Sample Category Title

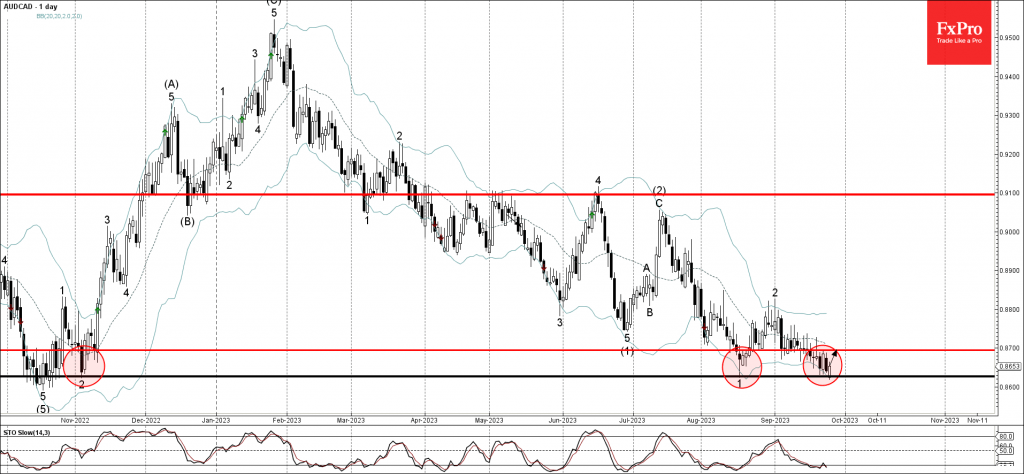

AUDCAD Wave Analysis

- AUDCAD reversed from key support level 0.8630

- Likely to rise to resistance level 0.8700

AUDCAD recently reversed up from the key support level 0.8630 (which has been repeatedly reversing the pair from last November) intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 0.8630 follows the earlier upward reversal from the same support level – which formed the daily Bullish Engulfing.

Given the oversold daily Stochastic and the strength of the support level 0.8630, AUDCAD can be expected to rise toward the next resistance level 0.8700.

