Sample Category Title

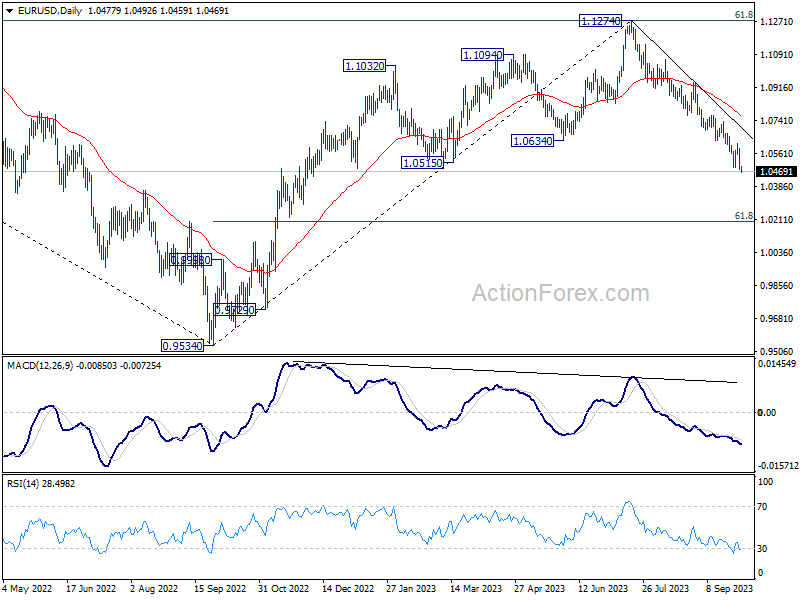

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0440; (P) 1.0516; (R1) 1.0554; More...

Intraday bias in EUR/USD stays on the downside and outlook is unchanged. fall from 1.1274 is in progress and should target 1.0199 fibonacci level next. On the upside, break of 1.0616 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0759) holds, in case of rebound.

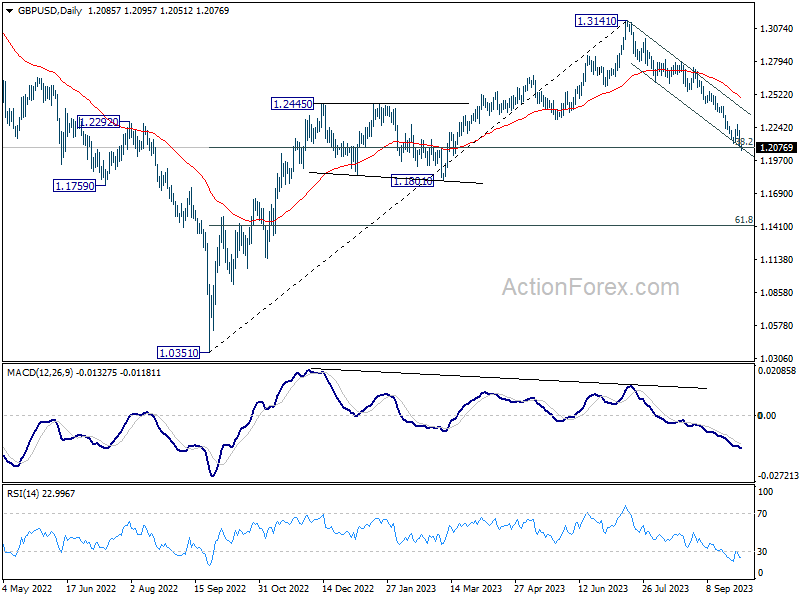

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2042; (P) 1.2131; (R1) 1.2176; More...

Intraday bias in GBP/USD remains on the downside and outlook is unchanged. Sustained trading below 1.2075 fibonacci level would carry larger bearish implication. Fall from 1.3141 should then target 1.1801 support next. On the upside, break of 1.2270 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2486) holds, in case of rebound.

