Sample Category Title

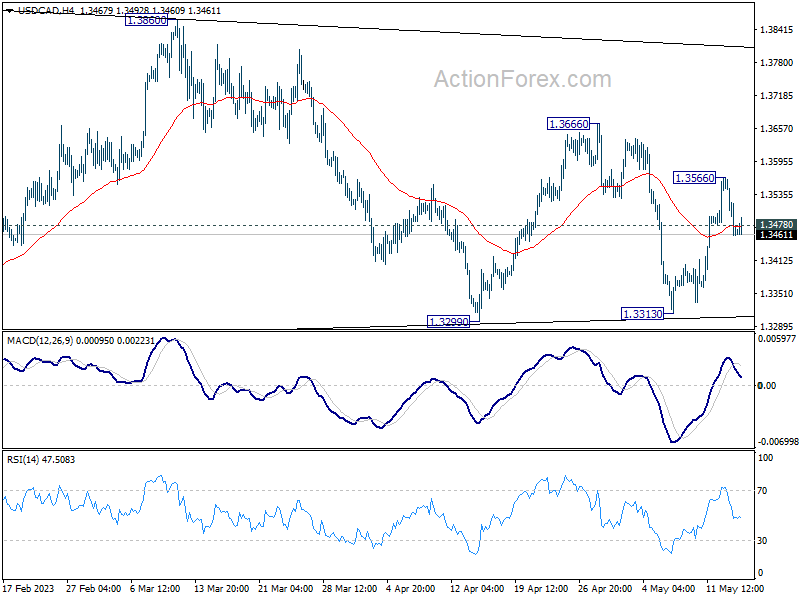

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3504; (P) 1.3534; (R1) 1.3589; More....

Intraday bias in USD/CAD is turned neutral again with break of 1.3478 minor support. Overall, it's seen as extending the triangle consolidation pattern from 1.3976. Above 1.3566 will resume the rebound towards 1.3666 resistance and then 1.3860. However, firm break of 1.3313 support will invalidate this view and indicate that deeper correction is underway.

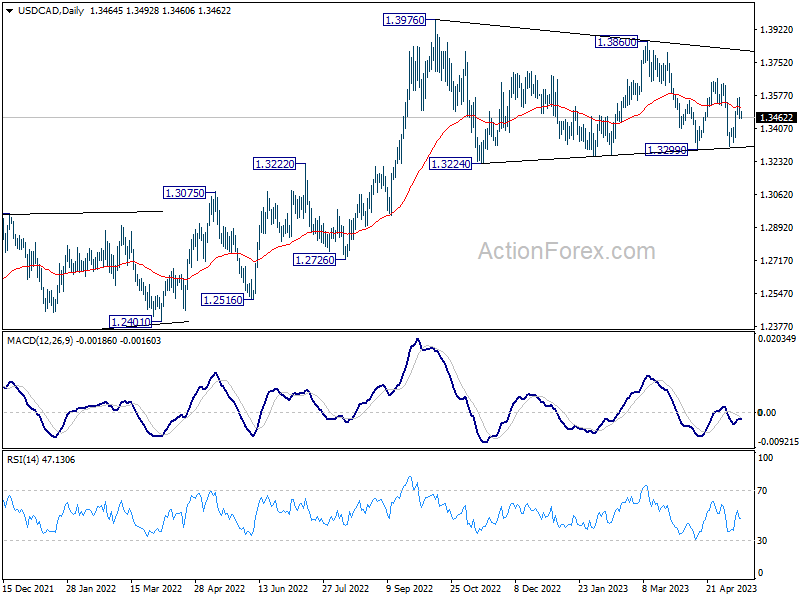

In the bigger picture, as long as 55 W EMA (now at 1.3321) holds, up trend from 1.2005 (2021 low) is still in favor to resume through 1.3976 at a later stage. However, sustained trading below the EMA and 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will raise the chance of bearish reversal. Deeper should then be seen to 61.8% retracement at 1.2758 next.

