Sample Category Title

WTI Oil Technical: Continuation of Potential Impulsive Up Move Within a Major Uptrend

- The recent minor corrective pull-back of -4.7% from its 19 September 2023 high of US$93.05 is likely to have ended.

- Bullish reversal candlestick, a daily “Hammer” sighted after a retest on its upward-sloping 20-day moving average.

- Key short-term support to watch will be at US$90.30, the pull-back of the former minor “pennant” range resistance.

West Texas Oil (a proxy of WTI crude oil futures) has indeed shaped the bearish counter-trend pull-back movement of -4.7% from its 19 September 2023 minor swing high of US$93.05/barrel to a low of US$88.66/barrel printed yesterday, 26 September which fell short of the earlier highlighted short-term support zone of US$86.30/US$84.90 as per highlighted in our prior analysis.

Overall, the price actions of West Texas Oil are still evolving within a major uptrend phase which is still intact since its 4 May 2023 low of US$63.67 per barrel.

Key bullish reversal sighted after a retest on the 20-day moving average

Fig 1: West Texas Oil medium-term& major trends as of 27 Sep 2023 (Source: TradingView, click to enlarge chart)

Interestingly, there was a significant change in sentiment yesterday that led to the formation of a daily bullish reversal “Hammer” candlestick pattern right after a retest on the upward-sloping 20-day moving average that is acting as a support at around US$88.90/barrel.

These positive technical elements where price actions have staged an intraday reversal from yesterday, 26 September intraday low of US$88.66/barrel and closed near the upper end of its intraday range suggests a potential start of another medium-term impulsive up move sequence within its major uptrend phase.

Bullish breakout from minor “pennant” range configuration

Fig 2: West Texas Oil minor short-term trend as of 27 Sep 2023 (Source: TradingView, click to enlarge chart)

Yesterday’s price actions of West Texas Oil have also staged a bullish breakout from a 5-day minor “pennant” range configuration which indicates a potential continuation of its prior short-term bullish movement above the 20-day moving average.

Watch the US$90.30 key short-term pivotal support for a potential push up towards US$93.80 and a clearance above it sees the next intermediate resistance coming in at US$95.80.

On the other hand, failure to hold at the US$90.30 key support invalidates the minor bullish breakout scenario for another round of corrective pull-back to expose the next intermediate support zone of US$88.90/US$88.06.

A Fragile Risk Environment, Even If It’s Not Outright Risk-off, May Support the Greenback

Markets

Stock markets took center stage yesterday. The technical break in the EuroStoxx50 below the 4200 support zone on Monday got confirmed by another 0.9% drop on Tuesday. US indices didn’t escape reckoning this time. The Dow Jones (-1.14%), S&P (-1.47%) and Nasdaq (-1.57%) all tumbled below the neckline of a double top formation. This risk-off initially triggered some safe haven bids for core bonds. But yields at both sides of the Atlantic found a bottom in early afternoon before rebounding back towards their opening levels. The net daily changes of -0.4 bps (2-y) to +2.6 bps (20-y) in the US and -0.6 to +1bp in Germany thus hide bigger intraday moves. Disappointing US economic data (see below) weighed additionally. Peripheral spreads in Europe widened, with Italy a notable underperformer over the past few days/weeks. Bloomberg citing people familiar with the matter reported that Italy’s budget deficit for 2024 would amount to 4.5% instead of the 3.7% envisaged in April. It is also well above the EU’s 3% limit. This becomes the standard again in 2024 after a few years with a special (softer) deficit regime. PM Meloni’s government publishes an official update later today. The USD strengthened with the trade-weighted greenback edging further north of 106 to a new YtD high. EUR/USD’s poor attempt to retake 1.06 failed miserably and instead fell further to 1.0572. Another verbal warning from Japanese finance minister Suzuki didn’t convince the yen. USD/JPY eked out a gain to 149.07, slowly but steadily approaching the symbolic 150 barrier. The dollar holds the upper hand in Asian dealings this morning as well. We think it’s the path of least resistance, especially given there is little on the economic calendar (except the usually second tier durable goods data) that could change that in one way or another. A fragile risk environment, even if it’s not outright risk-off, may support the greenback as well. Next technical references in EUR/USD pop up at 1.0516, followed by the critical 1.0484 area. EUR/GBP is testing the 0.87 big figure for a fourth day straight now with spillovers from EUR/USD the only thing preventing a break higher for now. Yesterday’s intraday movement in core bonds suggest the sell-off eases. Core bond yields may now stabilize or even ease a bit going into tomorrow’s and Friday’s European/US inflation readings (CPI and PCE).

