Sample Category Title

Has the Bank of Canada Reached its Interest Rate Summit?

Summary

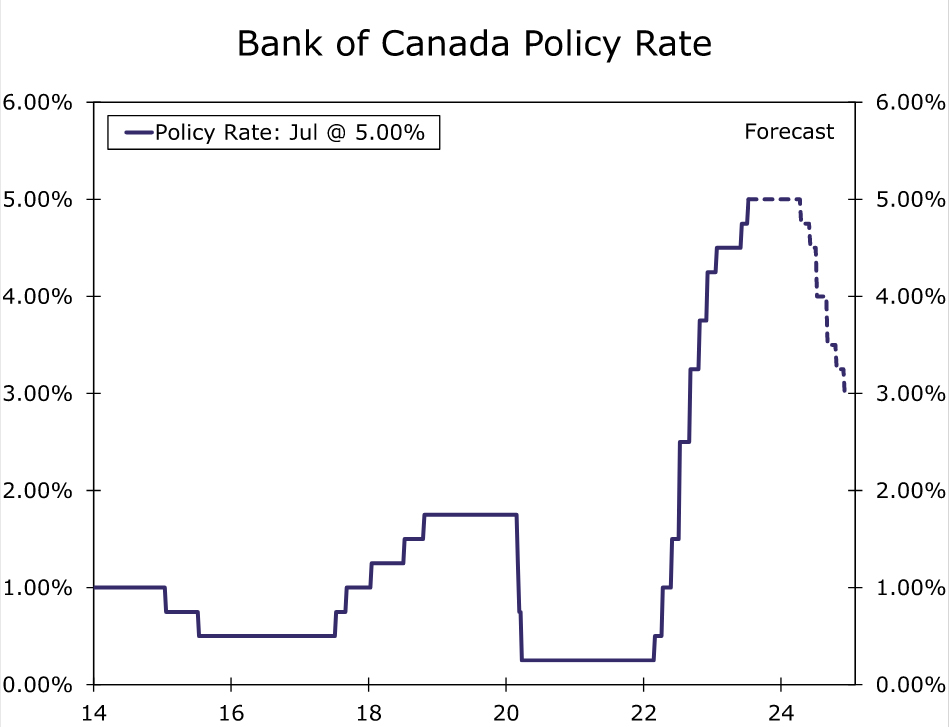

The Bank of Canada (BoC) raised its policy rate 25 bps to 5.00% at last week's announcement, and while BoC Governor Macklem suggested the end of the tightening cycle was close, there were nonetheless several hawlish elements in the announcement. In particular, the Bank of Canada expects excess demand within the Canadian economy to persist for longer than previously anticipated, while also raising its CPI inflation forecasts.

In our view, the onus is on the data to soften to dissuade the central bank from tightening further. So far there is limited evidence of a downshift, with employment, retail sales and GDP expanding at a steady pace, and underlying inflation trends persistent. While at this stage we lean towards the BoC remaining on hold at its September meeting, and for its policy rate of 5.00% to represent to peak for the current cycle, that view is heavily data dependent. If upcoming data, including July employment, the July CPI and Q2 GDP fail to show a perceptible softening, then the risk scenario of a 25 bps rate hike in September to 5.25% could crystalize. Either way, we do not expect rate cuts to begin until well into next year, and forecast a cumulative 200 bps of rate cuts between Q2-2024 and Q4-2024.

Bank of Canada Hikes Rates, Leaves The Door Open For Further Tightening

After resuming its rate hike cycle in June, the Bank of Canada (BoC) followed up with another 25 bps rate hike at its July announcement. While BoC Governor Macklem said “we think we're close” to the end of the tightening cycle, there were nonetheless several hawkish elements to the announcement:

- consumer spending has been stronger than expected, and the housing market has seen some pickup, suggesting more persistent excess demand in the economy.

- despite signs of increasing worker availability, labor market conditions remain tight and wage growth has been around 4%-5%

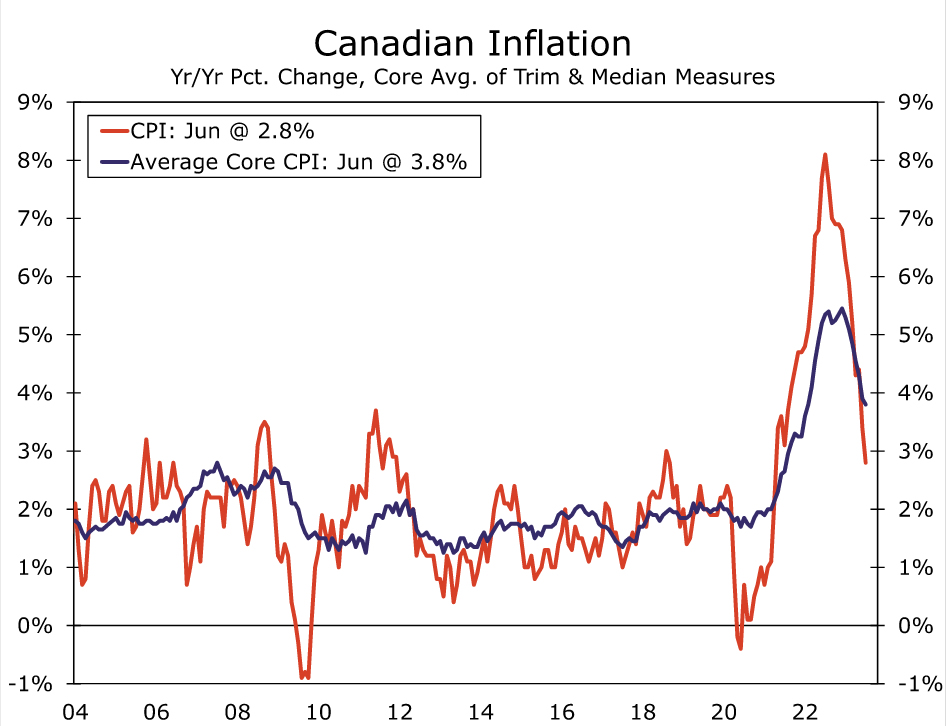

- three-month rates of core inflation have been more persistent than anticipated, running around 3.5%-4% since last September. Inflation is now expected to hover around 3% for the next year before gradually declining towards 2% by mid-2005, a slower return to target than forecast previously.

The updated economic projections from the Bank of Canada were particularly noteworthy. The central bank now sees GDP growth of 1.8% in 2023 (versus 1.4% in April), 1.2% in 2024 (versus 1.3%) and 2.4% in 2025 (versus 2.5%). Specifically, excess demand within the Canadian economy is now not projected to be eliminated until early 2024, three quarters later than previously forecast. CPI inflation is also forecast to be higher at 3.7% for 2023 (versus 3.5% in April), 2.5% in 2024 (versus 2.3%), and 2.1% in 2025 (also 2.1%) Overall, considering the upwards revisions to both growth and inflation forecasts, and with the BoC having raised interest rates at the past two meetings, we believe the onus is on both the growth and activity data to soften to dissuade the central bank from tightening further. For now, however, there appears to mixed evidence of a meaningful downshift in economic trends, meaning a September rate hike remains a possibility.