U.S. Government Shutdowns & U.S. Dollar Implications

Summary

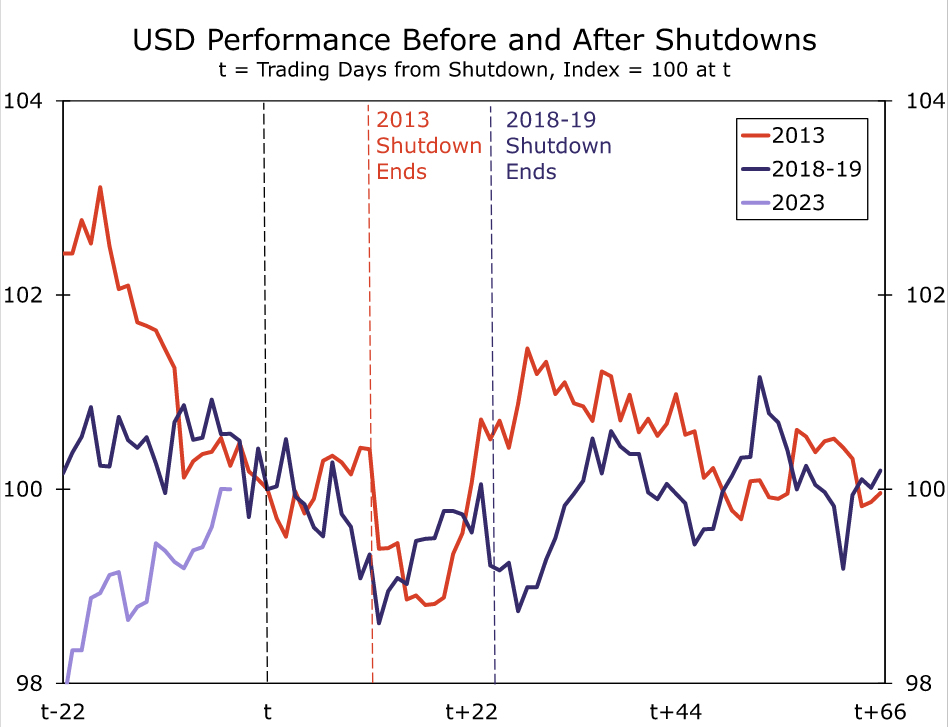

A potential U.S. government shutdown that could start October 1st looms, the chances of which are more or less seen as a coin flip at this point. Should a shutdown transpire, there could be a negative impact of the U.S dollar, albeit one that is likely to be modest and short-lived. Recent history suggests the U.S. dollar index (DXY) could fall by around 1%-1.5% in the several weeks following the start of the shutdown. Also in recent shutdown episodes, three months after the shutdown began the dollar had recovered its losses and there was no meaningful or long-lasting impact on the dollar. In the event a U.S. government shutdown does occur, we would expect a similar pattern to unfold, and we would not make significant changes to our longer-term outlook for the U.S. dollar.

Potential U.S. Shutdown Looms For the U.S. Dollar

Last week our U.S. economics colleagues wrote about the potential for a U.S government shutdown that could begin on 1 October. At this point, our teammates believe the chances of U.S. government shutdown are more or less a coin flip. In recent U.S. government shut down episodes, the direct hit to U.S. growth was modest. Consumer confidence has historically dipped during periods of a government shutdown, and while the impact to U.S. growth has typically been immaterial, not all the lost economic activity was fully recovered. The above report captures the economic impact of a government shutdown. In this report, we will assess the potential implications of a government shutdown on the U.S. dollar. History of U.S. government shutdowns is somewhat limited, but we can infer the potential impact on the dollar by examining the most recent episodes. To that point, we examined the shutdowns that began in October 2013 (which lasted for 16 calendar days or 11 trading days) and December 2018 (which lasted 35 calendar days or 24 trading days). In our view, these most recent episodes are likely to be the most instructive for a potential shutdown in 2023. The economic and political environment in 2013 as well as 2018-2019 more resembles the current political and economic climate than the backdrop during the prior shutdown of the 1990s.

We assess the greenback's performance using the U.S. dollar index (DXY). Our first observation is that, at least heading into these two shutdowns, the U.S. dollar's performance is varied and driven by the prevailing economic conditions, not necessarily anticipation of the shutdown. In 2013, the U.S. dollar softened in the weeks heading into the shutdown. At that time, U.S. economic growth was subdued and Federal Reserve interest rates were steady at essentially 0%. The 2013 government shutdown occurred toward the end of the Fed's “Taper Tantrum”, which is important to note as longer term U.S. Treasury yields had already started to stabilize and global equity markets had begun to recover. Against this backdrop, the U.S. dollar was softening as risk sentiment started to improve. During the 2013 government shutdown, the U.S. dollar index actually gained very slightly (by 0.4%) over those 11 trading days. However, U.S. dollar sentiment did take a short-term hit such that 17 trading days after the start of the shutdown, the U.S. dollar index saw the largest peak-to-trough decline of 1.2%. Nonetheless, three months from the start of the shutdown, the U.S. dollar index had recovered all of its losses.

In contrast, during the 2018-2019 period, the U.S. dollar was steadier heading into the shutdown. In this instance, the U.S. economic backdrop was firmer relative to 2013 in that U.S. GDP growth was on a clear upwards trend. The Federal Reserve was coming to the end of a rate hike cycle and, towards the end of 2018, U.S. equity markets also corrected lower, providing safe haven support to the greenback during a period of elevated financial market volatility. Over the course of the 2018-19 episode, the U.S. dollar index fell marginally (by 0.8%) during the actual shutdown episode. Once again, U.S. dollar sentiment took a short-term hit such that 12 trading days after the start of the shutdown, the U.S. dollar index saw the largest peak to trough fall, a decline of 1.4%. In similar fashion to 2013, the greenback also fully recovered its losses experienced during this period three months following the start of the shutdown.

