Sample Category Title

Fed’s Goolsbee highlights yet to be seen impact of Rate Hikes

In an interview with CNBC, Chicago Fed President Austan Goolsbee noted that the full impact of the 500 basis points increase executed over the past year has yet to fully materialize. He expressed concern over the tight credit conditions that currently prevail and urged careful monitoring of the economic landscape.

Goolsbee mentioned that his support for a rate hike earlier this month was a "close call." He stated, "The thing that made it a close call for me is this big question mark about what is going to be the impact of this on credit conditions."

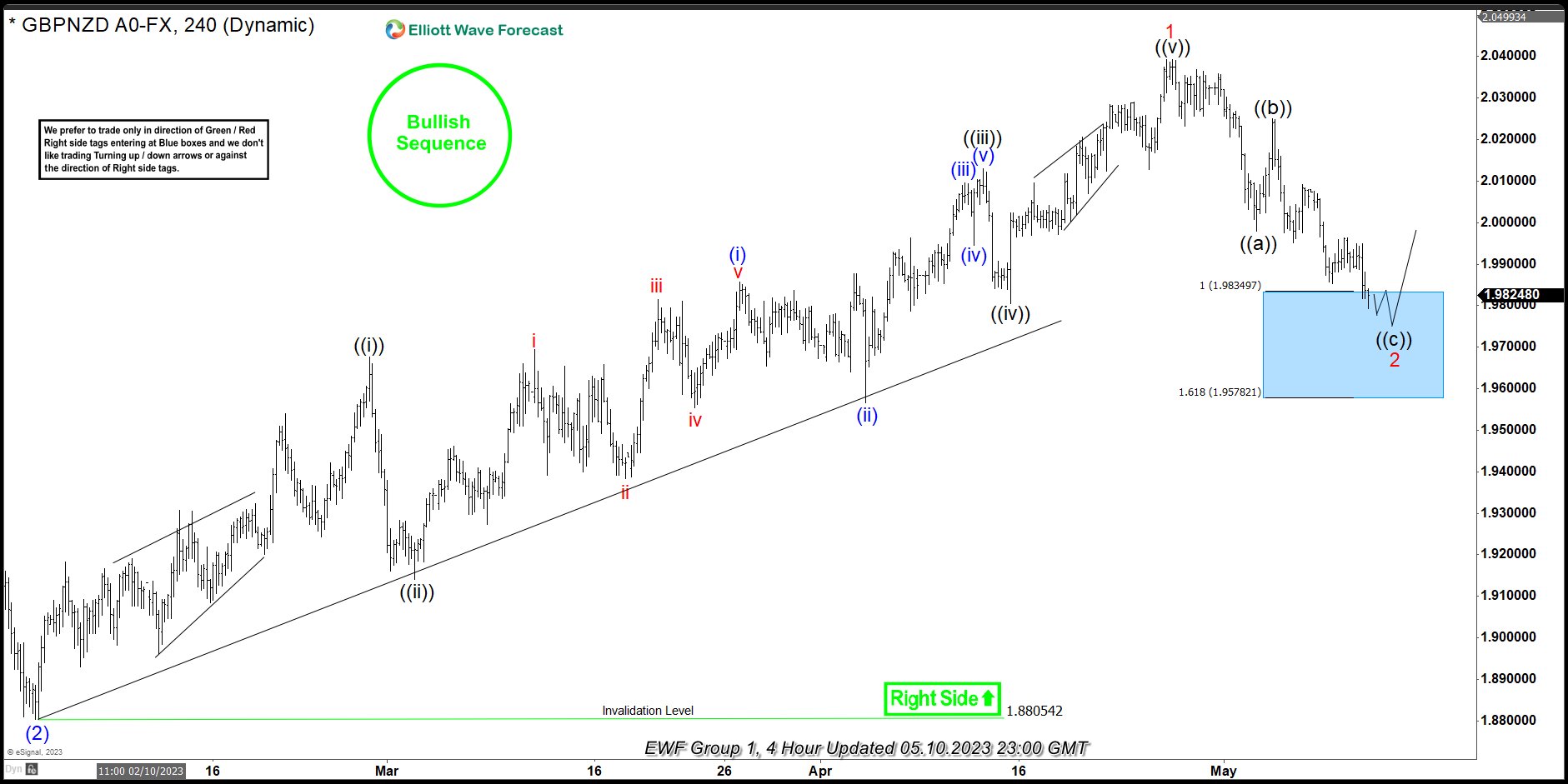

GBPNZD Reacting Strongly From The Blue Box Area

In this technical blog, we will look at the past performance of the 4-hour Elliott Wave Charts of GBPNZD. In which, the rally from the 03 February 2023 low unfolded as an impulse sequence and showed a higher high sequence with a bullish sequence stamp. Therefore, we knew that the structure in GBPNZD is incomplete & should see another extension higher to complete the sequence. So, we advised members not to sell the pair & buy the dips in 3, 7, or 11 swings at the blue box areas. We will explain the structure & forecast below:

GBPNZD 4-Hour Elliott Wave Chart From 5.10.2023

Here’s the 4hr Elliott wave Chart from the 5/10/2023 update. In which, the rally to 2.0393 high ended 5 waves from the 2/03/2023 low in wave 1 & made a pullback in wave 2. The internals of that pullback unfolded as Elliott wave zigzag correction where wave ((a)) ended at 1.9978 low. Then a bounce to 2.0250 high-ended wave ((b)) & started the next leg lower in wave ((c)) towards 1.9834-1.9578 blue box area. From there, buyers were expected to appear looking for new highs ideally or for a 3-wave bounce minimum.

GBPNZD 4-Hour Latest Elliott Wave Chart From 5.13.2023

This is the latest 4hr Elliott wave Chart from the 5/13/2023 Weekend update. In which the pair is showing a strong reaction higher taking place, right after ending the zigzag correction within the blue box area. Allowed members to create a risk-free position shortly after taking the long position at the blue box area. However, a break above 2.0393 high is still needed to confirm the next extension higher & avoid a double correction lower.

