Sample Category Title

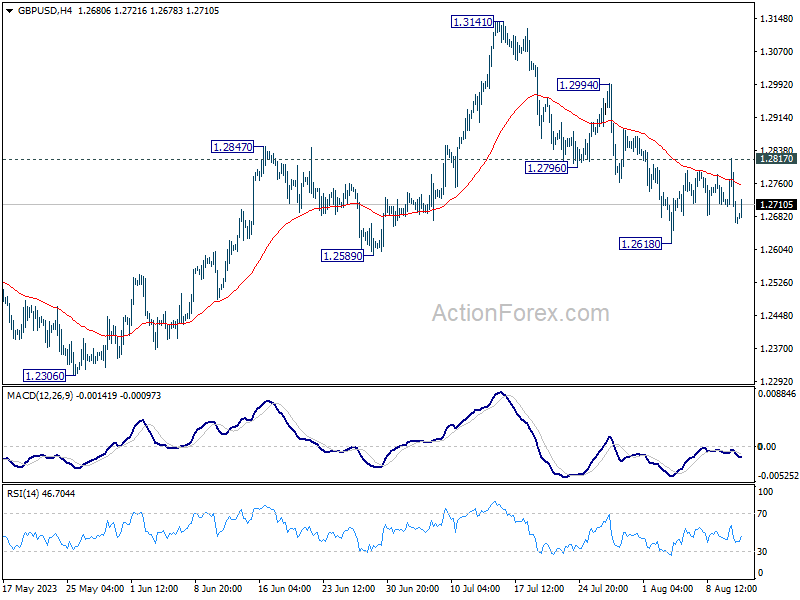

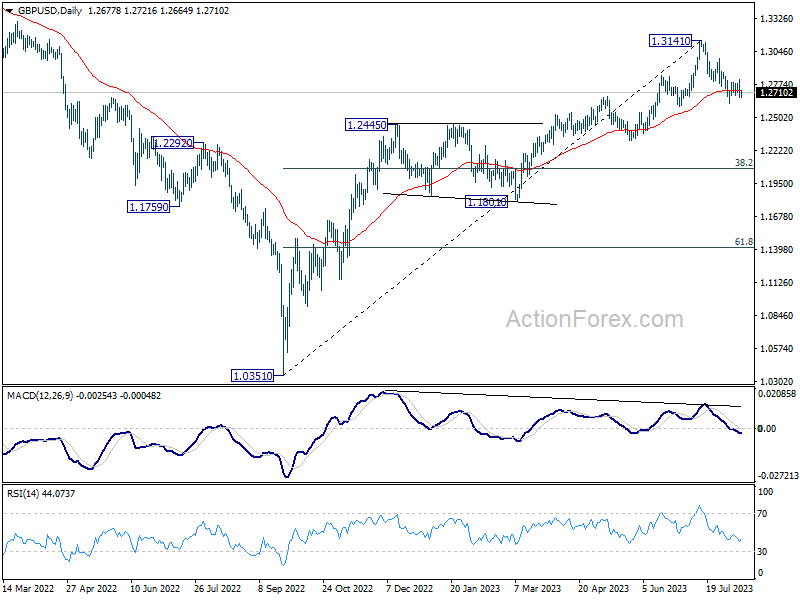

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2624; (P) 1.2721; (R1) 1.2773; More...

GBP/USD recovers mildly today but stays in range above 1.2618. Intraday bias stays neutral at this point. On the downside, below 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, firm break of 1.2817 minor resistance will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2726) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

Sterling Advances on Strong GDP Data; Swiss Franc Awaits Crucial Breakout

British Pound is showing notable strength in early European session today, buoyed by more robust than anticipated monthly and quarterly GDP figures. While the quarterly GDP has not yet bounced back to its pre-pandemic stature, the positive numbers come as a boon to BoE. This development supports the expectation that the BoE will maintain its prolonged tightening, as inflation remains elevated.

On the other side of the Atlantic, Dollar has displayed remarkable resilience post its CPI-induced dip. The greenback is staying as the strongest performer for the week, even though it's still bounded in range against all but Yen. Currently, Sterling occupies the third spot in performance rankings, with a potential to surpass Euro and secure second place. Yen, however, remains at the bottom of the pile, with minimal chances of a reversal before the week concludes. Commodity-based currencies also seem to be on the weaker end.

