Sample Category Title

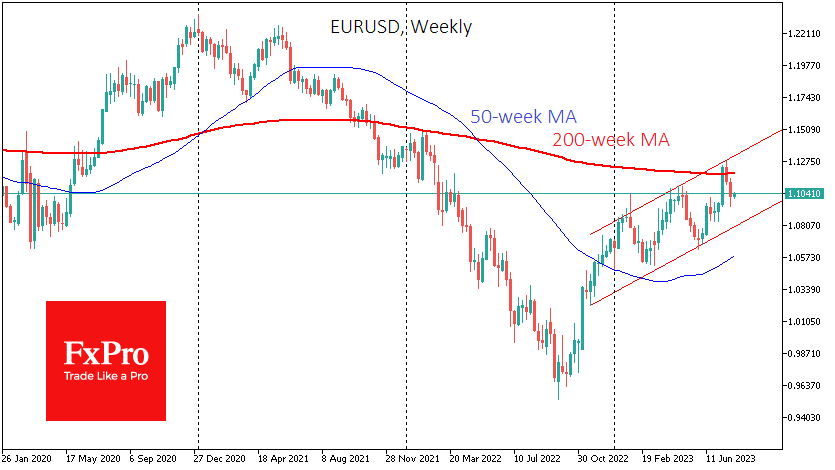

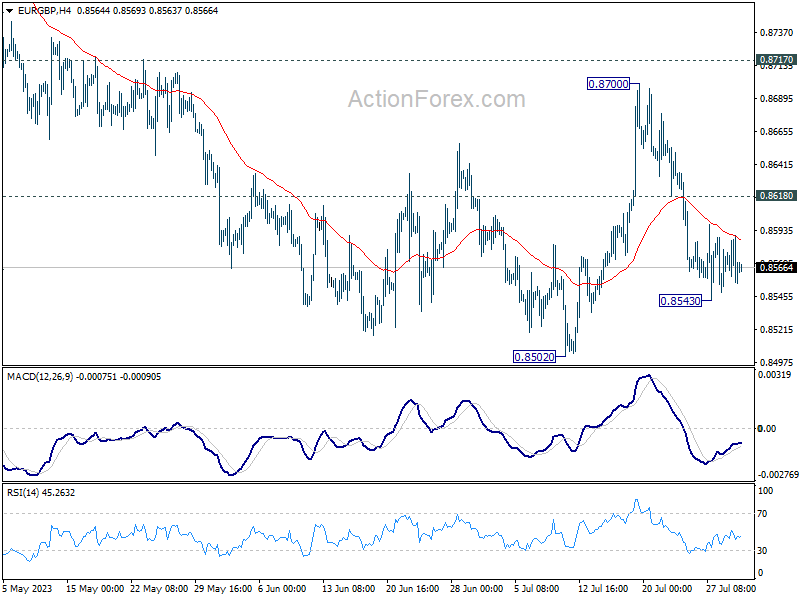

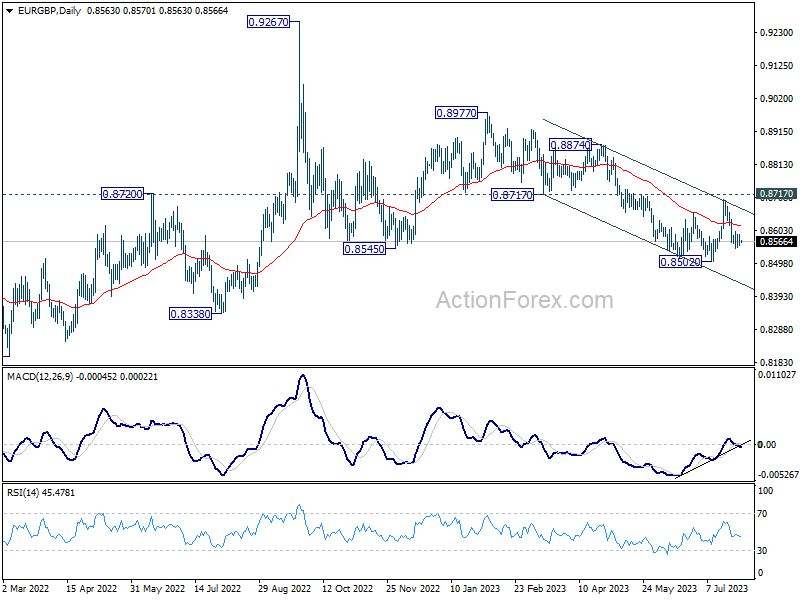

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8553; (P) 0.8572; (R1) 0.8587; More...

