Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.09; (P) 141.88; (R1) 143.07; More...

USD/JPY's rally from 137.22 continues today and intraday bias stays on the upside for retesting 145.60 resistance first. Decisive break there will resume whole rally from 172.20. Next target is 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76. On the downside, below 141.99 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

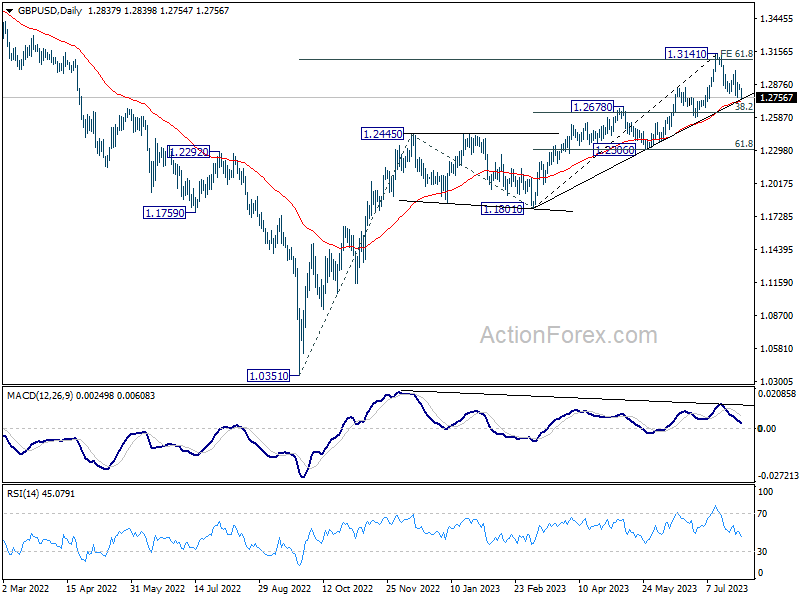

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2818; (P) 1.2845; (R1) 1.2863; More...

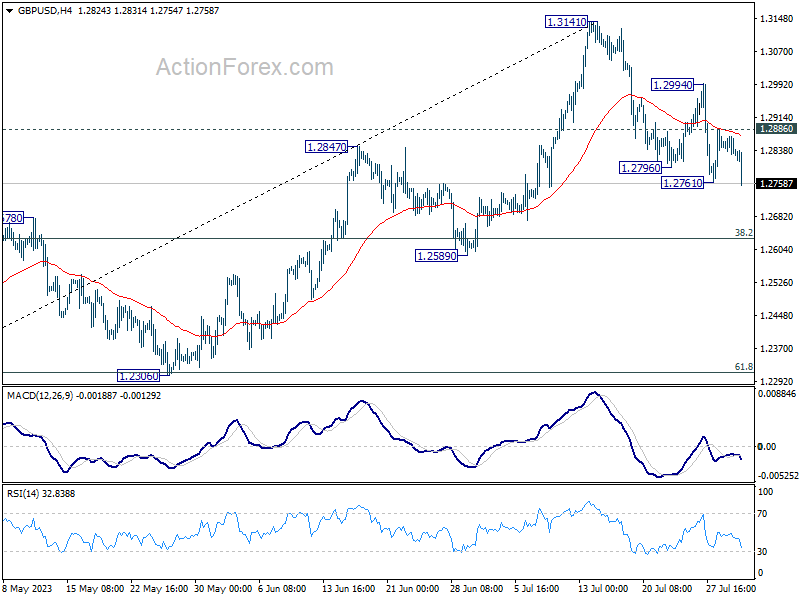

GBP/USD's breach of 1.2761 temporary low indicates resumption of fall from 1.3141. Intraday bias is back on the downside for 38.2% retracement of 1.1801 to 1.3141 at 1.2629, as a correction to rise from 1.1801. On the upside, above 1.2886 minor resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise from 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal.

Dollar Rising With Treasury Yields, Aussie Selloff Gains Momentum

Dollar rises broadly today, in the first trading day of August. The greenback is bolstered by mild risk aversion and rallying US yields. Meanwhile, traders are also probably starting to position ahead of the heavy weight data this week. However, the greenback is stuck below last week's high against Euro so far. Firm break there this resistance is needed to solidify upside momentum of Dollar.