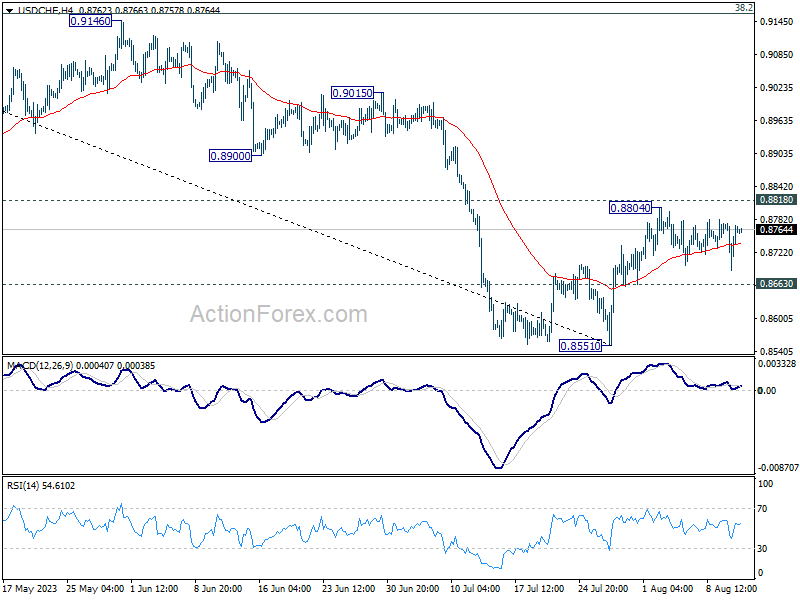

Technically, Swiss Franc is worth some attention for the near term. USD/CHF's price actions from 0.8804 are rather corrective looking, and argues that rebound from 0.8551 is not over. Break of 0.8804 would likely push the pair through 0.8818 support turned resistance, which would then signal a stronger medium term rebound is underway, even as a corrective move. At the same time, the selloff in Franc would be solidified if EUR/CHF could break through corresponding resistance levels at 0.9647 and 0.9670 too.

In Asia, Nikkei closed up 0.84%. Hong Kong HSI is down -0.78%. China Shanghai SSE is down -1.45%. Singapore Strait Times is down -0.92%. Japan 10-year JGB yield is up 0.0241 to 0.589. Overnight, DOW rose 0.15%. S&P 500 rose 0.03%. NASDAQ rose 0.12%. 10-year yield rose 0.068 to 4.080.

Fed's Daly on CPI: Not a Victory Yet

San Francisco Fed President, Mary Daly, offered a measured response to yesterday's US CPI release, stating that while the figures "came in largely as expected, and that is good news," it does not signify a comprehensive victory over the ongoing inflation challenges. "It is not a data point that says victory is ours," Daly warned.

Highlighting the nuanced nature of the current inflation landscape, Daly noted the decrease in goods inflation and indicated promising trends in housing. However, her main concern lies with core services inflation that excludes housing.

Despite the general trend of receding inflation, core services inflation remains stubborn. Daly emphasized, "We do need to see that come back to prepandemic levels if we're going to be confident that we can get to 2% on a sustainable basis."

Offering insight into Fed's future strategy, Daly was cautious: "Whether we raise another time, or hold rates steady for a longer period -- those things are yet to be determined."

She stressed the importance of upcoming data before Fed's next meeting, suggesting it would play a critical role in shaping decisions. "It would be premature to project what I think would happen because there's a lot of information coming in between now and our next meeting" in September, she added.

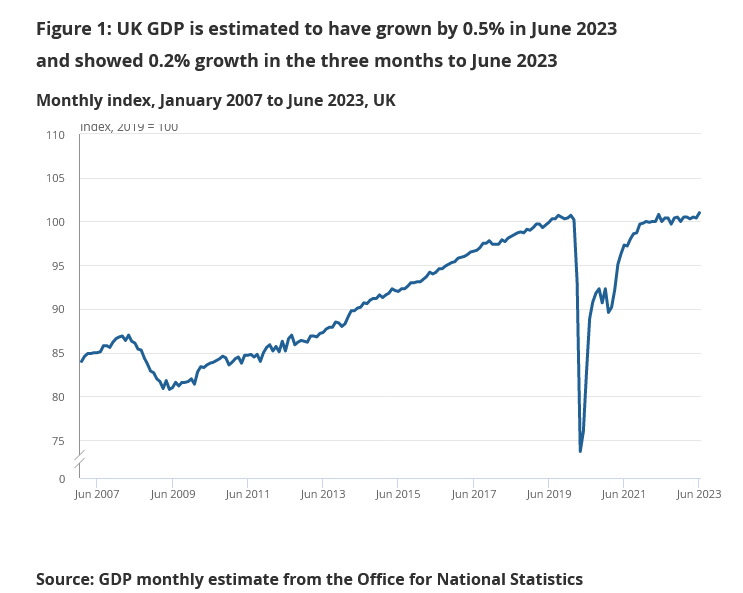

UK GDP rose 0.5% mom in Jun, up 0.2% qoq in Q2

UK GDP grew 0.5% mom in June, well above expectation of 0.2% mom. Production grew 1.8% mom. Services was up 0.2% mom. Construction also rose 1.6% mom.

