Sample Category Title

Silver Price Breaks February Resistance Line

As seen on the XAG/USD chart, silver has today breached the upper boundary of the descending channel formed by February’s lower highs and lows.

Bullish sentiment is supported by heightened geopolitical tensions and rising demand for safe-haven assets. According to media reports:

- → On Thursday, US President Donald Trump warned Iran that it must reach an agreement on its nuclear programme, or “really bad things” would happen, setting a 10–15 day deadline.

- → In response, Tehran threatened retaliatory strikes on US bases in the region if attacked.

On 11 February, analysing the XAG/USD chart, we noted that silver was consolidating between two key levels:

- → resistance around $87.5–95

- → support near $70

Today’s bullish breakout of the channel’s upper boundary – which acted as resistance in February – can be interpreted as a move towards the $87.5–95 zone.

Confidence for bulls is further reinforced by an inverted head and shoulders (SHS) pattern. If buyers are determined, this should be confirmed by XAG/USD holding above:

- → the channel breakout level near $79

- → the psychological $80 mark.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

The Market is Seeking a Haven

- JPY and EUR are giving back their safe-haven status to USD.

- USDJPY is rising amid slowing Japan inflation.

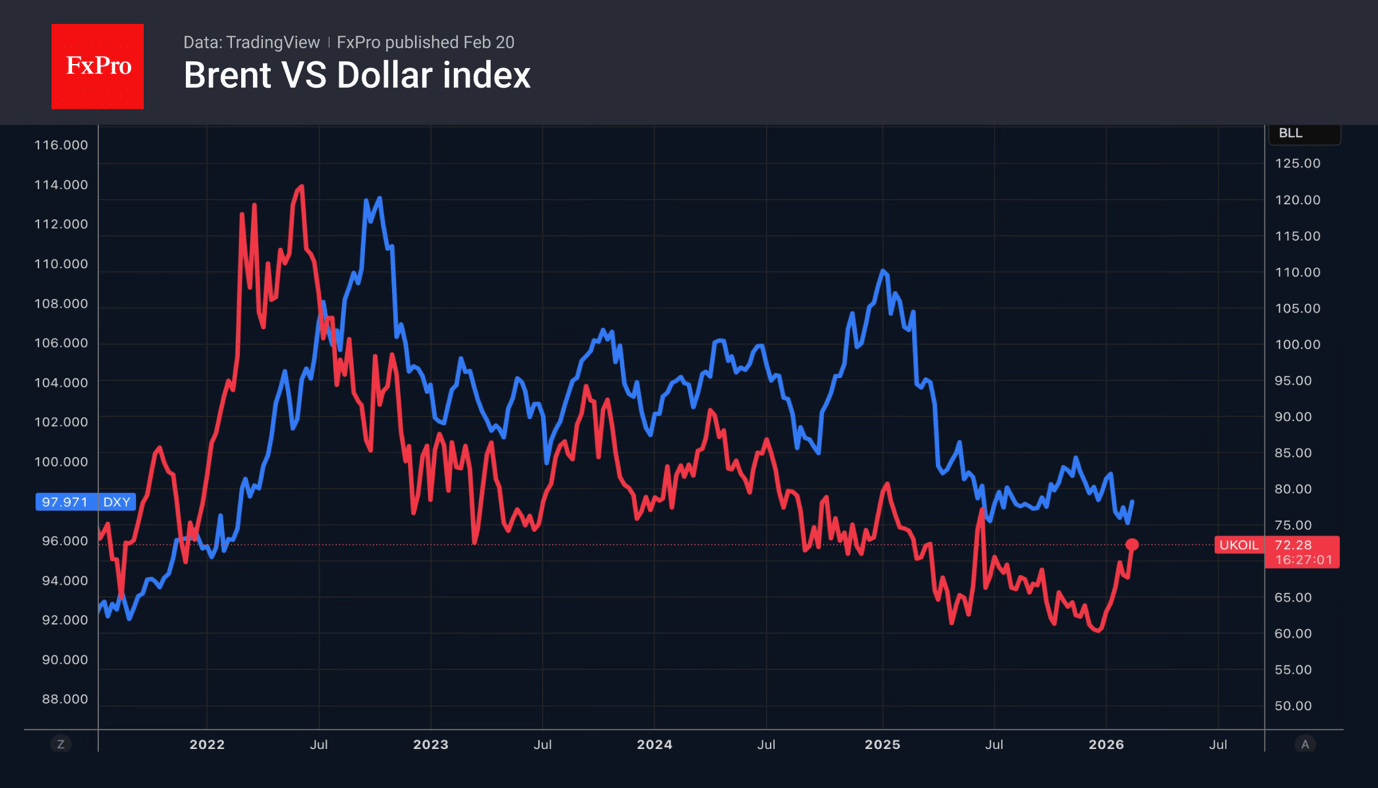

Growing geopolitical tensions in the Middle East and the Fed’s reluctance to resume its cycle of monetary expansion are driving the US dollar towards its best weekly performance in four months. According to a Wall Street Journal insider, Donald Trump is weighing a military strike on Iran to force it to sign a nuclear deal. If that doesn’t work, the US will launch a large-scale regime change campaign.

Fears of an escalation of the Middle East conflict have pushed Brent prices to six-month highs. Investors are rushing to buy safe havens. Suddenly, on Forex, one cannot find a better option than the US dollar. The yen and the euro are unable to compete with the greenback. The rise in oil prices will hit Japan and the eurozone, which are heavily dependent on energy imports.

Meanwhile, the drop in jobless claims has become another argument in favour of stabilisation in the US labour market. According to Stephen Mirman, the economy looks better than he had expected, so the Fed might lower rates by 100 bp this year to 2.75%, not by 150 basis points. San Francisco Fed President Mary Daly believes that the Fed should not hold back the economy with high interest rates. However, it should not lower them too much due to still high inflation.