Australian Dollar's decline gained pace in a slightly delayed reaction to RBA's decision to hold interest rates earlier today. As market analysts dissect and digest the statement, some are beginning to predict a prolonged pause from the Australian central bank, leading to an acceleration in Aussie's sell-off. New Zealand Dollar and Canadian Dollar are the next weakest currencies for the moment, with the Japanese Yen also underperforming, except against the Dollar.

Technically, while US 10-year yield reclaims 4% handle today, it's still kept below last week's high. More importantly, 4.091 resistance is the key level to overcome for the near term. TNX would just engage in sideway trading in a narrowing range until this resistance is broken decisively. However, firm break of 4.091 would set the stage for further rally to retest 4.333 high, possibly in rather quick manner, and give much support to extend Dollar's near term rise. Let's see if this week's data from the US would trigger the move.

In Europe, at the time of writing, FTSE is down -0.32%. DAX is down -0.92%. CAC is down -0.92%. Germany 10-year yield is up 0.048 at 2.540. Earlier in Asia, Nikkei rose 0.92%. Hong Kong HSI dropped -0.34%. China Shanghai SSE dropped -0.00%. Singapore Strait Times dropped -0.01%. Japan 10-year JGB yield dropped -0.0090 to 0.594.

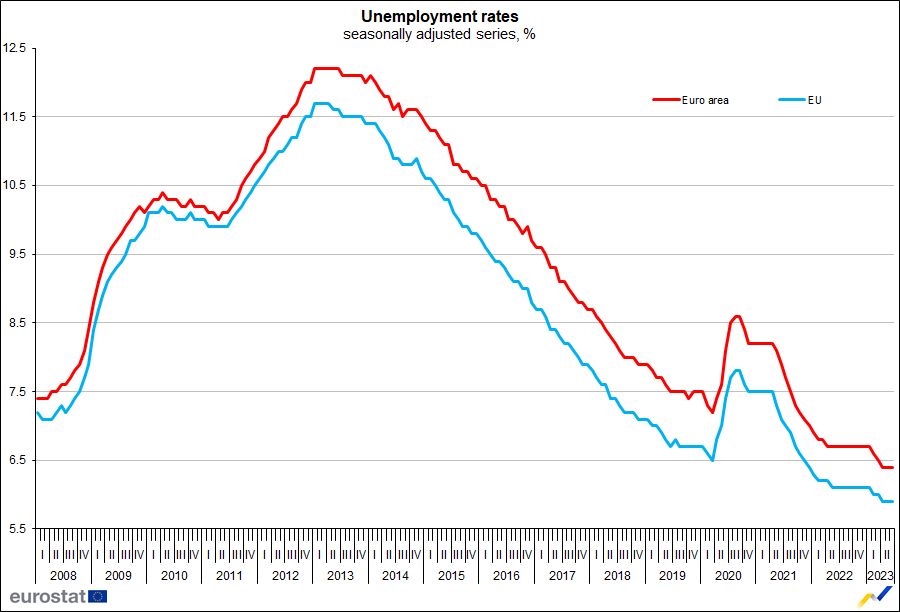

Eurozone unemployment rate unchanged at 6.4%, EU at 5.9%

In June, unemployment rates in both Eurozone the EU remained stable at 6.4% and 5.9% respectively, according to Eurostat data.

Eurostat estimated that as of June 2023, around 12.802m individuals in the EU were unemployed, 10.814m of whom are from Eurozone.

Despite the unchanged monthly figures, the unemployment rate has seen a year-on-year decrease. Compared with June 2022, unemployment decreased by -387k in the EU and by -441k in Eurozone.

Eurozone PMI manufacturing finalized at 42.7, manufacturing recession is here to...

Eurozone PMI Manufacturing was finalized at 42.7 in July, down from June's 43.4, marking a 38-month low. PMI Manufacturing Output correspondingly dipped to 42.7 from 44.2, signaling another 38-month low.

Among member states, Greece's PMI Manufacturing showed a promising uptick to 53.5, a 14-month high, whereas Germany and Austria both posted a dismal 38-month low at 38.8. France also hit 38-month low at 45.1. Other states exhibited mixed results, with Spain hitting a 7-month low at 47.8, and Italy experiencing a modest 2-month high at 44.5.

Commenting on these figures, Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated: "It looks like the manufacturing recession is here to stay in the eurozone. Stronger declines in output, new orders and purchase volumes at the start of the third quarter back up our view that the economy as a whole is in for a bumpy ride in the second half of the year."

de la Rubia also noted ECB's reaction to deflation of output prices, which have quickened their decline, falling at the fastest pace in nearly 14 years. However, he cautioned that "the worries about services inflation remain high on the agenda."