Sunset Market Commentary

Markets

There was little hard eco news to guide markets at the start of the week. In its spring forecasts, the European Commission raised its forecasts for EMU growth to 1.1% for 2023 and 1.6% for 2024 (was 0.9% and 1.5% in February winter forecast). The better performance is due to a ‘terms-of-trade countershock’ caused by declining energy prices, by abating supply constraints, improved business confidence and a strong labour market. The EC also took notice of a decline in headline inflation due to lower energy prices but acknowledged that core inflation firmed, pointing to persistence of price pressures. The inflation outlook for EMU was upwardly revised to 5.8% for 2023 and 2.8% for 2024 respectively 0.2% and 0.3% higher than in the winter forecast. The ECB in its March projections saw inflation at 5.3% and 2.9% respectively. In a model-based analysis published at its website, the ECB estimates that policy tightening lowered inflation by around 50 bps in 2022, while the downward impact on inflation is expected to average around 2 ppts over the period 2023-25. The transmission to economic activity is faster, with the impact on GDP growth expected to peak in 2023 and a downward impact of 2 percentage points on average over the period 2022-25. Both reports were interesting, but had little direct impact on trading. Yields maintained the gains from end last week after surveys in Europe (ECB) and the US (U. of Michigan) indicated higher than expected consumer inflation expectations. Early in US dealings, the US Empire manufacturing survey tumbled sharply from 10.8 to -31.8 (vs -3.8 expected). The release temporary aborted a tentative further rise in US (but also European) yields. Even so, the (negative) impact on yields after all remained limited. In an interview with CNBC, Fed’s Bostic repeated that he didn’t see a case for Fed rate cuts before well in 2024. In a slight steepening move, US yields are rising between 1.5 bp (2-y) and 4.25 bps (30-y). German yields also remain upwardly oriented rising between 2.0 bps (2-y) and 4.5 bps (30-y). Equities gradually lost opening gains early in US dealings and the disappointing Empire survey didn’t help. The Eurostoxx currently loses 0.25%. US indices open little changed/mixed.

