Sample Category Title

UK Growth Surprises in June, Cooling Pound Sell-off

According to a data set released on Friday, the UK economy performed better than expected across a wide range of indicators in June. GDP rose by 0.2% in the second quarter and 0.4% in the same quarter a year earlier. Expectations had been for growth of less than 0.2 percentage points.

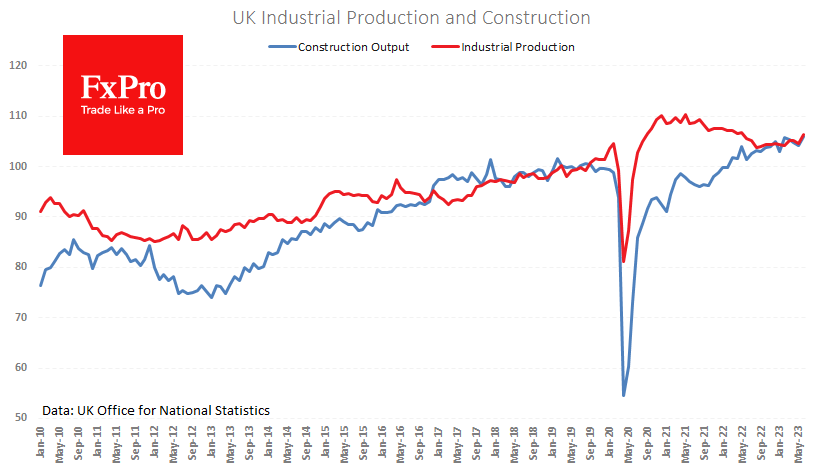

An impressive 1.8% m/m jump was recorded in industrial production, with manufacturing output rising by 2.4%. After many months of sluggish performance, the industrial production index is at its highest level since May 2022.

Activity in the construction sector did not lag, rising by 1.6% m/m and 4.6% y/y. The uptrend in these sectors contradicts expectations that high-interest rates are dampening economic activity.

Such robust data encourages the Bank of England to step up its fight against inflation without stopping to raise interest rates in the coming months. And that’s good news for the Pound, which rose almost 0.5% against the Dollar to 1.2735 on Friday after three weeks of declines.

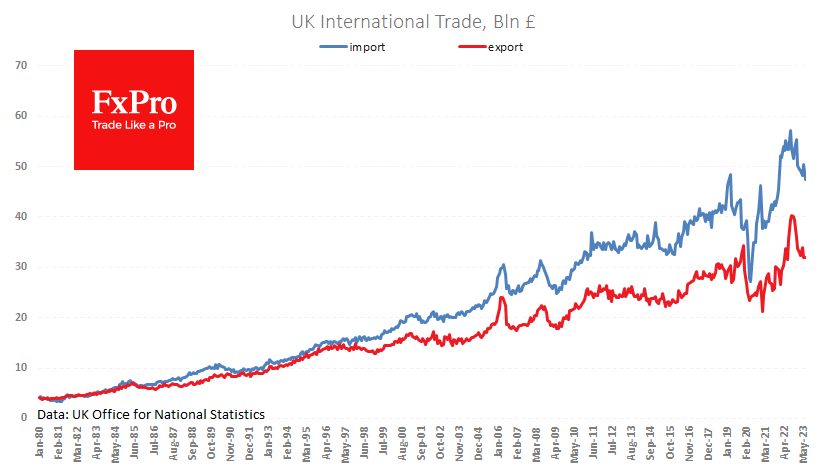

Strictly speaking, a smaller trade deficit than expectations and previous data is also positive for the Pound. However, the decline in exports and imports indicates weak demand and could be an early indicator of economic weakness.

The GBPUSD has fallen more than 3.5% from its peak of 1.3120 set about a month ago. The Pound’s momentum in August increasingly suggests that the almost year-long rally is entering a correction phase. The trajectory of the correction suggests a pullback to 1.2420 or further to 1.2060 before the speculative appeal of sterling buying returns.

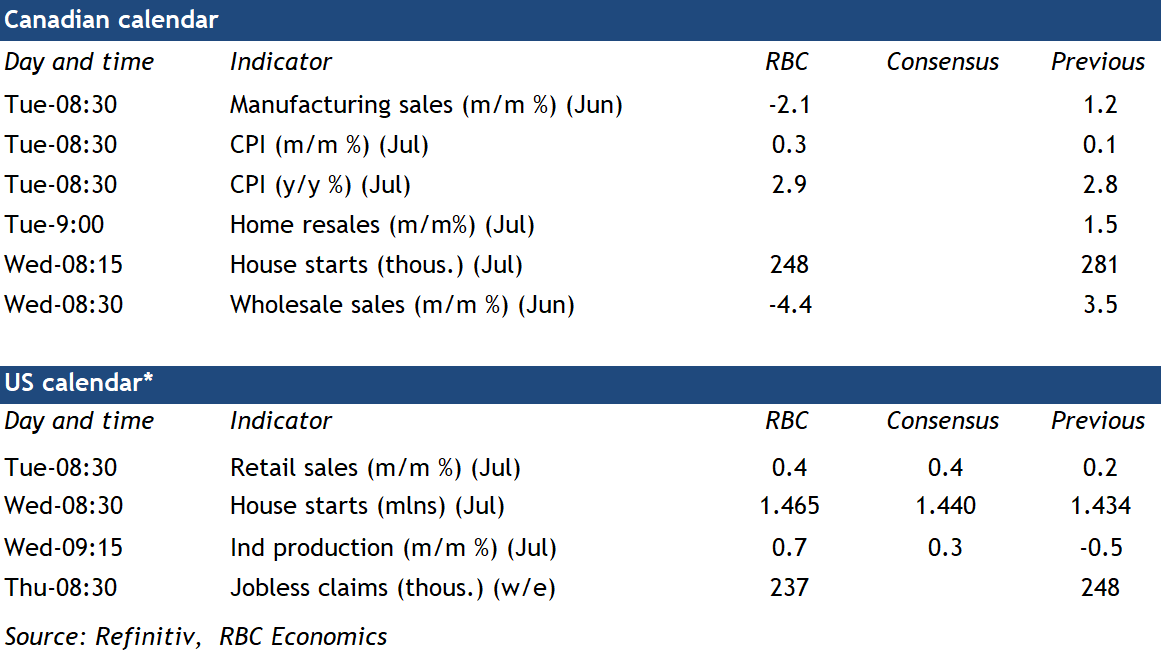

Forward Guidance: Canadian Inflation Likely Inched Up in July

Canada’s July CPI report lands among a slew of releases next week. But with the Bank of Canada signaling that its next rate hike decision will hinge on data—it will be the most closely scrutinized. Year-over-year inflation likely edged up to 2.9%. That’s after falling to 2.8% in June, putting it below the top end of the BoC’s 1% to 3% target range for the first time since spring 2021. The uptick in growth can be explained by rising energy prices. Though gas prices were still below year ago levels in July, the decline was smaller than in June. And with oil prices already above $80/barrel in August, energy costs will continue to add upward pressure to inflation in the near-term.

