Sample Category Title

Copper Takes Aussie Higher ahead of RBA

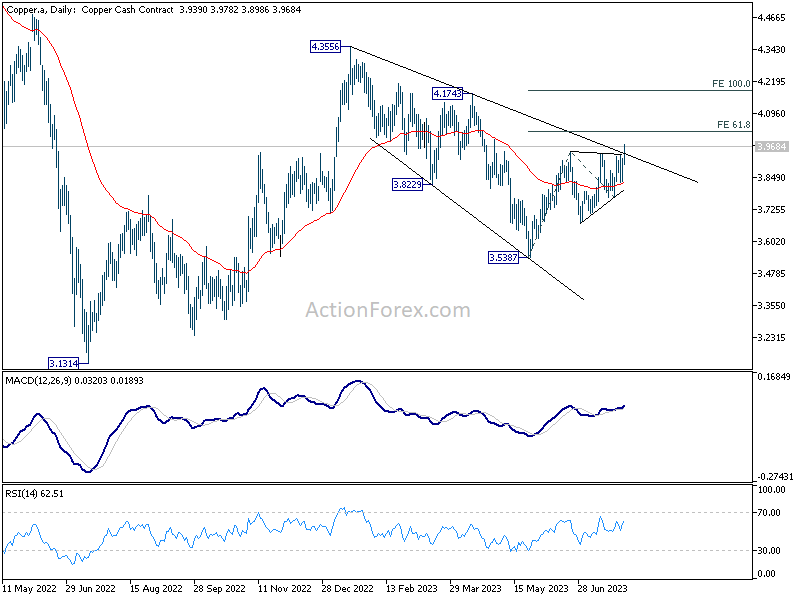

Commodity currencies are trading generally higher today on mildly positive market sentiment. Australian Dollar is the stronger one among them, ahead of RBA's rate decision tomorrow. Opinions on whether RBA would hike by 25bps next month (i.e. August 1 tomorrow) are divided . Major local banks exhibit this split sentiment, with Commonwealth Bank and Westpac predicting a 25bps hike, while ANZ and NAB foresee a pause. Still, it's actually more of a question of timing on whether the final hike will be delivered tomorrow or later in September. The rally in Copper prices is more likely the primary driver behind Aussie's rebound.

Elsewhere in the currency markets, European majors are mixed for now. But Euro does ride on slightly stronger than expected core inflation reading to rally against Swiss Franc. Yen is the worst performer, followed by Franc and then Dollar. The selloff in Yen is so far steady, and thus, it's likely to continue for a while. Dollar will need some strong ISM and NFP readings to revive its near term rebound, except versus the weak Yen.

Technically, Copper's solid rally today should confirm resumption of rise from 3.5387. It also affirms the case that corrective decline from 4.3556 has completed at 3.5387. Further rise is now expected, as long as 3.8986 minor support holds, to 61.8% projection of 3.5387 to 3.9501 from 3.7725 at 4.0267. Firm break there will solidify this bullish case and target 100% projection at 4.1839. Also, strong break of 4.0267 in Copper will give Aussie a solid boost this week, regardless of tomorrow's RBA decision.

In Europe, at the time of writing, FTSE is up 0.07%. DAX is up 0.19%. CAC is up 0.47%. Germany 10-year yield is up 0.0146 at 2.505. Earlier in Asia, Nikkei rose 1.26%. Hong Kong HSI rose 0.82%. China Shanghai SSE rose 0.46%. Singapore Strait Times rose 0.08%. Japan 10-year JGB yield rose 0.0531 to 0.603.

Eurozone GDP grew 0.3% qoq in Q2, EU flat

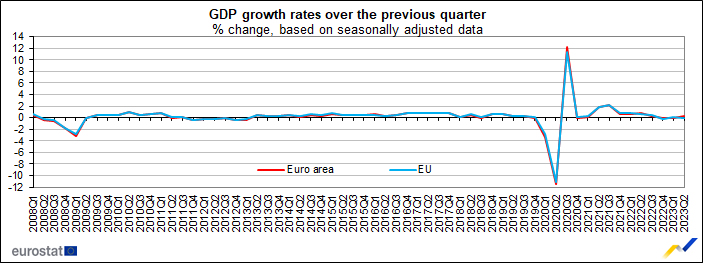

Eurozone GDP grew 0.3% qoq in Q2, above expectation of 0.2% qoq. EU GDP was flat at 0.0% qoq.

Among the Member States for which data are available, Ireland (+3.3%) recorded the highest increase compared to the previous quarter, followed by Lithuania (+2.8%). Declines were recorded in Sweden (-1.5%), in Latvia (-0.6%), in Austria (-0.4%) and in Italy (-0.3%).