On FX markets, the dollar lost some momentum after last week’s rebound. Also here the big miss in the NY Empire survey didn’t help. DXY currently trades near 102.45 (open near 102.67). EUR/USD tried a (for now unconvincing) rebound (1.0875 vs open near 1.085). Near 136, USD/JPY trades off the intraday top, but still holds in positive territory. UK yields are rising even less than in the US or EMU. Still, sterling outperforms (EUR/GBP 0.8695) as markets are counting down to tomorrow’s UK labour market data. News & Views

Headline Swedish CPI rose by 0.5% M/M and 10.5% Y/Y (from 10.6%). Rent increases for rental apartments and higher interest rate expenses for both owner occupied housing and tenant owned apartments were offset by lower food prices (-1.3% M/M) and lower electricity prices. These numbers were close to consensus, but core inflation gauges decelerated more than expected. The Riksbank’s preferred CPIF gauge (with fixed interest rate) rose 0.2% M/M (vs 0.5% expected) with the Y/Y-outcome slowing from 8% to 7.6%. Stripping out energy, CPIF rose by 0.4% M/M and 8.4% Y/Y. Today’s inflation figures suit the Swedish central bank that argued on April 26 to conduct one final 25 bps rate hike in either June or September. The Riksbank is convinced to see a steep decline in inflation in coming months. This doesn’t bode well for the national currency. The Swedish krone is a cause of concern for the central bank. It’s weakness is an additional inflation risk. With data now supporting the Riksbank scenario, SEK risks losing even more interest rate support against the euro. EUR/SEK rose from 11.25 to an intraday high of 11.32. The pair remains in a strong uptrend with the 2020 high (11.43) and YTD high (technical resistance) at 11.48 lining up.

Czech National Bank governor Michl said at a meeting with students at the Prague university of economics and business today that the CNB is considering whether to leave interest rates stable again or raise them at the June meeting in order for inflation to decline from current double digit levels to the 2% inflation target. Inflation is expected to dip to single digit levels from July. Michl affirmed that a strong currency is part of the CNB’s current playbook. He also reiterated that bets on a first CNB rate cut in Q3 are very premature. CZK lost some ground against majors last week as core bond yields corrected higher. EUR/CZK is testing the 23.60 upper bound of a narrow trading range in place since end March (23.20-23.60).