Growth in Activity Still Resilient

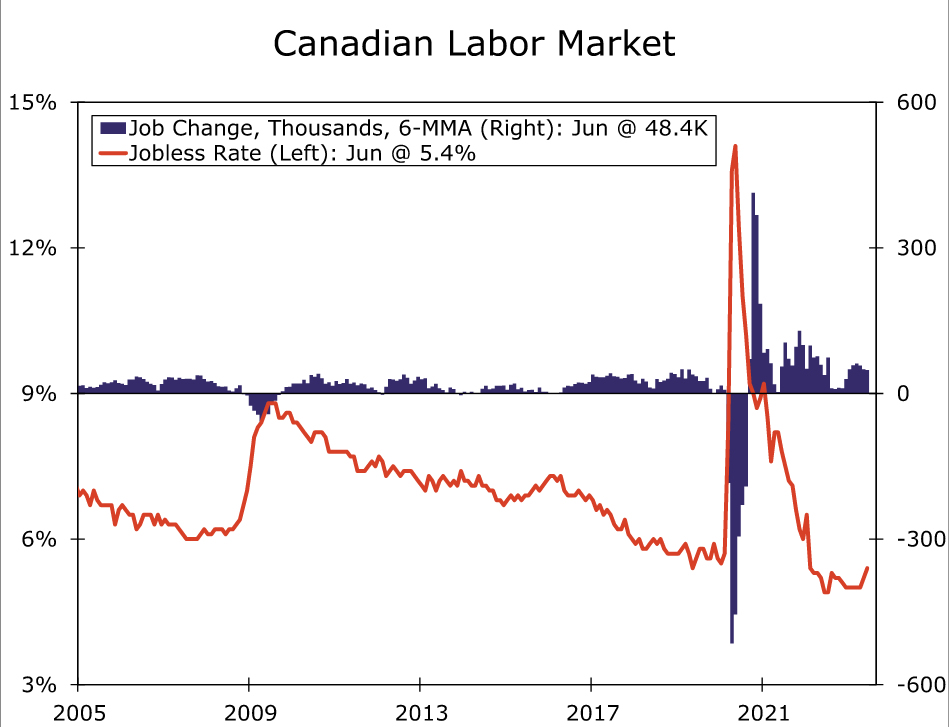

Recent data suggest growth in activity remains steady for now, and in some cases, even sturdy. June employment jumped 59,900, led by a full-time job gain of 109,600. The jobless rate moved slightly higher to 5.4% but, even so, is only moderately above the cyclical low of 4.9% from mid-2022. In terms of other activity indicators, retail sales showed a solid gain in April (1.0% month-over-month) and a further gain in May (0.2%), and although April GDP was flat for the month, Statistics Canada's early estimate is for GDP to rise 0.4% in May. The main negative signal was the BoC's Q2 Business Outlook Indicator, which fell further to -2.2. But that decline in sentiment would likely need to be confirmed by a slowing in the hard data to bring the BoC's tightening cycle to a decisive end. Given the resilience so far this year, it is not clear to us that key activity data between now and the 6 September BoC policy announcement (July employment, May GDP and Q2 GDP, June retail sales) will show a meaningful slowing of momentum, thus keeping a September rate hike in play.

Core Inflation Still Persistent

Meanwhile, on the price front, the progress in addressing underlying inflation pressures remains frustratingly slow. The June headline CPI slowed more than expected to 2.8% year-over-year, but the core CPI measures surprised to the upside, both slowing less than expected. Indeed, on a three-month annualized basis the disinflation of the core CPI measures has continued its stall in recent months, and in fact average core CPI inflation ticked higher to 3.8% on a three-month annualized basis in June. Without a significant downside surprise in the July CPI and/or a sharp slowing in July wage growth, the Bank of Canada's concerns about “sticky” underlying inflation could still be present by the time of September meeting.

For now, we lean towards the Bank of Canada remaining on hold at its September meeting, and for its policy rate of 5.00% to represent the peak for the current cycle. However, that view is heavily data dependent and, as we suggested above, we believe the onus is on the data to soften perceptibly to dissuade the central bank from tightening further. The key figures between now and the 6 September BoC policy announcement include July employment, the July CPI, Q2 GDP, and to a lesser extent June retail sales. Should those data fail to show a perceptible softening, then the risk scenario of a 25 bps rate hike in September to 5.25% could crystalize.

The interest rate sensitivity of Canadian households should still see economic growth slow over time, though to date the impact of higher interest rates has perhaps been blunted to an extent by some deferral in mortgage principal payments. Still, as the BoC's past interest rate increases bite more meaningfully on the consumer, we expect the Bank of Canada to bring its rate hike cycle to an end. Regardless of whether rates peak at 5.00% or 5.25%, we do not expect rate cuts to begin until well into next year, and forecast a cumulative 200 bps of rate cuts between Q2-2024 and Q4-2024, which would see the policy rate end next year around 3.00% to 3.25%.

Week Ahead – Fed, ECB and BoJ Decisions Take Center Stage

Following a relatively quiet week in terms of economic data and events, the spotlight now turns to three major central banks: the Federal Reserve, the European Central Bank, and the Bank of Japan. With investors anticipating only one more hike by the Fed, the focus will be on whether officials will signal the end of this hiking cycle, while with several ECB members pushing back on a September hike, it will be interesting to see whether Lagarde has also changed her stance. As for the BoJ, Governor Ueda’s latest remarks added to the likelihood of no action.

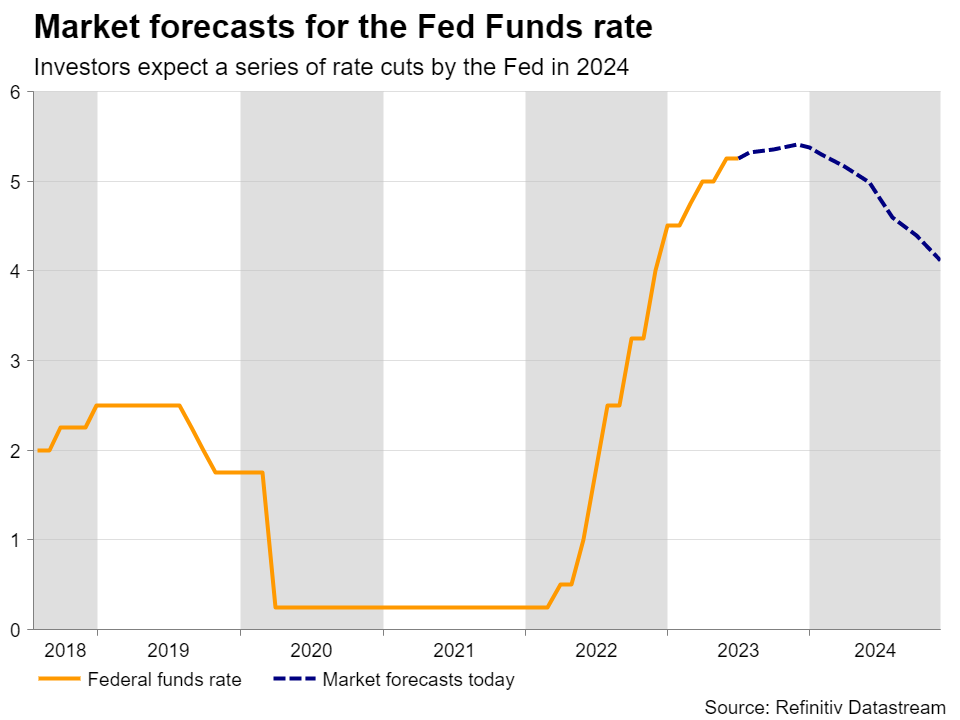

Will the Fed signal the end of this tightening crusade?

