Sample Category Title

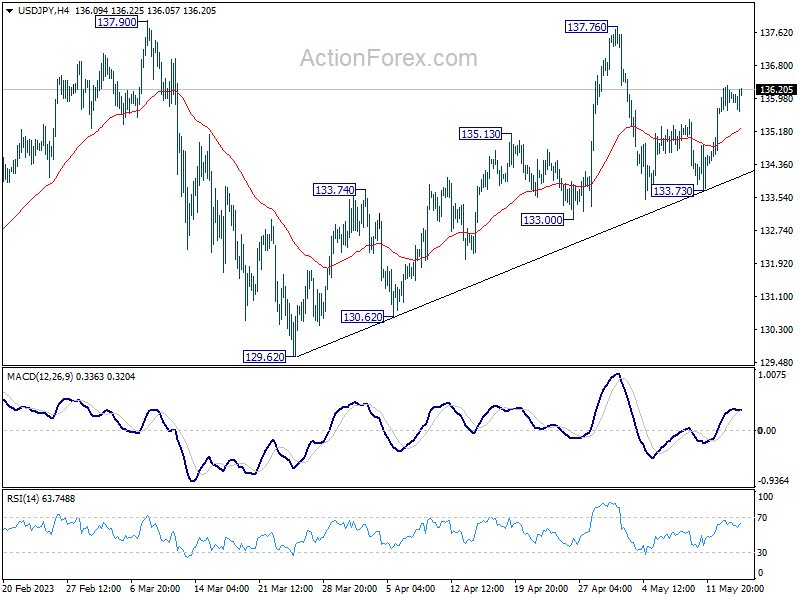

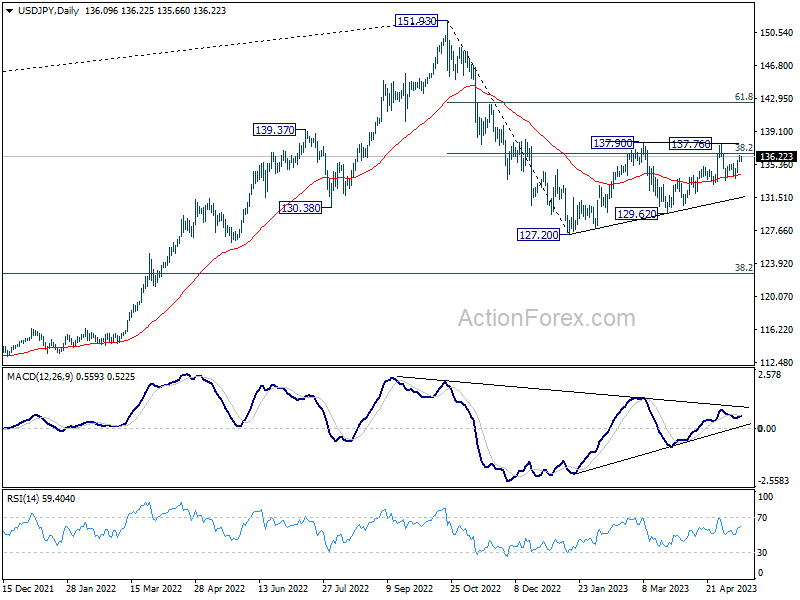

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 135.73; (P) 136.02; (R1) 136.40; More...

No change in USD/JPY's outlook as rise from 133.73 is still in progress. Intraday bias stays on the upside for 137.76/90 resistance zone. Decisive break there will resume whole rebound from 127.20. On the downside, break of 133.73 will resume the fall from 137.76 through 133.00 instead.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rise to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

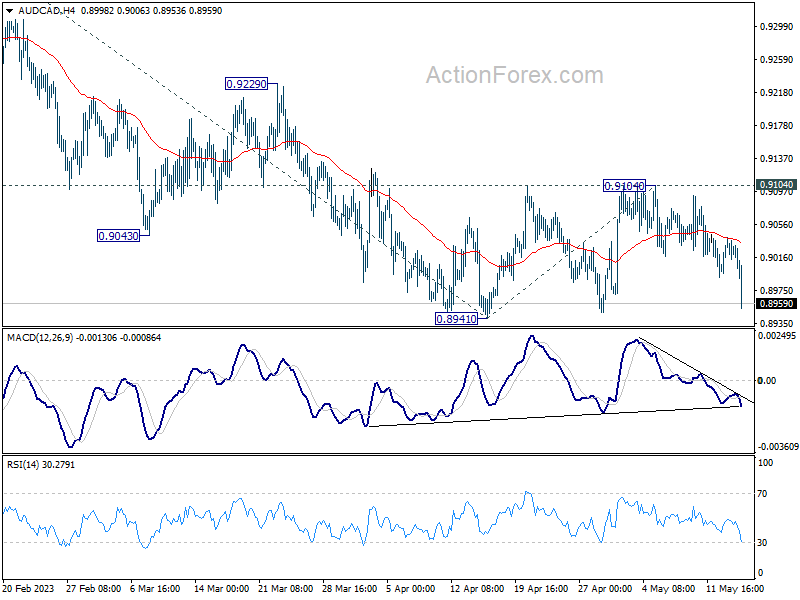

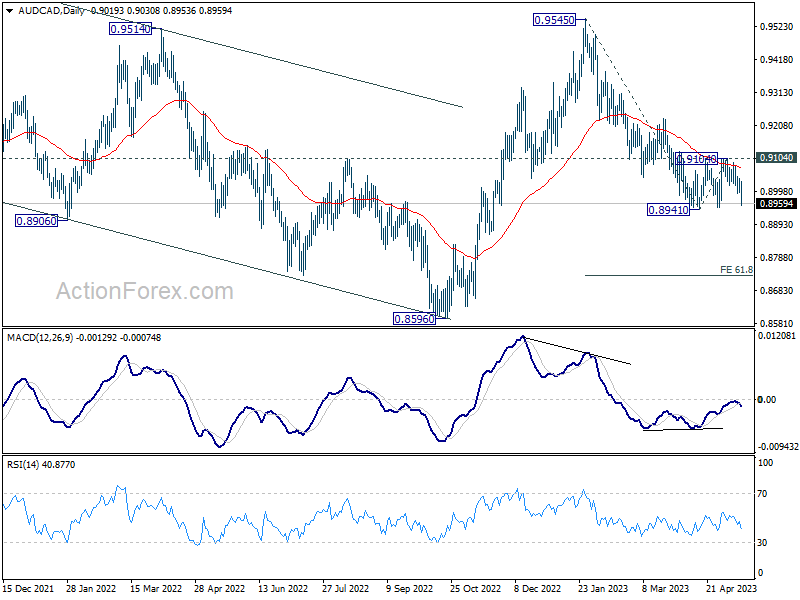

Canadian Dollar Rises on Unexpected Inflation Uptick; Australian Dollar Continues to Struggle

Canadian Dollar is enjoying a broad rally in early US trading session, fueled by data that revealed unexpected reacceleration in Canadian consumer inflation for April. The evidence for BoC to resume tightening measures is steadily accumulating. Amid slight risk-off sentiment in US markets, due to persistent uncertainties over debt ceiling negotiations, Swiss Franc and Japanese Yen are also seeing gains.