News and Views

US consumer confidence of the Conference Board and Richmond Fed manufacturing survey both gave somewhat of a similar message. Current activity shows ongoing signs of resilience but respondents are more cautious on the future. Headline consumer confidence eased to 103.1, but the August figure was upwardly revised from 106.1 to 108.7. Current conditions improved further from 146.7 from 147.1 while the expectations measure tumbled from 83.3 to 73.7. US consumers especially saw deteriorating business conditions, employment perspectives and income perspective over a six month horizon. Inflation expectations in 12 months were unchanged at 5.7%. The September Richmond manufacturing index improved from -7 to +5, with shipments, new orders, capacity utilization, wages and employment all showing higher readings in a monthly perspective. The prices paid indicator also again rose from 3.17% to 4.06%. Prices received eased marginally to 3.06%. However, the assessment for business six months for now was less optimistic with especially indices for shipments (12 from 22) and new orders (17 from 22) easing. Labour market forward looking indices remained solid. Expectations for price trends are expected to cool down.

Monthly CPI from the Australian Bureau of statistics reaccelerated to 5.2% Y/Y in August from 4.9% in July. The rises came after three consecutive declines and compare to a cycle top of 8.4% Y/Y in December last year. The indicator excluding volatile items (fruit and vegetables, auto fuel and holiday travel) still declined from 5.8% to 5.5%. Trimmed mean underlying inflation was unchanged at 5.6% Y/Y. The most significant price rises were housing (+6.6%), transport (+7.4%), food and non-alcoholic beverages (+4.4%) and insurance and financial services (+8.8%). Electricity prices rose 12.7% Y/Y, reflecting higher wholesale prices being passed on to customers. The rise even was tempered by the introduction of rebates from the Energy Bill relief Fund. Automotive full prices rose 13.9% Y/Y due to a 9.1%M/M rise in August. Both headline and core measures remain well above the 2-3% RBA target, keeping the debate on further tightening alive. The impact of the data on markets was limited. The 2-y Australian yield eased about 2.5 bps. Markets still see change of about 70% for a rate hike in Q1 next year. The Aussie dollar remains under pressure from a strong US dollar with AUD/USD trading near 0.6385.

Stocks Down, USD Up

Investors continue to dump stocks and buy US dollars on looming uncertainty regarding whether the US government will be shut in three days. There is progress regarding a 6-week short-term funding deal, but getting an approval from the Senate will be a challenge. In the meantime, falling savings, rising theft and delinquencies hint at the growing cost-of-living crisis whereas the central banks’ inflation fight is certainly not over just yet.

The looming government shutdown talks continue feeding into a stronger US dollar. US politicians have agreed to a 6-week short-term funding to keep the government running for another month and a half, but getting approval from the full Senate will be a challenge with far-right Republicans’ determination to ‘shoot it down if it reaches the floor’.

The S&P 500 fell to the lowest levels since the beginning of June and the Stoxx 600 could slip below 445 due to slowing European activity, waning Chinese demand, the European Central Bank’s (ECB) pledge to keep the monetary policy tight until inflation comes down significantly. The euro’s depreciation makes inflation harder to ease along with rising energy prices.

After a few sessions of consolidation, and despite a more than 1.5-mio-barrel build in US crude inventories last week, US crude is upbeat this morning, again. The barrel of American crude is trading above the $92 level, as the European nat gas futures flirt with the 200-DMA. The EURUSD lost around 6.5% since the July peak. Oversold market conditions call for consolidation, or recovery, yet appetite in the US dollar remains too strong to let the other currencies breathe. And if this is not enough bad news, the EU is now investigating the degree to which China has subsidized EV manufacturers. Tesla is clearly in a hot seat, but not only. Some European carmakers including Renault and BMW also have joint ventures in China and will be probed. The cherry on top, VW announced to cut EV output at German sites due to lacking demand. All this to say, there is little place to go in the market other than the FTSE 100, which could at least take advantage of the energy rally.