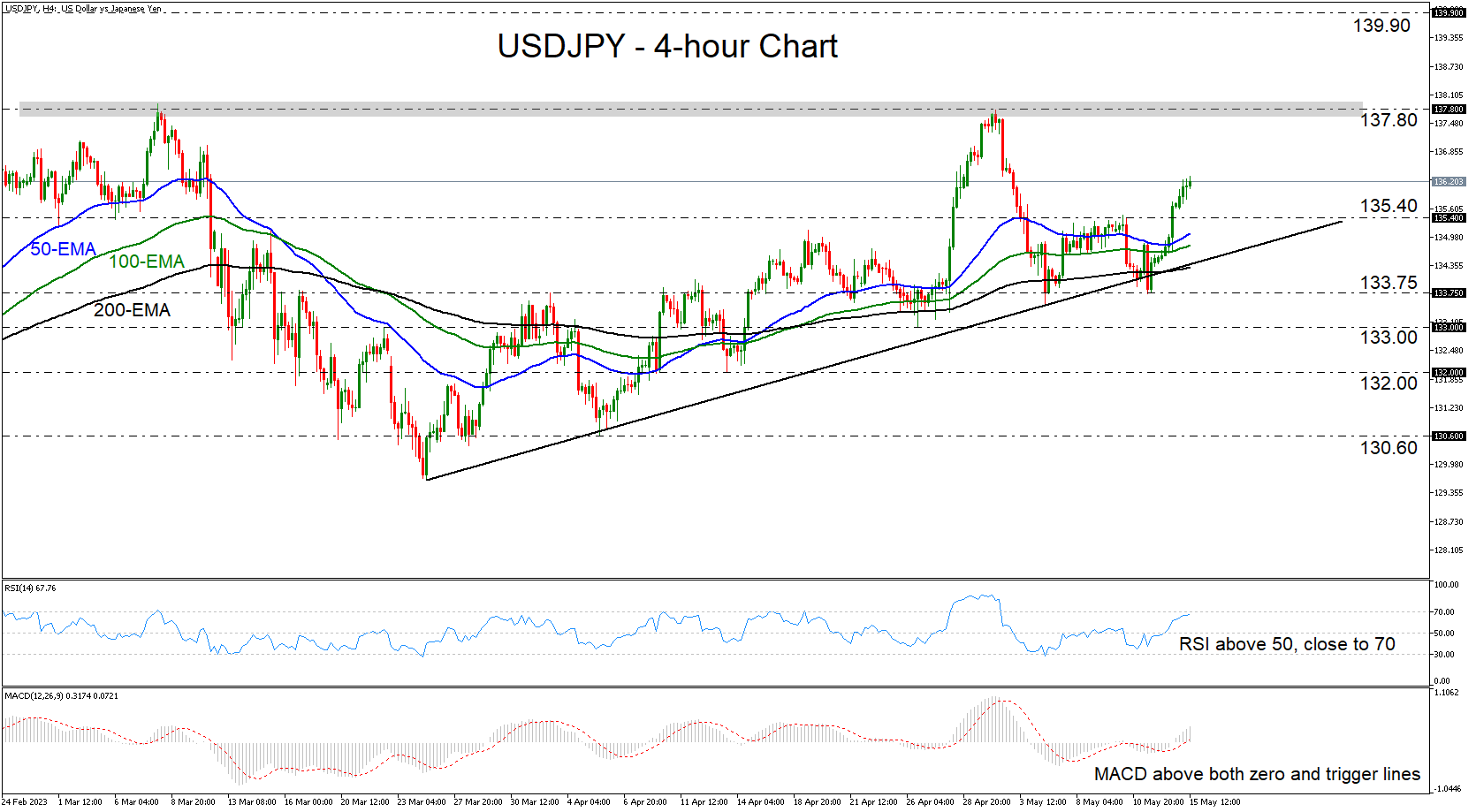

USDJPY Climbs Above Key Barrier of 135.40

USDJPY surged and broke above the key resistance barrier of 135.40 on Friday, after rebounding on Thursday from slightly below the uptrend line drawn from the low of March 24. Combined with the fact that the pair is also trading above all three of the plotted exponential moving averages (EMAs), this keeps the short-term picture positive.

The bullish outlook is also confirmed by the short-term oscillators, both of which are detecting upside momentum. The RSI is lying near its 70 line and is pointing up, while the MACD is running above both its zero and trigger lines, pointing north as well.

The break above the 135.30 barrier may have opened the door towards the next key hurdle of 137.80, which has been blocking the bulls since early December. If they are strong enough to pierce through that ceiling this time around, a higher high will be confirmed on bigger timeframes, and the upleg may extend towards the peak of November 30 at 139.90.

On the downside, the break that could signal a short-term reversal may be a dip below the 133.75 zone, which offered support last week. Such a move would also take the pair below the aforementioned uptrend line and perhaps initially aim for the low of April 26 at 133.00. If the bears are not willing to stop there, then a break lower may see scope for extensions towards the low of April 13 at 132.00.

To sum up, USDJPY has been in an uptrend since March 24, with the bulls now seem willing to aim once again for the key hurdle of 137.80. Nonetheless, a break above that barrier may be needed to signal a trend continuation on bigger timeframes.

Australian Dollar Stems Bleeding, RBA Minutes Eyed

- Australia to release RBA minutes and consumer sentiment

- US debt crisis pushes US yields and the US dollar higher

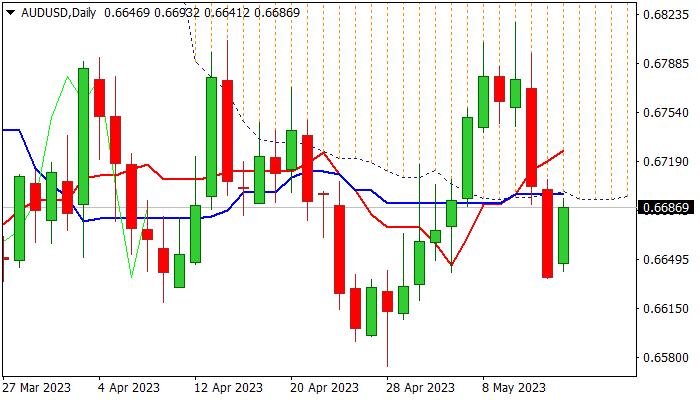

AUD/USD has rebounded on Monday, after a steep slide of 2% over the previous two sessions. The Australian dollar is trading at 0.6689, up 0.71% on the day.