Today's environment is quite similar to 2018-2019. The current backdrop is defined by resilient U.S. economic growth as well as a Federal Reserve that is approaching, or has possibly already reached, the end of its tightening cycle. Also, similar to 2018-2019, equity prices are correcting lower. While it is worth noting that the current landscape is most similar to 2018-19, the greenback has followed a consistent pattern once those shutdowns began, regardless of the pre-shutdown trend. That is, a short-lived and modest decline in the value of the dollar. We would expect the greenback to behave very similarly if a U.S. government shutdown transpires this time around, and a shutdown could translate into a 1%-1.5% decline in the DXY dollar index in the weeks after the event transpires. At the same time, we believe the same pattern of a dollar rebound would be repeated this time around. In our view, any greenback depreciation will be short-lived, and we would expect the dollar to recover in the months following the re-opening. Longer-term, once the shutdown ends and is in the rearview mirror, whether U.S. economic resilience survives the shutdown, and how high and for how long the Federal Reserve keeps its policy interest rate, will likely remain more consequential to the U.S. dollar's performance. In our view, with the Fed still leaning hawkish and a U.S. "soft landing" more possible, despite the short-term depreciation forces the dollar could experience, we would continue to forecast a stronger U.S. dollar through the end of 2023 as the broader economic environment proves to be the driving force of the greenback.

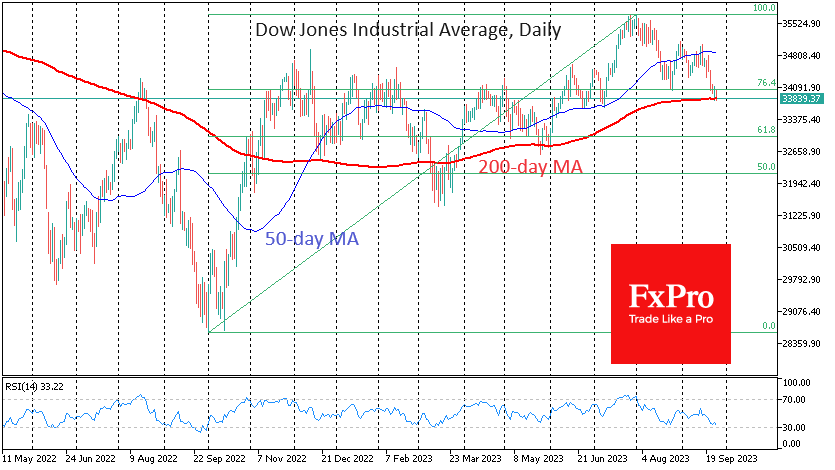

Dow Jones Index on Verge of Down-Trend

The Dow Jones Index is testing the long-term trend’s strength in the form of the 200-day moving average. The touching of this curve at the end of May and a brief dip below in March was characterised by increased buying. Are there enough buyers left in the markets to buy out the dive again? There are doubts.

The US Dow Jones has been trading below 34000 since the beginning of the week, back to the lows from early July, when we saw the last bullish attempt to warm up the market. Since August, the initiative has shifted to the bears, and they pretty quickly established a break of the medium-term trend in the form of the 50-day moving average.

Now, it is time to fight for the long-term trend in the form of the 200-day average. The German DAX40 and the pan-European Stoxx50 pulled back under those lines last week. Early last week, the Russell2000 – the broadest of the popular US indices – was also under this curve. And that only intensified the sell-off.

This week, the US Dow Jones – the oldest of the modern indices – is testing the strength of the 200-day moving average. Based on previous instances, a close under 33800 would open Pandora’s box, intensifying the sell-off.

In addition to breaking the uptrend, we will get confirmation that the market is on a deeper correction scenario, potentially heading for 33000 (61.8% of the October 2022 bottom to the July peak) after failing to cling to the 76.4% at 34000 (a shallower Fibonacci retracement).