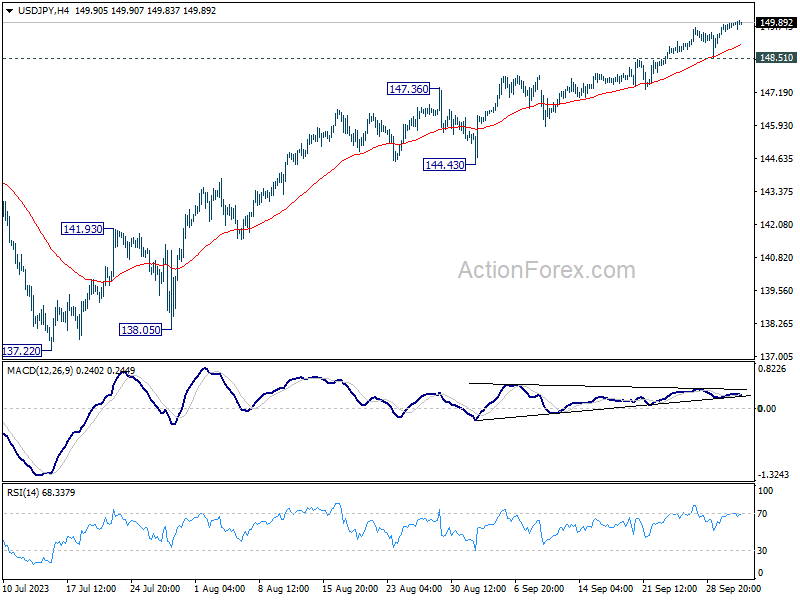

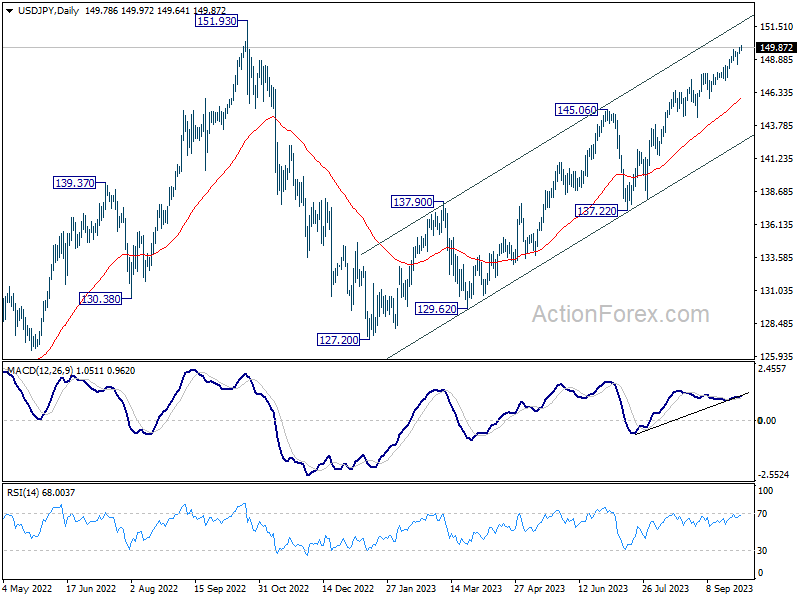

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.58; (P) 149.73; (R1) 150.02; More...

Intraday bias in USD/JPY remains on the upside and outlook is unchanged. Current rise from 127.20 should target a retest on 151.93 high next. On the downside, break of 148.51 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

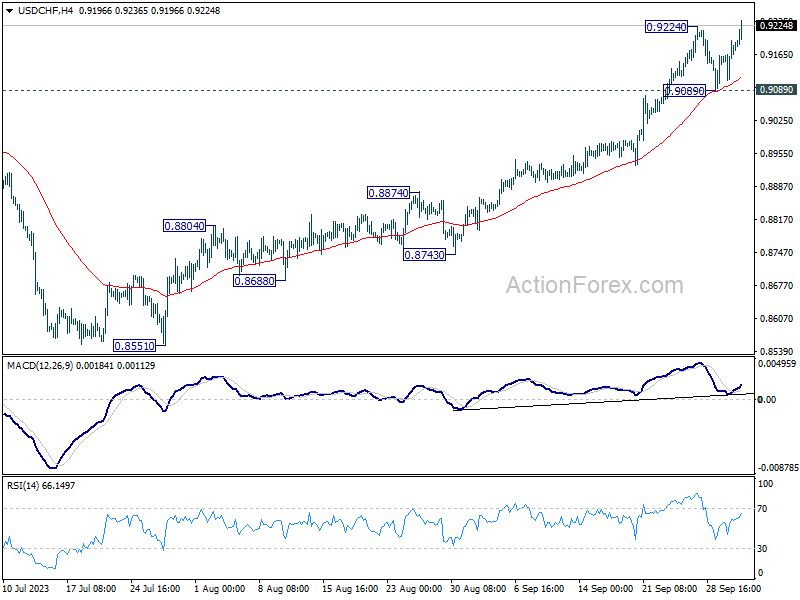

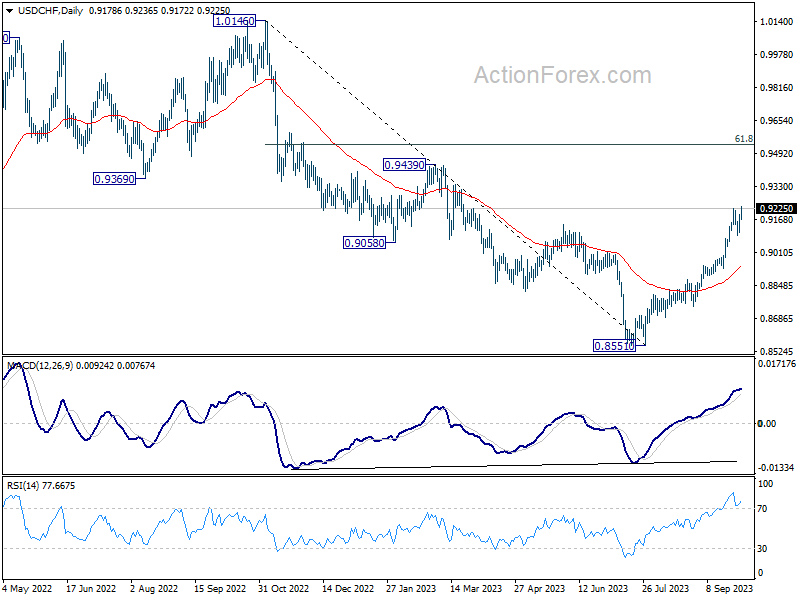

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9130; (P) 0.9163; (R1) 0.9215; More....