But the BoC will be more focused on broader inflation pressures beyond volatile energy costs. Food price growth probably remained high in July. But the pace of increases likely continued to slow, reflecting the lagged impact of lower commodity prices and easing supply chain disruptions. We expect price growth excluding food and energy products to slow further too, falling to 3% year-over-year from 3.5% in June. Mortgage interest costs will continue to account for a disproportionate share of that growth (accounting for almost a third of total CPI growth)—but the BoC will look through the impact of that component since it is a direct result of higher interest rates. The BoC’s preferred measures of ‘core’ inflation will also be closely watched. Those measures have been ‘stickier’ in recent months. But the three-month rolling average growth rate for the trim and median measures should slow as a large monthly increase in April falls out of that calculation. Growth in trim services ex-shelter (or “supercore”) should also subside, though it’s been running higher than other inflation measures in recent months.

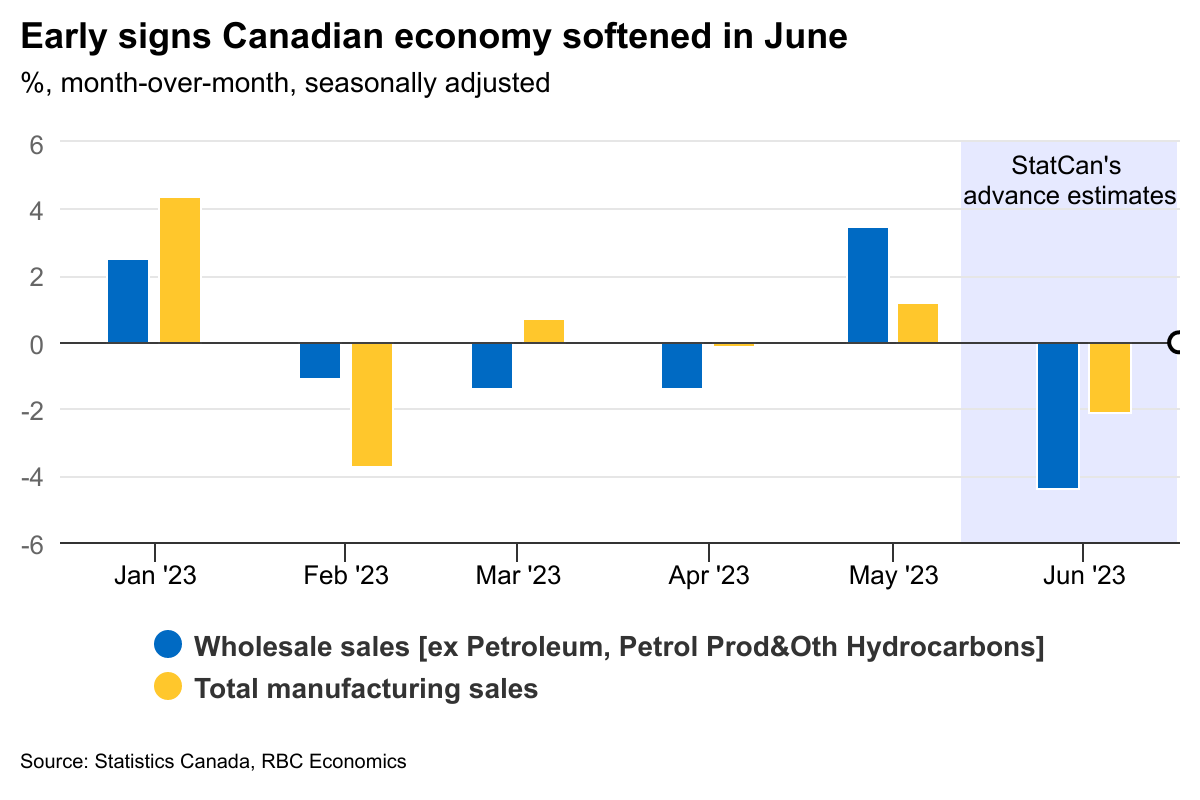

Where broader inflation trends go in the future still depends on the strength of the Canadian economic backdrop. And our own consumer spending tracker still shows resilient spending, particularly for discretionary services. But there have been more signs of softening recently. The unemployment rate is still low, but it’s increased by half a percentage point over the last three months (to the highest levels since February of last year). And manufacturing and wholesale sales reports next week should post steep drops given 2.1% and 4.4% declines, respectively, in Statistics Canada’s preliminary estimates. As more economic weaknesses emerge, underlying price pressures will continue to ease.

Week ahead data watch

Statistics Canada’s early indicator showed “core” wholesale sales dropped 4.4% in June, including a sharp pullback from the machinery, equipment and supplies sector.

Canada's housing market continues to cool off according to our latest housing report. July home resales data will be closely watched for further signs of easing.

Advance manufacturing sales indicated a 2.1% decline in June. Motor vehicle production likely edged lower, but the advance estimate implies substantial softness in other industries as well.

We expect Canadian housing starts to sink in July, from 281,000 in June to 248,000. Permit issuance ticked up on a 3-month rolling average basis (257,000).

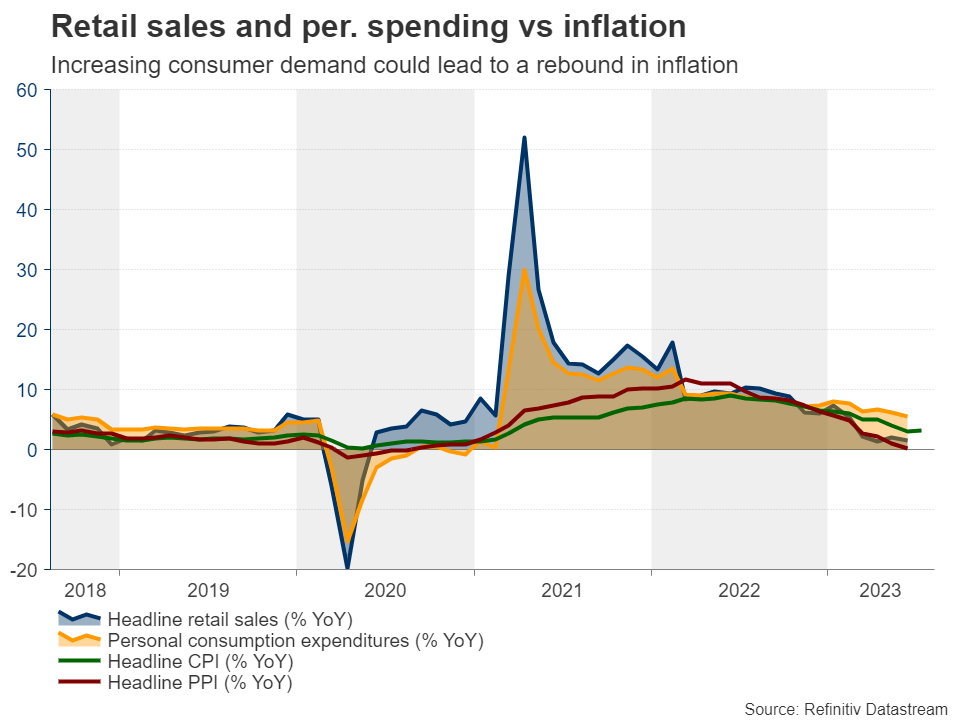

U.S. retail sales likely edged up 0.4% in July, primarily supported by sales increase in the building and auto sectors, and partially offsetting the sales drop at gas stations.