The growth rates compared to the same quarter of the previous year were positive for seven countries, with the highest values observed for Ireland (+2.8%), Portugal (+2.3%) and Spain (+1.8%). The highest declines were recorded for Sweden (-2.4%), Czechia (-0.6%) and Latvia (-0.5%).

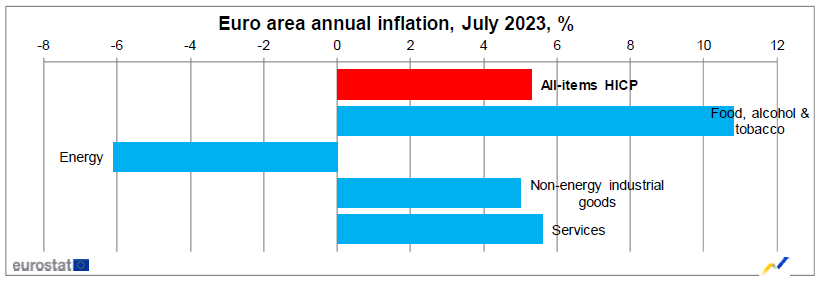

Eurozone CPI slowed to 5.3.% in Jul, core unchanged at 5.5%

Eurozone CPI slowed from 5.5% yoy to 5.3% yoy in July, matched expectations. CPI core (excluding energy, food, alcohol & tobacco) was unchanged at 5.5% yoy, above expectation of 5.4% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in July (10.8%, compared with 11.6% in June), followed by services (5.6%, compared with 5.4% in June), non-energy industrial goods (5.0%, compared with 5.5% in June) and energy (-6.1%, compared with -5.6% in June).

Japan's industrial production rose 2.0% mom in Jun, moderately picking up

Japan's Ministry of Economy, Trade and Industry reported 2.0% mom increase in industrial production in June, below expected 2.4%. This places the seasonally adjusted index of production at factories and mines at 105.3, with 2020 as the base of 100.

Motor vehicles led industrial production growth, surging 6.1% thanks to robust demand in both domestic and overseas markets. Out of 15 industrial sectors covered , 10 sectors saw increased output, while production in five dropped.

Despite the production growth coming in lower than expected, the Ministry maintained its basic assessment, noting that industrial production was "showing signs of moderately picking up."

Looking ahead, the Ministry's forecast based on a poll of manufacturers anticipates slight output decline of -0.2% in July, followed by climb of 1.1% in August.

Also released, retail sales rose 5.9% yoy in June, above expectation of 5.4% yoy, picked up from prior month's 5.7% yoy.

China's PMI manufacturing ticked up to 49.3, but marked 4th month of contraction

China's official Manufacturing PMI rose from 49.0 in June to 49.3 in July, slightly above anticipated 49.2. However, it marked the fourth consecutive month that this indicator remained below the 50-point mark separating expansion from contraction on a monthly basis.

Zhao Qinghe, a senior NBS official, indicated that while there was a slight rebound, many enterprises reported experiencing a "complicated and severe" external environment. In his statement, Zhao stated, "overseas orders have decreased, and insufficient demand is still the main difficulty faced by enterprises."

Meanwhile, Non-Manufacturing PMI, which measures activity in both services and construction sectors, dropped from 53.32 to 51.5, missing the expected 53.1, marking its fourth straight monthly decline. The services subindex fell from 52.8 to 51.5, while the construction subindex saw a significant drop from 55.7 to 51.2.

Composite PMI, which provides a broader picture of the economy, also declined from 52.3 in June to 51.1 in July, reflecting the challenges faced by both the manufacturing and non-manufacturing sectors.

NZ ANZ business confidence rose to -13.1, highest since Sep 2021

New Zealand's business confidence has reached its highest point since September 2021, with ANZ Business Confidence Index improved from -18.0 to -13.1. Although this remains in the negative territory, it shows a relative boost in optimism.

Looking at the details, Own Activity Outlook, a measure of businesses' expectations of their own activity, experienced a slight drop from 2.7 to 0.8. However, various components of the index witnessed improvements. Export intentions increased from -1.8 to 1.5, indicating a renewed confidence in overseas markets. Both investment and employment intentions showed minor improvements.

Inflation indicators were mixed, with cost expectations climbing from 76.0 to 80.6, while inflation expectations saw a slight ease from 5.29% to 5.14%. At the same time, profit expectations and pricing intentions edged slightly lower.

Despite expecting a recession and rising unemployment, ANZ's view on the current economic environment is that it's "patchy rather than capitulating," suggesting that although there are definite challenges ahead, New Zealand's economy might show more resilience than expected.