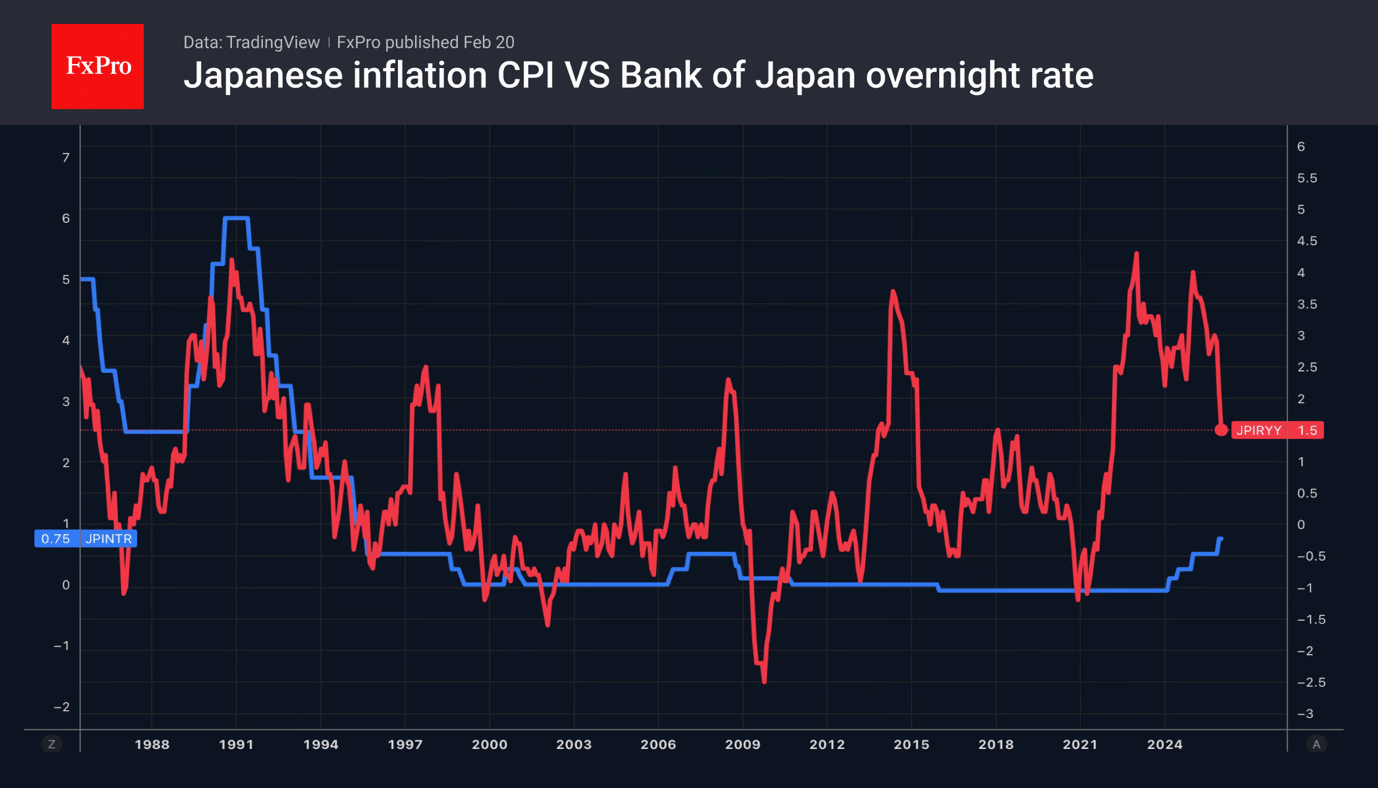

The fall in consumer prices in Japan to 1.5%, the lowest level since March 2022, added fuel to the USDJPY rally. The slowdown in inflation allows the central bank to take its time with raising rates. At the same time, this gives Sanae Takaichi a free hand in expanding fiscal stimulus. The prime minister intends to address parliament and outline her economic policy. Investors fear that excessive stimulus will revive the “Takaichi trade” and sink the yen.

Gold is behaving unusually. It rose on the back of the hawkish surprise in the minutes of the January FOMC meeting, the strengthening of the dollar and the fall in US Treasury bond yields. At the same time, the escalation of the geopolitical conflict in the Middle East is not particularly inspiring for gold bulls.

The volatility of the precious metal remains excessively high, and it is awaiting an influx of speculative demand from China after the Lunar New Year celebrations.