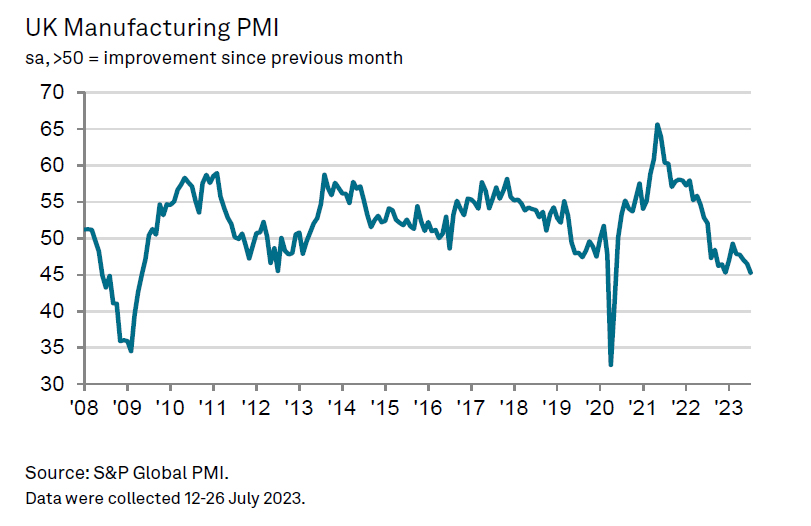

UK PMI manufacturing finalized at 45.3, deepening downturn

UK PMI Manufacturing was finalized at 45.3 in July. This level, matching the joint-weakest performance since May 2020, signals an ongoing deterioration in operating conditions, with PMI remaining below the pivotal 50.0 threshold for the twelfth consecutive month.

"July saw a deepening of the UK's manufacturing downturn," noted Rob Dobson, Director at S&P Global Market Intelligence. He attributed the slump to a combination of factors including overstocked clients, escalating export losses, rising interest rates, and the ongoing cost-of-living crisis.

Dobson also highlighted falling domestic and export demand and rapidly declining backlogs of work as precursors to potential cutbacks in production, employment, and purchasing in the near future. While falling prices offer some relief from inflation, he warned that they could signify more trouble ahead for manufacturers' profits and subsequent investment.

RBA on hold, keeps tightening bias

RBA kept its cash rate target at 4.10%, retaining a hawkish bias. The bank noted, "Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe." However, RBA underscored that any future decision will be data-dependent and based on an "evolving assessment of risks."

Explaining the decision to hold rates, RBA stated that "higher interest rates are working to establish a more sustainable balance between supply and demand in the economy and will continue to do so." Amidst "uncertainty" surrounding the economic outlook, maintaining the current rate provides "further time" to assess the impact of previous hikes.

While the central bank anticipates recent data to be "consistent" with an inflation return to its 2-3% target over the forecast horizon, it warned of "significant uncertainties".

RBA expressed concerns about the surprising persistence of services price inflation overseas, which could potentially reflect in Australia. Additionally, it mentioned uncertainties about "how firms' pricing decisions and wages will respond to the slowing in the economy at a time when the labour market remains tight." Also, it stated that "the outlook for household consumption is also an ongoing source of uncertainty."

Japan PMI manufacturing finalized at 49.6, but business optimism elevated

Japan PMI Manufacturing was finalized at 49.6 in July, down from June's 49.8. That also marked the second month of concurrent decline in output and new orders. Usamah Bhatti at S&P Global Market Intelligence highlighted the significant role of "quicker deterioration in new order inflows" and also "sustained" decline in production.

Despite these struggles, inflationary pressures showed signs of abating as the rate of input cost inflation was the slowest since February 2021. However, selling price inflation was "unchanged" and "sharp overall" as Japanese manufacturers passed on a portion of higher cost burdens to clients.

The industry displayed robust optimism about the future, with the second-highest positive sentiment recorded in the last 18 months, driven by expectations of a boost in domestic and international demand owing to new product launches and the ongoing mitigation of COVID-19 and inflation-related influences.

China Caixin PMI manufacturing down to 49.2, first contraction in three months

China's Caixin PMI Manufacturing index slipped from 50.5 to 49.2 in July, marking the first contraction in three months and falling below the expected 50.3. According to Caixin, there was a marginal contraction in output, and total sales plummeted due to a more pronounced decline in new export orders. Additionally, both input costs and output charges saw a decrease.

