Sample Category Title

Australian retail sales see modest 0.2% mom rise amid cost-of-living pressures

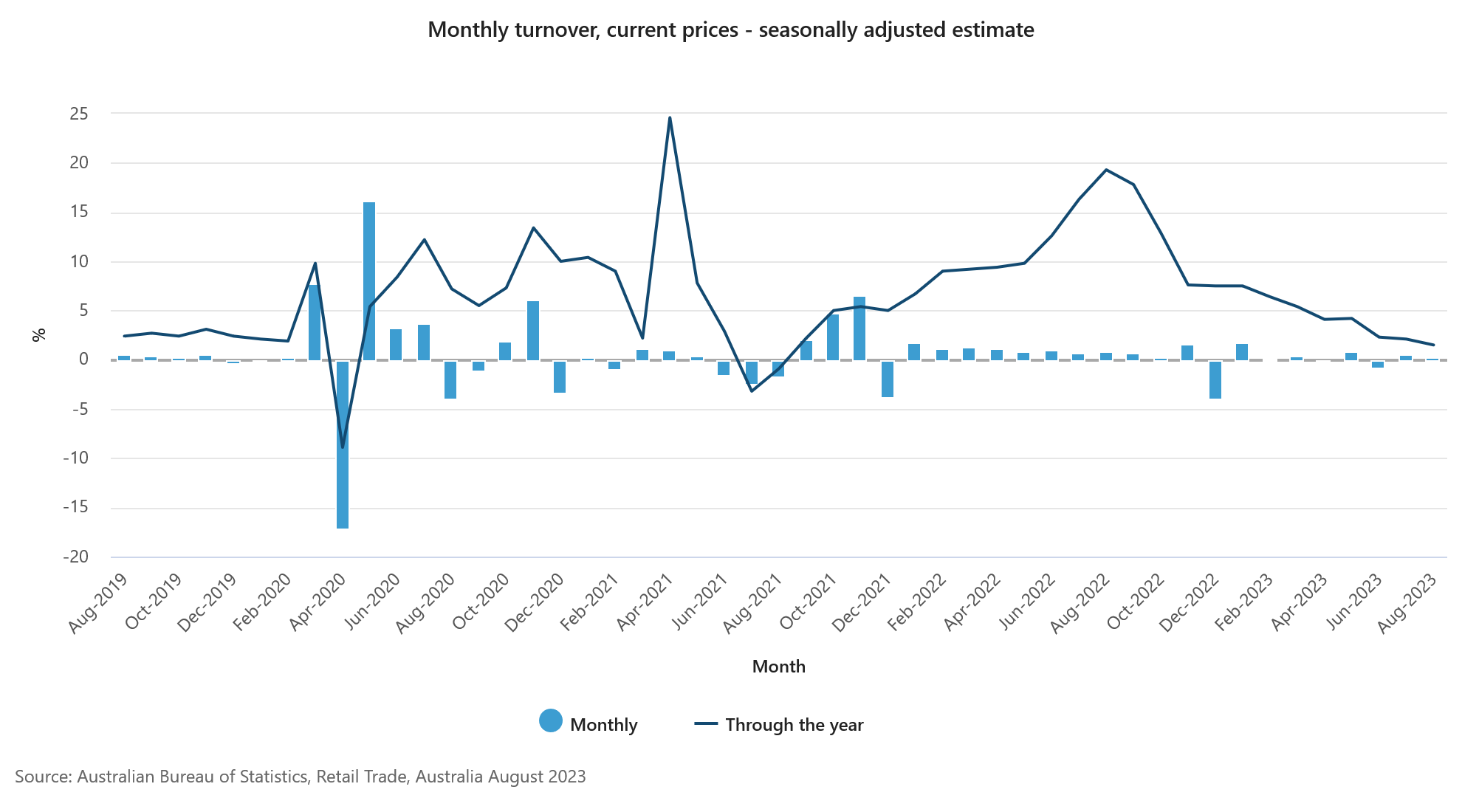

The latest retail statistics out of Australia show a muted picture of consumer spending, with retail sales turnover in August rising only 0.2% mom (in seasonally adjusted terms) to AUD 35.4B, falling short of the anticipated 0.3% increase. Through the year, sales turnover was up 1.5% yoy.