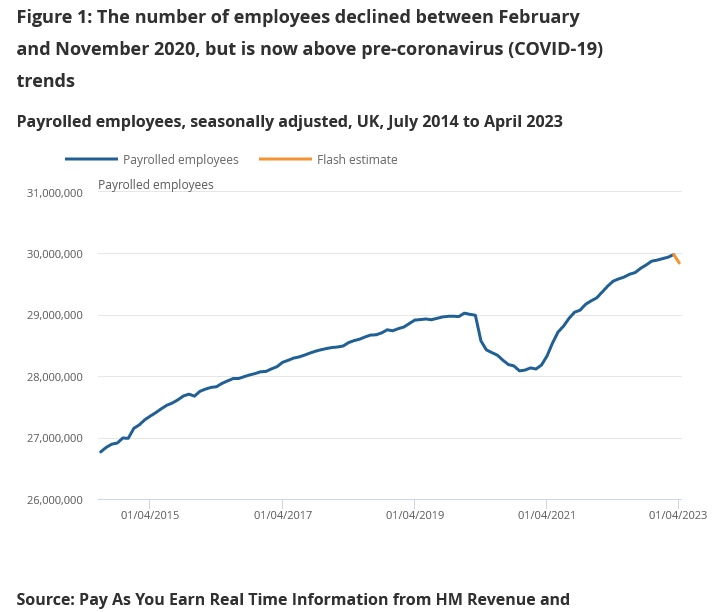

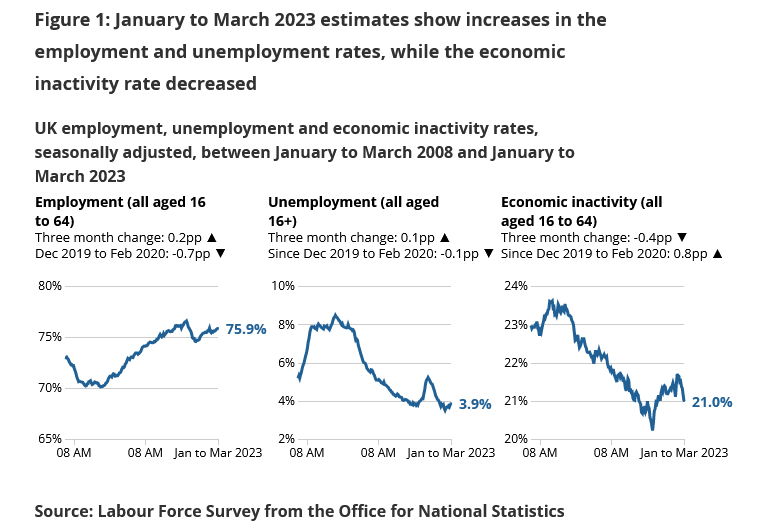

UK payrolled employees dropped -136k in Apr, unemployment rate rose to 3.9% in Mar

UK payrolled employees dropped -0.5% mom, or -136k in April, comparing with March. That is the first decline in total payrolled employees since the COVID pandemic. Comparing with April 2022, payrolled employees rose 1.0% yoy or 297k. Claimant counts rose 46.7k, above expectation of 31.2k. Median monthly pay rose 7.4% yoy.

In the three months to March, unemployment rate rose 0.1% to 3.9%, comparing to the previous quarter. Employment rate rose 0.2% to 75.9%. Average earnings including bonus rose 5.8% 3moy. Average earnings excluding bonus rose 6.7% 3moy.