USD/CHF's rally from 0.8551 resumed by breaking through 0.9224 resistance today. Intraday bias is back on the upside. Current rally should target 0.9439 resistance next. On the downside, break of 0.9089 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8942) holds, even in case of deep pullback.

Yield Rally Propels Dollar Forward; Swiss CPI Weighs on Franc

In the spotlight today are the developments within the treasury markets. US 10-year yields have soared, reaching their highest point since 2007. This surge is largely attributed to expectations that Fed will keep high interest rates for longer, if not push them even higher. Fed hawks have been vocal this week, indicating the plausible scenario of an additional rate hike this year. Meanwhile, Germany's 10-year yield is also experiencing a significant uptick, heading back towards a 12-year peak.

In contrast, Japan's 10-year JGB yield has seen a decline. This comes in the wake of BoJ's announcement to purchase bonds with five to ten-year maturities on Wednesday. This move by the BoJ clearly illustrates its commitment to "manage" the ascension of 10-year JGB yield. However, this control measure is likely to exert pressure on Yen due to the widening yield gap with US and Europe. This also offset impacts of repeated verbal intervention by Japanese Finance Minister Shunichi Suzuki.

Amid this backdrop, the US Dollar emerges as the unequivocal leader in the currency markets, trailed distantly by Euro and Yen. Aussie and Kiwi languish at the tail end, burdened by a pervasive risk aversion sentiment in Asia and plummeting copper prices. The Swiss Franc is not faring any better, grappling with the repercussions of disappointing CPI data, while Canadian Dollar and Sterling present a mixed picture.

From a technical standpoint, Copper falls sharply this week and breaks through 3.6008 support. Prior rejection by 55 D EMA also retains near term bearishness. Current decline form 4.0145 is probably resuming whole fall from 4.3556. Next target is 3.5387 support. Decisive break there will confirm this bearish case, and potentially exacerbating the woes of the already beleaguered Aussie.

In Europe, at the time of writing, FTSE is down -0.24%. DAX is down -0.83%. CAC is down -0.86%. Germany 10-year yield is up 0.0176 at 2.945. Earlier in Asia, Nikkei dropped -1.64%. Hong Kong HSI dropped -2.69%. Singapore Strait Times dropped -0.51%. Japan 10-year JGB yield fell -0.0125 to 0.764.

ECB's Lane: There is still work to be done

ECB's Chief Economist Philip Lane voiced his ongoing concerns regarding the elevated inflation levels in the Eurozone during a conference. Despite a drop in inflation in September to its lowest in two years, Lane emphasized the need for continued efforts to steer price increases back towards the 2% target.

Lane stated, "Price increases are still well above 2%, we are not at the inflation target yet and therefore there is still work to be done in terms of bringing inflation down."

While wage inflation is anticipated to decline, Lane cautioned that this process would be gradual, as "it's going to take months, it will take time". Lane's focus appears to be more on services inflation data. "I think we will be looking at services inflation data for quite a while," he shared

One key area of focus for the ECB is the unpredictable nature of energy prices. "We don't expect the current low gas price to be maintained, we do expect to see gas prices go up from where they are now," he said. "Energy has been such a volatile component, it's going to be very important to us to keep an eye on energy in the coming months and years."

Swiss CPI ticks up to 1.7% yoy, core down to 1.3% yoy

Swiss CPI fell -0.1% mom in September, below expectation of 0.0% mom. Core CPI (excluding fresh and seasonal products, energy and fuel) was down -0.1% mom. Domestic products prices dropped -0.2% mom. Imported products prices rose 0.3% mom.

For the 12-month period, CPI rose from 1.6% yoy to 1.7% yoy, below expectation of 1.8% yoy. Core CPI slowed from 1.5% yoy to 1.3% yoy. Domestic products prices slowed from 2.2% yoy to 2.1% yoy. Imported products prices turned positive from -0.3% yoy to 2.2% yoy.

RBA holds rates steady, maintains hawkish bias

In what was Michelle Bullock's inaugural meeting as Governor, RBA opted to maintain its cash rate target at 4.10%, aligning with broad market expectations. The central bank's statement carried a hawkish tone, noting that "some further tightening of monetary policy may be required. The exact course of such adjustments, however, would be determined by "the data and the evolving assessment of risks."

While RBA acknowledged that inflation had passed its pinnacle, the levels remain uncomfortably elevated. It observed a decline in goods price inflation but pointed out the brisk rise in service prices, as well as notable increases in fuel and rent prices.