Following the dollar’s tumble last week due to the larger-than-expected slowdown in consumer and producer prices, market participants have become more convinced that the Fed will deliver only one more hike before it ends this tightening crusade, while they increased their Fed cut bets for next year.

The last time they met, Fed officials hit the pause button, but the decision had a hawkish flavor, with the ‘dot plot’ pointing to two additional rate increases and Fed Chair Powell pushing back on rate cut expectations by saying that any reductions are “a couple of years out.” Although investors were not convinced back then and neither when Powell testified before Congress, they began lifting their implied path after the Fed chief appeared at a panel discussion organized by the ECB in a hawkish suit.

But that was only until last week’s inflation data. Therefore, Wednesday’s FOMC decision may attract special attention as investors will be eager to get a clearer picture regarding the Fed’s future course of action. Given that a 25bps hike is nearly priced in, should it materialize, the spotlight is likely to turn to the accompanying statement for hints as to whether this was the last hike or whether rates could go higher.

With core inflation more than double the Fed’s 2% objective, Powell and co are unlikely to signal that this tightening crusade has ended. They may reiterate the view that the fight against inflation is not over, while at the press conference, Powell could once again push against rate cut expectations.

However, it remains to be seen whether another round of hawkish rhetoric will be enough to convince market participants enough to scale back their rate cut bets, as some of them may be holding the view that prior hikes could still work in bringing inflation further down in the coming months.

They may get an idea of where inflation may be headed from the prices subindices of the preliminary PMIs for July, due out on Monday, while Friday’s core PCE index could also affect their view after the gathering.

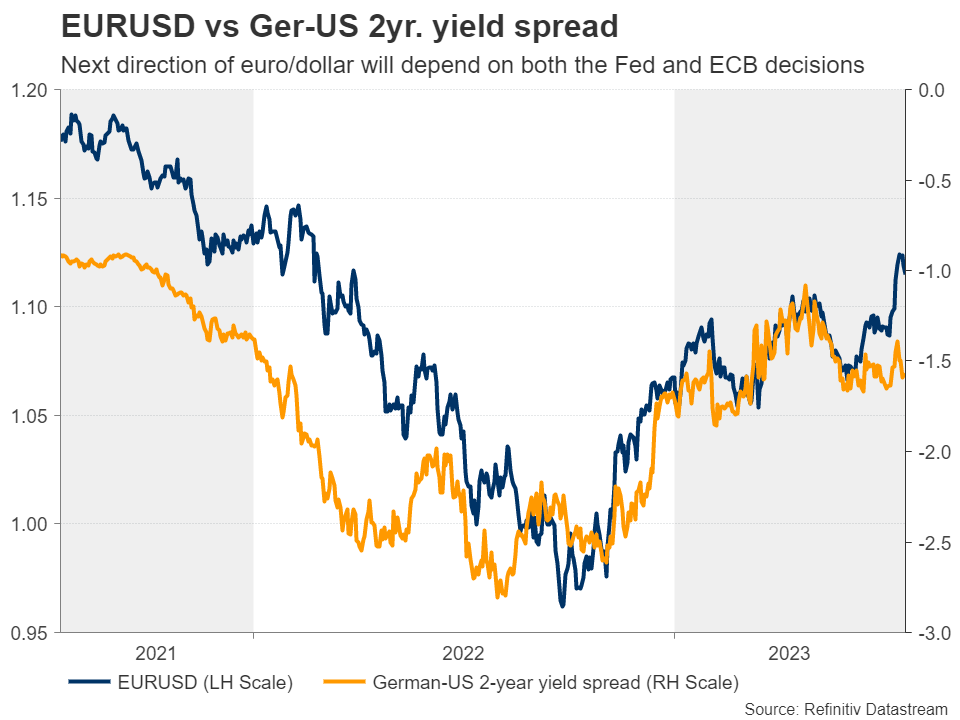

ECB to hike, focus to turn on Lagarde’s remarks

Up until this week, the ECB was seen as much more hawkish than the Fed, expected to deliver two more quarter-point hikes this year and no cuts at all thereafter. That said, with several ECB policymakers arguing that a September hike is not a done deal, that picture has changed. Yes, there are still nearly two quarter-point hikes priced in, but traders now believe that interest rates in the Euro area will end next year 25 basis points below current levels. In other words, conditional upon two hikes being delivered this year, the market expects three rate cuts in 2024.

That pricing may be affected by the preliminary PMIs due out on Monday, and although a July hike seems a done deal, signs that the Eurozone is losing more economic steam could prompt speculation of a softer language in the statement accompanying the decision. The big question though may be whether ECB President Christine Lagarde has also softened her stance or whether she will appear in her hawkish suit again, dismissing the Eurozone’s economic slowdown and prioritizing getting inflation in check.

If Lagarde sticks to her guns the euro is likely to gain and perhaps extend those gains on Friday if preliminary CPI data suggests that inflation in Germany is stickier than previously thought.

BoJ seen on hold as Ueda pushes back on shift expectations

On Friday, the central bank torch will be passed to the BoJ. After testing the psychological, intervention-debated, 145.00 level, dollar/yen came under strong selling interest, hitting a bottom at around 137.25, before rebounding again. The slide was not only the result of a weaker dollar but also a stronger yen as market participants may have started raising bets that the BoJ could tweak its policy at this gathering.

However, earlier this week, Governor Ueda reiterated his remarks that there is still some distance to achieve the 2% inflation target sustainably and stably, signaling determination to maintain ultra-loose policy for now. Traders have started scaling back their bets of an imminent policy shift, allowing dollar/yen to rebound. That said, even if the Bank does not act at this gathering, market participants may be interested in the new inflation projections as they may try to estimate the length of the distance Ueda is referring to.

If those projections are revised notably higher, the yen may gain, even if there is no policy shift now, as they will start speculating for a normalization step perhaps at the next gathering. The opposite may be true if Ueda and his colleagues place more emphasis on maintaining current policy due to inflation being mainly driven by expensive imports rather than domestic demand.

Australia CPIs, UK PMIs, and tech earnings

Elsewhere, Australia’s CPI data for Q2 are coming out on Wednesday. Just this Thursday, the employment data for June came in better than expected, increasing the probability for another hike at the RBA’s August meeting. Currently, investors are evenly split on whether the Bank should hike or not, and the CPIs have the potential to tip the scale.