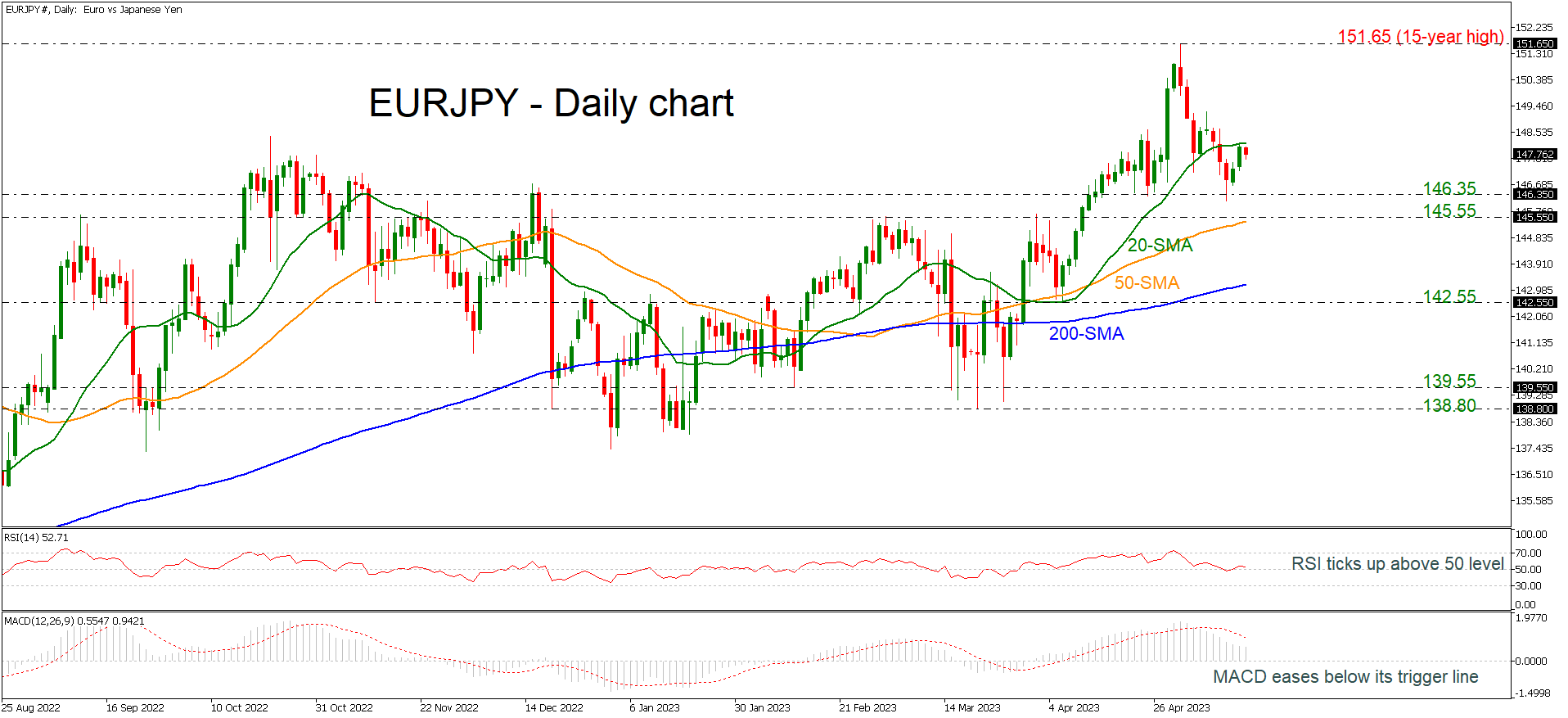

EURJPY Capped by 20-day SMA Before Bullish Move Can Continue

EURJPY is capped by the 20-day simple moving average (SMA) around 148.20 after the rebound off the 146.35 support level.

The short-term bias looks negative as the MACD keeps losing ground below its red signal line, while the RSI seems to be making its way down near its 50-neutral mark.

The 20-day SMA currently at 148.20 could be a trigger point for steeper bullish action if the pair manages to break the line. Higher resistance could run towards the 15-year high of 151.65, registered on May 2 through more buyers could be waiting to enter the 152.00 psychological region.

However, if the pair reverses back to the downside, investors could move first at 146.35 and then at 145.55. If the price continues to drop, support could next come somewhere near the 50- and the 200-day SMAs at 145.35 and 143.13 respectively.

In the near-term picture, the bounce off 146.35 turned the outlook from negative to neutral again. Chances for another bullish move are still rising as the 50-day SMA keeps rising above the 200-day SMA.

AUD/JPY Technical: Potential Push Up Within a Major Range

- Two conflicting fundamental factors are driving the short-term movement of the Aussie dollar.

- RBA’s hawkish rhetoric has provided a potential floor but a weak external environment due to China prevents bulls from taking an aggressive stance.