According to Ben Dorber, the head of retail statistics at the Australian Bureau of Statistics (ABS), this modest rise indicates a notable restraint in consumer spending. Dorber noted, "The modest rise in August shows consumers continued to restrain their retail spending."

The trend growth in retail sales paints an even starker image. "In trend terms, retail turnover rose 0.1 per cent, and was up only 1.3 per cent compared to August 2022 - the smallest trend growth over 12 months in the history of the series," Dorber added.

Dorber highlighted, "Considering how high inflation and strong population growth have added to retail turnover in the past year, the historically low trend growth highlights just how much consumers have pulled back in response to cost-of-living pressures."

Mixed signals in New Zealand business confidence, ANZ anticipates another RBNZ hike

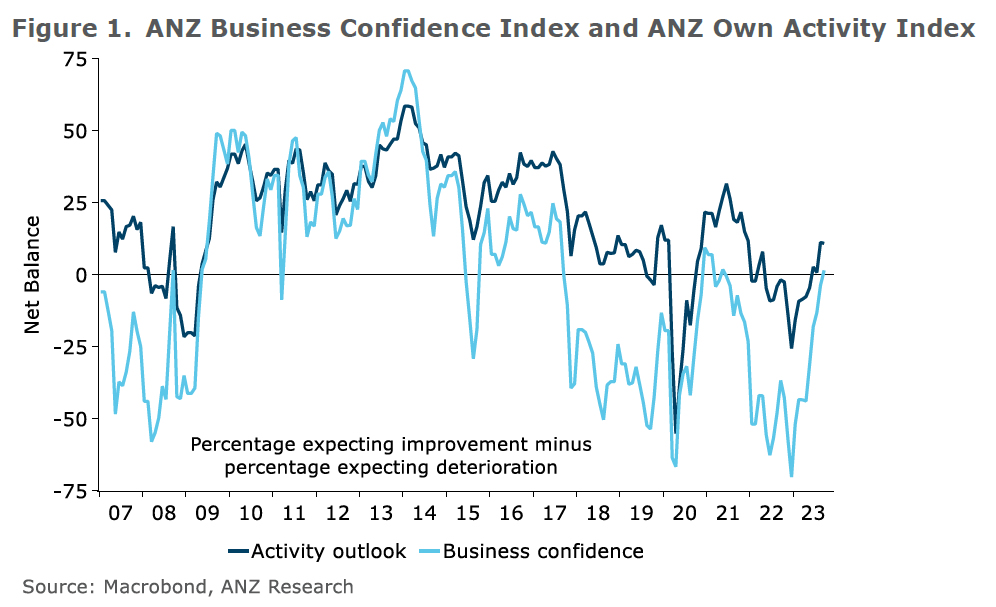

September has seen a noteworthy rebound in New Zealand's ANZ Business Confidence, rising from -3.7 to 1.5. However, a closer examination of the details offers a more nuanced picture.

Metrics such as own activity output experienced a slight decline, dropping from 11.2 to 10.9. More alarmingly, export intentions plummeted from a positive 7.5 to a -0.4. There were also declines in investment intentions (from -1.3 to -4.1) and employment intentions (from 4.6 to 1.2).

On the inflation front, cost expectations edged upwards from 75.3 to 78.6, while profit expectations showed an improvement, moving from -17.6 to -13.2. Pricing intentions rose from 44.0 to 47.1, but inflation expectations took a downward turn, shifting from 5.06 to 4.95.

ANZ provided their insights on this mixed bag of indicators, stating, "The New Zealand economy is certainly patchy, and the rebound in activity indicators – that's been evident since the start of the year – may be running out of steam."

They further highlighted the complexities in the inflation scenario: "Inflation pressures are gradually waning in the big picture, but not rapidly nor in a straight line, and the jury remains out on whether it's occurring fast enough to bring core inflation pressures down in a timely fashion."

Looking ahead, ANZ anticipates further action from RBNZ to ensure inflation is reined in effectively, with a 25 bps hike expected in November.

