Sample Category Title

Some Positives for BoE from UK Jobs Data, Chinese Figures Less Good

Stock markets are treading water on Tuesday, with jobs number from the UK not inspiring and Chinese data also highlighting weakness in the recovery.

Some positives for the BoE to cling to

UK jobs data was a mixed bag this morning as wages accelerated again to 6.7%, excluding bonuses, while unemployment also ticked higher as inactivity fell. The Bank of England will no doubt be concerned about the pace of wage growth, with it not being consistent with inflation returning to 2%, but there are signs of slack emerging which is encouraging.

If inflation does halve as expected this year, that in itself should have a dampening effect on wage growth alongside a less tight labour market. There's still a long way to go but there are promising signs. Sterling declined after the data amid signs that the numbers may soon be enough for the MPC to pause its tightening cycle. Markets are pricing in only one more hike this year before reversing course from the start of next.

An unbalanced recovery in China

Chinese data overnight disappointed, highlighting the likely need for further monetary support from the PBOC over the coming months. The consumer has been the engine of growth for the economy in the opening months of the year but that, as we've seen elsewhere post-pandemic, is primarily services based.

The recovery in China is simply not broad-based and there remain many pockets of weakness that targeted stimulus could provide a boost to. Industrial production and fixed asset investment were both well short of expectations last month and there's little sign of that improving without additional support.

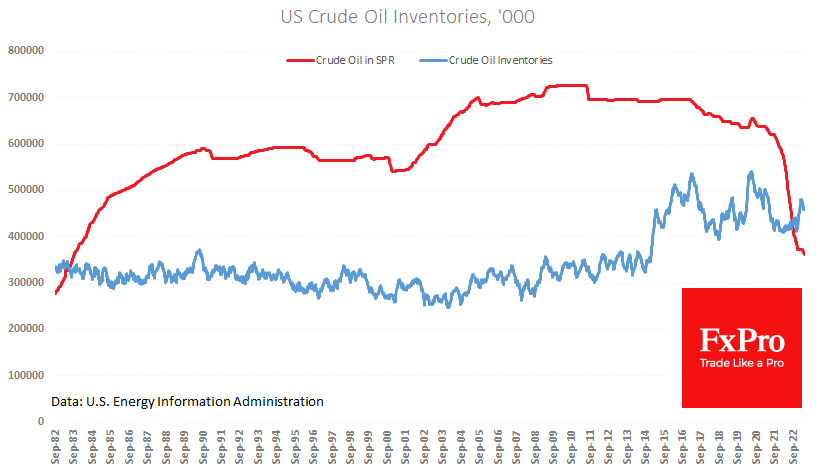

Oil settles in lower range and further declines may prove challenging

Oil prices are marginally higher on Tuesday but remain below the December to March range. The risks remain tilted to the downside amid a sluggish recovery in China, uncertainty around the US economy and banking system, and the impact of much higher interest rates on demand.

The primary bullish case for oil prices comes from OPEC+ and the prospect of another output cut in a couple of weeks but even that has been downplayed. Perhaps Brent has simply consolidated for now in a $70-$80 range, with a move below here potentially difficult as the US seeks to refill the SPR at these levels, while OPEC+ wouldn't hesitate to pull the trigger if prices slipped too far.

Gold buoyed by debt ceiling drama

Gold is a little lower on the day but remains above $2,000 as traders appear reluctant to concede on hopes of record highs. The yellow metal came within a whisker of record highs earlier this month and could take another run at it, depending on how things unfold over the coming weeks.

Debt ceiling drama could be supporting gold and preventing a deeper correction. I think everyone is extremely confident that a default will not happen but the closer we get to the deadline, the more we'll see those risks being priced into the markets which could support gold.

Beyond that, it's all about interest rates and whether we can get more evidence of inflation abating and the labour market becoming less tight. That will justify a pause next month and, if we see significant progress on that front, start the conversation around when easing will begin.

