Sample Category Title

Where Crude Oil Prices Could Pop

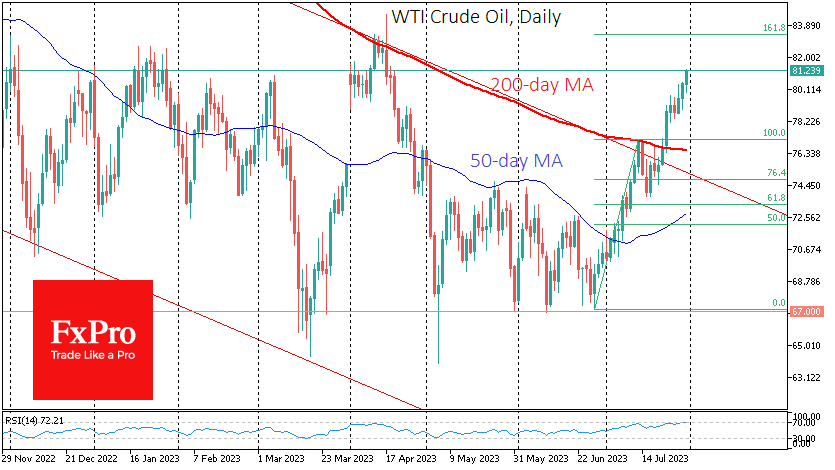

Oil has accelerated its gains over the past week, adding more than 20% to the lows of 28 June, when the latest rally began. Technical factors coming into play and excitement in the markets from robust macro data are adding fuel to the fire.

WTI broke above $81 on Monday and is making new multi-month highs after six weeks of strength. Last Monday, the price bounced sharply off its 200-day moving average, confirming the break of a downtrend that has been in place for more than a year.

The medium-term technical picture now points to a rise to the $83.50 area, centring on the May highs and the 161.8% Fibonacci retracement from the rally’s start to the first touch of the 200-day MA. However, oil’s rally may not stop there and could take it to levels above $90, the double top of October and November last year.

Fundamental factors also support higher prices than we are seeing now. Market investors are cheering lower inflation figures, suggesting that central banks will move more quickly to ease policy, supporting global demand for commodities.

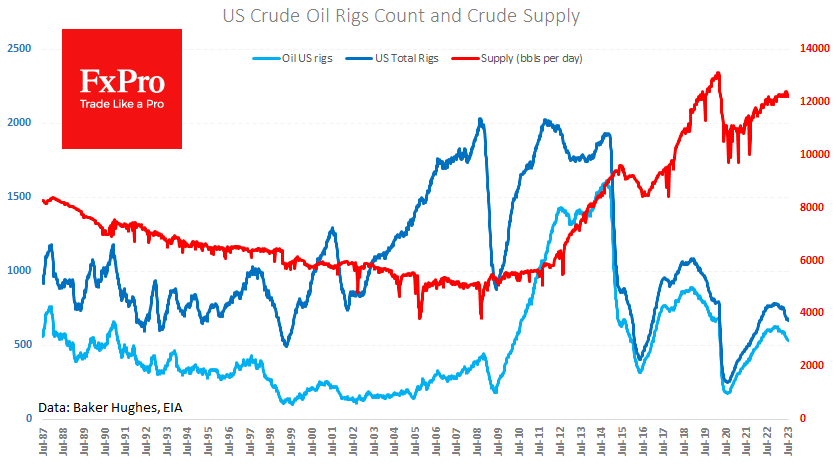

Interestingly, the multi-week price rally has not changed US oil producers’ mood. Oil inventories remained at 12.2M BPD last week – just below the average level since the start of the year, signalling a relatively cautious near-term sentiment. The number of active drillers fell to 528 (-2) for the week, the lowest since March last year.

That’s a sign of long-term pessimism, which is surprising, given the news that oil consumption has surpassed all-time highs and the supply/demand balance moved into deficit in July. On top of that, the US continues adding jobs, and China is ramping up its stimulus to accelerate economic growth.

Yen Slides to 3-Week Low vs Dollar as BoJ Buys JGBs

- BoJ announces JGB purchases

- Japanese yen’s slide continues

The Japanese yen has extended its slide on Monday and is trading at 142.22, down 0.75% against the US dollar.

BoJ surprises with JGB purchases

The Japanese yen continues to show sharp volatility, which can be attributed directly to moves by the Bank of Japan. On Friday, the BoJ caught the markets by surprise and loosened its yield curve control policy. The BoJ maintained its target for 10-year yields at around zero, but said that the 0.5% ceiling would be a reference point rather than a rigid limit and that it would offer to buy 10-year government bonds at 1%. Effectively, this widens the target band on 10-year bonds by a further 50 basis points.