For the pound, the week starts and ends on Monday with the preliminary PMIs for July. The British currency suffered this week on the back of a larger-than-expected cooling in UK inflation for July, prompting market participants to ditch bets of another double hike in August and take off the table some of the basis points worth of hikes they were expecting thereafter. So, should the surveys reveal that prices charged during July rose at a slower pace than in June, the pound could suffer more as traders reexamine the ultra-hawkish BoE narrative.

Finally, on the earnings front, we get the results from tech giants Alphabet, Microsoft, Meta and Amazon.

Yen Tumbles as BoJ Expected to Keep YCC Intact, Nasdaq’s Rebalancing

USD/JPY Yen dives on reports BOJ sees little need to adjust YCC

Central bank-a-palooza was supposed to start next week, but traders got a head start after reports surfaced that the BOJ saw little urgency to adjust their yield curve control program (YCC). It looks like FX traders are expecting the BOJ to maintain their ultra-loose monetary policy and for the Fed to deliver a quarter-point rate rise and to have a wait-and-see approach about the September meeting. The Japanese yen is the weakest major currency and that could remain the case if risk appetite remains healthy. It seems that while the BOJ stands pat, the other major central banks are tightening and that should continue to drive that interest rate differential trade.

Soft landing hopes are not getting derailed by earnings season so far, in fact market breadth in the stock market continues to improve which could help keep the rally going strong.

Initial Rate Decision Expectations

- The Fed will raise rates by 25bps and likely signal a wait-and-see approach for the September meeting (saving that decision for the end of August at Jackson Hole).

- Analysts are unanimous for the ECB to raise rates all three key rates by 25bps but are unsure what will happen in September

- The BOJ is expected to keep rates steady, no change to YCC, and revise up its inflation forecasts for this year alone.

Soft stochastics suggest euro pullback

The EUR/USD weekly chart shows a bearish bias could be emerging as the slow stochastics overbought conditions is seeing a tentative drop below the 200-week SMA. If bearish momentum accelerates key support will come from the 1.1080 level, with major support eyeing the heavily tested 1.1030 price level. Intraday resistance resides at the 1.1150 level, with major resistance be provided by the psychological 1.1200 handle.

Nasdaq Friday Volatility

The Nasdaq could see excessive volatility at the close as a special rebalancing will address overconcentration in the index by redistributing the weights. In addition to this special rebalancing, traders will have to deal with options expiration.

Three mega-cap tech giants (Apple, Nvidia and Microsoft) make up almost 30% of the weight in the fund, which is not diverse enough for a key index. Some profit-taking might occur ahead of busy next week that contains handful of market moving events that include three big rate decision, several key earnings, and key GDP, ECI , and PCE data.

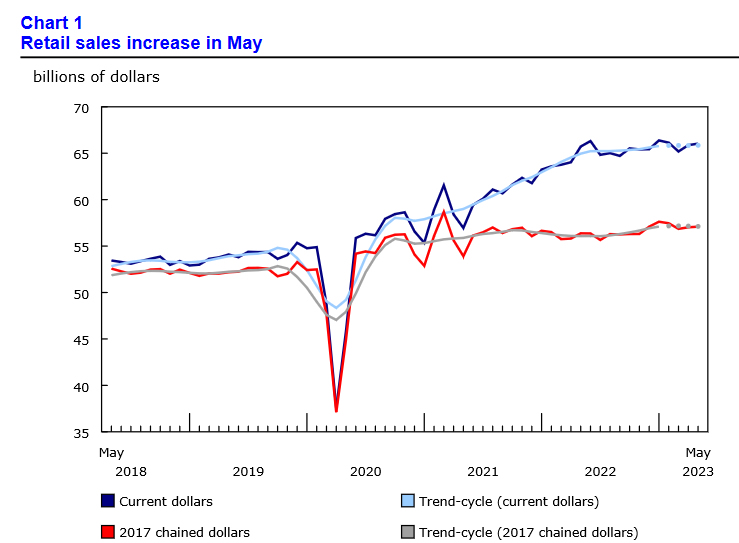

Canada: Auto Sales Drive Retail Sales Growth in May, But Momentum is Fading

Retail sales rose 0.2% month-on-month (m/m) in May, weaker than the Statistics Canada's advanced estimate of 0.5%. April's print was revised down slightly to 1.0% m/m from 1.1% reported originally.

Adjusting for the inflation, the volume of retail sales was 0.1% higher on the month.

As expected, sales at motor vehicle and parts dealers were strong, gaining 0.8% m/m and accounting for all of today's headline growth.

Receipts at gasoline stations and fuel vendors were flat on the month thanks to lower prices at the pump. Meanwhile, April's reading was revised down to -0.4% m/m from +0.3% m/m reported earlier.

Excluding these volatile categories, core retail sales were flat in May, below the consensus estimates of a 0.2% m/m increase.

Gains at electronics and appliance stores (+2.3% m/m), food and beverage (+1.0% m/m), and miscellaneous store retailers (+1.3%m/m) were offset by declines at furniture and home furnishings (-1.6% m/m), building materials and garden equipment dealers (-1.5% m/m), clothing and clothing accessories (-0.8% m/m) general merchandise retailers (-0.7% m/m).

E-commerce sales, which are not included in the headline tally, grew 2.1% m/m after a sizeable decline in April.

Statistics Canada's advanced estimate points to another flat reading in June.

Key Implications

May brought a sizeable deceleration in retail spending growth. The only sector that points to a decisive gain is auto sales, where both nominal and unit sales were up. The rest of the categories are a mixed bag that points to consumers prioritizing spending on groceries at an expense of discretionary purchases. In real terms, second quarter real consumer spending is now tracking just slightly below 1.0% quarter-on-quarter (annualized).

The "greater persistence of excess demand" remains a challenge for the Bank of Canada. The Bank expects that household consumption will slow over the course of next year as additional hikes work its way through the economy. With today's reading, there is evidence that this slowdown is materializing. Still, consumers have financial resources in the form of excess savings, so the path to moderation may not be a smooth one. For now, we expect that monetary policy will remain restrictive until after the first quarter of 2024.