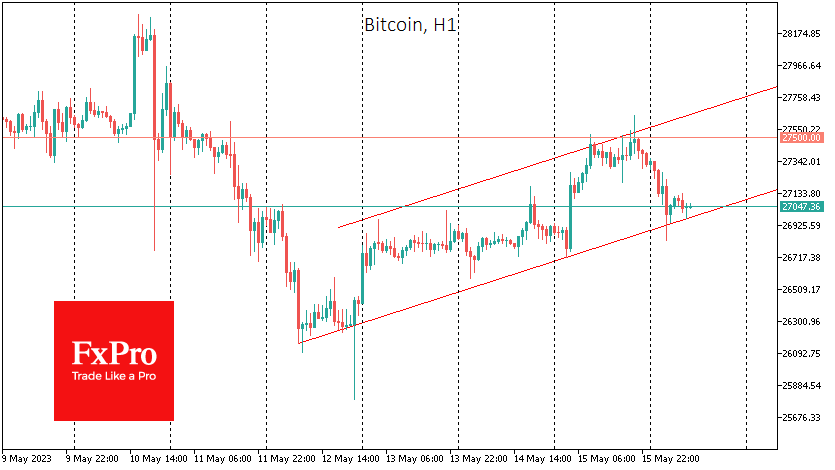

A deeper correction for Bitcoin?

Bitcoin appears to be consolidating around $27,000 in the short term but there remains downside risk after breaking this notable support level last week. It found support around $26,000 but may struggle to generate significant momentum higher. It's been a phenomenal run this year so a correction would make sense. If it does break below $26,000 then $25,000 would be the next potential support level.

Aussie Shrugs Off RBA Minutes, Weak Consumer Confidence

- RBA minutes state further rate hikes possible.

- Australian consumer confidence sinks.

- Australian wage growth to be released on Wednesday.

The Australian dollar has taken investors on a wild ride over the past few days but has settled down on Tuesday. AUD/USD is trading at 0.6687 in Europe, down 0.13% on the day.

RBA minutes indicate more rate hikes possible

The RBA released the minutes of its meeting earlier this month. That meeting was a barn-burner, with the RBA stunning the markets with a 25 basis-point hike. The central bank had finally taken a pause in its rate-tightening cycle in April and given the lukewarm economy, a second-straight pause seemed a safe bet, but in the end, the RBA opted for a rate increase.

The minutes noted that the decision to pause or hike was “finally balanced”, with strong arguments for both. In the end, policy makers opted to lift rates in order to lower the risks of inflation becoming entrenched in the economy. Strong population growth, low rental vacancy rates and a tight labour market supported a rate hike.

What can we expect next from the RBA? The minutes didn’t provide any insights, stating that more rate hikes “may be required” to drive down inflation, but that would “depend on how the economy and inflation evolve”. In other words, don’t look to the RBA for guidance, as rate policy will depend on economic data, particularly inflation.

Australian consumer confidence fell sharply, but the Australian dollar didn’t react. Westpac Consumer Confidence plunged 7.9% in May, a sharp reversal from the 9.4% gain in April and much worse than the estimate of -1.7%. The Westpac survey found that consumers were very pessimistic about the surprise rate hike and expect mortgage rates and house prices to move upwards.

We’ll get a look at wage growth on Wednesday, which is expected to rise in the first quarter. The RBA will be watching carefully and an unexpected reading could see the Aussie show some volatility.

AUD/USD technical

- AUD/USD is putting pressure on resistance at 0.6699. This is followed by 0.6761.

- 0.6579 and 0.6517 are providing support.

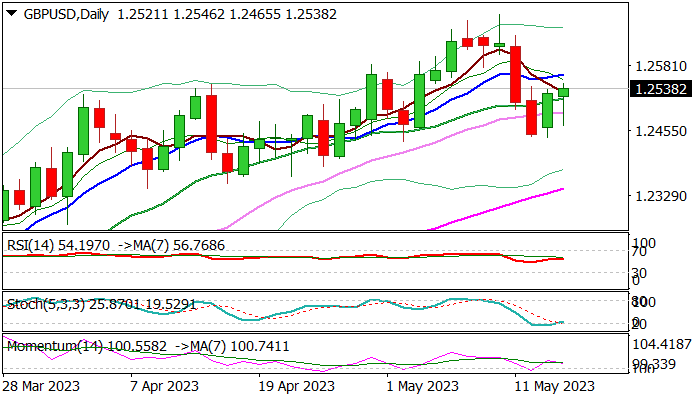

GBP/USD: Bulls Regain Traction and Generate Initial Signal that Correction Has Bottomed

Cable quickly regained ground after post-UK jobs data dip below 1.25 handle, following short-lived negative impact from higher unemployment and jobless claims, as prevailing expectations that the BoE would deliver another rate hike in June continue to underpin pound.

Fresh advance, if sustained, would generate an initial signal that correction from 1.2679 peak (May 10) might be over.