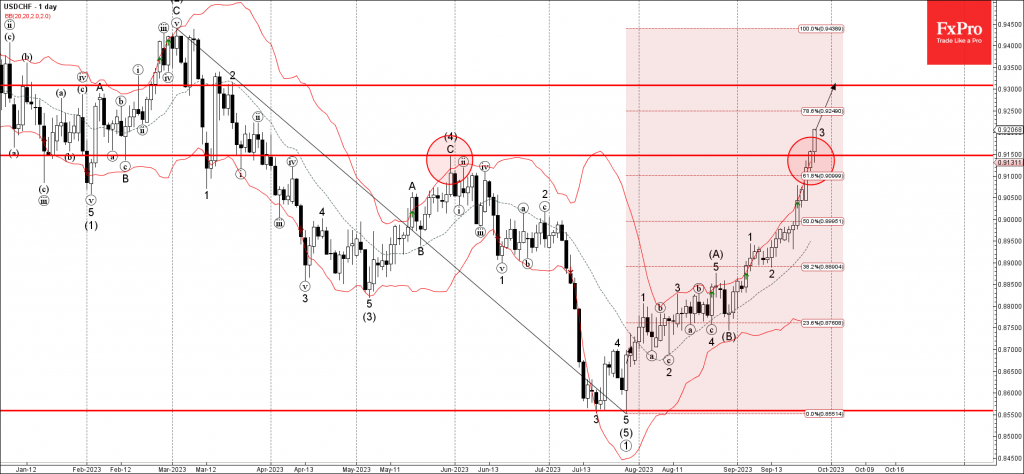

USDCHF Wave Analysis

- USDCHF broke resistance level 0.9150

- Likely to rise to resistance level 0.9300

USDCHF currency pair recently broke above the strong resistance level 0.9150 (former multi-month high from May) standing near the 61.8% Fibonacci correction of the previous upward impulse from March.

The breakout of the resistance level 0.9150 was accelerated the active impulse wave 3 of the intermediate impulse wave (C) from the end of August.

USDCHF currency pair can be expected to rise further toward the next resistance level 0.9300 (former top of wave 2 from the middle of March).

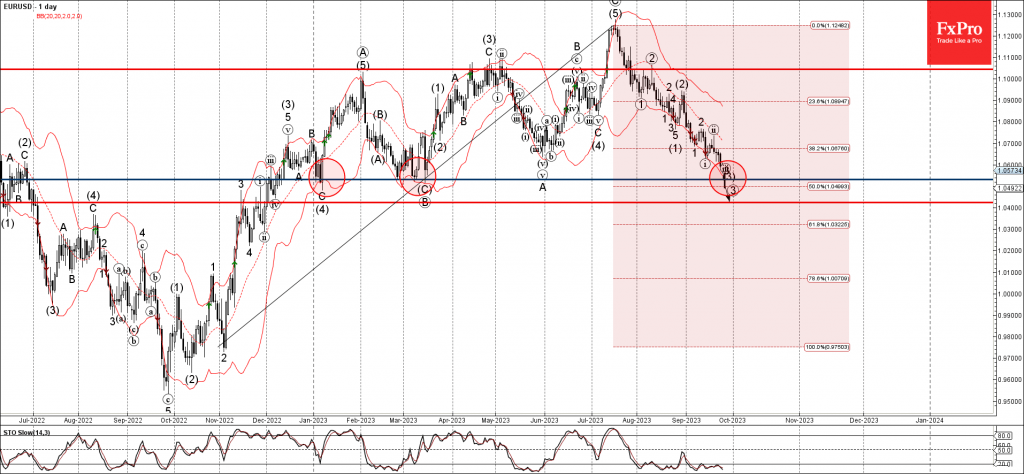

EURUSD Wave Analysis

- EURUSD broke key support level 1.0530

- Likely to fall to support level 1.0420

EURUSD currency pair recently broke key support level 1.0530 (which has been reversing the price from January) intersecting with the 50% Fibonacci correction of the previous upward impulse from November.

The breakout of the support level 1.0530 was accelerated the active impulse waves iii and 3.

Given the strongly bullish USD sentiment, EURUSD currency pair can be expected to fall further toward the next support level 1.0420.

New Zealand Dollar Edges Lower, Business Confidence Next

- New Zealand Business Confidence expected to rebound

The New Zealand dollar is slightly lower on Wednesday. NZD/USD is trading at 0.5937 in the North American session, down 0.13%.

