Sample Category Title

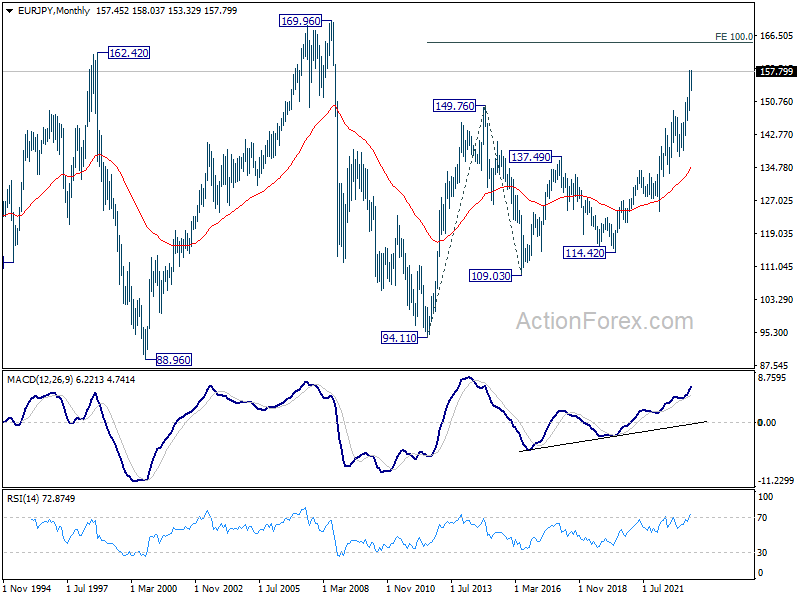

EUR/JPY Weekly Outlook

EUR/JPY's rebound from 153.32 extended higher last week and it's now pressing 157.99 high. Decisive break there will confirm resumption of larger up trend, and target 162.82 projection level next. Further rally will now in favor as long as 155.57 minor support holds, in case of retreat.

In the bigger picture, as long as 151.60 resistance turned support holds, rise from 114.42 (2020 low) is in progress. On resumption, next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. Nevertheless, sustained break of 151.60 will argue that larger correction is already underway.

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 109.03 at 164.68, and possibly further to 169.96 (2008 high).

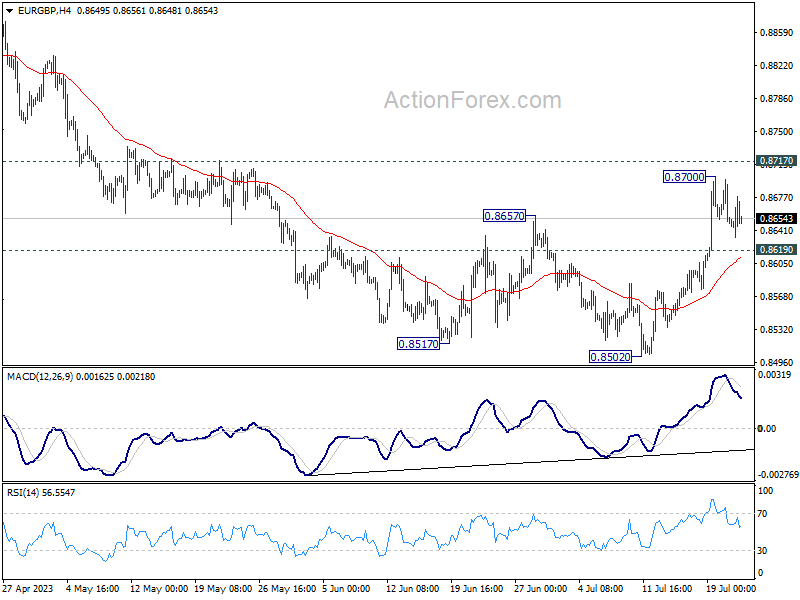

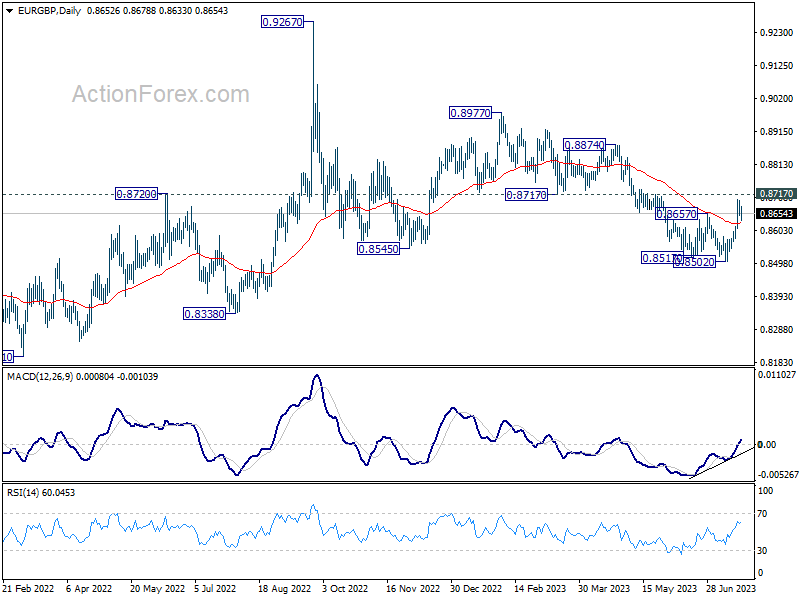

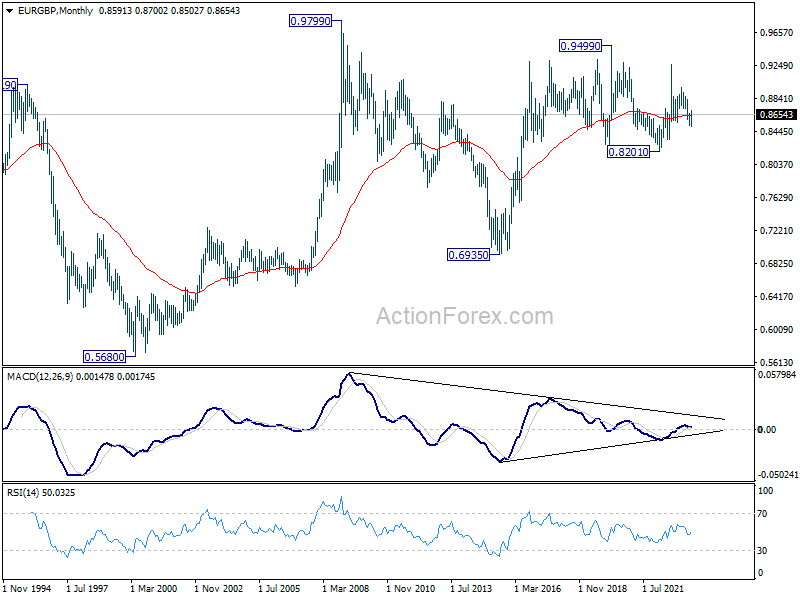

EUR/GBP Weekly Outlook

EUR/GBP's strong rebound and break of 0.8657 resistance last week confirmed short term bottoming at 0.8502. But as a temporary top was formed at 0.8700, initial bias is neutral this week first. On the upside, decisive break of 0.8717 support turned resistance will solidify that fall from 0.8977 has completed a five-wave decline. Further rally should then be seen to 0.8977 resistance next. On the downside, though, below 0.8619 minor support will mix up the outlook and turn bias back to the downside for retesting 0.8502 low.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, break of 0.8502 will resume the decline towards 0.8201 (2022 low).