Senior Economist at Caixin Insight Group, Wang Zhe, highlighted the deteriorating situation, stating, "Overall, manufacturing conditions contracted in July, with supply, demand, exports, and employment all deteriorating. Prices continued to decline, inventories rose without companies adjusting them, and logistics times increased." He noted that manufacturers' optimism remained, but it had weakened.

Wang further explained, "China's economic recovery in the first quarter exceeded expectations, but the momentum weakened in the second. Although the data for industrial production and investment in June showed some signs of recovery, macroeconomic growth remained sluggish, and considerable downward pressure on the economy persisted."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2818; (P) 1.2845; (R1) 1.2863; More...

GBP/USD's breach of 1.2761 temporary low indicates resumption of fall from 1.3141. Intraday bias is back on the downside for 38.2% retracement of 1.1801 to 1.3141 at 1.2629, as a correction to rise from 1.1801. On the upside, above 1.2886 minor resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise from 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | 3.50% | -2.20% | -2.30% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | 7.60% | 8.40% | ||

| 23:30 | JPY | Unemployment Rate Jun | 2.50% | 2.60% | 2.60% | |

| 00:30 | JPY | Manufacturing PMI Jul F | 49.6 | 49.4 | 49.4 | |

| 01:30 | AUD | Building Permits M/M Jun | -7.70% | -7.90% | 20.60% | |

| 01:45 | CNY | Caixin Manufacturing PMI Jul | 49.2 | 50.3 | 50.5 | |

| 04:30 | AUD | RBA Interest Rate Decision | 4.10% | 4.35% | 4.10% | |

| 07:45 | EUR | Italy Manufacturing PMI Jul | 44.5 | 43.9 | 43.8 | |

| 07:50 | EUR | France Manufacturing PMI Jul F | 45.1 | 44.5 | 44.5 | |

| 07:55 | EUR | Germany Unemployment Change Jun | -4K | 15K | 28K | |

| 07:55 | EUR | Germany Unemployment Rate Jun | 5.60% | 5.70% | 5.70% | |

| 07:55 | EUR | Germany Manufacturing PMI Jul F | 38.8 | 38.8 | 38.8 | |

| 08:00 | EUR | Italy Unemployment Rate Jun | 7.40% | 7.70% | 7.60% | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | 42.7 | 42.7 | 42.7 | |

| 08:30 | GBP | Manufacturing PMI Jul F | 45.3 | 45 | 45 | |

| 09:00 | EUR | Eurozone Unemployment Rate Jun | 6.40% | 6.50% | 6.50% | 6.40% |

| 13:30 | CAD | Manufacturing PMI Jul | 48.9 | 48.8 | ||

| 13:45 | USD | Manufacturing PMI Jul F | 49 | 49 | ||

| 14:00 | USD | ISM Manufacturing PMI Jul | 46.5 | 46 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jul | 42.3 | 48.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | 41.8 | |||

| 14:00 | USD | Construction Spending M/M Jun | 0.60% | 0.90% |

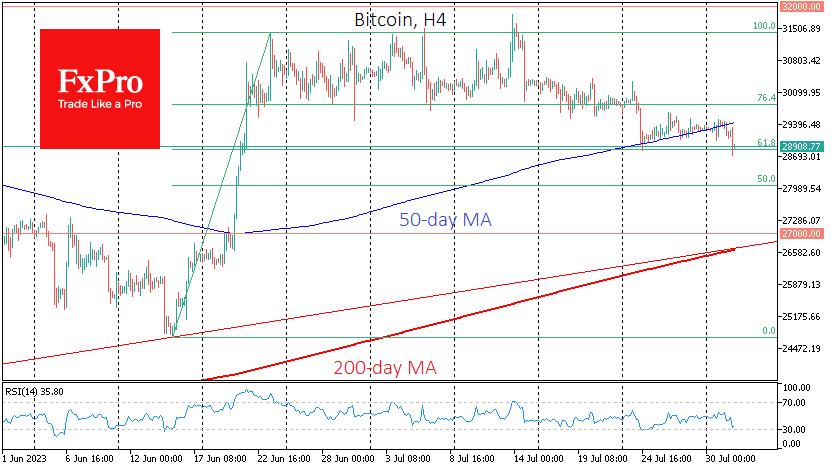

A New Round of Crypto Market Mistrust

Market picture

The crypto market has been selling off since Tuesday morning, losing 1.7% to 1.17 trillion in 24h. Bitcoin is down 1.6%, Ethereum is down 1.75%, while the top altcoins are losing between 0.9% for BNB and 3.7% for Solana.

