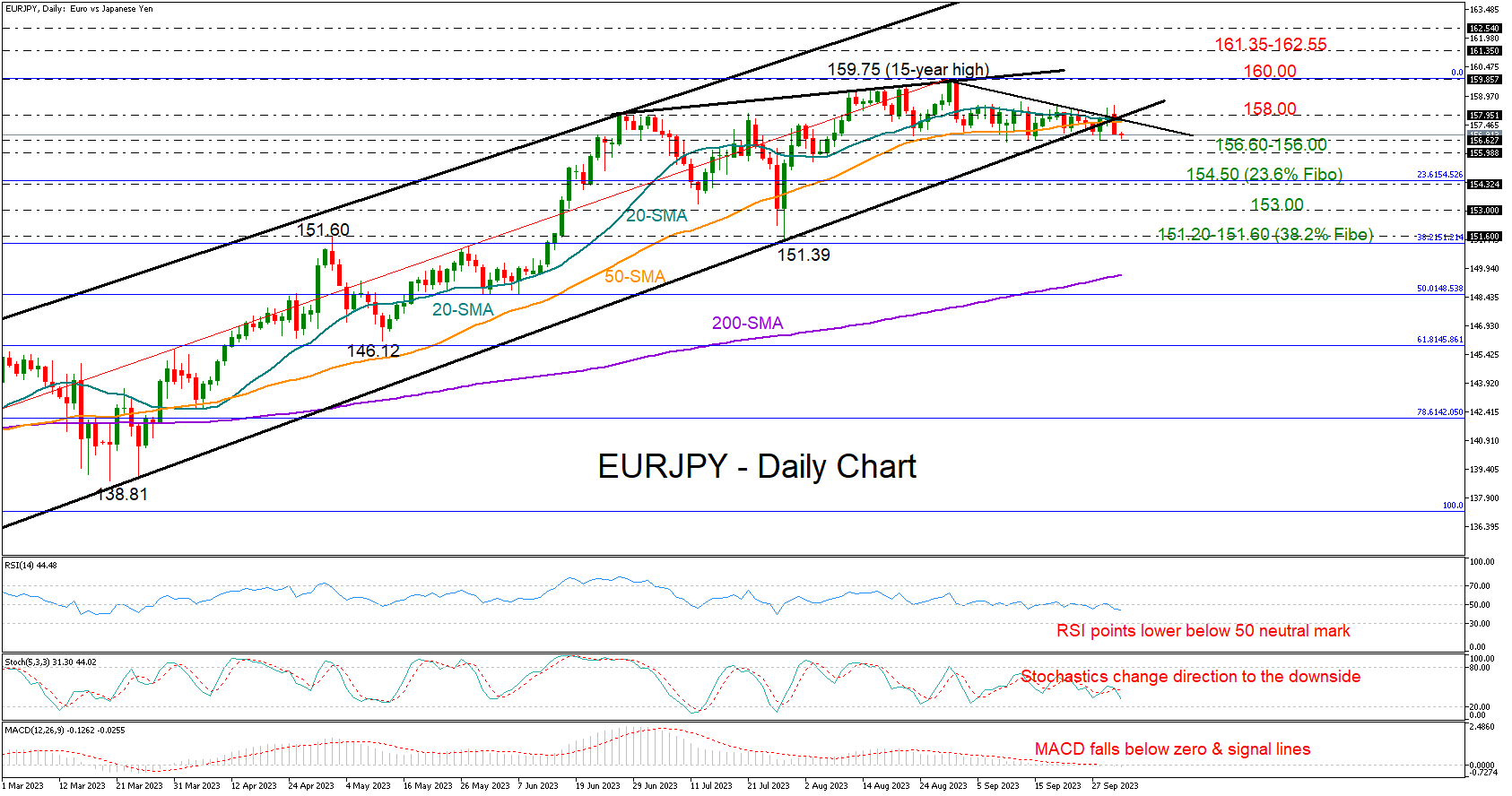

EURJPY Sends Bearish Warning

- EURJPY leans to the downside after a defeat

- Technical signals flag more weakness ahead

- Potential support expected at 156.00

EURJPY could not enter the 158.00 territory as the falling 20- and 50-day simple moving averages (SMA) managed to cool upside forces once again. The broken support trendline from March and the short-term resistance line from recent highs cemented that ceiling, increasing the risk for a new bearish wave.