On the other hand, Australian Dollar remains the day's weakest performer, hamstrung by a sharp drop in consumer sentiment and a string of disappointing data from China. Hot on its heels is British Pound, which is feeling the pinch from poor employment data that underlines the economy's rapidly slowing momentum. Both Euro and Dollar are exhibiting mixed performances, although the greenback seems to have a minor advantage in extending its near-term rebound.

From a technical perspective, AUD/CAD appears finally ready to resume its downtrend from 0.9545. Immediate attention is now on 0.8941 low, and decisive break of this level would see fall from 0.9545 resume to 61.8% projection of 0.9545 to 0.8941 from 0.9104 at 0.8731. Regardless, outlook will remain bearish as long as the 0.9104 resistance holds, even in the event of a recovery.

In Europe, at the time of writing, FTSE is up 0.05%. DAX is up 0.15%. CAC is up 0.02%. Germany 10-year yield is up 0.0002 at 2.313. Earlier in Asia, Nikkei rose 0.73%. Hong Kong HSI rose 0.04%. China Shanghai SSE dropped -0.60%. Singapore Strait Times dropped -0.02%. Japan 10-year JGB yield dropped -0.0123 to 0.396.

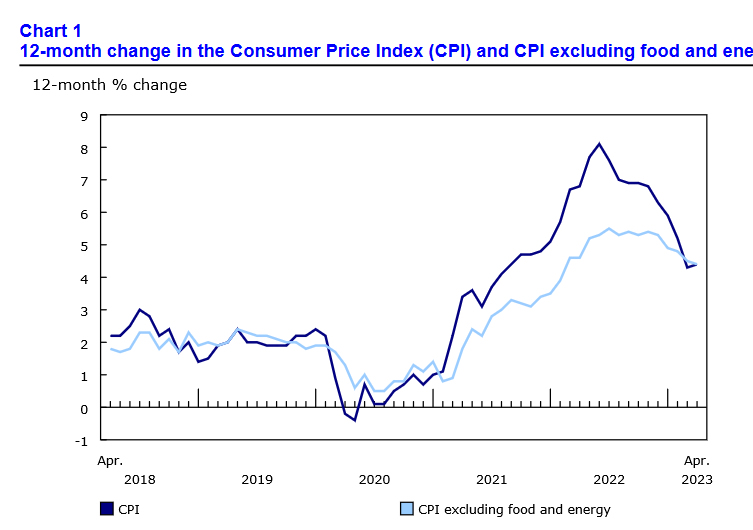

Canada CPI rose to 4.4% yoy in Apr, first acceleration since June 2022

Canada CPI rose 0.7% mom in April, above expectation of 0.5% mom. Prices for gasoline (+6.3%) contributed the most to the headline month-over-month movement. Excluding gasoline, the monthly CPI rose 0.5%.

Over the 12-month period, CPI accelerated from 4.3% yoy to 4.4% yoy, above expectation of 4.1% yoy. That's the first acceleration in headline CPI since June 2022. Statistics Canada said that higher rent prices and mortgage interest costs contributed the most to the all-items CPI increase.

CPI median slowed from 4.5% yoy to 4.2% yoy, below expectation of 4.3% yoy. CPI trimmed dropped from 4.4% yoy to 4.2% yoy, above expectation of 4.1% yoy. CPI common slowed from 6.0% yoy to 5.7% yoy, above expectation of 5.5% yoy.

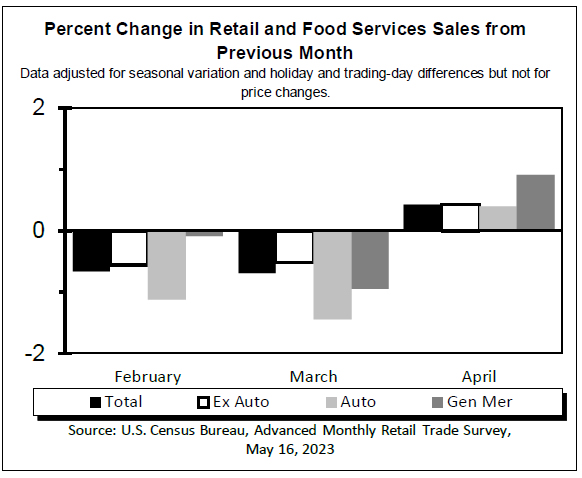

US retail sales up 0.4% mom in Apr, ex-auto sales up 0.4% mom

US retail sales rose 0.4% mom in USD 686.1B in April, below expectation of 0.8% mom. Ex-auto sales rose 0.4% mom to USD 556.1B, below expectation of 0.5% mom. Ex-gasoline sales rose 0.5% mom to USD 631.4B. Ex-auto, gasoline sales rose 0.6% mom to USD 501.4B. Total sales for the February through April period were up 3.1% yoy.

Germany ZEW dived to -10.7, economy could slip into recession

Germany ZEW Economic Sentiment recorded in significantly decline from 4.1 to -10.7 in May, even worse than expectation of -5.0%. Current Situation Index dropped from -32.5 to -34.8.

Eurozone ZEW Economic Sentiment fell form 6.4 to -9.4. Current Situation Index rose 2.7 pts to -27.5.

ZEW President Professor Achim Wambach said:

"The ZEW Indicator of Economic Sentiment has once again fallen sharply. The financial market experts anticipate a worsening of the already unfavourable economic situation in the next six months. As a result, the German economy could slip into a recession, albeit a mild one.

"The sentiment indicator decline is partly due to expectations of further interest rate hikes by the ECB. Additionally, the potential default by the United States in the coming weeks adds uncertainty to global economic prospects".

Eurozone imports fell -10% yoy in Mar, exports rose 7.5% yoy

Eurozone goods exports to the rest of the world rose 7.5% yoy to EUR 269.2B in March. Imports fell -10.0% yoy to EUR 243.5B. Trade surplus came in at EUR 25.6B. Intra-Eurozone trade rose 0.6% yoy to EUR 246.4B.

In seasonally adjusted term, goods exports dropped -0.1% mom to EUR 243.3B. Imports dropped -7.1% mom to EUR 226.2B. Trade balanced turned into EUR 17.0B surplus, above expectation of EUR 5.6B. Intra-Eurozone trade dropped from EUR 230.9B to EUR 223.2B.

UK payrolled employees dropped -136k in Apr, unemployment rate rose to 3.9% in Mar

UK payrolled employees dropped -0.5% mom, or -136k in April, comparing with March. That is the first decline in total payrolled employees since the COVID pandemic. Comparing with April 2022, payrolled employees rose 1.0% yoy or 297k. Claimant counts rose 46.7k, above expectation of 31.2k. Median monthly pay rose 7.4% yoy.

In the three months to March, unemployment rate rose 0.1% to 3.9%, comparing to the previous quarter. Employment rate rose 0.2% to 75.9%. Average earnings including bonus rose 5.8% 3moy. Average earnings excluding bonus rose 6.7% 3moy.

RBA Minutes: Further hikes may still be required

Minutes of RBA's May meeting revealed a detailed discussion where Board members weighed the pros and cons of keeping cash rate unchanged or increasing it by 25 basis points. Despite the fine balance of arguments, the Board saw it fit to raise the interest rates by 25bps to 3.85%, due to upside risks in inflation and tight labour market.