- AUD/JPY key short-term support stands at 90.30 with major range resistance coming in at 92.10/92.80.

The Aussie dollar seems to be trapped by two conflicting fundamental factors in the short to medium-term horizon.

Firstly, the positive factor that supports potential strength in the Aussie dollar comes from the hawkish rhetoric portrayed by Australia’s central bank, the Reserve Bank of Australia (RBA) after its surprise 25 basis points hike on its policy interest rate to 3.85% on 2 May.

Today’s release of the minutes of RBA’s monetary policy meeting for 2 May has revealed that policymakers were concerned about weak productivity growth that would trigger inflation risks, persistently high services inflation, and faster-than-expected rental increases that may require a further rise in interest rates.

In contrast, the current weak external environment is likely to have an adverse impact on the economic growth of Australia due to less demand for its top industrial-related commodities exports such as coal and iron ore.

In addition, the latest macro data from China; Australia’s top trading partner suggests more evidence of a slowdown in its recovery spurt. Both consumer spending and industrial activities grew slower than expected in April. Industrial production grew by 5.6% year-on-year from 3.9% recorded in March but way below the consensus of 10.9%. Retail sales increased by 18.4% year-on-year, below the consensus of 21% but above March’s print of 10.6%.

AUD/JPY Technical Analysis – May see a retest on its 92.10/92.80 major range resistance

Fig 1: AUD/JPY trend as of 16 May 2023 (Source: TradingView, click to enlarge chart)

Since its 20 December 2022 swing low of 87.00, the AUD/JPY cross pair has evolved into a major sideways range configuration below a key 200-day moving average that is acting as a resistance at a zone of 92.10/92.80 as seen from the daily chart.

In the shorter-term time horizon depicted by the hourly chart, the price actions of AUD/JPY have managed to trace out a series of “higher lows” that is being supported by a minor ascending trendline in place since the 26 April 2023 low of 87.87 that is now acting as a key short-term pivotal support at 90.30.

In addition, the hourly RSI oscillator has just managed to stage a bounce right above its corresponding support at the 47% level which suggests that potential short-term upside momentum remains intact.

The intermediate resistance to watch will be at 92.10. However, a break with an hourly close below 90.30 negates the bullish tone to expose the next support at 89.35 (swing low area of 5 May 2023 & ascending trendline from 24 March 2023 low).

Gold Seen in Consolidation Phase

Gold is bullish on higher time frame charts where we expect a break to new ATH high, but ideally, this will occur after the current complex correction is completed. Notice that recovery from 1970 to 2070 was made by three waves, ideally it was wave B as part of a higher degree fourth wave that can be even a triangle. If we are correct then more slow and sideways price action will show up to complete the pattern, ideally still some time this month when we will start looking up towards 2100. If we are correct then 1958 and 1971 levels should hold as a support. If they are broken then the structure and trend will change.

USD Consolidates Recent Gains

EUR/USD grinds critical floor

The US dollar consolidates amid worries about the debt ceiling stalemate. The euro’s drop below 1.0940 has led short-term buyers to liquidate their positions. The pair is testing 1.0840 from the start of a breakout rally in mi-April. This is a critical floor to maintain the single currency’s lead and a bearish breakout would open the door for a drop towards the March lows of 1.0550. The RSI’s oversold situation has attracted some bargain hunters and they have to clear the support-turned-resistance at 1.0940 to ease the pressure.

