Sample Category Title

Weekly Economic & Financial Commentary: Broadening Drivers of Growth – Unpacking GDP and Looking Ahead

Summary

U.S. Week in Review:

- This week’s data delivered a familiar theme with an important twist. The U.S. economy continues to be shaped by powerful forces in high-tech and AI-related investment, but recent releases suggest the growth story may finally be broadening. At the same time, trade flows are moving in a less supportive direction, reminding us that not all parts of the economy are pulling in sync.

U.S. Week Ahead:

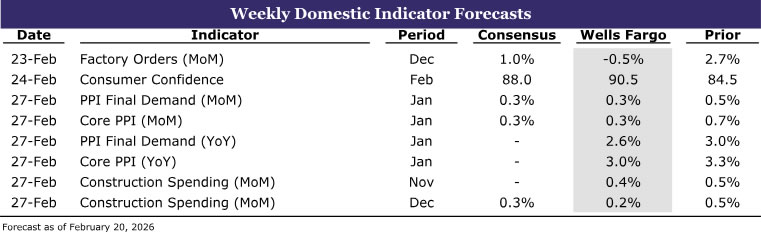

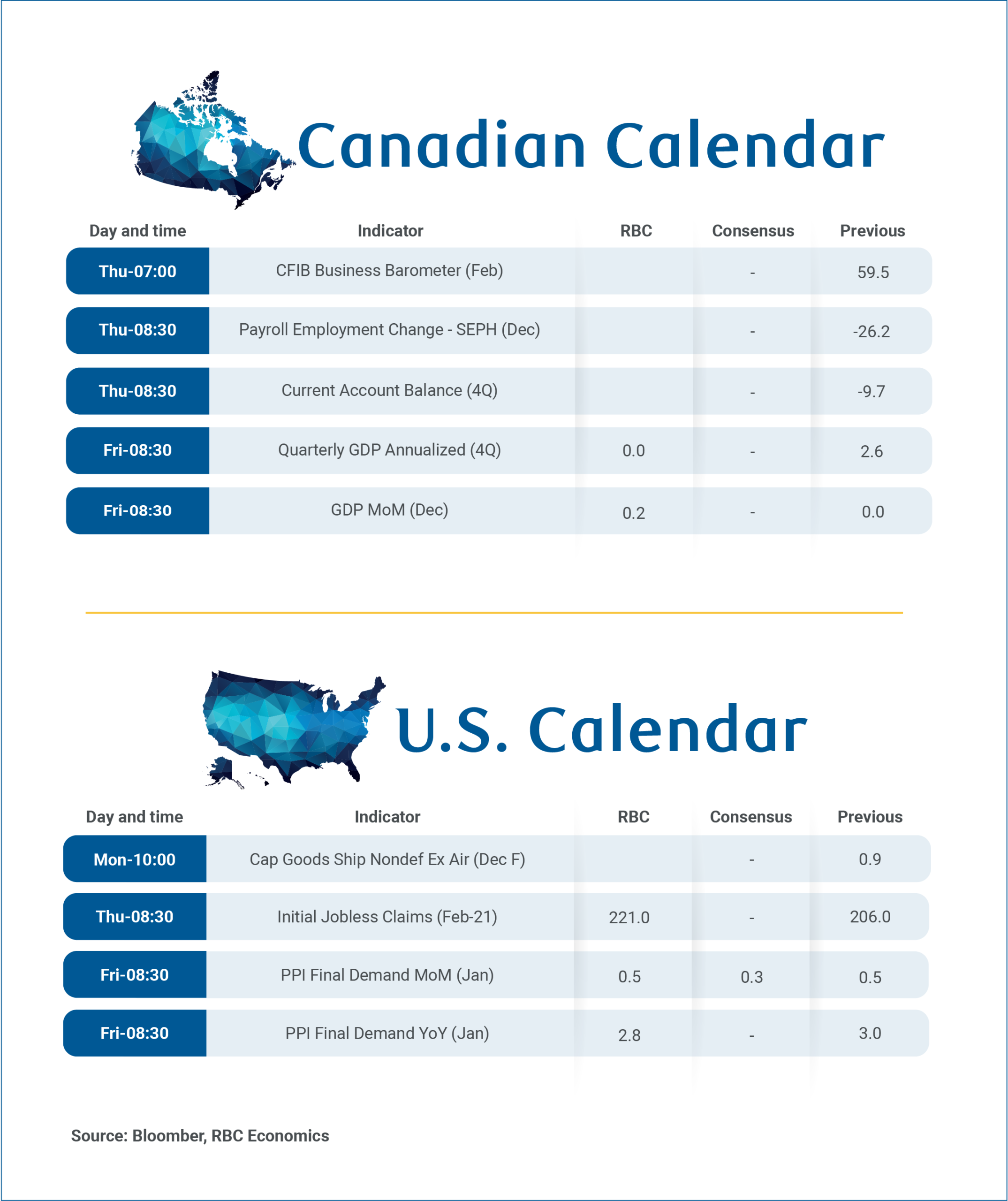

- Consumer confidence likely rebounded modestly in February after January’s decade low as cooler inflation and a better jobs report offered relief, even as high living costs and geopolitical risks persist.

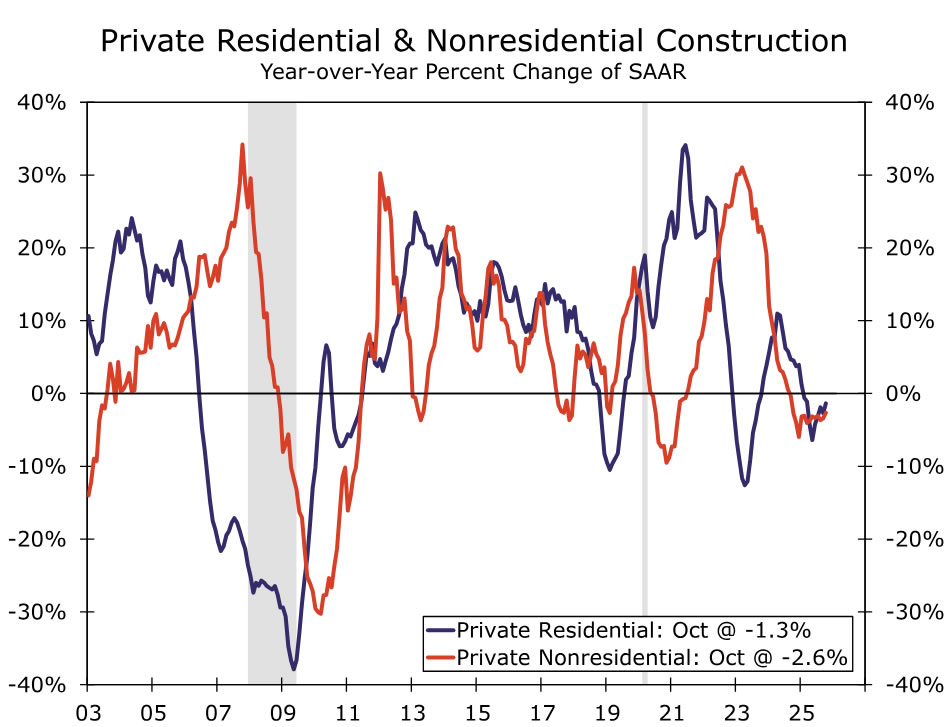

- Construction spending likely improved at year-end, though we expect the results to be mixed beneath the surface, with data center construction driving strength but continued weakness in residential and structures investment expected as high interest rates and economic uncertainty continue to constrain activity.