Markets await RBA minutes

RBA minutes are often on the dull side, but Tuesday’s release could be an exception. The minutes will provide details about the meeting earlier this month when the RBA surprised the markets with a 25-basis point hike. Investors had expected a second straight pause, but instead, the RBA zig-zagged. Governor Lowe had to explain why the pause was so short, blaming the strong labour market and concerns over services and energy price inflation.

The danger for the RBA in catching the markets off guard with a rate move is damage to credibility. The minutes should provide some insights into the Bank’s decision to hike and investors will also be looking for hints about what to expect in the future from the RBA.

Australia will also release consumer confidence for May. The markets are bracing for a decline of 1.7% after a stellar gain in April of 9.4%.

In the US, the debt ceiling crisis is looming, with a deadline of June 1st. Lawmakers will have to find a solution, but in the meantime, the Republicans and Democrats are playing a game of who blinks first. The uncertainty has sent US Treasury yields higher, which gave the US dollar a sharp boost late last week against most of the majors and sent the Aussie plunging by 2%.

In the US, it’s a fairly quiet start to the week. The highlight is the Empire State Manufacturing Index for May, which is projected to come in at -3.7, following a 10.8 reading in April. We’ll also hear from three Fed members.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6699. This is followed by 0.6761

- 0.6579 and 0.6517 are providing support

UK Employment Might Be the Catalyst Needed for BOE

The UK is expected to get another bit of good economic news. But upbeat forecasts make it easier for a disappointment to appear and drag on the market. After a string of positive results that have failed to energize the pound over the last few trading days, investors might be hoping for some upside in cable from the jobs numbers to be released tomorrow.

One of the issues plaguing the pound is the seeming reluctance of the BOE to take a stronger position to bring down inflation. Other central banks have been hiking at 50 and even 75 bps at a time, while the BOE has been plodding along. The division in the vote is also weighing on confidence. Both the Fed and the ECB have managed clear, unanimous votes for their policies. If the vote division were to be resolved - or there was data to indicate a resolution was nearing - then investors might have more confidence in the BOE bringing inflation down.

Getting the house in order

The two dissenters have stressed that it's more important to boost the economy than to fight inflation. The latest GDP numbers might have done something to assuage those worries, since the UK managed to avoid a recession. Sure, 0.1% quarterly growth isn't much to celebrate, and the IMF still hasn't changed their forecast that the UK will be the only major country to post negative growth this year.

On the other hand, the government cut spending by 2.5% last quarter, and the economy still managed to stay in the green. That's significant because government spending represents 45% of the country's GDP. Which implies the UK private sector managed over 1.1% quarterly growth.

The jobs situation

That supports the positive labor situation, which will be reported next week. Private businesses are still hiring, and are expected to keep the unemployment rate at 3.8%. That's below what is seen as the structural level, which has the negative aspect of pressuring wages.

What the BOE is most interested in is the average earnings since that can translate into inflationary pressure. There the earnings are expected to decelerate a little to 5.7% compared to 5.9% prior. This is significantly below inflation levels, meaning that UK workers are seeing their purchasing power erode over time. Not good for the long-term projections of the economy. On the other hand, it means there is little risk of a wage-price spiral, which would make raising rates more urgent.

The good news

The consensus is that the claimant count will be a negative 15.0K compared to an increase of 28.2 in the prior reading. Remember that the lower this figure is, the better it is for the economy, because it represents the number of people seeking unemployment benefits.