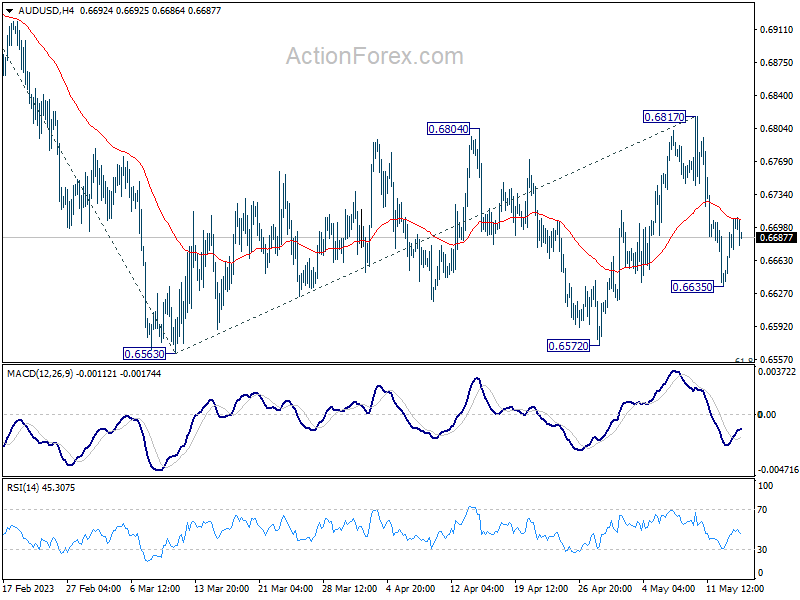

AUD/USD attempts to bounce back

The Australian dollar recouped some losses after hawkish RBA meeting minutes. The pair is striving to hold on to its gains from the rally earlier this month with the base of the bullish breakout at 0.6630 as an important level to keep the aussie’s edge. A close above 0.6700 is an encouraging signal and the bulls will need to lift 0.6750 before they could hope for a sustained extension. On the downside, a bearish breakout would expose the double bottom (0.6580) on the daily chart which is a critical floor in the medium-term.

Dow Jones 30 awaits breakout

The Dow Jones 30 steadies as traders wait for a breakthrough in the US debt-ceiling talks. The index is still consolidating its gains after breaking above 33500. 32950 is the current support where buyers have stepped in, but 33800 has proven to be a tough level to crack after two consecutive failed attempts. Its breach would bring the price back to the major supply zone around 34300 where a breakout could trigger an extended recovery towards 35000. On the flip side, a deeper correction may send the price to 32300.

Fed Speakers Show Growing Divergence on How to Proceed with Monetary Policy

Markets

Fed speakers show growing divergence on how to proceed with monetary policy. Atlanta Fed Bostic (non-voter) is inclined to pause at the June meeting, but he confirmed that the committee is still out on the issue. If he had a bias between going up or down as a next move, it would still be up. Resilient consumer spending and tight labour markets pose upside inflation risks even as the Fed’s earlier tightening measures will start having a bigger impact. Bostic pointed to the load of data coming out between the May and June policy meetings, which could alter the decision of him and his colleagues. Whatever the outcome in June, Bostic pushed back against the (financial markets’) idea about cutting policy rates soon. His baseline is to keep them at whatever peak rate until well into 2024. Minneapolis Fed Kashkari (voter) stressed that there is still a long way to go before inflation gets back down as the labour market is still hot. Therefore the Fed probably has more work to do and shouldn’t be fooled by a few months of positive (inflation) data. Richmond Fed Barkin (non-voter) told the Financial Times that there’s no barrier in his mind to further increase interest rates if inflation persists, or God forbid accelerates. He doesn’t see the urgency of making a different decision because of financial stability risks. He’s not convinced that the story of waning fiscal stimulus, eroding personal balance sheets, the lagged effects of rate moves, credit tightening and cooling demand will turn into reality which pulls inflation significantly down. Chicago Fed Goolsbee (voter) is on the other side of the aisle. He was close to dissenting last month given turmoil in the banking sector and is in for a pause in June as there’s still a lot of the impact of the 500 bps of Fed rate hikes to come. US Treasuries at the end of the day lost ground with yields adding 2.2 bps (2-yr) to 5.3 bps (30-yr). The German yield curve moved in similar fashion with yields adding 0.7 bps (2-yr) to 4.9 bps (30-yr). Both real rates and inflation expectations increased. EUR/USD recovered from last week’s losses, consolidating around 1.0870. Stock markets overall gained around 0.5%. Today’s eco calendar is stuffed with amongst others German ZEW investor confidence and US retails sales. Central bank speakers are plenty including ECB Lagarde. Another high level political meeting on raising the US debt ceiling serves as a wildcard. Strong UK labour market data this morning fail to inspire sterling after BoE chief economist yesterday hinted to prefer a rate pause at the next policy meeting. EUR/GBP remains just below the 0.87 big figure.