U.S. Week in Review

Broadening Drivers of Growth: Unpacking GDP and Looking Ahead

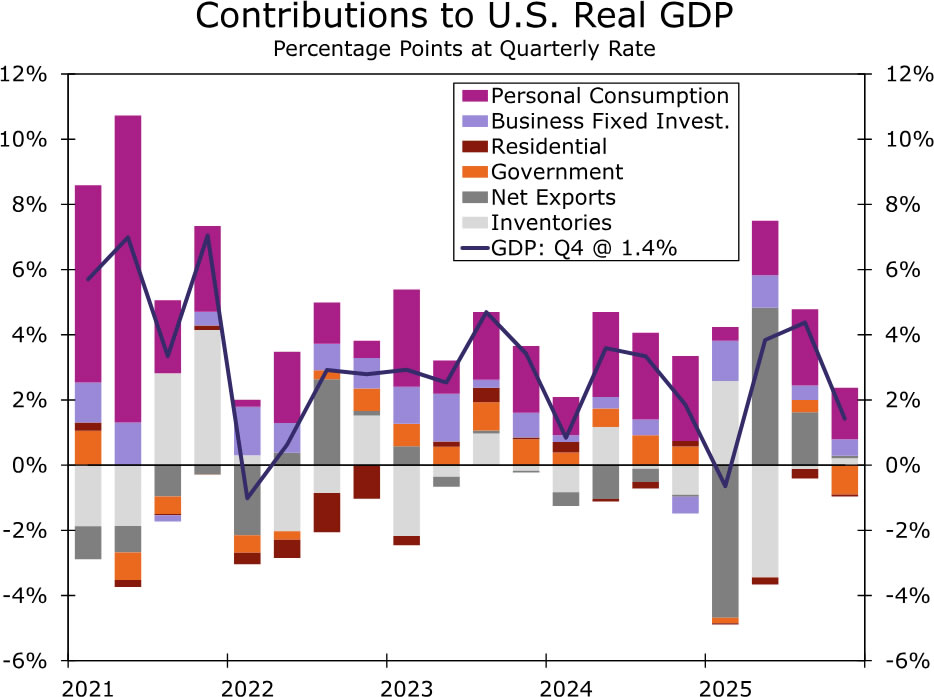

We had maintained a well-below consensus forecast for fourth quarter GDP and the official release this morning confirmed our suspicions that a government shutdown and a gold-excluded trade balance held back broader growth during the period. The annualized rate of GDP came in at just 1.4%, roughly half the 2.8% growth rate expected by the consensus.

Government spending, negatively impacted by the longest-ever shutdown, pulled growth lower by nine-tenths of a percentage point (chart). Net exports added less than a tenth of a percentage point (0.08) to the headline figure. Both commercial and residential fixed investment were slight drags during the fourth quarter as well.

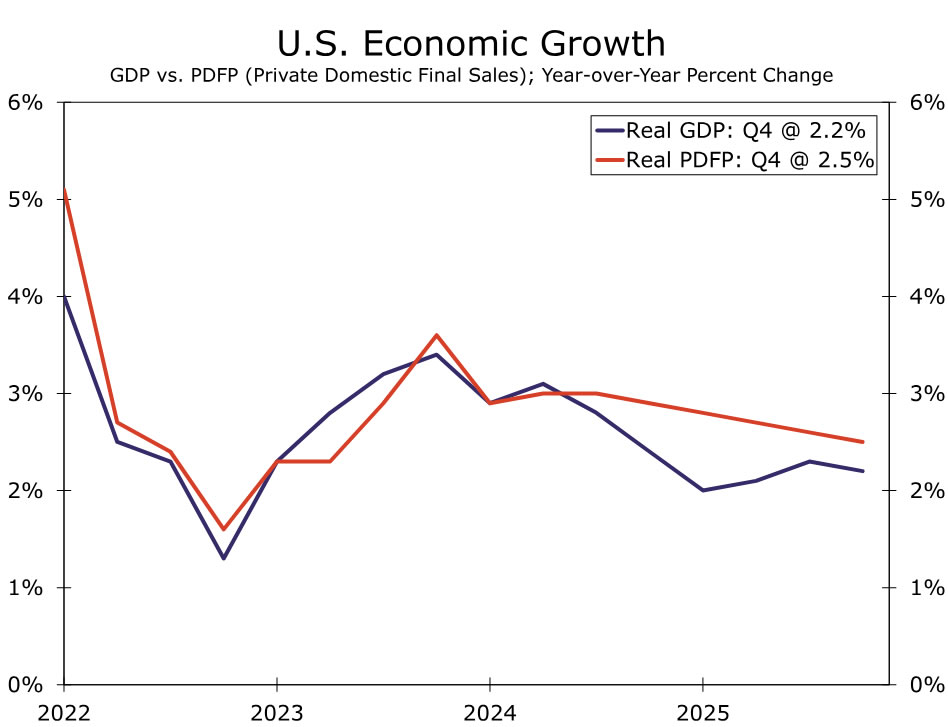

The growth drivers were largely consumer (which boosted growth 1.6 percentage points) and business fixed investment spending (which added 0.5 percentage points, even after accounting for the drag from structures). In terms of underlying U.S. growth, it was strong. We've emphasized this measure a lot throughout 2025: real final sales to private domestic purchasers, which removes government, inventories and net exports, the most volatile components this year. That measure was up at a 2.4% annualized clip in Q4 and 2.7% for the full year, only slightly below the pace registered last year, demonstrating a more stable growth picture (chart).