For Q1, GDP grew 0.2% qoq, above expectation of 0.0% qoq. But the level of quarterly GDP was -0.2% below its pre-pandemic level in Q4 2019. Services grew 0.1% on the quarter. Production grew by 0.7% with 1.6% growth in manufacturing. Construction rose 0.3%.

The implied price of GDP rose by 2.1% in Q2, which was primarily driven by higher price pressures for household consumption (1.5%) and government consumption (3.1%).

Also released, industrial production was up 1.8% mom, 0.7% yoy in June. Manufacturing production was up 2.4% mom, 3.1% yoy. Goods trade deficit narrowed to GBP -15.5B.

RBA Lowe: Possible that some further tightening will be required

Addressing the House of Representatives Standing Committee on Economics today, outgoing RBA Governor, Philip Lowe stated that the purpose behind the pauses in July and August was "to provide time to assess the impact of the (rates) increases to date and the economic outlook and the associated risks."

He reiterated that "it is possible that some further tightening of monetary policy will be required". But the decision would be largely based on incoming data and the Board's evolving analysis of economic forecast and potential risks.

Lowe expressed optimism about recent economic data, remarking, "It is encouraging that the recent data are consistent with inflation returning to target over the next couple of years."

But he also pinpointed two risks that RBA is closely monitoring. "The first is the outlook for household consumption," he said, attributing this concern to the myriad of factors currently influencing household finances and expenditures.

The second risk highlighted was the potential persistence of high services price inflation which could lead to "prolonging the period of inflation being above target."

Lowe emphasized the RBA's forecast, which assumes a resurgence in productivity rates, aligning with levels seen pre-pandemic. Such growth, he suggested, would help in moderating the unit labour costs and subsequently, inflation. Yet, he cautioned, "If this pick-up in productivity does not occur, all else constant, high inflation is likely to persist, which would be problematic."

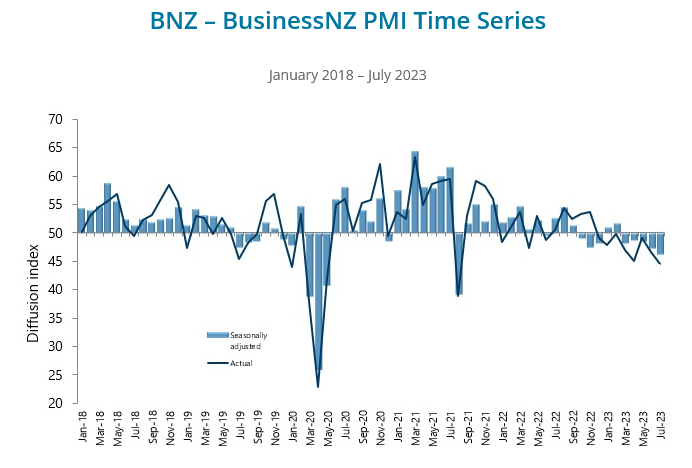

New Zealand BNZ manufacturing slumps to Post-GFC low in July

New Zealand's BusinessNZ Performance of Manufacturing Index has experienced a drop in July, declining from 47.4 to 46.3. Digging into the details, there was a notable dip in Production, which plummeted from 47.3 to 42.9, and Employment wasn't far behind, decreasing from 46.8 to 44.3. On a slightly brighter note, New Orders saw a modest increase, moving from 43.8 to 45.0, and Finished Stocks slightly ticked up from 52.3 to 52.6. However, Deliveries took a sharp hit, falling from 49.9 to 42.3.

Feedback from the manufacturing sector portrayed a gloomy picture. Negative comments in July stood at 72%, a slight decrease from June's 74.5%, but higher than May's 66.7% and April's 70.3%. The core concerns cited by manufacturers revolved around general market uncertainty, escalating costs, and inclement weather affecting demand, particularly during July.

Catherine Beard, BusinessNZ's Director of Advocacy, remarked on the PMI's July figures, indicating that they "showed very little signs of potential improvements for the sector as a whole." Echoing this sentiment, BNZ Senior Economist, Doug Steel, highlighted the gravity of the situation, noting that "the July result was the fifth consecutive monthly sub-50 reading and, outside of Covid lockdown periods, the lowest reading since the GFC days back in June 2009."

Looking ahead

Italy trade balance is the only feature in European session. Later in the day, US will release PPI and U of Michigan consumer sentiment.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2624; (P) 1.2721; (R1) 1.2773; More...