We also note the change in the information backdrop. The pull away from risks, i.e. equities, is intensified by the disagreement on the budget, which could cause a US government shutdown. Fed officials are emphasising the chances of further interest rate hikes, while news media highlight the severity of current financial conditions for Americans.

This agenda reinforces the negative news backdrop, which could play into the hands of the bears in the short term, thus triggering a domino effect in another market benchmark.

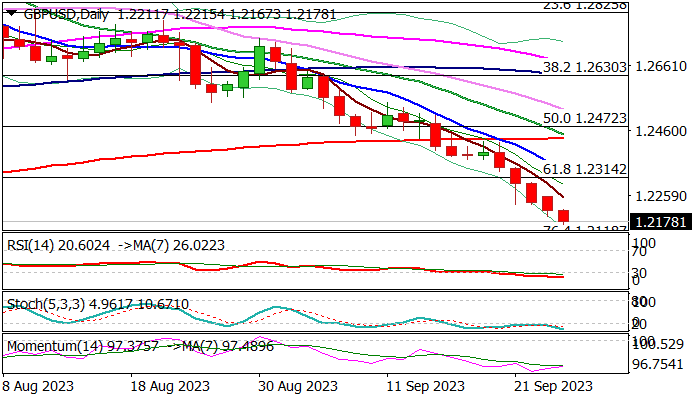

GBP/USD: Cable Falls Further, Psychological 1.20 Support Coming in Focus

Cable dips below 1.22 mark on Tuesday, hitting the levels last traded in mid-March, in extension of the downtrend which steepened in past five days.

Soured risk sentiment and strong dollar on signals that the Fed may raise interest rates further and keep them high for longer period, continues to weigh on sterling.

Bears eye target at 1.2118 (Fibo 76.4% of 1.1802/1.3141uplrg) and 1.2074 (Fibo 38.2% of larger 1.0348/1.3141 uptrend) which guard psychological 1.20 support.

Firmly bearish daily studies contribute to negative outlook, though strongly overbought conditions suggest that bears may soon start to run out of steam and some price adjustment. Upticks should be limited and ideally capped by broken Fibo 61.8% (1.2314) and nearby falling daily Tenkan-sen (1.2336) to keep bears intact.

Res: 1.2215; 1.2252; 1.2314; 1.2336

Sup: 1.2118; 1.2074; 1.2000; 1.1944

Brent Crude – Oil Pares Gains in Risk-Averse Trade

- Potential profit-taking after immense rally

- Economic pessimism may weigh in the future

- Bullish flag formation may suggest there's more to come

Risk aversion in markets may be weighing on oil prices a little, especially if economic fears are fueling that sentiment.

Oil prices have rallied strongly on the back of supply restrictions and the economy failing to live up to expectations was always going to be one of the primary counter-risks for the price.

I wouldn't say that is now unfolding but clearly, investors are a little concerned about whether the economy can sustain current levels of interest rates for a prolonged period of time.

From a technical perspective, I'm not seeing anything particularly concerning about the recent pullback. Brent crude still looks well supported, with today's initial declines being short-lived as the market rebounded around the highs from earlier this month.

We may still see more of a correction but there's no clear sign of sentiment turning bearish after such a strong rally over the summer.

A bullish continuation pattern?

The recent consolidation we've seen after such a strong rally looks a little like a bullish flag formation which may be a further sign that sentiment has not changed in the market over the last week.

Source – OANDA on Trading View

A break through the top of the descending channel could be a sign that the prior trend has resumed, especially if backed by momentum which will be key as we near some major psychological levels.

Euro Slips to 6.5-Month Low, Lagarde Dismisses Rate Cuts

- ECB’s Lagarde says rates to stay restrictive for as long as needed

The euro is unchanged on Tuesday, trading at 1.0593.

Euro slips despite Lagarde’s hawkish remarks

ECB President Lagarde said on Monday that interest rates would be “set at sufficiently restrictive levels for as long as necessary”, adding that the ECB was in a long race in the battle to bring down inflation to the 2% target. Lagarde stated categorically that the Governing Council was not considering rate cuts.