Intraday bias in EUR/GBP remains neutral at this point, and outlook is unchanged. On the downside, below 0.8543 will target a test on 0.8502 low. Decisive break there will resume larger decline from 0.8977. On the upside, above 0.8618 minor resistance will turn bias back to the upside for 0.8700, and possibly further to 0.8717 key support turned resistance.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

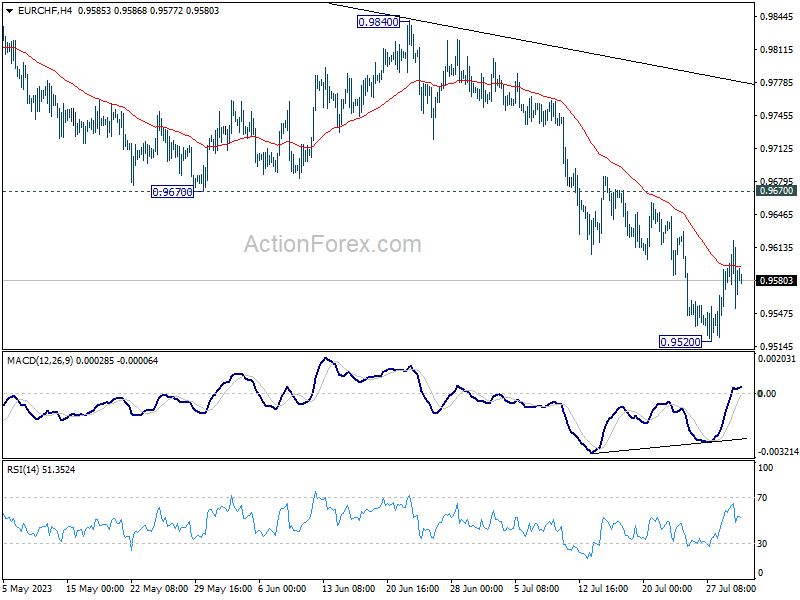

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9554; (P) 0.9588; (R1) 0.9622; More...

EUR/CHF is extending the consolidations above 0.9520 and intraday bias remains neutral at this point. While stronger recovery could be seen, outlook will remain bearish as long as 0.9670 support turned resistance holds. Break of 0.9520 will resume the fall from 1.0095 towards 0.9407 low.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9876). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9840 resistance holds, in case of strong rebound.

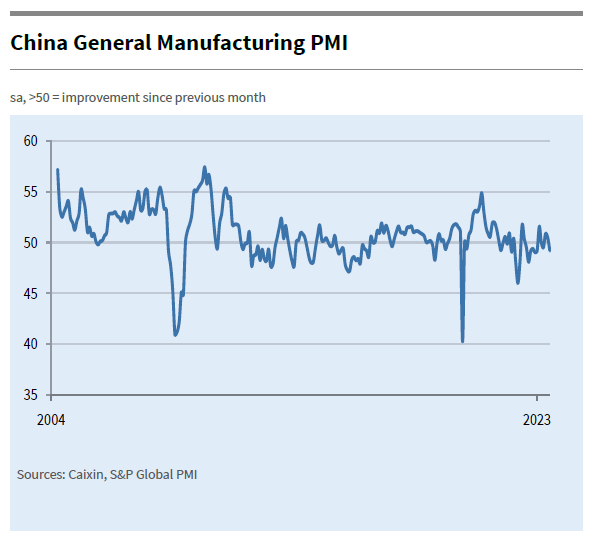

China Caixin PMI manufacturing down to 49.2, first contraction in three months

China's Caixin PMI Manufacturing index slipped from 50.5 to 49.2 in July, marking the first contraction in three months and falling below the expected 50.3. According to Caixin, there was a marginal contraction in output, and total sales plummeted due to a more pronounced decline in new export orders. Additionally, both input costs and output charges saw a decrease.