The technical indicators are in line with the bearish expectation. Both the RSI and the MACD are clearly sloping downwards in the negative region. Likewise, the stochastic oscillator is facing a new downturn, all flagging a discouraging session ahead.

If the pair exits the ongoing sideways trajectory below the nearby 156.60 support region, the 156.00 round level might instantly provide some footing. Traders might also pay attention to the 23.6% Fibonacci retracement of the 2023 uptrend at 154.50 before testing the base at 153.00. Failure to pivot there could generate a more aggressive decline towards the 151.20-151.60 area, where the 38.2% Fibonacci mark is placed.

In the bullish scenario, where the price surges above the 158.00 bar, a new battle could take place between the 15-year high of 159.75 and the 160.00 psychological mark. A successful step higher could immediately stall within the 161.35-162.50 constraining zone last seen in August 2008. If the bulls snap the latter too, the uptrend could stretch towards the 165.00 mark, which was also an important barrier during 2008. Then, the door would open for the the upper band of the broad rising channel at 166.20.

Overall, EURJPY has been handling a choppy uptrend so far this year, with the bears expected to take a lead in the short-term. A break below 156.00 could raise selling orders in the market.

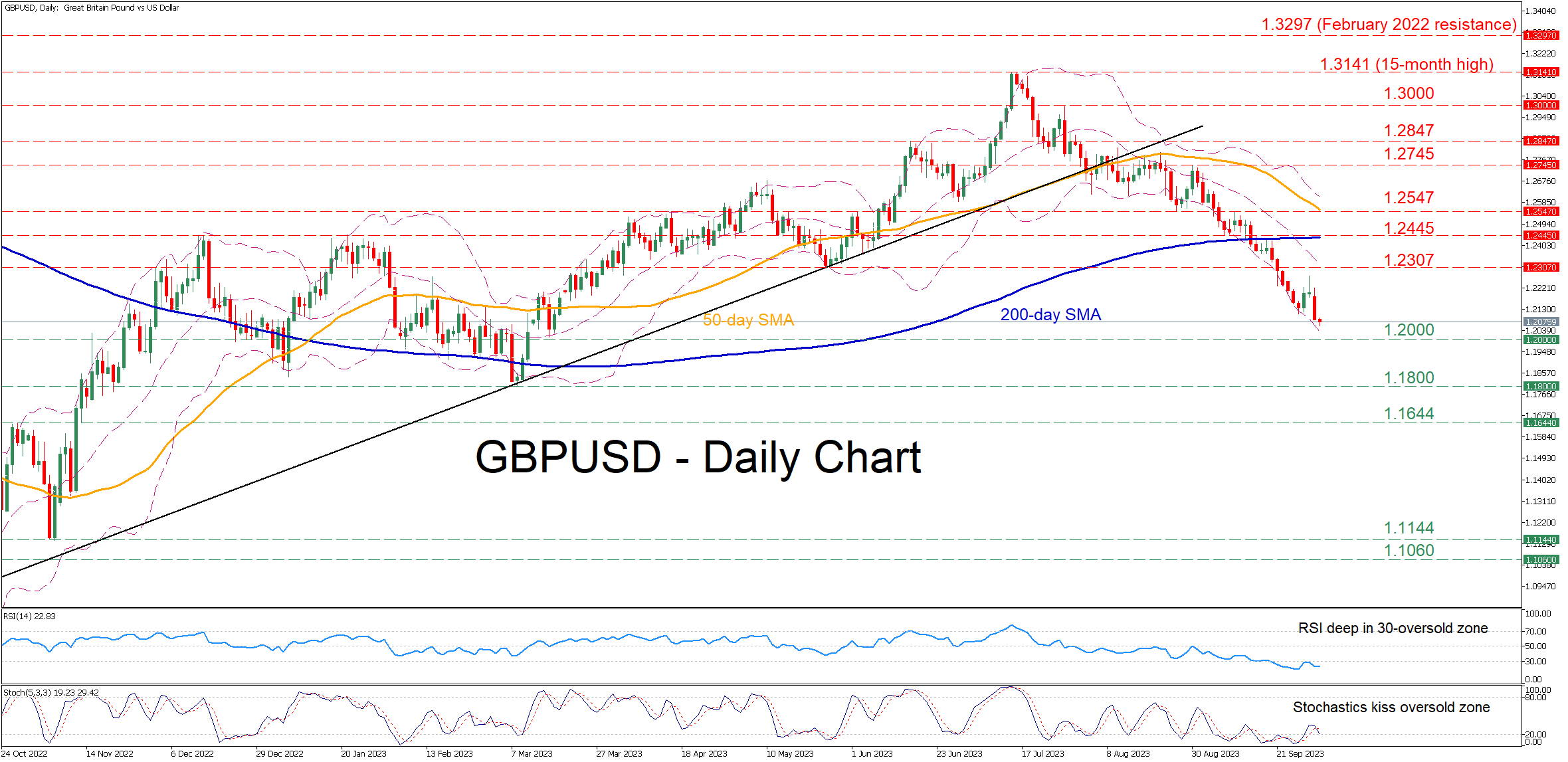

GBPUSD Tumbles to Fresh 6-month Low, Looks Oversold

- GBPUSD stuck in a steep decline since mid-July, appearing unable to recover

- Records consecutive multi-month lows as the bulls remain on the sidelines

- Given that momentum indicators are pointing at oversold conditions, can the price bounce back?

GBPUSD has been forming a structure of lower highs and lower lows since its 15-month peak of 1.3141. Meanwhile, in the near term, the RSI has entered its 30-oversold mark and the stochastic oscillator is touching its 20-oversold territory, both suggesting that the recent drop might be overstretched.

Should the downtrend resume, the price may initially face the 1.2000 psychological mark. A violation of that floor could pave the way for the March bottom of 1.1800. Failing to halt there, the pair could then descend towards the October 2022 resistance of 1,1644, which could serve as support in the future.