At first glance, Lagarde’s comments appeared hawkish. Investors were less than impressed, however, as the euro fell 0.48% on Monday. Last week, the ECB raised its key interest rate to a record high of 4.0%, but that too failed to support the euro, which lost ground after the decision. Lagarde signalled at the meeting and again in her remarks on Monday that rates may have peaked and investors responded on both occasions with a thumbs-down for the euro.

The ECB’s decision was a close call, with both doves and hawks able to present strong cases. Inflation is running at a 5.3% clip, more than double the target rate of 2%, and last week’s rate hike will help curb inflation. At the same time, eurozone growth has weakened and Germany, the traditional powerhouse, is a glaring weak spot. The global economy is weak and the slowdown in China isn’t helping matters.

Against this background of high inflation and sluggish growth, the ECB opted for a ‘dovish hike’, with the rate statement noting that rates have likely reached the peak level. The euro has reeled off 10 straight losing weeks, declining more than 600 basis points during that period. Unless eurozone data shows an improvement, the downswing could continue.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0594. Next, there is resistance at 1.0666

- There is support at 1.0544 and 1.0472

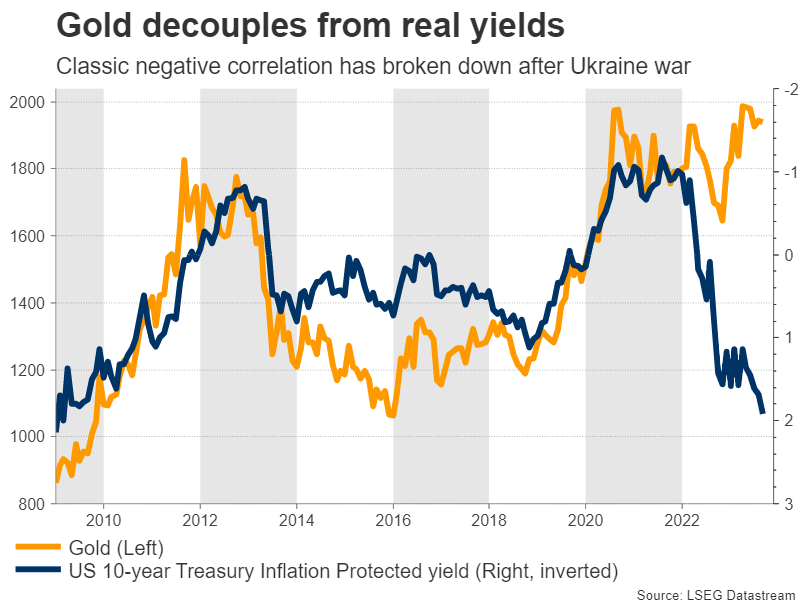

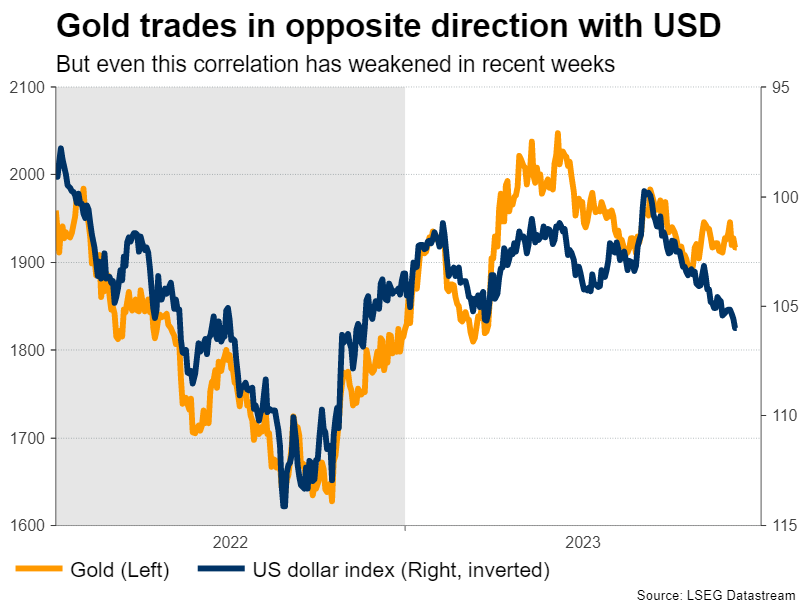

Gold Decouples from Interest Rates, What’s Next?