The reason for the pressure is the collapse of Curve (CRV) amid a possible liquidation of the position of the company’s founder, who pledged CRV to buy USDT. However, the story impacts the broader altcoin market and reduces confidence in the sector.

The risk-off pull mode has further clouded Bitcoin’s technical picture. After bouncing back to $28.8K, BTCUSD took a step back from the 50-day moving average, which has been acting as support since last Monday. Without any sudden positive news, the main scenario is a decline to $28K (50% of June’s upside amplitude). However, it is more likely that no significant demand will emerge at this level and that the price will retreat to $27,000, the lower boundary of the rising channel from November, where the 200-day average is passing.

In terms of seasonality, August is considered unfavourable for BTC. Over the past 11 years, bitcoin has only ended the month higher five times and lower seven times. The average gain was 26%, and the average loss was 16%.

News background

According to CoinShares, investments in crypto funds fell by $21 million last week, the second week of outflows after four weeks of active investment. Bitcoin investments decreased by $19 million, and Ethereum investments by $2 million.

George Milling-Stanley, chief gold investment strategist at State Street Global Advisors, says Bitcoin cannot be called a substitute for gold because of the risk of significant losses.

The SEC has sued Richard Hart, founder of HEX, PulseChain and PulseX, for allegedly selling unregistered securities. According to the SEC, the businessman has raised over $1 billion through token sales of the three projects since 2019.

CoinGecko published a study showing the banking sector’s growing interest in the crypto market. Over half of the top 50 banks already use exchanges to buy Bitcoin and other crypto assets.

Bendigo Bank, one of Australia’s largest banks, has banned its customers from transferring funds to crypto exchanges to protect them from the risks of fraud and scams.

Australian Dollar Takes a Tumble as RBA Pauses

- RBA pauses rates

- Australian dollar slides 1.3%

- ISM Manufacturing PMI expected to remain in negative territory

The Australian dollar continues to swing wildly this week. In Tuesday’s European session, AUD/USD is trading at 0.6630, down 1.30%. On Monday, AUD/USD jumped 1% higher.

RBA pauses rates, as expected

There were no surprises from the Reserve Bank of Australia, which paused for a second straight month and maintained the cast rate at 4.10%. The money markets had priced in a pause but the Australian dollar still took a nosedive after the decision, as the money markets have lowered the probability of a rate hike in September to below 20%.

Recent key data showed that the Australian economy has cooled off, with inflation easing in the second quarter and retail sales for June falling by 0.8%. These numbers provided support for the RBA to take a pause at today’s meeting. Still, the argument can be made that with inflation at 6%, double the upper band of the RBA’s target range, there is room for further rate hikes. The RBA did not change its inflation outlook, predicting that inflation would not return to the 2%-3% target range before late 2025. Services inflation, which includes rising rent prices, remains sticky and this is a key concern for the central bank.

Governor Lowe’s rate statement said that future rate decisions “will depend upon the data and the evolving assessment of risks.” This is a reminder that inflation and employment reports will play a key role in determining the RBA’s rate path. There is speculation that the RBA is done with tightening, but with inflation still at high levels, Lowe’s message to the markets was that further hikes remain on the table.

In the US, today’s key event is ISM Manufacturing PMI. The manufacturing sector remains in the doldrums and has been in decline since October, with readings below the 50.0 level. In June, the Manufacturing PMI slipped to 46.0, the lowest level since May 2020. Another decline is expected for July, with a consensus estimate of 46.8 points.

AUD/USD Technical

- AUD/USD has pushed below support at 0.6697. Below, there is resistance at 0.6573