Senior Economist at Caixin Insight Group, Wang Zhe, highlighted the deteriorating situation, stating, "Overall, manufacturing conditions contracted in July, with supply, demand, exports, and employment all deteriorating. Prices continued to decline, inventories rose without companies adjusting them, and logistics times increased." He noted that manufacturers' optimism remained, but it had weakened.

Wang further explained, "China's economic recovery in the first quarter exceeded expectations, but the momentum weakened in the second. Although the data for industrial production and investment in June showed some signs of recovery, macroeconomic growth remained sluggish, and considerable downward pressure on the economy persisted."

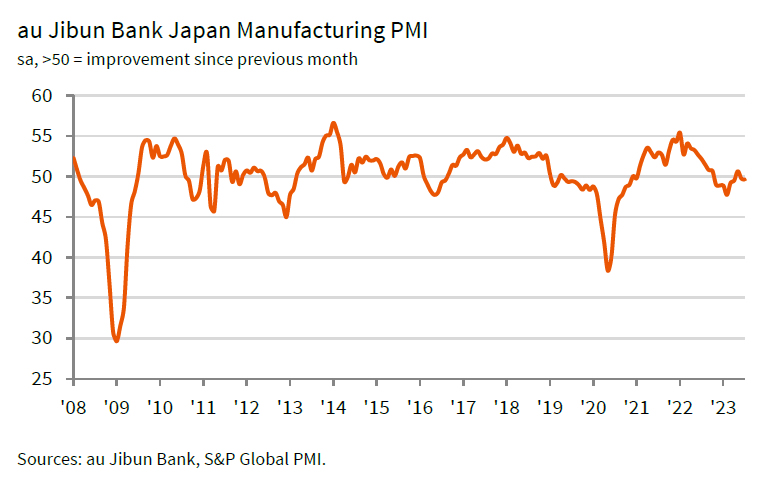

Japan PMI manufacturing finalized at 49.6, but business optimism elevated

Japan PMI Manufacturing was finalized at 49.6 in July, down from June's 49.8. That also marked the second month of concurrent decline in output and new orders. Usamah Bhatti at S&P Global Market Intelligence highlighted the significant role of "quicker deterioration in new order inflows" and also "sustained" decline in production.

Despite these struggles, inflationary pressures showed signs of abating as the rate of input cost inflation was the slowest since February 2021. However, selling price inflation was "unchanged" and "sharp overall" as Japanese manufacturers passed on a portion of higher cost burdens to clients.

The industry displayed robust optimism about the future, with the second-highest positive sentiment recorded in the last 18 months, driven by expectations of a boost in domestic and international demand owing to new product launches and the ongoing mitigation of COVID-19 and inflation-related influences.

AUD/USD Technical: Hovering Below 200-day Moving Average as RBA Looms

- AUD underperformed among the major currencies against the USD from 27 to 28 July 2023 ex-post FOMC, ECB, and BoJ.

- Split view among economists and interest rates traders on RBA monetary policy decision today.

- Short-term bearish downside momentum at this juncture as the AUD/USD failed to trade above the 200-day moving average.

- Key short-term resistance on AUD/USD is at 0.6740.

The AUD/USD staged a rebound thereafter and reached an intraday high of 0.6821 on 27 July, just shy of the 0.6835 intermediate before it staged a bearish reversal and shed -198 pips ex-post FOMC, ECB, and BoJ to print an intraday low of 0.6623 on last Friday, 28 July.

The Aussie has underperformed among the major currencies against the US dollar in the last two trading days of last week where the AUD/USD recorded an accumulated loss of -1.68% from 27 July to 28 July versus EUR/USD (-0.63%), GBP/USD (-0.71%), and JPY/USD (-0.65%) over the same period.