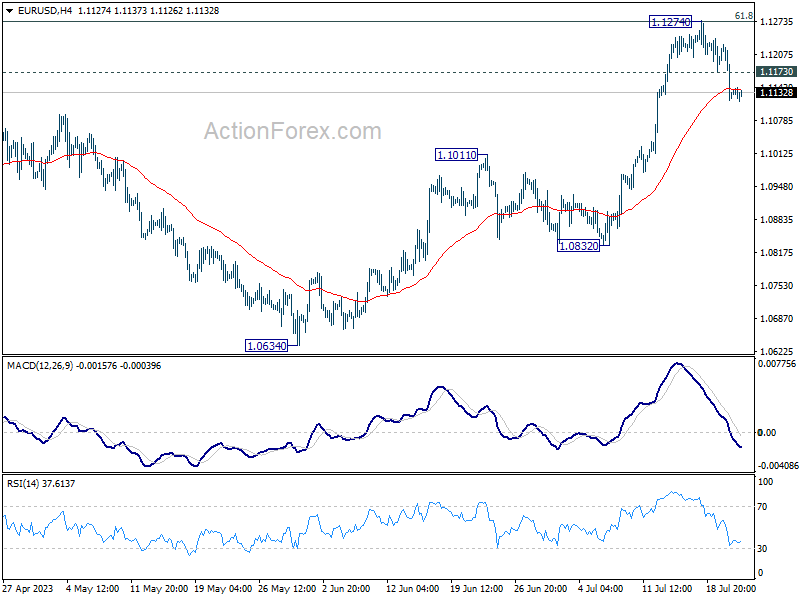

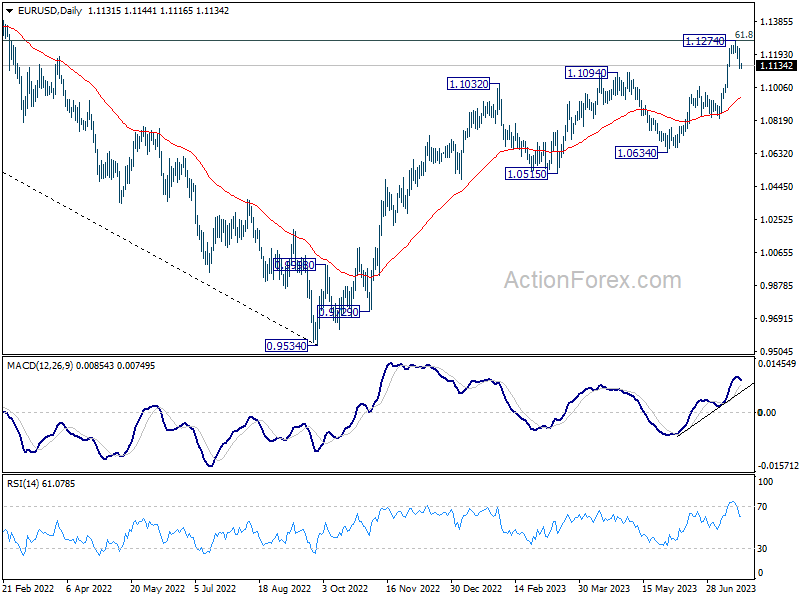

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1089; (P) 1.1159; (R1) 1.1200; More...

Intraday bias in EUR/USD remains on the downside at this points. Correction from 1.1274 short term top could extend towards 1.1011 resistance turned support. For now, risk is mildly on the downside as long as 1.1274 resistance holds, in case of recovery.

In the bigger picture, as rise from 0.9534 extends, focus is now on 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next. Meanwhile, outlook will continue to stay bullish as long as 1.0832 support holds, even in case of deep pull back.

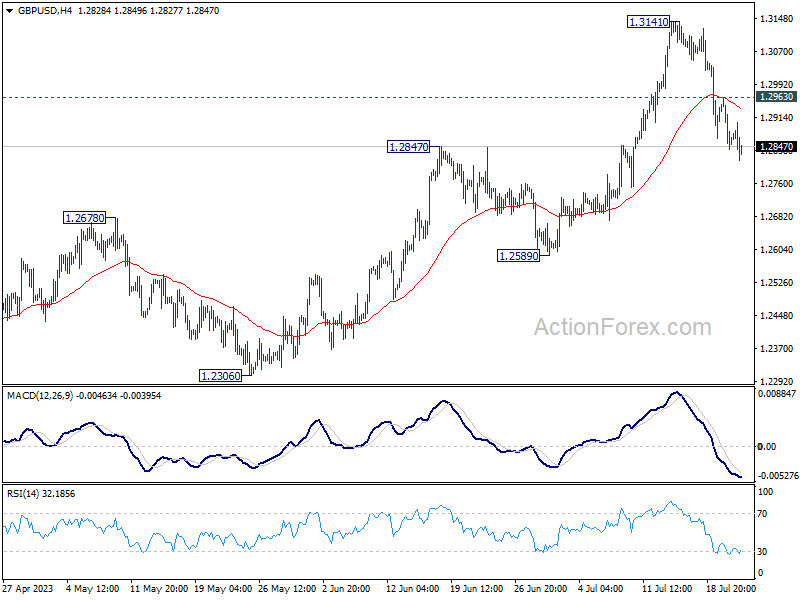

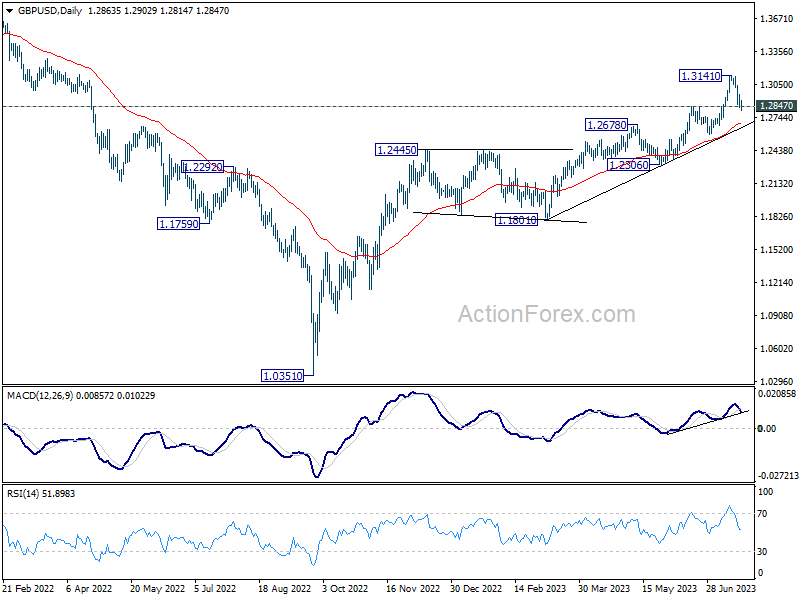

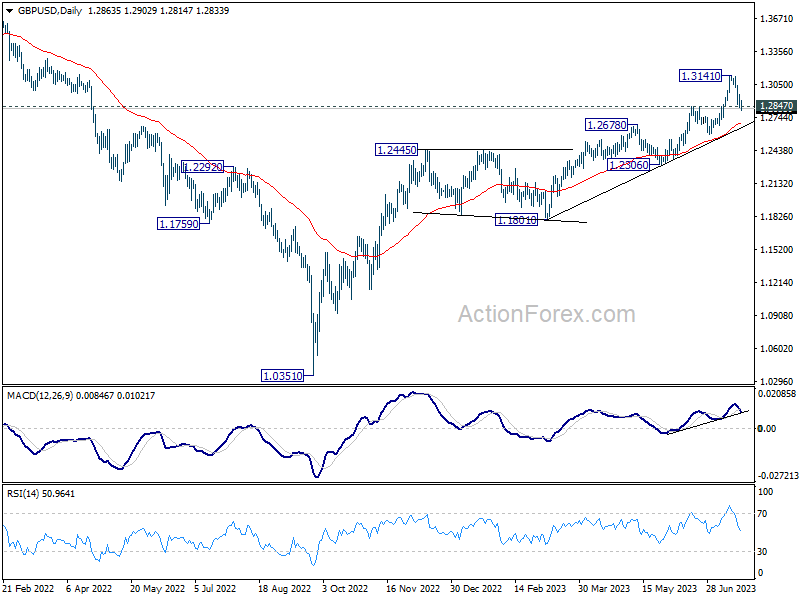

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2816; (P) 1.2891; (R1) 1.2941; More...