Alternatively, if the bulls re-emerge and push the price higher, the May low of 1.2307 could prove to be the first obstacle for the price to overcome. Breaking above that zone, the pair could test the December-January resistance zone of 1.2445. Further advances might then cease at the April resistance of 1.2547, which also acted as support in August.

In brief, GBPUSD seems to be in a relentless decline, but its end could be approaching as the pair has reached oversold conditions. Hence, traders should not rule out an impending bounce.

Australian Dollar Falls as RBA Leaves Interest Rates on Hold for a Fourth Month

The Australian dollar softened this morning after the RBA opted to leave the Cash Rate at 4.1% but warned some further tightening may be required.

The decision and statement - the first under new Governor Michele Bullock - was largely in line with what we've heard before and was a long way from suggesting another rate hike is imminent.

The language around further hikes potentially being needed is being used by all central banks that have just undergone a severe tightening process as they are hesitant to declare victory until it's absolutely clear without doubt. That's what happens when you're heavily criticized for a slow start.

In reality, the RBA like most other central banks is probably done. We are seeing a lot of hawkish commentary from policymakers at the moment though, perhaps one final hawkish push to get every last drop from their tightening efforts, which is clearly unsettling investors.

The data will obviously be crucial now as we're entering a period in which it's assumed substantial progress will be seen. That alongside the lag effects of past measures could see that language soften a little from some policymakers, although others like the Fed may hold the hawkish line for longer as the labour market remains remarkably resilient.

Oil extends pullback ahead of OPEC+ meeting

Oil prices are continuing to slide ahead of the OPEC+ meeting tomorrow. While the rally was already running on fumes prior to the pullback, it is interesting the scale of the move we've seen in recent days, with Brent off more than 5% since Thursday.

Perhaps there's an element of profit-taking ahead of the OPEC+ meeting after such a strong rally since mid-August or maybe risk-aversion elsewhere is weighing, driven by economic fears. The question now is whether trading in recent days or the recent shift in risk appetite will influence the outcome of the meeting.