Look for signal on close above cracked Fibo barrier at 1.2534 (38.2% of 1.2679/1.2444), which will require verification on lift and close above 1.2562 (10DMA/50% retracement) and open way for further recovery towards targets at 1.2590 and 1.2624 (Fibo 61.8% and 76.4% respectively) in extension).

This would bring daily MA’s into full bullish setup and contribute to existing signals from bullish momentum and Stochastic reversing from oversold territory.

Today’s long tailed daily candle also signals strong bids, though close above broken 20DMA (1.2517) is needed to keep near-term bias with bulls.

Res: 1.2562; 1.2590; 1.2624; 1.2640.

Sup: 1.2518; 1.2472; 1.2444; 1.2402.

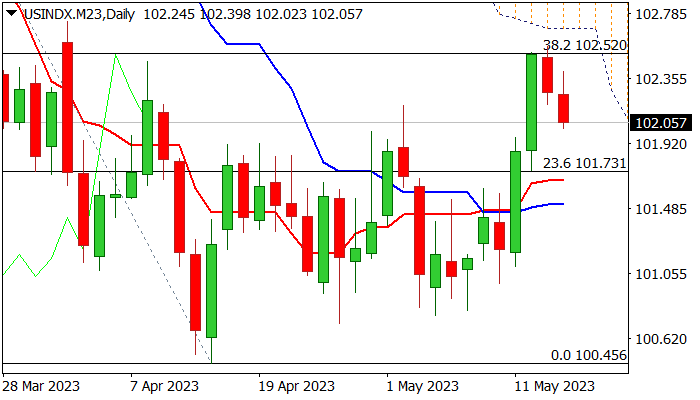

Dollar Index in Defensive after a Double Upside Rejection

The dollar dipped further on Tuesday morning, extending pullback into second consecutive day after bulls repeatedly failed to break through pivotal Fibo support at 102.52 (38.2% of 105.85/100.45 downleg).

Upside rejection formed a double-top and signals a bull-trap, which adds to the downside pressure.

Conflicting signals on daily chart (strong bullish momentum, overbought stochastic and MA’s in mixed setup) require caution as last week’s strong recovery stalled at a breakpoint zone, also weighed by the nearby base of falling and thickening daily Ichimoku cloud (102.68).

The action failed to violate these barriers and generate fresh bullish signals for further gains, as subsequent pullback shifts near-term risk to the downside, although hopes that bulls may regain ground would be still alive if dips stay above 101.70 (broken Fibo 23.6% / daily Tenkan-sen).

Near-term action remains weighed by uncertainty over debt ceiling crisis, as President Biden was optimistic, while Republicans say that two sides are still far from reaching a deal, ahead of the expected meeting later today.

Res: 102.52; 102.68; 103.15; 103.26.

Sup: 101.91; 101.70; 101.52; 101.09.

S&P500 (SPX) Elliott Wave: Calling The Rally From The Equal Legs Area

In this technical article we’re going to take a quick look at the Elliott Wave charts of SPX published in membership area of the website. As our members know, S&P500 is trading within the cycle from the October 2022 low, which is unfolding as 5 waves structure. We got 3 waves pull back which found buyers right at equal legs area as we expected. In the further text we are going to explain the Elliott Wave Forecast

SPX 1h Elliott Wave Analysis 05.04.2023

SPX is doing wave 4 red pull back. The index is correcting the cycle from the 3837.92 low. Pull back looks incomplete at the moment. It’s still short of equal legs area that comes at 4051.78-3991.85. At that area SPX should ideally find buyers for further rally in wave 5 red or for a 3 waves bounce at least.

SPX 1h Elliott Wave Analysis 05.16.2023

SPX made extension down toward equal legs area as we expected. Buyers appeared at the marked extreme zone and we are getting good reaction from there. As far as 4048.28 low holds, SPX should ideally keep trading higher in wave 5 red targeting 4218.9-4271.7 area.