Data available in the month leading up to the meeting confirmed significant inflationary pressures and highlighted upside risks to the inflation outlook. The Board was concerned that if these risks materialised, it would "further delay the return of inflation to target levels" and potentially trigger a "damaging shift in inflation expectations".

While acknowledging considerable uncertainties surrounding the economic outlook, particularly with respect to household consumption, the Board's strong commitment to price stability and the necessity of anchoring inflation expectations tipped the scales in favour of a rate hike.

Looking forward, the Board indicated that "further increases in interest rates may still be required", depending on the evolution of the economy and inflation.

Australian consumer sentiment plunges in May following unexpected RBA rate hike

Australia Westpac Consumer Sentiment Index dropping sharpy by -7.9% from 85.8 to 79.0 in May. This decline brings the index close to the grim levels observed in March, which were the lowest since COVID-19 outbreak in 2020 and, prior to that, since the severe recession of early 1990s.

The unexpected decision by RBA to raise the cash rate by an additional 0.25% in May, as well as the Federal Budget, were cited by Westpac as the two main factors impacting consumer sentiment over the last month.

Westpac stated, "Interest rates were again a key driver of the May survey. The RBA raised the official cash rate by a further 0.25% at its May meeting in the week before the survey. The move came as a major surprise to markets and most commentators, clearly stoking consumer fears of more increases to come."

Looking ahead, Westpac predicts that RBA will likely pause in June, awaiting further data on inflation and the state of the economy. While the bank's central view anticipates the current cash rate will remain at its peak due to economic weakness and clear progress toward the Board's inflation target, it acknowledges that the risks are still "evenly balanced".

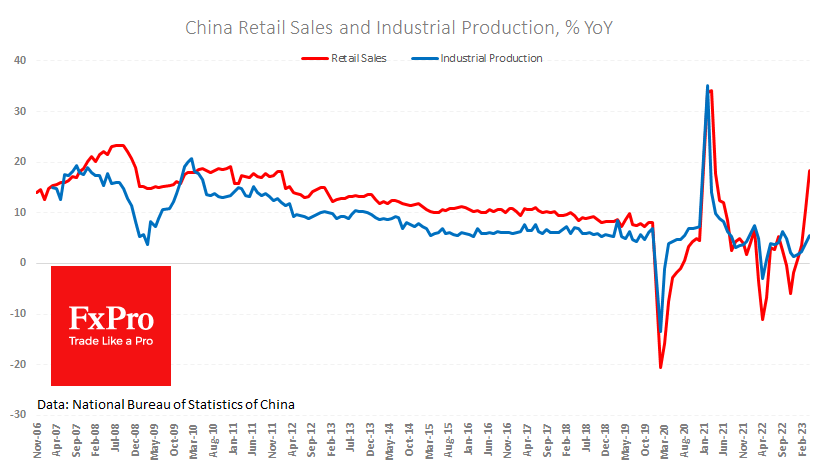

China's industrial production, retail sales miss expectations; youth unemployment hits record high

China's industrial production growth fell short of expectations in April, with a year-on-year increase of 5.6% yoy, significantly under expectation of 10.1% growth. Despite missing the mark, the growth rate outpaced March's 3.9% yoy rise and marked the fastest expansion since September 2022.

Retail sales also grew less than expected, posting 18.4% yoy rise, which fell short of anticipated 20.1% yoy growth. The figure was largely inflated due to a low comparison base, as retail sales plummeted by -11.1% yoy in April of the previous year due to severe lockdowns. On a monthly basis, retail sales contracted by -7.8% mom from March.

Fixed asset investment growth also came in below expectations 4.7% ytd yoy growth, underperforming expectation of 5.2%.

Urban jobless rate ticked down from 5.3% to 5.2%. However, unemployment among 16-24 age group spiked to a record high of 20.4%, up from 19.6% in the previous month. This exceeded the previous record of 19.9% set in July 2022.

The National Bureau of Statistics (NBS) stated, "In general, in April, the national economy continued to recover, and positive factors accumulated and increased. But we must also see that the international environment is still complex and severe, domestic demand is still insufficient, and the endogenous driving force for economic recovery is not yet strong."

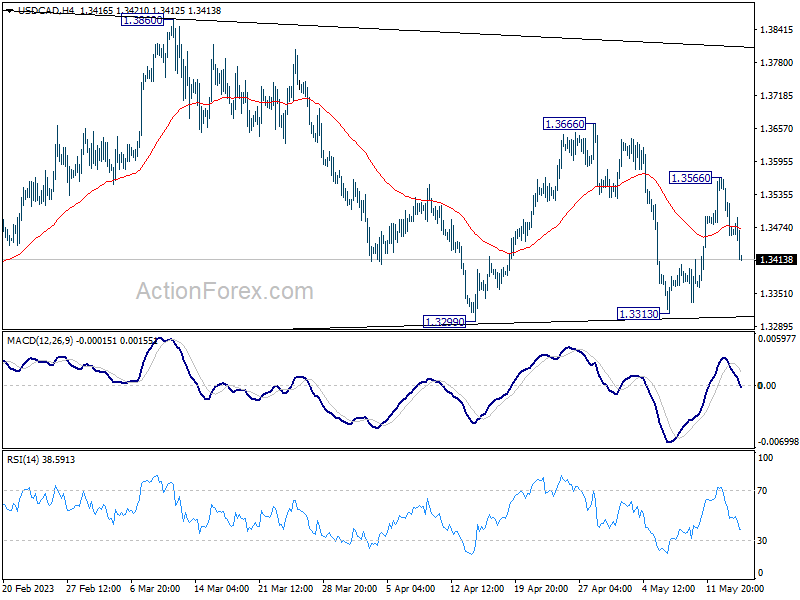

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3504; (P) 1.3534; (R1) 1.3589; More....

USD/CAD's fall from 1.3566 extends lower today but stays well above 1.3313 support. Intraday bias remains neutral first. Overall, it's seen as extending the triangle consolidation pattern from 1.3976. Above 1.3566 will resume the rebound towards 1.3666 resistance and then 1.3860. However, firm break of 1.3313 support will invalidate this view and indicate that deeper correction is underway.