The combination of higher energy and stronger dollar has well pushed inflation in Australia to 5.2% in August, up from 4.9% printed a month earlier -which was a 17-month low. We could see a similar upturn in global inflation metrics due to rising oil prices. The Eurozone data will soon be coming in. Unfortunately for the Aussie, the uptick in inflation won’t prevent it from getting smashed against the US dollar. The pair will likely test and take out the September support of 0.6360.

Dollar Rally

Market movers today

Today focus will be on US durable goods orders and euro area M3 money supply growth. Consensus expects that durable goods orders fell 0.5% m/m in august and that euro area M3 money growth will dive further into negative territory. While much of the decline in the money supply is due to base effects from quantitative tightening (QT), we have also seen a continued weakening in credit to the private sector. This should naturally be seen in light of the tightening monetary policy stance.

In Sweden, we receive a string of data points including trade balance figures, NIER confidence survey, and household lending growth.

The 60 second overview

ECB: Governing council member Robert Holzmann yesterday said that he thought it was unclear whether the policy rate had peaked due to persistence in inflation, i.e. raising the possibility that the ECB may have to hike further.

Japan: Minutes from the July Bank of Japan meeting revealed that most members did not think achievement of inflation goal was in sight, while one member thought it might be possible to assess whether the target was hit in Q1 next year.

Gold: The gold price has held up relatively well amid rising bond yields and rebound in the USD. However, this week it has started to give in and yesterday it fell to the lowest level in over a month.

Equities: Equities were lower for another session, thereby reversing some of Monday's modest gains. S&P 500 dropped a full -1.5% and Stoxx 600 -0.6%. Nasdaq is now only a percentage point away from a full correction the last month. Yields continued to govern the direction of equities. As such, yield sensitive groups of stocks underperformed, like utilities and tech (Vestas, Evolution, Orsted). Unlike Monday, this was a risk off session. VIX rose and is now inches away from the important 20-level. Defensives outperformed cyclicals, with energy, consumer staples and health care holding up (Novo Nordisk, Genmab and Sampo in the Nordics). Pulp names also against the stream, with SCA and Stora Enso up about 1%. US futures are turning around this morning though and Asian markets are mixed.

FI: Yields to stay higher and potential advancement of the PEPP reinvestments sparked another "higher yield and wider spreads"-reaction. Fed's Kashkari said that rates could probably go higher while ECB's Holzmann said that they hopefully can discuss PEPP soon. Holzmann added that he would not favour outright APP sales. That combined the German finance agency revised Q4 issuance plans lower led to an outperformance of core yields. Reports of potential Italian budget deficits above 4% (initial 3.7%) weighed heavily on the BTPs, where 10y BTPs-Bund spread widening 7bp to 192bp which is the widest since March. Today the TLTROs repayment settles, with EUR101bn repaid. This will reduce the excess liquidity by roughly the similar amount.

FX: Another strong day for the USD, with USD/JPY challenging new highs and EUR/USD moving further below 1.06. Thus far into the week however, SEK outperforms rest of G10 (inc. USD) and USD/SEK broke below 11.00 yesterday, despite another sour day for risk. Neighbouring NOK does not follow suit however, and instead EUR/NOK continues to trade within the 11.40-50 interval.

Credit: Credit markets took a sharp leg wider yesterday where iTraxx Xover widened almost 12bp and Main almost 3bp. The cautious tone was also visible in the primary market where activity was subdued.

Nordic macro

In Sweden various statistics drop today. Trade balance figures is first out (CET 8:00). It has been suggested to be one of the major contributors for the eventual decline in Swedish growth. However, as the July numbers bounced back upwards it is of interest if the statistic will further strengthen the improving trend. We also get household lending growth figures which may be bottoming out which we hope these numbers will signal.