The central bank projects a gradual return of CPI inflation to its 2-3% target range by the end of 2025. This aligns with their prediction of sustained below-trend growth for the economy, expecting this trend to persist. Consequently, they anticipate the unemployment rate to inch up, reaching approximately 4.5% towards the end of the following year.

Outlook is shrouded in "significant uncertainties." These encompass variables like service price inflation, delays in monetary policy transmission monetary policy, and businesses' reactions in terms of pricing and wages. Consumer behavior, particularly household consumption patterns, also remains an unpredictable factor.

On a global scale, RBA expressed concerns over China's economy, especially given the prevalent disturbances in its property market.

NZ NZIER survey shows mild recovery in business sentiment

NZIER Quarterly Survey of Business Opinion reveals a modest improvement in business confidence for the September quarter, climbing to -52.7 from its previous position at -60.3. However, it's evident that overall sentiment within the business community remains pessimistic. Trading activity for the next three months improved from -16.6 to -14.2.

One major positive shift observed was the pronounced decrease in reported labour shortages. Fewer businesses now list the challenge of finding labour as their principal operational bottleneck, shifting their concerns instead to a softer demand environment. This transition in concerns implies that the recent hikes in interest rates may be suppressing economic demand in the country.

On the flip side, the easing of capacity pressures hasn't provided much respite to businesses in terms of costs. A significant 68.2% of respondents noted a rise in their operating costs over the past three months, only a minor reduction from the prior quarter's 67.1%. Moreover, the inclination to transfer these cost pressures to consumers has subsided, with 57.3% of businesses raising output prices in the recent quarter, down from a previous 68.8%.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9130; (P) 0.9163; (R1) 0.9215; More....

USD/CHF's rally from 0.8551 resumed by breaking through 0.9224 resistance today. Intraday bias is back on the upside. Current rally should target 0.9439 resistance next. On the downside, break of 0.9089 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8942) holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | NZIER Business Confidence Q3 | -52 | -63 | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Aug | 6.20% | 6.90% | ||

| 00:30 | AUD | Building Permits M/M Aug | 7.00% | 3.30% | -8.10% | |

| 03:30 | AUD | RBA Interest Rate Decision | 4.10% | 4.10% | 4.10% | |

| 06:30 | CHF | CPI M/M Sep | -0.10% | 0.00% | 0.20% | |

| 06:30 | CHF | CPI Y/Y Sep | 1.70% | 1.80% | 1.60% |

Dollar Traders Lock Gaze on US Nonfarm Payrolls

- US performs better than other major economies

- After higher Fed rate projections, focus turns to US jobs data

- A still-tight labor market could further lift the dollar

- The data is coming out on Friday, at 12:30 GMT

Hawkish Fed turbocharges the dollar

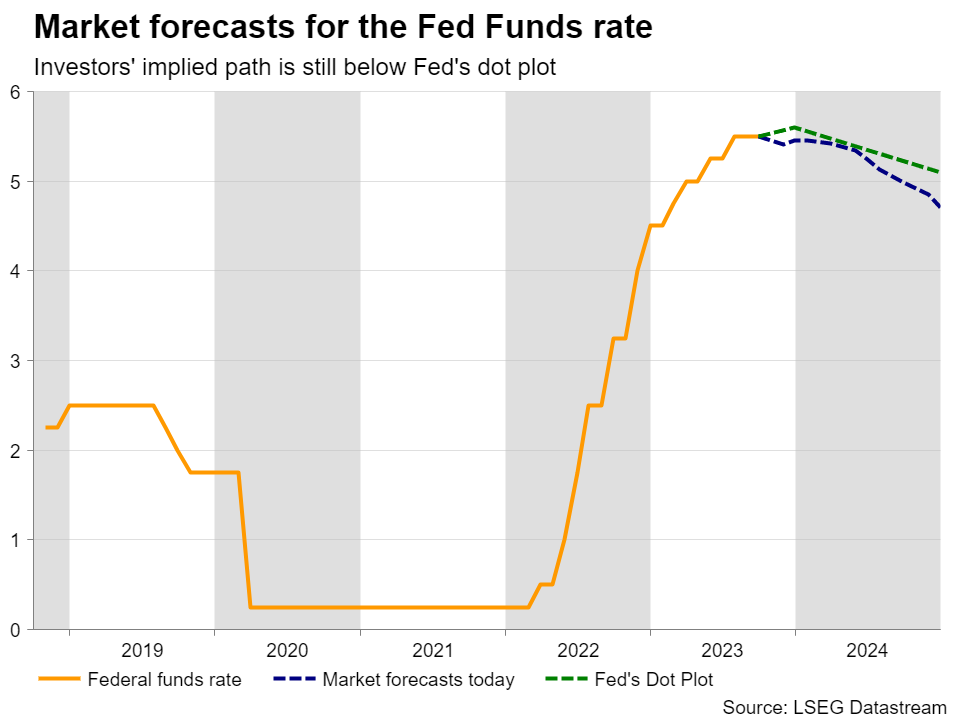

With the US economy proving more resilient than other major ones and inflation rebounding on the back of rallying oil prices, the Fed raised its rate-path projections at its latest gathering, although it did not press the hike button. Specifically, policymakers forecasted one more quarter-point increase before the end of this year, while they saw interest rates ending 2024 at 5.1%, up from June’s projection of 4.6%.