The US dollar has been on a tear against the major currencies. Everything seems to be clicking for the greenback – the US dollar index is at a 10-month high, while 10-year US Treasury yields have hit their highest level since 2oo7.

The US economy remains strong despite high interest rates. The Federal Reserve held rates last week, but the pause was hawkish as the Fed warned the markets to expect a ‘higher for longer’ rate path as it battles to lower inflation to the Fed’s 2% target.

The New Zealand dollar has held its own against the US dollar in September, although NZD/USD was pummelled in August when it plunged 3.9%. That downturn can be attributed to a large extent to the deterioration in China’s economy, as the Asian giant is New Zealand’s largest trading partner.

Major central banks are looking to wind up their aggressive tightening cycles and the Reserve Bank of New Zealand is no exception. The New Zealand economy is getting squeezed by weak domestic consumption and reduced global demand for exports. The central bank has projected a recession and an end to tightening would make sense if it weren’t for inflation running at a 6% clip in the second quarter, double the upper band of the 1-3% target range for inflation. Unless inflation falls quickly, there’s a strong chance that the RBNZ is not yet done with rate increases.

We’ll get a look at New Zealand’s ANZ Business Confidence on Thursday. The index improved to -3.7 in August and is expected to push into positive territory in September, with a market consensus of 5.0.

The US releases third-estimate GDP for August on Thursday, with a market consensus of 2.0%. This would mark a downward revision from the second estimate of 2.1% and the preliminary estimate of 2.4%. The US economy continues to post respectable growth figures despite the Federal Reserve’s sharp tightening, as the labour market has remained strong and consumers continue to spend.

NZD/USD Technical

- NZD/USD tested resistance at 0.5948 earlier. The next resistance line is 0.6002

- There is support at 0.5908 and 0.5854

Sunset Market Commentary

Markets

The recent breathtaking rally in yields took a breather today. Investors adapting to central bankers’ ‘higher for (much) longer’ guidance via higher real yields hammered core bonds especially at longer tenors. Yields reached levels not seen since 2011 (Germany) or even 2007 (US 5 & 10-y). The US 10-y real yield settling well north of 2% also forced investors to a revaluate almost all assets, pushing US and EMU equity indices significantly below key support levels. The rise in real yields was the driver for other (FX and markets of riskier) assets and this process probably has further to go. However, sharp equity losses at some point might cause some investors to re-enter the market of (previously presumed) ‘safe haven’ bonds at a discount. At least today, bond markets found some short-term equilibrium with US yields easing 0.5 bps (5-y) to 3.0 bps (30-y). The 5.0 bps decline in the 2-y US yield was due to a benchmark change. US durable goods orders’ report (orders +0.2% vs -0.5% expected, shipments of capital goods non-defense ex aircraft +0.7%) was above consensus, but wasn’t able to revive the established trends. The German curve shows similar to the US (-2y -1.5 bp, 30-y -3.0 bps). 10-y intra-EMU spreads versus Germany also ‘stabilized’. The Italian spread ‘eased’ 2bps after a cumulative widening of about 20 bps over the previous week as markets await a (negative) government update on the 2023 and 2024 budget.

The limited easing on bond markets hardly supports equities for now (EuroStoxx 50 + 0.3%, S&P +0.35%). At the same time, Brent oil revisits recent peak levels (Brent $95.5 p/b) reinforcing a stagflationary mindset. Inflation data published tomorrow (Germany, Spain), and on Friday (EMU, US PCE deflators) will provide the next ‘hard’ reality check on recent markets’ trends.

On FX markets, softer yields and some calm returning to the equity markets hardly slowed the USD-uptrend. The DXY trade-weighted index gains further, admittedly at a more modest pace (106.35). USD/JPY touched a minor ST top at 149.25. EUR/USD at 1.0520 nears to 1.0516/1.0484 key support area. EUR/GBP (0.8683) for the fourth consecutive session tested the 0.87 range top. However, some UK specific news apparently is needed to force the break, especially with the euro also fighting an uphill battle.