We look for an uptick in the U.S. industrial production (+0.7%) in July. Manufacturing hours worked edged lower in July but electricity output jumped sharply.

Dollar Turns to US Retail Sales and FOMC Minutes

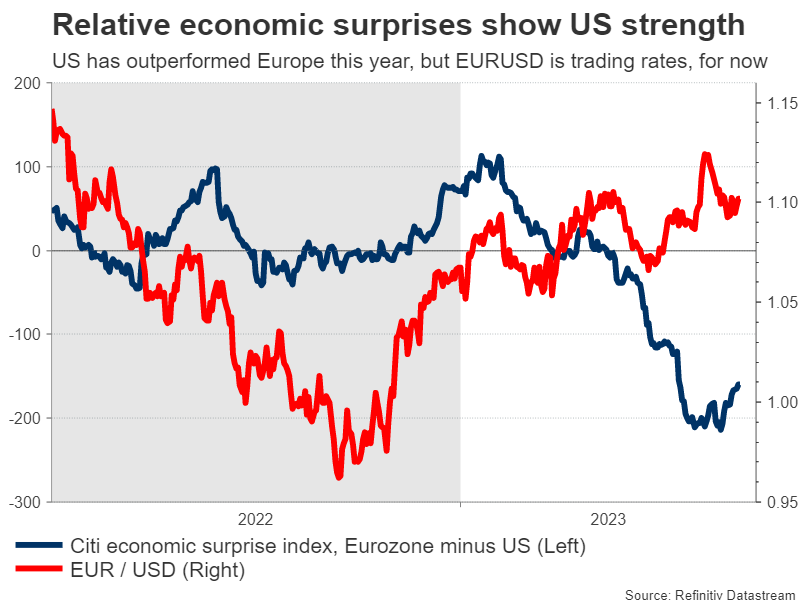

With the US inflation report out of the way, dollar traders will turn their focus on the next edition of retail sales on Tuesday and the minutes of the latest FOMC meeting on Wednesday. Overall, it is becoming clear that the US economy is superior to its competitors at this stage, something that might be increasingly reflected in the FX arena moving forward.

US outperforms

The United States is currently the bright spot of the global economy. According to the Atlanta Fed GDPNow model, economic growth in the current quarter is running at around 4%, showing no signs of damage from the meteoric rise in interest rates.

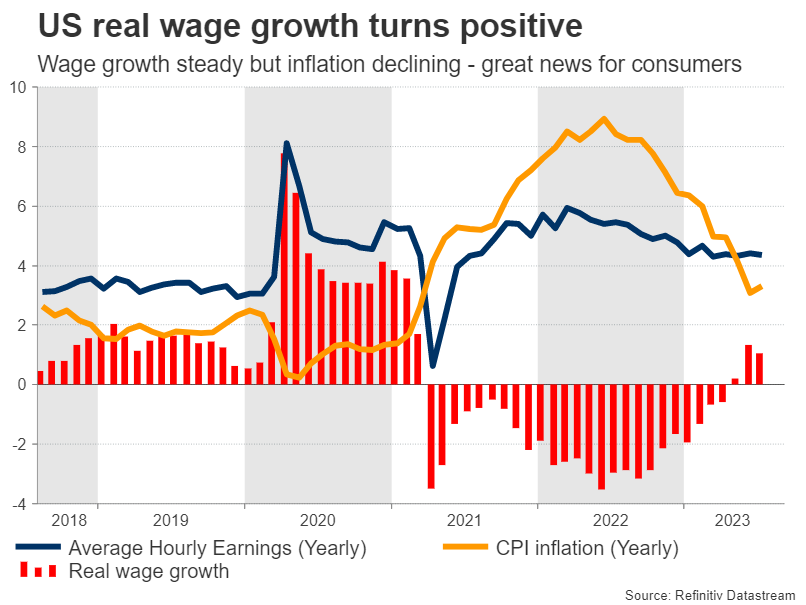

Meanwhile, the labor market is still in great shape. The unemployment rate is hovering near its lowest levels in five decades and with inflation falling lately, real wage growth has returned to positive territory. If sustained, that would be a blessing for consumers.

But the most striking part is the housing sector, which has staged an impressive recovery. Home prices have reached new record highs in many parts of the country, even with mortgage rates hanging around 7%, amid a shortage of available homes for sale.

Add it all together and the US economy is firing on most cylinders, in sharp contrast to Europe and China, where storm clouds seem to be gathering. Business surveys suggest the Eurozone is teetering on the verge of recession, while Chinese growth is losing steam thanks to the troubles in global manufacturing.

Retail sales and Fed minutes eyed

Turning to the upcoming events, the ball will get rolling on Tuesday with the latest edition of US retail sales. Forecasts point to an acceleration in July, something supported by the latest card spending data from Bank of America, which showed a solid increase in consumption.

Then on Wednesday, the spotlight will turn to the minutes of the Fed’s July meeting that will be released at 18:00 GMT. This was the meeting where the Fed raised rates by a quarter-point, but was hesitant to signal any more. Hence, the minutes will be scrutinized for some color around this debate - did the majority of officials favor another rate hike or not?

Judging by the comments from various FOMC officials, it seems the consensus is that interest rates are unlikely to be raised again. That’s what market pricing suggests too, as futures imply only a 30% probability for another rate hike this year and point to rate cuts as early as March next year.

Dollar seems well positioned

Even if the Fed does not raise rates again, the dollar could still find some love. With the US economy so much stronger than its European and Chinese counterparts, it seems likely that investment flows will continue to favor the United States.

Generally speaking, capital does not flow into struggling economies. The US economy is not amazing, but foreign economies are much weaker. Hence, this relative economic outperformance might be increasingly reflected in the FX complex moving forward, tilting the risks surrounding euro/dollar to the downside.

Arguing in the same direction are the dynamics in the US bond market. Amid runaway government deficits, the Treasury has been forced to increase its bond issuance. This increase in bond supply exerts upward pressure on yields, which can benefit the dollar by making it more attractive through the channel of interest rate differentials.