This allowed Treasury yields to climb higher and added more fuel to the dollar’s engines. Although the greenback pulled back at the end of last week, it staged a remarkable comeback on Monday following the better-than-expected ISM manufacturing PMI, suggesting that last week’s retreat was probably due to investors rebalancing their portfolios and hedge funds closing their books for the end of Q3, instead of changing fundamentals.

Will job numbers allow trend continuation?

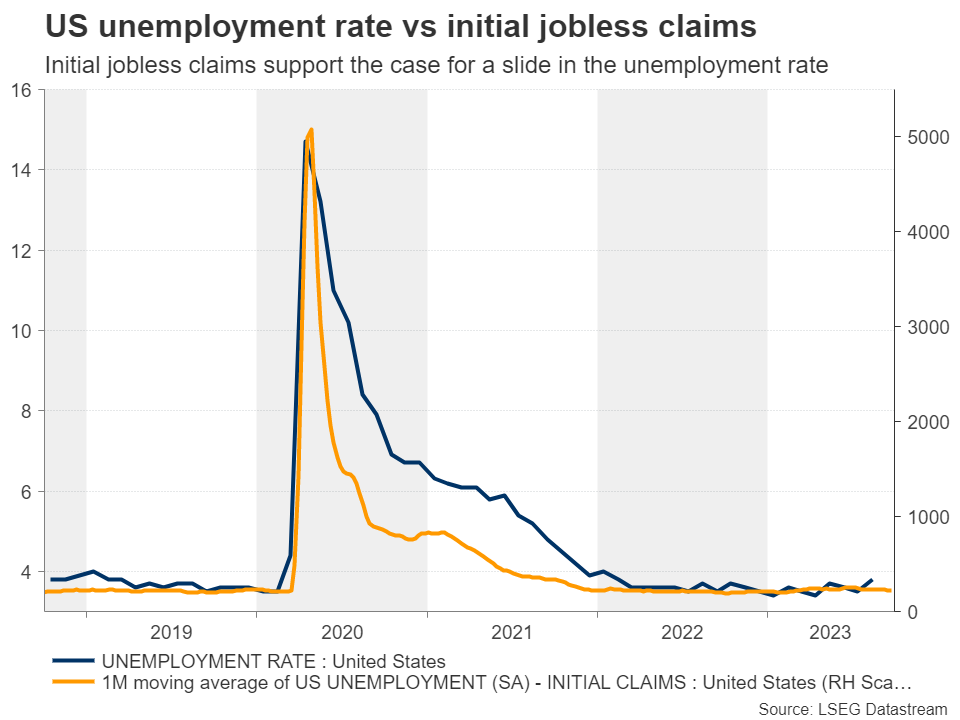

Moving forward, whether this impulsive wave in the greenback’s uptrend will continue may depend on Friday’s employment report. Nonfarm payrolls are expected to have slowed to 163k from 187k, but the unemployment rate is forecast to have ticked back down to 3.7% from 3.8%, which is supported by the modest decline in the 4-week moving average of initial jobless claims.

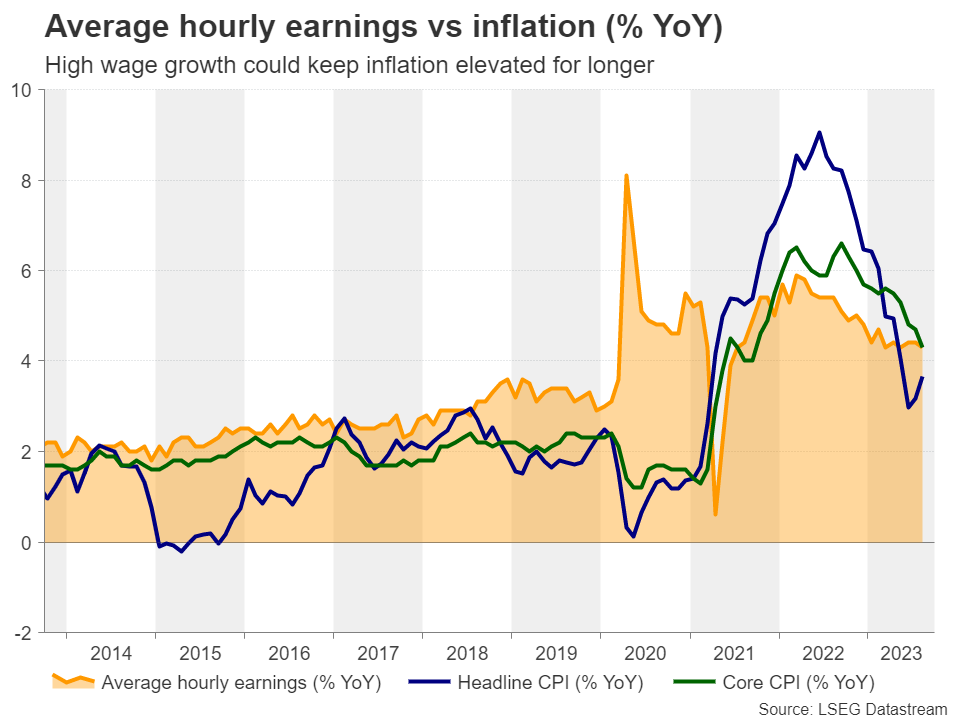

That said, although the initial reaction in the dollar may come from any surprise in the NFPs or the unemployment rate, whether it will be a lasting one could depend on wage growth, which may provide a glimpse of where inflation may be headed in the months to come. Average hourly earnings are expected to have slightly accelerated in monthly terms, keeping the yoy rate steady at 4.3%.

