Sample Category Title

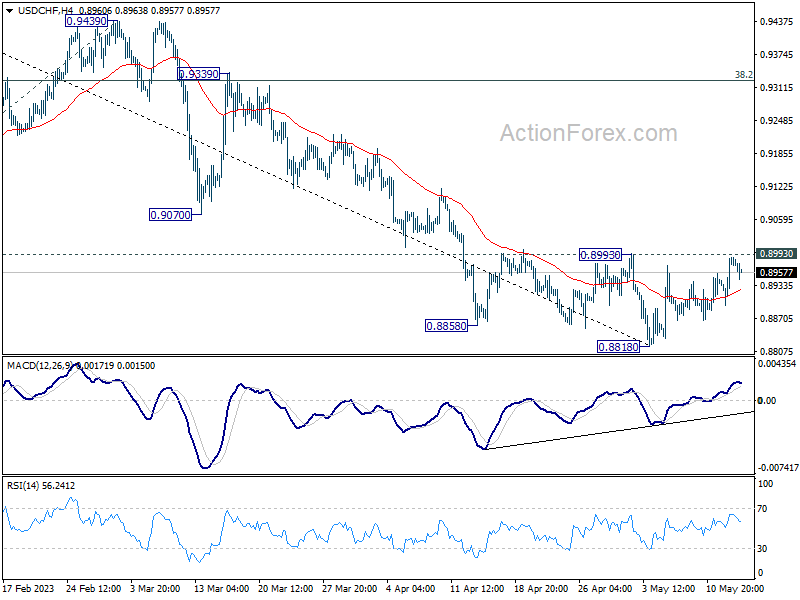

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8925; (P) 0.8956; (R1) 0.9016; More...

No change in USD/CHF's outlook and intraday bias stays neutral with immediate focus on on 0.8993 resistance. Decisive break there will confirm short term bottoming at 0.8818, on bullish convergence condition in 4H MACD. Intraday bias will be turned back to the upside for 55 D EMA (now at 0.9052) and possibly above. In case of another fall, strong support should be seen from 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support, to bring rebound.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

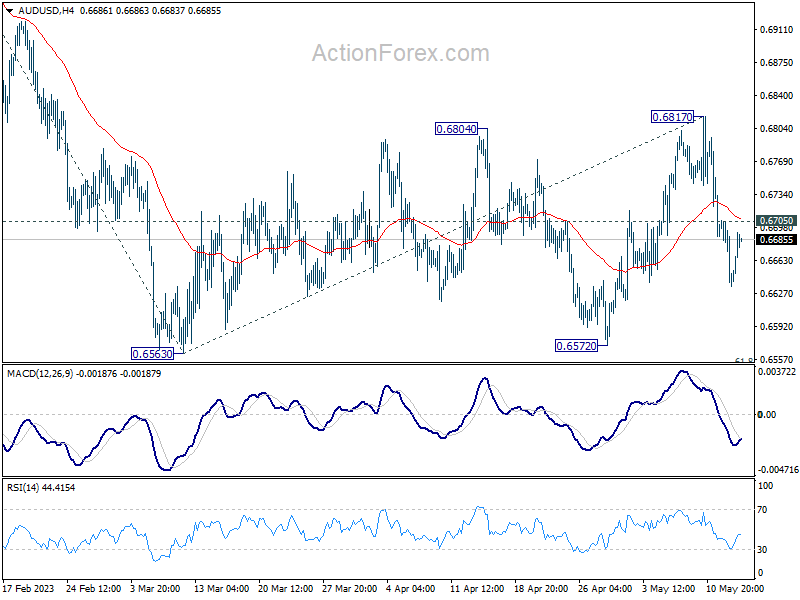

Market Sentiments Rebound on US Debt Ceiling Negotiation Optimism

Market sentiments show signs of revival today, appeared to be buoyed by optimism over a potential debt ceiling agreement between US Democrats and Republicans. Over the weekend, Treasury Secretary Janet Yellen delivered upbeat remarks, indicating that negotiations were in full swing and marked by "some areas of agreement."