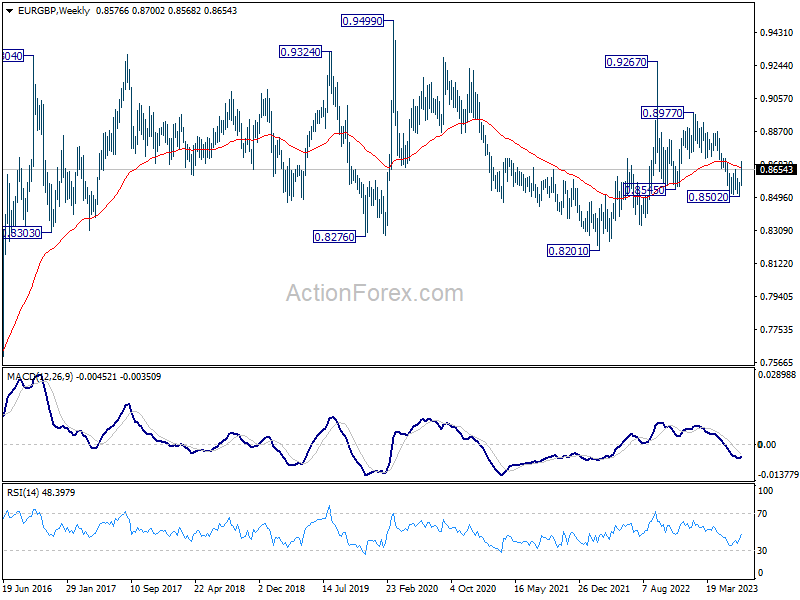

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to extend at a later stage, to 0.9799 (2009 high).

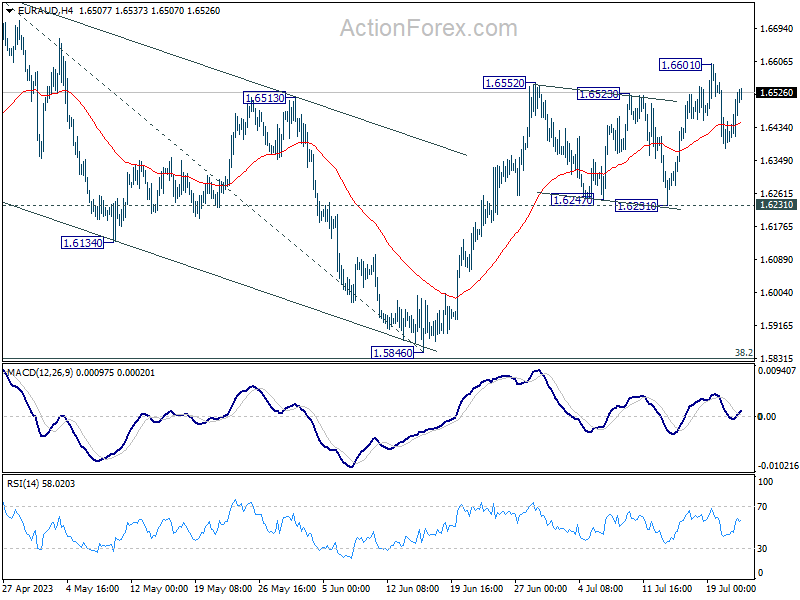

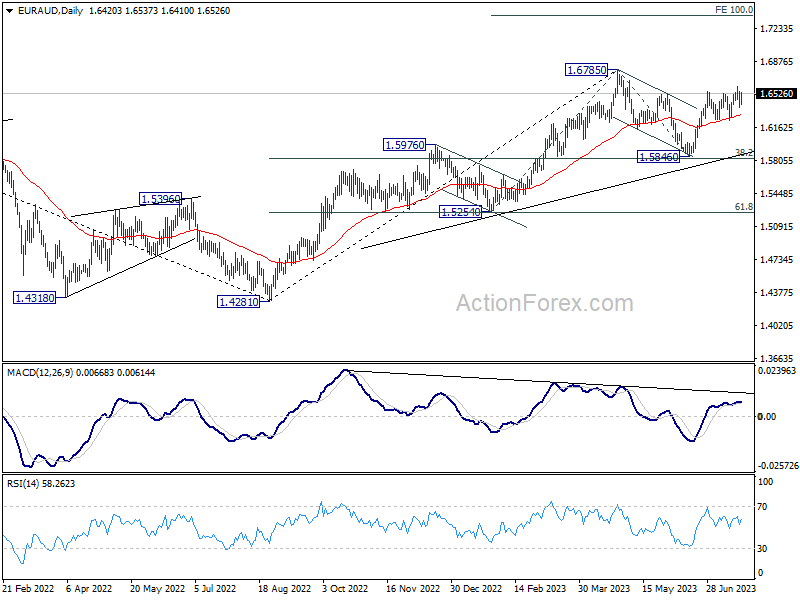

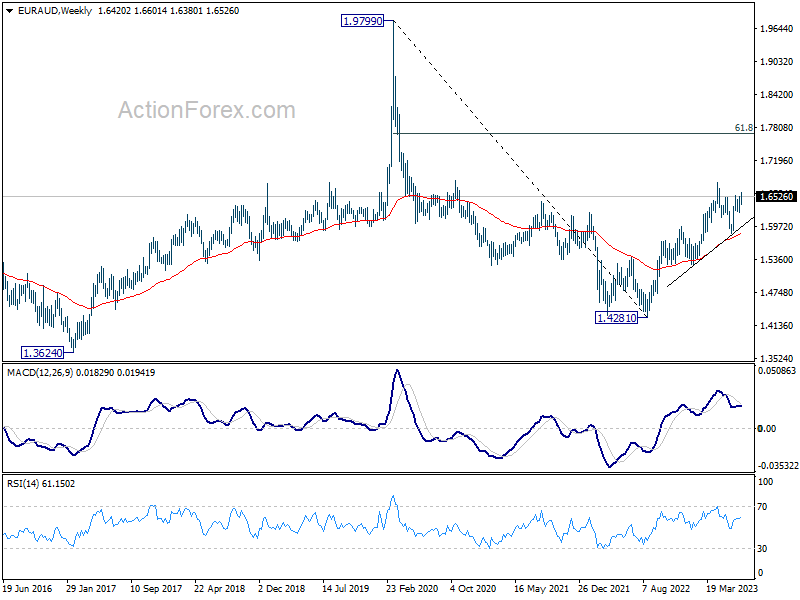

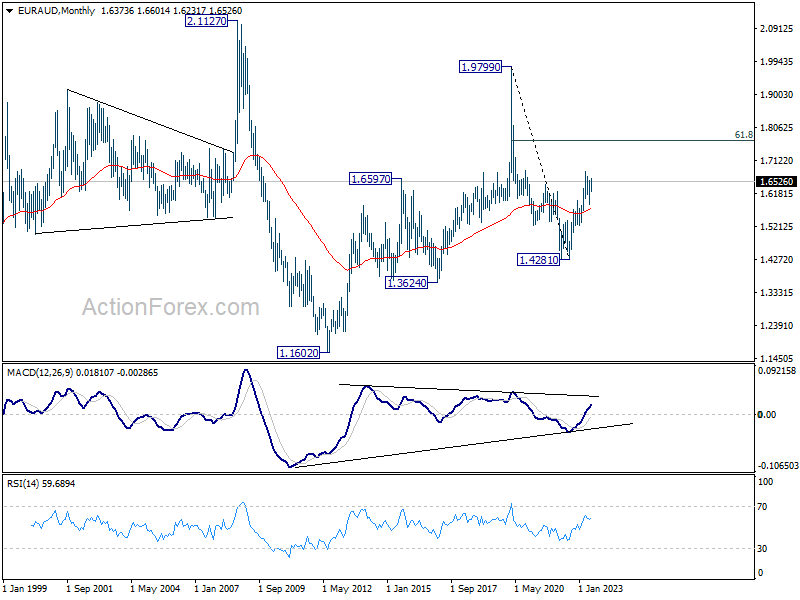

EUR/AUD Weekly Outlook

EUR/AUD's rebound from 1.5846 tried to resume last week, but retreated after edging higher to 1.6601. Initial bias remains neutral this week first. Near term outlook stays cautiously bullish as long as 1.6231 support holds. On the upside, break of 1.6601 will target 1.6785 high next.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5254 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