- There is resistance at 0.6771 and 0.6875

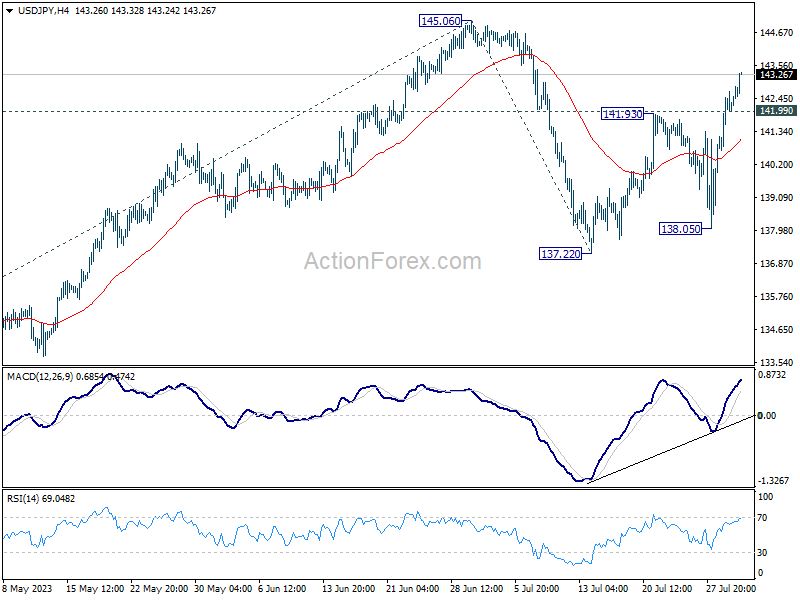

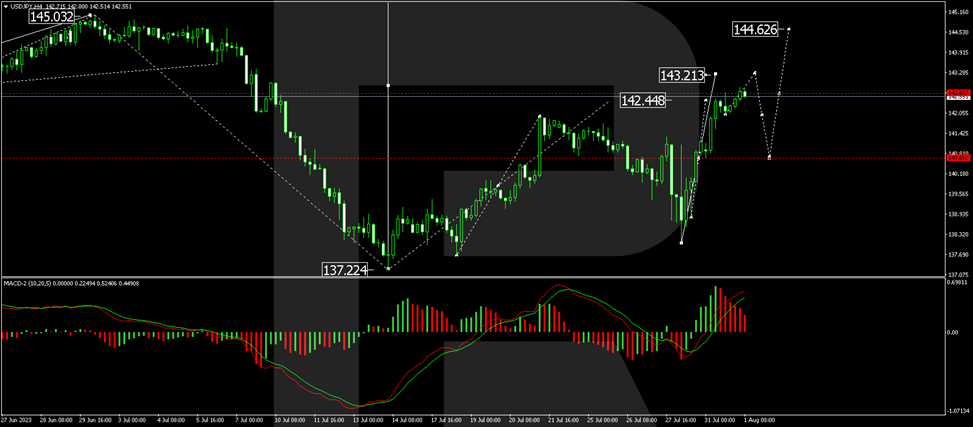

Japanese Yen Depreciated After the Bank of Japan Meeting Outcome

The USD/JPY pair surpassed its local daily high of 141.95 on Monday and is currently trading near 143.00.

USD/JPY experienced increased volatility at the end of last week: it initially fell by about 2% on the Nikkei news report that the Bank of Japan (BOJ) might announce the beginning of normalising its "soft" monetary policy but then returned to the area of daily highs after the Bank of Japan announced the meeting outcome.

The BOJ kept the interest rate at -0.1% and did not raise the upper bound of yield on 10-year Japanese government bonds. In its issued statement, it noted that this limit is not a "dogma" but merely a reference serving as a guide to action.

As a result, the expectations of the Bank of Japan winding down its "soft" monetary policy due to rapidly rising inflation have not been confirmed yet. According to Bloomberg surveys, many economists and analysts expect the Bank of Japan to begin normalising monetary policy no earlier than October.