- Gold prices have remained stable lately, even as interest rates shot higher

- Central bank purchases have boosted demand, offsetting impact from rates

- Downside risks dominate for now, but longer-term outlook seems bright

Gold stable, despite 'bad news'

Gold continues to trade with impressive resilience. Even though conditions in financial markets have turned against the precious metal in recent months, gold prices have not absorbed much damage, defying the negative pressure exerted by soaring interest rates and an appreciating US dollar.

In normal times, gold and interest rates have a negative relationship. When rates rise and yields on government bonds race higher, gold becomes less attractive, as it pays no interest to hold. If investors can buy a US government bond that pays them a yield of 4.5% per year, like they can today, they are less likely to buy the non-yielding precious metal. That's what theory suggests, at least.

Similarly, a stronger US dollar is bad news for gold because the metal is mostly priced in US dollars. This means that when the dollar appreciates, it becomes more expensive for investors outside of the United States to buy gold, which inevitably dampens demand.

But these classic correlations have broken down lately. Yields on inflation-protected bonds went through the roof in September to reach their highest levels in almost 15 years and the dollar has staged a phenomenal recovery. Going purely by the historical relationships, this combination should have smashed gold down.

Yet, the yellow metal has remained relatively flat, and continues to trade 8% away from record highs. Therefore, some new element has come into play to change gold's trading dynamics.

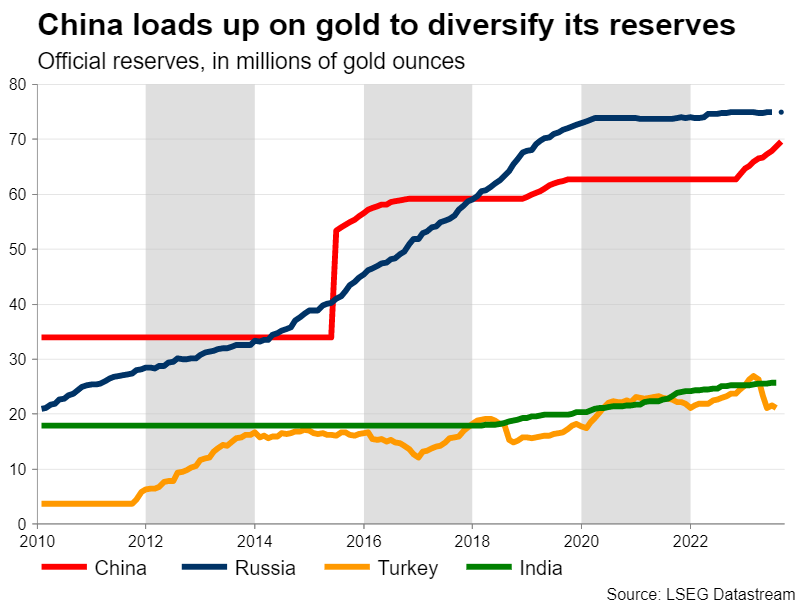

Central bank demand

This new element has been the direct buying of gold by central banks in an effort to raise their reserves. Central bank gold purchases reached a new record in the first half of this year, a pattern that likely persisted in the third quarter, spearheaded by China.

Geopolitics lie behind this boom in central bank demand. The invasion of Ukraine resulted in the immediate freezing of Russia's reserves held abroad in dollars and euros - around half of the assets held by the Bank of Russia were frozen under Americans and European sanctions. That was the beginning of a paradigm shift for how central banks manage their reserves.