This optimism has brought a ripple effect in the currency markets, with commodity currencies experiencing a rise, led by Australian Dollar, with British Pound in between. Japanese Yen is having a significant slump, trailed by Dollar, Euro, and Swiss Franc.

However, the durability of these risk rallies for the remainder of the week remains uncertain. From a currency market standpoint, a convincing break of 0.6705 minor resistance by AUD/USD would be needed to neutralize its near-term bearish stance. Absent such a breakthrough, risk of dipping to retest the 0.6563 low remains an imminent possibility, probably alongside another bearish turn in risks.

In Europe, at the time of writing, FTSE is up 0.29%. DAX is down -0.10%. CAC is down -0.01%. Germany 10-year yield is up 0.038 at 2.312. Earlier in Asia, Nikkei rose 0.81%. Hong Kong HSI rose 1.75%. China Shanghai SSE rose 1.17%. Singapore Strait Times rose 0.19%. Japan 10-year JGB yield rose 0.0191 to 0.408.

Fed's Bostic indicates bias towards further hikes, no cut until well into 2024

In an interview with CNBC, Atlanta Fed President Raphael Bostic emphasized the importance of combating inflation, which he deems as "job No. 1". He expressed his readiness to bear the cost necessary to achieve the Fed's target, underscoring the need for a more aggressive stance on rate hikes given the current economic scenario.

Bostic stated, "What we've seen is that inflation has been persistently high, consumers have been really resilient in terms of their spending, and labor markets remain extremely tight. All of those suggests that there's still going to be upward pressure on prices." His comments highlight the ongoing pressures that may trigger further inflationary spikes.

He showcased leaning towards a proactive approach in dealing with inflation, stating, "If there's going to be a bias to action, for me it would be a bias to increase a little further as opposed to cut."

Bostic remained confident in Fed's policy measures, asserting, "There's still a lot of confidence that our policies are going to be able to get inflation back down to our 2% target." He made clear Fed's determination to ensure this target is met, even if it means holding off on rate cuts until well into 2024.

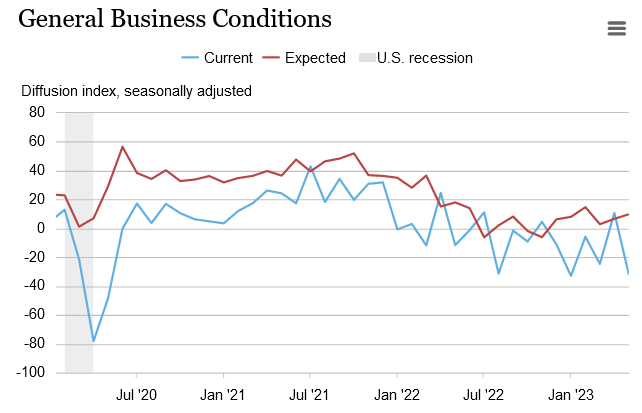

US Empire State business conditions index plunges, fueling recession fears

In a significant downturn, New York Fed Empire State Business Conditions Index plummeted to -31.8 in May, a drastic drop of -42.6 points from its April reading of 10.8. This disappointing figure significantly underperforms market expectations of -1.9, and any reading below zero signals deteriorating conditions.

This precipitous drop comes just a month after the index defied expectations with a 35.4 point surge to 10.8 in April. The recent plunge not only eradicates last month's gains but also heightens concerns about a potential recession.

In parallel with the overall index, new orders sub-index fell a whopping -53.1 points to -28 in May, effectively erasing the sharp 46.7 point increase seen in April. Additionally, shipments index witnessed a substantial decline, falling -40.3 points to -16.4, negating the 37.3 point gain from the previous month.

Interestingly, amid this overall downturn, the six-month expectations measure managed to tick up slightly, gaining 3.2 points to reach 9.8.