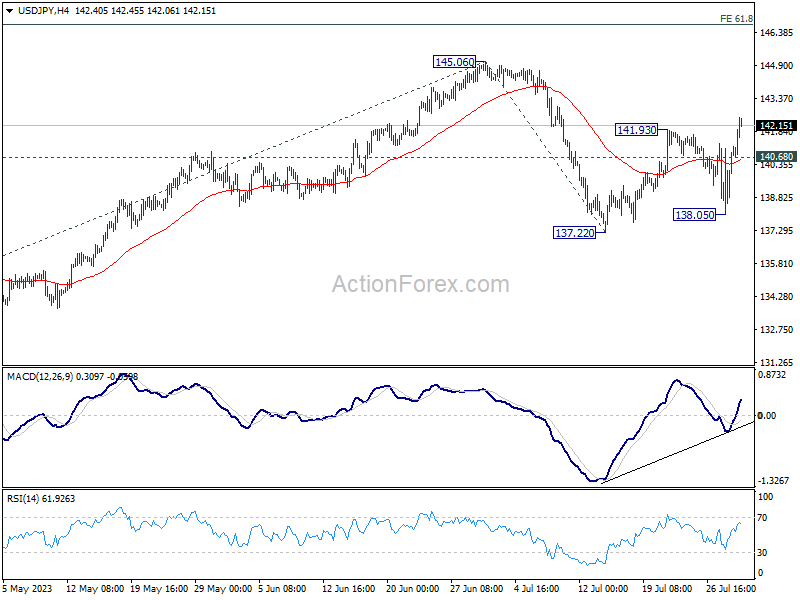

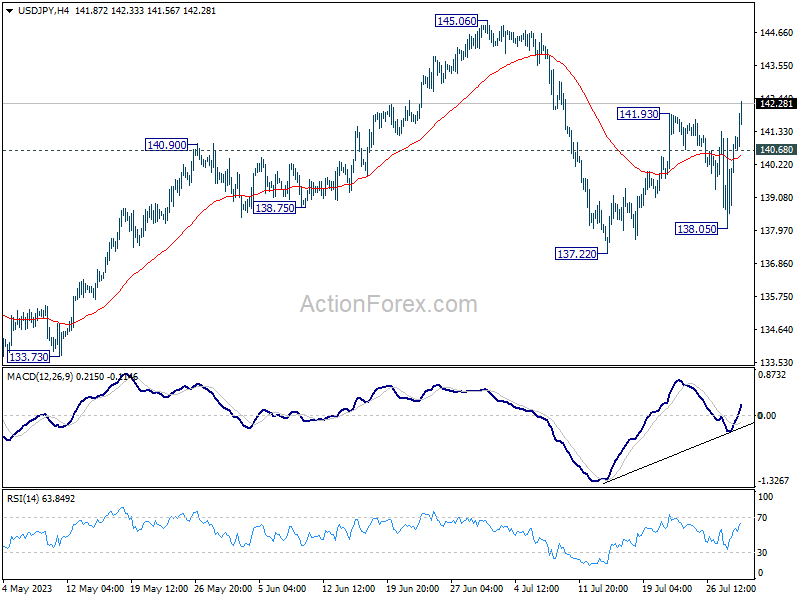

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.10; (P) 140.14; (R1) 142.21; More...

Intraday bias in USD/JPY remains on the upside for retesting 145.60. Firm break there will resume whole rally from 172.20. Next target is 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76. On the downside, below 140.68 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Jun P | 2.00% | 2.40% | -2.20% | |

| 23:50 | JPY | Retail Trade Y/Y Jun | 5.90% | 5.40% | 5.70% | |

| 01:00 | CNY | NBS Manufacturing PMI Jul | 49.3 | 49.2 | 49 | |

| 01:00 | CNY | Non-Manufacturing PMI Jul | 51.5 | 53.1 | 53.2 | |

| 01:00 | NZD | ANZ Business Confidence Jul | -13.1 | -18 | ||

| 01:00 | AUD | TD Securities Inflation M/M Jul | 0.80% | 0.10% | ||

| 01:30 | AUD | Private Sector Credit M/M Jun | 0.20% | 0.40% | 0.40% | |

| 05:00 | JPY | Housing Starts Y/Y Jun | -4.80% | -0.20% | 3.50% | |

| 05:00 | JPY | Consumer Confidence Index Jul | 37.1 | 37 | 36.2 | |

| 06:00 | EUR | Germany Import Price Index M/M Jun | -1.60% | -0.80% | -1.40% | |