GBP/USD recovers mildly today but stays in range above 1.2618. Intraday bias stays neutral at this point. On the downside, below 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, firm break of 1.2817 minor resistance will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2726) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jul | 46.3 | 47.5 | 47.4 | |

| 06:00 | GBP | GDP Q/Q Q2 P | 0.20% | 0.00% | 0.10% | |

| 06:00 | GBP | GDP M/M Jun | 0.50% | 0.20% | -0.10% | |

| 06:00 | GBP | Industrial Production M/M Jun | 1.80% | -0.10% | -0.60% | |

| 06:00 | GBP | Industrial Production Y/Y Jun | 0.70% | -2.10% | -2.30% | -2.10% |

| 06:00 | GBP | Manufacturing Production M/M Jun | 2.40% | 0.10% | -0.20% | -0.10% |

| 06:00 | GBP | Manufacturing Production Y/Y Jun | 3.1% | -1.00% | -1.20% | -0.60% |

| 06:00 | GBP | Goods Trade Balance (GBP) Jun | -15.5B | -16.2B | -18.7B | -18.4B |

| 08:00 | EUR | Italy Trade Balance (EUR) Jun | 4.23B | 4.71B | ||

| 11:00 | GBP | NIESR GDP Estimate (3M) Jul | 0.00% | |||

| 12:30 | USD | PPI M/M Jul | 0.20% | 0.10% | ||

| 12:30 | USD | PPI Y/Y Jul | 0.70% | 0.10% | ||

| 12:30 | USD | PPI Core M/M Jul | 0.20% | 0.10% | ||

| 12:30 | USD | PPI Core Y/Y Jul | 2.30% | 2.40% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 70.9 | 71.6 |

UK GDP rose 0.5% mom in Jun, up 0.2% qoq in Q2

UK GDP grew 0.5% mom in June, well above expectation of 0.2% mom. Production grew 1.8% mom. Services was up 0.2% mom. Construction also rose 1.6% mom.

For Q1, GDP grew 0.2% qoq, above expectation of 0.0% qoq. But the level of quarterly GDP was -0.2% below its pre-pandemic level in Q4 2019. Services grew 0.1% on the quarter. Production grew by 0.7% with 1.6% growth in manufacturing. Construction rose 0.3%.

The implied price of GDP rose by 2.1% in Q2, which was primarily driven by higher price pressures for household consumption (1.5%) and government consumption (3.1%).

Consumers Not Convinced Rate Hikes are Over But RBA Looks to be More Firmly On Hold

Consumer sentiment continues to show little or no positive response to the pause in interest rate tightening. This is partly due to ongoing pressures on family finances but also to fears of further rate rises to come. The RBA Governor’s latest House of Reps testimony again suggests the hurdle for further rate rises is high, with policy moving to a new phase that will be more focused on risks relating to productivity and unit labour costs, where risks look may play out as a constraint on potential easing rather than trigger further hikes.

Inflation may be off its peaks and the RBA on hold but the ‘inflation lockdown’ continues to weigh heavily on Australian consumers.

The Westpac-Melbourne Institute Consumer Sentiment survey continues to show only a muted response to the RBA Board’s decision to leave the cash rate on hold in recent meetings, up only 2.3% in the two months since June, and slightly lower for the mortgage belt. Continued pressures on family finances from sharp rises in the cost of living, fears of further rate hikes to come and concerns about the near-term economic outlook continue to weigh heavily on confidence.

Around living costs, the easing in reported headline inflation is likely being offset by continued strong rises in a range of essentials, most notably around rents, fuel, and electricity. On the last two: petrol prices have lifted 10% in the last month as a rally in global oil prices has combined with a lower AUD; while electricity costs rose significantly from July 1 with ‘benchmark maximum’ rates up 20-25% across the major eastern states and expected to be up 7% on average national in the September quarter.

On interest rates, consumer fears partly relate to the RBA’s continued warnings that further tightening may still be required. Our survey shows most consumers are still bracing for further rate rises with over two thirds of those surveyed after the RBA’s August decision expecting rates to move higher over the year ahead, nearly half of this group expecting a rise of over 1ppt. That is about the same hawkish mix of responses we saw when the RBA first actively paused its rate rise cycle back in April.

Westpac’s view is that the RBA tightening cycle is now over. While there are still clear risks, particularly around the tight labour market, these are unlikely to form a strong enough case for the RBA to tighten further in coming months, particularly with inflation continuing to ease and growth outcomes confirming a sharp economic slowdown. The RBA’s recent commentary has shown increased confidence in achieving a reasonably timely return to low inflation and that it is also comfortable with inflation ‘only’ returning to the 2-3% range by late 2025 rather than being more intent on hitting the mid-point of that range.