In plain English: If you exclude trade volatility and the associated impact on inventories, the overall economy is doing about the same as last year. Yet, for much of that period, resilience in business investment has been more optical than organic—a surge in AI and high-tech spending masking softness elsewhere. Orders, production, and imports tied to computers, communications equipment, and semiconductors have surged, while more traditional capital goods struggled to keep pace. This was true in Q4 as well where the 3.2% annualized pickup in real equipment investment was due entirely to stronger investment in information processing equipment, while other areas of capex (industrial, transportation, other) declined.

December durable goods orders and January industrial production also released this week hint that this imbalance may be starting to ease. Core capital goods orders stabilized, and shipments rose at a pace consistent with solid equipment investment growth. Stripping out the notoriously volatile aircraft category reveals modest but broad-based gains across most durable goods sectors, enough to handily exceed low expectations.

On the production side, manufacturing output rose at the fastest monthly pace in nearly a year. While high-tech continues to dominate in level terms, output excluding high-tech also posted its strongest gain in almost 12 months, reaching its highest index reading in more than two years. In short, the AI investment boom remains intact, but it is no longer the only game in town.

Supportive tax incentives and an early year pickup in commercial and industrial lending appear to be encouraging firms to finance projects beyond AI infrastructure. That shift matters: A more balanced capex cycle would make the expansion more durable and less dependent on a single sector carrying the load.

If investment and production offered a positive signal, trade delivered a counterweight. December saw a sharp widening in the trade deficit, driven by a large increase in imports alongside a decline in exports. On the surface, that combination pointed to a meaningful drag on fourth quarter growth. But digging deeper tempers the headline. More than half of the widening was due to non-monetary gold flows, which are excluded from GDP calculations and reflect asset reallocation rather than underlying production demand. Adjusting for gold significantly reduces the apparent deterioration in net exports, thus explaining the flat contribution to headline Q4 growth.

The trade data also underscore how much last year’s import weakness may have been overstated. Goods imports finished 2025 well below where they began the year, particularly outside of high-tech categories, but the evidence points more toward caution than capitulation. Firms appeared to adopt a wait-and-see approach amid tariff uncertainty rather than execute a wholesale restructuring of supply chains.

With inventories lean and little sign of large scale onshoring, there is scope for imports to rebound modestly this year—even if tariff rates remain elevated. Ongoing legal and policy uncertainty around tariff authority, as well as upcoming reviews of trade agreements, means trade policy will remain a swing factor, but not necessarily an ever-tightening constraint.

At the end of the day, consumers are still spending. Real personal consumption expenditures advanced at a 2.4% annualized rate in Q4, driven by solid services-sector demand, which offset a modest pullback in goods purchases. If you're looking for a sign of caution in the GDP data, we'd highlight the fact that the services resilience looks to be driven by non-discretionary categories like healthcare, housing & utilities and financial services. The more discretionary-oriented areas (transportation, recreation and food & accomodation) all lagged or posted modest growth rates. That development doesn't leave us overly concerned of a consumer pullback as we've cautioned of a soft finish, but it signals some stress in the consumer sector. We expect more favorable after-tax income growth and larger average tax refunds to help offset some of this household pressure this year.

Taken together, this week’s indicators tell a nuanced story. Beneath the noise, there are early and encouraging signs that investment and production growth are becoming more broad based, reducing the economy’s reliance on the high-tech sector alone. At the same time, trade is shifting from a big tailwind to a mild headwind for growth as imports normalize.

The message is not one of reversal, but of rebalancing. Momentum within the domestic economy is improving in a healthier way, even as external dynamics complicate the growth arithmetic. As we look ahead, the sustainability of the expansion will hinge less on a single sector’s boom and more on whether this nascent broadening continues to take hold.