Then we have the NIER confidence survey (CET 9:00). It includes price plans for the retail and service sector which are still above levels that are not in accordance with the inflation target. Furthermore, it also includes labour market indicators which is of relevance to see if the increase in the unemployment rate in August were indicative or only a deviation.

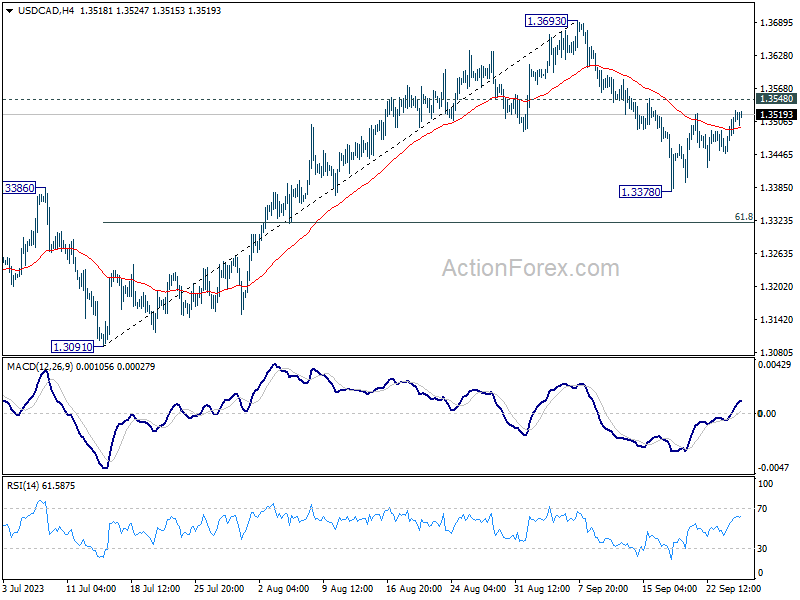

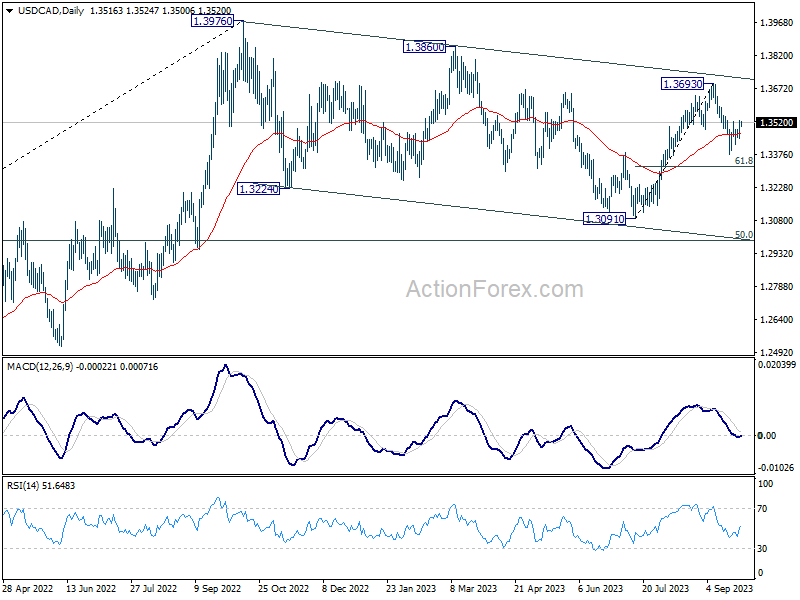

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3442; (P) 1.3467; (R1) 1.3480; More....

Intraday bias in USD/CAD remains neutral for the moment. Break of 1.3378 will resume the fall from 1.3693, as another leg in the corrective pattern from 1.3976 high, to 61.8% retracement of 1.3091 to 1.3693 at 1.3321. However, firm break of 1.3548 will turn bias back to the upside for retesting 1.3693 instead.

In the bigger picture, price actions from 1.3976 are viewed as a corrective pattern to the up trend from 1.2005 (2021 low). Deeper decline could be seen as the pattern is now extending. But downside should be contained by 50% retracement of 1.2005 to 1.3796 at 1.2991. Rise from 1.2005 is still expected to resume after the correction completes.