The BoJ’s easing of yield curve control (YCC) raised speculation that the central bank could shift ultra-accommodative policy and this caused the yen to decline by 1.2% on Friday. Earlier on Monday, the BoJ announced it would buy an unlimited amount of JGBs. The BoJ did not wait for JGBs to hit 1% and decided to intervene in the bond market. The Bank’s intervention was a surprise and extended the yen’s losses, which have amounted to 2% since Thursday.

Governor Ueda tried to downplay the tweaking of yield curve control, saying that it did not mark a normalization of policy. Nevertheless, the move was significant, as the BoJ has diluted its yield cap of 0.50%, which it has heavily defended in the past.

In the US, the manufacturing sector remains in recession and has not shown expansion since October. Manufacturing PMI fell to 46.0 in June its worst showing since May 2020. The July Manufacturing PMI will be released on Tuesday, with a consensus of 46.8 points.

USD/JPY Technical

- USD/JPY is testing resistance at 1.4263. Above, there is resistance at 144.09

- There is support at 142.21 and 1.4035

USD/JPY Retesting Strong Intraday Resistance

USDJPY is retesting the 142 – 143 resistance zone as a larger 3-3-5 regular A-B-C flat correction, where wave C can be already in final stages. So, still watch out for strong bears, especially if we will get sharp or impulsive intraday reversal down. Bearish confirmation is below 138 level.

Fed’s Goolsbee undecided on Sep FOMC decision

Chicago Fed President Austan Goolsbee, a voting member of this year's monetary policy committee, expressed his ambivalence about the upcoming FOMC meeting in September. In a interview by Yahoo Finance, Goolsbee remarked, "I haven't made up my mind for what should happen in September."

Goolsbee underscored the significance of several key data points that the Fed will have to consider before the September meeting. "We'll get several more major data points before the next meeting," he elaborated, indicating a reliance on these forthcoming data to inform any decisions about the policy rate.

Despite the uncertainty, Fed President is satisfied with the current progress, remarking, "But it's looking like we're walking the line pretty well." Goolsbee also suggested that future actions would need to be responsive to changing conditions, explaining that the Fed will have to "play by ear" on whether the policy rate is sufficiently restrictive.

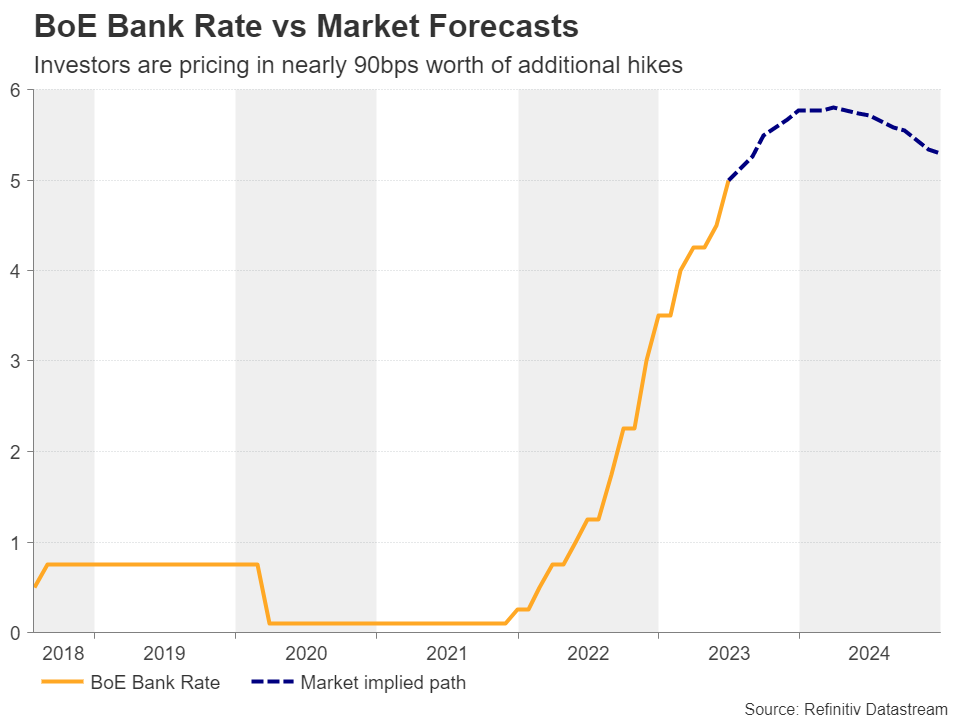

Will BoE Go Back to 25bps Interest Rate Increments?