U.S. Week Ahead

Consumer Confidence • Tuesday

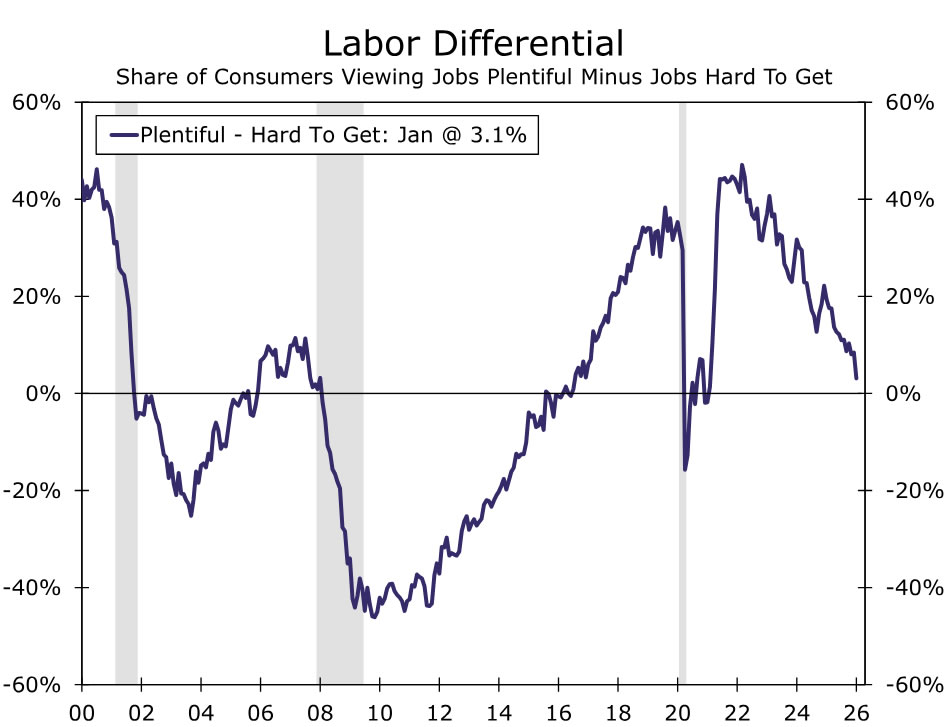

The Consumer Confidence Index fell to its lowest level in a decade in January, with a deterioration in the labor market, high living costs and geopolitical tensions contributing to the drop. The weakening jobs backdrop is particularly weighing on household sentiment: The labor differential fell to a post-pandemic low, with more consumers reporting jobs as "hard to get." While this alone is not enough to stop households from spending, it does result in more cautious spending behavior, especially for those with less discretionary income.

We look for a bit of payback in February's print and expect the index to rise to 90.5 from 84.5 previously. Though the labor market is far from perfect, the employment report for January was broadly encouraging, which will likely provide some relief to consumer's weakening views of the labor market. Likewise, the CPI report came in cooler than expected in January, which may also provide support to consumer confidence. That said, despite the more-positive month of data, persistent worries of tariffs, foreign interventions and high cost of living are likely not going away soon and will continue to weigh on consumer confidence.

Construction Spending • Friday

Construction spending declined 0.6% in September before rebounding 0.5% in October, making overall construction spending virtually unchanged since August. Private construction was the main drag, with residential and nonresidential outlays both declining on an annual basis. Single‑family residential spending fell sharply as builders pulled back amid high mortgage rates and elevated inventories, while at the same time manufacturing, commercial and healthcare construction also weakened. Multifamily spending stabilized after earlier declines, and public construction outperformed, rising year-over-year on gains concentrated in education, water and waste projects.

November and December construction spending data will be released next week, and we look for modest monthly increases of 0.4% and 0.2%, respectively. While there remains room for growth in areas such as data center construction, we look for continued near-term weakness in residential and structures investment as high interest rates and economic uncertainty continue to constrain activity.

Preserving CUSMA Exemptions: Canada’s Real Priority amid U.S. IEEPA Ruling

The U.S. Supreme Court ruling against broad tariffs imposed by the U.S. administration under the International Emergency Economic Powers Act (IEEPA) removes government authority to collect them going forward. Still, other legislative authorities are open for the administration to re-instate tariffs.

IEEPA measures accounted for about 60% of tariff revenue reported by U.S. Customs and Border Control in fiscal 2025 and 2026 to-date. The remaining 40% of revenue were collected via other statues including Section 301 and 232 that are not impacted by the ruling.

There are significant questions that also remain—including if or when tariff revenues collected under IEEPA will be repaid.