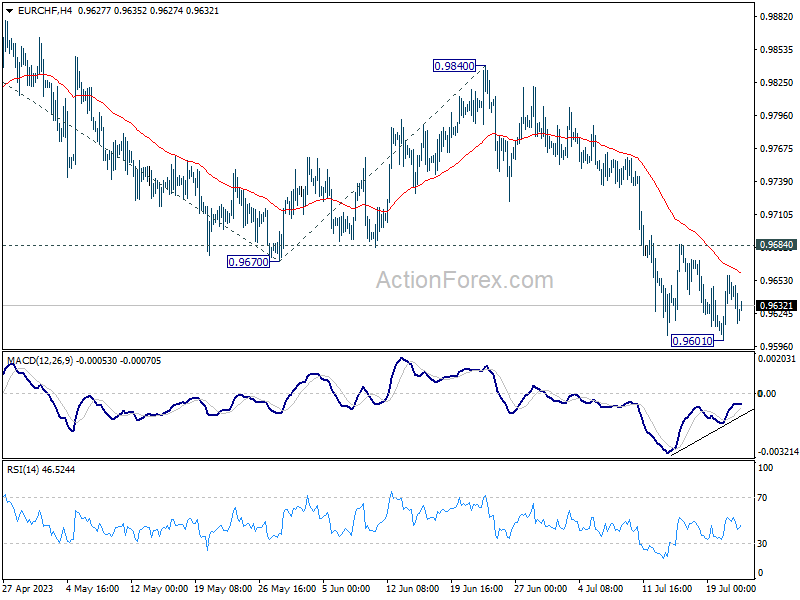

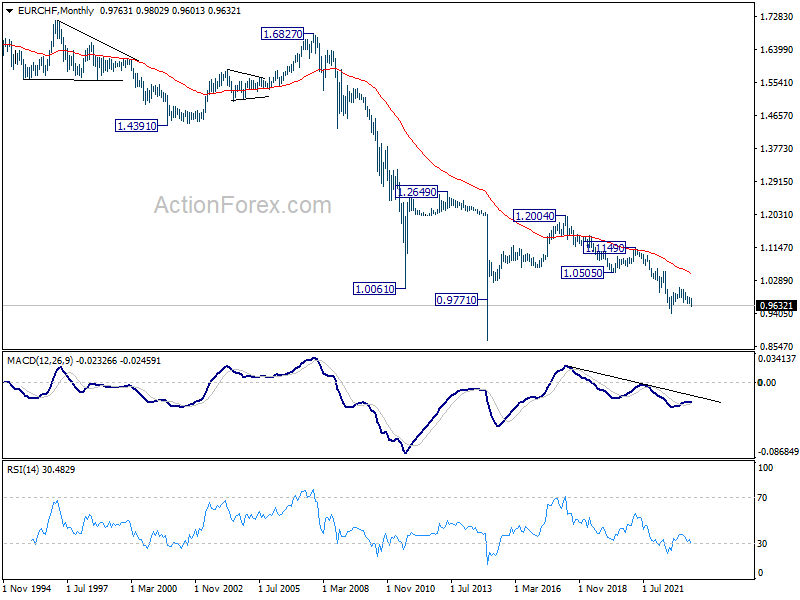

EUR/CHF Weekly Outlook

EUR/CHF edged lower to 0.9601 last week but recovered since then. Initial bias remains neutral this week for consolidations. Outlook will stay bearish as long as 0.9684 resistance holds. On the downside, break of 0.9601 will resume larger decline from 1.0095, and target 100% projection of 0.9995 to 0.9670 from 0.9840 at 0.9515. On the upside, however, break of 0.9684 will indicate short term bottoming, and bring stronger rebound.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9889). Down trend from 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0459) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Week Ahead – Bracing for Next Week’s Earnings, Rate Decisions, and Major Economic Data

US

The Fed is expected to resume raising rates at the July 26th FOMC meeting. Fed funds futures see a 96% chance that the central bank will deliver a quarter-point rate rise, bringin the target range to between 5.25% and 5.50%, almost a 22-year high. The Fed delivered 10 straight rate increases and then paused at the June FOMC meeting. The Fed is going to raise rates on Wednesday and seems poised to be noncommittal with what they will do in September. The economic data has been mixed (strong labor data/cooling pricing pressures) and that should support Powell’s case that they still could deliver a soft landing, a slowdown that avoids a recession. This seems like it will be the last rate hike in the Fed’s tightening cycle, but we will have two more inflation reports before the Fed will need to commit that more rate hikes are no longer necessary.

The Fed will steal the spotlight but there are several other important economic indicators and earnings that could move markets. Monday’s flash PMI report should show both the manufacturing and service sectors continue to soften, with services still remaining in expansion territory. Tuesday’s Conference Board’s consumer confidence report could fuel expectations of a soft landing. Thursday’s first look at Q2 GDP is expected to show growth cooled from 2.0% to 1.8% (0.9%-2.1% consensus range) as consumer spending moderated. Friday contains the release of personal income and spending data alongside the Fed’s preferred inflation and wage gauges. The Q2 Employment Cost Index (ECI) is expected to dip from 1.2% to 1.1%. The personal consumption expenditures price index is expected to cool both on a monthly and annual basis (M/M: 0.2%e v 0.3% prior;Y/Y: 4.2%e v 4.6% prior).

Earnings will be massive this week as we get updates from 3M, AbbVie, Alphabet, Airbus, AstraZeneca, AT&T, Barclays, BASF, Biogen, BNP Paribas, Boeing, Boston Scientific, Bristol-Myers Squibb, Chevron, Chipotle Mexican Grill, Comcast, Exxon, Ford Motor, General Electric, General Motors, GSK, Hermes International, Honeywell International, Intel, Mastercard, McDonald’s, Meta Platforms, Microsoft, Nestle, PG&E, Procter & Gamble, Raytheon Technologies, Samsung Electronics, STMicroelectronics, Texas Instruments, Thermo Fisher Scientific, UniCredit, Unilever, Union Pacific, Verizon Communications, Visa, and Volkswagen

Eurozone

A 25 basis point rate hike from the ECB is almost entirely priced in ahead of the meeting on Thursday but what comes after is up for much more debate. Recent commentary from policymakers suggests a pause may very much be on the cards in September, on the back of some progress in the inflation data recently. The ECB has taken a hawkish stance after meetings until now but next week could see President Lagarde and her colleagues tweak the communication and leave the door open to a pause at the following meeting.

The following day we’ll get some flash inflation data from member states including Germany, France and Spain while the week will start with flash PMIs from Germany, France and the eurozone.

Finally, Spain goes to the polls this weekend in a highly unusual late summer snap election in which a party from the far left or right will probably be kingmaker. It promises to be an eventful week.

UK

A very quiet week for the UK following one in which inflation was shown to be finally falling and interest rate expectations have been pared back. The focus this week will be on the PMI surveys and whether we can get any further signs of disinflationary pressures building and the economy cooling.

Russia

No major economic releases or events next week. Industrial output and central bank reserves are the only items on the agenda.

South Africa

The SARB paused its tightening cycle in July while stressing it is not the end – although it likely is as both headline and core inflation are now comfortably within its 3-6% target range – and that future decisions will be driven by the data. With that in mind, next week is looking a little quiet with the leading indicator on Tuesday and PPI figures on Thursday.

Turkey

Next week offers mostly tier three data, with the only release of note being the quarterly inflation report. Against the backdrop of a plunging currency and a central bank that finally accepts it needs to raise rates but refuses to do so at the pace required, it should make for interesting reading. Though it likely won’t do anything to restore trust and confidence in policymakers to fix the problems.

Switzerland

Next week consists of just a couple of surveys, the KOF indicator and investor sentiment.

China

No key economic data but keep a lookout for a possible announcement of more detailed fiscal stimulus measures in terms of monetary amount, and scope of coverage. Last week, China’s top policymakers announced a slew of broad-based plans to boost consumer spending and support for private companies in share listings, bond sales, and overseas expansion but lacking in detail.