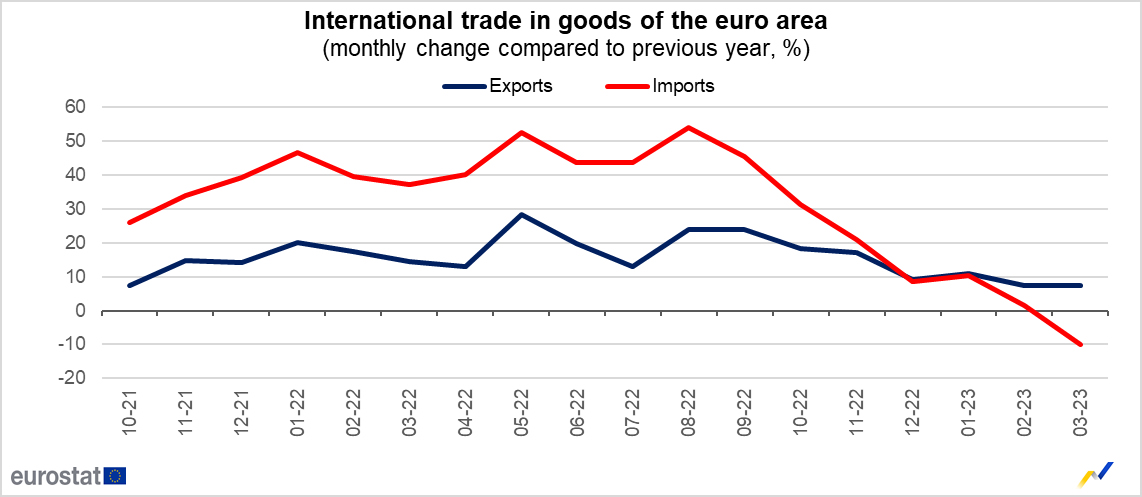

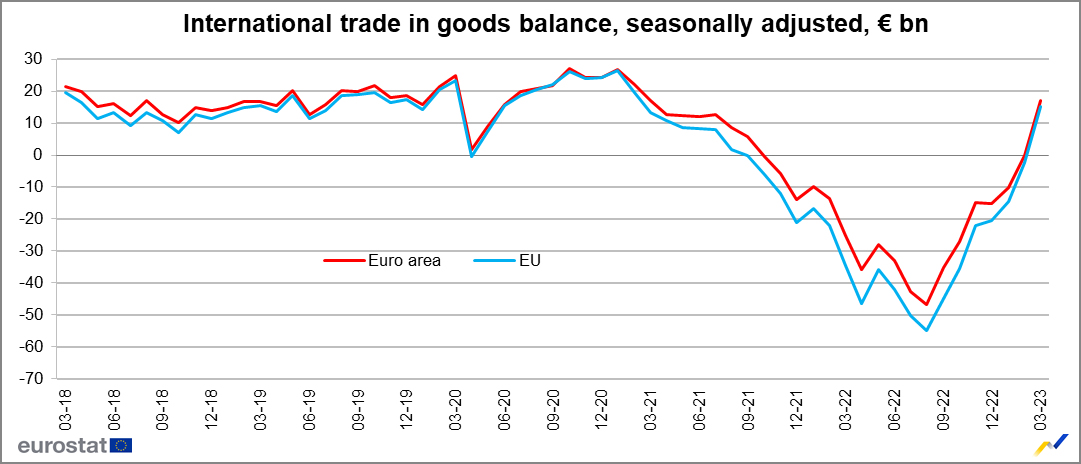

Eurozone imports fell -10% yoy in Mar, exports rose 7.5% yoy

Eurozone goods exports to the rest of the world rose 7.5% yoy to EUR 269.2B in March. Imports fell -10.0% yoy to EUR 243.5B. Trade surplus came in at EUR 25.6B. Intra-Eurozone trade rose 0.6% yoy to EUR 246.4B.

In seasonally adjusted term, goods exports dropped -0.1% mom to EUR 243.3B. Imports dropped -7.1% mom to EUR 226.2B. Trade balanced turned into EUR 17.0B surplus, above expectation of EUR 5.6B. Intra-Eurozone trade dropped from EUR 230.9B to EUR 223.2B.

Germany ZEW dived to -10.7, economy could slip into recession

Germany ZEW Economic Sentiment recorded in significantly decline from 4.1 to -10.7 in May, even worse than expectation of -5.0%. Current Situation Index dropped from -32.5 to -34.8.

Eurozone ZEW Economic Sentiment fell form 6.4 to -9.4. Current Situation Index rose 2.7 pts to -27.5.

ZEW President Professor Achim Wambach said:

"The ZEW Indicator of Economic Sentiment has once again fallen sharply. The financial market experts anticipate a worsening of the already unfavourable economic situation in the next six months. As a result, the German economy could slip into a recession, albeit a mild one.