The People's Bank of China started loading up on gold to diversify the nation's reserves away from dollars and euros, concerned about suffering the same fate in case diplomatic relations with the West turn colder in the future. This diversification strategy has seen China consistently buy gold for ten consecutive months through August, in what could be a multi-year trend.

Sovereign purchases have fueled underlying demand for gold, almost establishing a floor under prices. When there are such massive buyer whales active in the market, which are not sensitive to prices because their motives are mostly political, it helps to prevent any massive selloffs. Hence the resilience of gold prices in the face of sky-high rates.

The central bank buying spree has also suppressed volatility. Gold options contracts have seen their implied volatility fall to pre-pandemic levels over the summer, which essentially means investors are not hedging as much for any massive movements in gold, expecting the boost in demand to translate into smoother trading conditions moving forward.

New record highs possible, but not imminent

In the near term, downside risks for gold will probably continue to dominate. The negative forces of rising real yields and a roaring US dollar could continue to dampen the appeal of the precious metal, keeping a lid on any rallies.

It is difficult to say exactly how much further the rally in the dollar and yields can go. The US economy is superior to its competitors at this stage from a growth perspective, the Fed has shifted to a stance of higher-for-longer interest rates, and the Treasury will continue to flood the markets with newly issued debt next quarter, maintaining the upward pressure on yields.

Therefore, it seems premature to call for a trend reversal in gold. Most likely, these factors will keep the precious metal under selling interest in the coming weeks. That said, any losses could also be relatively limited considering the purchases from central banks, so gold prices might only bleed lower in a slow manner.

Looking at the charts, the most crucial regions to watch on the downside are $1,900, and beyond that the August low near $1,885. If that zone is violated too, the spotlight would turn to $1,860, a level marked by the inside swing high in March.

In the bigger picture, though, it seems quite plausible that gold can eventually rally to new records. If the highest bond yields in a generation could only knock gold 8% down from record highs, the precious metal can likely take out those highs once yields cool off again.

For that to happen, it might require some panic event in global markets or signs of an imminent US recession that fuel speculation of Fed rate cuts. That's not on the horizon for now, but the economic cycle does seem to be in its final stages, so it might simply be a matter of time.

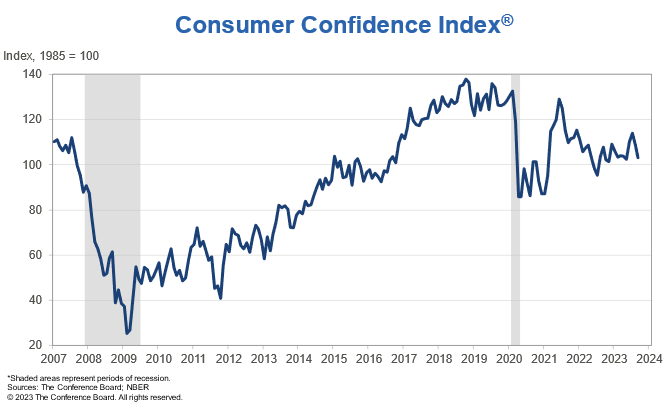

US consumer confidence fell to 103, expectations point to impending recession

US Conference Board Consumer Confidence for September took a hit, dropping from previous reading of 108.7 to 103.0, falling short of the anticipated 105.9. While Present Situation Index noted a modest rise from 146.7 to 147.1, Expectations Index saw a more significant drop, moving from 83.3 down to 73.7. Notably, this decline brought the Expectations Index beneath 80 mark, a level that has been traditionally viewed as early warning of an impending recession within the following year.

Dana Peterson, Chief Economist at The Conference Board, remarked, "Consumer confidence fell again in September 2023, marking two consecutive months of decline."

The main driver behind September's lackluster headline figure was identified as the dip in the Expectations Index, even as the Present Situation Index saw negligible changes.