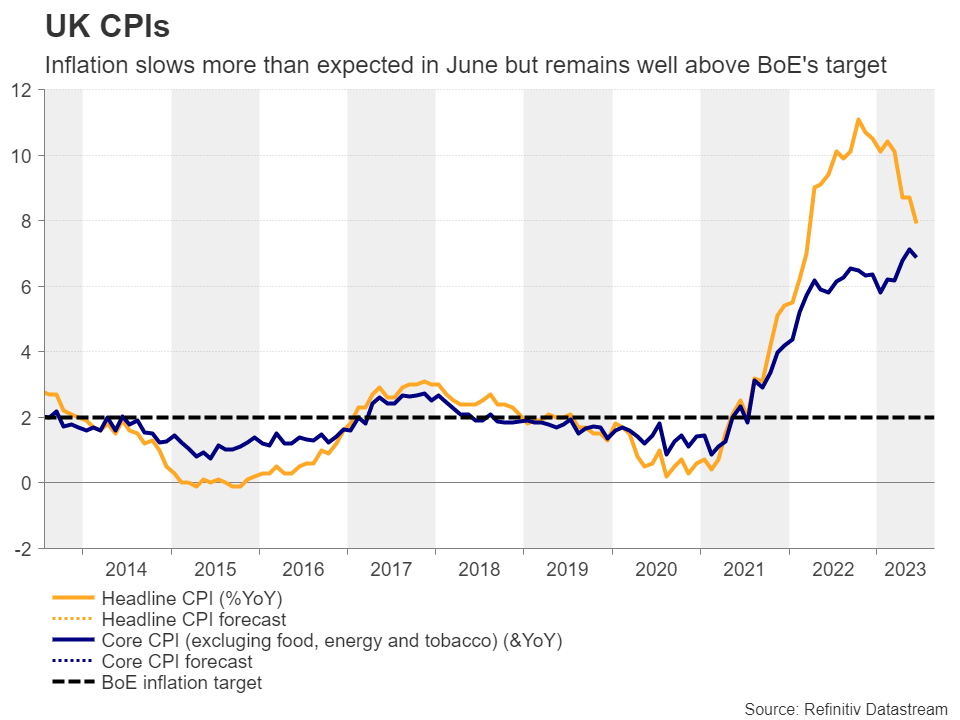

With inflation in the UK slowing by more than expected in June and the July PMIs revealing that UK business activity continues to weaken, investors have become increasingly convinced that the Bank of England may need to slow down the pace of its future hikes and return to 25bps increments. The Bank meets on Thursday at 11:00 GMT and it will be interesting to see whether this will be the case and how the overall outcome could affect the British pound.

BoE accelerates tightening pace in June

At its June meeting, the Bank of England decided to proceed with a 50bps rate increment amid stubbornly high inflation and mounting political pressure, reiterating the guidance that if there were evidence of more price pressures, further tightening in monetary policy would be required.

The decision and remarks by Governor Bailey in the following days that they must act to bring inflation to heel, allowed market participants back then to maintain bets of another 50bps hike at the August meeting and more than 100bps worth of additional rate increases thereafter. This put the BoE at the top spot in terms of hike expectations among other major central banks and allowed the pound to stay in the front seat in terms of year-to-date performance of the major currencies.

But data since then has come on the soft side

Nonetheless, investors changed their minds as soon as the inflation data for June was out. The headline CPI rate fell to 7.9% year-on-year from 8.7%, while the core one slid to 6.9% y/y from 7.1% instead of holding steady as the forecast suggested.