Combined with the uptrend in oil prices, as well as the rebound in headline inflation and projections that the US economy likely performed much better in Q3 than in Q2, elevated wage growth may add to the risk of underlying price pressures intensifying in the months to come.

With investors still projecting a lower rate path than the Fed, assigning only around a 50% probability for another hike and expecting rates to fall to 4.7% by the end of next year, it seems that there is ample room for upside adjustment should Friday’s jobs data come in strong, which could push yields higher and thereby encourage traders to buy more dollars.

At the same time, equities are likely to resume their slide as expectations of ‘higher for longer’ interest rates could exert downside pressure on valuations. Yes, upbeat economic data usually have a positive impact on a nation’s stock market, but the financial community is still in an environment where good news is bad news as it increases the need for additional rate hikes.

Fed not the sole driver

What’s more, expectations about the Fed’s future course of action are not the sole driver of the US dollar and Wall Street. There is also a strong note of uncertainty due to the economic challenges facing China, Eurozone and the UK. And with no other alternative, the only place to seek safety seems to be the US dollar. The yen has long lost its safe-haven status due to the BoJ maintaining a lid on Japanese government bond yields at a time when US rates are keep rising, while gold has fallen victim to both surging yields and a strong dollar, which has lost nearly 6% since September 25.

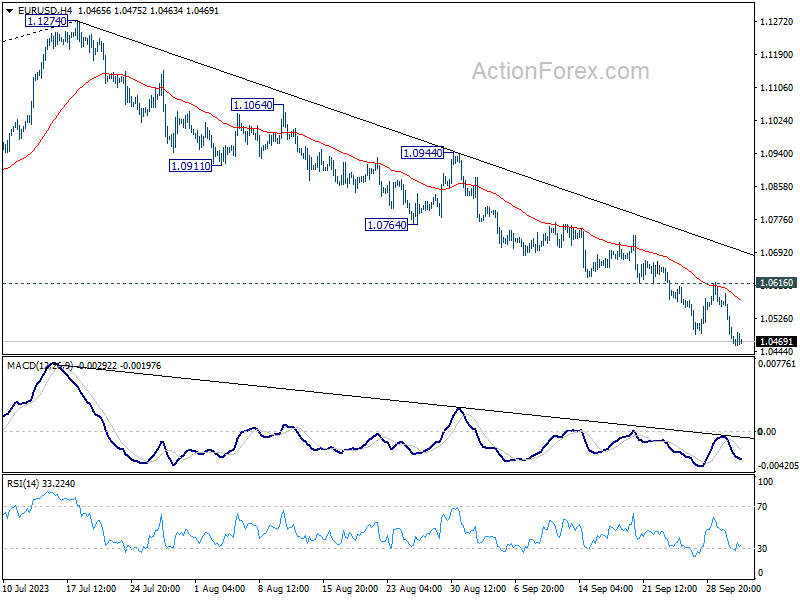

Euro/dollar keeps printing lower highs and lower lows

Euro/dollar was among the pairs that rebounded decently at the end of last week due to the dollar’s pullback. The rebound happened after the price hit support at 1.0485. However, the pair surrendered those gains on Monday, staying below the downtrend line drawn from the high of July 18 and thereby confirming that the short-term outlook remains negative. The bears managed to push the action slightly below 1.0485 today, and if they are willing to stay in the driver’s seat, a dive towards the low of November 30 at 1.0290 could be possible.

For traders to allow a bigger dollar correction, Friday’s data may need to disappoint. However, even if euro/dollar climbs above 1.0665, the outlook will not turn positive, rather just neutral as the price would be back within the sideways range that contained most of the price action between January 9 and September 22.