The RBA Governor’s testimony to the House of Representatives Standing Committee on Economics gave some further articulation to the Bank’s views. Within this long and wide-ranging Q&A was a particularly notable discussion of the RBA’s ‘reaction function’ – how it is assessing the risks and trade-offs involved with different policy approaches. Governor Lowe described two alternatives: one in which the RBA set out to achieve an earlier return to low inflation by the end of 2024 (in line with many other central banks overseas); and another in which inflation was allowed to run higher for longer, only returning to target some time in 2026.

His assessment was that, given the strong inflation already locked-in around rents and electricity near term, achieving the inflation target in 2024 would require a substantial additional tightening in interest rates – in the order of as “at least a further 1ppt” – delivering a significantly larger shock to the economy that would result in a significantly higher unemployment rate. This trade-off was not one the Board was willing to make (presumably partly on the notion that rent and electricity cost inflation would become less of an issue beyond 2024).

On a slower return to target, the Governor’s key concern was that such a prolonged return, which would see inflation above target for over four years in a row, risked losing public confidence that the Bank was serious about achieving its inflation goals.

Separately, the Governor’s discussion of the evolution of the return to low inflation also provides some clues to how risks may play out from here – in our view, more as a constraint on prospective policy easing rather than additional tightening.

The Governor described the ‘next phase’ of the return to low inflation as one that requires slower growth in unit labour costs. That in turn relies on the extent to which labour costs rise and the degree to which we see a lift in labour productivity – output per unit of labour. Unit labour costs have surged 7.9% over the year to March, well above the 2.5% average seen over the inflation-targeting period. However, measures have been heavily impacted by COVID disruptions, making identifying shifts in underlying trends extremely difficult, particularly for what was already a volatile measure. Productivity and unit labour cost updates are only available quarterly with the national accounts figures on GDP. Going by the Governor’s testimony, it could take several quarters for a definitive shift to emerge.

Assessing the extent to which productivity is normalising and the rate of inflation in the ‘cost base’ of the economy is easing will clearly not be easy – inflation updates may well give more clues before the productivity data does. These uncertain and slow dynamics will make it difficult to make a case for further policy tightening. Instead, the main implications from ‘unit labour cost’ risks are likely to be for the timing and extent to which the RBA can ease policy. We expect scope for easing to emerge in the second half of 2024 with a rate cut cycle beginning in the September quarter. But that scope could be challenged if unit labour cost growth looks likely staying well above the 2.5%yr pace seen in the past.

For now, however, the main message is still of an RBA that is comfortable with policy settings as they are, more confident of achieving the ‘narrow path’ back to low inflation over a reasonable timeframe without doing too much damage along the way in terms of unemployment, and sees the requirement for further policy tightening as a ‘possibility’ but as part of a more balanced range of risks. Next week’s wage and labour force updates will be important, as will the monthly CPI indicator release later in the month but given the high hurdle for any further rate increases another ‘on hold’ decision at the RBA’s September meeting looks very likely at this stage.

US Inflation Data Sent Bond Yields Higher

Market movers today

On the macro data front, the focus remains on inflation signals. The US July PPI is expected to reflect yesterday's modest CPI print, growing 0.2% m/m both in headline and core terms. We will also keep an eye out for the University of Michigan's flash August consumer survey, and especially the short-term inflation expectations, which have been on a declining trend this year.

From the UK, the preliminary Q2 GDP estimate is due for release, consensus expects that growth has stopped completely in q/q terms after already weak Q1 (+0.1%).

The 60 second overview

US July CPI came out slightly below expectations with headline at 0.17% m/m (consensus 0.2%) and core at 0.16% m/m (consensus 0.2%). The modest downside surprise was driven by sharper-than-expected deflation in core goods prices (-0.33% m/m; June -0.05%), while our preferred measure for underlying inflation, core services ex. shelter and health care, accelerated after a very low June print (0.45% m/m; June 0.13%). As the Fed focuses more on the services prices, UST yields eventually ended the day higher despite another low core CPI print. But overall, the figures illustrated that broader US price pressures have continued to ease over summer, and while tight labour market remains an upside risk for inflation, we think the latest data generally supports our view that the Fed is already done hiking rates for now.

This morning, there has been modest movements in the Asian market, but the US Treasury market in Asian trade is closed today due to a holiday in Japan.

Oil and gas prices continue to be elevated as the oil price is close to the level seen in early 2023. The gas price has rebounded modestly, but still well above the level before the spike earlier this week.

Equities: Global equities were higher yesterday as US CPI data came in very close to expectation. Simply the fact of inflation coming in as expected should be seen as a positive sign after the extreme inflation surprises we have been witnessing the last 2½ years. No big surprise to see the cyclicals beating defensive and banks/financials doing good with the soft-landing scenario getting some more traction. Growth outperformed value despite yields ending higher, and we are still not back in the more or less 100% yields-dictated rotation between value and growth. In the US, Dow +0.2%, S&P 500 +0.03%, Nasdaq +0.1% and Russell 2000 -0.4%.