| 06:00 | EUR | Germany Retail Sales M/M Jun | -0.80% | -0.20% | 0.40% | 1.90% |

| 08:00 | EUR | Italy GDP Q/Q Q2 P | -0.30% | 0.00% | 0.60% | |

| 08:30 | GBP | Mortgage Approvals Jun | 55K | 49K | 51K | |

| 08:30 | GBP | M4 Money Supply M/M Jun | -0.10% | 0.50% | 0.20% | |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.30% | 0.20% | -0.10% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | 5.30% | 5.30% | 5.50% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | 5.50% | 5.40% | 5.50% | |

| 13:45 | USD | Chicago PMI Jul | 43.5 | 41.5 |

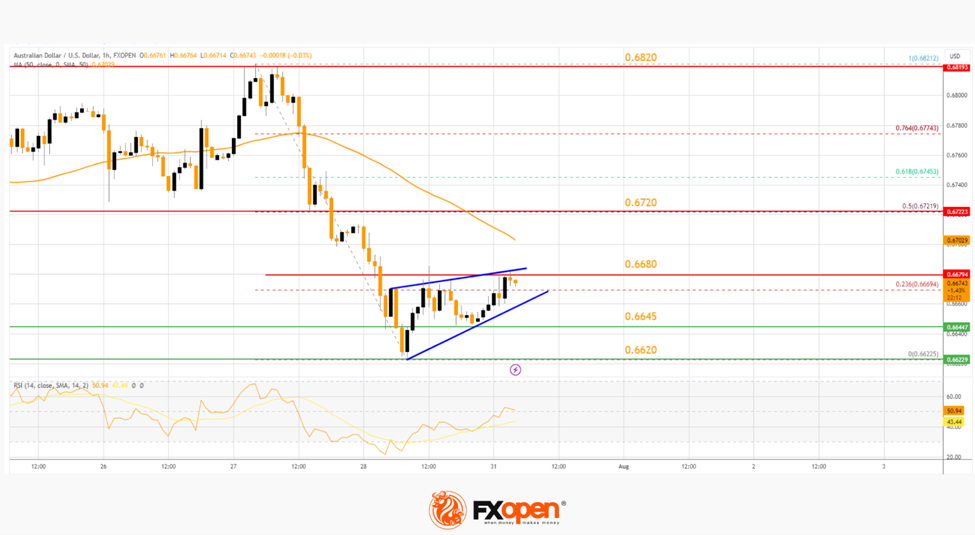

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair gained bearish momentum below the 0.6720 zone. The Aussie Dollar entered a bearish zone after breaking below the 0.6680 support level.

The pair even settled below the 50-hour simple moving average and tested 0.6620. AUD/USD is now consolidating losses and facing resistance near the 0.6680 level. The first breakout zone could be near the 50-hour simple moving average or 0.6720.

If there is an upside break above the 0.6720 zone, the pair could rise steadily toward the 0.6820 level. Any more gains might send AUD/USD toward 0.6840.

Conversely, the pair could start a fresh decline below 0.6645. The first major support is near the 0.6620 level, below which the pair could drop toward 0.6600. Any more losses might send AUD/USD toward the 0.6565 support.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