India

No major key data releases.

Australia

Several pieces of data to digest. Firstly, flash Manufacturing and Services PMIs for July out on Monday. Forecasts are expecting a further deterioration for both; a decline in Manufacturing PMI to 47.6 from 48.2 in June, and Services PMI slip to contraction mode at 49.2 from June’s reading of 50.3.

Secondly, the all-important Q2 inflation data out on Wednesday where the consensus is expecting a slow down to 6.2% year-on-year from 7% y/y printed in Q1. Even the expectation for the less volatile RBA-trimmed median CPI released on the same day is being lowered to 6% y/y for Q2 from 6.6% y/y in Q1. These latest inflationary data will play a significant contribution in shaping the expectations of the monetary policy decision outlook for the next RBA meeting on 1 August. Based on the RBA Rate Indicator as of 21st July, the ASX 30-day interbank cash rate futures for the August 2023 contract have priced in a 48% probability of a 25-bps hike to bring the cash rate to 4.35%, that’s an increase in odds from 29% seen in a week ago.

Lastly, retail sales for June out on Friday where the forecast is expected a decline to -0.3% month-on-month from 0.7% m/m in May.

New Zealand

One key data to note will be the Balance of Trade for June out on Monday where May’s trade surplus is being forecasted to reverse to a deficit of -NZ$1 billion from NZ$ 46 million.

Japan

On Monday, we will have the flash Manufacturing and Services PMI for July. The growth in the manufacturing sector is expected to improve slightly to 50 from 49.8 in June while growth in the services sector is forecasted to slip slightly to 53.4 from 54.0 in June.

Next up, on Friday, the leading Tokyo CPI data for July will be released. Consensus for the core Tokyo inflation (excluding fresh food) is expected to slip to 2.9% year-on-year from 3.2% y/y in June, and Core-Core Tokyo inflation (excluding fresh food & energy) is forecasted to dip slightly to 2.2% y/y from 2.3% y/y in June.

Also, BoJ’s monetary policy decision and latest economic quarterly outlook will be out on Friday as well. The consensus is an upgrade of the FY 2023 inflation outlook to be above 2% and a Reuters report out on Friday, 21 July stated that it is likely no change to the current band limits of the “Yield Curve Control” (YCC) programme on the 10-year JGB yield based on five sources familiar with the BoJ’s thinking. Prior to this Reuters news flow, there is a certain degree of speculation in the market place the BoJ may increase the upper limit of the YCC to 0.75% from 0.50%.

Singapore

Two key data to watch out for. Firstly, inflation for June is out on Monday. Consensus is expecting core inflation to cool down to 4.2% year-on-year from 4.7% y/y in May. If it turns out as expected, it will be the second consecutive month of a slowdown in inflationary pressure.

Next up, industrial production for June out on Wednesday, another month of negative growth is expected at -7.5% year-on-year but at a slower magnitude than -10.8% y/y recorded in May.

Markets

Energy

The oil market looks like it is going to continue to tighten as OPEC+ delivers on their pledges and as China improves business conditions. Energy traders will have a lot to stay on top of this week. In addition to the global flash PMI readings, a handful of major energy companies earnings, and the standard weekly stockpile data points, there will be a few energy conferences which could provide some insight for the future shifts with supply and demand.

Key earnings from Shell, TotalEnergies, Exxon and Chevron will provide key insights on capex spending and expectations for future drilling. The G20 Energy Transitions Ministerial meeting will focus on clean initiatives. The 5th International Conference on Power and Energy Technology will provide insights on Chinese crude demand outlooks.

Gold

Gold’s is poised for a third straight weekly advance as Wall Street anticipates the Fed could be done with their rate hiking cycle after next week. A strong labor market however keeps the risk for more tightening to occur in the fall, so gold isn’t quite ready to make a move back above the $2000 level. The FOMC decision will be key for gold and could trigger a corrective move below the $1,960 level if the Fed decides to keep optionality on the table for September. If Powell is able to signal that it seems they are done tightening, gold may attempt to capture the $1980 level, with $2,000 being a major psychological barrier.

Crypto

Bitcoin remains anchored around the $30,000 level as no major developments have so far occurred with government action or regulation. The past week saw the SEC acknowledge ETF filings from BlackRock, Wise Origin Bitcoin Trust, WisdomTree Bitcoin Trust, VanEck Bitcoin Trust and Invesco Galaxy Bitcoin ETF.

The cryptoverse is still celebrating a partial victory after a federal judge said Ripple’s XRP token wasn’t a security when sold to retail investors on exchanges. The ruling is potentially paving the way for the House Republicans’ bill for a US crypto market overhaul. The Bitcoin consolidation seems like it isn’t going away just yet but it could if the House’s bill advances or if the Fed delivers a hawkish surprise.

Saturday, July 22

Economic Events:

- G20 Energy Transitions Ministerial meeting in India.

Sunday, July 23

Economic Events:

- Spanish national election

- Italian PM Meloni hosts Euro-African conference on migration in Rome.

Monday, July 24

Economic Data/Events:

- US Flash PMIs

- European Flash PMIs: Eurozone, Germany, France and the UK

- Japan Manufacturing PMI

- New Zealand trade

- Singapore CPI

- Taiwan jobless rate, industrial production

- Taiwan holds annual Han Kuang military drills

Tuesday, July 25

Economic Data/Events:

- US July Conf. Board consumer confidence: 112.0e v 109.7 prior

- Germany IFO business climate

- Eurozone bank lending survey.

- Mexico international reserves

- Earnings results form Alphabet, 3M Company and Microsoft Corp

- EU agriculture ministers meet in Brussels.

Wednesday, July 26

Economic Data/Events:

- FOMC rate decision: Expected to raise rates by 25bps, bringing target range to 5.25-5.50%.

- US new home sales

- Australia CPI

- Russia industrial production

- Singapore industrial production

- Bank of Canada releases summary of deliberations.

- Australian PM Albanese makes first official trip to Wellington, New Zealand

- EU commissioners Breton, Gentiloni and Hahn speaks at Austria’s Salzburg Summit

- Earnings from Meta Platforms

Thursday, July 27

Economic Data/Events:

- US Q2 Advance GDP Q/Q: 1.8%e v 2.0% prior, durable goods orders, initial jobless claims, wholesale inventories

- China industrial profits

- ECB rate decision: Expected to raise rates by 25bs to 4.25%

- Mexico unemployment, trade

- Singapore unemployment

- Russia hosts African heads of state for a summit

- Italy PM Meloni meets with President Biden at the White House

Friday, July 28

Economic Data/Events:

- BOJ rate decision: To keep rates steady, no change to YCC, possibly upgrade price outlook

- US PCE Core Deflator, consumer income, employment cost index, University of Michigan consumer sentiment

- Australia retail sales

- Canada monthly GDP

- Eurozone economic confidence, consumer confidence

- France GDP, CPI

- Germany CPI

- Japan Tokyo CPI, BOJ rate decision

- Singapore home prices

- Spain CPI, GDP

Sovereign Rating Updates:

- Netherlands (Moody’s)