Gold continues to crumble amid hawkish central bank warnings

Gold is on course to extend its losing run to seven sessions, with the yellow metal currently down around a quarter of one percent, having been down three times as much earlier in the day. Rising bond yields have hammered gold prices which have fallen from $1,900 to near $1,800 remarkably fast.

This will be the next test for the sell-off, with gold having rebounded strongly off this level back in February and March before rallying back toward record highs. I'm not sure traders will be that confident of a repeat performance but it will be an interesting test amid some very hawkish central bank commentary.

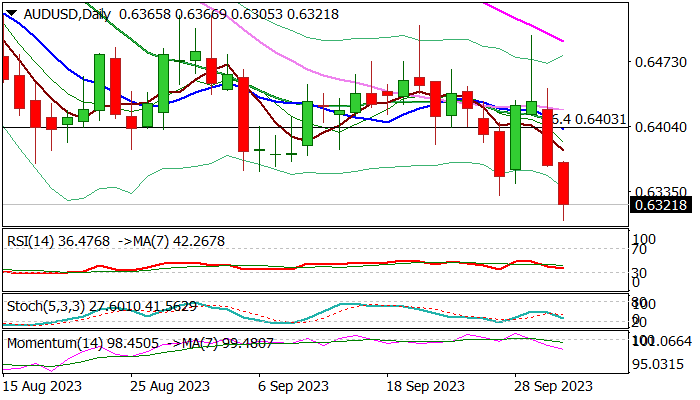

AUD/USD: Australian Dollar Hit 11-Month Low after RBA Kept Rates Unchanged

AUDUSD extends steep fall into second consecutive day and hit new lowest in eleven months in early Tuesday.

The pair was down 0.8% in Asian / early European trading on Tuesday, in extension of Monday’s 0.93% drop, signaling bearish continuation after limited correction.

Australian dollar is pressured by strong US dollar on expectations that the Fed will keep high interest rates for longer period, while policy decision of Reserve Bank of Australia was a key driver this morning.

The RBA kept its interest rates unchanged at 4.1% for the fourth month and said that recent rather positive economic data suggest that things are moving in desired way, though did not rule out further tightening, if needed.

Today’s decision also negatively influenced expectations for rate hike in November, dropping bets from initial 44% to 36%, which may further deflate Aussie dollar.

Daily studies remain firmly bearish, though fresh bears need close below last week’s low at 0.6331 to confirm signal and open way for extension towards targets at 0.6300/0.6272 (psychological / Nov 11 trough) which guards key support at 0.6170 (2022 low).

Limited corrections should be capped under broken Fibo 76.4% at 0.6403 (reinforced by 10DMA) to keep bears intact and provide better selling opportunities.

Res: 0.6357; 0.6378; 0.6403; 0.6444.

Sup: 0.6305; 0.6300; 0.6272; 0.6210.