The weak performance of the AUD/USD is likely to be attributed to the wishy-washy monetary policy guidance of the Australian central bank, RBA that led to a split forecast among economists and traders for today’s RBA monetary policy decision.

Split view among economists and traders on RBA decision

According to polls, the consensus among economists is calling for a hike of 25 basis points hike to bring the policy cash rate to 4.35% after a pause in the previous meeting in July. In contrast, data from the ASX 30-day interbank cash rate futures as of 31 July 2023 has indicated a patty pricing of only a 14% chance of a 25-bps hike, down significantly from a 41% chance priced a week ago.

Fig 1: AUD/USD medium-term trend as of 1 Aug 2023 (Source: TradingView, click to enlarge chart)

From a technical analysis standpoint, the price actions of the AUD/USD are still trapped within a major sideway range configuration with its range resistance and support at 0.6930 and 0.6580 respectively.

Short-term momentum has turned bearish

Fig 2: AUD/USD minor short-term trend as of 1 Aug 2023 (Source: TradingView, click to enlarge chart)

The AUD/USD has managed to stage a minor rebound of 117 pips from its last Friday, 28 July intraday low of 0.6622 in conjunction with an oversold reading seen in the hourly RSI oscillator on the same day.

Interestingly, the minor rebound has challenged and retreated at the key 200-day moving average yesterday, 31 July during the US session (printed an intraday high of 0.6739). Right now, the hourly RSI oscillator has broken below its ascending support after it hit an overbought condition yesterday which indicates that short-term momentum has turned bearish.

Watch the 0.6740 key short-term pivotal resistance to maintain the bearish tone, and a break below 0.6625 intermediate support exposes the major range support of 0.6600/6580.

However, a clearance above 0.6740 negates the bearish tone to see the next resistance at 0.6835 in the first step.

GBP/USD at Clear Risk of Further Declines

Key Highlights

- GBP/USD declined below the 1.3000 and 1.2900 levels.

- A connecting bearish trend line is forming with resistance near 1.3020 on the 4-hour chart.

- EUR/USD might struggle to clear the 1.1075 resistance zone.

- The US ISM Manufacturing Index could rise from 46.0 to 46.5 in July 2023.

GBP/USD Technical Analysis

The British started a fresh decline from the 1.3140 zone against the US Dollar. GBP/USD declined below the 1.3000 and 1.2900 support levels.

Looking at the 4-hour chart, the pair even traded below the 1.2880 support and the 100 simple moving average (red, 4 hours). Finally, the pair found bids near the 1.2780 zone and the 200 simple moving average (green, 4 hours).

A low is formed near 1.2763 and the pair is now attempting a recovery wave. There was a minor increase above the 1.2840 level.

On the upside, the pair is facing resistance near the 1.2920 level and the 100 simple moving average (red, 4 hours). The first major resistance is near 1.2950. The main resistance could be near the 1.3000 zone.

There is also a connecting bearish trend line forming with resistance near 1.3020 on the same chart. A close above the trend line could set the pace for a fresh increase toward 1.3140.

If not, the pair could start a fresh decline. On the downside, the pair might find bids near the 1.2800 level. The next major support is near 1.2765, below which GBP/USD could slide toward the 1.2660 zone.

Looking at EUR/USD, the pair also attempted a recovery wave but it won’t be easy to settle above the 1.075 resistance zone.

Economic Releases

- Germany’s Manufacturing PMI for July 2023 - Forecast 38.8, versus 38.8 previous.

- Euro Zone Manufacturing PMI for July 2023 – Forecast 42.7, versus 42.7 previous.

- UK Manufacturing PMI for July 2023 – Forecast 45.0, versus 45.0 previous.

- US Manufacturing PMI for July 2023 – Forecast 49.0, versus 49.0 previous.

- US ISM Manufacturing Index for July 2023 – Forecast 46.5, versus 46.0 previous.