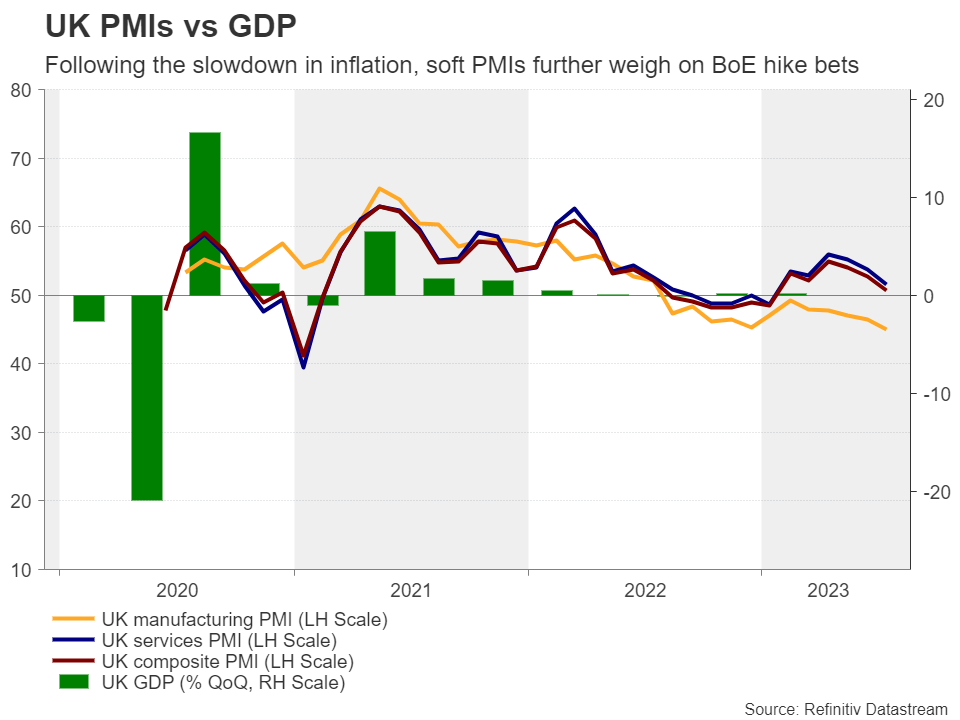

The preliminary PMIs for July revealed that business activity continued to suffer, with the manufacturing index falling further into the contractionary territory, and the composite one, although still pointing to expansion, getting closer to the boom-or-bust zone of 50. On top of that, in the composite report, it was noted that the latest round of prices charged inflation was the slowest for nearly two-and-a-half years, suggesting that inflation may continue its cooling trajectory in the months to come.

Investors expect a return back to 25bps

Putting all these new variables into their calculations, investors are now seeing more chances for a 25bps hike on Thursday, and they have scaled back their bets with regards to the number of basis points worth of additional increments in the next gatherings. According to the UK overnight index swaps (OIS), there is a 70% probability for a quarter-point increase on Thursday, with the remaining 30% still pointing to a double hike. As for the future, conditional upon a 25bps hike now, investors expect around 65bps worth of additional rate increases thereafter.

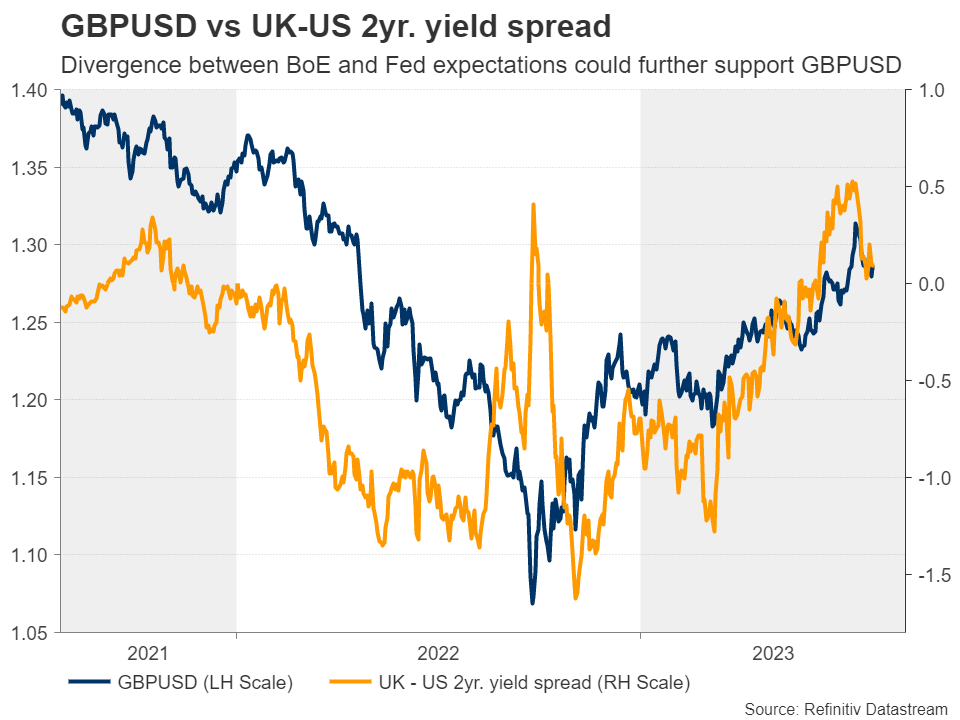

But market pricing could still prove supportive for the pound

Having said all that though, underlying inflation in the UK rests higher than in other major economies and more than triple the BoE’s objective. With that in mind, investors’ implied BoE path, despite being lowered lately, remains steeper than those of other major central banks.

Combined with expectations that the Fed may have concluded its own tightening crusade last week and seen cutting rates massively next year, this divergence could still work in favor of pound/dollar if the BoE remains committed to deliver more in the coming months, even if it hikes by only 25bps at this gathering. Yes, a quarter-point hike could disappoint the 30% expecting more and thereby result in a small retreat, but a hawkish message could help the pair rebound quickly and extend its prevailing uptrend.

For the pound to suffer against its US counterpart post meeting, the BoE may need to signal that they are also getting closer to the end of their own tightening campaign. Now, in the case of another double hike, the pound is likely to shoot higher instantly.