Labor tightness implies that there is dynamism in the private economy. The problem is that the government is being forced to spend less as it has to make more payments in interest as the BOE hikes rates to bring down inflation. That slowing public growth weighs on GDP, making it difficult for the BOE to keep hiking without causing secondary effects. If the labor market continues to show resilience, however, it might finally convince the dissenters that bringing inflation down is possible without hurting the economy too much.

AUD/USD: Aussie Rebounds on Improved Risk Sentiment

Australian dollar regained traction after nearly 2% drop last Thu/Fri and bounced 0.6% in Asian/European trading on Monday.

Fresh recovery was driven by improved risk sentiment, which prompted traders to collect some profits after a sharp two-day fall.

Prospects for stronger recovery are not very bright as positive momentum is conflicting with moving averages still in bearish setup on daily chart, with the base of thick daily cloud, reinforced by daily Kijun-sen (0.6692) and Fibo 38.2% of 0.6818/0.6636 (0.6705), marking strong obstacles which threaten to stall recovery.

Near-term picture is not very clear, with initial bullish signal expected on break into daily cloud, and likely acceleration towards next pivot at 0.6727 (daily Tenkan-sen), violation of which would add to reversal signals.

Caution on failure at cloud base, which will weaken near-term structure and keep the downside vulnerable.

A number of Fed’s policymakers are due to speak in the afternoon and may influence pair’s performance.

Res: 0.6692; 0.6727; 0.6748; 0.6775.

Sup: 0.6631; 0.6607; 0.6573; 0.6563.

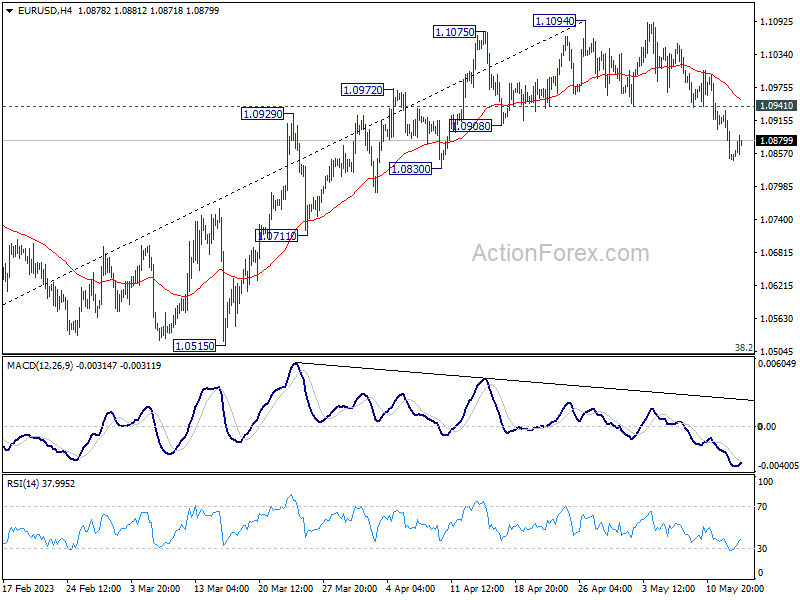

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0820; (P) 1.0878; (R1) 1.0907; More...