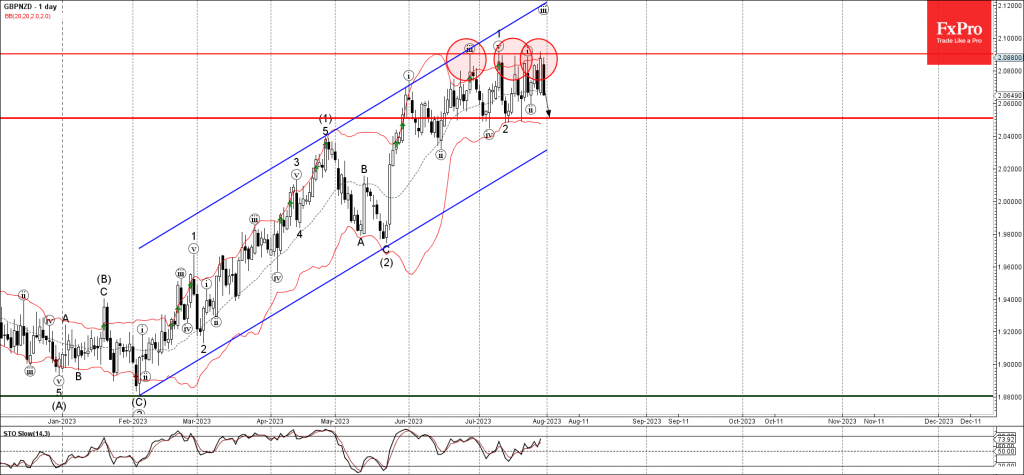

GBPNZD Wave Analysis

- GBPNZD reversed from pivotal resistance level 2.090

- Likely to fall to support level 2.050

GBPNZD currency pair recently reversed down from the pivotal resistance level 2.090 (which has been steadily reversing the price from the end of June).

The resistance level 2.090 is likely to form today the Bearish Engulfing, strong sell signal for this currency pair – highlighting the strength of this price level.

Given the strength of the resistance level 2.090, GBPNZD currency pair can be expected to fall further toward the next support level 2.050 (which has been reversing the pair from June).

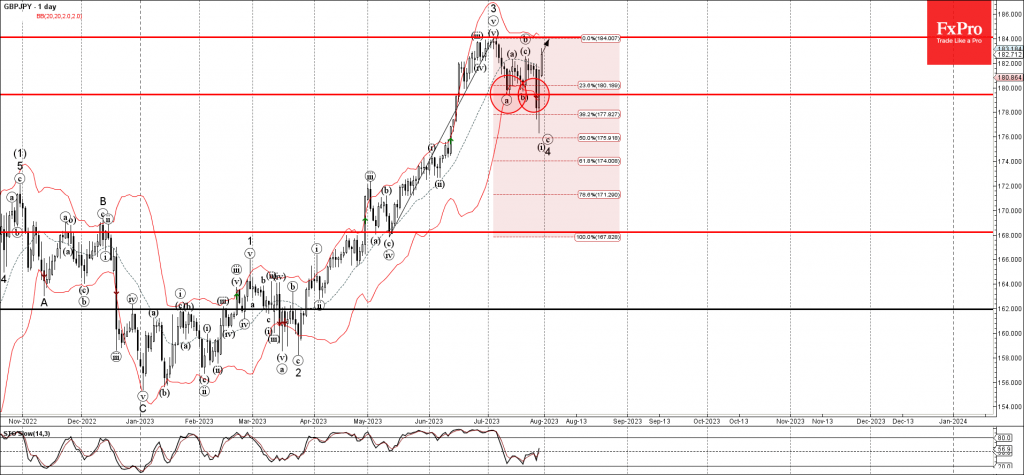

GBPJPY Wave Analysis

- GBPJPY reversed from key support level 179.45

- Likely to rise to resistance level 184.00

GBPJPY currency pair recently reversed up from the key support level 179.45 (which stopped the previous waves a and b).

The support level 179.45 was strengthened by the lower daily Bollinger Band and by the 38.2% Fibonacci correction of the upward impulse from May.