Asians markets mostly lower this morning with Japan being closed. European futures are lower while US once are flat.

FI: Global bond yields rose even though the US inflation data suggest that the Federal Reserve will be on hold at the next meeting, but with comments from Federal Reserve's Mary Daly that inflation is moving the right way, but there is still more work to be done. Hence, the 10Y US government bond yield rose some 10bp and the curve steepened between 2Y and 10Y with 5-6bp.

The spread between 10Y Italy and German government bond tightened another few bp and we are now close to the 150bp level. The Schatz ASW-spread has tightened modestly after the big jump earlier this week. Hence, we are once again seeing a stabilisation in the German ASW-spreads.

FX: The US CPI numbers prompted a knee-jerk yet modest 'risk on' reaction in FX space, however this was soon over and reversed. Instead, the dollar had a strong US session alongside higher US rates where NOK was the currency within G10 that took the hardest hit: USD/NOK rose a massive 20 figures to 10.30 whereas USD/SEK advanced 10 figures to 10.70. USD/JPY was up 100 pips and almost pierced 145. Stable markets overnight.

Credit: Credit markets were clearly positive yesterday following the US CPI announcement with iTraxx Main going 2bp tighter to 71bp while Xover tightened by 11bp to 396bp. In addition, primary market activity is gradually picking up steam. An example of good investor appetite was seen when SEB priced a EUR500m 10NC5 Tier 2 instrument at MS+190bp, travelling from IPT of MS+210bp area with books above EUR1bn.

Is China on Path for Longer Economic Stagnation?

Released yesterday, the latest CPI data showed that the headline inflation in the US ticked higher from 3 to 3.2%. That was slightly lower than the 3.3% penciled in by analysts, core inflation eased to 4.7% in July from 4.8% expected by analysts and printed a month earlier.

But the rising energy and crop prices threaten to heat things up in the coming months and inflation’s downward trajectory could rapidly be spoiled. That’s certainly why an increasing number of investors and the Federal Reserve’s (Fed) Mary Daly warned that this was ‘not a data point that says victory is ours’.

And indeed, looking into details, the fact that the 20% fall in gasoline prices is what explains the decline in headline number is concerning. The barrel of US crude bounced lower yesterday after a 27% rally since the end of June, and the latest OPEC data indicated that we would see a sharp supply deficit of more than 2mbpd this quarter as Saudi cuts output to push prices higher. And this gap could further widen as global demand continues growing and shift to alternative energy sources is nowhere fast enough to reverse that upside pressure.

On the other hand, we also know that the rising energy prices fuel inflation expectations and further rate hikes expectations around the world. And that means that oil bears are certainly waiting in ambush to start trading the recession narrative and sell the top. The $85pb could be the level that could trigger that downside correction despite the evidence of tightening supply and increasing gap between rising demand and falling supply.

Today, eyes will be on the July PPI figures before the weekly closing bell, where core PPI is seen further easing, but headline PPI may have ticked higher to 0.7% on monthly basis, probably on higher energy, crop and food prices.

In the market

Yesterday’s slightly softer-than-expected inflation numbers and the initial jobless claims which printed almost 250K new applications last week - the highest in a month - sent the probability of a September pause to above 90%, though the US 2-year yield advanced past the 4.85% level, and the longer-terms yields rose with a weak 30-year bond action, which saw the highest yield since 2011.

Major stock indices stagnated. The S&P500 was up by only 0.03% yesterday while Nasdaq 100 closed 0.18% higher, as Walt Disney rallied as much as 5% even though Disney+ missed subscription estimates and said that it will increase the price of the streaming service. Disney is considering a crackdown on password sharing, which, combined with higher prices could lead to a Netflix-like profit jump further down the road.

In the FX

The USD index consolidates above the 50 and 100-DMAs and just below a long-term ascending channel base. The EURUSD sees support at the 50-DMA, near the 1.0960 level, and could benefit from further weakness in the US dollar to attempt another rise above the 1.10 mark.

European nat gas futures fell 7% yesterday after a 28% spiked on Wednesday on concerns that strikes at major export facilities in Australia could lead to a 10% decline in global LNG exports. Yet, the European inventories are about 88% full on average and the industrial demand remains weak due to tightening financial conditions imposed by the European Central Bank (ECB) hikes. Therefore this week’s massive move seems to be mostly overdone, and we shall see some more downside correction.

Chinese property market is boiling

The property crisis in China is being fueled by a potential default of Country Garden, which is one of the biggest property companies in China and which recently announced that it may have lost up to $7.6bn in the first half of the year as home sales slumped and the government stimulus measures didn’t bring buyers back to the market. Equities in China slumped further today, as property crisis is not benign. In fact, China’s local governments have plenty of debt, and their major source of income is… land and property sales. Consequently, the property crisis explodes local governments’ debt to income ratios- And the debt burden prevents China from rolling out stimulus measures that they would’ve otherwise, because the government doesn’t want to further blast the debt levels.