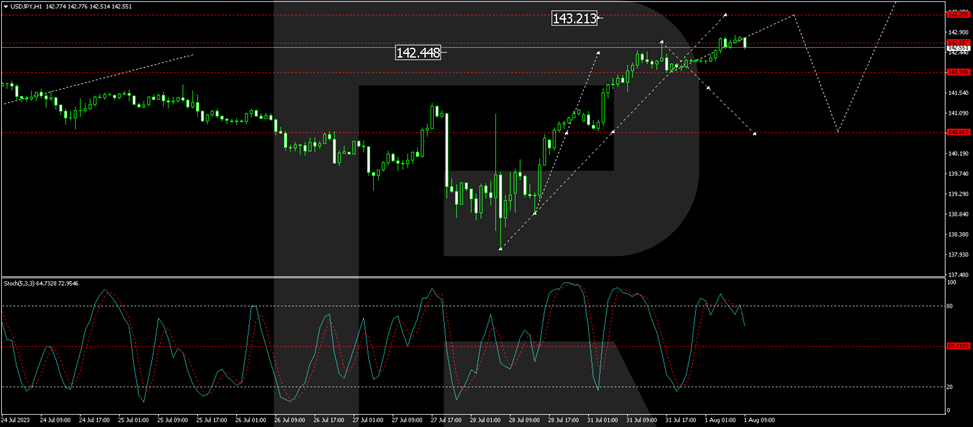

Technical analysis of the USD/JPY currency pair

On the H4 chart of USD/JPY, the calculated target for the fifth upward wave has been reached at 142.44. Today, the market is forming a consolidation range around this level. An expansion to 143.21 is not ruled out. Next, we will consider a decline to the level of 140.66, followed by a rise to 144.62. Technically, this scenario is confirmed by the MACD oscillator. Its signal line is trading above the zero mark and has exited the histogram zone. We expect the indicator to begin decreasing towards the zero level.

On the H1 chart of USD/JPY, a consolidation range has formed around the level of 140.66. After breaking above this range, the local target at 142.44 was achieved. Currently, the market is forming a consolidation range around this level. A potential upward move to the level of 143.23 is not excluded if there is a breakout above this range. In case of a downward breakout, we will assess the probability of a correction to 140.66, followed by a rise to 143.28. Technically, this scenario is supported by the Stochastic oscillator, with its signal line above the 80 mark, preparing to decline towards the 50 mark. After this anticipated decline, we expect another upward movement towards the 80 mark.

Eurozone unemployment rate unchanged at 6.4%, EU at 5.9%

In June, unemployment rates in both Eurozone the EU remained stable at 6.4% and 5.9% respectively, according to Eurostat data.

Eurostat estimated that as of June 2023, around 12.802m individuals in the EU were unemployed, 10.814m of whom are from Eurozone.

Despite the unchanged monthly figures, the unemployment rate has seen a year-on-year decrease. Compared with June 2022, unemployment decreased by -387k in the EU and by -441k in Eurozone.

UK PMI manufacturing finalized at 45.3, deepening downturn

UK PMI Manufacturing was finalized at 45.3 in July. This level, matching the joint-weakest performance since May 2020, signals an ongoing deterioration in operating conditions, with PMI remaining below the pivotal 50.0 threshold for the twelfth consecutive month.

"July saw a deepening of the UK's manufacturing downturn," noted Rob Dobson, Director at S&P Global Market Intelligence. He attributed the slump to a combination of factors including overstocked clients, escalating export losses, rising interest rates, and the ongoing cost-of-living crisis.

Dobson also highlighted falling domestic and export demand and rapidly declining backlogs of work as precursors to potential cutbacks in production, employment, and purchasing in the near future. While falling prices offer some relief from inflation, he warned that they could signify more trouble ahead for manufacturers' profits and subsequent investment.

Australian Dollar Plummeting After RBA Decision

The Reserve Bank of Australia (RBA) this morning decided to leave the interest rate at 4.10%, although market participants expected an increase to 4.35%.

According to the forecast of the central bank, inflation in Australia will return to its target range of 2-3% by the end of 2025 from the current 6%. At the same time, a warning was made that additional tightening (rate increase) may be required to curb inflation.

Amid the RBA's decision, the Australian dollar weakened against other currencies. So, on the AUD/USD chart, the price fell below the level of 0.665. At the same time, a reversal was formed from the median line of the channel, shown in blue; at yesterday's maximum, it was tested as a resistance line.

If the downward movement on the AUD/USD pair caused by the RBA decision continues, then the market may find support:

- at the level of 0.6624 – where important July lows were formed;

- at the level of 0.66 – there are important June lows;

- near the lower border of the blue channel.