News and views

A series of monthly eco data (April) published this morning showed a rather sluggish post-pandemic recovery in China. At 18.4% Y/Y (8.5% YTD Y/Y) and 5.6% Y/Y (3.6% YTD Y/Y) respectively for retail sales and industrial production, both series disappointed. The high April Y/Y figures mostly mirror a low comparison base due to lockdowns in Shanghai and other cities that heavily impacted growth in April last year. Investment activity was below consensus as well with fixed asset investment rising only 4.7% YTD Y/Y (from 5.1% in March). Property investment even declined (-6.2% YTD Y/Y from -5.8% in March). The jobless rate eased from 5.3% to 5.3%, but a record high 20.4% youth unemployment rate is a high source of concern. The data are raising speculation that the PBOC will have to take additional easing measures to support activity. The yuan weakens slightly further this morning with USD/CNY trading just below 6.96.

The Westpac-Melbourne Institute index showed that Australian consumer confidence tumbled substantially in May. The deterioration was visible in most subcategories of the index. Overall sentiment dropped from 9.4% to -7.9%, with the decline being visible both in current conditions (-4.8% from +10.0%) and expectations (-9.6% from 9.1%). Families turned negative both on their financial conditions and the on the economy. According to the Westpac Chief economist, the decline in sentiment was affected by the announcement of the new Budget and the unexpected RBA decision to further raise the policy rate by 25 bps at its May meeting. Minutes of that RBA May 2 policy meeting revealed that some members wanted a pause and that the arguments were finely balanced but finally higher inflation risks prevailed as inflation was not expected to decline to the top of the 2-3% inflation target till mid-2025. Further increases in the interest rate might still be required, but this will depend on how the economy and inflation will evolve. The Aussie dollar declines modestly this morning from the AUD/USD 0.671 area to 0.6685, but this is probably in part due to lower than expected Chinese data rather than Australia related news.

Chinese April Data Disappoints

Market movers today

Today we will look out for one of the early indicators of May economic activity in Germany with the ZEW index.

The US releases retail sales providing more insights to the state of the US consumer. We also have FOMC members Mester, Williams and Bostic on the wires.

In Sweden, Prospera inflation expectations are published, see more below.

Overnight, the first Q1 GDP estimate is released from Japan. The service sector has improved through Q1 while the manufacturing sector is struggling like we see globally. Consensus has a 0.1% increase.

The 60 second overview

Chinese April data disappoints: As signalled by weak PMI's lately, April activity was weaker than expected. Retail sales increased from 10.6% y/y in March to 18.4% y/y in April but it was less than consensus expectation of 21.9% and it hides over a big monthly drop in April, as the y/y rate is lifted by favourable base effects from the plunge in April seen last year during the Shanghai lockdown. Industrial production also disappointed rising only to 5.6% y/y (consensus 10.9% y/y) from 3.9% y/y, despite similar positive base effects. Home sales were also soft showing a big monthly decline in April. Overall the data clearly suggests, the recovery weakened in April after a very strong Q1.

The coming months will be key for showing whether this is a temporary set-back to a "too strong" Q1 after the reopening or whether it reflects a faltering recovery. Comments from the National Bureau of Statistics showed concern saying that "the property market is in recovery but more efforts are needed" and that "insufficient demand restricts the industrial sector". We are likely to see more monetary policy stimulus soon on the back of these data as inflation is also running close to 0% currently. Chinese stocks were slightly higher overnight as the soft data was already priced in markets.

Weak US data: The US Empire index, the first regional survey for May, dropped sharply from 10.8 to -31.8, close to the recent low in January. The indicator is very volatile so monthly observations should be taken with a grain of salt. Yet, it points to a still weak US manufacturing sector.