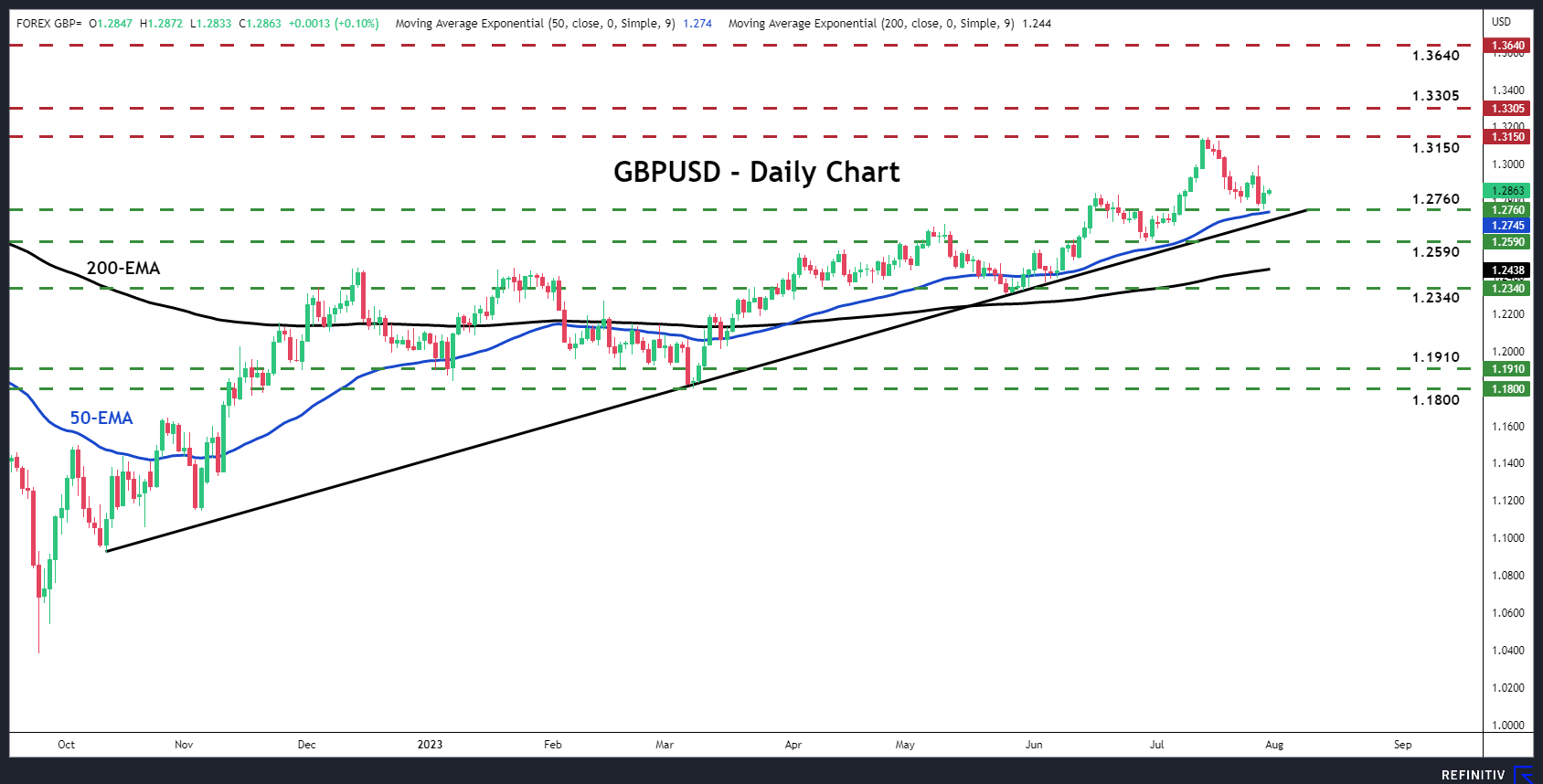

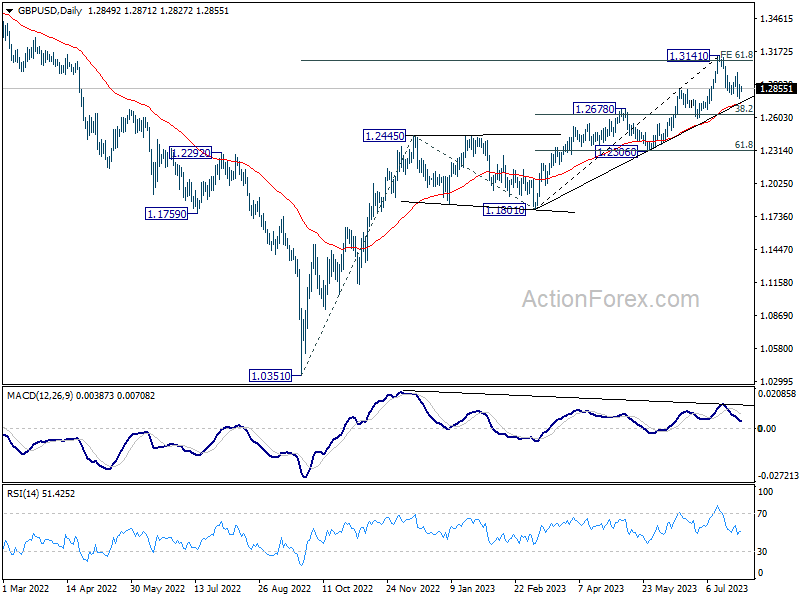

Cable remains in uptrend mode, despite pullback

From a technical standpoint, Cable has been trading in an uptrend mode since the end of September, and above an upward sloping trend line since October 12. Despite pulling back lately, the pair remains above that trendline and above both the 50- and 200-day exponential moving averages (EMAs). All these technical indications keep the picture positive.