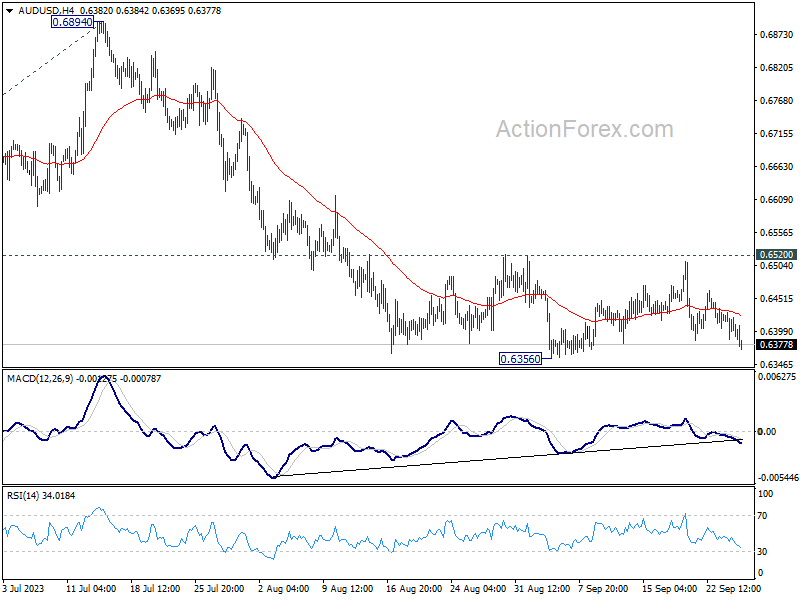

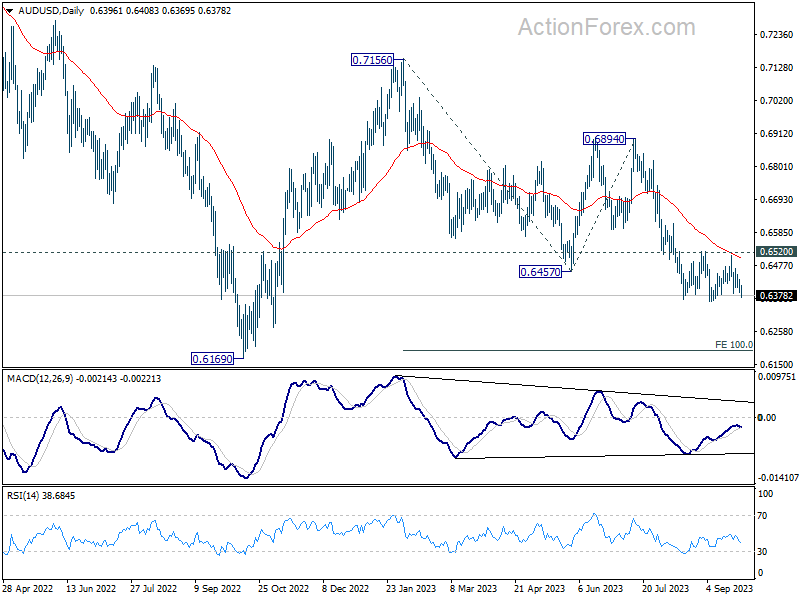

AUD/USD Daily Report

Daily Pivots: (S1) 0.6380; (P) 0.6405; (R1) 0.6423; More...

Range trading continues in AUD/USD and intraday bias stays neutral. Further decline is expected as long as 0.6520 resistance holds. Break of 0.6356 will resume larger down trend to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