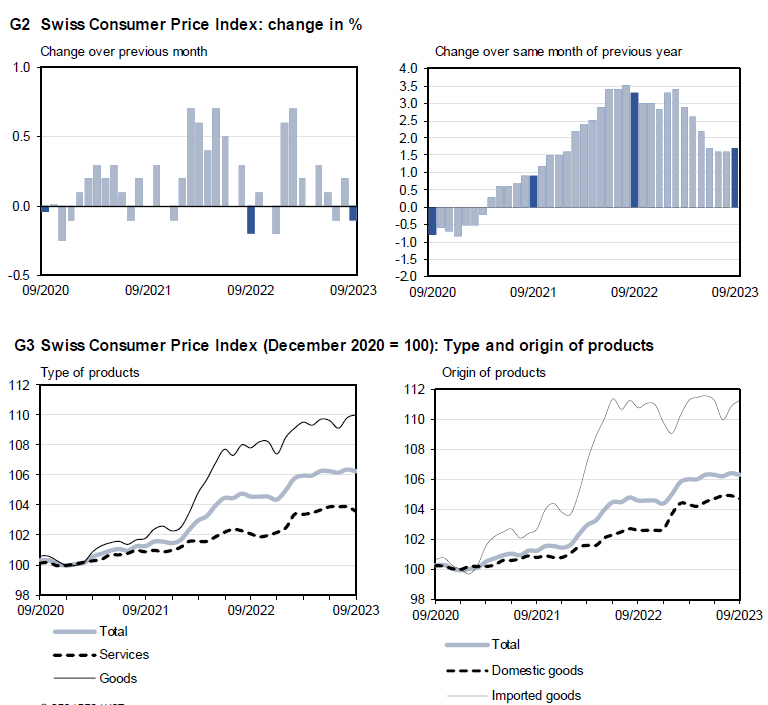

Swiss CPI ticks up to 1.7% yoy, core down to 1.3% yoy

Swiss CPI fell -0.1% mom in September, below expectation of 0.0% mom. Core CPI (excluding fresh and seasonal products, energy and fuel) was down -0.1% mom. Domestic products prices dropped -0.2% mom. Imported products prices rose 0.3% mom.

For the 12-month period, CPI rose from 1.6% yoy to 1.7% yoy, below expectation of 1.8% yoy. Core CPI slowed from 1.5% yoy to 1.3% yoy. Domestic products prices slowed from 2.2% yoy to 2.1% yoy. Imported products prices turned positive from -0.3% yoy to 2.2% yoy.

RBA Governor Bullock Left Rates Unchanged at Her First Meeting

Governor Bullock has made absolutely minimal changes in her first Statement despite evidence of higher inflation in the September quarter. She is likely to make her mark in November when the staff refreshes their forecasts for growth and inflation.

As expected, the Reserve Bank Board decided to leave the cash rate target unchanged at 4.1% at its October meeting.

While the decision was widely anticipated the issue for markets was whether new Governor Bullock would decide to send some different messages than had been signalled in previous Statements under Governor Lowe.

For instance, these messages may have indicated a greater concern around achieving the inflation target in the appropriate time frame; more concern about the underperforming Australia economy; the resilience of the labour market; or, the surprise recovery in house prices.

There were no such changes in the Statement.

The inflation issue was the most likely “candidate” for a revised approach.

However, as with the other key topics the Governor chose to almost exactly stick to the script that had been established by Governor Lowe.

The most contentious issue is around the implications of the August Inflation Indicator for the September quarter Consumer Price Index.

Westpac has lifted its forecast for Trimmed Mean Inflation from 0.8% to 1.1%, mainly due to higher inflation in the services sector for which the August report provides valuable information for the whole quarter.

The Governor’s Statement refers to “the prices of many services are continuing to rise briskly” although this is little changed from the September Statement “the prices of many services are rising briskly.”

As a result of our increase in our forecast for the Trimmed Mean in September we have lifted our forecast for annual Trimmed Mean inflation in 2023 from 3.8% to 4.1%.

Services plus higher fuel prices have lifted our September quarter forecast for headline inflation from 0.9% to 1.1% and annual inflation in 2023 from 3.9% to 4.3%.

The RBA is currently forecasting inflation by end 2023 at 3.9% (Trimmed Mean) and 4.1% (Headline).

Presumably the RBA forecasters would also be revising their own forecasts on the basis of the August Inflation Indicator but there is no such indication in the Statement.

In the Governor’s Statement the sentence “The central forecast is for CPI inflation to continue to decline and to be back within the 2–3% range in late 2025.

Despite our slightly higher profile for inflation in 2023 our forecasts are still in line with the RBA achieving their 2025 target.

The Governor chose not to react to those possible upgrades to the inflation forecasts – better to await the official September quarter CPI report which will be a key input into any forecast revisions.

Governor Bullock has opted to maintain the status quo prior to reviewing her position once the staff’s revised forecasts are available for the November meeting.

On the basis of our revised inflation forecast we expect the September Inflation Report will provide grounds for the staff inflation forecasts for the end of 2023 to be revised a little higher but not threaten the key goal of reaching the inflation target by 2025.

We do not see such revisions as providing sufficient evidence for a rate hike at the November meeting.