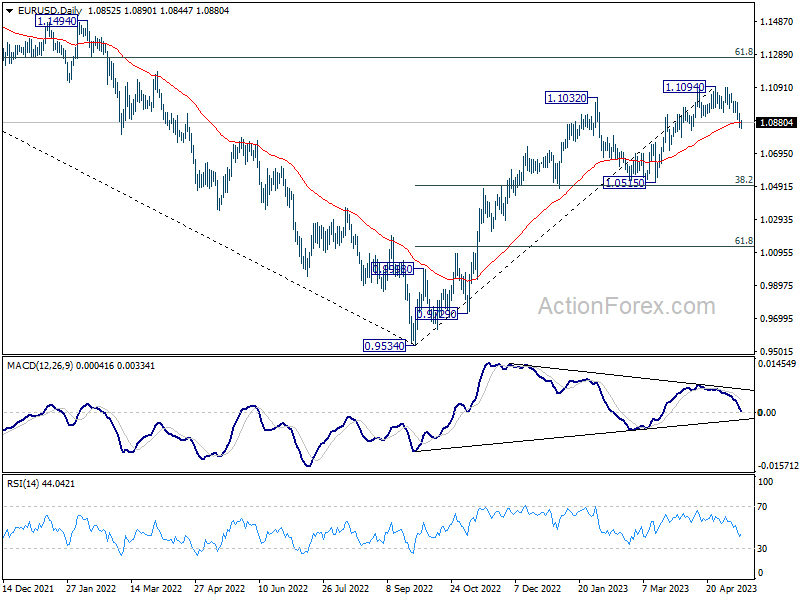

Intraday bias in EUR/USD remains on the downside despite today's mild recovery. Fall from 1.1094 short term top is seen as correcting whole up trend from 0.9534. Deeper decline would be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, though, above 1.0941 resistance will turn bias back to the upside for retesting 1.1094 high.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

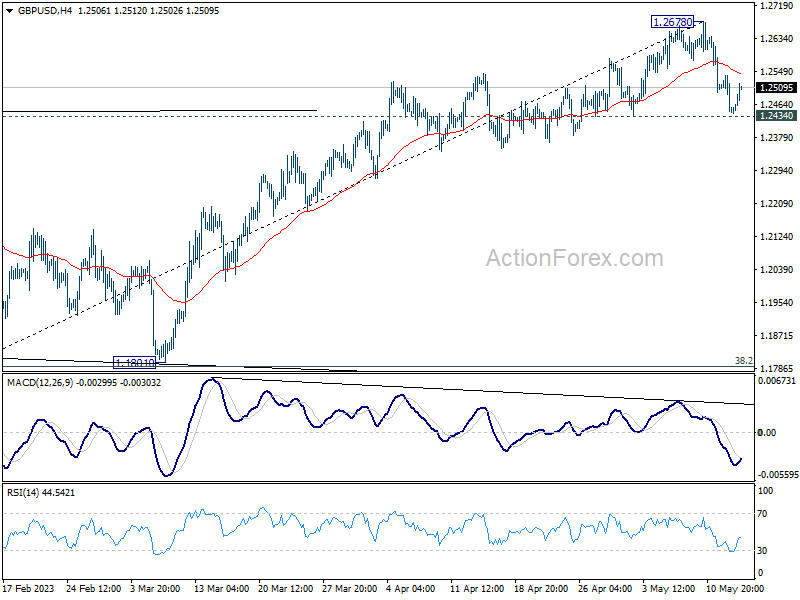

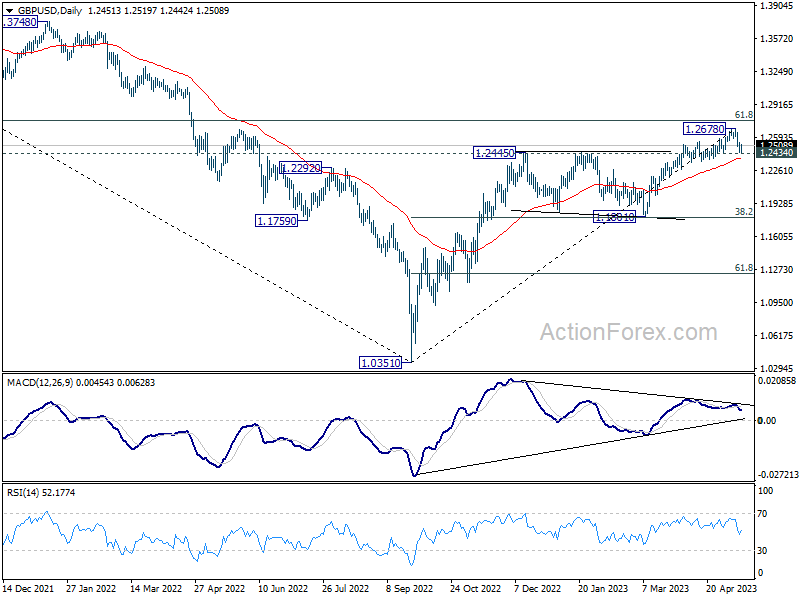

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2415; (P) 1.2478; (R1) 1.2511; More...