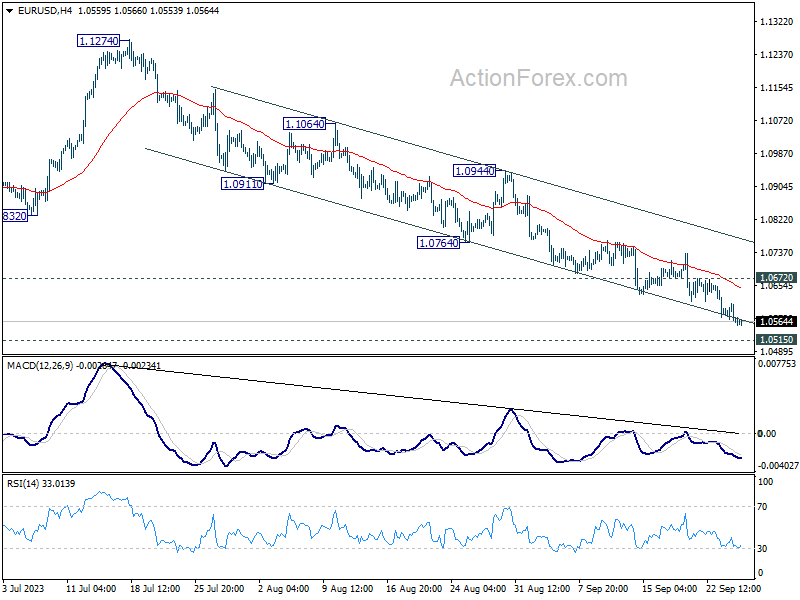

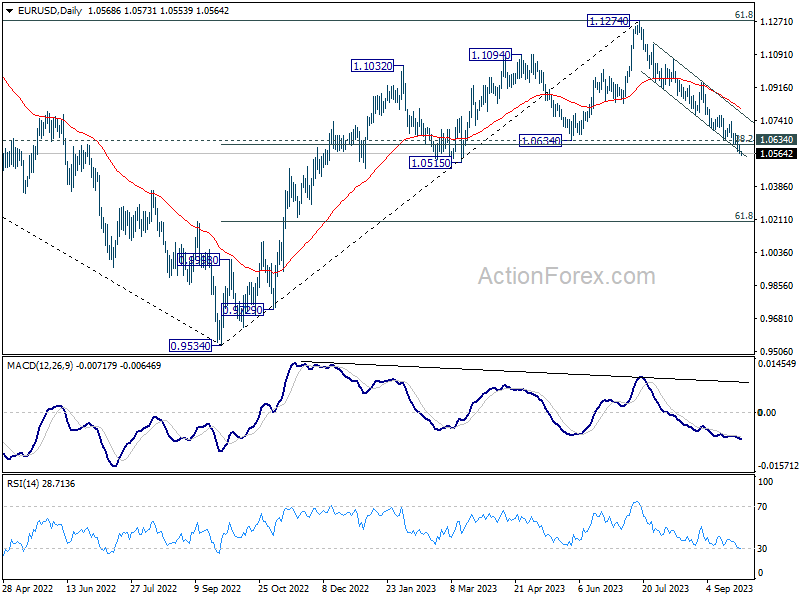

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0553; (P) 1.0581; (R1) 1.0600; More...

EUR/USD's fall from 1.1274 is still in progress and intraday bias remains on the downside. Next target is 1.0515 support. On the upside, above 1.0672 minor resistance will turn intraday bias neutral and bring consolidations. But outlook will stay bearish as long as 1.0764 support turned resistance holds.

In the bigger picture, focus stays on 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Sustained trading below there would rase the chance of bearish trend reversal. That is, fall from 1.1274 could be reversing whole rise from 0.9534 (2022 low). But even if it's just a corrective move, deeper decline would be seen to 61.8% retracement at 1.0199. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0825) holds, in case of rebound.