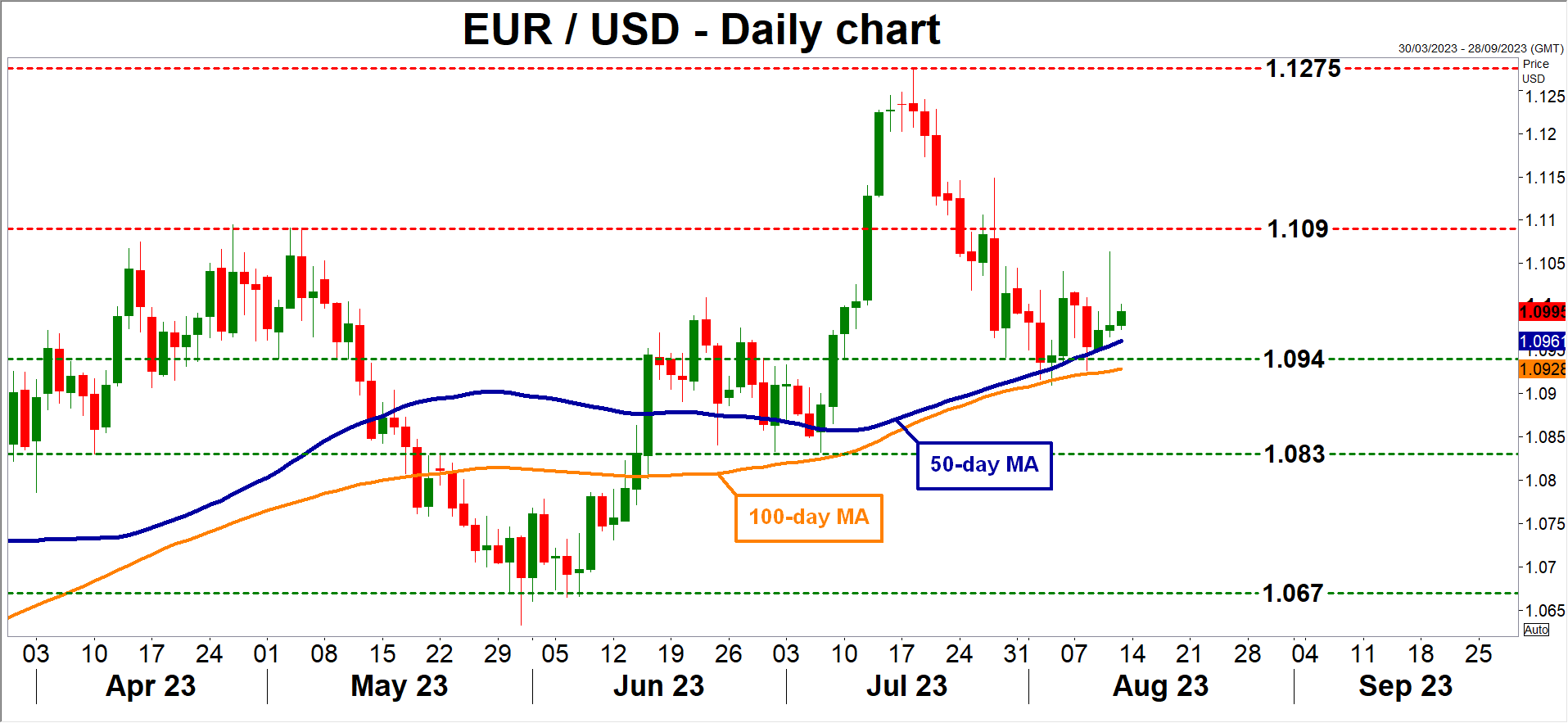

Looking at the charts, the most important region to watch in euro/dollar is 1.0940. That is the 50% Fibonacci retracement of the entire 2021-2022 downtrend, where the 50- and 100-day moving averages have converged, and there’s also a trendline drawn from the September lows in the vicinity. The pair has rebounded from this zone several times lately, so a break lower would be an important technical signal.

Week Ahead – Fed Minutes, US Retail Sales and UK CPIs the Highlights of a Packed Week

The dollar pulled back after the miss in the US inflation data, but traders may have another opportunity to adjust their dollar positions as next week’s agenda includes the minutes from the latest Fed meeting and the retail sales for July. The pound will also enter the limelight as the UK CPIs could confirm whether investors were correct to slash their hike bets following the latest BoE gathering. Other releases include the RBNZ decision, where no action is expected, and Canada’s CPIs.

Dollar traders turn attention to retail sales and Fed minutes

Following the lower-than-expected CPI data for July, investors remained convinced that the Fed will not proceed with any other hikes and that nearly 130bps worth of rate reductions may be warranted for next year. This kept the euro/dollar uptrend intact, despite the US currency holding strong since July 18, as the pair rebounded somewhat from the upward sloping line drawn from the low of September 26.

At the latest FOMC meeting, Fed Chair Jerome Powell said that they will make decisions meeting by meeting, closely watching economic data, adding that they could hike again in September if the data suggests so, but also that they could choose to hold steady.

Therefore, after the CPIs, Tuesday’s retail sales and Wednesday’s industrial production for July may also be of high importance as they could determine whether the dollar can stage a solid comeback or not. Both the headline and excluding-autos sales are expected to have accelerated to 0.4% month-on-month from 0.2%, while industrial production is forecast to have rebounded 0.3% m/m after shrinking 0.5%.

Although these releases are unlikely to significantly alter the market’s Fed implied rate path on their own, they could add to hopes of a soft landing, while they could make it easier for investors to eventually rethink the probability of a September hike if later on Wednesday, the minutes of the last Fed meeting reveal that there was a decent number of policymakers that were in favor of delivering more hikes before signaling the end of this tightening cycle.

Combined with the US Treasury’s pledge to issue more bonds, this may help yields and the dollar move higher. At the same time, equities may extend their latest correction. The opposite may be true if the data come in softer than expected and the meeting minutes suggest that most Fed officials were skeptical about whether more hikes are needed.