Intraday bias in GBP/USD is now on the downside. Sustained trading below 1.2847 resistance turned support will indicate that larger correction is underway. Deeper fall would be seen to 55 D EMA (now at 1.2692). On the upside, break of 1.2963 minor resistance will turn bias back to the upside retest 1.3141 high instead.

In the bigger picture, rise from 1.0351 medium term bottom (2022 low) is in progress. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. Break there will target 1.4248 key long term resistance (2021 high) next. This will now remain the favored case as long as 1.2678 resistance turned support holds.

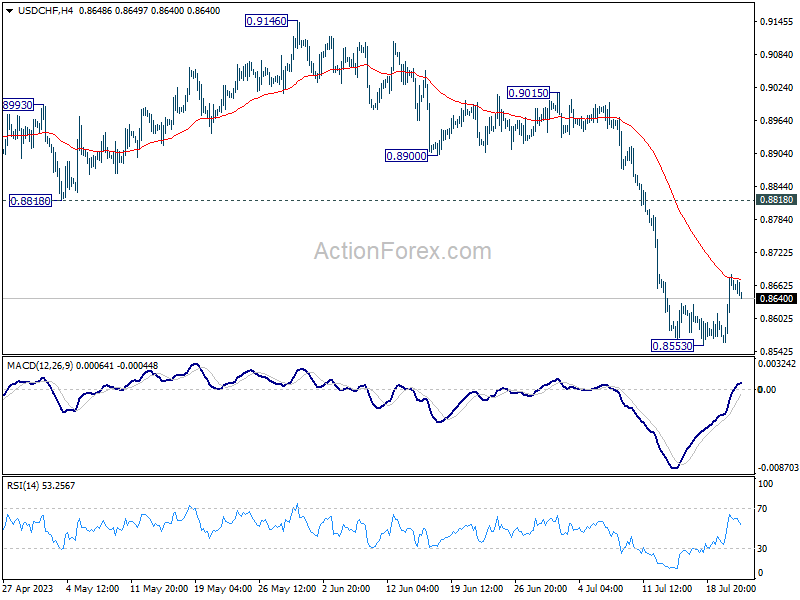

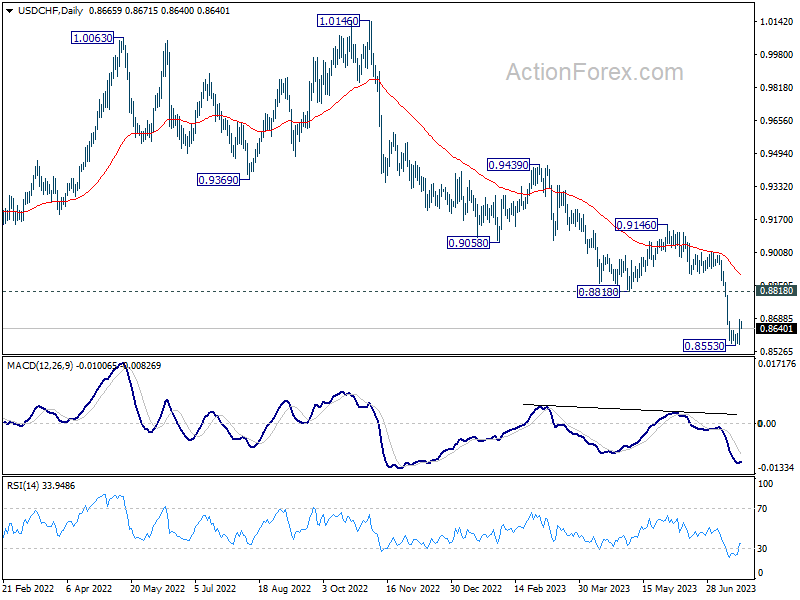

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8591; (P) 0.8637; (R1) 0.8714; More...

Intraday bias in USD/CHF stays mildly on the upside at this point. Rebound from 0.8553 short term bottom would extend towards 0.8818 support turned resistance. For now, risk will stay mildly on the upside as long as 0.8553 holds, in case of retreat.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen to 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317 next.