Summary 7/24 – 7/28

Monday, Jul 24, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:45 | NZD | Trade Balance NZD Jun | 46M | |

| 23:00 | AUD | Manufacturing PMI Jul P | 48.2 | |

| 23:00 | AUD | Services PMI Jul P | 50.3 | |

| 00:30 | JPY | Manufacturing PMI Jul P | 50.1 | 49.8 |

| 07:15 | EUR | France Manufacturing PMI Jul P | 46.1 | 46 |

| 07:15 | EUR | France Services PMI Jul P | 48.4 | 48 |

| 07:30 | EUR | Germany Manufacturing PMI Jul P | 41.2 | 40.6 |

| 07:30 | EUR | Germany Services PMI Jul P | 53.1 | 54.1 |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul P | 43.5 | 43.4 |

| 08:00 | EUR | Eurozone Services PMI Jul P | 51.5 | 52 |

| 08:30 | GBP | Manufacturing PMI Jul P | 46.1 | 46.5 |

| 08:30 | GBP | Services PMI Jul P | 53.1 | 53.7 |

| 13:45 | USD | Manufacturing PMI Jul P | 46.3 | |

| 13:45 | USD | Services PMI Jul P | 54.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:45 | NZD | Trade Balance NZD Jun | |

| Forecast: | Previous: 46M | ||

| 23:00 | AUD | Manufacturing PMI Jul P | |

| Forecast: | Previous: 48.2 | ||

| 23:00 | AUD | Services PMI Jul P | |

| Forecast: | Previous: 50.3 | ||

| 00:30 | JPY | Manufacturing PMI Jul P | |

| Forecast: 50.1 | Previous: 49.8 | ||

| 07:15 | EUR | France Manufacturing PMI Jul P | |

| Forecast: 46.1 | Previous: 46 | ||

| 07:15 | EUR | France Services PMI Jul P | |

| Forecast: 48.4 | Previous: 48 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jul P | |

| Forecast: 41.2 | Previous: 40.6 | ||

| 07:30 | EUR | Germany Services PMI Jul P | |

| Forecast: 53.1 | Previous: 54.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul P | |

| Forecast: 43.5 | Previous: 43.4 | ||

| 08:00 | EUR | Eurozone Services PMI Jul P | |

| Forecast: 51.5 | Previous: 52 | ||

| 08:30 | GBP | Manufacturing PMI Jul P | |

| Forecast: 46.1 | Previous: 46.5 | ||

| 08:30 | GBP | Services PMI Jul P | |

| Forecast: 53.1 | Previous: 53.7 | ||

| 13:45 | USD | Manufacturing PMI Jul P | |

| Forecast: | Previous: 46.3 | ||

| 13:45 | USD | Services PMI Jul P | |

| Forecast: | Previous: 54.4 | ||

Tuesday, Jul 25, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Jul | 88 | 88.5 |

| 08:00 | EUR | Germany IFO Current Assessment Jul | 93 | 93.7 |

| 08:00 | EUR | Germany IFO Expectations Jul | 83 | 83.6 |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y May | -1.40% | -1.70% |

| 13:00 | USD | Housing Price Index M/M May | 0.60% | 0.70% |

| 14:00 | USD | Consumer Confidence Jul | 112.1 | 109.7 |

| 14:00 | USD | Richmond Fed Manufacturing Index Jul | -10 | -7 |

| 23:50 | JPY | Corporate Service Price Index Y/Y Jun | 1.50% | 1.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Jul | |

| Forecast: 88 | Previous: 88.5 | ||

| 08:00 | EUR | Germany IFO Current Assessment Jul | |

| Forecast: 93 | Previous: 93.7 | ||

| 08:00 | EUR | Germany IFO Expectations Jul | |

| Forecast: 83 | Previous: 83.6 | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y May | |

| Forecast: -1.40% | Previous: -1.70% | ||

| 13:00 | USD | Housing Price Index M/M May | |

| Forecast: 0.60% | Previous: 0.70% | ||

| 14:00 | USD | Consumer Confidence Jul | |

| Forecast: 112.1 | Previous: 109.7 | ||

| 14:00 | USD | Richmond Fed Manufacturing Index Jul | |

| Forecast: -10 | Previous: -7 | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Jun | |

| Forecast: 1.50% | Previous: 1.60% | ||

Wednesday, Jul 26, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Jun | 5.40% | 5.60% |

| 01:30 | AUD | CPI Q/Q Q1 | 1.00% | 1.40% |

| 01:30 | AUD | CPI Y/Y Q1 | 6.20% | 7.00% |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 1.10% | 1.20% |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 6.00% | 6.60% |

| 08:00 | CHF | Credit Suisse Economic Expectations Jul | -30.8 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jun | 1.00% | 1.40% |

| 14:00 | USD | New Home Sales Jun | 720K | 763K |

| 14:30 | USD | Crude Oil Inventories | -0.7M | |

| 17:30 | CAD | BOC Summary of Deliberations | 6.70% | 7.10% |

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.25% |

| 18:30 | USD | FOMC Press Conference |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Jun | |

| Forecast: 5.40% | Previous: 5.60% | ||

| 01:30 | AUD | CPI Q/Q Q1 | |

| Forecast: 1.00% | Previous: 1.40% | ||

| 01:30 | AUD | CPI Y/Y Q1 | |

| Forecast: 6.20% | Previous: 7.00% | ||

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | |

| Forecast: 1.10% | Previous: 1.20% | ||

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | |

| Forecast: 6.00% | Previous: 6.60% | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Jul | |

| Forecast: | Previous: -30.8 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jun | |

| Forecast: 1.00% | Previous: 1.40% | ||

| 14:00 | USD | New Home Sales Jun | |

| Forecast: 720K | Previous: 763K | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -0.7M | ||

| 17:30 | CAD | BOC Summary of Deliberations | |

| Forecast: 6.70% | Previous: 7.10% | ||

| 18:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.25% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

Thursday, Jul 27, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Import Price Index Q/Q Q1 | -0.80% | -4.20% |

| 06:00 | EUR | Germany Gfk Consumer Confidence Aug | -24.7 | -25.4 |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.25% | 4.00% |

| 12:15 | EUR | ECB Rate On Deposit Facility | 3.75% | 3.50% |

| 12:30 | USD | Initial Jobless Claims (Jul 21) | 233K | 228K |

| 12:30 | USD | Initial Jobless Claims 4-week average (Jul 21) | 237.5K | |

| 12:30 | USD | GDP Annualized Q2 P | 1.60% | 2.00% |

| 12:30 | USD | GDP Price Index Q2 P | 3.10% | 4.10% |

| 12:30 | USD | Goods Trade Balance (SUD) Jun P | -91.8B | -91.1B |

| 12:30 | USD | Wholesale Inventories Jun P | 0% | |

| 12:30 | USD | Durable Goods Orders Jun | 1.00% | 1.80% |

| 12:30 | USD | Durable Goods Orders ex Transportation Jun | 0.10% | 0.70% |

| 12:45 | EUR | ECB Press Conference | ||

| 14:00 | USD | Pending Home Sales M/M Jun | -0.50% | -2.70% |

| 14:30 | USD | Natural Gas Storage | 41B | |

| 23:30 | JPY | Tokyo CPI Y/Y Jul | 2.80% | 3.10% |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jul | 2.90% | 3.20% |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Jul | 3.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Import Price Index Q/Q Q1 | |

| Forecast: -0.80% | Previous: -4.20% | ||

| 06:00 | EUR | Germany Gfk Consumer Confidence Aug | |

| Forecast: -24.7 | Previous: -25.4 | ||

| 12:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 4.25% | Previous: 4.00% | ||

| 12:15 | EUR | ECB Rate On Deposit Facility | |

| Forecast: 3.75% | Previous: 3.50% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 21) | |

| Forecast: 233K | Previous: 228K | ||

| 12:30 | USD | Initial Jobless Claims 4-week average (Jul 21) | |

| Forecast: | Previous: 237.5K | ||

| 12:30 | USD | GDP Annualized Q2 P | |

| Forecast: 1.60% | Previous: 2.00% | ||

| 12:30 | USD | GDP Price Index Q2 P | |

| Forecast: 3.10% | Previous: 4.10% | ||

| 12:30 | USD | Goods Trade Balance (SUD) Jun P | |

| Forecast: -91.8B | Previous: -91.1B | ||

| 12:30 | USD | Wholesale Inventories Jun P | |

| Forecast: | Previous: 0% | ||

| 12:30 | USD | Durable Goods Orders Jun | |

| Forecast: 1.00% | Previous: 1.80% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Jun | |

| Forecast: 0.10% | Previous: 0.70% | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:00 | USD | Pending Home Sales M/M Jun | |