In the bigger picture, as long as 55 W EMA (now at 1.3321) holds, up trend from 1.2005 (2021 low) is still in favor to resume through 1.3976 at a later stage. However, sustained trading below the EMA and 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will raise the chance of bearish reversal. Deeper should then be seen to 61.8% retracement at 1.2758 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 02:00 | CNY | Industrial Production Y/Y Apr | 5.60% | 10.10% | 3.90% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Apr | 4.70% | 5.20% | 5.10% | |

| 02:00 | CNY | Retail Sales Y/Y Apr | 18.40% | 20.10% | 10.60% | |

| 06:00 | GBP | Claimant Count Change Apr | 46.7K | 31.2K | 28.2K | |

| 06:00 | GBP | ILO Unemployment Rate (3M) Mar | 3.90% | 3.80% | 3.80% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Mar | 5.80% | 5.10% | 5.90% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Mar | 6.70% | 6.80% | 6.60% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | 17.0B | 5.6B | -0.1B | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.10% | 0.10% | 0.10% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment May | -10.7 | -5 | 4.1 | |

| 09:00 | EUR | Germany ZEW Current Situation May | -34.8 | -35.3 | -32.5 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | -9.4 | 2.3 | 6.4 | |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 P | 0.60% | 0.30% | 0.30% | |

| 12:30 | CAD | Manufacturing Sales M/M Mar | 0.70% | 0.70% | -3.60% | |

| 12:30 | CAD | CPI M/M Apr | 0.70% | 0.50% | 0.50% | |

| 12:30 | CAD | CPI Y/Y Apr | 4.40% | 4.10% | 4.30% | |

| 12:30 | CAD | CPI Median Y/Y Apr | 4.20% | 4.30% | 4.60% | 4.50% |

| 12:30 | CAD | CPI Trimmed Y/Y Apr | 4.20% | 4.10% | 4.40% | |

| 12:30 | CAD | CPI Common Y/Y Apr | 5.70% | 5.50% | 5.90% | 6.00% |

| 12:30 | USD | Retail Sales M/M Apr | 0.40% | 0.80% | -0.60% | -0.70% |

| 12:30 | USD | Retail Sales ex Autos M/M Apr | 0.40% | 0.50% | -0.40% | -0.50% |

| 13:15 | USD | Industrial Production M/M Apr | 0.00% | 0.40% | ||

| 13:15 | USD | Capacity Utilization Apr | 79.70% | 79.80% | ||

| 14:00 | USD | Business Inventories Mar | 0.10% | 0.20% | ||

| 14:00 | USD | NAHB Housing Market Index May | 45 | 45 |

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3504; (P) 1.3534; (R1) 1.3589; More....

USD/CAD's fall from 1.3566 extends lower today but stays well above 1.3313 support. Intraday bias remains neutral first. Overall, it's seen as extending the triangle consolidation pattern from 1.3976. Above 1.3566 will resume the rebound towards 1.3666 resistance and then 1.3860. However, firm break of 1.3313 support will invalidate this view and indicate that deeper correction is underway.

In the bigger picture, as long as 55 W EMA (now at 1.3321) holds, up trend from 1.2005 (2021 low) is still in favor to resume through 1.3976 at a later stage. However, sustained trading below the EMA and 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will raise the chance of bearish reversal. Deeper should then be seen to 61.8% retracement at 1.2758 next.

Canada CPI rose to 4.4% yoy in Apr, first acceleration since June 2022

Canada CPI rose 0.7% mom in April, above expectation of 0.5% mom. Prices for gasoline (+6.3%) contributed the most to the headline month-over-month movement. Excluding gasoline, the monthly CPI rose 0.5%.

Over the 12-month period, CPI accelerated from 4.3% yoy to 4.4% yoy, above expectation of 4.1% yoy. That's the first acceleration in headline CPI since June 2022. Statistics Canada said that higher rent prices and mortgage interest costs contributed the most to the all-items CPI increase.

CPI median slowed from 4.5% yoy to 4.2% yoy, below expectation of 4.3% yoy. CPI trimmed dropped from 4.4% yoy to 4.2% yoy, above expectation of 4.1% yoy. CPI common slowed from 6.0% yoy to 5.7% yoy, above expectation of 5.5% yoy.

US retail sales up 0.4% mom in Apr, ex-auto sales up 0.4% mom

US retail sales rose 0.4% mom in USD 686.1B in April, below expectation of 0.8% mom. Ex-auto sales rose 0.4% mom to USD 556.1B, below expectation of 0.5% mom. Ex-gasoline sales rose 0.5% mom to USD 631.4B. Ex-auto, gasoline sales rose 0.6% mom to USD 501.4B. Total sales for the February through April period were up 3.1% yoy.

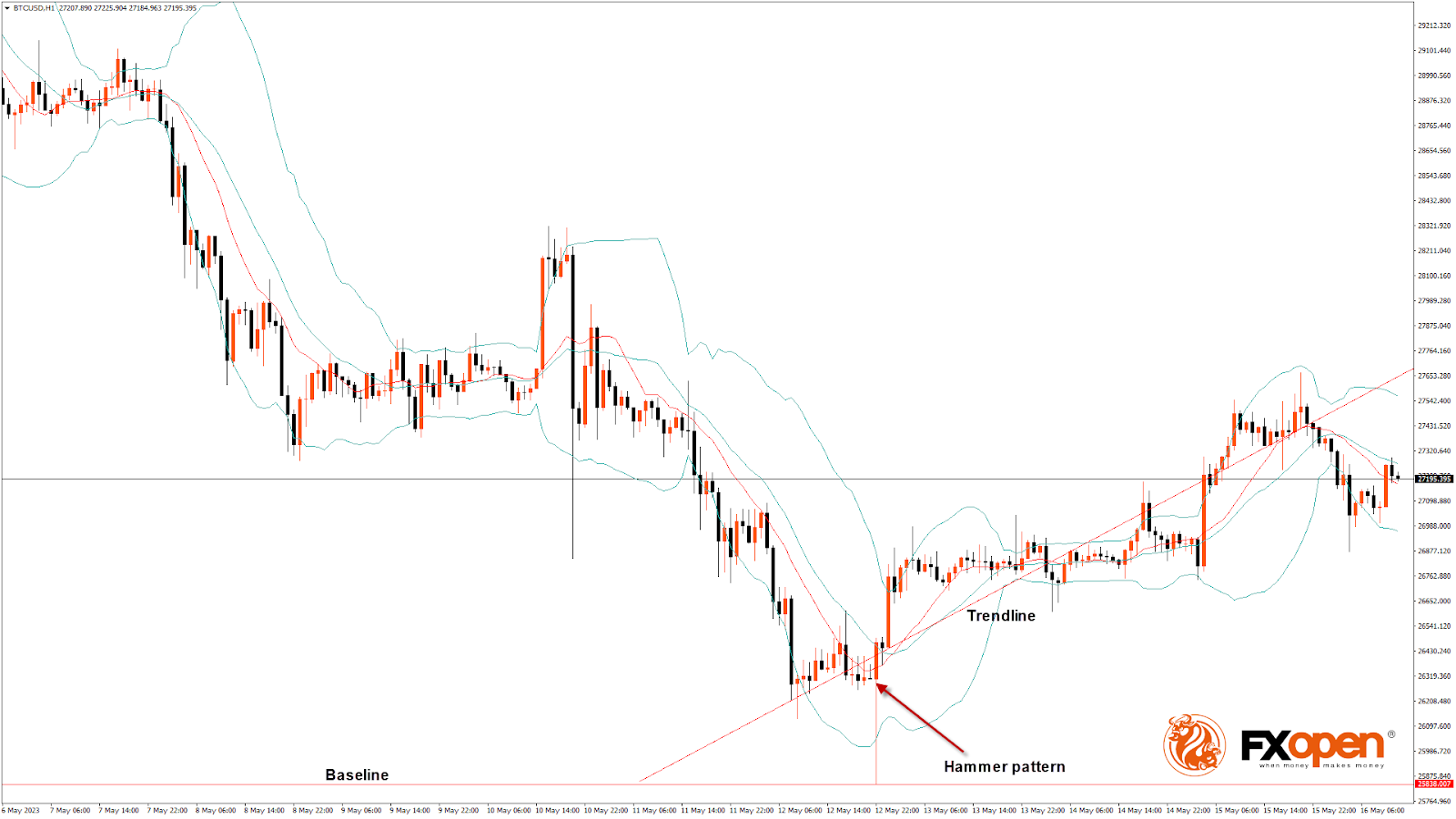

BTCUSD Analysis: Hammer Pattern above $25,838

Bitcoin price continues its bullish momentum from last week, and after touching a low of $25,838 on May 12, we can see a move towards a consolidation phase, after which we are expecting upsides in the range of $28,500-$29,000.