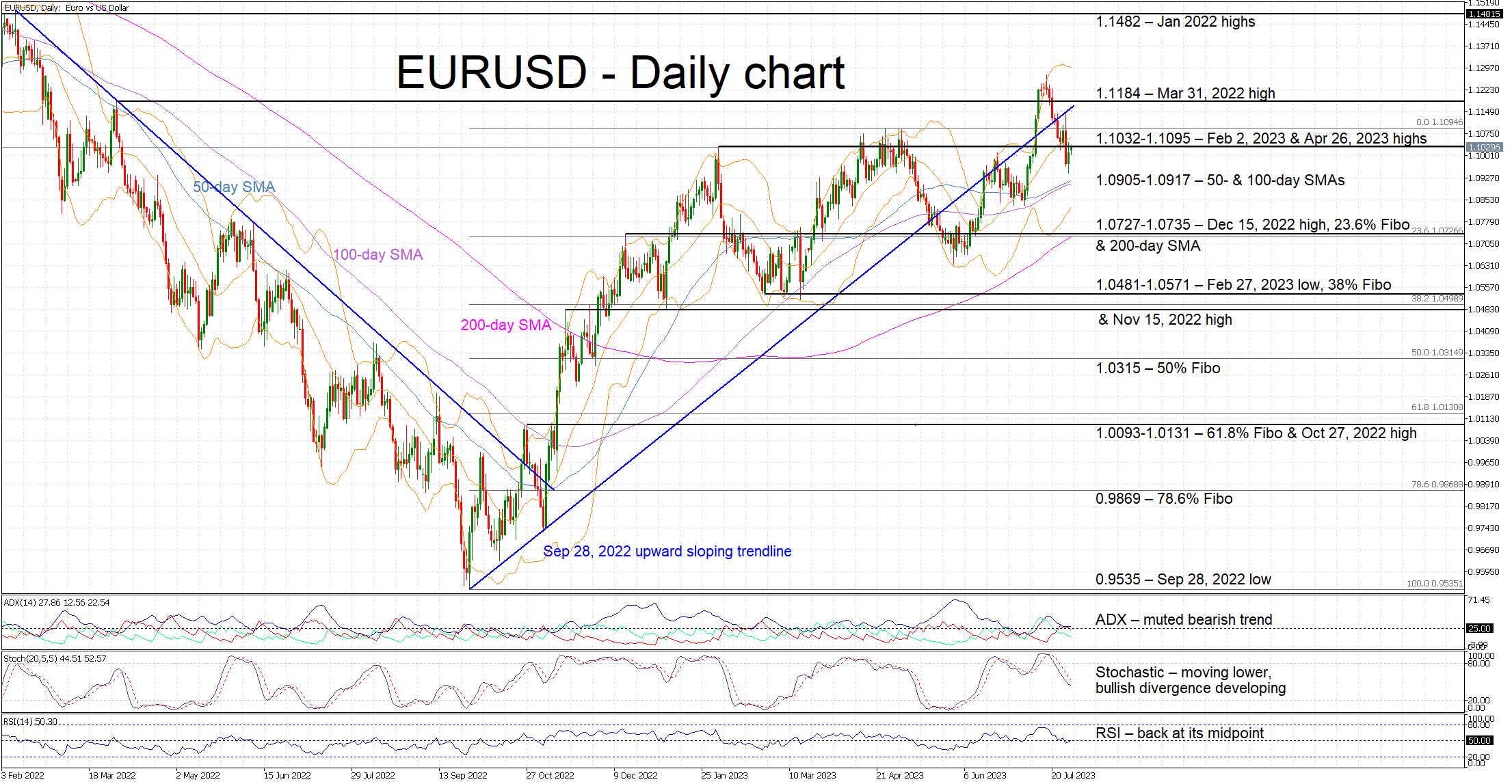

EURUSD Correction Halts as Overall Technical Picture Unclear

EURUSD is edging higher today as it is trying to find its footing following an eventful week. The pair is hovering a tad below the busy 1.1032-1.1095 area and remains comfortably below the September 28, 2022 upward sloping trendline. The convergence of the 50- and 100-day simple moving averages (SMAs) persists and thus keeps the door open to a sizeable move soon.

In the meantime, most momentum indicators appear to have reset following their recent decent moves. The Average Directional Movement Index (ADX) is slightly above its 25-threshold and thus pointing to a muted bearish trend in the market, and the RSI is again hovering around its midpoint. More interestingly, the stochastic oscillator is moving lower and has built a good gap from its moving average. However, the current lower low in the stochastic has been met by a higher low in EURUSD, giving rise to the formation of a bullish divergence.

Should the bulls try to take advantage of the stochastic’s developing divergence, they would aim for a move above the busy 1.1032-1.1095 range that is populated by the February 2, 2023 and April 26, 2023 highs respectively. They would then have the chance of testing the resistance set by the September 28, 2022 upward sloping trendline, a tad below the March 31, 2022 high at 1.1184.

On the flip side, the bears are looking for a continuation of the current downleg. If they manage to successfully defend the 1.1032-1.1095 range, they could then have a go at the 1.0905-1.0917 area. This appears to be a strong support region as it is defined by the 50- and 100-day SMAs. Even lower, the path remains tricky with the next key area coming at the 1.0727-1.0735 range.

To conclude, EURUSD bears appear to be still in control, but the developing bullish divergence could quickly reverse market sentiment.

EUR/GBP Technical: Recent Downside Momentum Subsided

- The 4-hour RSI oscillator has traced out a bullish divergence condition at its oversold region.

- A break above the 50-day moving average now acts as a 0.8600 intermediate resistance may rekindle another leg of short-term rebound for EUR/GBP.

- The next resistance stands at 0.8720 which is also the 200-day moving average.

The recent 157 pips slide seen on the EUR/GBP cross pair from its 0.8701 high printed on 19 July 2023 to 27 July 2023 intraday low of 0.8544 has managed to find support at the former medium-term descending channel resistance from 26 April 2023 high now turns pull-back support at the 0.8550 level.