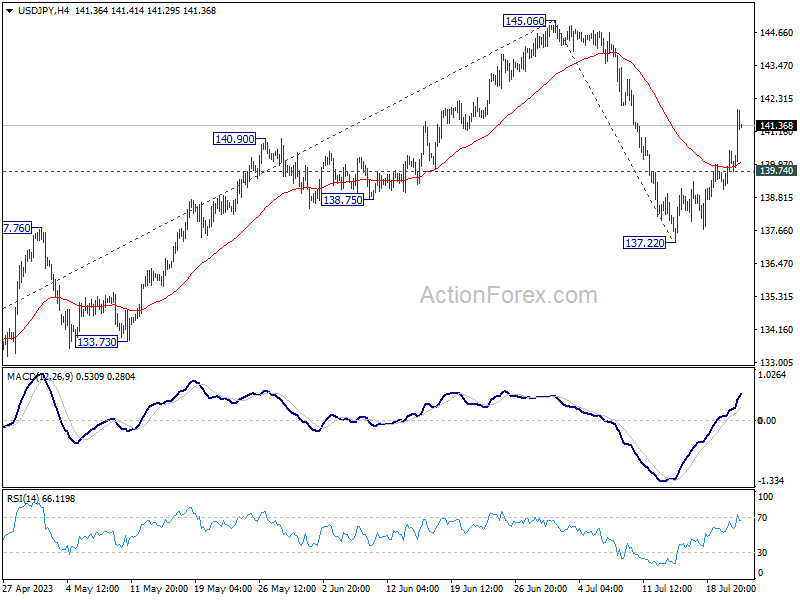

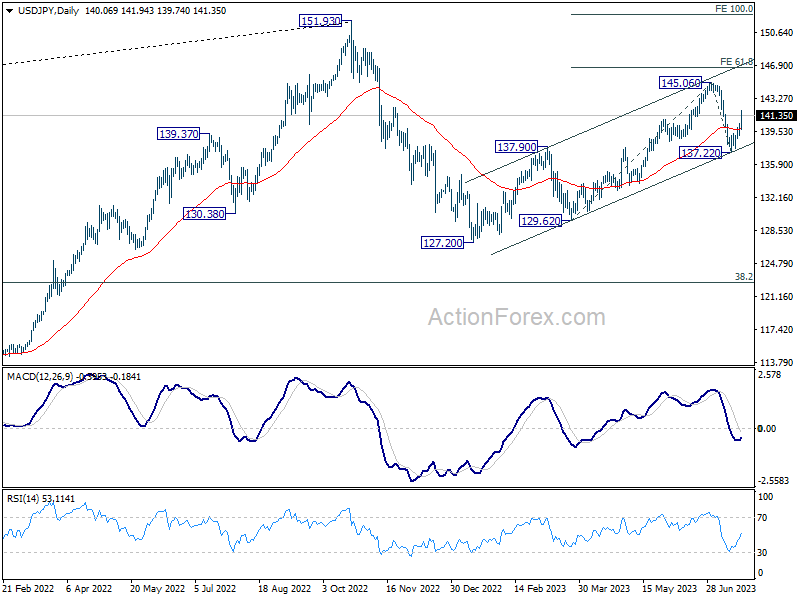

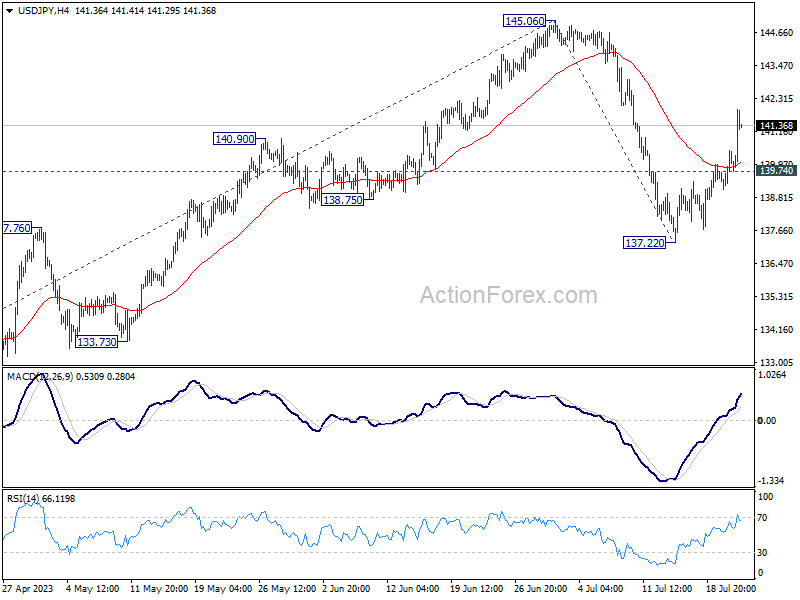

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.29; (P) 139.90; (R1) 140.67; More...

Intraday bias in USD/JPY stays on the upside at this point. Rise from 137.22 should extend to retest 145.05 high first. Firm break there will resume larger rise from 127.20 to 61.8% projection of 129.62 to 127.22 from 145.06 at 146.76 next. On the downside, below 139.74 minor support will bring retest of 137.22 instead.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Current development suggests that the second leg (the rise from 127.20) might not be over yet. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Yen Plunges Amidst BoJ’s Speculations; Fresh Selling Seen in Sterling

Japanese Yen experienced a sharp fall today after reports emerged suggesting that BoJ is "leaning towards" maintaining its current yield curve control policy unchanged in the upcoming meeting next week. The development has come in the wake of Japanese inflation data for June, which showed a relatively unchanged yet high level. Notably, 10-year JGB yield is presently trading comfortably below 0.5%, eliminating any necessity even to adjust the yield cap. This has intensified the pressure on Yen, leading to a significant downward shift.

Meanwhile, Canadian Dollar lost ground after release of weaker-than-expected retail sales data. Sterling, which exhibited relative stability earlier today, faced fresh selling pressure in early US session. Despite these developments, Australian Dollar and New Zealand Dollar are currently underperforming even more, edging out only the beleaguered Yen. On the other end of the spectrum, Swiss Franc currently occupies the strongest position for the day, followed by Dollar and the Euro.

Technically, GBP/USD's break of 1.2847 support argues that it's already in correction to rise from 1.2306 at least. Deeper fall would be seen to 55 D EMA (now at 1.2692), or even below. Downside momentum in GBP/USD would be affected by whether EUR/GBP could power through 0.8717 support turned resistance to confirm bullish trend reversal.

In Europe, at the time of writing, FTSE is up 0.29%. DAX is down -0.33%. CAC is up 0.41%. Germany 10-year yield is down -0.0266 at 2.461. Earlier in Asia, Nikkei dropped -0.57%. Hong Kong HSI rose 0.78%. China Shanghai SSE dropped -0.06%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield rose 0.0063 to 0.466.

Canada retail sales rose 0.2% mom in May, missed expectations

Canada retail sales rose 0.2% mom to CAD 66.0B in May, below expectation of 0.5% mom. Sales increased in five of nine subsectors and were led by increases at motor vehicle and parts dealers (+0.8%) and food and beverage retailers (+1.0%).

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were unchanged in May.

In volume terms, retail sales increased 0.1%.

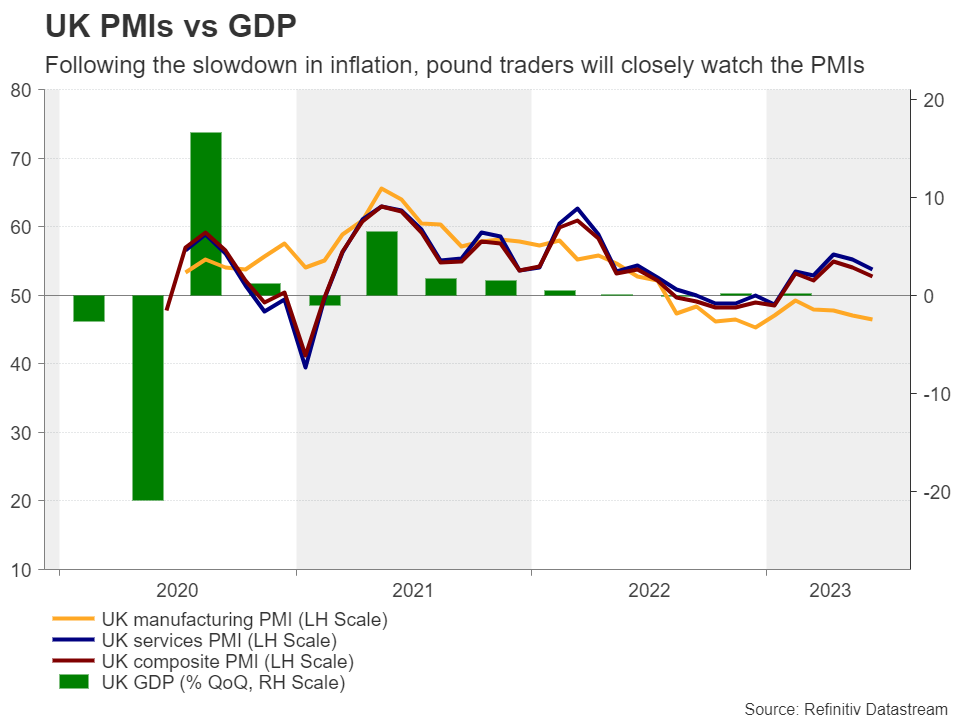

UK retail sales volume rose 0.7% mom in Jun, sales value up 0.7% mom

UK retail sales volume rose 0.7% mom in June, well above expectation of 0.2% mom. Retail sales value also rose 0.7% mom. During the month, sales volumes increased across all the main sectors (food, non-food and non-store retailing) except automotive fuel.