Japanese Yen Tries to Withstand Laws of Gravity

Markets

US Treasuries gapped open lower at the start of the trading week as US Congress narrowly avoided a government shutdown. From there on, Treasuries and other core bonds just resumed the sell-off which characterized most of the months of August and September with real yields still in the driver’s seat. The move accelerated after an upward surprise from the September manufacturing ISM (49 from 47.6 vs 47.9 consensus) which was the third consecutive increase with the headline number matching the highest level since November 2022 and the graph showing a tentative bottoming out pattern. Details showed improvements in new orders (49.2 from 46.8; 12-month high), new export orders (47.4 from 46.5), production (52.5 from 50), employment (51.2 from 48.5) with the drawdown in inventories slowing (45.8 from 44) but customer inventories still accelerating (47.1 from 48.7). Together with a less dire activity picture, prices paid fell for a fifth month running with the pace fastening (43.8 from 48.4). The ISM release brought same soft landing vibes which is the Fed’s preferred scenario. November rate hike bets increased from 18% at last week’s close to 30% currently. Fed Chair Powell and Philly Fed Harker joined a roundtable during US dealings, but neither of them commented on the near term outlook for rates or the economy. Overnight, Cleveland Fed Mester said that she suspected the Fed may well need to raise the fed funds rate once more this year and then hold it there for some time as it accumulates more information on economic developments and assesses the effects of the tightening in financial conditions that has already occurred. US yields closed 5.9 bps to 10.7 bps (10-yr) higher yesterday, registering new cycle closing highs at the longer (5+) tenors. German yields increased by 2.5 bps (2-yr) to 9.8 bps (30-yr) with a new cycle closing high for the 30-yr yield. The dollar got a new push in the back with the trade-weighted greenback above 107 for the first time since November of last year this morning. EUR/USD got hammered from an intraday top around 1.0580 to 1.0460 currently. Next support levels stand at 1.0406 and 1.0201 which respectively are 50% and 62% retracement on the EUR/USD uplegs between September 2022 and July 2023. The Japanese yen tries to withstand the laws of gravity, but we’re likely only minutes/hours away from a push beyond USD/JPY 150 which could trigger interventions by the MoF/BoJ. Unless the BoJ profoundly changes its monetary policy stance, we believe that any interventions will eventually be in vain. Strong underlying trade dynamics are likely to remain at play today (higher real rates, stronger dollar and equity weakness).

News and Views

The British Retail Consortium indicated that price rises in British chain stores slowed further in September. Overall prices were unchanged compared to the previous month. Y/Y price growth slowed for 6.9% to 6.2%. Food prices for the first time in more than 2 years declined on a monthly basis (-0.1%), easing the Y/Y food price measure from 11.5% to 9.9%. Non-food prices rose 0.1% M/M and 4.4% Y/Y (from 4.7%). BRC chief economist Hellen Dickinson said BRC expects shop price to continue to fall further this year, but there are still mainly risks including “high interest rates, climbing oil prices, global shortages of sugar, as well as the supply chain disruption from the war in Ukraine."

At the first meeting presided by Michele Bullock as governor of the Reserve Bank of Australia, the RBA kept its policy rate unchanged at 4.10% for the fourth consecutive month. The RBA assesses that higher interest rates are working to establish a more sustainable balance between supply and demand in the economy and will continue to do so. Given a higher degree of uncertainty on future developments the RBA maintains a wait-and-see attitude for now. The RBA sees goods price inflation has eased further, but prices of many services are continuing to rise briskly and fuel prices have risen noticeably of late. Rent inflation also remains elevated. The RBA holds its assessment for CPI inflation to fall back within the 2–3% target range in late 2025. The Australian economy is still operating at a high level of capacity utilization, but this is expected to ease. RBA concludes that “some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will continue to depend upon the data and the evolving assessment of risks”. The Australian 2-y yield this morning started about 7 bps higher due to the sharp rise in the US, but gradually eased back to the 4.10% area (+1.5bp). The Aussie dollar suffers from broad-based USD strength. AUD/USD at 0.6315 trades at the lowest level since early November 2022.