EUR/GBP short-term trend as of 31 Jul 2023 (Source: TradingView, click to enlarge chart)

In addition, the 4-hour RSI oscillator has shaped a bullish divergence condition at its oversold region and inched backed up above the 50 level today, 31 Jul which suggests that short-term downside momentum has eased.

A clearance above the intermediate resistance of 0.8600 (also the 50-day moving average) sees the next resistance coming at 0.8720 (congestion area of 13 May to 23 May 2023 & 200-day moving average).

On the flip side, a break below 0.8505 key medium-term pivotal support invalidates the short-term rebound scenario to expose the next support at 0.8410.

AUD/USD Rebounds on Stronger Inflation Release

- Australian MI Inflation gauge jumps 0.8%

- AUD/USD climbs 0.80%

- RBA expected to pause rates on Tuesday

The Australian dollar has started the week with strong gains. In the European session, AUD/USD is trading at 0.6700, up 0.80%. The Aussie has rebounded after falling 1.25% last week.

RBA expected to pause rates

The Reserve Bank of Australia meets on Tuesday and is expected to maintain the cash rate at 4.10%. The past two rate meetings have been close calls and that could be the case at Tuesday’s meeting. The money markets, however, are squarely leaning towards a pause, with only a 14% chance of a hike, according to the ASX RBA Rate Tracker.

Investors are basing expectations for a second straight pause on lower inflation and weaker retail sales. Both headline and core CPI eased in the second quarter, as inflation appears to be heading in the right direction. Retail sales surprised on the downside with a -0.8% reading in June, erasing the 0.8% gain in May and missing the consensus estimate of 0.0%.

The RBA could surprise the markets with a hike, as inflation has fallen to 6% but is double the RBA’s upper band of its 1%-3% range. As well, the labour market remains tight and the central bank is concerned that could lead to higher wages which means an increase in inflation. Tuesday’s meeting will be the second to last for Governor Lowe, who may want to deliver another hike or two before his watch ends, in a bid to push inflation closer to the RBA’s target. The RBA will release updated economic forecasts at the meeting, and investors will be especially interested in the inflation projections.

The Melbourne Institute Inflation Gauge jumped 0.8% in July, rebounding from 0.1% in June and beating the consensus estimate of 0.5%. The upswing was somewhat surprising given last week’s inflation report which showed a significant slowdown in inflation. The Australian dollar has moved sharply higher following the release.

AUD/USD Technical

- AUD/USD is testing support at 0.6767. Below, there is support at 0.6687

- There is resistance at 0.6811 and 0.6891

Bitcoin Avoids Sharp Moves. Unlikely for Long

Market picture

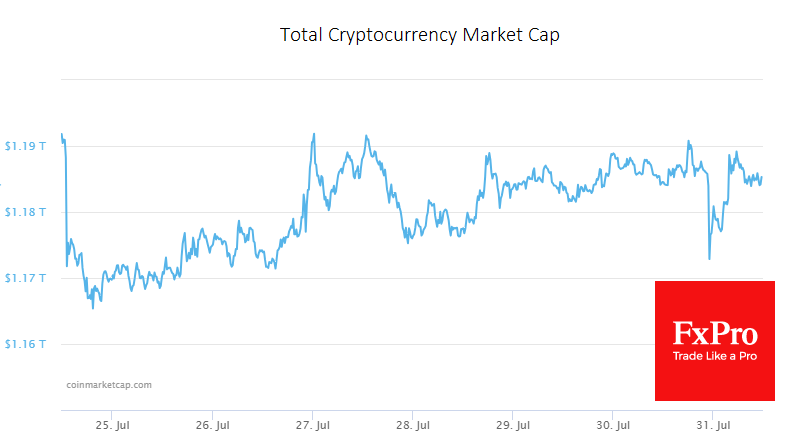

Crypto market capitalisation fell by 0.5% over the week, gradually recovering from last Monday’s dip. The Crypto Market Sentiment Index fell 5 points to 50, firmly in the middle of the scale.

For the week, bitcoin lost 1.2%, Ethereum lost 0.2%, and the top altcoins ranged from -5.7% (Polygon) to +10% (Dogecoin).