Shattered investor and consumer confidence, shrinking demographics, property crisis and deflation hints that the Chinese economy could be on path for a longer period of economic stagnation. We could therefore see rapid pullback in investor optimism regarding stimulus measures and their effectiveness. Hang Seng’s tech index fell to the lowest levels in two weeks yesterday, as all members fell except for Alibaba which jumped after beating revenue estimates last quarter.

RBA Lowe: Possible that some further tightening will be required

Addressing the House of Representatives Standing Committee on Economics today, outgoing RBA Governor, Philip Lowe Lowe stated that the purpose behind the pauses in July and August was "to provide time to assess the impact of the (rates) increases to date and the economic outlook and the associated risks."

He reiterated that "it is possible that some further tightening of monetary policy will be required". But the decision would be largely based on incoming data and the Board's evolving analysis of economic forecast and potential risks.

Lowe expressed optimism about recent economic data, remarking, "It is encouraging that the recent data are consistent with inflation returning to target over the next couple of years."

But he also pinpointed two risks that RBA is closely monitoring. "The first is the outlook for household consumption," he said, attributing this concern to the myriad of factors currently influencing household finances and expenditures.

The second risk highlighted was the potential persistence of high services price inflation which could lead to "prolonging the period of inflation being above target."

Lowe emphasized the RBA's forecast, which assumes a resurgence in productivity rates, aligning with levels seen pre-pandemic. Such growth, he suggested, would help in moderating the unit labour costs and subsequently, inflation. Yet, he cautioned, "If this pick-up in productivity does not occur, all else constant, high inflation is likely to persist, which would be problematic."

New Zealand BNZ manufacturing slumps to Post-GFC low in July

New Zealand's BusinessNZ Performance of Manufacturing Index has experienced a drop in July, declining from 47.4 to 46.3. Digging into the details, there was a notable dip in Production, which plummeted from 47.3 to 42.9, and Employment wasn't far behind, decreasing from 46.8 to 44.3. On a slightly brighter note, New Orders saw a modest increase, moving from 43.8 to 45.0, and Finished Stocks slightly ticked up from 52.3 to 52.6. However, Deliveries took a sharp hit, falling from 49.9 to 42.3.

Feedback from the manufacturing sector portrayed a gloomy picture. Negative comments in July stood at 72%, a slight decrease from June's 74.5%, but higher than May's 66.7% and April's 70.3%. The core concerns cited by manufacturers revolved around general market uncertainty, escalating costs, and inclement weather affecting demand, particularly during July.

Catherine Beard, BusinessNZ's Director of Advocacy, remarked on the PMI's July figures, indicating that they "showed very little signs of potential improvements for the sector as a whole." Echoing this sentiment, BNZ Senior Economist, Doug Steel, highlighted the gravity of the situation, noting that "the July result was the fifth consecutive monthly sub-50 reading and, outside of Covid lockdown periods, the lowest reading since the GFC days back in June 2009."