GBP/USD recovered ahead of 1.2434 support and intraday bias remains neutral for the moment. On the downside, firm break of 1.2434 will confirm short term topping at 1.2678, on bearish divergence condition in 4H MACD. Intraday bias will be back on the downside for 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789), as correction to whole up trend from 1.0351. On the upside, however, break of 1.2678 will resume larger up trend from 1.0351 instead.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

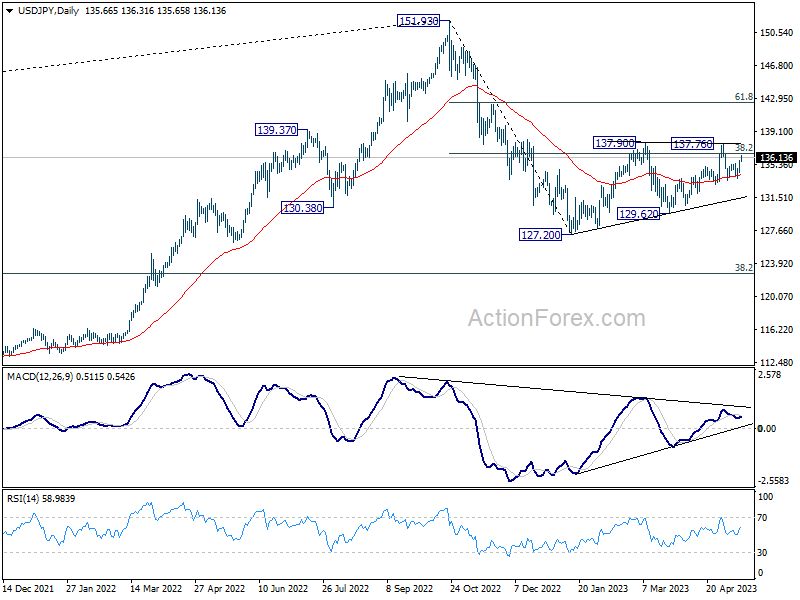

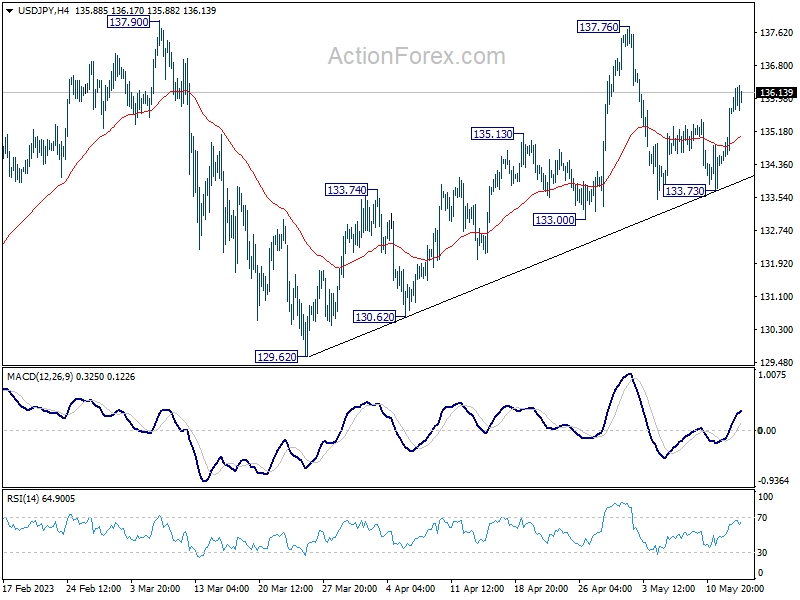

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 134.85; (P) 135.30; (R1) 136.20; More...

USD/JPY's rally from 133.73 is still in progress and intraday bias stays on the upside for retesting 137.76/90 resistance zone. Decisive break there will resume whole rebound from 127.20. On the downside, break of 133.73 will resume the fall from 137.76 through 133.00 instead.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rise to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.