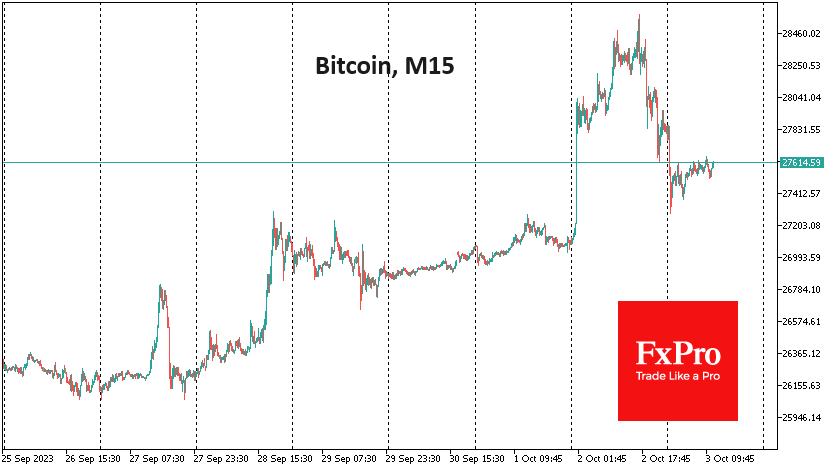

Crypto Fails to Accelerate But Sticks to an Uptrend

Market picture

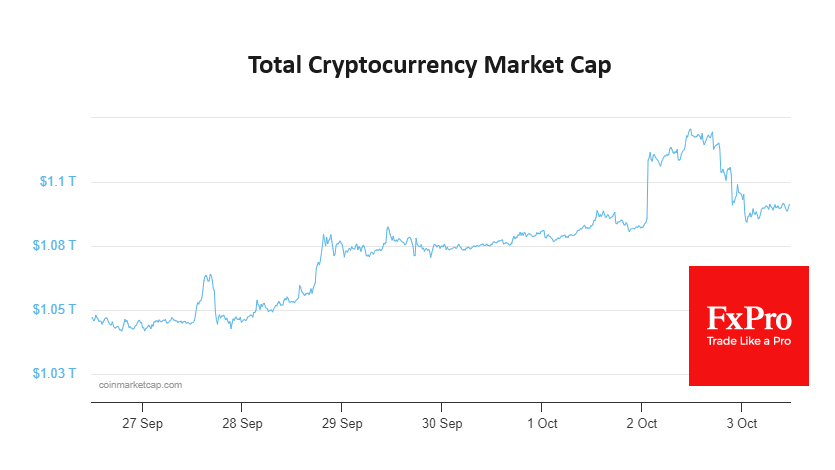

Crypto market capitalisation fell by 2.5% to $1.09 trillion. The market failed to accelerate but remains in an uptrend despite the general decline in demand for risk assets.

After peaking above $28.5K on Monday, Bitcoin gradually slid shortly after the main US session. At one point on Tuesday morning, the price fell to $27.3K, where the first cryptocurrency found buyers. However, it’s easy to see that buyers dominate in a calm state. Excluding short-term spikes and pullbacks, it is easy to see a steady upward trend since the 25th of September.

Bitcoin received support when it touched the area of previous highs, turning resistance into support. This is a bullish sign that sets up another test of the 200-day ($28K) with potential for further strength.

News background

The main factors holding back further growth in the asset are the SEC’s strict policies and global recession risks.

According to CoinShares, investments in crypto funds rose by $21 million last week after six weeks of outflows. Bitcoin investments increased by $20 million, while Ethereum investments fell by $1.5 million. Solana investments rose sharply, up $5 million at a time.

Grayscale has filed with the SEC to convert the Grayscale Ethereum Trust into a spot Ethereum ETF. The company expects this to “expand the regulatory boundaries” of the leading altcoin in the US.

UBS Asset Management, one of the world’s most significant stock market players, has launched the first tokenised money market fund pilot on the Ethereum blockchain.

The total value locked (TVL) in the Solana blockchain exceeded $339 million, the highest since November 2022. However, the current figures are still far from the historic highs of November 2021, when the ecosystem’s TVL reached nearly $10 billion.

AUD/JPY Technical – Bearish Reaction from Key Long-Term Range Resistance in Place Since Oct 2007

- The multi-year up move of the AUD/JPY from the March 2020 low of 59.88 has shown bullish exhaustion conditions right at the long-term secular range resistance of 96.88.

- Today’s RBA monetary policy decision has reinforced the short-term bearish tone via the breakdown below the 20-day moving average.

- Key short-term resistance to watch will be at 95.70 which also coincides with the 50% Fibonacci retracement of the current minor short-term downtrend phase from 29 September 2023 high to today, 3 October current intraday low of 94.50.

The cross-pair AUD/JPY has continued to tumble in today’s Asia session (3 October) and broke below its 20-day moving average right after the monetary policy decision of the Australian central bank, RBA to keep its cash policy rate unchanged at 4.1% for the fourth consecutive meeting.

Today’s move from RBA has been widely expected as inflationary pressure in Australia has started to ease with the latest reading released yesterday, 2 October from the private sector compiled Melbourne Institute’s monthly inflation gauge that slipped to 0% m/m in September from 0.2% m/m in August.

The RBA has continued to offer a “balance view” in terms of its latest monetary policy guidance where it painted a picture that stated the current inflationary environment in Australia is still too high despite it may have passed its peak as it may stay at elevated levels for quite some time. Reiterated that any interest rate adjustment will be data dependent due to the evolvement of economic growth and inflation pressure.