We can clearly see a hammer pattern above the $25,838 handle on the H1 timeframe.

Bitcoin today continues to move in a consolidation phase, after which we can see upside moves towards the $27,000 handle.

Both the STOCH and Williams’s percent range are in overbought zones, which means that in the immediate short term a decline in the price is expected.

We can also see the formation of a bullish harami pattern in the 15-minute and weekly timeframes.

The relative strength index is at 48.98, indicating a neutral demand for Bitcoin and the continuation of the consolidation in the markets.

Bitcoin price is now moving above its 100-hour simple moving average and its 100-hour exponential moving average.

Most of the major technical indicators are giving a bullish signal, which means that in the immediate short term, we are expecting targets of $27,500 and $28,500.

The average true range indicates low market volatility with mild bullish momentum.

- Bitcoin price bullish continuation is seen above $25,838.

- The RSI remains below 50, indicating a neutral market.

- The Bitcoin price is now trading below its pivot level of $27,242.

- The short-term range is mildly bullish.

- Bitcoin price is ranging near the support of the channel and triangle.

Bitcoin Bullish Continuation Seen Above $25,838

The Bitcoin to USD exchange rate entered into a consolidation zone above the $25,000 handle after which we can see the start of the bullish moves.

There is a bullish trend reversal pattern with 200 and 50-period adaptive moving averages in the 2-hour timeframe.

The Aroon indicator is giving a bullish trend signal in the 30-minute timeframe.

We have also seen a bullish harami cross pattern located in the 15-minute timeframe.

A support zone is at $25,881, which is a 1-month low, and at $26,624, which is a 38.2% retracement from 13-week high.

BTCUSD is now facing its classic resistance level of $27,280 and Fibonacci resistance level of $27,303, breaking which the price will be able to move to $28,000.

The price is above the Ichimoku cloud in the 15-minute timeframe.

The short-term outlook for Bitcoin is mildly bullish, the medium-term outlook has turned bullish, and the long-term outlook remains neutral under present market conditions.

The Week Ahead

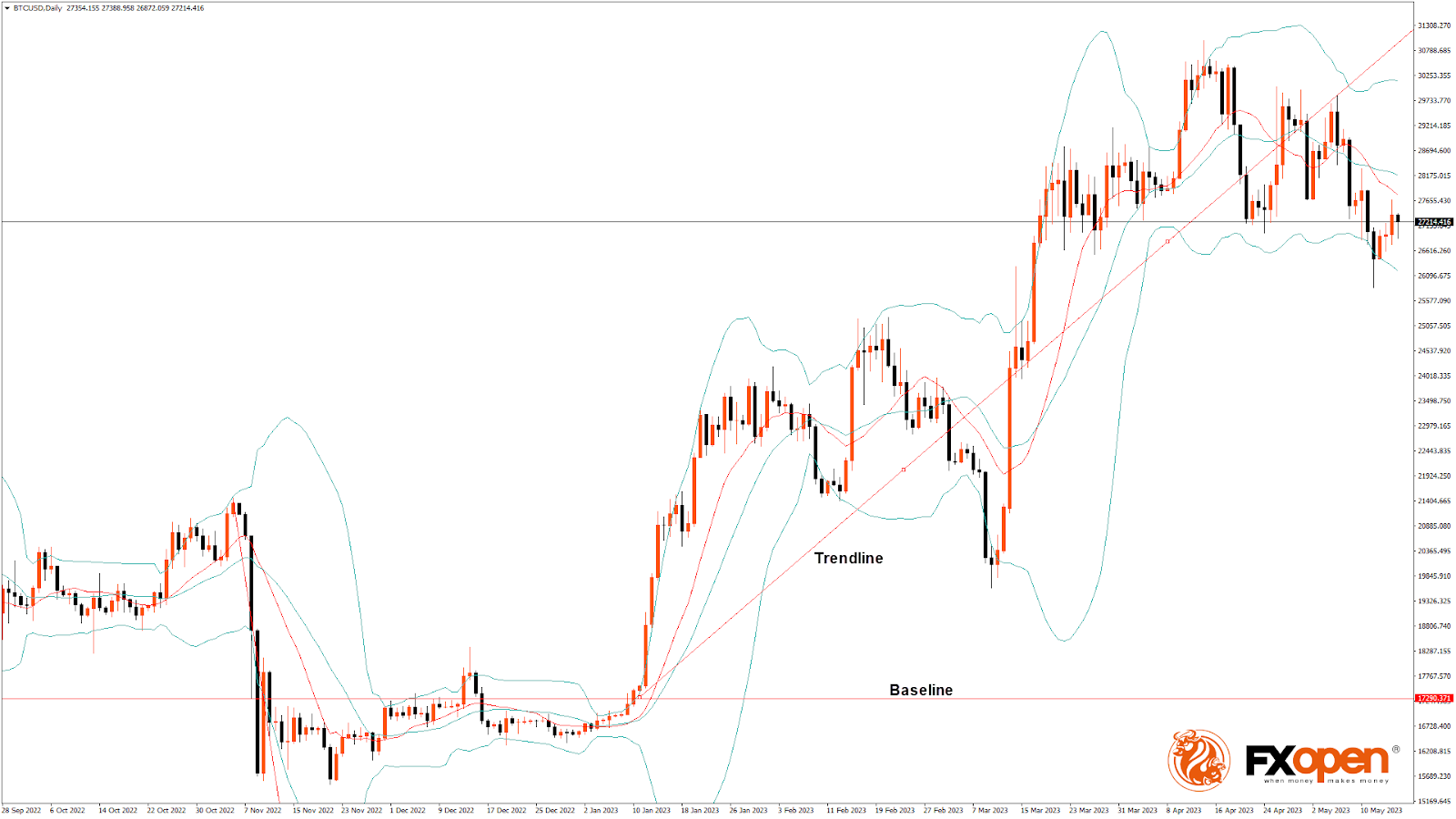

We can see that on a daily chart, Bitcoin remains well supported above the $25,000 handle and there is a medium-term continuation pattern, with the current support at $25,281, which is a 50% retracement from 13-week high/low.

The immediate expected target is $28,000, after which we may see some consolidation in the $28,500 zone.

Monthly RSI is at 49.38, which indicates the neutral market and the shift towards the consolidation zone in the medium-term range.

We can see the formation of a bullish trendline from $25,838 to $27,690.

The BTCUSD is now facing resistance at $27,682, which is a 38.2% retracement from 4-week low, and at $27,786 at which the price crosses the 9-day moving average.

The weekly outlook for Bitcoin price is projected at $28,500 with a consolidation zone of $28,000.