| Forecast: -0.50% | Previous: -2.70% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 41B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Jul | |

| Forecast: 2.80% | Previous: 3.10% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jul | |

| Forecast: 2.90% | Previous: 3.20% | ||

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Jul | |

| Forecast: | Previous: 3.80% | ||

Friday, Jul 28, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | -0.10% | ||

| 01:30 | AUD | Retail Sales M/M Jun | 0.00% | 0.70% |

| 01:30 | AUD | PPI Q/Q Q1 | 0.90% | 1.00% |

| 01:30 | AUD | PPI Y/Y Q1 | 5.20% | |

| 07:00 | CHF | KOF Economic Barometer Jul | 90 | 90.8 |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jul | 95 | 95.3 |

| 09:00 | EUR | Eurozone Industrial Confidence Jul | -7.5 | -7.2 |

| 09:00 | EUR | Eurozone Services Sentiment Jul | 5.3 | 5.7 |

| 09:00 | EUR | Eurozone Consumer Confidence Jul F | -15.1 | -15.1 |

| 12:00 | EUR | Germany CPI M/M Jul P | 0.30% | 0.30% |

| 12:00 | EUR | Germany CPI Y/Y Jul P | 6.20% | 6.40% |

| 12:30 | CAD | GDP M/M May | 0.30% | 0.00% |

| 12:30 | USD | Personal Income M/M Jun | 0.50% | 0.40% |

| 12:30 | USD | Personal Spending M/M Jun | 0.40% | 0.10% |

| 12:30 | USD | PCE Price Index M/M Jun | 0.10% | |

| 12:30 | USD | PCE Price Index Y/Y Jun | 3.80% | |

| 12:30 | USD | Core PCE Price Index M/M Jun | 0.20% | 0.30% |

| 12:30 | USD | Core PCE Price Index Y/Y Jun | 4.20% | 4.60% |

| 12:30 | USD | Employment Cost Index Q1 | 1.10% | 1.20% |

| 13:45 | USD | Chicago PMI Jul | 41.5 | |

| 14:00 | USD | Michigan Consumer Sentiment Index Jul F | 72.6 | 72.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: | Previous: -0.10% | ||

| 01:30 | AUD | Retail Sales M/M Jun | |

| Forecast: 0.00% | Previous: 0.70% | ||

| 01:30 | AUD | PPI Q/Q Q1 | |

| Forecast: 0.90% | Previous: 1.00% | ||

| 01:30 | AUD | PPI Y/Y Q1 | |

| Forecast: | Previous: 5.20% | ||

| 07:00 | CHF | KOF Economic Barometer Jul | |

| Forecast: 90 | Previous: 90.8 | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jul | |

| Forecast: 95 | Previous: 95.3 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jul | |

| Forecast: -7.5 | Previous: -7.2 | ||

| 09:00 | EUR | Eurozone Services Sentiment Jul | |

| Forecast: 5.3 | Previous: 5.7 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jul F | |

| Forecast: -15.1 | Previous: -15.1 | ||

| 12:00 | EUR | Germany CPI M/M Jul P | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:00 | EUR | Germany CPI Y/Y Jul P | |

| Forecast: 6.20% | Previous: 6.40% | ||

| 12:30 | CAD | GDP M/M May | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 12:30 | USD | Personal Income M/M Jun | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 12:30 | USD | Personal Spending M/M Jun | |

| Forecast: 0.40% | Previous: 0.10% | ||

| 12:30 | USD | PCE Price Index M/M Jun | |

| Forecast: | Previous: 0.10% | ||

| 12:30 | USD | PCE Price Index Y/Y Jun | |

| Forecast: | Previous: 3.80% | ||

| 12:30 | USD | Core PCE Price Index M/M Jun | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Jun | |

| Forecast: 4.20% | Previous: 4.60% | ||

| 12:30 | USD | Employment Cost Index Q1 | |

| Forecast: 1.10% | Previous: 1.20% | ||

| 13:45 | USD | Chicago PMI Jul | |

| Forecast: | Previous: 41.5 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jul F | |

| Forecast: 72.6 | Previous: 72.6 | ||

The Weekly Bottom Line: Fed Gearing Up for Another (Likely Final) Hike

U.S. Highlights

- Retail sales disappointed market expectations overall in June, but underneath the surface sales in the control group, which are used to calculate consumption, were much stronger, rising 0.6% on the month.

- Elevated mortgage rates and low inventories continue to weigh on existing home sales. The latter resumed their downward trend in June.

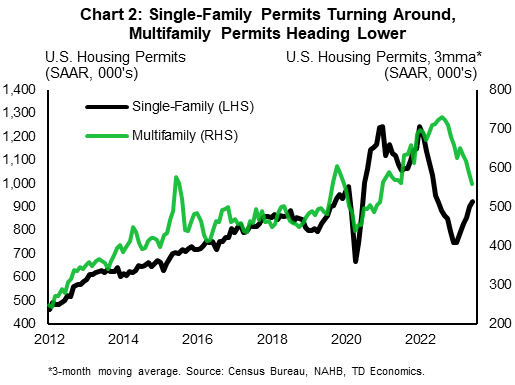

- Housing starts also fell in June. But, permitting data reveals a clear divergence between an upward trend in single-family permits and a downswing in multifamily permits.

Canadian Highlights

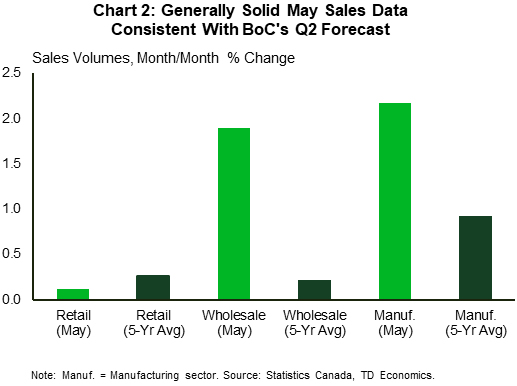

- Gains in manufacturing, wholesale, and retail volumes are roughly consistent with the Bank of Canada’s economic growth forecast for the second quarter.

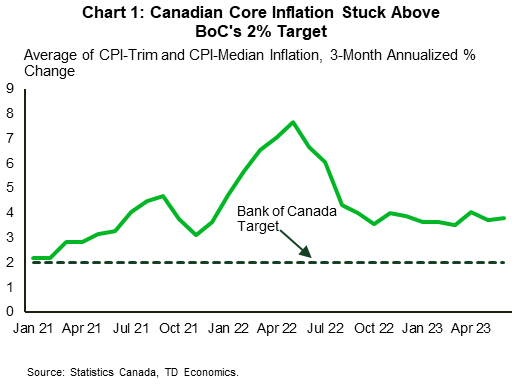

- However, the Bank’s preferred core inflation metrics continued to run too hot in June, with the average of CPI-trim and CPI-median inflation stuck too far above the 2% target.

- All told, developments this week likely did nothing that would move the Bank of Canada off of its hawkish stance.

U.S. – Fed Gearing Up for Another (Likely Final) Hike

Economic data this week wasn’t entirely positive, but it still pointed to an economy that continues to chug along at a decent clip. With no major red flags on the way, the Fed has the green light to hike the policy rate once more next week, before likely hitting the pause button.

While we expect the labor market to cool ahead, recent high frequency data still points to resilient demand for workers. Continuing jobless claims rose in the week ending July 8th, but initial claims continued to trend lower, easing for the second week in a row last week. With unemployment near multidecade lows, June retail sales suggested consumers are still spending, even as inflation bites into purchasing power. Headline retail sales growth was below market expectations, but an upward revision to the month prior helped provide some offset. The headline was dragged down by lower sales at gasoline stations, and at building material and garden equipment stores. A notable deceleration in sales at auto and food service establishments didn’t provide much support either. Stronger momentum was seen in the control group, which are used to calculate personal consumption expenditures, with sales rising 0.6% m/m – continuing a healthy pattern for the quarter.