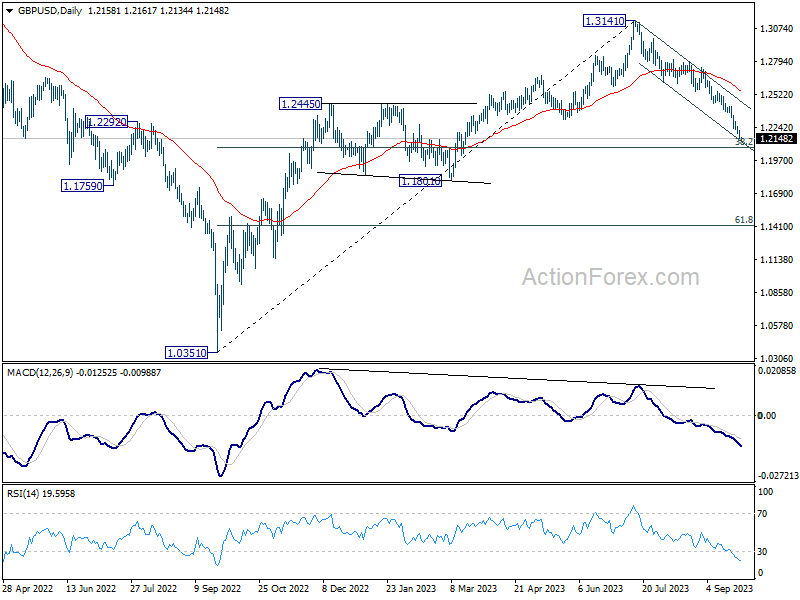

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2134; (P) 1.2175; (R1) 1.2198; More...

Intraday bias in GBP/USD remains on the downside as fall from 1.3141 is extending. Next target is 1.2075 fibonacci level. On the upside, above 1.2306 minor resistance will turn intraday bias neutral and bring consolidations. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal and target 1.1801 structural support next.

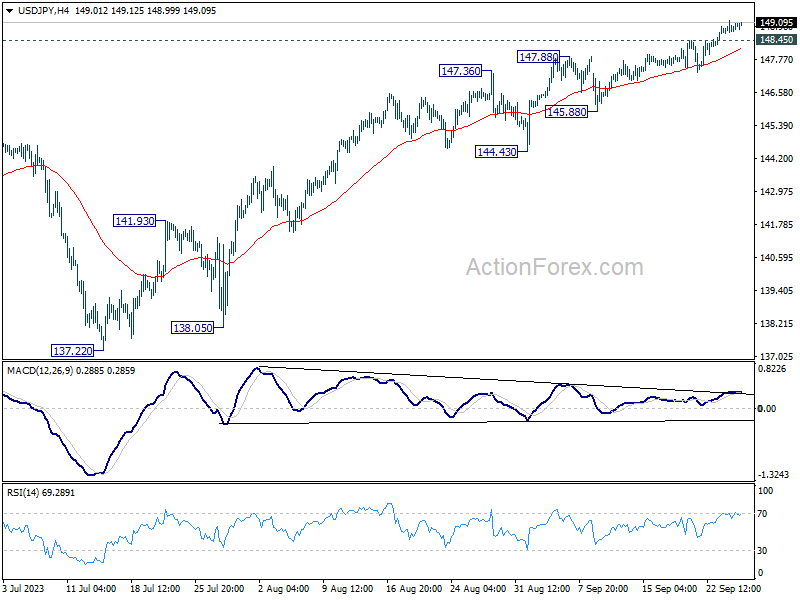

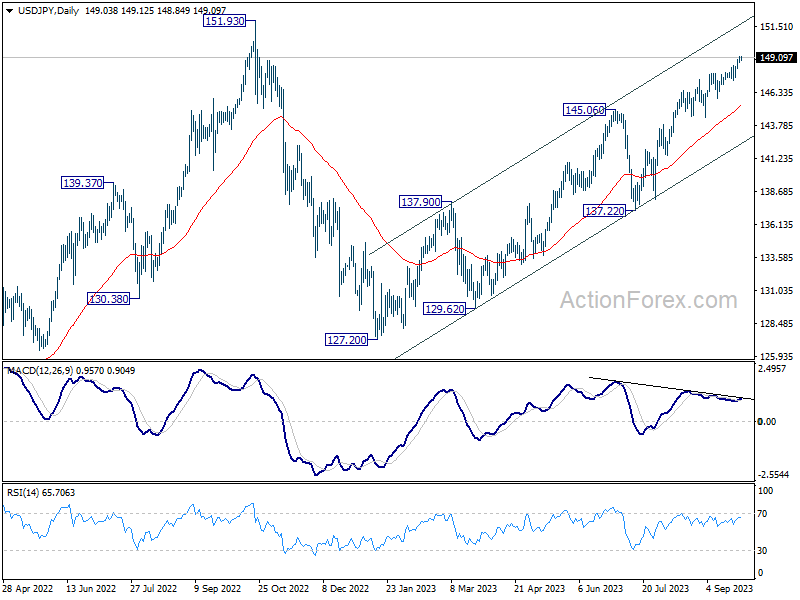

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.79; (P) 148.99; (R1) 149.27; More...