News & Views

The KOF Swiss Economic Institute released its Autumn forecast today. This year’s growth forecast remains virtually unchanged at 0.8% (from 0.9% in June). Next year’s GDP prognosis was downwardly revised from 2.1% to 1.9% mainly because of the weaker performance of Switzerland’s trade balance (lower growth in goods exports). In a first forecast, 2025 growth is put at 1.6%. The KOF institute still projects Swiss inflation at 2.2% this year, but upped its call for next year from 1.5% to 2.1% before returning to 1.1% in 2025. The upward revision is due to a sharp rise in electricity prices at the beginning of the year and further rent increases. Inflation imported from abroad will play hardly any role at all. The Swiss National Bank is expected to keep its policy rate unchanged at 1.75% for some time with rate cuts only being implemented at the end of the forecasting horizon. The central bank will likely intervene by selling currency to ensure a strong CHF and further reduce imported inflation. KOF still expects the nominal effective exchange rate to appreciate. The Swiss franc corrected last week after the SNB kept its policy rate unchanged. It tries to take out the 0.97 big figure for the first time since early July (from low 0.95-area ahead of SNB). First resistance stands at 0.9738 (38% retracement on YTD decline).

The Czech National Bank unanimously decided to keep its policy rate unchanged at 7% today. The press conference with CNB governor Michl just started. He believes that inflation is still at unacceptably high levels, adding that the central bank board sees the future interest rate path above its July baseline in coming quarters. Czech rates increase at the front end of the curve as these early comments seem to suggest that the CNB is pushing back against November rate cut bets. EUR/CZK drops from 24.50 to 24.40.

Markets Fat as the Dust Settles on a Massive Week of Central Bank Meetings

Equity markets are pretty flat in the middle of the week, struggling to pick themselves up off the floor as investors worry about higher for longer interest rates and the economy.

Last week was action-packed and it seems investors are still piecing it all together in the absence of much else happening. While I often refer to them as eternal optimists, when faced with the prospect of recession in Europe, a sluggish recovery in China, and a Fed that's seemingly determined to push the economy to the edge despite huge progress already without much pain, it would appear investors are struggling to see the upside.

The only thing that can change that is the economic data providing further evidence that significant progress is continuing to be made. But if the government shuts down, we won't be getting that any time soon which would make the October Fed meeting interesting, depending on how long it lasts. There are potentially uncertain times ahead and as the old adage goes, markets hate uncertainty.

Oil on the rise again after taking a small breather

After a week of consolidation, oil prices are on the rise again on Wednesday ahead of the release of inventory data from EIA. The API release yesterday may have surprised some, recording an increase of 1.586 million barrels, a lot more than the 0.7 million decline that's expected today.

But it won't alter the view that the market is extremely tight following a number of supply cuts from OPEC+ countries. I think what we've seen over the last week or so is a little profit-taking and the fact it's already on the march higher is potentially a sign of how bullish traders still are.

Hawkish Fed pushes Gold back below $1,900

Gold continues to drift lower after breaking below $1,900, a key area of support in recent weeks. The yellow metal had been range-bound between $1,900 and $1,950 around the major central bank meetings this month and it would appear a hawkish Fed when others have adopted a more neutral tone has pushed it over the edge.

The dollar has been charging higher over the last week and weighed heavily on gold, which may now be eyeing last month's lows around $1,885 for support. It's not looking good for the yellow metal though, with the insistence that rates in the US could rise again and stay there for longer far from ideal.

EUR/USD Extends Losses, Eyes German Inflation

- German consumer confidence decelerates

- German inflation expected to fall to 4.6%

The euro has extended its losses on Wednesday and has declined close to 1% this week. In the European session, EUR/USD is trading at 1.0552, down 0.18%.

Germany has traditionally been the powerhouse of Europe but finds itself lagging in the rear, with a struggling economy and high inflation. The GfK Consumer Climate index fell to -26.5 for October, down from a revised -25.6 in September and shy of the market consensus of -26.0. This was the lowest reading since April and suggests that consumer sentiment will remain weak in the near future. The GfK report warned that private consumption will not contribute towards Germany’s recovery, which is grim news for the eurozone.

Eyes on German inflation, retail sales

One of most eagerly waited eurozone releases is the German inflation report, which will be released on Thursday. The consensus estimate for German CPI stands at 4.6% y/y, compared to 6.4% y/y in August. If the estimate is on track, it would mark a significant win for the ECB, which has been raising rates aggressively in order to curb high inflation.