Fed's Bostic does not see rate cuts until well into 2024: "My baseline case is we won't really be thinking about cutting until well into 2024," Bostic said Monday in an interview on CNBC. "If you look at most measures of inflation, they're still two times where our target is. And so that's a long distance still to go." "If I had a bias between going up and going down as our next action, I would say we might have to go up." This contrasts with market expectations of 65bp in H2 this year. We expect the Fed to be on hold rest of the year.

New forecasts from the EU Commission: Yesterday, the EU Commission lifted euro area growth forecasts saying that the economy had performed better over the winter. 2023 growth was revised higher to 1.0% from 0.8% and 2024 growth to 1.7% from 1.6%. The Commission sees inflation falling from 5.8% this year to 2.8% in 2024 (Danske Bank 2.1%), and hence still clearly above the ECB's 2% target.

Equities: Global equities higher yesterday despite very weak macro data. Yet another day with little volatility and relatively little market moving news. Markets reacted negatively to the big plunge in the Empire Fed index but moves started to fade the shortly after the surprise. In US, Dow +0,1%, S&P500 +0,3% and Nasdaq + 0,7%. Asian markets are holding on to gains this morning despite weaker than expected data from China. European futures a little higher while US futures are a little lower.

FI: There was a modest rise in global bond yields yesterday combined with a bearish steepening of the global yield curves. However, the spread between the peripherals and Bunds tightened modestly. Furthermore, the German ASW-spreads also tightened and the Bund ASW-spread dipped below 70bp.

FX: Commodity currencies AUD, NZD, CAD and NOK were the biggest winners on the back of a rising oil price in a relatively quiet session yesterday. EUR/USD still trading below the 1.09-mark. USD/JPY climbed above 136. EUR/NOK fell to around 11.53, while EUR/SEK initially appreciated on a soft CPI print from Sweden but later retraced and ended the session lower below 11.25. GBP strengthened and took EUR/GBP below 0.87.

Nordic macro

In Sweden, Prospera May money market inflation expectations will be released. In recent months 1y CPIF expectations have stabilized at 4%, while 2 and 5 y expectations have risen slightly to 2.4 % and 2.2 %, respectively. We expect to see a resumption of the downward trend on all horizons as other survey data suggests declining corporate selling price expectations.

Agreement on US Debt Ceiling Unlikely Before Last Minute

US stocks kicked off the week on a slightly positive note on the back of weak economic data – that fueled the Federal Reserve’s (Fed) pause expectations, glim hope that the debt ceiling talks between Joe Biden and Kevin McCarthy could lead to resolution and on Microsoft gaining EU approval to buy Activision.

But all of the latter are weak reasons to jump on a bullish trade because,

1. the New York Empire State Manufacturing index slumped to -31.80 in May, versus a slump to around -3.70 expected by analysts. Slowing activity brings forward the idea that the Fed will stop hiking interest rates on slowing growth, but Minneapolis Fed head Kashkari warned investors that the Fed will tighten more, Atlanta Fed’s Bostic said the Fed should hold, but in no case cut the rates this year, while Chicago Fed’s Goolsbee didn’t want to promise a pause in June. He said that he watches the data and remains ‘extra mindful of the hikes’ impact on credit conditions.

While a June Fed hike is still off the table, activity on Fed funds futures hint that investors see higher odds for a rate hike next month. The probability of a 25bp hike now stands at 19%. But of course, the data and how the debt ceiling talks go will be crucial in what the Fed could and would do.

2. Even though investors bought hope of a possible breakthrough on US debt ceiling impasse when Biden and McCarthy meet today, McCarthy warned that they ‘are nowhere near reaching a conclusion’. The negotiations will likely remain tight as Republicans ask decent spending cuts to accept a debt ceiling relief, while Biden is not willing to compromise on spending into the election year. Therefore, even if Biden was to blink, he’d better do it at the last minute – to show his electors that he did his best to avoid an otherwise unavoidable default. Anything else would probably be a political mistake.

In this context, there is little chance we will see a resolution to the US debt ceiling issue today. And that’s certainly why the US 2-year yield pushed higher yesterday despite the scary NY manufacturing index read. The 2-year yield is again in a tight range around 4%, with looming risks to the upside in the short-run, which could lead to an interesting buying opportunity at discount for investors who bet that the US won’t default on its payments and that the Fed will loosen its policy later this year.