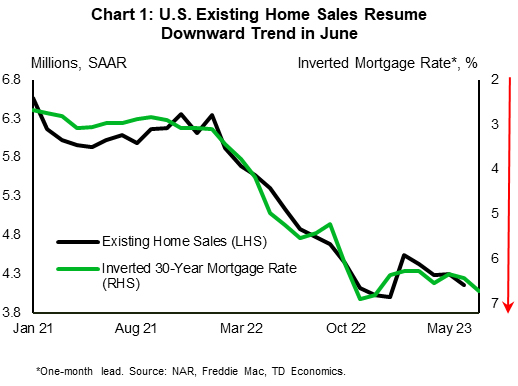

Consumers weren’t as upbeat on homes, with existing home sales resuming their downward trend in June (see here). Elevated mortgage rates are likely to have been a major hurdle, given the tight relationship with sales recently (Chart 1). The higher rate environment has persisted through the first half of July, suggesting that there’s no turnaround in sight for the weakness in existing home sales. Low inventory is also restraining activity. There were only 1.08 million homes for sale in June – 170k less than last year and 840k less than in June 2019 – making for slim pickings.

As we note in a recent report, the tight conditions in the resale housing market are pushing more people toward the new home market. This is much to the delight of homebuilders, whose confidence has been improving rapidly since the start of the year. This optimism has been confined to the single-family segment, however. Multifamily homebuilders have been pulling back. Housing starts retreated in June in both segments, but permitting data reveals a clear divergence between the two segments (Chart 2). The recent softness in the multifamily space is consistent with a rise in the multifamily vacancy rate, and a record-setting number of units under construction in June.

All told, interest-sensitive areas of the economy remain under pressure. But with the employment backdrop continuing to hold up well, consumers still spending, and inflation appearing to move in the right direction, chances of a soft-landing look to have improved. The Federal Reserve is nonetheless expected to maintain a tightening bias over the near-term, and is almost certain to hike the policy rate once more next week. A Fed hike is fully priced in by markets at this point. Provided inflation continues to cool, this will likely be the Fed’s last hike this cycle.

Canada – Resilience is the Name of the Game

It was risk-on for financial markets this week, buoyed by a sense of optimism that the elusive soft landing is now seemingly more achievable for the U.S. economy. Notably, the TSX was tracking a 1% weekly gain (as of writing), while longer-dated bond yields pushed higher, and oil prices increased for the third straight week.

This week's flow of top tier economic indicators portrayed a Canadian economy that continues to hang tough. While headline inflation showed some encouraging signs in June, surprising to the soft-side at 2.8% year-on-year, developments under the hood were less favourable. For one, the softness in the headline was due to base effects for energy prices, like gasoline. And, gasoline is likely to exert less of a year-on-year drag on the overall index in the months ahead.

In addition, Russia pulled out of a deal struck one year ago that ensured the safe export of Ukrainian grains. It also warned that ships servicing Ukrainian ports could be attacked (a threat reciprocated by Ukrainian authorities about ships servicing Russian-occupied Ukraine), while attacks at key ports have destroyed 60 thousand tons of grain and key infrastructure. Amid these tensions, prices for grains like wheat have predictably pushed higher. This could have knock-on effects to food prices in the coming months.

Most importantly for the Bank of Canada, core inflation is proving stubbornly persistent. Average core inflation (measured as the average of the BoC's CPI-trim and CPI-median) accelerated in 3-month annualized terms (Chart 1).

The B.C. port strike is also hitting Canadian supply chains, creating backlogs that industry participants suggest will take months to clear. The work stoppage has already disrupted the flow of about $10 billion worth of cargo. The status of the labour dispute is still up in the air, but it seems to be moving in an encouraging direction.

Indicators of economic activity were almost uniformly strong during the week (Chart 2). Housing starts surged to 281k units in June - the highest in 9 months. Meanwhile, improving auto supply chains made their mark on manufacturing and wholesaling activity, with volumes in the former up 2% month-on-month (m/m) and 3% m/m in the latter. Retail sales were the one fly in the ointment, with volumes up a modest 0.1% m/m, while the preliminary estimate for June showed only flat growth in nominal sales.

While the activity data was generally firm, it was still consistent with economic growth expanding around 1.5% annualized in the second quarter, which is what the Bank of Canada's expects. In that respect, this data would be unlikely to shift the pendulum on monetary policy (though policymakers should draw some comfort from evidence of softer consumer spending). Core inflation, however, continues to hover in ranges that are too high for the Bank's comfort. All told, events this week likely did nothing to move policymakers off their hawkish stance.

Weekly Economic & Financial Commentary: Fed to Hike Next Week, but What Then?

Summary

United States: Rate Sensitive Sectors Struggle as E-commerce Boosts Retail Sales

- The FOMC’s balancing act became more daunting this week. Its rate hikes thus far still have not fully repressed consumer spending, but there are signs of fallout in other rate-sensitive parts of the economy, such as the industrial sector and housing. Is the economy in good shape or bad? The answer is both.

- Next week: New Home Sales (Wed), GDP (Thu), Personal Income & Spending (Fri)

International: China's Economy Lacking Momentum

- China's Q2 GDP figures, along with activity data for June, confirmed the economy is losing momentum. Q2 GDP rose 0.8% quarter-over-quarter, well down from 2.2% in Q1. June activity data were mixed, as retail sales slowed more than expected, but industrial output unexpectedly firmed. Still, China's central bank appears on course to ease monetary policy further in Q3, while waning momentum also suggests downside risk to our 2023 growth forecast for China.

- Next week: Australia CPI (Wed.), ECB Rate Announcement (Thu.), BoJ Policy Announcement (Fri.)

Interest Rate Watch: Fed to Hike Next Week, but What Then?

- The FOMC's decision to leave policy unchanged in June was delivered with a hawkish message. We expect another 25 bps hike at next week's meeting, bringing the target range to 5.25%-5.50%. While markets doubt the prospect for further tightening beyond July, we look for the post-meeting statement and press conference to signal further hikes remain possible.

Credit Market Insights: Consumers Increasingly Facing Credit Application Rejections

- The New York Fed's Survey of Consumer Expectations (SCE) Credit Access Survey demonstrated that consumers faced steep hurdles when making big-ticket purchases. Rejections for all kinds of credit have increased in light of the uncertainty surrounding the near-term economic outlook.

Topic of the Week: Breaking Down the 2023 FIFA Women's World Cup

- World Cup season is not over yet as the women's tournament kicked off this week in Australia and New Zealand. The 2023 FIFA Women's World Cup gives us another opportunity to apply economic analysis toward picking a champion. We also take the chance to dive into the global gender pay gap.

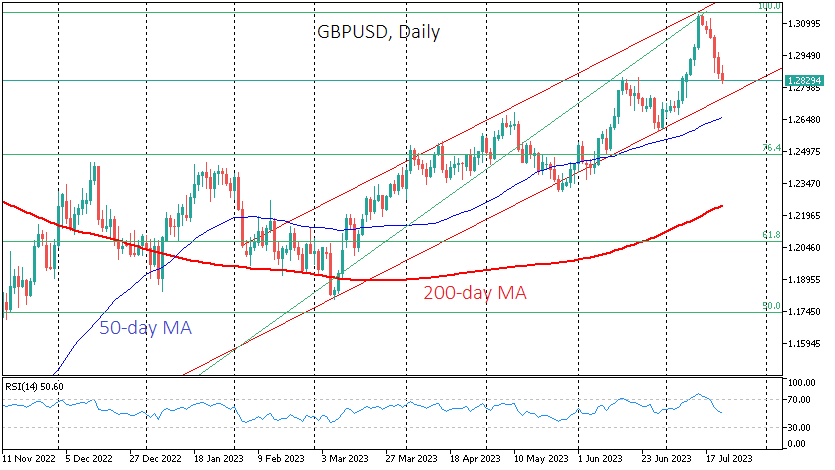

GBPUSD: From Correction to Uptrend Breakdown

The British Pound is losing ground for the 6th consecutive session, falling 2.2% to 1.2850. The downward movement began as a correction after a 9-sessions rally from 30 June but accelerated following the release of weak inflation data earlier in the week.