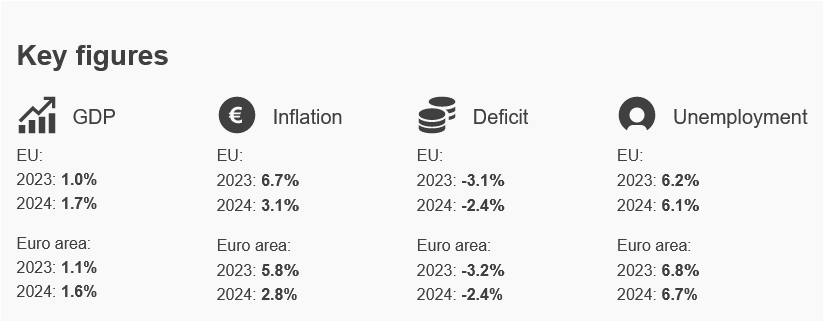

EU Spring Forecast: Upgraded GDP growth and inflation

In its Spring 2023 Economic Forecast, European Commission presented a cautiously optimistic outlook for the Eurozone, with GDP growth projections revised upwards to 1.1% and 1.6% for 2023 and 2024 respectively. This positive adjustment, credited to a stronger-than-expected start to the year, exceeds winter forecasts of 0.9% in 2023 and 1.5% in 2024.

However, the report did not shy away from the challenges posed by inflation. Persisting core price pressures have led the Commission to revise its inflation forecasts for Eurozone to 5.8% in 2023 and 2.8% in 2024, up from winter's projected 5.6% and 2.5% respectively. On an annual basis, core inflation is set to average 6.1% in 2023 before falling to 3.2% in 2024, remaining above headline inflation in both forecast years.

While the overall picture painted by the Commission is one of steady recovery, it also acknowledges increase in downside risks to economic outlook. The report warned that persistent core inflation could continue to squeeze household purchasing power and necessitate stronger response from monetary policy, leading to wider macro-financial implications.

Potential threats also include renewed financial stress, which could trigger tightening of lending standards, and exacerbation of inflation by expansionary fiscal policies.

The forecast also flagged the ongoing turmoil in the banking sector and broader geopolitical tensions as possible sources of further economic challenges. On the other hand, the Commission noted that more favorable developments in energy prices could lead to a faster decline in headline inflation, boosting domestic demand.

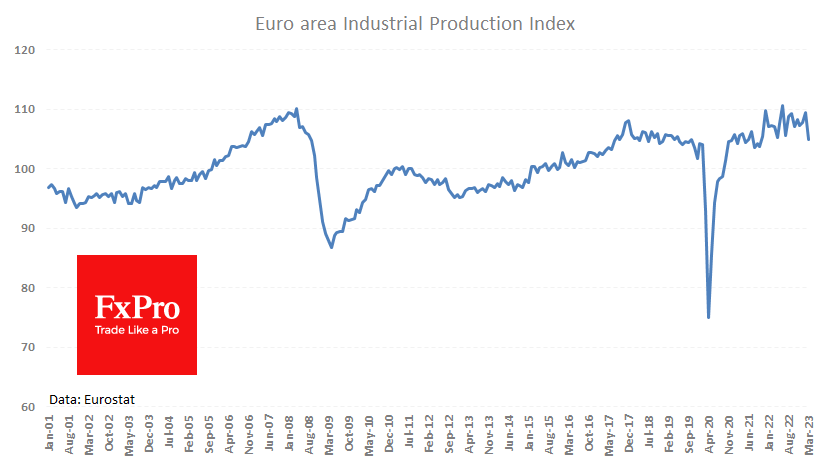

Eurozone industrial production down -4.1% mom in Mar

Eurozone industrial production contracted -4.1% mom in March, much worse than expectation of -1.2% mom. Production of capital goods fell by -15.4% mom, intermediate goods by -1.8% mom, energy by -0.9% mom and non-durable consumer goods by -0.8% mom, while production of durable consumer goods rose by 2.8% mom.

EU industrial production declined -3.6% mom. Among Member States for which data are available, the largest monthly decreases were registered in Ireland (-26.3%), Sweden (-3.9%) and Germany (-3.1%). The highest increases were observed in Finland (+3.0%), Slovenia (+2.3%), Czechia and Slovakia (both +1.7%).

Japan cabinet office stresses importance of avoiding relapse into deflation

Japan's Cabinet Office emphasized, at a meeting of the government's economic council, the need for stability and sustainability in these positive signs to ensure that Japan does not fall back into a deflationary spiral. They stated, "While there have been some positive signs in recent data, we must ensure they are stable and sustainable so that Japan won't revert to deflation."

In a separate discussion involving academics and private-sector experts, some participants called for BoJ to end quantitative easing once inflation stabilizes around its 2% target. Meanwhile, some participants suggested BoJ should mull over altering its extraordinary stimulus measures if inflation and wages continue their upward trajectory.

Prime Minister Fumio Kishida emphasized the need for a coordinated approach between the government and the BoJ amidst the growing uncertainty surrounding the economic outlook. He said, "We're aiming to pull Japan out of deflation and achieve sustained, private demand-driven economic growth" by influencing public perceptions that growth and inflation will continue to rise.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8925; (P) 0.8956; (R1) 0.9016; More...

No change in USD/CHF's outlook and intraday bias stays neutral with immediate focus on on 0.8993 resistance. Decisive break there will confirm short term bottoming at 0.8818, on bullish convergence condition in 4H MACD. Intraday bias will be turned back to the upside for 55 D EMA (now at 0.9052) and possibly above. In case of another fall, strong support should be seen from 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support, to bring rebound.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Apr | 49.8 | 54.4 | 53.8 | |

| 23:50 | JPY | PPI Y/Y Apr | 5.80% | 5.60% | 7.20% | 7.40% |

| 06:30 | CHF | Producer and Import Prices M/M Apr | 0.20% | -0.10% | 0.20% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Apr | 1.00% | 1.10% | 2.10% | |

| 09:00 | EUR | EU Economic Forecasts | ||||

| 09:00 | EUR | Eurozone Industrial Production M/M Mar | -4.10% | -1.20% | 1.50% | |

| 12:15 | CAD | Housing Starts Y/Y Apr | 262K | 221K | 214K | |

| 12:30 | USD | Empire State Manufacturing Index May | -31.8 | -1.9 | 10.8 |

US Empire State business conditions index plunges, fueling recession fears

In a significant downturn, New York Fed Empire State Business Conditions Index plummeted to -31.8 in May, a drastic drop of -42.6 points from its April reading of 10.8. This disappointing figure significantly underperforms market expectations of -1.9, and any reading below zero signals deteriorating conditions.

This precipitous drop comes just a month after the index defied expectations with a 35.4 point surge to 10.8 in April. The recent plunge not only eradicates last month's gains but also heightens concerns about a potential recession.

In parallel with the overall index, new orders sub-index fell a whopping -53.1 points to -28 in May, effectively erasing the sharp 46.7 point increase seen in April. Additionally, shipments index witnessed a substantial decline, falling -40.3 points to -16.4, negating the 37.3 point gain from the previous month.

Interestingly, amid this overall downturn, the six-month expectations measure managed to tick up slightly, gaining 3.2 points to reach 9.8.

Fed’s Bostic indicates bias towards further hikes, no cut until well into 2024

In an interview with CNBC, Atlanta Fed President Raphael Bostic emphasized the importance of combating inflation, which he deems as "job No. 1". He expressed his readiness to bear the cost necessary to achieve the Fed's target, underscoring the need for a more aggressive stance on rate hikes given the current economic scenario.

Bostic stated, "What we've seen is that inflation has been persistently high, consumers have been really resilient in terms of their spending, and labor markets remain extremely tight. All of those suggests that there's still going to be upward pressure on prices." His comments highlight the ongoing pressures that may trigger further inflationary spikes.

He showcased leaning towards a proactive approach in dealing with inflation, stating, "If there's going to be a bias to action, for me it would be a bias to increase a little further as opposed to cut."

Bostic remained confident in Fed's policy measures, asserting, "There's still a lot of confidence that our policies are going to be able to get inflation back down to our 2% target." He made clear Fed's determination to ensure this target is met, even if it means holding off on rate cuts until well into 2024.

Eurozone Industrial Production Falls to the Lowest Since October 2021

Eurostat today reported that eurozone industrial production fell by 4.1% in March, the most significant drop since July last year. Compared with the same month of the previous year, output fell by 1.4%, instead of the expected +0.9%, whereas, in February, it was up +2.0%.

The seasonally adjusted industrial production index fell to its lowest level since October 2021, failing to stick to a steady growth path and reversing down from roughly the same level it has been at since 2008. The following manufacturing report promises to be quite interesting, as it will help determine whether we see a reversal to decline, as we did in 2008 and 2018, or just a tactical retreat.

In a separate publication, German wholesale prices fell by 0.4% m/m, against expectations for a rise of 0.3%. Year-on-year, the decline is 0.5%. Import prices are also in negative territory year-on-year, which should contribute to a fall in consumer inflation.

Trends in industrial production are often ahead of the economy and determine long-term trends and the performance of the euro against the major currencies. However, they rarely cause an immediate market reaction immediately after publication.

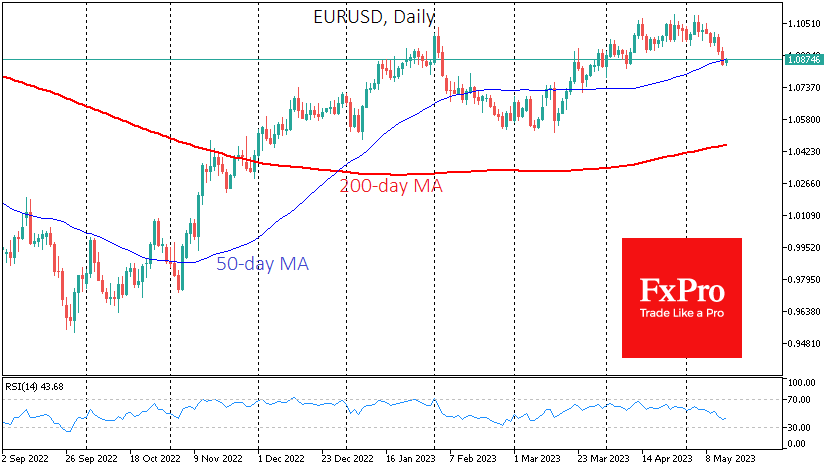

The single currency suffered short-term losses due to weak industrial production data and falling wholesale prices in Germany. This publication did not disrupt the EURUSD’s overall intraday trend, with buying interest increasing as the pair touched its 50-day moving average near 1.0850.

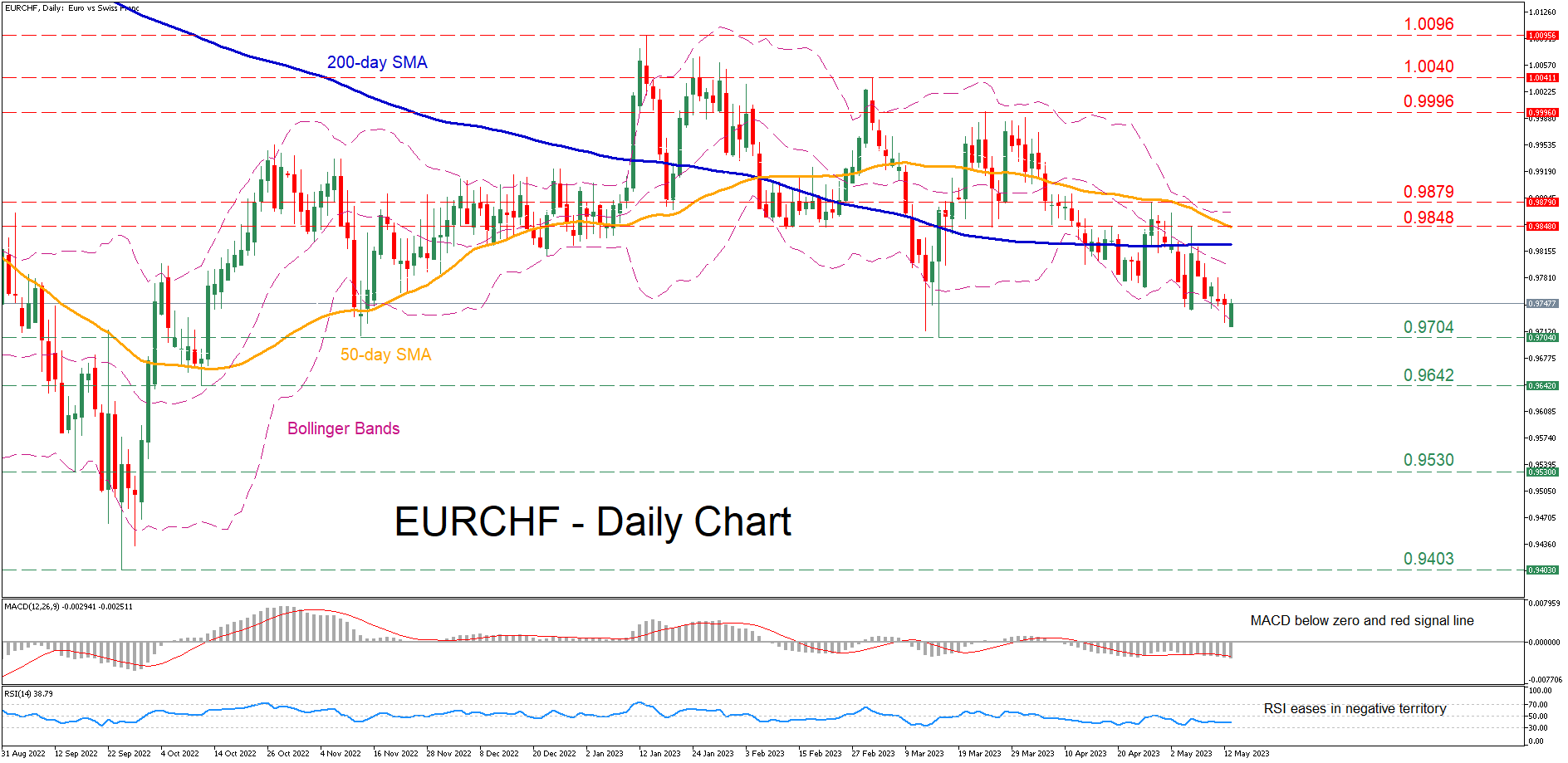

EURCHF Extends Decline Near 2023 Lows

EURCHF has been trending lower since its latest rebound got rejected just shy of the parity level in late March. In addition, the price retreated below both its 50- and 200-day simple moving averages (SMAs), which are set to post a bearish cross, painting an even gloomier technical picture for the pair.

The short-term oscillators currently suggest that bearish forces are reigning supreme. Specifically, the MACD dropped below its red signal line in the negative territory, while the RSI is flatlining beneath its 50-neutral mark.

Should the recent downtrend resume, the price could be on track to challenge the 2023 bottom of 0.9704. Breaking below that zone, the pair might descend to levels not seen in months, where the October support of 0.9642 may provide downside protection. If that barricade fails, the spotlight could turn to the 0.9530 hurdle.

On the flipside, bullish actions could propel the price towards 0.9848, which served as both resistance and support in the past, and overlaps with the 50-day SMA. Conquering this obstacle, the price could ascend towards the April resistance of 0.989 before 0.9996 comes under examination. Further advances might then stall around the February peak of 1.0040.

Overall, EURCHF seems to be extending its structure of lower highs and lower lows, getting ready to test its 2023 bottom. However, the price is currently below its lower Bollinger band, indicating that the market could have reached oversold conditions and hinting at a potential upside correction.

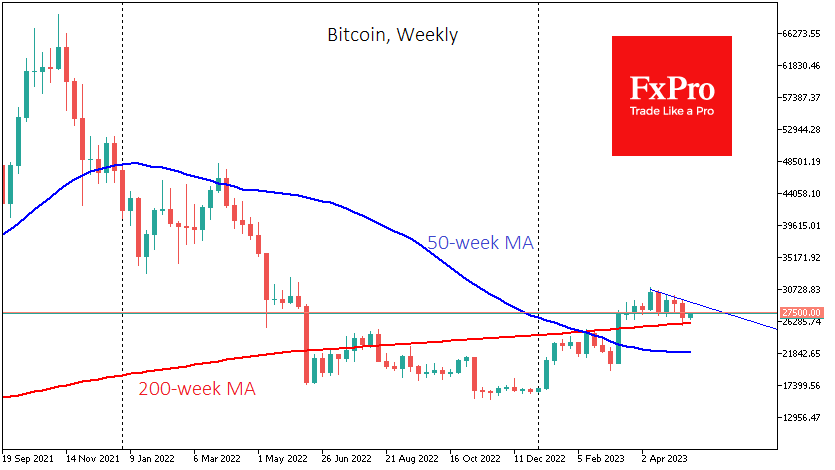

Bitcoin Attracts Buyers on the Dip to 200-Week MA

Market picture

Bitcoin fell 6.9% last week to close at $26,900, while Ethereum lost 6.2% to $1800. Top-10 leading altcoins lost between 3.1% (Cardano) and 12.2% (Polygon).

The total capitalisation of the crypto market fell by 5.5% over the week to $1.13 trillion, according to CoinMarketCap. One of the main reasons was issues at Binance, where BTC withdrawals were suspended twice.

Bitcoin proved interesting for sellers as it touched the 200-week average, passing close to $26,000 last Friday. By defending this key average, the bulls have convinced the market of the sustainability of the long-term bullish trend. On Saturday and Sunday, the Bulls defended the $26.8K level. On Monday, investors switched to active buying and pushed the price to $27.5K. However, cautious buyers will likely want to see a $28-28.5K takedown as confirmation of the break of last month’s downtrend.

The Ethereum core network experienced two massive outages that prevented transactions from being completed for some time. Blocks were created, and transactions were completed but could be altered. The developers of the Ethereum client Prysm released an emergency update.

News background

CryptoQuant believes that institutional investors will start buying Bitcoin in late 2023 when the Fed starts to cut interest rates.

MicroStrategy founder Michael Saylor described Bitcoin as a solution to growing financial problems and a tool that gives hope to eight billion people to hold their savings. According to him, BTC is a commodity of necessity and traditional money in its current form is already “dying”.

The US Chamber of Commerce issued a brief report on the case of trading platform Coinbase and the US Securities and Exchange Commission (SEC), criticising the agency for illegal actions against cryptocurrencies.

The European Banking Authority (EBA) believes central banks should ban large stablecoins if they threaten certain countries’ monetary policies. EU lawmakers plan to require companies involved in digital asset storage, trading, and investment to report their clients’ balance sheets to tax authorities.

DJIA Technical: Capped Below the 20-day Moving Average

- Since its 1 December 2022 high, the Dow Jones Industrial Average has evolved into a major “Expanding Wedge” range configuration.

- In the short-term, no clear signs of upside momentum as its price actions are being capped below the 20-day moving average.

- Key short-term resistance to watch will be at 33,580.

The Dow Jones Industrial Average (DJIA) is one of the underperforming major US stock indices together with the Russell 2000 so far with a recent weekly loss of -1.11% for the week of 8 May and a 2023 year-to-date return of 0.46% against the Nasdaq 100 (+0.61%/21.94%) and S&P 500 (-0.29%/7.41%).

DJIA Technical Analysis – Potential short-term weakness below 33,580 key resistance

Fig 1: DJIA trend as of 15 May 2023 (Source: TradingView, click to enlarge chart)

Since its 1 December 2022 high of 34,628, the US Wall St 30 Index (proxy of the Dow Jones Industrial Average futures) has started to evolve into a major “Expanding Wedge” range configuration as depicted on the daily chart.

An important point to note is that the Dow Jones Industrial Average is one of the underperforming major US stock indices together with the Russell 2000 so far with a recent weekly loss of -1.11% for the week of 8 May and a 2023 year-to-date return of 0.46% against the Nasdaq 100 (+0.61%/21.94%) and S&P 500 (-0.29%/7.41%).

On a shorter-term frame, using the 1-hour chart, the Index has so far failed to make any headways above its slightly downward-sloping 20-day moving average now acting as a resistance at around 33,580 since the recent break below it on 2 May 2023. In addition, the 1-hour RSI oscillator has remained below a corresponding descending resistance at around the 56% level.

These observations suggest a potential build-up in short-term downside momentum. A break below minor support at 33,100 may expose the 4 May 2023 swing low area at 32,950. On the other hand, a clearance with an hourly close above the 33,580 key short-term pivotal resistance negates the bearish tone to see the next resistance coming in at 33,750 (minor swing high areas of 3 May/8 May/10 May 2023).

New Zealand Dollar Rebounds after Sharp Losses

- New Zealand dollar rebounds after sharp losses on Friday

- New Zealand Services Index contracts

- US consumer confidence slips, inflation expectations rise

The New Zealand dollar has started the week with strong gains. NZD/USD is trading at 0.6218, up 0.46% on the day. This follows a huge decline of 1.7% on Friday, its worst one-day showing since February.

New Zealand services PMI contracts

New Zealand’s services sector has enjoyed prolonged growth, with the Services index posting 13 straight readings above 50.0, which indicates expansion. The streak ended today, as the Services index dropped from a downwardly revised 54.8 to 49.8 points. With manufacturing struggling, the services sector has been a key driver of economic growth.

The weak Services PMI follows a soft Inflation Expectations release on Friday, which eased in Q1 to 2.79%, down from 3.30% in Q4 of 2022. This marked a second straight deceleration and the first time inflation expectations have fallen below 3% in six months. These are further indications that the New Zealand economy is showing signs of slowing, which could result in the Reserve Bank of New Zealand easing on the pace of rate hikes. The central bank delivered an oversize 50-basis points hike at its April meeting but could trim that to a 25-bp increase at the May 24th meeting.

The US wrapped the week with weak data. UoM Consumer Sentiment slipped to 57.7 in May, down from 63.5 and below the market consensus of 6.30 points. Consumers also see prices rising at 3.2% over the next 5-10 years, which marked a 12-year high. The data points to a sour consumer, who is losing confidence in the economy and is worried about inflation. There are no signs of recession, but a weakening in consumer confidence is an alarm bell about the health of the US economy.

On the economic calendar, the US releases the NY Empire State Manufacturing Index, which the market bracing for a -2.5 reading in May after rising 10.8 points in April.

NZD/USD Technical

- There is resistance at 0.6252 and 0.6332

- 0.6120 and 0.6049 are providing support

EU Spring Forecast: Upgraded GDP growth and inflation

In its Spring 2023 Economic Forecast, European Commission presented a cautiously optimistic outlook for the Eurozone, with GDP growth projections revised upwards to 1.1% and 1.6% for 2023 and 2024 respectively. This positive adjustment, credited to a stronger-than-expected start to the year, exceeds winter forecasts of 0.9% in 2023 and 1.5% in 2024.

However, the report did not shy away from the challenges posed by inflation. Persisting core price pressures have led the Commission to revise its inflation forecasts for Eurozone to 5.8% in 2023 and 2.8% in 2024, up from winter's projected 5.6% and 2.5% respectively. On an annual basis, core inflation is set to average 6.1% in 2023 before falling to 3.2% in 2024, remaining above headline inflation in both forecast years.

While the overall picture painted by the Commission is one of steady recovery, it also acknowledges increase in downside risks to economic outlook. The report warned that persistent core inflation could continue to squeeze household purchasing power and necessitate stronger response from monetary policy, leading to wider macro-financial implications.

Potential threats also include renewed financial stress, which could trigger tightening of lending standards, and exacerbation of inflation by expansionary fiscal policies.

The forecast also flagged the ongoing turmoil in the banking sector and broader geopolitical tensions as possible sources of further economic challenges. On the other hand, the Commission noted that more favorable developments in energy prices could lead to a faster decline in headline inflation, boosting domestic demand.