Not Much Relief, After All

Relief that came with the news of a temporary avoidance of a potential government shutdown remained short lived. Sentiment in stocks markets turned rapidly sour, both in Europe and in the US, while the US treasury yields didn’t even react positively to the no shutdown news in the first place. The selloff in the US 10-year bonds accelerated instead; the 10-year yield hit the 4.70% mark, whereas the 2-year yield remained steady-ish at around the 5.10% level, as the Federal Reserve (Fed) Chair Jerome Powell didn’t say much regarding the future of the monetary policy yesterday, but his colleagues continued to sound hawkish. Fed’s Michelle Bowman said that multiple more interest rate hikes could be needed to tame inflation, while Micheal Barr repeated that the rates are likely restrictive enough, but they should stay higher for longer. Sufficiently hawkish words combined to a set of still-contracting-but-better-than-expected manufacturing PMI data justified the positive pressure on US sovereigns.

The gap between the US 2 and 10-year yields is now closing, but not necessarily for ‘good’ reasons. Normally, you would’ve expected the short-term yields to ease more rapidly than the long-term yields when approaching the end of a tightening cycle, with the expectations of future rate cuts kicking in. But what we see today is bear steepening where the 10-year yield accelerates faster than the 2-year yield. The latter suggests rising inflation expectations where investors prefer to buy short-term papers and to wait for the rate hikes to end before returning to long-term papers. The US political uncertainties and a potential government shutdown before the end of the year, and an eventual US credit downgrade likely add an additional downside pressure in long dated US papers.

The rising yields do no good to stocks. But interestingly, yesterday, the S&P 500 closed flat but the more rate-sensitive Nasdaq stocks were up. The US dollar index extended gains past the 107 level; the index has now recovered half of losses it recorded since a year ago, when the dollar depreciation had started.

The AUDUSD extended losses to the lowest levels since last November as the Reserve Bank of Australia (RBA) maintained its policy rate unchanged at the first meeting under its new Governor Michelle Bullock. This is the 4th consecutive month pause for the RBA. The bank said that there may be more tightening in the horizon to bring inflation back to the 2-3% range (inflation currently stands at 5.2%). But the fact that Australians biggest trading partner, China, is not doing well, the fact that real estate market in Australia is battered by rising rates and the fact that the Chinese property crisis is now taking a toll on Australia’s steel exports toward China are factors that could keep Australian growth below target and prevent the RBA from hiking further. If China doesn’t get well soon, Australia will see its iron ore revenues, among others, melt in the next few years, and that’s negative for the Aussie in the medium run.

Elsewhere, the EURUSD sank below the 1.05 level on the back of accelerated dollar purchases and softening European Central Bank (ECB) expectations following last week’s lower-than-expected inflation figures. Cable slipped below a critical Fibonacci support yesterday, and is headed toward the 1.20 psychological mark. The weakening pound is not bad news for the British FTSE100, as around 80% of the FTSE100 companies’ revenues come from abroad, and they are dollar denominated. Plus, cheaper sterling makes the energy-rich FTSE100 more affordable for foreign investors. Even though FTSE100 fell with sliding oil prices yesterday - and this year’s performance is less than ideal compared to European and American - London’s stock market is closing the gap with Paris, and rising oil prices and waning appetite for luxury stuff could well offer London its status of Europe’s biggest stock market, yet again.

Speaking of oil prices, crude oil sank below $90pb level yesterday, partly due to the overbought market conditions that resulted from a more than a 40% rally since end of June, and partly because the ‘higher for longer rates’ expectations increased odds for recession.

Higher Yields and Stronger Dollar

Market movers today

ECB's Lane speaks on "key factors of inflation and ECB's response".

Public holiday in Germany.

We will receive inflation data from Switzerland, but after last month's surprise decision not to hike rates the release is unlikely to change the view that no more rate hikes are coming.

In Sweden, we get service PMIs, read more in the Nordic section below.

In the US, we get job openings, which is an important labour demand indicator for the Fed.

The Reserve Bank of New Zealand will announce its rate decision at 3.00 CET Wednesday.

The 60 second overview

Labour market: The euro area unemployment rate declined to a record-low 6.4% in August from 6.5% in July (revised up from 6.4%), highlighting the strength of the labour market this year. We still expect to see a slow and muted rise in unemployment going forward, though, in line with the weakening signals from the PMI employment figures in August and September.