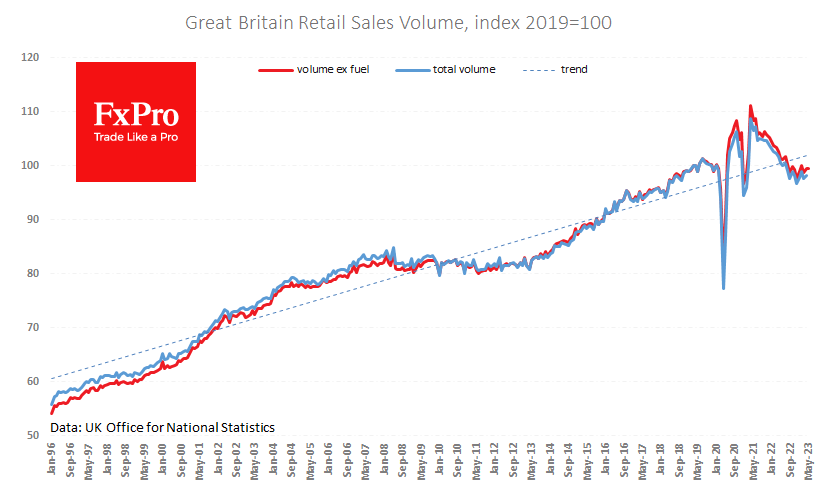

Strong retail sales figures failed to reverse the GBPUSD’s downward trend on Friday. The data, released before the London session, showed that total sales rose 0.7% in the month (+0.2% expected), marking the third consecutive month of growth. In the same month last year, the decline had narrowed to 1% from a peak of 6.7% in December.

So far, however, we can only confidently talk about the end of the recession, not the emergence of sustainable positive momentum. The volume index for retail sales is now roughly at the level of October and August last year and is 2.3% above the lows. And with the five-year period after 2008, the UK knows how difficult the road to full recovery can be. Moreover, back then, the economy was supported by loose monetary conditions. And the current level of sales is locked in with relatively high employment and tight monetary policy.

And that’s not good for Sterling. The big question now is how low it will go. GBPUSD has been trading in a fairly narrow uptrend since March. And all this fits into a broader trend of the pair’s recovery from multi-year lows last September.

The lower boundary of this uptrend is now at 1.2750, 0.6% lower at the time of writing. A break below this level would be the first sign of a break in the recent trend and final confirmation would come from a drop to 1.2650 with a test of the 50-day moving average and entry into the levels where the pair has reversed several times.

The GBPUSD corrective pullback may not stop at these levels, and we will see a decline to 1.23 by the end of September and 1.2070-1.2100 in the next few quarters. Reaching these levels will require a reassessment of the Bank of England’s monetary policy outlook. The inflation report has dramatically reduced the chances of a 50-point rate hike in two weeks’ time. However, it is also likely that markets will revise their expectations for a top rate of 6.00%, moving closer to the economists’ average expectation of a top rate of 5.5%.

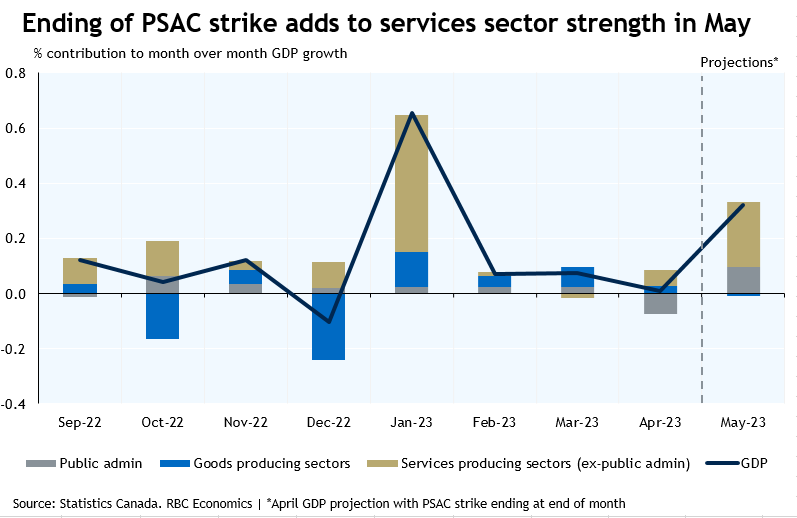

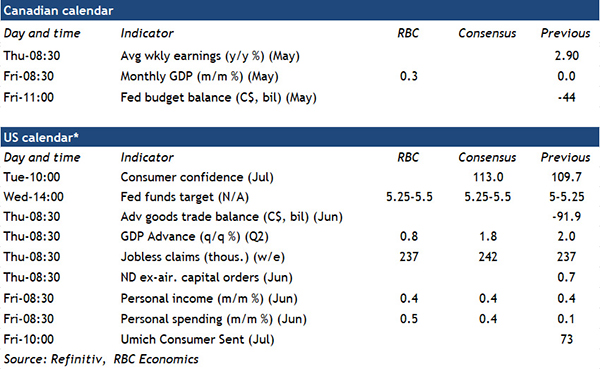

Strong Economic Growth for Canada in May

Canadian GDP is likely to have stayed strong May. Statistics Canada’s advance estimate pointed to a 0.4% month over month increase in output—a hair off of our own estimate for a 0.3% increase. With wildfires disrupting production in Alberta, oil and gas extraction was very likely a weak spot. But stronger manufacturing production suggests output from goods producing sectors likely remained at April’s level. And the end of the federal workers strike—which lowered output in April—will have brought arebound in public administration, boosting services output. We expect that factor alone to account for about a third of expected GDP growth in the month. Wholesale and retail sales also both posted sizable gains—rising 3.3% and 0.1%, in real terms respectively in May. Real estate and rental activities improved too on stronger home resales. Hours worked were little changed in June, suggesting a softer print for GDP in that month. But that still leaves GDP growth tracking up one per cent at an annualized basis (slightly above our own 0.5% forecast, but close to the BoC’s current 1.5% forecast.)

With growth also resilient south of the border, the U.S. Federal Reserve is grappling with how much more to tap the brakes. In line with markets, we think the Fed will raise the fed funds range by 25 basis points, to 5.25% - 5.50% next week. That’s after skipping a hike at its last meeting on June 14th. U.S. Inflation data for June surprised to the downside, with the Fed’s ‘super core’ (core services CPI ex-shelter) measure dropping to 1.4% on a three-month annualized basis. For context, the pre-pandemic trend rate of increase for that measure was around 2.5%.

But policymakers will be concerned that the economic backdrop and consumer spending remain too firm for lower inflation pressures to last. Labour market conditions are still tight and wage growth is stuck at elevated levels above what would be consistent with a long-run 2% inflation objective. Beyond the widely expected hike in rates next week however, the path for interest rates is uncertain. Similar to prior statements, the Fed is likely to keep its options open. Our view remains that more weaknesses to domestic demand will emerge over the second half of 2023 as households are strained by elevated borrowing costs and slowing labour markets. That should in turn keep inflation low—and the Fed on the sidelines for the remainder of this year.

Next week’s job vacancy data from the May SEPH release will be closely watched. According to the latest Business Outlook Survey, labour shortages are already easing due as immigration add to labour supply. Job vacancies have been falling on a seasonally adjusted basis in recent months, and we expect that trend to continue.

Our call is for the U.S. GDP to have risen by an annualized 0.8% in Q2 of 2023, down from 2% in the prior quarter. Stronger consumer fundamentals continue to support personal consumption expenditure in Q2. Alongside that there will be a series of data releases for June, including personal income, personal spending, and the advance trade report, all for the U.S.