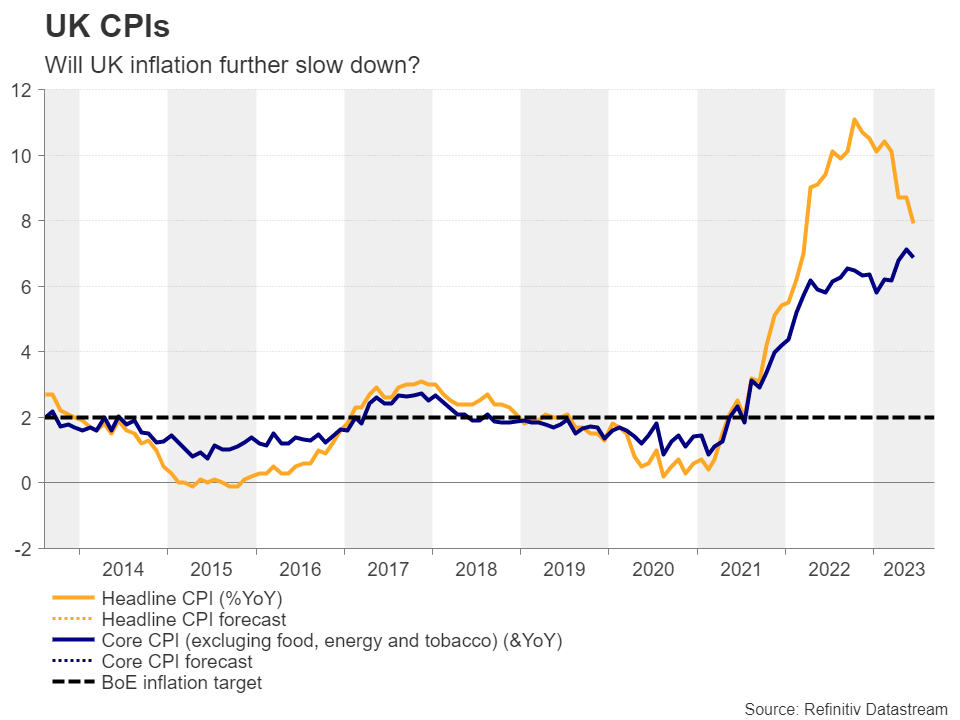

Will UK inflation come further down?

The BoE raised interest rates by the expected 25bps when it last met, but failed to appear as hawkish as many may have anticipated, with Governor Bailey noting that he didn’t think there was a case for another 50bps hike.

Following the decision, investors slashed their rate-hike expectations, now seeing only a 70% probability of a quarter point hike at the September meeting, with the remaining 30% pointing to no action. As for the future, they are anticipating only one more quarter-point increment before this Bank ends its own tightening crusade as well.

Next week, pound traders will likely pay close attention to the UK CPIs for July, due out on Wednesday, as they try to evaluate whether their assessment appears correct or not. No forecast is currently available, but the S&P Global PMIs suggested further cooling of inflationary pressures, which tilts the risks surrounding the CPIs to the downside. Further declines in the CPI rates, especially the core one, could add credence to investors’ choice to lower their implied rate path and may further weigh on the pound.

The nation’s employment report for June and retail sales for July are also due to be released on Tuesday and Friday respectively.

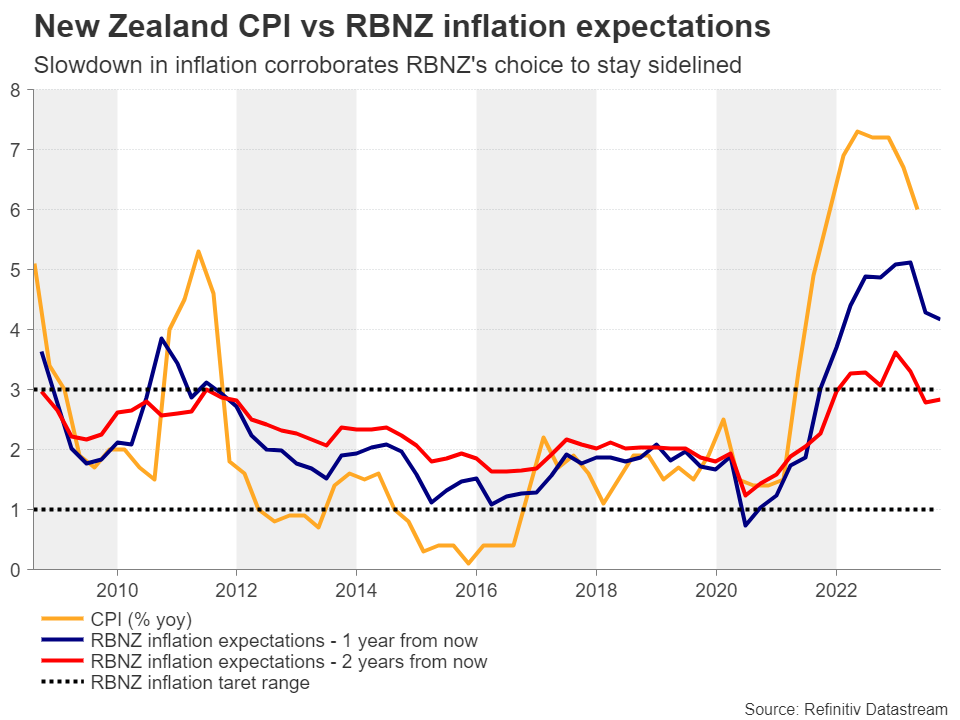

RBNZ to stay sidelined, kiwi exposed to risk sentiment

The RBNZ meets on Wednesday and staying sidelined appears a virtual certainty, with the probability of a hike resting at a mere 4%. Back in May, this Bank signaled that it is done raising rates and in July, it took the sidelines, saying that high interest rates had constrained spending as anticipated.

With data revealing that the CPI rate fell to 6.0% in Q2 from 6.7%, it seems that this meeting is unlikely to result in any fireworks, as the cooling in inflation corroborates officials’ past choices.

Thus, the kiwi experiencing huge volatility due to this decision is very doubtful, rather it may stay more sensitive to the broader market sentiment and specifically to developments surrounding the Chinese economy.

China data dump, RBA minutes and Australia jobs data

Speaking about China, the world’s second largest economy releases its fixed asset investment, industrial production, and retail sales numbers for July on Tuesday. Following the worsening contraction in both exports and imports, as well as the fall in consumer prices, another set of disappointing numbers could weigh further on market sentiment and especially the currencies whose nations have close trade ties with China, like the kiwi and the aussie.

Aussie traders will also have to digest the RBA meeting minutes on Tuesday and Australia’s employment report on Thursday, although they are nearly certain that the RBA will remain sidelined at its September meeting.