US: The final PMI and ISM surveys painted a slightly more upbeat picture for US manufacturing in September. Leading new orders indices remain at contractionary levels (below 50), reflecting still weak consumer demand for manufactured goods. But as inventory levels are now declining faster than orders, production has slowly started to recover, which was evident in higher output and employment components driving the upticks in headline indices. That said, for inflation and the Fed, the development in the services sector matters more, and we continue to see weakening consumption growth towards the winter. The mixed outlook was reflected in yesterday's Fed commentary as well. Bowman, who is among the most hawkish FOMC participants, stuck to her earlier view that rates would have to be hiked further. Barr, on the other hand, sounded more cautious saying that rates are 'likely at or near sufficiently restrictive levels'. Powell did not touch on the monetary policy outlook in the roundtable discussion with Harker. Today's main focus will be on the JOLTs Job Openings release, which is a key labour demand indicator for the Fed, and a decent leading indicator for wage growth. In addition, Cleveland Fed's Mester (non-voter, hawk) and Atlanta Fed's Bostic (non-voter, dove) will be on the wires discussing economic outlook.

RBA: As expected, the Reserve Bank of Australia kept rates unchanged at a meeting this morning, arguing that recent data was consistent with inflation returning to its 2-3 percent target over time with output and employment still growing.

Equities: Global equities had a tough day yesterday! At headline level the moves were not so bad with MSCI world down 0.2%. However, underneath there was a very interesting rotation with cyclicals outperforming defensives by more than 1% and growth outperforming value despite the yield curve across the western world moving higher. US tech outperformed while utilities got crushed and had the worst day since the Covid downturn. Fortum and not least Ørsted were part of the utility sell-off. Long duration small caps received the same treatment. Russell 2000 is down 12% since Aug-1st and is now lower for the year. Higher and steeper curve is a large part of the explanation but still not 100% descriptive of the rotation as banks underperformed in what should all else equal be a very benign environment for the sector. In the US, Dow -0.2%, S&P 500 +0.01%, Nasdaq +0.7% and Russell 2000 1.6%.

Asian still with markets close and celebration of Golden Week in China. Hong Kong open with Chinese H-shares down 3% and rest of the open markets lower as well. European and US futures lower but not to the same extend as the sell-off in Asia could suggest.

FI: The first trading day of the quarter ended with a strong sell-off driven by a combination of the higher-for-longer narrative and strong US data. 10y German bunds tested 2.92% which was about 7bp higher than Friday's close. ECB's de Guindos repeated the ECB guidance of no imminent rate cuts. On the question of MRR, de Guindos pushed back and said that ECB is not focusing on profit/loss of the central bank but on price stability. Similar to previous yield curve dynamics, the long end staged the sell-off with the 2s30s yield curve 8bp steeper on the day. Germany is out for a public holiday today.

FX: The first session of the week was characterised by a setback to European cyclically sensitive currencies such as SEK, GBP NOK and HUF while the USD and CAD were among the top-performers. EUR/USD has moved below the 1.05-level while EUR/NOK and EUR/SEK have rebounded to the high 11.30s and 11.50s, respectively.

Credit: Credit markets were negatively affected by the weak European equity markets on Monday. The primary market was also muted with limited activity. ITraxx Main was 2bp wider at 82bp while iTraxx Xover was 4bp wider at 438bp.

Nordic macro

PMI Manufacturing released yesterday was bleak, where four out of five sub-indices contributed to the decline in the PMI total for September to 43.3 compared to a downwardly revised 45.5 in August. Furthermore, Riksbank minutes were published yesterday. The SEK continues to be in focus (mentioned 43 times vs 44 in June), and especially with respect to the impact on inflation. Overall, as indicated in the rate path, the door is open for a possible hike in November as well (or even later according to the governor of the board, Erik Thedéen).

Looking forward, Service PMI may drop today. This would be a more stable development as it is hovering around the 50-point expansion threshold. Most interesting will be how the sub-index for suppliers' input prices develop as the sticky service inflation was one of the main worries of the Riksbank's board members in yesterday's published minutes.