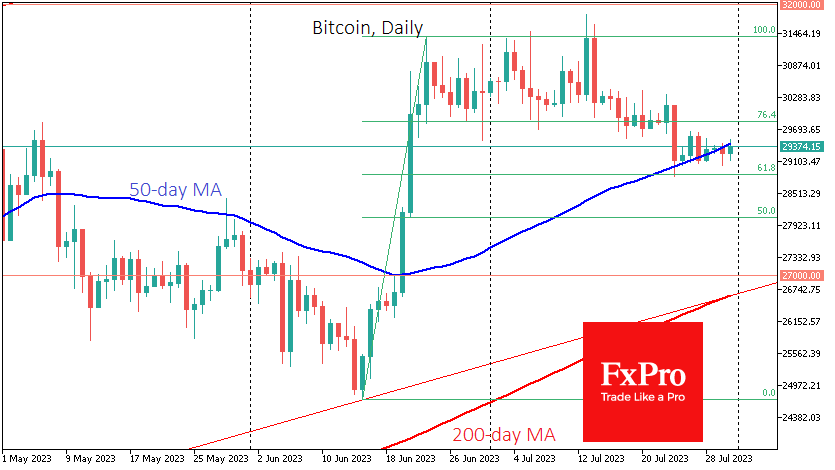

Bitcoin continues to move strictly to the right, with decreasing intraday volatility and passively closing slightly below its 50-day moving average, which is pointing up. In theory, this is a signal of a medium-term trend change. In practice, however, it may simply be market noise.

In such conditions, waiting for a significant impulse in any direction makes sense, assuming further movement in the same direction. In numerical terms, a return above $30.1K opens the way to $31.4K with a long-term target of $35.5K. A break below $29K would drop the main scenario to the near-term target of $28K and the long-term target of $27K.

News background

Well-known trader and financial industry veteran Peter Brandt believes Bitcoin will eventually become a leading investment asset. According to him, US regulators are sure to approve the launch of spot bitcoin ETFs, but this could put pressure on BTC.

Gary Gensler, head of the US SEC, said the crypto market is “rife with scammers and peddlers”. Investors starting in crypto assets should be warned that no protections exist.

The SEC has adopted new rules requiring cryptocurrency companies to disclose significant cybersecurity incidents. According to the document, companies will have four days to provide the agency with “significant” hacks details.

Despite the drop in trading volumes in the crypto market, the volume of Bitcoin and Ethereum futures transactions on the Chicago Mercantile Exchange (CME) reached record highs in January 2022.

According to CME research, tech-heavy Nasdaq 100 index fluctuations tend to affect Ethereum more than Bitcoin.

Eurozone GDP grew 0.3% qoq in Q2, EU flat

Eurozone GDP grew 0.3% qoq in Q2, above expectation of 0.2% qoq. EU GDP was flat at 0.0% qoq.

Among the Member States for which data are available, Ireland (+3.3%) recorded the highest increase compared to the previous quarter, followed by Lithuania (+2.8%). Declines were recorded in Sweden (-1.5%), in Latvia (-0.6%), in Austria (-0.4%) and in Italy (-0.3%).

The growth rates compared to the same quarter of the previous year were positive for seven countries, with the highest values observed for Ireland (+2.8%), Portugal (+2.3%) and Spain (+1.8%). The highest declines were recorded for Sweden (-2.4%), Czechia (-0.6%) and Latvia (-0.5%).

Eurozone CPI slowed to 5.3.% in Jul, core unchanged at 5.5%

Eurozone CPI slowed from 5.5% yoy to 5.3% yoy in July, matched expectations. CPI core (excluding energy, food, alcohol & tobacco) was unchanged at 5.5% yoy, above expectation of 5.4% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in July (10.8%, compared with 11.6% in June), followed by services (5.6%, compared with 5.4% in June), non-energy industrial goods (5.0%, compared with 5.5% in June) and energy (-6.1%, compared with -5.6% in June).

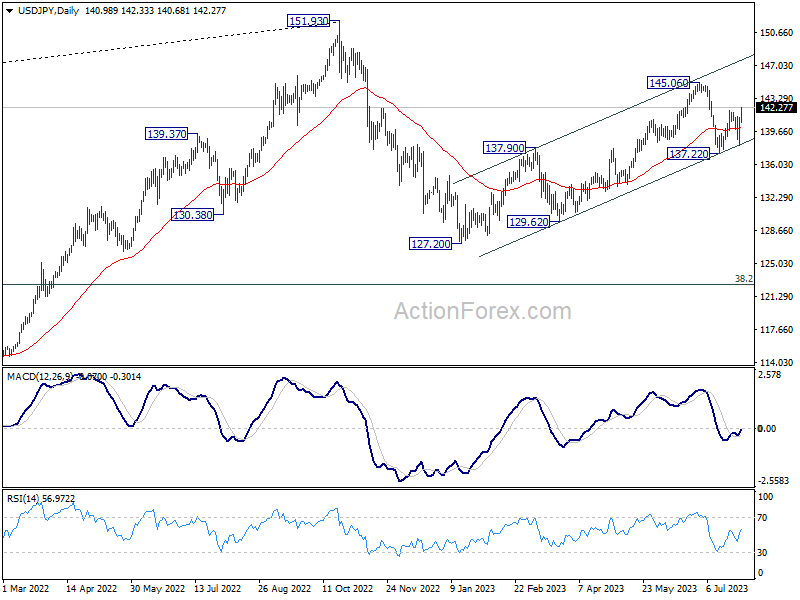

USD/JPY Daily Outlook

Daily Pivots: (S1) 139.10; (P) 140.14; (R1) 142.21; More...