Given the clear daily uptrend, GBPJPY currency pair can be expected to rise further toward the next resistance level 184.00 (which stopped the previous impulse wave 3).

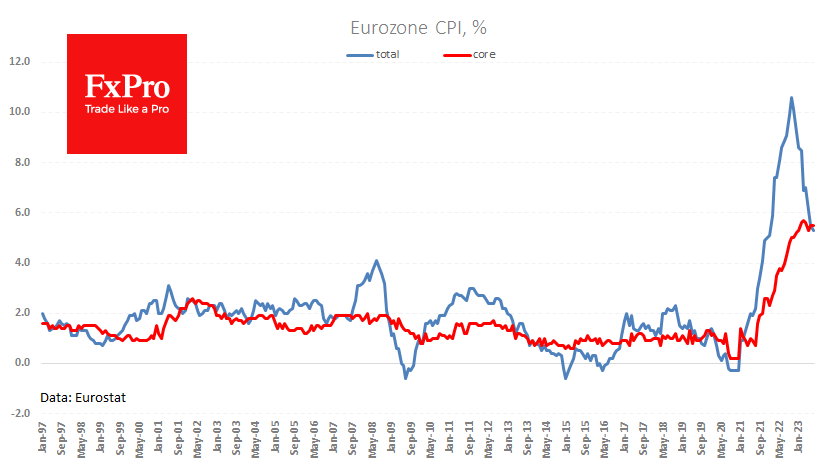

Eurozone Inflation is a Persistent Challenge

According to Eurostat’s preliminary estimate, eurozone inflation slowed to 5.3% year-on-year in July. This is the lowest rate since January 2022 and aligns with analysts’ expectations.

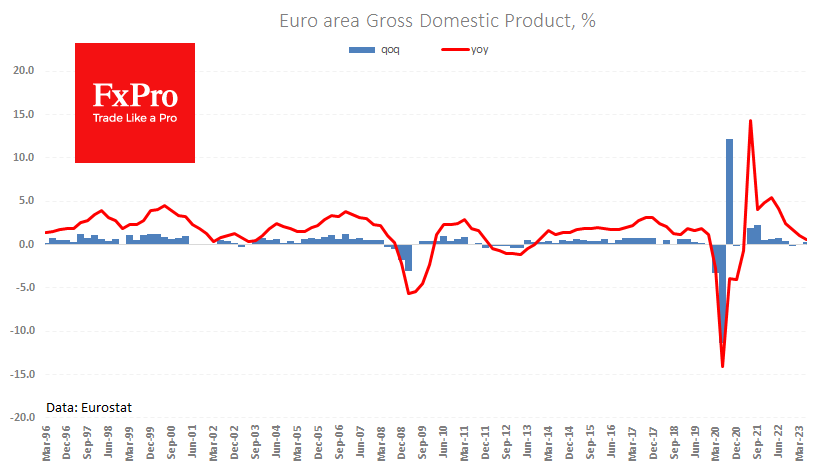

The core index stood at 5.5%, above the headline rate for the first time since February 2021. The momentum of this core index is coming to the forefront, and so far, there is little good news here, as the data are beating forecasts and not showing as strong a turnaround as we see in producer prices and headline inflation figures. As in the US, the likely reason is growth in the services sector after the coronavirus. The only thing that can change this situation is further tightening by the central bank, which is likely to dampen demand. The latest GDP estimates for the second quarter show that there is still room to work in this direction.

The eurozone economy grew by 0.3% QoQ after two quarters of virtually flat growth. This was despite aggressive interest rate hikes in previous quarters to dampen final demand for credit.

Better-than-expected price and GDP dynamics favour the euro, which rose for a second consecutive day on Monday after Thursday’s sell-off following the ECB press conference. We note that inflationary trends in Europe are more resilient than in the US, reviving speculation that the former will either have to raise rates more or hold them for longer. If this turns out to be the case, the uptrend in EURUSD that has been in place since September 2022 will gain traction in the coming quarters.