Peterson further elaborated on the underlying sentiments, saying, "Write-in responses showed that consumers continued to be preoccupied with rising prices in general, and for groceries and gasoline in particular. Consumers also expressed concerns about the political situation and higher interest rates."

Sunset Market Commentary

Markets

It seemed at first that today was going to be a repeat of yesterday at the start of the European session, be it in less dramatic fashion. Both US and German yields eked out a few more basis points at first. But momentum dwindled after stock markets opened and in no time stacked losses of up to 1.3%. But unlike Monday, core bonds reversed course and began profiting from the risk aversion instead of causing it. Some end-of-quarter repositioning (closing post-Fed bond shorts) could be playing as well. US yields eased between 0.8-3.9 bps with the belly of the curve outperforming the wings. German rates shed 2.2-2.4 bps across the curve. We note that in both cases, yields cut losses in half after the US joined. Today’s main event on the economic calendar is still due after finishing this report with the US Conference Board consumer confidence for September. Several ECB speakers hit the wires but they were of little informative value. Lithuanian governing council member Simkus did repeat the need to discuss (ending) PEPP (reinvestments) “sooner rather than later”.

Dynamics on FX markets were similar to Monday too with a stronger dollar setting the tone initially before paring some gains later on. EUR/USD currently trades virtually unchanged at 1.0591 after having touched an intraday low of 1.057. DXY tentatively forfeits the 106 mark. USD/JPY also gives up earlier, be it minor gains to change hands around 148.89. Japan’s finance minister this morning stepped up verbal warnings, saying they are watching market moves with “high sense of urgency”. EUR/GBP for a third time straight attacked the 0.87 big figure but so far without a sustained break higher. The pair is filling bids in the high 0.86 area currently. Cable loses the 1.22 mark for the first time since March this year. The Hungarian forint in CE stands out against local peers, strengthening to EUR/HUF 388.17. The Hungarian central bank further reduced the O/N deposit tender rate by 100 bps to align it with the 13% base rate. The Monetary Council in this respect concluded the normalisation of the extraordinary interest rate environment. After today’s decision, the central bank’s set of monetary policy instruments will be changed and simplified. Even while implementing a technical simplification, the MNB indicated it is necessary to maintain tight monetary conditions in order to achieve price stability. Taking a cautious approach to changing the base rate is warranted in order to address fundamental inflation risks. With the acceleration of disinflation, the domestic real interest rate will move to positive territory in September and that process is expected gradually continue.

News & Views

According German IFO institute, expectations in the German export industry dropped considerable in September. The Ifo Export Expectations index fell to -11.3 points, down from -6.5 points in August. According to the head of Ifo surveys, Klaus Wholrabe Germany’s export economy is going through a weak phase as Exports to all key regions are currently in decline. At the present time, only manufacturers of leather goods and furniture, as well as a handful of food companies, are said to expect a rise in exports. All other sectors are predicting a drop in international business. The hopes for growth expressed last month in the chemical industry have evaporated. Automakers are now more skeptical as well. Printing companies are currently the most pessimistic. Ifo concludes that that export demand likely won’t pick up significantly until next year.

Inflation in Brazil in September reaccelerated at 0.35% M/M and 5% Y/Y up from 0.28% M/M and 4.24 Y/Y in August. The rebound in inflation was relatively broad-based as 6 out of nine subcategories showed higher monthly prices with transportation prices rising 2.02% M/M. The release of the September inflation data came on the same day the Central Bank of Brazil released the minutes of last week’s policy meeting when the Bank reduced its policy rate by 50 bps to 12.75%. According to the minutes board members saw it appropriate to continue the easing cycle at current gradual pace of 50 bps steps at current meeting. Only substantial positive surprises in the decline of long term inflation expectations or in the services price dynamics would allow for a faster pace of reductions. A survey of the central bank among market participants still saw inflation above the 3.0% target for 2024 and 2025 at respectively 3.86% and 3.5%. The real maintains recent most losses against the dollar with USD/BRL trading 4.97.