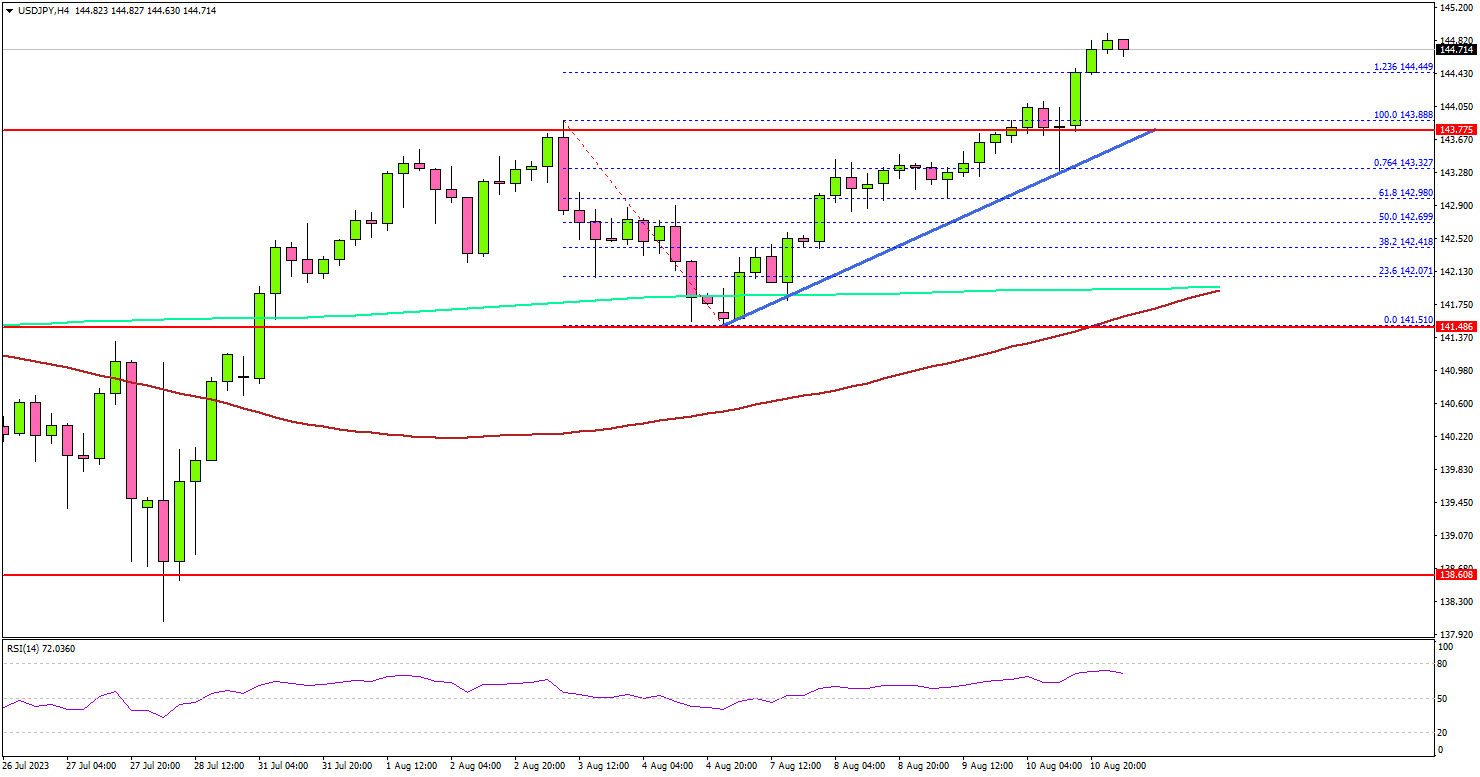

USD/JPY Extends Rally, Can It Reach 150?

Key Highlights

- USD/JPY is rising above the 142.00 resistance.

- A connecting bullish trend line is forming with support near 143.80 on the 4-hour chart.

- EUR/USD is recovering losses and trading well above 1.0950.

- Crude oil prices are struggling to surpass $85.

USD/JPY Technical Analysis

The US Dollar started a fresh increase above the 140.00 pivot level against the Japanese Yen. USD/JPY broke the 142.50 resistance to enter further into a positive zone.

Looking at the 4-hour chart, the pair settled above the 142.50 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

There was also a spike above the 144.00 level. The pair traded to a new multi-week high and might extend gains above the 145.00 level. The next major resistance is near the 146.20 level. A close above the 146.20 resistance could push the pair toward 148.00. Any more gains could start a fresh increase toward the 150.00 level.

Initial support is near the 143.80 level. There is also a connecting bullish trend line forming with support near 143.80 on the same chart.

The next major support is near 143.00, below which USD/JPY could gain bearish momentum. In the stated case, the pair could test the 142.00 support.

Looking at EUR/USD, the pair started an upside correction and was able to clear the 1.1000 resistance zone.

Economic Releases

- UK GDP for Q2 2023 (Preliminary) (QoQ) - Forecast 0%, versus +0.1% previous.

- UK Industrial Production for June 2023 (MoM) - Forecast +0.1%, versus -0.6% previous.

- UK Manufacturing Production for June 2023 (MoM) - Forecast +0.2%, versus -0.2% previous.

Fed’s Daly on CPI: Not a Victory Yet

San Francisco Fed President, Mary Daly, offered a measured response to yesterday's US CPI release, stating that while the figures "came in largely as expected, and that is good news," it does not signify a comprehensive victory over the ongoing inflation challenges. "It is not a data point that says victory is ours," Daly warned.

Highlighting the nuanced nature of the current inflation landscape, Daly noted the decrease in goods inflation and indicated promising trends in housing. However, her main concern lies with core services inflation that excludes housing.

Despite the general trend of receding inflation, core services inflation remains stubborn. Daly emphasized, "We do need to see that come back to prepandemic levels if we're going to be confident that we can get to 2% on a sustainable basis."

Offering insight into Fed's future strategy, Daly was cautious: "Whether we raise another time, or hold rates steady for a longer period -- those things are yet to be determined."

She stressed the importance of upcoming data before Fed's next meeting, suggesting it would play a critical role in shaping decisions. "It would be premature to project what I think would happen because there's a lot of information coming in between now and our next meeting" in September, she added.