Quarterly comparing with the three months to March, sales volume rose 0.4 in the three months to June. Sales value rose 1.7

Comparing with the same month a year ago, sales volume dropped -1.0% yoy. Sales value rose 4.3% yoy.

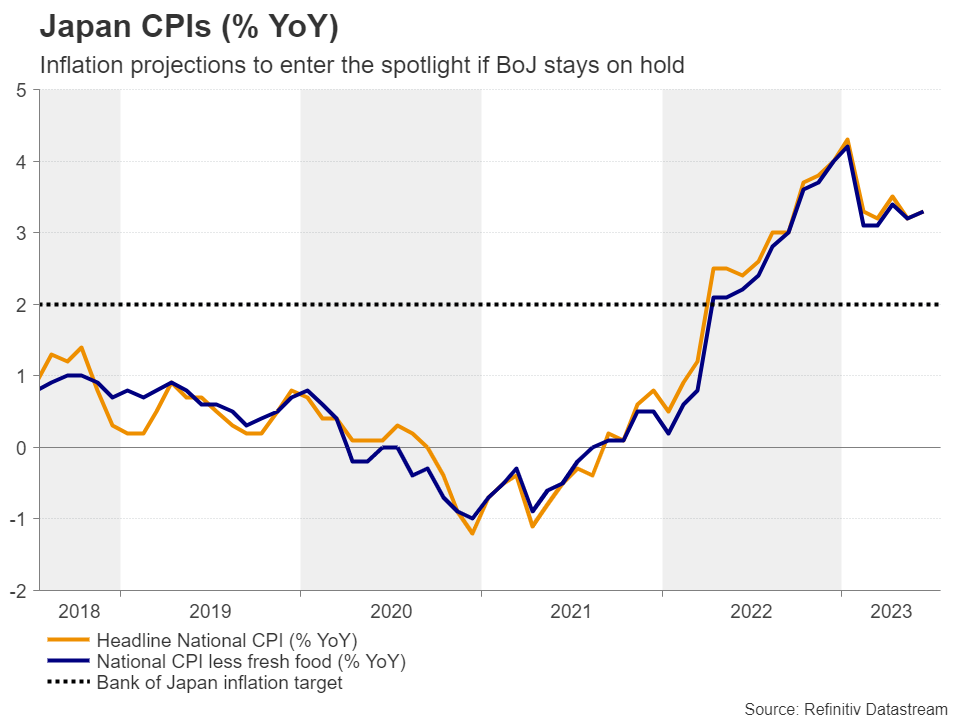

Japan CPI core ticked up to 3.3% yoy, CPI core-core edged down to 4.2% yoy

Japan's Core CPI, which excludes food, matched expectations, ticked up from 3.2% yoy to 3.3% yoy in June. This marks the 15th month that the inflation reading has remained above BoJ's 2% target.

Meanwhile, CPI core-core, which excludes both food and energy, dropped marginally from 4.3% yoy to 4.2% yoy, aligning with expectations. This slight decrease represents the index's first slowdown since January 2022. Headline CPI edged higher from 3.2% yoy to 3.3% yoy, surpassing 3.2% yoy expectation.

Looking at some details, service prices slightly decelerated from 1.7% yoy to 1.6% yoy. Nevertheless, food prices remained robust, rising by 9.2% yoy. A significant increase was also observed in durable household goods, which rose by 6.7% yoy. Conversely, energy prices fell by -6.6% yoy.

These figures raises the probability of BoJ making an upward revision to its inflation outlook for the current fiscal year, with its two-day policy-setting meeting slated for next week. However, BOJ might still perceive the economy as being far from a virtuous cycle of higher wages, robust consumption, and further price hikes. As Governor Kazuo Ueda indicated earlier this week, if this assumption holds true, "our overall narrative on monetary policy remains unchanged."

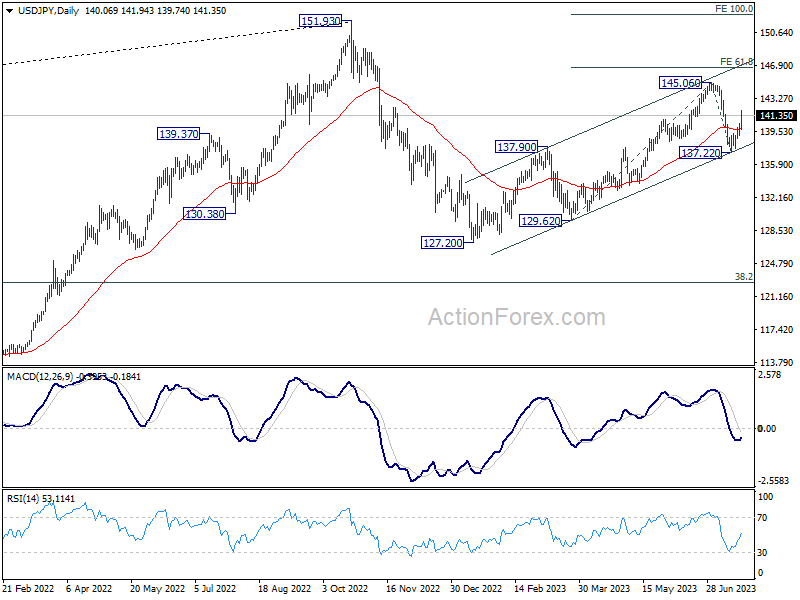

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.29; (P) 139.90; (R1) 140.67; More...

Intraday bias in USD/JPY stays on the upside at this point. Rise from 137.22 should extend to retest 145.05 high first. Firm break there will resume larger rise from 127.20 to 61.8% projection of 129.62 to 127.22 from 145.06 at 146.76 next. On the downside, below 139.74 minor support will bring retest of 137.22 instead.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Current development suggests that the second leg (the rise from 127.20) might not be over yet. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Jul | -30 | -26 | -24 | |

| 23:30 | JPY | National CPI Y/Y Jun | 3.30% | 3.20% | 3.20% | |

| 23:30 | JPY | National CPI Core Y/Y Jun | 3.30% | 3.30% | 3.20% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | 4.20% | 4.20% | 4.30% | |

| 06:00 | GBP | Retail Sales M/M Jun | 0.70% | 0.20% | 0.30% | 0.10% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 17.7B | 20.7B | 19.2B | 15.8B |

| 12:30 | CAD | Retail Sales M/M May | 0.20% | 0.50% | 1.10% | 1.00% |

| 12:30 | CAD | Retail Sales ex Autos M/M May | 0.00% | 0.20% | 1.30% | 1.20% |

| 12:30 | CAD | New Housing Price Index M/M Jun | 0.10% | 0.00% | 0.10% |

Canada retail sales rose 0.2% mom in May, missed expectations

Canada retail sales rose 0.2% mom to CAD 66.0B in May, below expectation of 0.5% mom. Sales increased in five of nine subsectors and were led by increases at motor vehicle and parts dealers (+0.8%) and food and beverage retailers (+1.0%).

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were unchanged in May.

In volume terms, retail sales increased 0.1%.