More data from Canada and Japan

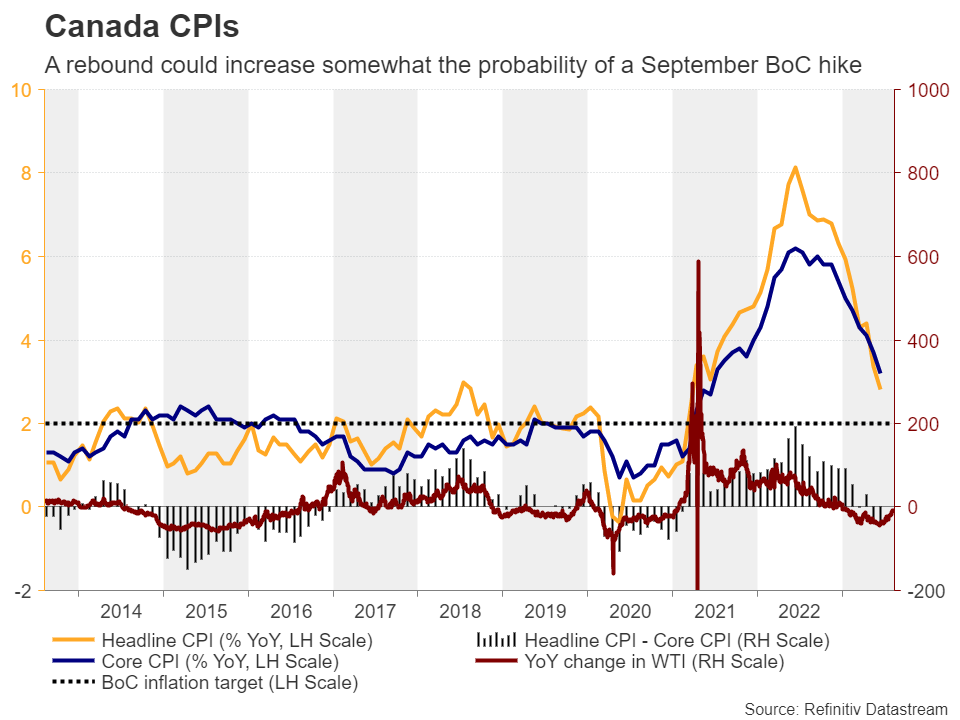

The Canadian dollar has also been on the back foot lately, despite the strong recovery in oil prices. Perhaps the deteriorating risk appetite and a strong US dollar did not allow traders to consider buying the loonie.

They will however have an opportunity to reevaluate the outlook of this currency on Tuesday when Canada’s CPI data for July are coming out. With the year-on-year change in oil prices rebounding strongly lately, the headline CPI rate may be poised to rebound from 2.8% y/y. If the core rate increases notably as well, then the probability of another rate increase by the BoC at the September gathering may increase from its current level of around 20% and thereby add some support to the loonie. The opposite may be true in the case of an inflation slowdown.

The yen has been under pressure for the whole week as the slowdown in Japan’s wage growth may have weighed on expectations of further tightening by the BoJ. On Tuesday, the nation’s preliminary GDP numbers for Q2 are due to be released and the forecast points to a small acceleration to 0.8% qoq from 0.7%. That said, a potential miss in this data set may corroborate the view that Japanese officials may need to wait for a while longer, and thereby push the yen lower, especially if Friday’s CPIs reveal a slowdown.

Weekly Focus – Central Banks Opt for Cautious Tone as Growth Falters

As many Europeans continue to enjoy their summer breaks, their mood can be lifted by expectations that peak rates loom in the horizon. In July, the ECB hiked the deposit rate to 3.75%, as expected, but at the press conference, President Lagarde opted for a clearly dovish tone. Service sector, the prime engine for economic growth in Europe this year, has started to lose steam, and the ECB is clearly more concerned about growth than before. As it is evident the ECB has now entered the fine-tuning phase in its policy tightening, Lagarde emphasized that they could hike rates again in September, or they could choose to pause, depending on the upcoming data. Furthermore, if they pause in September, they could still hike later on, if necessary. We keep our call of one more hike in September, read more on Flash ECB Review - A decisive maybe, 27 July.

After pausing in June, the Federal Reserve also delivered a 25bp hike in July to 5.25-5.50%. No doubt the US economy has performed better than expected lately. Nevertheless, as there are clear signs of inflation now starting to stabilise to levels consistent with the central bank's 2% mandate, we think this was the final hike of the cycle (see Research US - Fed Review: Balancing act with focus on data, 26 July). The BoE also delivered according to expectations and hiked the policy rate by 25bp, bringing the bank rate to 5.25%. We expect one more hike in September and stay negative on GBP.

Boosted by expectations of rates peaking in near future, the US stock market rallied in June-July with the S&P500 rising 10%, converging with European stocks that have been outperforming since last November. Until now, high inflation has led to a rising corporate profit share at the cost of earners, which makes sense since selling prices move more flexibly than wages. Going forward, however, corporate profits will have to absorb the increases in wages, if inflation is to be tamed. Alternatively, corporates maintain their pricing power, passing through rising wage costs to prices, in which case inflation could again prove stickier than expected. In this light, could it be that the markets are relying on a central bank pivot that will not happen, not as soon as the markets expect anyway?

Risk market rally also drove a weaker in USD in early July, and EUR/USD hit a 16-month high before changing course around mid-month. We still like our strategic call for a weaker EUR/USD (see FX Forecast Update - holiday edition: Q3 to mark peak in policy rates, 17 July). This week, energy sector concerns have again raised their head after news of a planned strike at Australian LNG plants led to a spike in gas prices.

The Bank of Japan surprised the markets in July by keeping its yield curve control (YCC) but announcing they would allow long-term interest rates to rise up to 1%. The practical modalities were likely intentionally left vague, but at least the BoJ can now choose not to intervene in the market if pressure builds up for higher yields. We expect a gradual easing of the YCC in the course of the autumn.

Next week, focus will be on US July retail sales and other real sector data. FOMC minutes will be released on Wednesday. In euro area, we keep an eye on the ZEW index on Tuesday and the final July HICP print due on Friday.

Japanese Yen Knocking on the 145 Door

- US CPI accelerates to 3.2%

- US PPI climbs 0.7%

The Japanese yen is trading quietly on Friday. In the European session, USD/JPY is trading at 144.82, up 0.07%. It has been an awful week for the yen, which is down about 2% against the US dollar. The yen fell as low as 144.89 today, and it looks like the yen will breach the 145 line for the first time since June.

There are no Japanese events on the calendar, so it could be a quiet day for the yen. In the US, the Producer Price Index for July surprised on the upside. The index jumped 0.8% m/m, up from 0.2% in June and above the consensus estimate of 0.7%. Core PPI rose 0.3%, following a -0.1% reading in June and beat the estimate of 0.2%. The US dollar hasn’t shown much movement against the major currencies following the release.

US inflation rises, core rate ticks lower

The July US inflation report showed a divergence between headline CPI and core CPI. Headline CPI accelerated for the first time in 13 months, with a reading of 3.2%, up from 3.1%. The rare uptick in inflation didn’t rustle any market feathers, as the estimate stood at 3.3% and the acceleration was due to base effects rather than new inflationary pressures.

Core CPI, which the Fed pays close attention to, ticked lower to 4.7% in July, down from 4.8% in June. On a monthly basis, the core rate climbed by 0.2% for a second straight month. This is encouraging for the Fed as it points to core inflation losing steam. Headline inflation has fallen sharply due to a sharp drop in energy prices, but the core rate excludes food and energy prices.

The inflation report appears to have cemented a Fed pause in September. The markets are widely expecting the Fed to hold rates next month and have also priced in a pause in November. The markets are already looking ahead to rate cuts next year but the Fed is taking a more hawkish stance, as it has more work to do before it can declare victory over inflation.