RBA: Minutes to May Board Meeting Make Strong Case to Justify Rate Increase

Despite the strong case the Minutes point to the decision in May being “finely balanced” – this still argues for the next ‘live’ meeting being August.

The Minutes of the Reserve Bank Board meeting make a strong case for the surprise decision to raise the cash rate at the May Board meeting.

In interpreting these Minutes we must be mindful that when a central bank makes a decision that is not expected it will go out of its way to justify the decision.

The key change in the rhetoric which certainly enforces the case for the rate hike is the recognition that the current forecast for inflation does not have it reaching the top of the target band until mid-2025. In previous communications the Board made a virtue of that long period as the ‘price’ to pay for maintaining most of the employment gains of recent years. Now we are hearing that the strategy is risky, leaving “little room for upside surprises to inflation given that inflation would have been above the target for around four years by that time”. This risk, which has been part of the policy scenario since the Bank began the tightening cycle, now appears to be unnerving the Board.

The upside risks, which are not new, centre on: services inflation in other countries, which has been persistently high; strong population growth; upward pressures on rents; weak productivity growth boosting unit labour costs; and a potential shift in inflation expectations (although still no evidence so far that this is occurring, and actual inflation is now declining).

The Board now also points directly at asset markets, the pause in April seen as likely partly contributing to a lift in house prices and lower Australian dollar. Commentary on both of these links them to the outlook for activity and inflation rather than implying policy is targeting asset markets. Concerns about a wealth effect from the housing market at this stage of the cycle seem to be a marked over-reaction.

The case for a pause was familiar: weak consumption; rising aggregate mortgage rates as low fixed rate mortgages expire; and a forecast increase in unemployment that might see inflation slow more quickly than forecast. The argument here is to hold steady to gain more information.

Given this rhetoric it seems surprising that “the arguments were finely-balanced” rather than overwhelmingly in favour of the hike.

That ‘finely balanced’ assessment also seems inconsistent with the return in the rhetoric to the February approach of discussing multiple rate hikes, although the phrasing “are likely to be needed” is replaced by “may still be required”.

Also, in the concluding line of the ‘Considerations for monetary policy’ section – “Members also agreed that further increases in interest rates may still be required, but it would depend on how the economy and inflation evolves” – the phrasing ‘further increases’ has replaced ‘monetary policy may need to be tightened’ which comes across as stronger language.

So we are left with a somewhat confusing message. The decision was ‘finely balanced’ but the case for tightening was made much more strongly than the case to hold.

The importance of the clear slowing in activity and its implications for demand-related inflation pressures seems to be underplayed. There is now a ‘cost’ of pausing – boosting asset prices.

The attraction of pausing to assess the cumulative impact of the most rapid tightening cycle we have seen seems to have less weighting, e.g. “there was a case to hold the cash rate steady in order to gather more information.” And the high frequency of meetings no longer rates a mention.

How the productivity argument can impact the near term outlook for policy is not explained – productivity, which is driven by the supply side of the economy, will evolve over the medium term and should not be a factor affecting the immediate policy outlook unless the Board is convinced that Australia is set for an extended period of further productivity erosion in which case the tightening cycle would have significantly further to run.

Conclusion

We still expect that the Board will choose to pause at the next Board meeting on June 6. But the case for further near-term rate increases cannot be dismissed.

The concerns the Board has around the risks to its inflation target are understandable but so are the signals around the sharp slowdown in spending and the likely feedback this will have on inflation and labour markets.

As the Board has outlined, the decision in May was ‘finely balanced’, therefore given the relentless frequency of Board meetings the case for a pause in June is respectable.

However, unless we see data on wages and the labour market later in the week that shocks the Board the next ‘live’ meeting should still be August 2 when there will be more information on the Board’s progress towards its inflation target while evidence around the consumer slowdown will be clearer.

As was the case in May, the arguments in August will again be ‘finely balanced’ although our forecasts point to an ‘on hold’ decision.

Will Australia’s Labor Data Tempt RBA to Hike Again?

Despite the Reserve Bank of Australia (RBA) saying at its May meeting that more rate increases may be required, investors are nearly convinced that it will take no action at the June gathering, and evenly split on whether another 25bps may be warranted in August or September. So, to get a better sense of how the RBA may proceed henceforth, they may pay close attention to wage growth and employment data, due out on Wednesday and Thursday, respectively.

Market expects the RBA to return to the sidelines

At its latest gathering, the RBA raised interest rates by 25bps, stunning investors who were expecting officials to stay sidelined for the second time in a row. Policymakers decided to hike due to stubbornly high services inflation and faster-than-expected rental increases, adding that more hikes may be required depending on how the economy and the inflation outlook evolve.

In the minutes of that meeting, released today, it was revealed that board members were considering staying sidelined for another month, but the inflation risks convinced them that a hike was a more appropriate decision.

Having said all that though, despite officials saying that more hikes may be required, and despite Australia’s consumer prices increasing 6.3% year-on-year in March, market participants are currently assigning an 87% probability for no change at the upcoming meeting in June, with the remaining 13% pointing to another quarter-point hike.

Perhaps that’s due to inflation being in a downtrend since December, when it hit 8.4% y/y, and due to Chinese data suggesting that after the post-reopening boost, the world’s second largest economy and Australia’s main trading partner is losing momentum.

Will the jobs data increase the chances of another hike?

Beyond June, investors are pricing in around a 30% chance for a quarter-point hike in July, while they are evenly split for August and September. So, as they try to better understand how the RBA could proceed later this year, they may pay attention to the wage price index for Q1 and the employment report for April, due out during the Asian sessions Wednesday and Thursday, respectively.

Wages are forecast to have continued to accelerate for the 9th consecutive quarter, which could add to concerns about inflation staying elevated, and although the employment change is expected to show that the economy added less than half the jobs it gained in March, the unemployment rate is seen holding steady at 3.5%, just a tick above its record low of 3.4%.

A tight labor market and rising wage growth, which according to the S&P Global services PMI, is contributing to accelerating price pressures for firms in Australia, could prompt investors to price in a higher probability for a hike during the summer months.