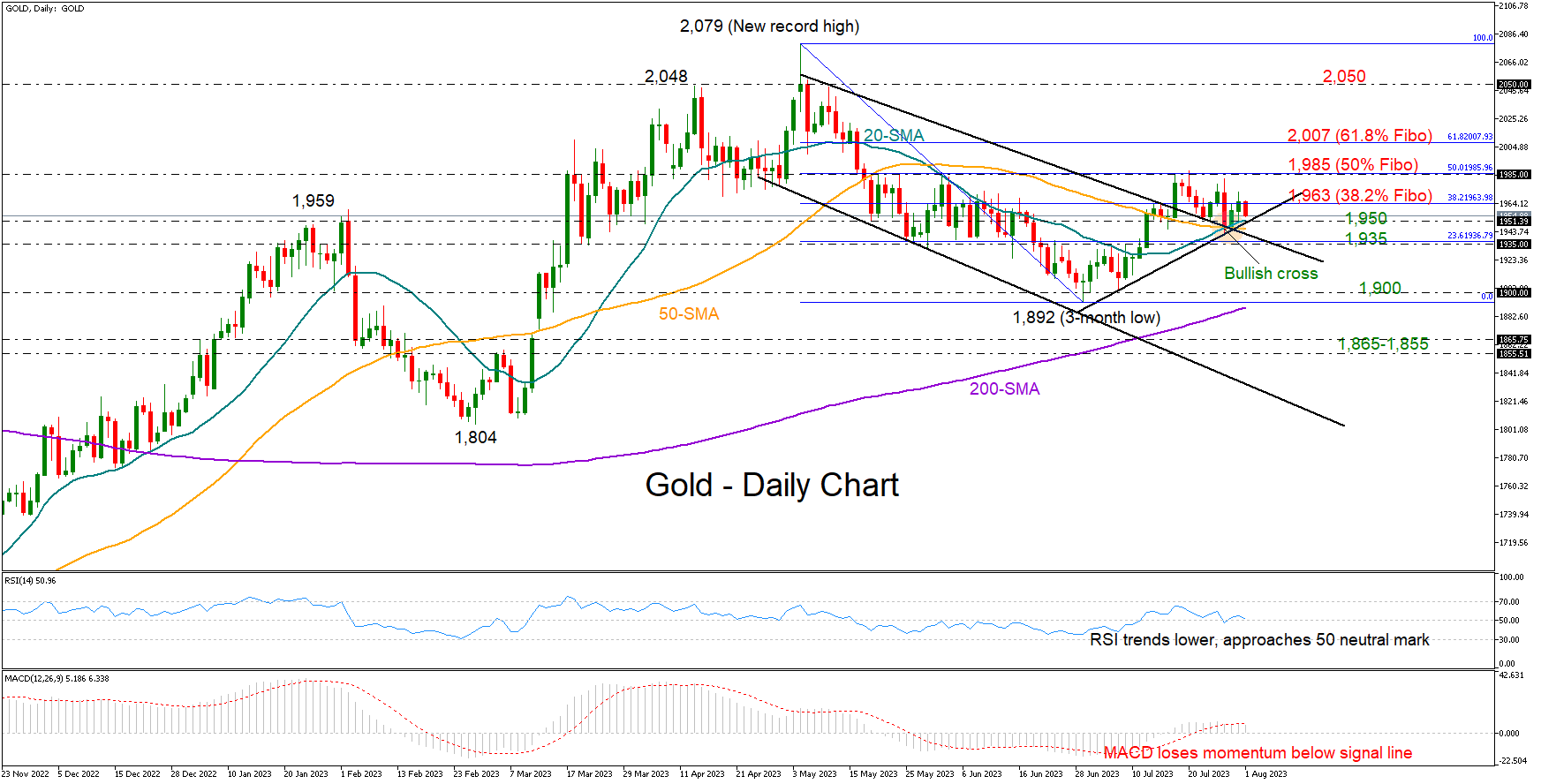

Gold Has a Good Support Zone But Patience Needed

Gold has been forming lower lows and lower highs over the past two weeks, with the 50-day simple moving average (SMA) preventing major declines once again along with the 20-day SMA near 1,945 last Friday.

The price maintained its position above the broken bearish channel, which is a good sign for July's upleg continuation. The progressing bullish cross between the 20- and 50-day SMAs is endorsing that case as well. Yet, the negative trajectory in the RSI and the MACD is reflecting some persisting weakness in demand.

Traders are waiting for the price to go above 1,985 and beyond the 50% Fibonacci retracement of the previous downleg before focusing on 2,000. If the bulls claim the latter, the price could accelerate towards the 2,050 bar and perhaps attempt to touch the record high of 2,079.

On the downside, the area of 1,935-1,950, which encapsulates the shorter-term SMAs, the tentative ascending trendline from June’s lows and the channel’s upper band, will be closely watched. The 38.2% Fibonacci mark is placed there too. Therefore, a downfall below that region could motivate an aggressive sell-off towards the 1,892-1,900 zone, where the 200-day SMA is converging. A deeper fall could take a halt somewhere between 1,865 and 1,855.

All in all, gold is currently showing mixed signals, with investors expected to stay patient until the price crosses above 1,985 or slides below 1,935-1,950.