If the bulls are strong enough to recharge from near the aforementioned trendline, they could aim for another test near the high of July 14 at 1.3150. If they manage to overcome that obstacle, a higher high would be confirmed, and the 1.3305 barrier may come into play. A break higher could see scope for extensions towards the 1.3640 zone, which offered resistance in February 2022.

A dovish decision could result in a break below the uptrend line, but for a bearish reversal to be fully completed, the pair may need to fall below the 1.2340 key zone, which acted as both support and resistance in the past.

Sunset Market Commentary

Markets

European CPI numbers and Q2 GDP growth were the main (and only) dish for today. The economy expanded more-than-expected 0.3% in the previous quarter after stagnating in Q1. Compared to the same period last year, GDP is 0.6% larger. It’s only the flash reading, so changes may still take place. That said, the figure suggests the economy for the time being is weathering all sorts of headwinds rather well, including coming from the ECB’s aggressive tightening cycle and slowing growth abroad (US, China …). The upside surprise, amongst others, came after a whopping 3.3% q/q advance in Ireland and 0.5% q/q in France. Italy’s economy, on the other hand, unexpectedly contracted by 0.3%. Headline inflation, then, fell 0.1% m/m – as expected – to be up 5.3% y/y in July. It’s only a minor deceleration from the 5.5% in June. In addition, underlying price pressures remain stubborn as ever. Core inflation (ex. food and energy) came in at an unchanged 5.5%, defying expectations/hopes for even the smallest cooldown possible (5.4%). HICP m/m increased for goods, food and energy. Service price pressures hit a new record high of 5.6%. The uptick is probably to a large extend the result of German base effects as the country introduced cheap transport tickets from June to August last year. Core/services inflation is thus unlikely to drop sharply in the summer months.

As the ECB at the gathering last week adopted a data-dependent meeting-by-meeting approach, today’s releases (including GDP) keep a September rate hike firmly on the table for now. Euro area money markets need a bit more convincing though, with a final hike to 4% given a 70% chance give or take. European yields are up 1-2 bps across the curve. US yields painted a similar picture with current changes amounting to less than 1 bp. Markets’ guarded approach today isn’t surprising given the slew of (particularly US) eco data still scheduled for release this week (US ISMs, JOLTS, ADP, payrolls). The Japanese yen on currency markets is strongly underperforming global peers. EUR/JPY rises towards 156.83, nearing the previous 15-year highs of 158+. USD/JPY surpassed 142. The currency is under pressure after the BoJ announced an unscheduled bond buying operation following Friday’s yield surge (which was extended today, 30-y + 11.7 bps). At the other side of the spectrum we find the Aussie and kiwi dollar. Both profit from hopes that China will unveil additional measures to stimulate local consumption to boost the economy. EUR/USD is a tight balance currently turning slightly in favour of the common currency. The pair is filling bids in the 1.103 area. Sterling isn’t going anywhere either as it awaits the Bank of England policy meeting this Thursday.

News & Views

Czech GDP after three quarters in a row grew again in Q2 this year. The economy expanded at a nevertheless slow 0.1% q/q clip. According to the Czech statistical office (CZSO) said domestic “The quarter-on-quarter growth was contributed to by domestic demand while final consumption expenditure of households was stagnating.” Compared to the same quarter in 2022, GDP is 0.6% lower amid a negative influence from lower final household consumption and lower gross capital formation. External demand had a positive influence again, CZSO said. The Czech koruna appreciates today, extending a recent turnaround after having lost more than 4% against the euro since mid-April. EUR/CZK is currently changing hands at 23.89.

Polish CPI dropped 0.2% m/m to be up 10.8% y/y in July, down from 11.5% the month before. Expectations were for the monthly figure to flatline a third month straight while the yearly figure was estimated at 11%. Fueling the decline were food & nonalcoholic drinks (-1.2% m/m). Polish price pressures have eased since February this year, lifting market bets for a cutting cycle to start fairly soon. National Bank of Poland governor Glapinski earlier in July said a 25 bps cut was possible in September in the not so unlikely scenario inflation by then has fallen into the single digits. That’s what is currently priced in by Polish money markets today. The Polish zloty lost marginal territory in a kneejerk move lower before paring losses again. EUR/PLN (4.406) is currently still trading at the weakest (PLN strongest) level since September 2020.