"The sentiment indicator decline is partly due to expectations of further interest rate hikes by the ECB. Additionally, the potential default by the United States in the coming weeks adds uncertainty to global economic prospects".

GBPUSD Trapped Between Key Barriers

GBPUSD attempted to recover some lost ground on Monday after its pullback from the 2021 descending trendline stalled near 1.2442. Despite its latest bullish efforts, the pair could not overcome its 20-day simple moving average (SMA), which has been acting as resistance over the past three days around 1.2520.

Given the falling MACD and the negative slope in the RSI, which is set to cross below its 50 neutral mark, the risk is tilted to the downside rather than the upside. That said, the pair is currently well supported around the ascending trendline drawn from September’s record low at 1.2445. If the bears breach that floor, the 50-day SMA could immediately come to the rescue at 1.2388. Otherwise, the decline could continue towards the 50% Fibonacci retracement of the 2021-2022 downtrend at 1.2285 and the 1.2200 round-level. Another failure here could initially test the 1.2130 barrier before squeezing the price down to the 1.2000 psychological mark and the 200-day SMA at 1.1960.

In the bullish scenario, where the price closes above the 20-day SMA at 1.2520, the spotlight will fall again on the crucial long-term descending trendline seen around 1.2635. Should that ceiling crack this time, with the pair extending its uptrend above the one-year high of 1.2678, the uptrend may stretch up to the 1.2800-1.2860 constraining zone. The 61.8% Fibonacci mark of 1.3000 could be the next destination, while a steeper increase could reach the short-term resistance line from March at 1.3140.

Summing up, GBPUSD seems to be preparing for a new bearish wave following another rejection near a long-term resistance trendline. Yet, the pair may have another opportunity for a rebound, unless the price slips below the upward-sloping trendline at 1.2445 and the 50-day SMA.

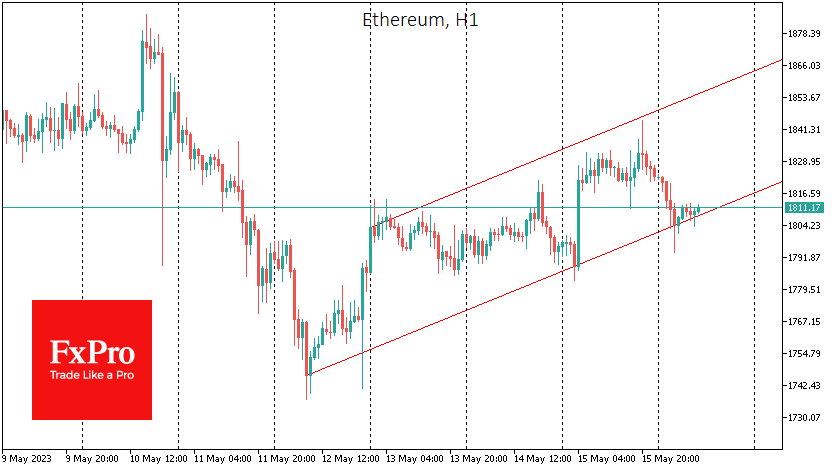

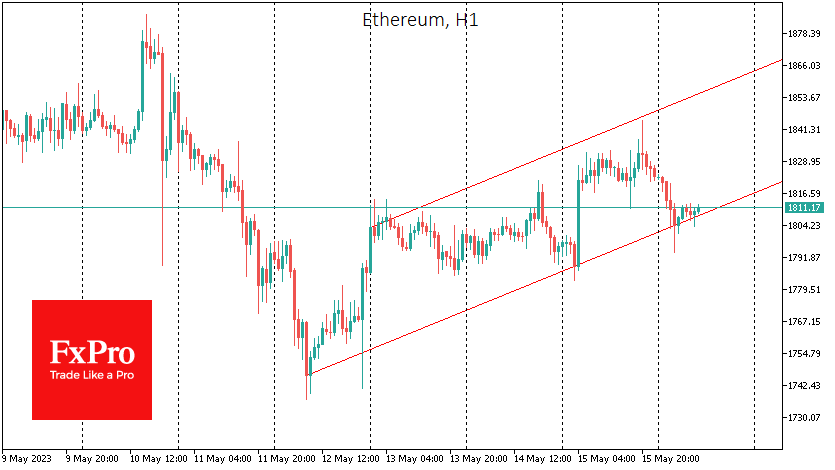

Ether and Bitcoin Seek Local Support

Market picture

The total crypto market capitalisation is down 1.7% over the last 24 hours to $1.13 trillion. Bitcoin is down 1.6%, Ether is losing 1%, and among the top altcoins, only Litecoin and Tron show positive dynamics, adding around 0.8%.