Break of 141.93 resistance confirms resumption of rebound from 137.22 in USD/JPY. Intraday bias is back on the upside for retesting 145.06 first. Firm break there will resume whole rise from 172.20. On the downside, below 140.68 minor support will turn intraday bias neutral first.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

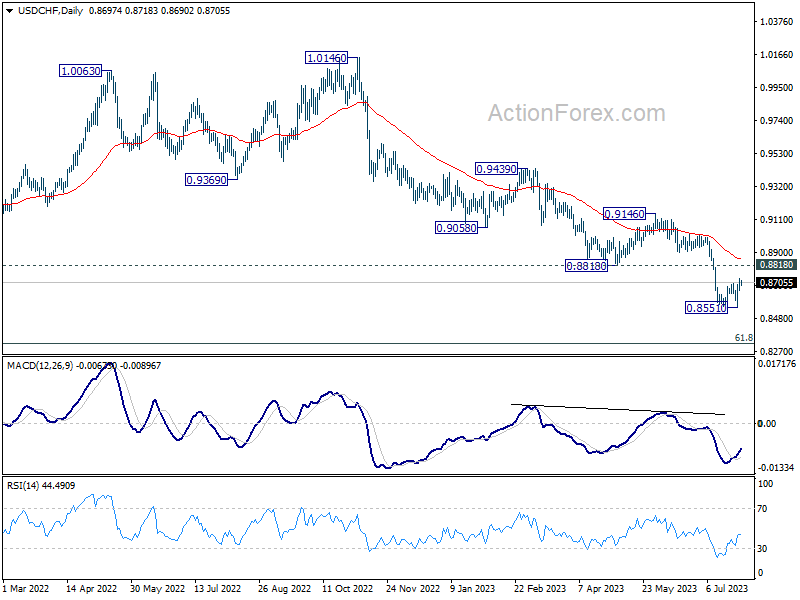

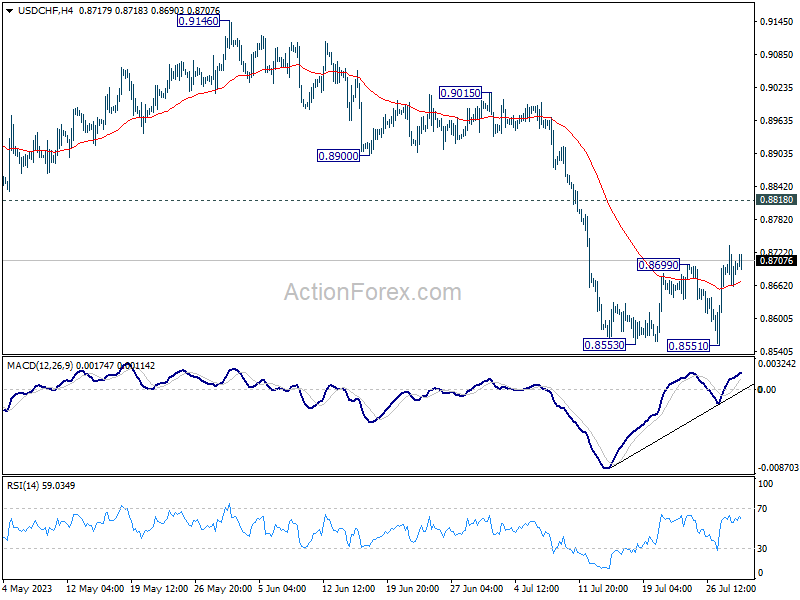

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8665; (P) 0.8701; (R1) 0.8740; More....

Intraday bias in USD/CHF stays mildly on the upside at this point. Rebound from 0.8851 would extend higher towards 0.8818 support turned resistance. Strong resistance could be seen there to complete the recovery and bring down trend resumption. On the downside, firm break of 0.8551 will resume larger down trend from 1.0146, targeting 0.8317 fibonacci level.

In the bigger picture, down trend from 1.0146 is seen as in progress as long as 0.8188 support turned resistance holds. Next target is 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317. However, sustained break of 0.8818 will be the first sign of medium term bottoming, and turn focus back to 0.9146 resistance for confirmation.