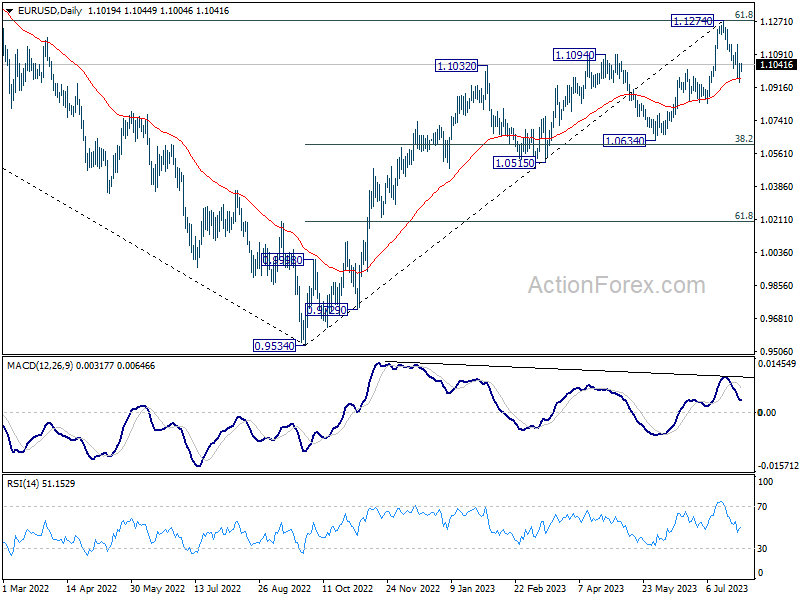

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0958; (P) 1.1003; (R1) 1.1061; More...

Range trading continues in EUR/USD and intraday bias stays neutral. Further fall is expected as long as 1.1148 resistance holds. Below 1.0942 will target 1.0832 support next. Nevertheless, break of 1.1148 will argue that the decline has completed and bring retest of 1.1274 high.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0963) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

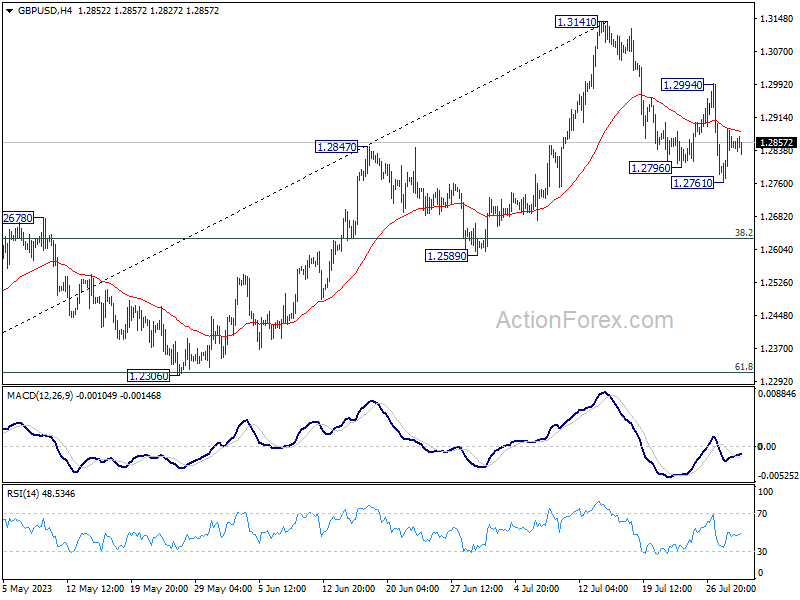

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2780; (P) 1.2834; (R1) 1.2904; More...

Range trading continues in GBP/USD and intraday bias stays neutral. Further decline is in favor as long as 1.2994 resistance holds. Break of 1.2761 will target 55 D EMA (now at 1.2720) and below. Nevertheless, on the upside, break of 1.2994 resistance will argue that the pull back has completed, and bring retest of 1.3141 high.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise from 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal.