USD/JPY Technical

- There is resistance at 143.55 and 144.28

- 142.12 and 141.47 are providing support

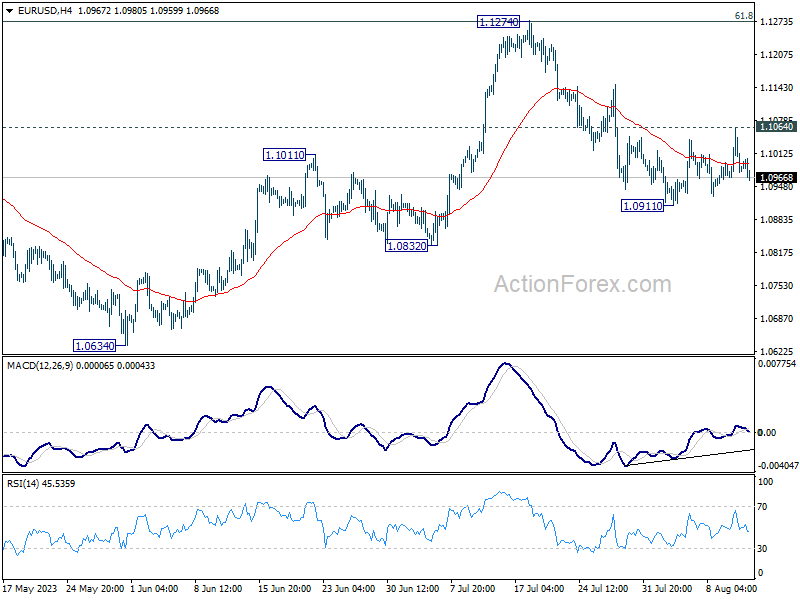

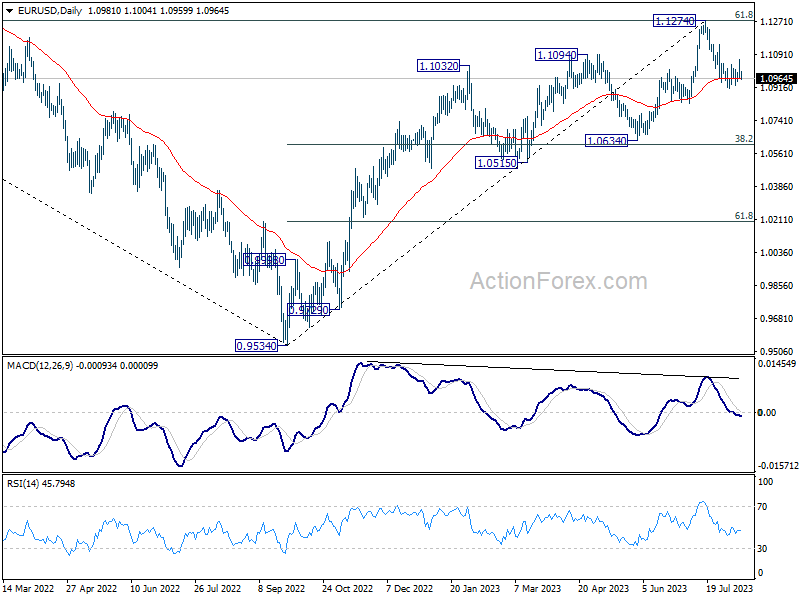

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0944; (P) 1.1004; (R1) 1.1042; More...

No change in EUR/USD's outlook and intraday bias stays neutral first. On the downside, break of 1.0911 will resume the fall from 1.1274 to 1.0832 support. Sustained trading below there will target 1.0609/34 cluster support. However, firm break of 1.1064 minor resistance will argue that pull back from 1.1274 has completed, and bring stronger rebound.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0966) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

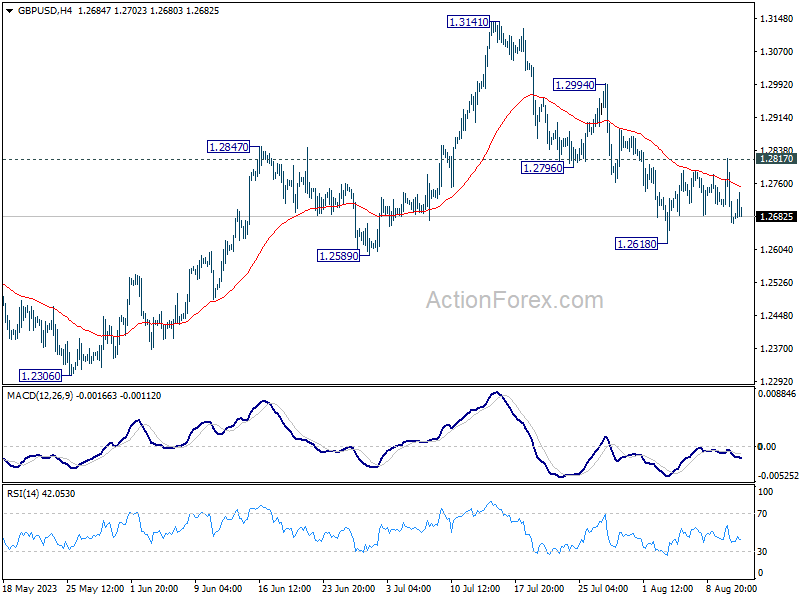

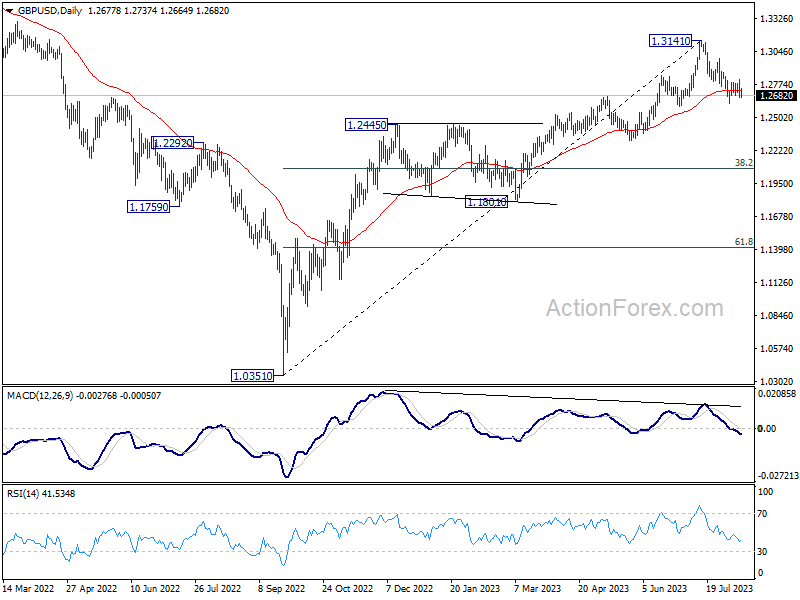

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2624; (P) 1.2721; (R1) 1.2773; More...