The ECB raised rates last week, but the lead-up to the meeting was dramatic as it was a 50-50 call whether the ECB would hike or hold. A sharp drop in German inflation could send the euro lower as it would support the ECB taking a pause at the October meeting.

The week wraps up with German retail sales on Friday. After back-to-back declines, retail sales for August are expected to rebound to 0.5% m/m.

The US releases third-estimate GDP on Thursday, with a market consensus of 2.0%. This follows the second-estimate of 2.1% and the preliminary estimate of 2.4%. The US economy has recorded respectable growth figures despite the Federal Reserve’s sharp tightening, as the labour market has remained strong and consumers continue to spend.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0594. Next, there is resistance at 1.0666

- There is support at 1.0544 and 1.0472

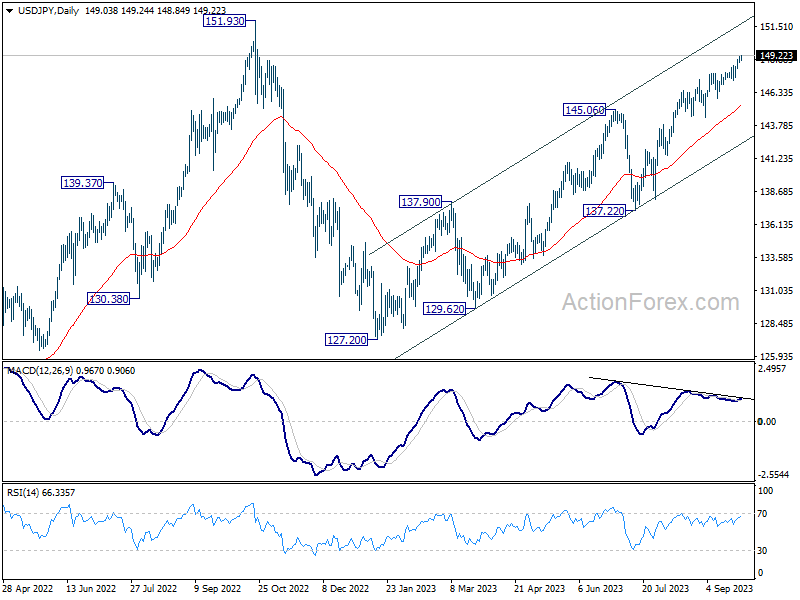

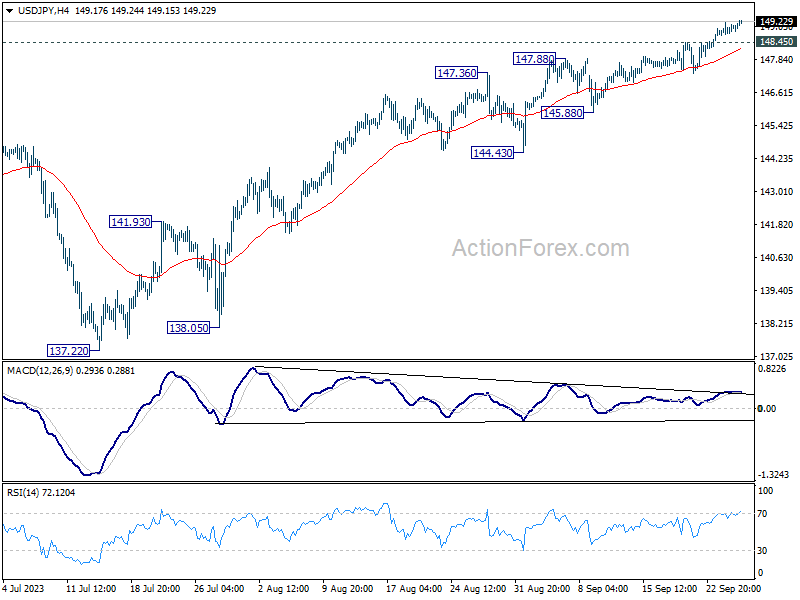

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.79; (P) 148.99; (R1) 149.27; More...

Intraday bias in USD/JPY stays on the upside for the moment. Current rise from 127.20 should target a retest of 151.93 high. On the downside, below 148.45 minor support will turn intraday bias neutral first. But outlook will now stay bullish as long as 145.88 support holds, in case of retreat.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.