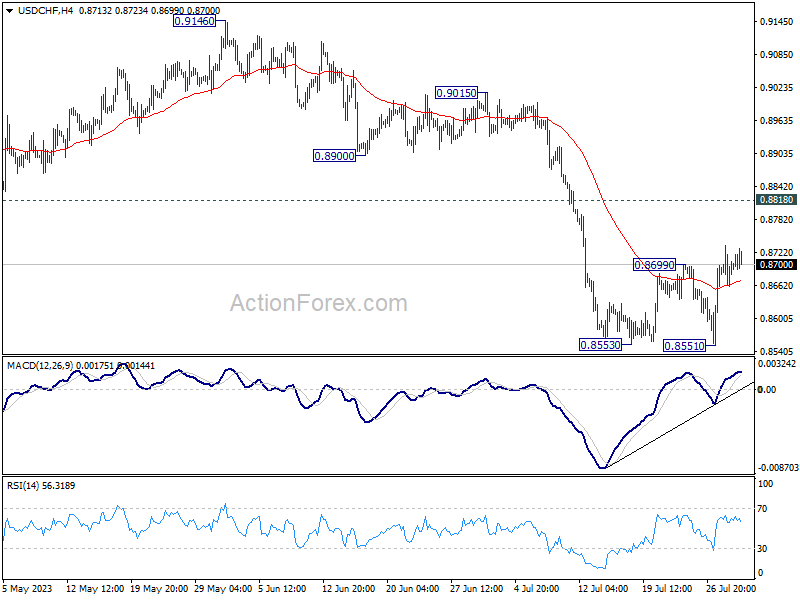

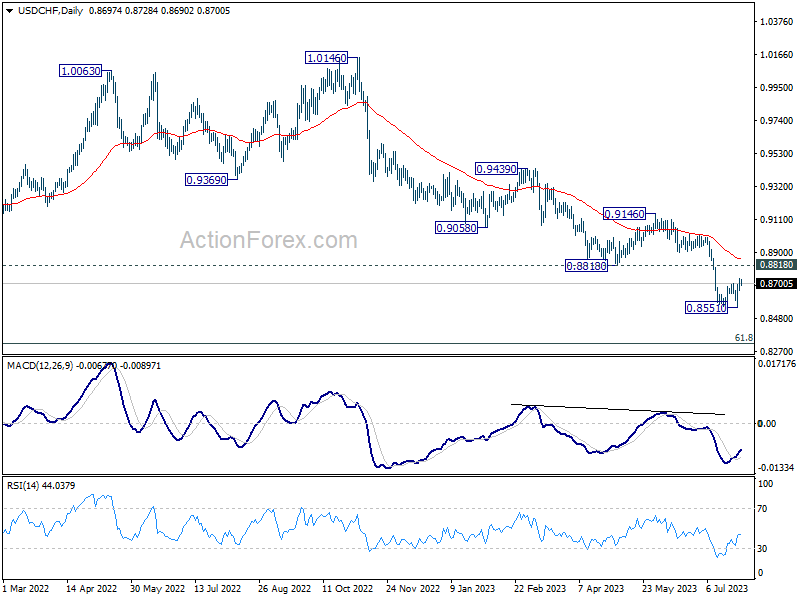

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8665; (P) 0.8701; (R1) 0.8740; More....

USD/CHF's rebound from 0.8551 is in progress, and intraday bias stays on the upside for further rise. But strong resistance could be seen from 0.8818 support turned resistance to complete the recovery and bring down trend resumption. On the downside, firm break of 0.8551 will resume larger down trend from 1.0146, targeting 0.8317 fibonacci level.

In the bigger picture, down trend from 1.0146 is seen as in progress as long as 0.8188 support turned resistance holds. Next target is 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317. However, sustained break of 0.8818 will be the first sign of medium term bottoming, and turn focus back to 0.9146 resistance for confirmation.

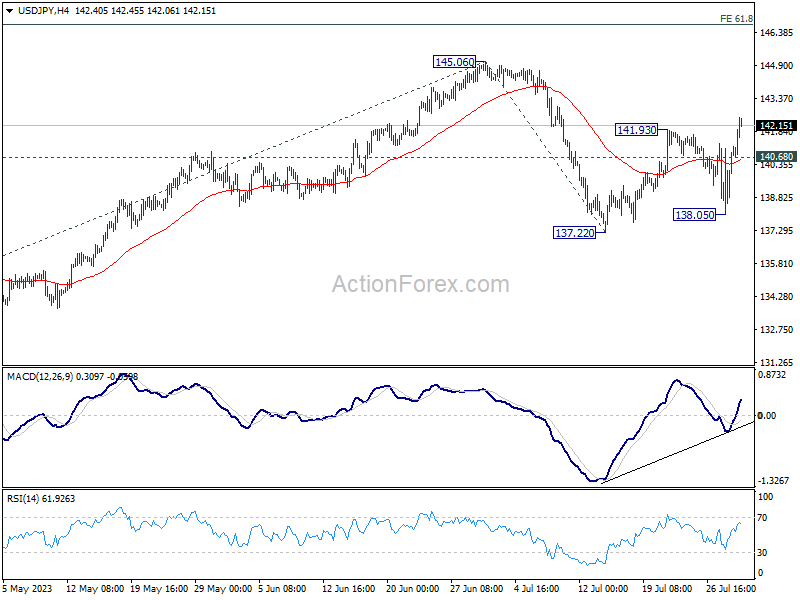

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.10; (P) 140.14; (R1) 142.21; More...

Intraday bias in USD/JPY remains on the upside for retesting 145.60. Firm break there will resume whole rally from 172.20. Next target is 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76. On the downside, below 140.68 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.