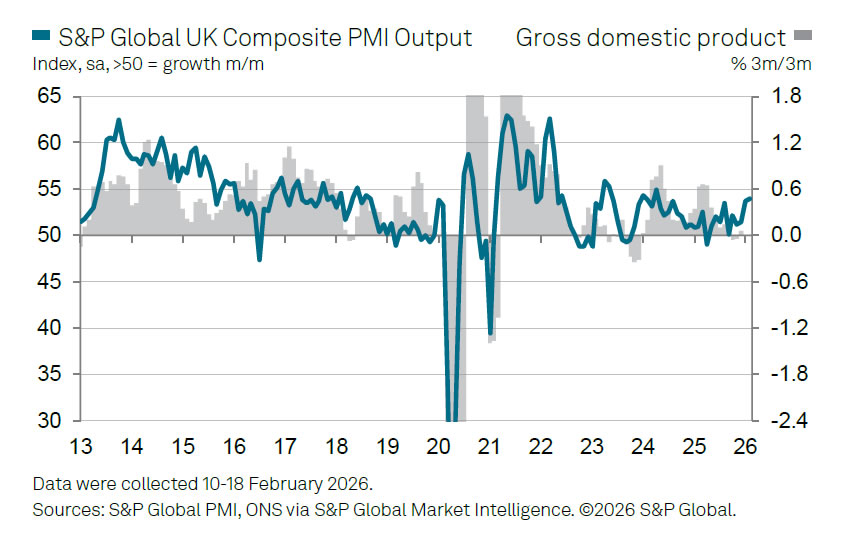

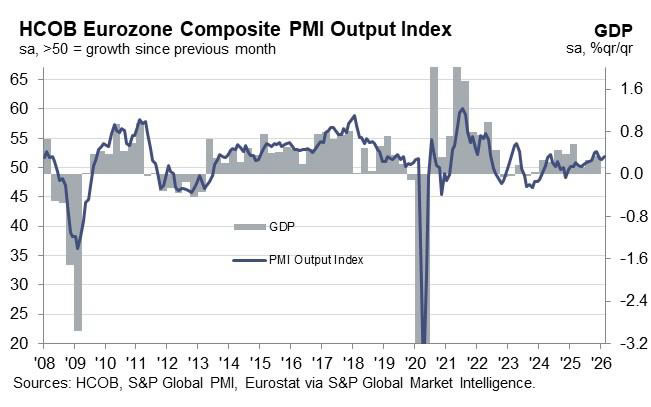

UK PMI composite rises to 53.9, consistent with over 0.3% Q1 GDP growth

UK business activity continued to expand in February, with PMI Manufacturing rising from 51.8 to 52.0, marking an 18-month high. PMI Services edged slightly lower from 54.0 to 53.9. PMI Composite improved from 53.7 to 53.9, reaching its strongest level in 22 months.

According to S&P Global’s Chris Williamson, the data point to an "encouraging start" to the year. Output growth across both manufacturing and services has accelerated in January and February. Current readings are consistent with GDP rising just over 0.3% in the first quarter if momentum carries through March.

For the BoE, while firmer activity will be welcomed, relatively modest price pressures and ongoing labor market weakness may keep pressure on BoE to consider further easing.

BTC/USD Analysis: Are the Bulls Stirring?

According to media reports, Bitcoin’s fall from its all-time high in October 2025 to February’s low near $60k triggered the largest outflow from spot Bitcoin ETF funds since their launch in January 2024.

Glassnode data show that more than 100,000 BTC were withdrawn from these funds in January alone, though the total remains substantial, with roughly 1.25 million coins still held on balance sheets.

Analysing trading volumes on Coinbase, however, reveals a trend of declining activity (as indicated by the arrow). From a long-term perspective, this may suggest the ETF outflow trend is easing, potentially allowing the market to resume its multi-year uptrend. How plausible is this scenario?

Technical Analysis of BTC/USD

Bitcoin’s price fluctuations are currently compressing between the thick lines on the chart – a sign of market stabilisation, where supply and demand appear balanced.

Notable bullish patterns include:

- A double bottom (A1–B1) on 11–12 February, aligning with the lower boundary of the long-term descending channel.

- A second double bottom (A2–B2) on 18–19 February, featuring a slightly lower secondary low.

In the short term, traders might anticipate a rebound towards the upper boundary of the triangle. While the descending channel remains relevant, a decisive bullish break of this consolidation pattern would signal improving sentiment in the crypto market following February’s panic selling.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service (additional fees may apply). Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

GBP/USD: Slide Enters Fifth Consecutive Day

GBP/USD fell for the fifth consecutive day, reaching 1.3445. The slowdown in headline price growth has boosted expectations of an imminent rate cut by the Bank of England, although underlying price pressures remain robust.

Annual inflation in January slowed to 3.0% from 3.4% in December, in line with forecasts. However, inflation in the services sector, which reflects domestic price pressures, only fell to 4.4% from 4.5%, above the expected 4.3%. This partly supported the pound. Earlier, sterling had fallen after weak labour data raised expectations of a rate cut.

According to Chris Turner, Head of Global Research at ING, the market had been counting on a more pronounced slowdown in inflation, but the data were not unambiguously weak. A better-than-expected figure for services gave sterling "only limited respite."

Investors now price the chance of a 25bp rate cut by the Bank of England next month at around 85%. By the end of the year, the market fully prices in two 25bp reductions.

The political situation remains an additional factor of uncertainty. The upcoming parliamentary by-election in Greater Manchester could reignite discussions about Prime Minister Keir Starmer's leadership in the event of a Labour defeat. According to ING, a major loss for the party could increase pressure on the pound and the government bond market.

Technical Analysis

The H4 chart maintains a pronounced downtrend. After a series of lower highs, the pair broke through the 1.3490–1.3500 zone and accelerated its decline to 1.3430–1.3440. The price moves along the lower band of the Bollinger Bands, confirming the dominance of sellers.

Local rebound attempts remain weak and are quickly sold into. The nearest resistance stands at 1.3490–1.3520, followed by 1.3660. Support is at 1.3430; a break below would open the path to further losses.

The H1 time frame shows a sharp sell-off on 19 February, followed by narrow consolidation at the lows. The Bollinger Bands have begun to narrow, suggesting volatility is easing after the recent sharp move.

The price is holding near 1.3430–1.3450. A sustained move above 1.3490 would allow for a more pronounced corrective pullback. The bearish scenario remains intact while the pair trades below 1.3490.

Conclusion

In summary, GBP/USD remains entrenched in a sustained downtrend, extending its losing streak to five sessions. While headline inflation softened as expected, sticky services inflation and resilient underlying pressures complicate the BoE's policy calculus. The market remains firmly priced for a March rate cut, with political risks adding to the uncertainty. Technically, the pair has breached key support and trades with a clear bearish bias. Any corrective bounces are likely to be capped near 1.3490–1.3520, with a break below 1.3430 opening the door to deeper losses. The near-term outlook remains firmly negative unless prices can reclaim the 1.3490 level.

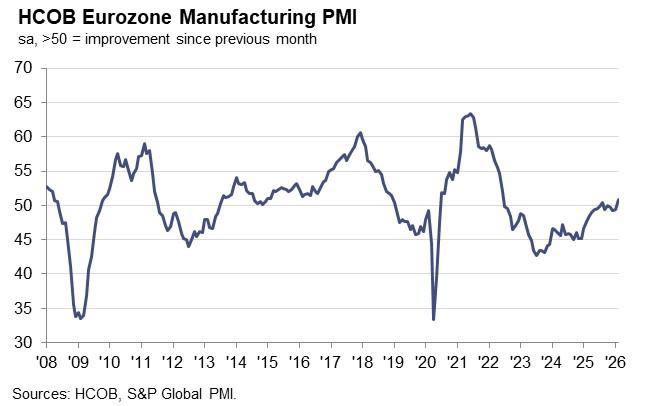

Eurozone manufacturing returns to growth, PMI hits 44-month high

Eurozone PMI Manufacturing rose from 49.5 to 50.8 in February, moving back into expansion territory and reaching its highest level in 44 months. PMI Services edged up from 51.6 to 51.8. PMI Composite climbed from 51.3 to 51.9.

According to Hamburg Commercial Bank’s Cyrus de la Rubia, this could mark a potential "turning point" for the manufacturing sector. Manufacturing has been a persistent drag since mid-2022, and although the index briefly crossed 50 last August, this time the foundation appears stronger. New business improved across both manufacturing and services, pointing to continued expansion in coming months.

Germany is playing a central role in the improved outlook. Higher public spending on infrastructure and defence, along with firmer external demand, are supporting industrial activity. However, de la Rubia cautioned that overall growth momentum has softened slightly compared with the fourth quarter, suggesting expansion remains moderate rather than accelerating.

Price pressures in services — closely watched by ECB — "relaxed a bit". Nevertheless, service inflation remains elevated enough to discourage a shift in policy stance. With activity stable and inflation not yet fully subdued, ECB appears inclined to keep rates steady for now.

Gold (XAUUSD) Signals Wave C Breakout

Gold has completed a 7-swing corrective decline in wave B at 4838 and has since turned higher, signaling the start of a new impulsive sequence in wave C. The reaction from 4838 was decisive, suggesting that the correction has likely ended and buyers have regained control of the short-term trend. Within wave C, we have already seen a clear five-swing advance in wave ((i)), confirming the impulsive nature of the move higher. Following that advance, the market is now correcting in wave ((ii)). At this stage, wave ((ii)) may have already completed; however, there remains a possibility of one more marginal low between 4966 and 4937 to complete a three-swing pullback from the recent peak.

As long as price remains above the wave B low at 4838, the overall outlook continues to favor further upside. The next key objective stands at 5339, which represents equal legs measured from the 4402 low. Reaching that area would complete the larger corrective sequence in proportional symmetry.

In the near term, pullbacks are expected to remain corrective, with wave C projected to extend higher toward the 5339 target. The broader structure supports continued upside while holding above critical support at 4838.

Gold (XAUUSD) 1-Hour Elliott Wave Chart From 2.20.2026

Gold Elliott Wave Video:

https://www.youtube.com/watch?v=DGGzkDt2rCE

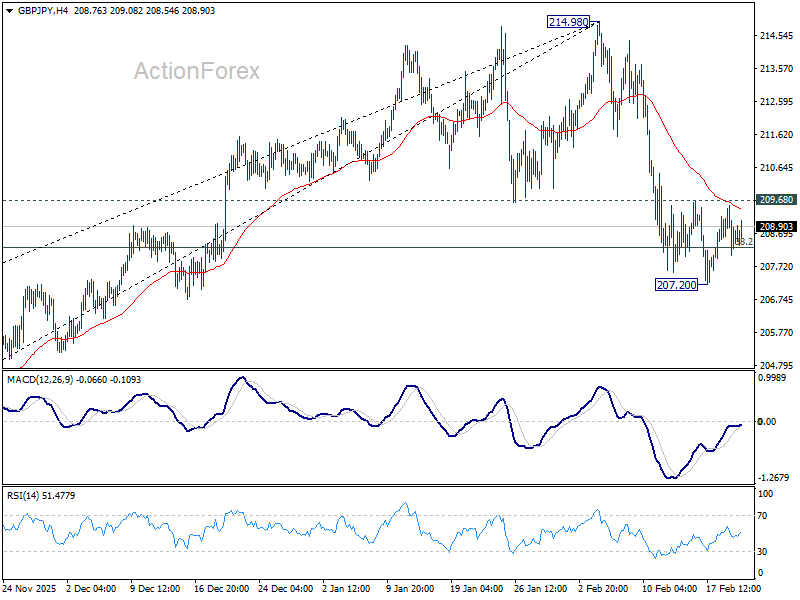

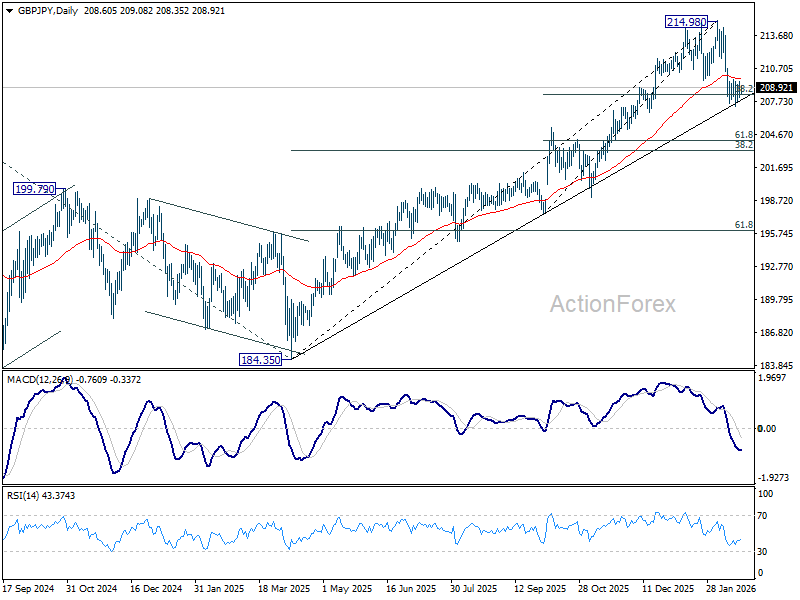

GBP/JPY Daily Outlook

Daily Pivots: (S1) 207.99; (P) 208.76; (R1) 209.45; More...

Intraday bias in GBP/JPY stays neutral at this point and outlook is unchanged. On the downside, sustained break of 38.2% retracement of 197.47 to 214.98 at 208.29 will suggest that larger scale correction is already underway and target 203.27 fibonacci level. Nevertheless, strong rebound from current level, followed by break of 210.47 minor resistance will retain near term bullishness, and bring retest of 214.83/98 resistance zone.

In the bigger picture, considering the break of 55 D EMA, a medium term top could be formed at 214.98. Deeper correction would be seen, but downside should be contained by 38.2% retracement of 184.35 to 214.98 at 203.27. On the upside, break of 214.98 will resume larger up trend from from 123.94 (2020 low), and target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90.

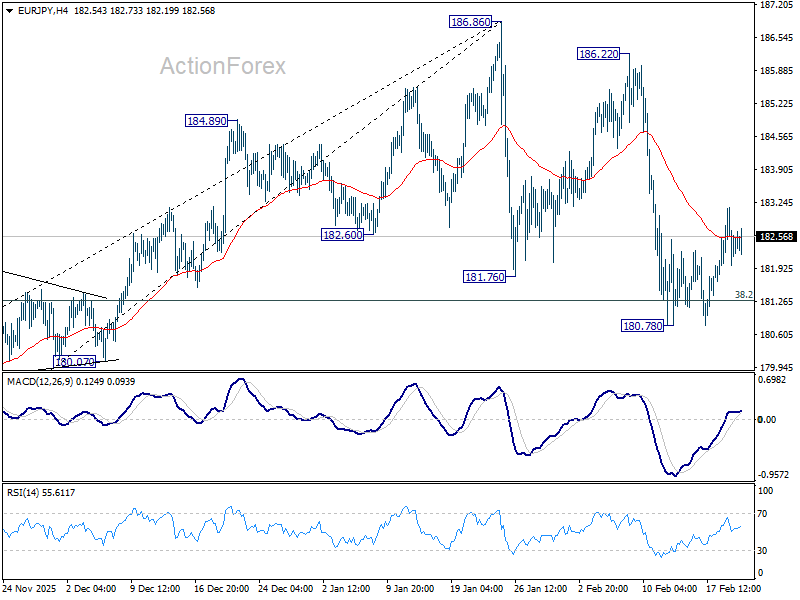

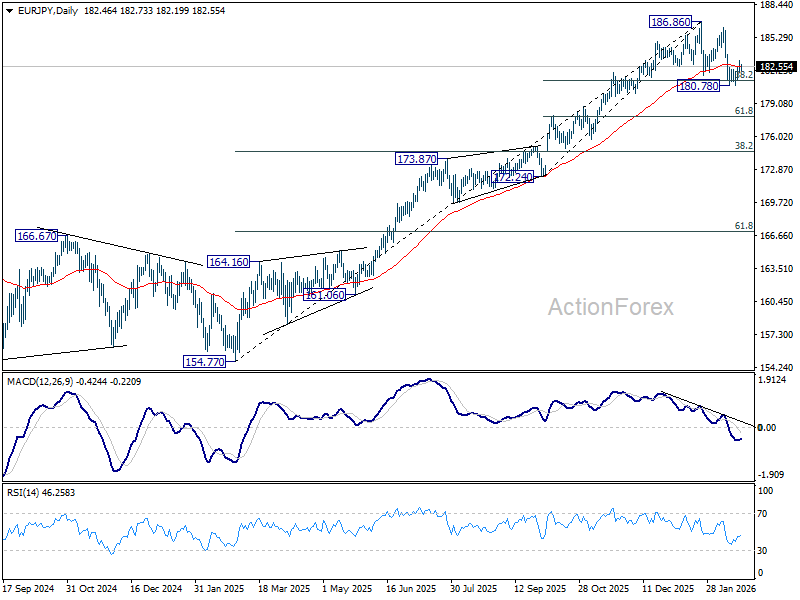

EUR/JPY Daily Outlook

Daily Pivots: (S1) 181.94; (P) 182.54; (R1) 183.08; More...

Intraday bias in EUR/JPY remains mildly on the upside for the moment. Corrective fall from 186.86 could have completed after drawing support from 38.2% retracement of 172.24 to 186.86 at 181.27. Further rise should be seen to retest 186.22/186.86 resistance zone first. One the downside, however, sustained break of 181.27 will argue that fall from 186.86 is correcting whole up trend from 154.77.

In the bigger picture, considering bearish divergence condition in D MACD and break of 55 D EMA, a medium term top could be formed at 186.86 already. Deeper correction would be seen but downside should be contained by 38.2% retracement of 154.77 to 186.86 at 174.60 to bring rebound. Meanwhile, firm break of 186.86 will resume larger up trend to 78.6% projection of 124.37 to 175.41 from 154.77 at 194.88 next.

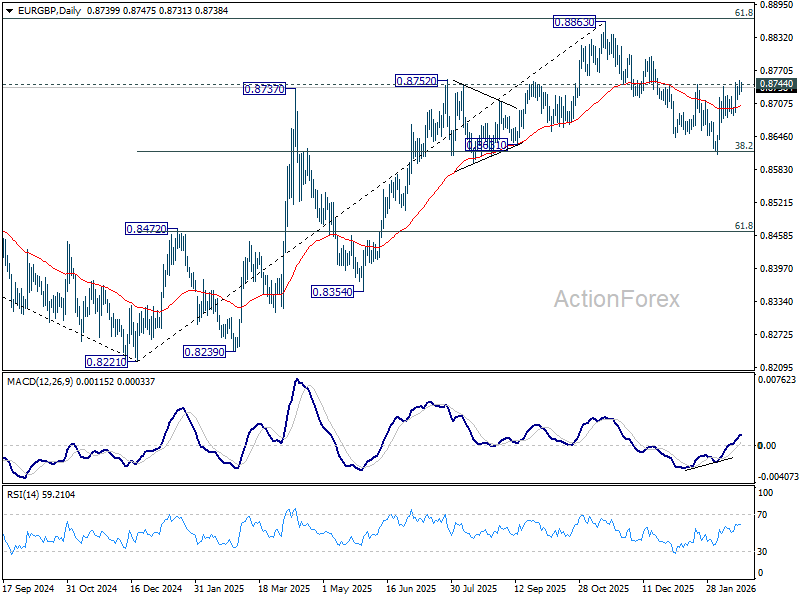

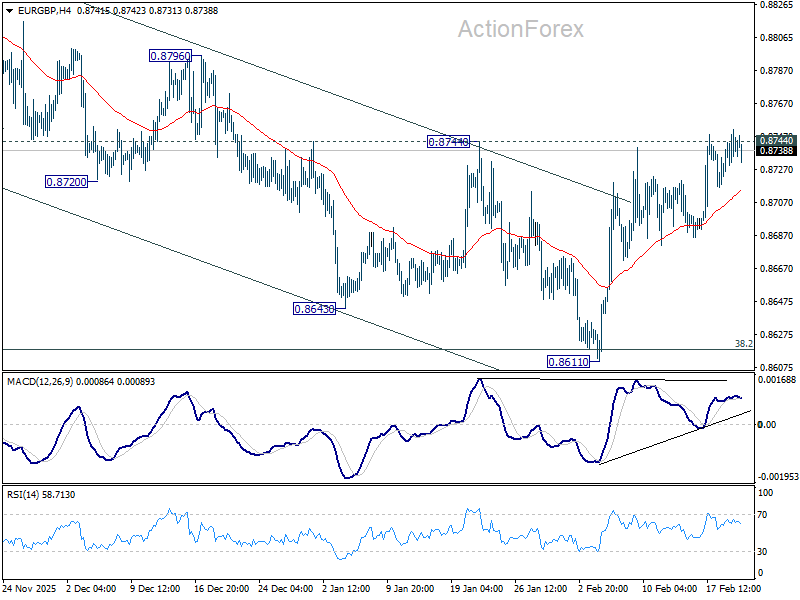

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8729; (P) 0.8740; (R1) 0.8756; More…

Intraday bias in EUR/GBP remains neutral with focus on 0.8744 resistance. Decisive break there should confirm that fall from 0.8863 has completed as a correction. Further rally should then be seen back to retest 0.8863 high. On the downside, sustained break of 38.2% retracement of 0.8221 to 0.8663 at 0.8618 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8631) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.