USD/JPY's rally is still in progress and intraday bias remains on the upside. Current rise from 127.20 should target to retest 151.93 high. On the downside, below 148.45 minor support will turn intraday bias neutral first. But outlook will now stay bullish as long as 145.88 support holds, in case of retreat.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

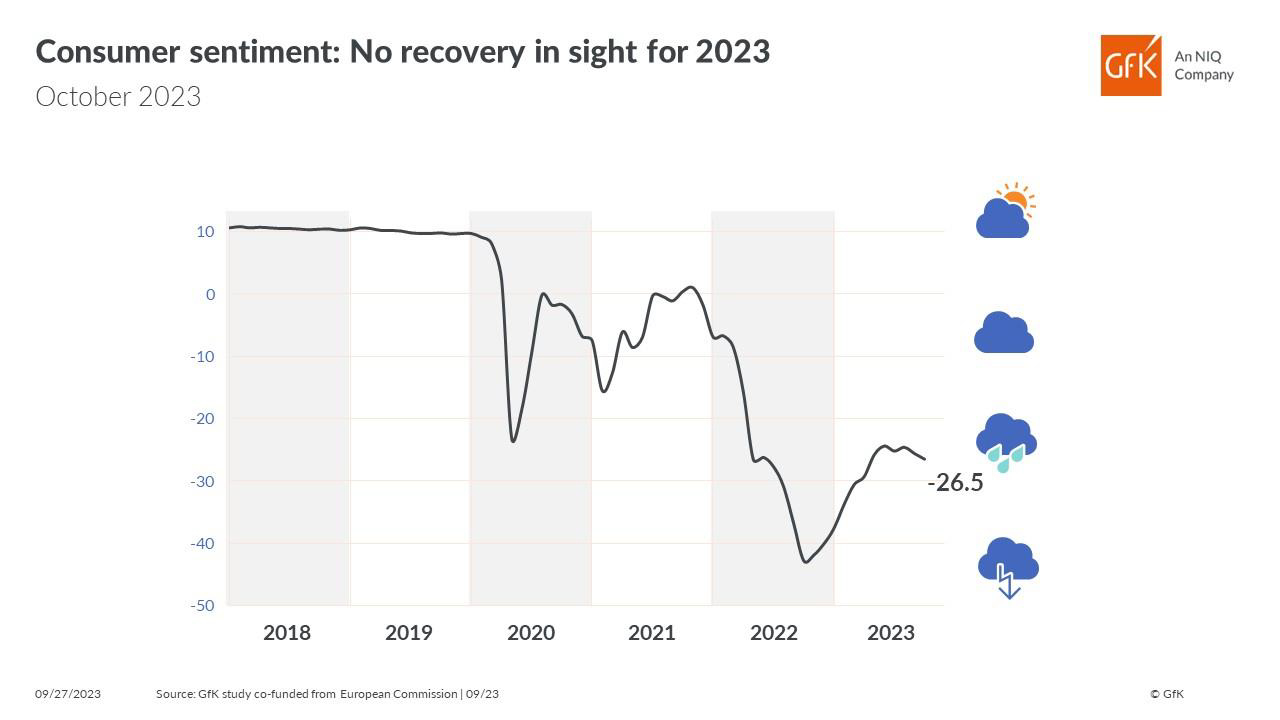

German Gfk consumer sentiment fell to -26.5, chance of recovery probably fallen to zero

Germany's Gfk Consumer Sentiment for October fell from -25.6 to -26.5. In September, economic expectations rose from -6.2 to -3.4. Income expectations ticked up from -11.5 to -11.3. Propensity to buy rose slightly from -17.0 to -16.4. Propensity to save jumped from 0.5 to 8.0, highest since April 2011.

"This means that the chances of a recovery in consumer sentiment this year have probably fallen to zero," explains Rolf Bürkl, GfK consumer expert. "The reasons for this are a persistently high inflation rate due to sharply rising food and energy prices. Consequently, private consumption will not be able to positively contribute to overall economic development this year."