Intraday bias in GBP/USD stays neutral as range trading continues. On the downside, below 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, firm break of 1.2817 minor resistance will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2726) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

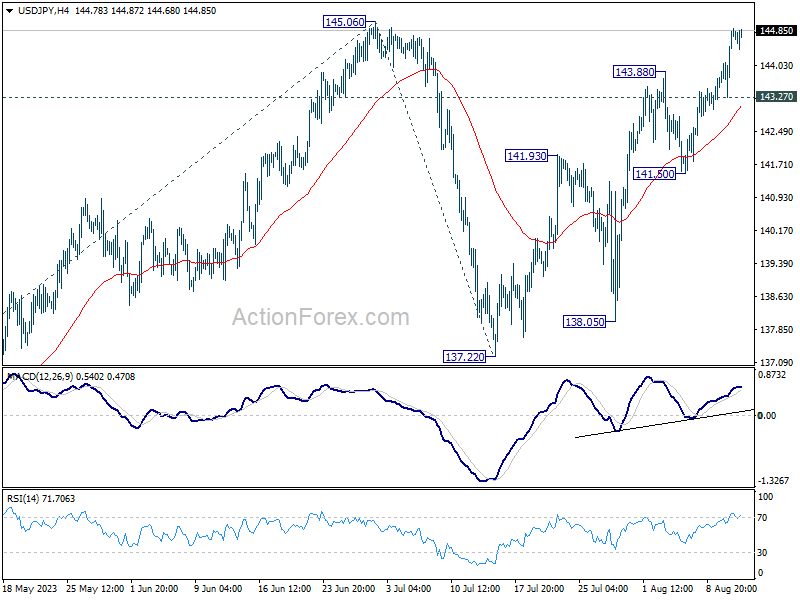

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.75; (P) 144.28; (R1) 145.29; More...

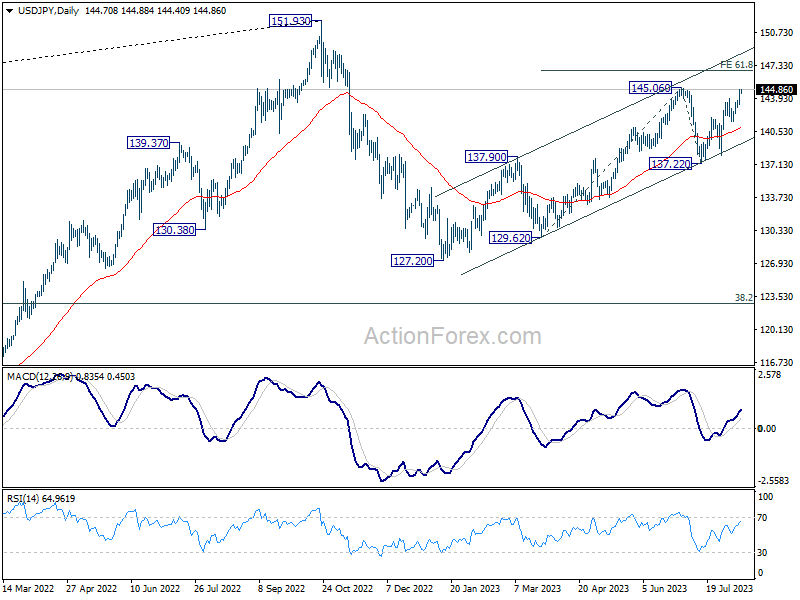

USD/JPY's rally is in progress and intraday bias stays on the upside. Decisive break of 145.06 will resume whole rise from 127.20. Next target is 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76. On the downside, however, below 143.27 minor support will delay the bullish case and turn intraday bias neutral again.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

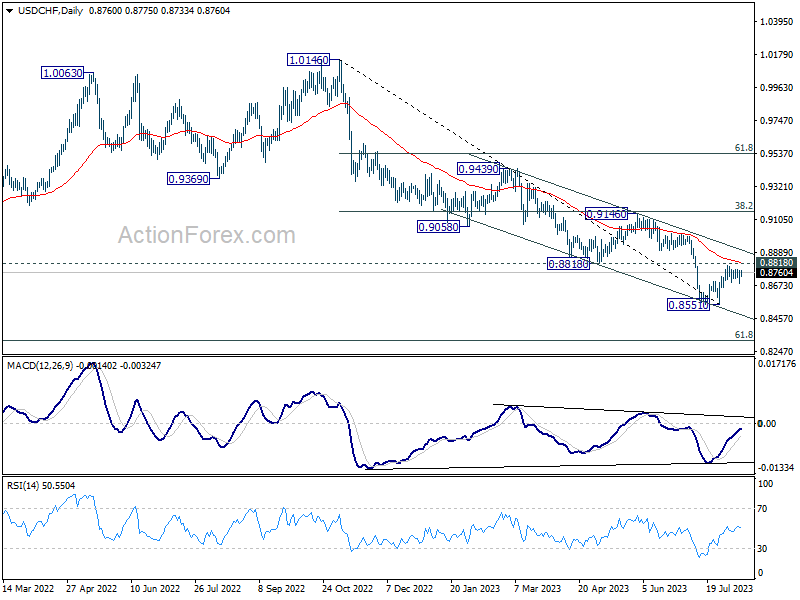

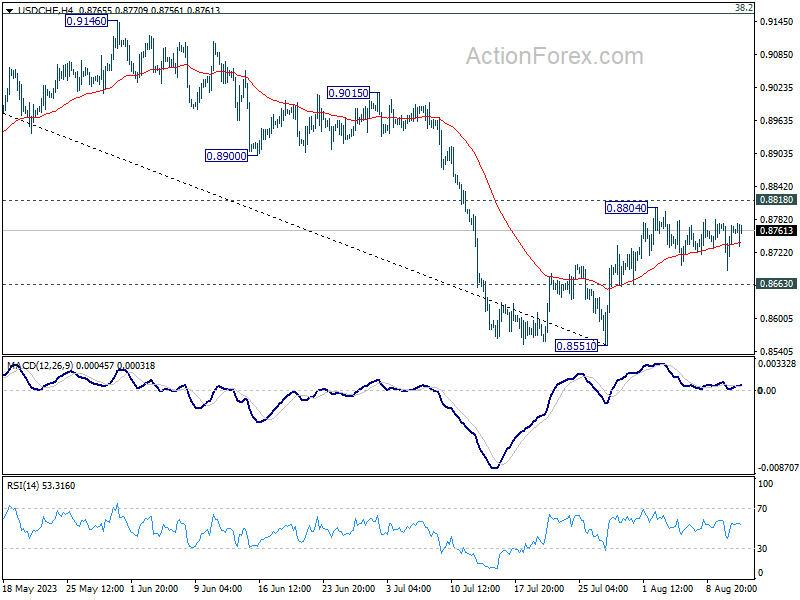

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8713; (P) 0.8746; (R1) 0.8800; More....

Sideway trading continues in USD/CHF and intraday bias stays neutral. On the downside break of 0.8663 minor support should confirm rejection by 0.8818 and turn intraday bias back to the downside for retesting 0.8551 first. Nevertheless, decisive break of 0.8818 will carry larger bullish implication, and target 0.9146 cluster resistance next.

In the bigger picture, down trend from 1.0146 is seen as in progress as long as 0.8188 support turned resistance holds. Next target is 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317. However, sustained break of 0.8818 should indicate medium term bottoming, and bring stronger rise back to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction.