Sample Category Title

Australian Dollar Tumbles on Weak Consumer Sentiment and China Data

Australian Dollar took a dive in today's Asian trading session, reeling from a sharp decline in consumer sentiment and a slew of weaker-than-anticipated economic data from China. Despite the headwinds facing Aussie, New Zealand Dollar held its ground, buoyed by Westpac's predictions of continued monetary tightening by RBNZ from the present 5.25% to 6.00% in the coming months.

Meanwhile, Canadian Dollar, like its Australian counterpart, is on a downward trajectory as the second weakest performer of the day so far. Dollar trails close behind, undermined by uncertainty surrounding debt ceiling negotiations. Conversely, Japanese Yen is riding high, closely following Kiwi as the day's second strongest currency, with Euro and Swiss Franc not far behind. British Pound is demonstrating mixed performance as it anticipates job data from the UK.

Technically, AUD/NZD's recovery from 1.0600 might have hit a ceiling at 55 D EMA. Risk is mildly back on the downside for now. Firm break of 1.0600 support should resume the decline from 1.1085 through 1.0585 towards 1.0469 low. Nevertheless, another rise would likely push AUD/NZD through 55 D MA (now at 1.0760) to 1.0928 resistance instead.

Overnight, DOW rose 0.14%. S&P 500 rose 0.30%. NASDAQ rose 0.66%. In Asia, at the time of writing, Nikkei is up 0.84%, continuing its march to 30k handle. Hong Kong HSI is up 0.39%. China Shanghai SSE is up 0.01%. Singapore Strait Times is down -0.05%.

Fed's Barkin questions "whether we need to do more"

Richmond Fed President Thomas said yesterday that he is unconvinced that inflation will taper off rapidly with only a marginal economic slowdown. Barkin stated, "You could tell yourself a story where inflation comes down relatively quickly ... with only a modest economic slowdown."

He quickly added, "But I'm not yet convinced ... I do wonder whether we're not going to need more impact on demand to bring inflation down to where we need to go."

Barkin stayed open-minded about Fed's policy direction at the upcoming June 13-14 meeting. Despite having raised the policy rate by 5 percentage points since March 2022, Barkin isn't ruling out the possibility of another hike.

In terms of the labor market, Barkin noted the shift from what he described as "red hot" to merely "hot." He asserted, "On the unemployment side, I think you could fairly say it's moved from red hot to hot, right? There's nothing about 3.4% unemployment that feels ... cool."

Despite the gradual effects of rate hikes beginning to show, Barkin emphasized that the job market remains robust and inflation persistent. He admitted, "I'm still seeing data that suggests a hot job market and enduring inflation," leading him to believe inflation could persist longer than market measures suggest. Therefore, he concluded, "I'm still looking to ask myself the question whether we need to do more."

Separately, Minneapolis Fed President Neel Kashkari said the central bank probably has "more work to do on our end, to try to bring inflation back down," adding that "we should not be fooled by a few months of positive data."

BoE Pill: Self-sustaining, second-round-effect momentum could keep inflation high

BoE Chief Economist, Huw Pill, voiced his concern about the enduring momentum of inflation in the UK during an online event yesterday. Pill warned of the risk of a self-sustaining inflation cycle, where despite the dissipation of key short-term inflation drivers like rising energy and food costs, businesses and workers would continue to seek substantial price and wage increases.

He said, "The risk is ... that self-sustaining, second-round-effect momentum within the UK economy keeps inflation running at above-target levels."

This trend could still align with a significant drop in headline inflation, Pill noted, but he expressed concern that headline inflation could stagnate at around 4% or 5% over the next two to three years.

"That's still compatible with quite a big fall in headline inflation, but maybe headline inflation - other things equal - getting stuck at that 4%, 5% level over the next two or three years," he clarified.

Meanwhile, Pill also highlighted the potential of AI to increase productivity and, subsequently, living standards. He emphasized, "Using AI to make ourselves more productive is one example of how we can do that to boost living standards. This is a win-win if we all get better off because we're all more productive."

RBA Minutes: Further hikes may still be required

Minutes of RBA's May meeting revealed a detailed discussion where Board members weighed the pros and cons of keeping cash rate unchanged or increasing it by 25 basis points. Despite the fine balance of arguments, the Board saw it fit to raise the interest rates by 25bps to 3.85%, due to upside risks in inflation and tight labour market.

Data available in the month leading up to the meeting confirmed significant inflationary pressures and highlighted upside risks to the inflation outlook. The Board was concerned that if these risks materialised, it would "further delay the return of inflation to target levels" and potentially trigger a "damaging shift in inflation expectations".

While acknowledging considerable uncertainties surrounding the economic outlook, particularly with respect to household consumption, the Board's strong commitment to price stability and the necessity of anchoring inflation expectations tipped the scales in favour of a rate hike.

Looking forward, the Board indicated that "further increases in interest rates may still be required", depending on the evolution of the economy and inflation.

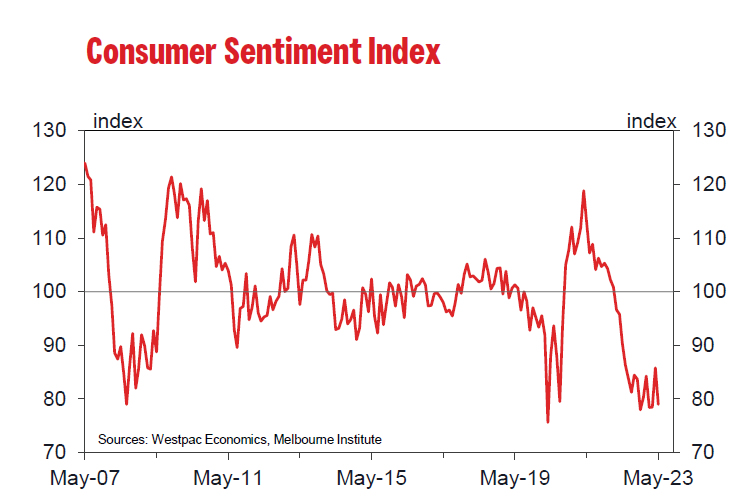

Australian consumer sentiment plunges in May following unexpected RBA rate hike

Australia Westpac Consumer Sentiment Index dropping sharpy by -7.9% from 85.8 to 79.0 in May. This decline brings the index close to the grim levels observed in March, which were the lowest since COVID-19 outbreak in 2020 and, prior to that, since the severe recession of early 1990s.

The unexpected decision by RBA to raise the cash rate by an additional 0.25% in May, as well as the Federal Budget, were cited by Westpac as the two main factors impacting consumer sentiment over the last month.

Westpac stated, "Interest rates were again a key driver of the May survey. The RBA raised the official cash rate by a further 0.25% at its May meeting in the week before the survey. The move came as a major surprise to markets and most commentators, clearly stoking consumer fears of more increases to come."

Looking ahead, Westpac predicts that RBA will likely pause in June, awaiting further data on inflation and the state of the economy. While the bank's central view anticipates the current cash rate will remain at its peak due to economic weakness and clear progress toward the Board's inflation target, it acknowledges that the risks are still "evenly balanced".

China's industrial production, retail sales miss expectations; youth unemployment hits record high

China's industrial production growth fell short of expectations in April, with a year-on-year increase of 5.6% yoy, significantly under expectation of 10.1% growth. Despite missing the mark, the growth rate outpaced March's 3.9% yoy rise and marked the fastest expansion since September 2022.

Retail sales also grew less than expected, posting 18.4% yoy rise, which fell short of anticipated 20.1% yoy growth. The figure was largely inflated due to a low comparison base, as retail sales plummeted by -11.1% yoy in April of the previous year due to severe lockdowns. On a monthly basis, retail sales contracted by -7.8% mom from March.

Fixed asset investment growth also came in below expectations 4.7% ytd yoy growth, underperforming expectation of 5.2%.

Urban jobless rate ticked down from 5.3% to 5.2%. However, unemployment among 16-24 age group spiked to a record high of 20.4%, up from 19.6% in the previous month. This exceeded the previous record of 19.9% set in July 2022.

The National Bureau of Statistics (NBS) stated, "In general, in April, the national economy continued to recover, and positive factors accumulated and increased. But we must also see that the international environment is still complex and severe, domestic demand is still insufficient, and the endogenous driving force for economic recovery is not yet strong."

Looking ahead

UK emplyment and Germany ZEW economic sentiment are the main focus in European session. Eurozonne will also release Q1 GDP revision and trade balance. Later in the day, Canada CPi will take center stage with US retail sales.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6658; (P) 0.6684; (R1) 0.6725; More...

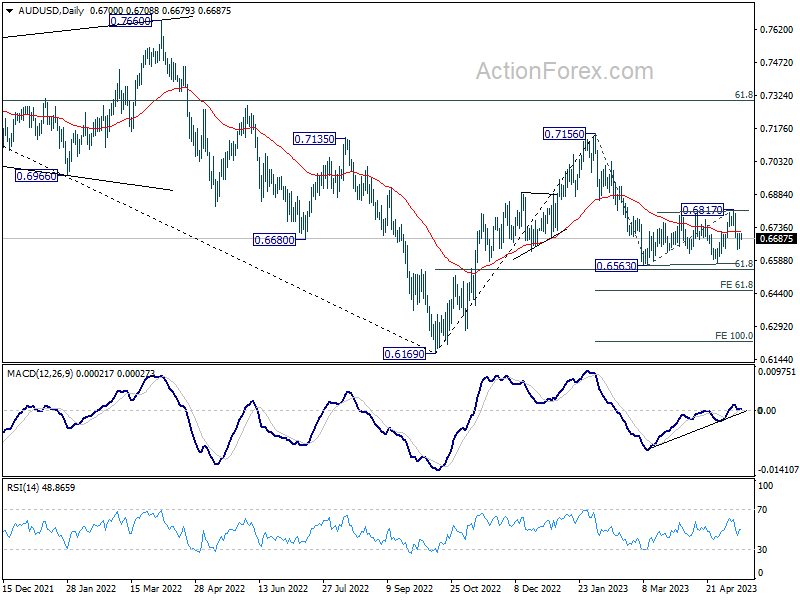

Intraday bias in AUD/USD is turned neutral first with current recovery. But risk will stay on the downside as long as 0.6817 resistance holds. Consolidation pattern from 0.6563 could have completed with three waves to 0.6817. Below 0.6635 will bring retest of 0.6563 low first. Decisive break there will resume larger decline from 0.7156 to 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451.

In the bigger picture, the failure to break through 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Firm break of 61.8% retracement of 0.6169 to 0.7156 at 0.6546 will raise the chance of long term down trend resumption through 0.6169 low. This will now be the favored case as long as 0.6817 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 02:00 | CNY | Industrial Production Y/Y Apr | 5.60% | 10.10% | 3.90% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Apr | 4.70% | 5.20% | 5.10% | |

| 02:00 | CNY | Retail Sales Y/Y Apr | 18.40% | 20.10% | 10.60% | |

| 06:00 | GBP | Claimant Count Change Apr | 31.2K | 28.2K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Mar | 3.80% | 3.80% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Mar | 5.10% | 5.90% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Mar | 6.80% | 6.60% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | 5.6B | -0.1B | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.10% | 0.10% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment May | -5 | 4.1 | ||

| 09:00 | EUR | Germany ZEW Current Situation May | -35.3 | -32.5 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | 2.3 | 6.4 | ||

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 P | 0.30% | 0.30% | ||

| 12:30 | CAD | Manufacturing Sales M/M Mar | 0.70% | -3.60% | ||

| 12:30 | CAD | CPI M/M Apr | 0.50% | 0.50% | ||

| 12:30 | CAD | CPI Y/Y Apr | 4.10% | 4.30% | ||

| 12:30 | CAD | CPI Median Y/Y Apr | 4.30% | 4.60% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Apr | 4.10% | 4.40% | ||

| 12:30 | CAD | CPI Common Y/Y Apr | 5.50% | 5.90% | ||

| 12:30 | USD | Retail Sales M/M Apr | 0.80% | -0.60% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Apr | 0.50% | -0.40% | ||

| 13:15 | USD | Industrial Production M/M Apr | 0.00% | 0.40% | ||

| 13:15 | USD | Capacity Utilization Apr | 79.70% | 79.80% | ||

| 14:00 | USD | Business Inventories Mar | 0.10% | 0.20% | ||

| 14:00 | USD | NAHB Housing Market Index May | 45 | 45 |

Technical Outlook and Review

DXY:

The Dollar Index (DXY) is currently observing a significant bullish momentum, suggesting a potential continued upward movement. The bullish tendency could potentially lead the price to bounce off the first support and head towards the first resistance.

Our first support stands at 102.24. This key level serves as a pullback support, indicating a strong potential for price stability. Additionally, it aligns with a 23.6% Fibonacci retracement, further suggesting the robustness of this support level.

If the price manages to rebound from the first support, it could potentially rise towards the first resistance level, which is situated at 102.79. This level is a swing high resistance, suggesting it could be a significant barrier to further price increases.

However, should the price fail to maintain above the first support, our second support at 101.83 could come into play. This level also serves as a pullback support. Additionally, it is a point of Fibonacci confluence, coinciding with both a 61.8% Fibonacci projection and a 50% Fibonacci retracement, making it a crucial level to monitor.

Looking beyond the first resistance, our second resistance stands at 103.04. This level, a swing high resistance, coincides with a 145% Fibonacci extension, indicating it could be a significant hurdle for bullish momentum.

EUR/USD:

The EUR/USD pair is currently experiencing a pronounced bearish momentum with high confidence, suggesting a potential continued downward movement. The strong bearish tendency is indicated by the price’s position below the bearish Ichimoku cloud and a major descending trend line, suggesting that further bearish momentum is likely.

Our first resistance stands at 1.0909. This level serves as a pullback resistance, aligning with a 23.6% Fibonacci retracement. This suggests that it might be a significant barrier to any potential upward movement. If the price reacts bearishly off this first resistance, it could potentially drop towards the first support level.

The first support is found at 1.0846, a multi-swing low support level. This suggests a strong potential for price stability at this level. It is crucial to monitor the market’s reaction at this point, as a significant break below could further bolster the bearish momentum.

Should the price fail to maintain above the first support, our second support at 1.0792 could come into play. This level serves as a swing low support, making it a critical level to watch for potential price rebounds.

Looking beyond the first resistance, our second resistance stands at 1.0942. This level is an overlap resistance, suggesting that it could present a significant hurdle for any bullish momentum.

GBP/USD:

The GBP/USD pair is currently observing a notable bearish momentum, indicating the possibility of a downward trend continuation. There’s a potential for the price to react bearishly off the first resistance level, leading to a potential drop towards the first support level.

Our first resistance stands at 1.2536, serving as a multi-swing high resistance and coinciding with a 38.2% Fibonacci retracement. This suggests that it might present a significant barrier to any upward price movements.

In the event of a bearish reaction from this first resistance, the price could potentially descend towards the first support level, situated at 1.2446. This level serves as a multi-swing low support, indicating a strong potential for price stability at this point.

However, should the price fail to hold above the first support, our second support at 1.2392 could come into play. This level also serves as a multi-swing low support, making it a crucial level to watch for potential price rebounds.

Beyond the first resistance, our second resistance is at 1.2575. This level is a pullback resistance and aligns with a 61.8% Fibonacci retracement, suggesting that it could pose a significant hurdle for any potential bullish momentum.

Additionally, there is an intermediate support level at 1.2464, which is a swing low support, further emphasizing the bearish bias of the current price movement.

USD/CHF:

The USD/CHF pair is currently demonstrating notable bullish momentum, indicating a potential continuation of the upward trend. This bullish tendency is further suggested by the price’s position above a major ascending trend line, suggesting that further bullish momentum is likely.

Our first support level stands at 0.8943, which serves as an overlap support and aligns with a 38.2% Fibonacci retracement. This suggests a strong potential for price stability at this level. In the event of a bullish bounce from this first support, the price could potentially rise towards the first resistance level at 0.9002.

The first resistance level is an overlap resistance, suggesting that it might pose a significant barrier to further price increases.

However, should the price fail to maintain above the first support, the second support at 0.8871 could come into play. This level serves as a multi-swing low support, making it a crucial level to watch for potential price rebounds.

USD/JPY:

The USD/JPY pair is currently demonstrating strong bullish momentum, indicating the potential for a continuation of the upward trend. This bullish tendency is further suggested by the price’s position above a major ascending trend line, suggesting further bullish momentum is likely.

Our first support level stands at 135.28, which serves as a pullback support and coincides with a 38.2% Fibonacci retracement. This suggests a strong potential for price stability at this level.

However, in light of the current bullish momentum, the focus is on the potential for the price to break through the first resistance level, situated at 136.14. This level serves as a multi-swing high resistance and aligns with a 61.8% Fibonacci retracement, suggesting it might present a significant barrier to further price increases. A bullish breakthrough of this level could potentially lead to a rise towards the second resistance level.

The second resistance stands at 136.99 and is characterized as a pullback resistance. It also coincides with a 78.6% Fibonacci retracement, suggesting that it could pose a significant hurdle for any potential bullish momentum.

In the event the price fails to maintain above the first support, the second support at 134.80 could come into play. This level serves as an overlap support and coincides with a 61.8% Fibonacci retracement, making it a crucial level to watch for potential price rebounds.

AUD/USD:

The AUD/USD pair is currently demonstrating significant bearish momentum, indicating a possible continuation of the downward trend. There’s a potential for the price to continue bearishly towards the first support level.

Our first support level is located at 0.6635, which serves as an overlap support, suggesting a strong potential for price stability at this point. A bearish continuation from the current price levels might lead the price towards this first support.

However, should the price fail to maintain above the first support, our second support at 0.6582 could come into play. This level serves as a multi-swing low support, making it a crucial level to watch for potential price rebounds.

Looking upwards, our first resistance stands at 0.6707. This level is a multi-swing high resistance and aligns with a 38.2% Fibonacci retracement, suggesting that it might present a significant barrier to any upward price movements.

Beyond the first resistance, our second resistance is at 0.6751. This level is a pullback resistance and coincides with a 61.8% Fibonacci retracement, suggesting that it could pose a significant hurdle for any potential bullish momentum.

Additionally, there is an intermediate support level at 0.6663, which aligns with a 61.8% Fibonacci retracement, further emphasizing the bearish bias of the current price movement.

NZD/USD

The NZD/USD pair is currently showing significant bearish momentum, indicating a possible continuation of the downward trend. There’s a potential for a bearish reaction off the first resistance, leading to a drop towards the first support level.

Our first support level is located at 0.6187, functioning as a swing low support. This suggests a strong potential for price stability and may serve as a pivot for any potential bullish reversal.

However, should the price fail to maintain above the first support, our second support at 0.6160 could be activated. This level serves as an overlap support and coincides with a 38.2% Fibonacci retracement, making it a significant level to watch for potential price rebounds.

Looking upward, our first resistance is at 0.6261. This level acts as a pullback resistance and coincides with a 61.8% Fibonacci retracement, suggesting that it may present a substantial barrier to any upward price movements.

Beyond the first resistance, our second resistance is at 0.6316. This level is a pullback resistance, suggesting it could pose a significant hurdle for any potential bullish momentum.

USD/CAD:

The USD/CAD pair is currently demonstrating significant bearish momentum, suggesting a possible continuation of the downward trend. There’s potential for a bearish continuation towards the first support level.

Our first support level is located at 1.3420, acting as a pullback support and coinciding with a 61.8% Fibonacci retracement. This suggests a strong potential for price stability and may serve as a pivot point for any potential bullish reversal.

However, should the price fail to hold above the first support, our second support at 1.3318 could come into play. This level serves as a multi-swing low support, making it a significant level to watch for potential price rebounds.

Looking upwards, our first resistance stands at 1.3580. This level acts as an overlap resistance and aligns with a 78.6% Fibonacci retracement, suggesting it might present a significant barrier to any upward price movements.

Beyond the first resistance, our second resistance is at 1.3638. This level is a multi-swing high resistance, suggesting it could pose a significant hurdle for any potential bullish momentum.

DJ30:

The Dow Jones Industrial Average (DJ30) currently exhibits a neutral momentum, leaving the market in a state of anticipation. The DJ30 might potentially fluctuate between the first resistance and the first support level, suggesting that neither the bulls nor the bears have a strong hold over the market direction.

The first support level stands at 33150.28, acting as a pullback support and aligning with a 78.6% Fibonacci retracement. This level could offer considerable support to the index, should it face any downward pressure.

Should the index breach the first support, the second support at 32951.12 could come into play. This level is a swing low support, and its significance lies in its ability to potentially halt further losses.

On the upside, the first resistance is at 33769.35, acting as a multi-swing high resistance and coinciding with a 61.8% Fibonacci retracement. This level could pose a challenge for the bulls, and any significant move above this level could signal a shift in the market sentiment.

Further up, the second resistance at 34309.09, another multi-swing high resistance, could provide a robust barrier to any sharp bullish momentum.

Intriguingly, the DJ30’s recent price action has formed a symmetrical triangle chart pattern, often seen as a period of consolidation before a significant breakout or breakdown. A break above the upper trendline of this pattern could signal a bullish breakout, while a break below the lower trendline might indicate a bearish breakdown.

GER30:

The GER30, or the DAX 30 Index, currently finds itself in a neutral momentum, indicating an ongoing tussle between the bulls and the bears. The market might potentially see the GER30 fluctuate between the first resistance and the first support level, highlighting a state of balance between upward and downward forces.

The first support level is located at 15701.61, functioning as an overlap support. This level is significant as it represents a price point where the market previously found enough demand to halt a downward move and start an upward one. Hence, it could act as a robust floor, propping the GER30 up if downward pressures materialize.

On the upside, the first resistance stands at 15993.46, a multi-swing high resistance. This level denotes a point where the GER30 previously faced selling pressure strong enough to halt an upward move and start a downward one. It could serve as a substantial ceiling, challenging any bullish attempts to push higher.

A further upward push might encounter the second resistance at 16088.30, a swing high resistance. This level marks a previous high point on the chart, which might again attract selling pressure.

BTC/USD:

The overall momentum of the BTC/USD (Bitcoin/US Dollar) pair is currently bearish, suggesting a likely continuation of the downward move towards the first support level.

The first support is seen at 26497.00, which serves as a pullback support and aligns with the 61.80% Fibonacci retracement level. This key technical level, derived from the Fibonacci sequence, is often used by traders to anticipate areas of possible support or resistance.

A further drop could test the 2nd support at 25807.00, a level marked by a previous swing low. Here, the market had once found enough buying pressure to stop a downward trend and begin an upward move. As such, it could be a challenging barrier for the bears.

On the upside, the first resistance is placed at 27682.00, characterized as an overlap resistance and coinciding with the 78.60% Fibonacci retracement. This level denotes a previous price zone where selling pressure overcame buying pressure, hence it could potentially impede any bullish attempts.

Beyond that, the second resistance is located at 28291.00, another overlap resistance, indicating a price zone that has acted as both support and resistance in the past.

An intermediate support level is also observed at 26934.00, functioning as an overlap support and lining up with the 38.20% Fibonacci retracement. This level could act as a safety net for any steeper falls.

US500

The US500 index is currently demonstrating a neutral momentum, indicating that the price might fluctuate between the first resistance and the first support levels.

The first support level is located at 4099.80, an overlap support that also corresponds with the 50% Fibonacci retracement level. This convergence of key technical indicators might strengthen this level’s potential to halt any downside movement.

If the price continues to fall, the 2nd support level to watch out for is 4061.00. This level, identified as a multi-swing low support, has acted as a floor for the price in the past, suggesting a potential area where buying interest could resurface.

On the upside, the first resistance is placed at 4149.38. This level is characterized as a multi-swing high resistance and aligns with the 78.60% Fibonacci retracement, implying it could pose a significant hurdle for bullish attempts.

Further up, the second resistance is found at 4172.29. This overlap resistance level, where the price has previously alternated between support and resistance, could further limit upside potential.

An intermediate support level is also observed at 4113.03, serving as a swing low support that could offer a temporary resting spot for the price during a potential downward move.

The presence of a symmetrical triangle chart pattern suggests a period of consolidation. This pattern typically precedes a breakout or breakdown. A break above the pattern’s upper trendline might indicate a bullish breakout, while a break below could signal a bearish breakdown.

ETH/USD:

Ethereum’s recent price action against the US Dollar (ETH/USD) indicates a bearish momentum, suggesting a potential bearish reaction off the first resistance level and a subsequent drop towards the first support.

The first level of support is found at 1791.77. This multi-swing low support has been tested multiple times in the past, making it a critical level to watch. Should the price action respect this level, we could see a bounce back upwards. However, a break below this support could see the price slide further to the second support at 1762.65, another well-tested multi-swing low support level.

On the upside, the first resistance level is at 1832.43. This overlap resistance, which aligns with the 38.20% Fibonacci retracement level, could pose a significant barrier to bullish price action. Any upside movement could be capped at this point, potentially driving the price back towards support levels.

Further up, the second resistance level is at 1876.00. This is another overlap resistance and coincides with the 50% Fibonacci retracement level, suggesting a significant area of potential sell pressure.

Importantly, the chart pattern indicates a bearish rising wedge formation. This type of wedge pattern is typically bearish, signaling that the price is likely to drop and move in the downward direction soon.

WTI/USD:

The current chart for West Texas Intermediate (WTI) Crude Oil suggests a bearish momentum, with the price potentially making a bearish continuation towards the first support level.

The first support level to watch for is at $69.33, an overlap support that has proven to be a significant level in the past. If this support holds, it could lead to a price bounce. However, if the price breaks through this level, it could fall further towards the second support at $67.56, which is a multi-swing low support level.

On the upside, the first resistance level is at $73.97. This overlap resistance coincides with the 38.20% Fibonacci retracement level, potentially posing a challenge for any bullish momentum. If the price reaches this level and fails to break through, we could see a reversal towards the support levels.

Higher still, the second resistance level is at $76.91, another overlap resistance that aligns with the 61.80% Fibonacci retracement level. This could be a significant hurdle for any bullish price movement, potentially driving the price back down.

In between these levels, there’s an intermediate resistance at $71.73, which is also an overlap resistance and matches up with the 61.80% Fibonacci retracement level. This level could act as a minor barrier to upward price action.

XAU/USD (GOLD):

The overall momentum of the Gold (XAU/USD) chart is bearish. Factors contributing to this bearish momentum include the price being below a major descending trend line, suggesting further downward momentum is likely.

Given the current market conditions, the price could potentially continue its downward move towards the first support level.

The first support level is at $2009.36, which is an overlap support. This support level has been tested multiple times in the past, making it a significant level for traders to watch.

If the price continues to fall, the next level to watch would be the second support at $1999.52. This level has acted as a multi-swing low support and could potentially halt further downward movement.

On the upside, the first resistance is at $2021.47. This level is an overlap resistance and aligns with the 50% Fibonacci retracement level, making it a significant barrier for any bullish price movements.

The second resistance is at $2033.07, which corresponds to the 78.60% Fibonacci retracement level. This level could act as a strong barrier for price, making it difficult for bullish momentum to continue.

The intermediate support level is at $2014.28, which is an overlap support and corresponds with the 38.20% Fibonacci retracement level. This level could potentially act as a stopping point for price during a bearish retracement.

China’s industrial production, retail sales miss expectations; youth unemployment hits record high

China's industrial production growth fell short of expectations in April, with a year-on-year increase of 5.6% yoy, significantly under expectation of 10.1% growth. Despite missing the mark, the growth rate outpaced March's 3.9% yoy rise and marked the fastest expansion since September 2022.

Retail sales also grew less than expected, posting 18.4% yoy rise, which fell short of anticipated 20.1% yoy growth. The figure was largely inflated due to a low comparison base, as retail sales plummeted by -11.1% yoy in April of the previous year due to severe lockdowns. On a monthly basis, retail sales contracted by -7.8% mom from March.

Fixed asset investment growth also came in below expectations 4.7% ytd yoy growth, underperforming expectation of 5.2%.

Urban jobless rate ticked down from 5.3% to 5.2%. However, unemployment among 16-24 age group spiked to a record high of 20.4%, up from 19.6% in the previous month. This exceeded the previous record of 19.9% set in July 2022.

The National Bureau of Statistics (NBS) stated, "In general, in April, the national economy continued to recover, and positive factors accumulated and increased. But we must also see that the international environment is still complex and severe, domestic demand is still insufficient, and the endogenous driving force for economic recovery is not yet strong."

RBA Minutes: Further hikes may still be required

Minutes of RBA's May meeting revealed a detailed discussion where Board members weighed the pros and cons of keeping cash rate unchanged or increasing it by 25 basis points. Despite the fine balance of arguments, the Board saw it fit to raise the interest rates by 25bps to 3.85%, due to upside risks in inflation and tight labour market.

Data available in the month leading up to the meeting confirmed significant inflationary pressures and highlighted upside risks to the inflation outlook. The Board was concerned that if these risks materialised, it would "further delay the return of inflation to target levels" and potentially trigger a "damaging shift in inflation expectations".

While acknowledging considerable uncertainties surrounding the economic outlook, particularly with respect to household consumption, the Board's strong commitment to price stability and the necessity of anchoring inflation expectations tipped the scales in favour of a rate hike.

Looking forward, the Board indicated that "further increases in interest rates may still be required", depending on the evolution of the economy and inflation.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Perth – 2 May 2023

Members present

Philip Lowe (Governor and Chair), Michele Bullock (Deputy Governor), Mark Barnaba AM, Wendy Craik AM, Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Carol Schwartz AO, Alison Watkins AM

Others present

Christopher Kent (Assistant Governor, Financial Markets), David Jacobs (Head, Domestic Markets Department), Marion Kohler (Head, Economic Analysis Department)

Anthony Dickman (Secretary), David Norman (Acting Deputy Secretary)

International economic developments

Members commenced their discussion of the global economy by noting that headline inflation had passed its peak in most advanced economies and core inflation had moderated. The easing in inflation had occurred as the supply-demand balance in goods markets had improved and earlier increases in energy prices had reversed. However, members acknowledged that inflation remained high and the decline in core inflation had slowed in recent months. Services prices were quite persistent and being underpinned by wages growth above rates consistent with inflation targets in several economies. Members discussed the implications of this for Australia, given the high degree of commonality in inflation globally since the COVID-19 pandemic. Most central banks expected inflation to return to their targets, but not in the year ahead.

Growth in advanced economies had slowed over the preceding six months or so, but by less than had been expected. Conditions in the services sector had remained resilient. Household consumption was being supported by ongoing increases in employment and wages, as well as relatively strong household balance sheets owing to the savings buffers that had been built up in preceding years. Real household disposable incomes had also stopped falling in most major advanced economies as headline inflation had declined. Timely indicators suggested that demand for labour had eased, but unemployment rates remained close to their historical lows.

Members noted that growth in Australia's major trading partners was expected to remain below trend over the coming years, in the range of 3½ to 3¾ per cent, compared with growth of around 4½ per cent prior to the pandemic. However, growth in 2023 was expected to be a little stronger than previously forecast, and the trough in growth in advanced economies was expected to occur later. The risks to growth were perceived to be tilted slightly to the downside; in particular, members observed that the outlook for monetary policy remains uncertain, as central banks balance uncertainty about the pace of disinflation with the possibility of further stress in the financial sector.

The forecast for growth in China in 2023 had been revised higher, reflecting information that the economy had been less affected by, and bounced back more strongly from, the COVID-19 restrictions imposed during 2022 than had been expected. The bounce-back in growth in China had been driven by a strong recovery in consumer spending on services and ongoing robust growth in infrastructure investment. In contrast to most other economies, inflation in China was still below the authorities' target.

Members noted that, while property developers in China remain under financial pressure and demographic trends continue to be unfavourable, there were clearer signs that demand for property may be strengthening. Housing demand had increased, with new sales well above their recent trough and prices for new housing rising in most cities. Despite this, concerns about the outlook for Chinese steel production had affected iron ore and coking coal prices received by Australian exporters over the preceding month. Global oil and gas prices had also fallen during April.

Domestic economic conditions

Turning to the domestic economy, members noted that inflation had eased in the March quarter, confirming the staff assessment that inflation had passed its peak. Despite this, inflation in Australia remained too high and broadly based. Headline inflation had declined to 7 per cent over the year to the March quarter and underlying inflation had declined to 6.6 per cent. Inflation had eased in the quarter for a number of goods-related categories, including consumer durables, groceries and new dwelling purchases. However, input cost pressures (both labour and non-labour) and strong demand continued to contribute to strong price increases for many services. Rent inflation in the CPI continued to rise, with an influx of net overseas arrivals over preceding months adding pressure to rental markets that were already strained.

The staff forecasts were for inflation to return to around the top of the target band by the end of the forecast period in mid-2025, consistent with the forecasts from three months earlier. Further disinflation in goods prices was expected to lead to a further decline in overall inflation, as was below-trend growth in aggregate demand. However, growth in unit labour costs, which had been strong in prior quarters, was expected to be a key driver of underlying inflation over the forecast period. Energy costs were also expected to increase over the coming years, although the Government's Energy Price Relief Plan would reduce the size of the increase in 2023/24 and provide targeted support to low-income earners and small businesses. Rent inflation was expected to continue to pick up over the coming year or so and add materially to inflation over the forecast period, including because of the recent increase in net overseas migration. Members considered a scenario in which goods prices fell over coming years, unwinding a portion of the preceding rise; in this scenario, inflation would return to the middle of the target band by mid-2025. However, this outcome was not considered particularly likely given trends to date and the absence of broad-based falls in goods prices internationally.

Members noted that a range of indicators suggested that wages growth was running at an annual rate of around 3½ to 4 per cent in the March quarter. The Wage Price Index was expected to peak at around 4 per cent later in 2023, before easing slightly. The forecasts incorporated information that suggested strong wage outcomes for some workers were likely in the period ahead. Members noted that unit labour costs had been growing strongly, owing in part to the very limited productivity growth over the preceding three years. Various factors might explain the weak productivity outcomes, including COVID-19-related disruptions and strong growth in employment in government-funded services, where achieving productivity increases is often difficult. Members discussed the importance of unit labour costs in determining inflation over the forecast period and that a rise in productivity growth would be needed to ensure consistency of the wages growth forecast with the Bank's inflation target.

The tightening in monetary policy over the preceding year had contributed to a slowing in output growth. Timely indicators suggested that growth in the March quarter had been subdued, especially in per capita terms. Population growth had been stronger than expected, reflecting a strong pick-up in net overseas migration as foreign students and working holiday makers returned. Despite the pick-up in population growth, output growth was expected to reach its trough in the second half of 2023 at 1¼ per cent and to pick up gradually after that as the effect of earlier policy tightening starts to wane, inflation moderates and housing prices recover.

Turning to the labour market, members noted that employment growth was very strong in the month of March and that growth in the March quarter had been concentrated in full-time employment. Members discussed how much of this persistent strength was because employment typically lags output and how much reflected ongoing strength in activity in the services sector. The unemployment rate remained near historical lows, at 3½ per cent, but was expected to reach 4½ per cent by late 2024. Conditions in the labour market were not as tight as a few months earlier, with some easing in indicators of hiring intentions and a modest decline in vacancies. The increase in numbers of overseas arrivals had supported strong growth in employment in prior months and had also helped alleviate labour shortages in some areas. Even so, labour shortages remained a constraint for many firms, including in the construction sector.

Recent indicators suggested that consumer spending was subdued in the March quarter. Information from the Bank's liaison contacts pointed to a further modest decline in retail spending in April, with evidence continuing to suggest that some consumers had been trading down to cheaper items. Consumer sentiment remained weak, particularly among households with mortgages on their homes. Household disposable income had also been falling in real terms, given high inflation, rising interest rates and the effect of 'bracket creep' on income tax payments as nominal incomes rise. While the significant decline in housing prices over the preceding year had constrained consumption spending, housing prices had recently stabilised and some increases had been recorded. In recognition of this, the forecast for consumption growth by mid-2025 had been revised a little higher.

Demand for new housing had been weak but was expected to be supported by strong fundamentals in the medium term, including population growth over coming years. Despite higher rental yields, incentives to expand residential building had been impeded by high construction costs, the increase in interest rates and construction delays, including because of labour shortages. Building approvals, greenfield land sales and new home sales were all at their lowest levels in a number of years. As a result, building activity was expected to decline once the backlog of construction is worked through. A shortfall in supply relative to strong demand had translated into upward pressure on rents, which was expected to continue for some time.

In the business sector, the outlook for non-mining investment over the coming years had softened a little but remained positive. While non-residential construction activity was expected to be supported by a large pipeline of projects, a shortage of skilled tradespeople would constrain how quickly these projects can be undertaken. The outlook for mining investment growth was subdued and little changed from three months earlier.

Members noted that public demand was expected to remain at a high level over the next few years, even as pandemic-related expenditure fades. Spending would be supported by a substantial program of public engineering works and a general expansion of public consumption, as the population increases and due to specific schemes (including the National Disability Insurance Scheme). Export volumes were expected to grow further over the year ahead, driven by services exports. The forecast for services exports had been revised up owing to a significant upgrade in the expected number of students living in Australia and the expected return of international travel to pre-pandemic levels.

International financial markets

Members noted that international financial markets had stabilised in prior weeks as banking concerns had eased somewhat, although fragilities had again come to the fore with the failure of First Republic Bank in the United States. Alongside the earlier banking concerns, deposits had shifted into money market funds because of the safety of the short-dated government assets in which those funds invest. This accelerated a trend that had begun in 2022 as savers were attracted by the higher returns on those funds relative to bank deposits. Nevertheless, the recent actions of policymakers continued to support confidence in the broader stability of the global banking system. Banks' share prices had picked up somewhat but remained lower than earlier in the year, while the broader equity market had been supported by corporate earnings, which had generally been better than expected.

Market participants' expectations for the path of policy rates had shifted up a little for most central banks over the preceding month. Members observed that some central banks, including the Reserve Bank of New Zealand and Sveriges Riksbank, had increased policy rates further, emphasising the need to address persistent inflationary pressures. The US Federal Reserve, the European Central Bank and the Bank of England were expected to raise their policy rates further in the period ahead. Several central banks had also emphasised that policy rates were unlikely to decline later in the year, in contrast to market-implied expectations. Despite moving a little higher in the period leading up to the May meeting, the expected paths of policy rates generally remained below their levels before the collapse of Silicon Valley Bank. This partly reflected an expectation that the recent bank stresses would result in some tightening of broader financial conditions, especially in the United States, which by itself would weigh on demand and thereby help to reduce inflationary pressures.

In most advanced economies, government bond yields had risen somewhat as banking concerns had eased, although they were still lower than earlier in the year. The Australian dollar had depreciated a little further and was lower against the US dollar and on a trade-weighted basis than earlier in the year.

In China, financial conditions remained accommodative, with bond yields having declined recently as inflation remained lower than expected. Credit growth had increased, aided by policy measures in support of infrastructure spending and the property sector. However, many highly leveraged property developers still faced considerable financial stress.

Domestic financial markets

Members noted that the earlier increases in the cash rate had continued to pass through to broader financial conditions. Scheduled mortgage payments, which comprise interest and scheduled principal payments, had risen to almost 9 per cent of household disposable income in the March quarter – an increase of around 1¾ percentage points from a year earlier. Scheduled payments would continue to rise even if the cash rate remains unchanged, given the large number of low-rate fixed-rate loans that will roll-off over the year.

Extra mortgage payments (over and above scheduled payments) had increased a little in the March quarter, resulting in a notable increase in total mortgage payments. By contrast, extra payments had declined materially over the prior year, which had offset much of the rise in scheduled payments over that time. Members discussed several potential interpretations of the recent increase in extra payments. It could reflect: a transfer of other forms of savings into mortgage redraw and offset accounts, as fixed-rate mortgages converted to variable-rate mortgages; or households constraining their non-essential spending to avoid running down the savings they had built up during the pandemic, particularly given that higher interest rates provide an additional incentive to save; or quarterly variation around a downward trend, as had been seen in the past.

Consistent with the effects of tighter monetary policy, credit growth had continued to slow. However, members observed that a range of indicators suggested that conditions in the housing market were stabilising. This partly reflected a rise in population growth, although shifting expectations for the outlook for monetary policy may also have contributed.

Market pricing suggested that no further increases in the cash rate were expected, which was little changed from the previous meeting. The decision to leave the cash rate unchanged in April had been widely anticipated by market participants. Most market economists expected no change at the May meeting, although some expected one or two more quarter-point increases in the months ahead based on a need to do more to address inflationary pressures. Those economists who expected no further increases noted that consumption growth had slowed, labour market tightness had eased a little and inflation had peaked; they also noted that the Board's approach was to bring inflation back to target in a measured fashion to preserve gains in the labour market.

Members reviewed the Bank's approach to reducing its holdings of government bonds, which had been purchased during the pandemic to support markets and provide stimulus. As had been decided by the Board a year earlier, the strategy was to hold these bonds until maturity rather than selling them prior to that. This approach recognised that the Bank's balance sheet was already set to decline rapidly given the maturity of funding under the Term Funding Facility, and that bond sales might complicate governments' bond issuance and reduce the effectiveness of any future quantitative easing program.

Members agreed that this approach remained appropriate for the time being. However, they noted that the initial tranche of Term Funding Facility maturities would occur in coming months and would provide information on how financial markets respond as the Bank's balance sheet declines. More generally, the Bank's large holdings of government bonds exposed its balance sheet to a significant level of interest rate risk. Accordingly, members agreed it was appropriate to review the current approach periodically.

Considerations for monetary policy

In turning to the policy decision, members noted that inflation was still very high but had peaked, consumption growth was forecast to remain subdued for some time, and the unemployment rate was low and expected to rise gradually. Members judged that the forecasts were still consistent with the economy remaining on the narrow path on which inflation comes down steadily and the unemployment rate increases but remains below pre-pandemic levels. At the same time, members acknowledged that there were significant uncertainties, and that history highlights the challenges of staying on such a path.

Members discussed two options: holding the cash rate unchanged; or increasing the cash rate by 25 basis points.

The case for holding the cash rate unchanged rested on several arguments.

Members noted that inflation had peaked and was showing signs of slowing further. They considered the possibility that inflation could return to the centre of the inflation target band earlier than forecast if there was a reversal of some of the significant increase in goods prices recorded over preceding years. Members also noted that while wages growth had increased, it was still consistent with the inflation target if productivity growth picked up to its pre-pandemic rate. Further, indicators from liaison contacts and private sector surveys signalled that wages growth was stabilising.

Members observed that the outlook for consumption was weak and had been revised a little lower in the near term. They noted that consumption per capita was not expected to rise over the year ahead and discussed the possibility that consumption could turn out weaker than expected. Many households were experiencing significant financial pressures associated with the higher cost of living and increased mortgage payments, and a further increase in aggregate mortgage payments was expected as fixed-rate loans progressively expire. Subdued growth in consumption was expected to lead to a moderation in inflation, and it was possible that the forecast increase in unemployment could result in inflation slowing more quickly than expected.

Finally, members noted that the lags associated with monetary policy transmission and the extent of policy tightening over the prior year created additional uncertainty around the outlook for the economy. Given this, there was a case to continue to hold the cash rate steady in order to gather additional information.

On the other hand, there were several arguments supporting an increase in the cash rate.

While the staff's central forecast had inflation declining, inflation was not expected to reach the top of the target band until mid-2025. Members noted that, although this was consistent with the Bank's mandate and objectives, it left little room for upside surprises to inflation given that inflation would have been above the target for around four years by that time.

In this context, members discussed the potential for upside risks to inflation. They noted the persistence in services price inflation in many other countries and discussed the possibility that Australia might have the same experience. Strong population growth and low rental vacancy rates could also see rents grow even faster than the central forecast envisaged.

Another upside risk to inflation was the possibility that productivity growth remains very weak. Members observed that the forecast for inflation to return to the top of the target band by mid-2025 was predicated on productivity growth returning to around the modest pace recorded prior to the pandemic. If this did not occur, growth in unit labour costs would be uncomfortably fast.

A related upside risk was the possibility that a prolonged period of high inflation leads to a shift in inflation expectations and a change in price- and wage-setting behaviour. If so, this would make it more difficult to bring inflation back to target within a reasonable timeframe. It would require even larger increases in interest rates and involve a worse outlook for the labour market.

Members also reviewed recent developments in asset markets – in particular, they noted the depreciation of the exchange rate and the increase in housing prices. While several factors had contributed to these developments, the decision to hold interest rates steady in April was likely to have contributed. Although the Board does not target asset prices, members agreed that movements in asset prices provide relevant information and need to be considered when assessing the outlook for activity and inflation.

Members discussed the economic data over the prior month and their implications. They particularly noted the strong growth in employment in March, the high rate of services price inflation in the March quarter CPI, further evidence of persistent services sector inflation abroad, and some easing in the stresses in global banking markets.

In weighing up the two options, members recognised that the arguments were finely balanced but judged it was appropriate to increase interest rates at this meeting.

The information available over the prior month had confirmed that the labour market remained tight and that inflationary pressures were significant. That information also pointed to upside risks to the outlook for inflation. If these risks materialised, they would further delay the return of inflation to target, with the prospect of a damaging shift in inflation expectations. Further, members noted that the forecasts presented at the meeting were predicated on a technical assumption for the path of the cash rate that involved one further increase.

In reaching their decision, members acknowledged that there were still significant uncertainties surrounding the economic outlook, particularly for household consumption. But, on balance, given the Board's strong commitment to price stability and the importance of ensuring that inflation expectations remain anchored, members judged that a further increase in interest rates was warranted.

Members discussed how best to communicate the Board's decision. They concluded that it was important to emphasise the implications of the recent data releases as well as the updated set of forecasts and the evolving nature of the risks, including from weak productivity growth. Members reaffirmed the Board's determination to do what is required to bring inflation back to target, while emphasising that it is still seeking to traverse the narrow path. Members also agreed that further increases in interest rates may still be required, but that this would depend on how the economy and inflation evolve.

The decision

The Board decided to increase the cash rate target to 3.85 per cent and to increase the interest rate on Exchange Settlement balances to 3.75 per cent.

Australian consumer sentiment plunges in May following unexpected RBA rate hike

Australia Westpac Consumer Sentiment Index dropping sharpy by -7.9% from 85.8 to 79.0 in May. This decline brings the index close to the grim levels observed in March, which were the lowest since COVID-19 outbreak in 2020 and, prior to that, since the severe recession of early 1990s.

The unexpected decision by RBA to raise the cash rate by an additional 0.25% in May, as well as the Federal Budget, were cited by Westpac as the two main factors impacting consumer sentiment over the last month.

Westpac stated, "Interest rates were again a key driver of the May survey. The RBA raised the official cash rate by a further 0.25% at its May meeting in the week before the survey. The move came as a major surprise to markets and most commentators, clearly stoking consumer fears of more increases to come."

Looking ahead, Westpac predicts that RBA will likely pause in June, awaiting further data on inflation and the state of the economy. While the bank's central view anticipates the current cash rate will remain at its peak due to economic weakness and clear progress toward the Board's inflation target, it acknowledges that the risks are still "evenly balanced".

BoE Pill: Self-sustaining, second-round-effect momentum could keep inflation high

BoE Chief Economist, Huw Pill, voiced his concern about the enduring momentum of inflation in the UK during an online event yesterday. Pill warned of the risk of a self-sustaining inflation cycle, where despite the dissipation of key short-term inflation drivers like rising energy and food costs, businesses and workers would continue to seek substantial price and wage increases.

He said, "The risk is ... that self-sustaining, second-round-effect momentum within the UK economy keeps inflation running at above-target levels."

This trend could still align with a significant drop in headline inflation, Pill noted, but he expressed concern that headline inflation could stagnate at around 4% or 5% over the next two to three years.

"That's still compatible with quite a big fall in headline inflation, but maybe headline inflation - other things equal - getting stuck at that 4%, 5% level over the next two or three years," he clarified.

Meanwhile, Pill also highlighted the potential of AI to increase productivity and, subsequently, living standards. He emphasized, "Using AI to make ourselves more productive is one example of how we can do that to boost living standards. This is a win-win if we all get better off because we're all more productive."

Fed’s Barkin questions “whether we need to do more”

Richmond Fed President Thomas said yesterday that he is unconvinced that inflation will taper off rapidly with only a marginal economic slowdown. Barkin stated, "You could tell yourself a story where inflation comes down relatively quickly ... with only a modest economic slowdown."

He quickly added, "But I'm not yet convinced ... I do wonder whether we're not going to need more impact on demand to bring inflation down to where we need to go."

Barkin stayed open-minded about Fed's policy direction at the upcoming June 13-14 meeting. Despite having raised the policy rate by 5 percentage points since March 2022, Barkin isn't ruling out the possibility of another hike.

In terms of the labor market, Barkin noted the shift from what he described as "red hot" to merely "hot." He asserted, "On the unemployment side, I think you could fairly say it's moved from red hot to hot, right? There's nothing about 3.4% unemployment that feels ... cool."

Despite the gradual effects of rate hikes beginning to show, Barkin emphasized that the job market remains robust and inflation persistent. He admitted, "I'm still seeing data that suggests a hot job market and enduring inflation," leading him to believe inflation could persist longer than market measures suggest. Therefore, he concluded, "I'm still looking to ask myself the question whether we need to do more."

Separately, Minneapolis Fed President Neel Kashkari said the central bank probably has "more work to do on our end, to try to bring inflation back down," adding that "we should not be fooled by a few months of positive data."

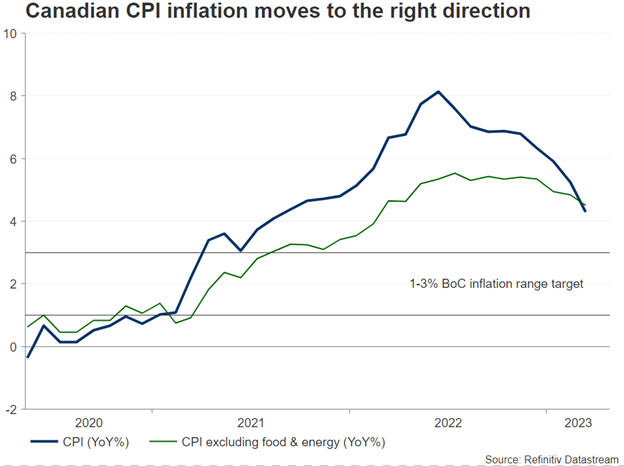

Canadian CPI Inflation to Cool Further

Investors will look for clues on whether the rate cut pricing in Canada is unseasonable after the BoC chief claimed that the rate hike cycle may resume if necessary to press inflation to the target. The figures are expected to weaken for the fifth consecutive month on Tuesday at 12:30 GMT, likely creating some extra downside pressure in the Canadian dollar.

Credit conditions

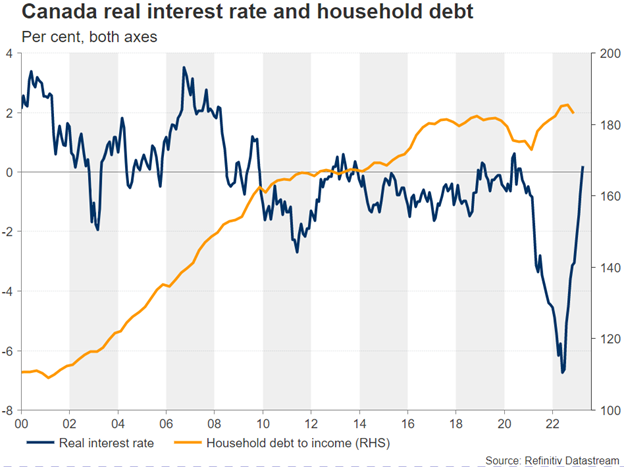

The Bank of Canada (BoC) was the first major central bank to pause monetary tightening in March and maintain interest rates flat since then at 4.5% y/y as concerns over the effects of previous rate hikes mounted after the bank turmoil in the US.

Household debt has been a headache for the Canadian economy before the pandemic and became even more concerning when household-debt-to-disposable income hit a record high at 185.39% in the third quarter of 2022 before inching slightly lower. With real interest rates skyrocketing from 0.25% to 4.50% in just one year, Canada’s financial sector could get closer to a brink given that fixed rates are scheduled to expire earlier in Canada than in other major economies, while its high exposure to the US in terms of exports and commodity prices is adding to the negative risks.

The labor market has been another source of strength for the economy, creating more jobs than expected in March and keeping the unemployment rate steady at record lows for the fourth consecutive month. Strikingly, average wage growth held resilient above 5.0% and higher than inflation.

Of course, the Royal Bank of Canada warned that the mortgage delinquency rate could rise by a third in a year, though as long as the jobs market supports economic growth and inflation stands above the target, the central bank will not cut interest rates as some investors forecast.

CPI inflation estimates

The headline CPI inflation figure is expected to edge lower to 4.1% y/y in April from 4.3% previously – the lowest since August 2021 – , with the monthly reading also inching down to 0.4%. While that could put smiles on policymakers’ faces, especially if the core measures drift lower too, the BoC may need more evidence in the coming months before confirming that inflation will not pivot higher again. According to the BoC’s latest business survey, respondents believe that inflation will stay above 3.0% over the next two years, while the turnup in house prices in Toronto, which persisted for the third consecutive month in April – after a year of declines – raised speculation that inflation expectations may stay elevated.

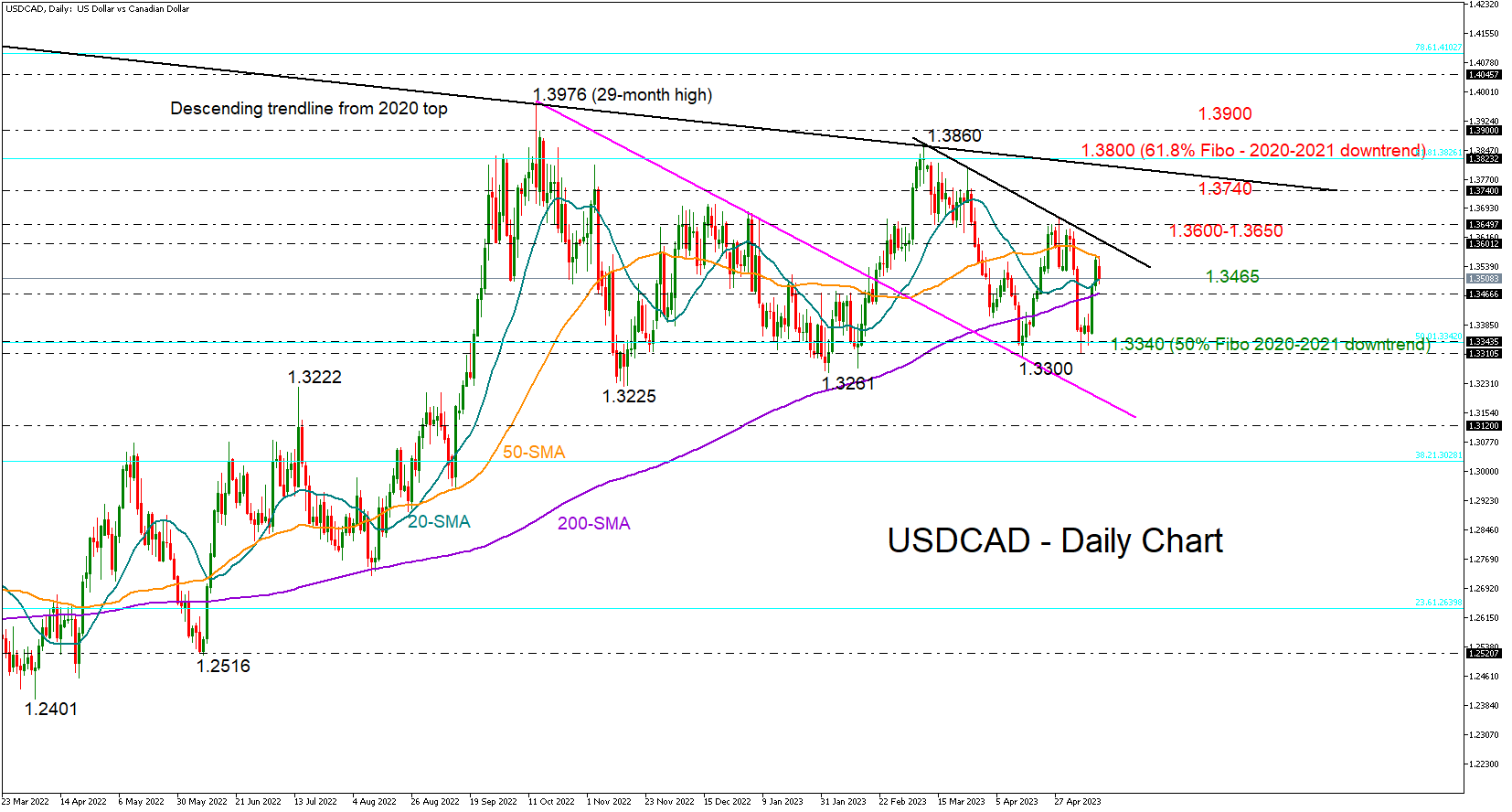

USD/CAD

Hence, if CPI readings arrive above expectations, questioning the rate cut pricing in markets and signaling that the BoC has still some job to do to achieve its price stability target, the loonie may recoup some of its recent losses. In this case, dollar/loonie could slide back below its 200-day simpe moving average (SMA) at 1.3465 and towards the key 1.3340 support zone. Note that futures markets provide a 36% probability for a rate cut to 4.25% in December.

In the event inflation falls at a faster pace than investors believe, endorsing the central bank’s stance and perhaps making a rate cut more likely in the year ahead, dollar/loonie may re-challenge last week’s tough resistance of 1.3600. A break above that border and beyond April’s bar of 1.3650 is required to lift the price up to the crucial 1.3740-1.3800 constraining zone.

On Friday, retail sales might attract some additional attention even though the data tend to cause little volatility in the loonie. Forecasts point to a 1.4% m/m decline in March, the fastest since September 2022. The measure which excludes automobiles is expected to diminish by -0.8% m/m from -0.7% previously.

A day earlier on Thursday, the BoC Governor and Senior Deputy Governor will hold a press conference to discuss the contents of the Financial System Review—a detailed analysis of developments in the financial system.