Bitcoin’s advance on Monday stopped near $27.5K, and at the time of writing, the price has rolled back to $27K, the lower boundary of last Friday’s short-term uptrend channel. A break below $ 26.7K could put more pressure on the cryptocurrency.

There is also a similar short-term channel in ETHUSD, and a failure from the current $1,810 to $1,780 would mark a new short-term victory for the bears, potentially triggering a downward spike.

According to CoinShares, investments in crypto funds fell by $54 million last week, the fourth consecutive week of outflows. Bitcoin investments fell by $38 million, while Ethereum rose by $0.1 million. Investments in bitcoin short funds fell by $10 million.

News background

According to a Bloomberg survey, Bitcoin has become one of the three most attractive assets amid default risk in the US. About 10% of US investors said they would hedge their risks by buying the first cryptocurrency. The first two positions were taken by gold and US government bonds.

According to Kaiko, the correlation between Bitcoin and Ethereum exchange rates has declined for over two months and fallen below 80%. This is the lowest level in a year and a half. This is due to the banking crisis in the US, which has led to an increase in investment in safe-haven assets, including BTC.

According to Glassnode, the number of investors with 1 BTC or more has exceeded one million.

The popularity of Bitcoin Ordinals and BRC-20 tokens will fade in a few months as they overload the blockchain and lead to higher transaction fees, says JAN3 CEO Samson Mow.

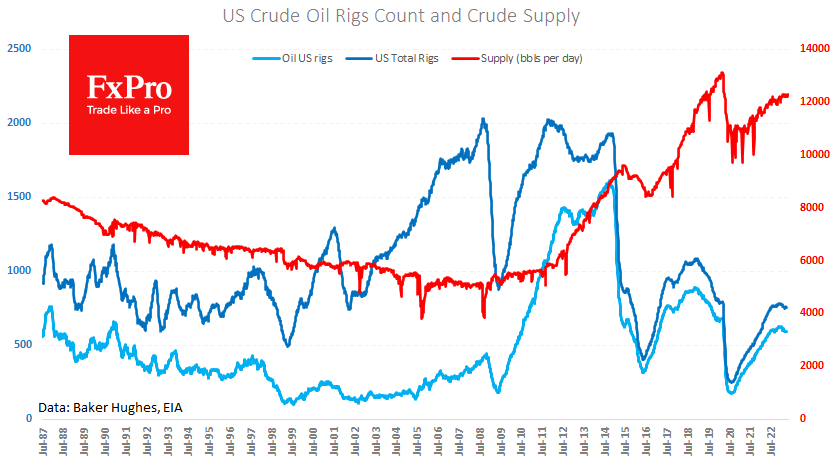

Oil Under Pressure, But Downside Limited

WTI crude oil rebounded on Monday after three sessions of declines in the second half of last week. Oil found support just before the start of active trading in Europe after falling to a 10-day low of $69.40.

Today’s pullback is still within the recent downtrend. Behind the buying is Friday’s data showing a further drop in the number of rigs operating in the US, from 748 last week to 731, the lowest since June last year and the continuation of the downtrend since November last year. This dynamic reflects doubts among US producers about maintaining and increasing oil supply over the six-month to one-year outlook.

However, while at the end of last year, this sentiment was influenced by fears of a recession in the developed world, it is now more a reaction to deteriorating financial conditions.

Another explanation from oil producers is worth considering. Over the past five weeks, the US government has returned to selling oil from the Strategic Petroleum Reserve, discouraging producers from making new investments as it tends to lower final prices. Late last week, administration officials confirmed their intention to return to replenishing the reserves this coming summer, but this is not the first time that date has been pushed back.

The sharp fall in oil prices, which peaked at the start of trading on 4 May, looked like a turning point for the market. However, buyers failed to provide sufficient traction, and the pressure on prices soon returned, briefly pushing prices back below $70.

Judging by the emerging short-term technical picture, it is better to be prepared for another test of the $65-67 per barrel WTI area. However, we expect oil to stay within this level, given the monumental task of replenishing US reserves and replacing Russia’s share of oil, shifting the supply/demand balance in favour of the former.