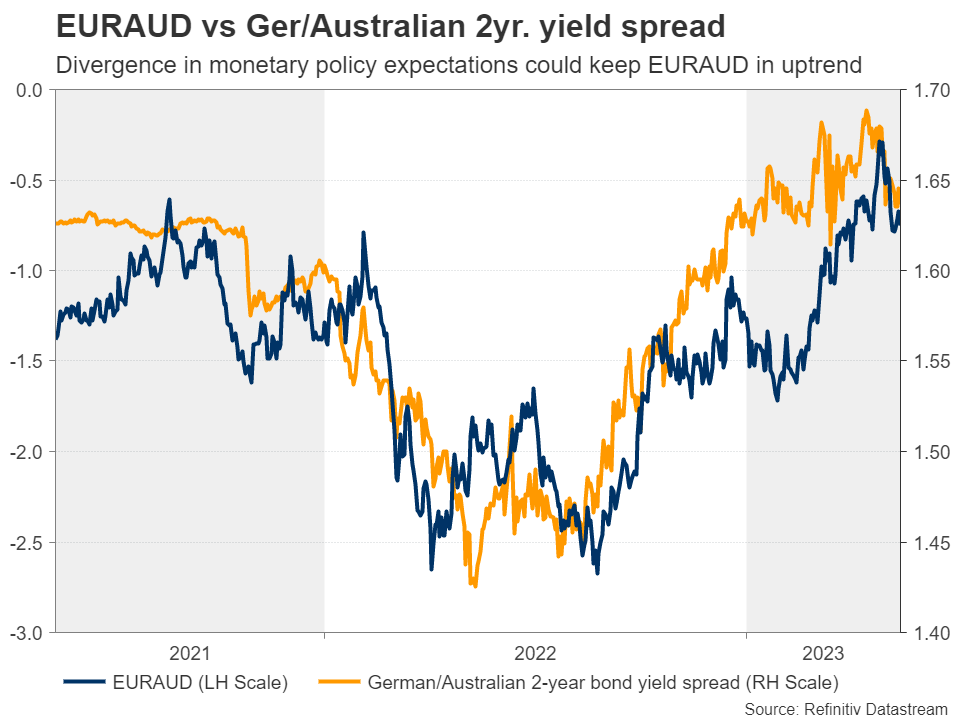

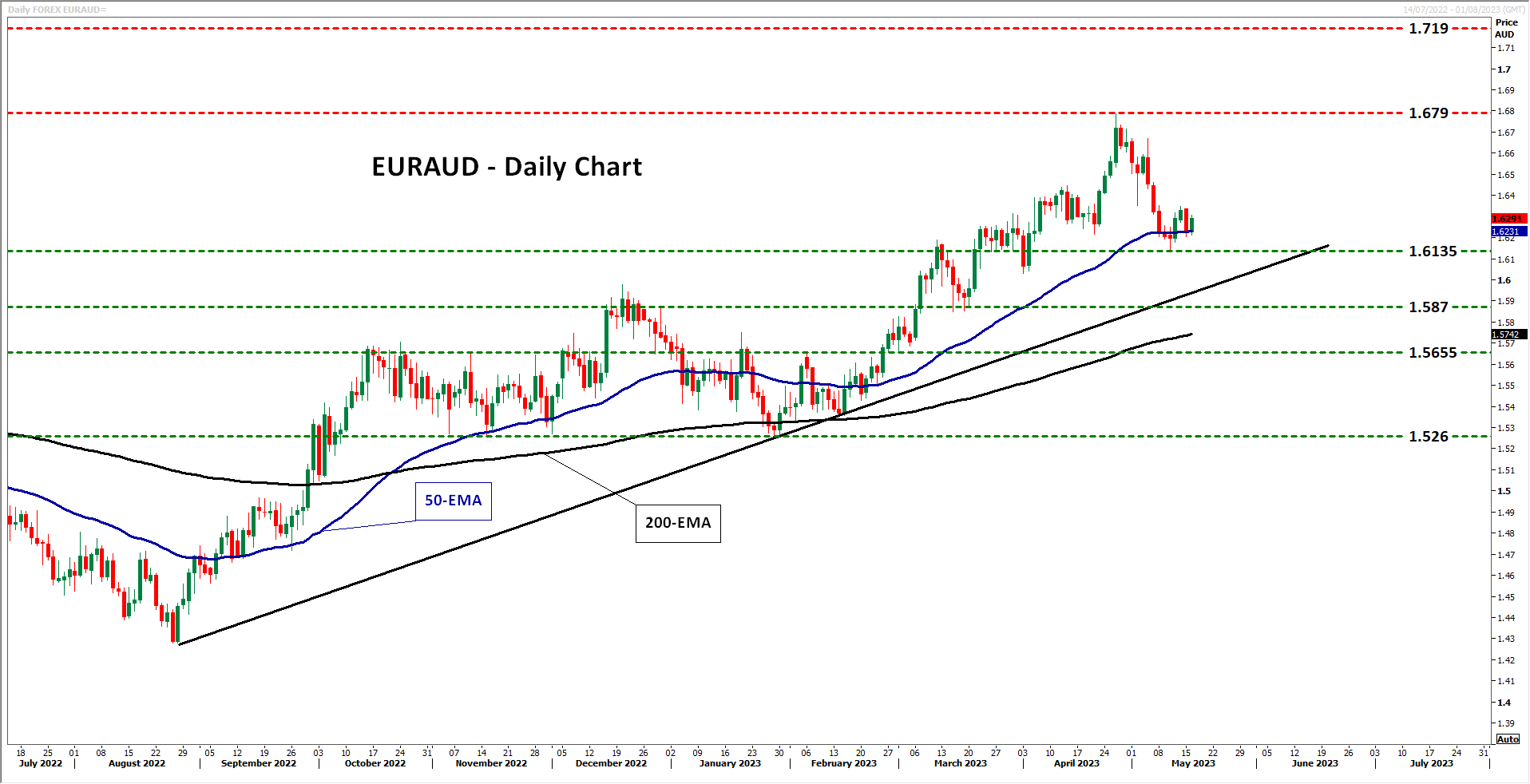

Aussie may be destined to stay weak for a while longer

This could prove positive for the Australian dollar, but its upside may be capped by market participants’ concerns over the outlook of the Chinese economy. With the Fed expected to proceed with nearly three quarter-point cuts by the end of the year, the picture in ausie/dollar may not be so clear, but with the ECB seen hiking by another 50bps, euro/aussie may be destined to continue its uptrend for a while longer, even if the Australian currency temporarily benefits by this week’s data.

Euro/aussie has been in a sliding mode since April 26, when it hit resistance at 1.6790, a territory that threw the bulls out of the game back in October 2020 as well. Nonetheless, the pair remains above the uptrend line drawn from the low of August 26, which keeps the bigger picture positive.

Even if the slide extends beyond last week’s low of 1.6135, the buyers could still step back into the action from near the uptrend line and perhaps stage another march towards the 1.6790 zone. If they manage to break that zone, they could then put the 1.7190 area on their radar, which offered resistance back in early May 2020.

The outlook could start darkening if the bears are able to break the aforementioned uptrend line, but also the 1.5870 support. Should this happen, they may get encouraged to dive towards the 1.5655 territory, marked by the inside swing high of February 6, the break of which could see scope for extensions towards the 1.5260 area, which acted as a floor between November 4 and January 30.

US Default: If the US Government Runs Out of Money, What Direction Will the Markets Take?

Who would have thought that we would ever see a time during our lives in which it could be possible for the United States, the world’s commercial and economic superpower since the industrial revolution, to potentially run out of money?

Perhaps even more of a stretch of imagination would be needed to comprehend that the United States national coffers would run up a debt so high that it would not be able to service the repayments, despite the country’s almost 250-year long history of hard work, ingenuity and commercial marketing genius.

Nowadays the American Dream is made in China, and the overall cost of operations is at an all-time high, whilst competition from almost every corner of the earth is rife and has been challenging American corporate hegemony for a while now.

A national economy which now survives on debt means that at some point, the borrowing needs to be repaid, and in the case of the United States, there is a ‘debt ceiling’ in place which is an actual law which limits the amount that the US government is allowed to borrow, which currently stands at $31 trillion.

National debt is now at such a high point that the debt ceiling has been almost approached, and the government is weighing up making plans to raise it so that it can borrow more money.