P.S For investors, a default means US government not servicing the debt. Period. Investors don’t care much whether the US government workers will get paid or not. They just care about whether the US will be able to service its debt. So here, there is a nuance. And even in an extreme case, like in 2013 when we saw the US government shut for weeks, it wasn’t considered a default because 1. US didn’t default on its debt payments, so for investors, frankly speaking, there was no default whatsoever. Ut even politicians didn’t call the 2013 government shutdown a default, they said it was just a ‘lapse in appropriations’. So even in case of a government shutdown, the US can avoid a proper default.

3. Microsoft won the EU approval to buy Activision. The European Commission says its analysis shows that the huge $69bn acquisition would not harm competition because Microsoft will let its cloud rivals offer titles such as Call of Duty on their own platforms for 10 years, the US and UK regulators are not convinced. The British regulators clearly said they stand by their decision that it’s not a go!

Weak Chinese data

The latest economic data released in China showed that retail sales and industrial production grew slower than expected in April, while fixed asset investment unexpectedly fell. Crude oil traded past $71pb yesterday on news that People’s Bank of China boosts liquidity to fuel growth in China, but as long as the hard data is not there to confirm improved activity, it will be hard for oil bulls to justify an advance above the 50-DMA, which stands a touch below the $75pb.

Moving forward

Investors will keep an eye on European growth and sentiment data, the US retail sales figures and Home Depot earnings. In the coming days, other US retailers including Target and Walmart are due to announce earnings to give a sense of how US consumers are coping with the sticky-high inflation.

The latest GDP report revealed surprisingly resilient consumer spending – which in return puts a positive pressure on inflation expectations, and Fed bets. Therefore, any further resilience in retailer earnings would keep the Fed hawks alert.

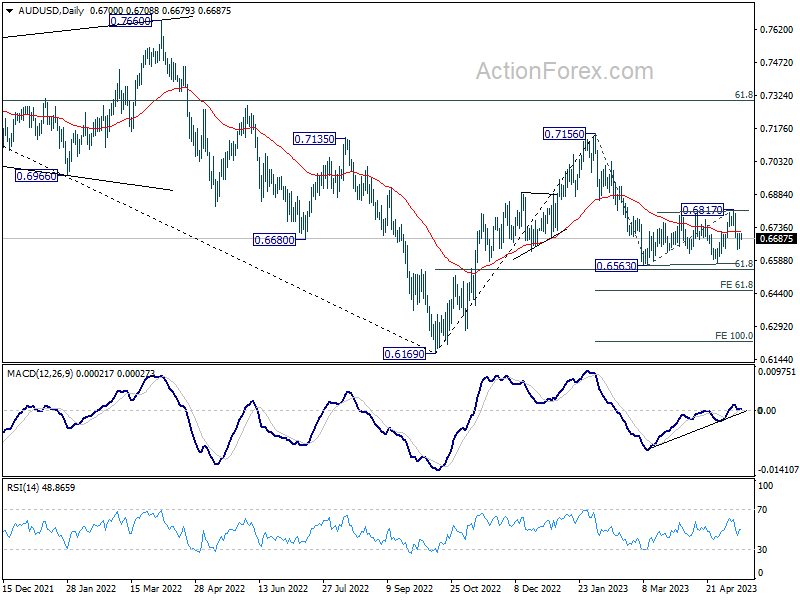

AUD/USD Daily Report

Daily Pivots: (S1) 0.6658; (P) 0.6684; (R1) 0.6725; More...

Intraday bias in AUD/USD is turned neutral first with current recovery. But risk will stay on the downside as long as 0.6817 resistance holds. Consolidation pattern from 0.6563 could have completed with three waves to 0.6817. Below 0.6635 will bring retest of 0.6563 low first. Decisive break there will resume larger decline from 0.7156 to 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451.

In the bigger picture, the failure to break through 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Firm break of 61.8% retracement of 0.6169 to 0.7156 at 0.6546 will raise the chance of long term down trend resumption through 0.6169 low. This will now be the favored case as long as 0.6817 resistance holds.