Potential start of multi-week down move sequence

Fig 1: AUD/JPY long-term secular trend as of 3 Oct 2023 (Source: TradingView, click to enlarge chart)

Overall, from the lens of technical analysis, the current short-term downtrend phase of the AUD/JPY that shed – 241 pips from its 29 September 2023 high of 96.92 to today’s current intraday low of 94.50 has reacted off from a long-term secular range resistance at 96.88 (see monthly chart) which suggests a potential medium-term bearish reversal may be in progress.

Hence, an increase in odds that the AUD/JPY is likely to shape a multi-week down move to test its 200-day moving average that is now acting as a support at 92.25 which also coincides with the major ascending trendline from March 2020 swing low of 59.88.

Oversold in the short-term

Fig 2: AUD/JPY minor short-term trend as of 3 Oct 2023 (Source: TradingView, click to enlarge chart)

The price actions of the AUD/JPY have reached an oversold condition as indicated by the hourly RSI indicator which in turn may see a minor corrective bounce to retest the 20-day moving average and the former minor ascending support from 8 September 2023 low that now confluences at an intermediate resistance zone of 95.05/95.20.

Watch the 95.70 key short-term pivotal resistance to maintain the status of short-term downtrend scenario for a further potential down leg to test the next intermediate support at 93.70 (minor swing low areas of 5/8 September 2023) in the first step.

On the flip side, a clearance above 95.70 invalidates the bearish tone to see a retest on the 96.88 key long-term secular resistance.

Swiss Franc Slips as Inflation Falls

- Swiss inflation declines by 0.1%

The Swiss franc has extended its losses on Tuesday. In the European session, USD/CHF is trading at 0.9212, up 0.31%.

Swiss inflation declines by 0.1%

Major central bankers have their hands full as they continue to battle stubborn inflation. The Swiss National Bank is also concerned about inflation, but other central bankers would love to have the SNB’s problem, as inflation remains within the SNB’s target range of 0%-2%.

Today’s Swiss CPI release showed inflation declining by 0.1% m/m in September, compared to a gain of 0.2% m/m in August. On an annual basis, inflation ticked higher to 1.7%, up from 1.6% in August. The core inflation rate decreased to 1.3% y/y, down from 1.5% in August.

This inflation data should be encouraging for the SNB, which has likely wrapped up its rate-tightening cycle. The central bank raised rates five straight times but took a pause at last month’s meeting and left the benchmark rate at 1.75%. This surprised the markets, which had expected a quarter-point hike. The SNB’s tightening has cooled down the economy and the decline in September inflation supports the SNB continuing to pause at the next meeting in December. The markets may even be looking for a rate cut, but I don’t expect the SNB to start trimming rates until it is convinced that inflation will remain low.

The SNB views currency intervention as a tool to help stabilize the exchange rate, and a Reuters report last week found that the SNB sold $44.2 billion worth of foreign currencies in the second quarter, the largest sale since the SNB started keeping records of its forex transactions in 2020. The SNB’s strategy has been to boost the Swiss franc, which has lowered the price of imports, thus dampening inflation.

USD/CHF Technical

- USD/CHF is putting pressure on resistance at 0.9231. Above, there is resistance at 0.9310

- 0.9145 and 0.9067 are providing support

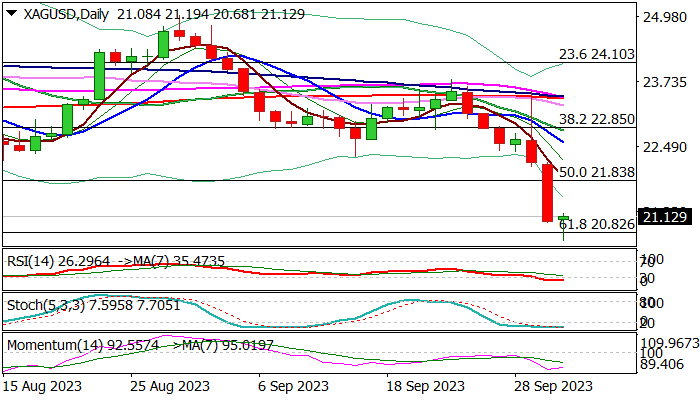

XAG/USD: Silver Consolidating Above New Multi-month Low

Silver price edged higher early Tuesday, as bears take a breather after strong acceleration in past two days (down almost 7%) hit the lowest in over six months.

The US dollar rose further and remains supported by signals that the Fed is likely to keep restrictive monetary policy for some time, as the US economy remains surprisingly resilient despite strong negative impact from high borrowing cost.

Bears found a temporary footstep at $20.82 (61.8% retracement of $17.54/$26.12 rally) with partial profit-taking to push the price higher to offer better selling opportunities, as traders await release of the first from three key reports from US labor sector - JOLTS job openings (Aug f/c 8.80M vs July 8.82M) with release at /above consensus to provide fresh positive signals for dollar.

Firm break of cracked support at $20.82 to expose supports at $20.28 (200MMA); $20 (psychological) and $19.88 (early March higher base). Broken Fibo 50% ($21.83) should ideally cap, with extended upticks not to exceed former range floor ($22.10/20) to keep bears in play.

Res: 21.83; 22.20; 22.56; 22.84.

Sup: 20.82; 20.68; 20.28; 20.00.