Every few years, a government can, according to the law, bring in a vote to increase the debt ceiling, however, at a time during which the country is on paper heading toward bankruptcy, is borrowing more a good idea?

During the discussions within the US Congress over recent days, many have observed that the United States government could run out of money as soon as June 1 this year.

That may well be an alarming prospect, but rather interestingly, there are swathes of reports which depict a very calm approach by investors and traders.

The question remains: which assets will likely be affected?

1: American big tech: The FAANG stocks

During the past two years, the ‘big tech’ arena of American stocks listed on the NASDAQ and New York Stock Exchange have been surprisingly volatile.

These days, ‘big tech’ does not refer to engineering or physical hardware manufacturers, but largely to internet companies which either offer e-commerce such as Amazon, search & SEO giants like Google, social media platforms such as Facebook (Meta), or online video streaming such as Netflix.

These tend to dominate the American stock markets, and their Silicon Valley base tends to dominate the entire tech development for the world.

During the lockdowns of 2020 and 2021, the American government along with many western allies attempted to change the behaviour of the population, largely succeeding to do so, and tens of millions of people moved their social life and work life online. These platforms boomed.

Then in 2021 and 2022, they crashed. There was a US tech stock downturn, which lasted almost a year.

Now, with costs up and a national debt which is becoming unserviceable in their homeland, will Chinese, Indian and Eastern European locations become favourable for global tech giants?

If so, the tremendously high cost of operating in Silicon Valley may be looked at.

We saw Israeli-owned American high tech firms pull over $30 billion in operating funds out of Israel when the new government took office earlier this year, resulting in a downgrading of the entire country’s credit rating. $30 billion is a lot for a small country but is nothing for the US. Imagine what may happen if large, borderless multinationals become concerned about the fluidity of the US economy and move their business to Mexico, India, Brazil, China or a combination of all of these.

Right now, nobody is panicking, but who knows what decisions will be made if the credit crunch arrives.

2: The US Dollar

Aside from corporate concerns in the boardrooms of American publicly listed giants, there is a simpler aspect to consider: The US Dollar.

America’s sovereign currency has for many decades been the de facto major currency against which everything, everywhere in the world is measured.

It is regarded as the most stable, most traded and most circulated currency in the world. Everyone is safe with Dollars, right?

Well….

Since September last year, the British Pound, which was on a road to oblivion during most of 2022, has been gaining significant ground against the US Dollar.

On September 16, 2022, the British Pound was at 1.16 against the US Dollar, whereas today, a few US bank demises, billions spent on overseas wars, and a credit catastrophe later, the British Pound is at 1.25 against the US Dollar.

Fluctuations that great are usually reserved for exotic currencies and it is very rare that majors would experience such a degree of volatility, but here we are in May, with a strong Pound against the US Dollar despite the UK’s own economic problems including high inflation, an energy price crisis and 12 years of ‘austerity’.

The US Dollar would perhaps be worth watching if a default does actually happen, as it may well be the first time in decades that its standing as the de facto currency has been challenged. After all, if its own central bank and central government is bankrupt, it would be being issued by an insolvent institution.

3: Credit Default Swaps

What is a Credit Default Swap? These are relatively unheard of by many mainstream traders, and of course are less relevant to the everyday lives of most currency and commodity traders, however, they’re worth a quick mention here.

A Credit Default Swap is a derivative which allows one investor to swap a default on a debt with another investor. To swap the risk of default, the lender buys this particular product from another investor who agrees to reimburse them if the borrower defaults.

These have been spiking as traders head toward betting on the possibility of a default and attempting to profit from it.

Therefore, the popularity of these swaps is a demonstration of the sentiment that many people are considering that a default by the US government on its debt could actually happen.

4: FTSE 100

The good, old-fashioned London Stock Exchange. What do you mean old fashioned? You may ask. Well, the London Stock Exchange may indeed be state of the art in its execution and electronic trading prowess, but the companies listed on it, especially the top drawer, blue-chip companies, are very much of the old school.

Compared to the NASDAQ’s straight-to-market, out-of-the-blue SPAC-listed startups with valuations of several billion dollars, many of which have barely distributed a product, London Stock Exchange is a bastion of established, well-rounded companies which rarely take risks and are evergreen.

The FTSE 100 index is the basket of stocks which make up the 100 most prestigious, large-cap companies on the London Stock Exchange, many of which are in traditional sectors such as pharmaceuticals, mineral extraction and mining, air and rail travel, shipping, retail and commercial banking, entertainment and leisure, and supermarkets and food distribution.

Should the US government default on its debts and destabilise the US economy, investors may look toward the steady, tortoise-like FTSE 100 index for its age-old corporations with histories as long as most people can remember, and eschew the Silicon Valley crowd, both established or SPAC listed, across the pond on New York’s trading venues.

Whichever way, this is a very turbulent time and will be regarded as an historic moment on the US commercial landscape.

Will the default take place or will America get even deeper into debt?

We shall soon find out…

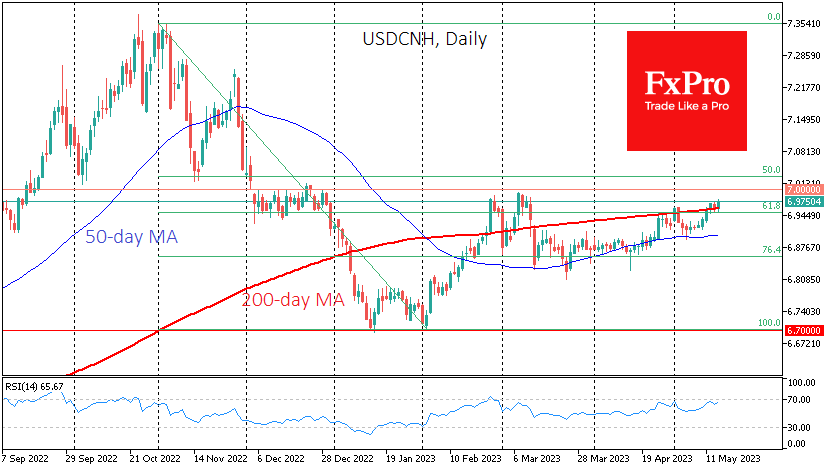

China’s Recovery Falls Short of Expectations

China’s economic growth is falling short of economists’ expectations, putting pressure on the yuan and raising questions about the sustainability of the national and global economies.

Industrial production rose 5.6% y/y in April, but the average forecast was 10.9% y/y due to low base effects. Retail sales growth also missed expectations, reaching 18.4% y/y versus the expected 22%.

Disappointing data is more a manifestation of economic inertia than a sign of weakness. Assuming that the problem is simply one of the inflated market expectations, the situation in China looks much better than in most developed countries. The unemployment rate has fallen to its lowest level since November 2021, which bodes well for the coming months. With jobs, people are spending more, so the outlook for the coming months is less bleak.

The weaker-than-expected data put pressure on the renminbi. The USDCNH briefly touched 6.978, a high of 6.978 this morning, and is now approaching a test of the psychologically important 7.0 level, which the pair has failed to break since last December. A break above this level could be an important milestone for the forex market, adding to the general pressure on the renminbi and risk assets.