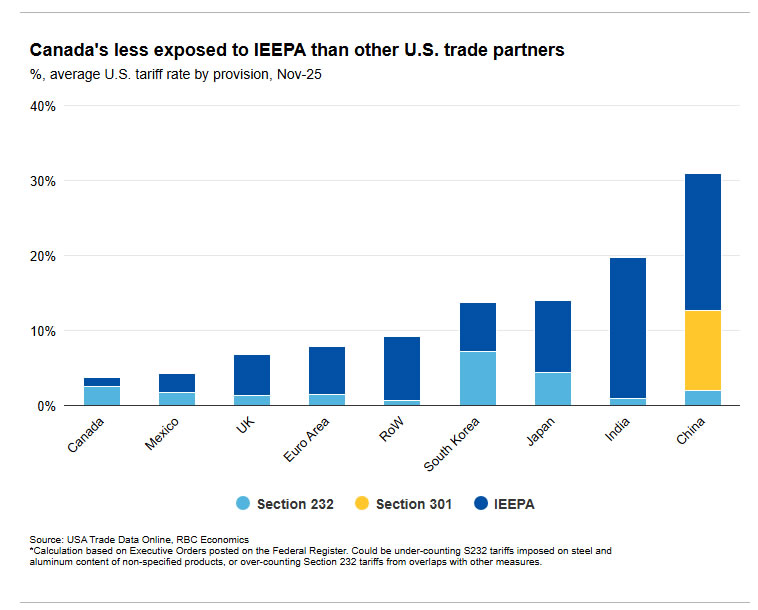

The ruling will have less impact on Canadian trade than most other countries. Most Canadian exports are already exempt from IEEPA tariffs via an exemption for CUSMA compliant trade.

Other product specific (section 232) tariff measures have been a larger issue for the Canadian economy and those were not impacted by the court ruling.

We continue to view maintaining free trade under CUSMA—including through negotiations to extend the agreement later this year—as more important for the Canadian external demand outlook than court rulings.

Our 2026 forecast rests on the key assumption that CUSMA exemptions will be preserved to maintain lower-friction bilateral trade with the U.S.

IEEPA ruling likely won’t meaningfully change Canada’s tariff backdrop

The U.S. administration has vowed to re-instate tariffs if IEEPA measures are struck down. Statutorily, there are various other channels that allow them to do so.

In the meantime, non-IEEPA measures that account for about half of U.S. tariffs in place prior to the ruling remain unaffected by the court decision.

Other measures, including Section 232 tariffs imposed on a key range of Canadian products like metals, autos, and lumber, accounted for the bulk of duties collected from Canadian exports so far. Importantly, these measures were not under review by the U.S. Supreme Court.

Source: USA Trade Data Online, RBC Economics

*Calculation based on Executive Orders posted on the Federal Register. Could be under-counting S232 tariffs imposed on steel and aluminum content of non-specified products, or over-counting Section 232 tariffs from overlaps with other measures.

Canada has limited exposure to IEEPA tariffs

By our count, 89% of Canadian exports to the U.S. in December were not charged with tariffs because they’re compliant with rules of origin requirements in CUSMA.

That leaves IEEPA measures only effective on less than 5% of exports to the U.S. In December (with the remainder accounted for by Section 232 tariffs), Canada faced an average effective U.S. tariff of 3.1%—the lowest of all major U.S. trade partners.

Moving forward, there are reasons to be optimistic that exemptions will remain in place, largely because they benefit businesses on both sides of the border.

We counted in the past that they effectively lower the U.S. average tariff by 6%, particularly benefitting importers in the 22 U.S. states where Canada is the largest source of imports as of 2025. Still, potential for changes remains a key risk to our baseline forecast.

Canada may lose advantage globally but could see increased U.S. demand

For other major U.S. trade partners (outside of Mexico, which also benefits from lower tariffs thanks to CUSMA/USMCA exemptions), IEEPA tariffs tend to account for the majority of U.S. tariffs, making the Supreme Court ruling more consequential.

If IEEPA tariffs are not replaced, other countries could see significant tariff reductions, and Canada could lose status as the lowest tariffed U.S. trade partner. On the flip side, U.S. tariffs will be halved, leading to increases in U.S. industrial activity and foreign demand.

We continue to view Canada’s international trade risks as a function of one: Canada’s competitive position in the U.S. import market; and two: broader, overall resilience in U.S. import demand tied to the severity of tariffs—the removal of IEEPA tariffs (if not replaced) is actually a negative for the former, but would be a positive for the latter, balancing the impact of the IEEPA ruling on Canada’s economy.

Stronger Growth in December Likely Left Canadian GDP Flat in Q4

The U.S. administration’s response to the Supreme Court’s ruling against IEEPA tariffs could overshadow economic data releases in the week ahead. We have noted before that the government has multiple options to reimpose those measures using other legislation.

And, in Canada’s case, an exemption for CUSMA compliant trade means most exports were already exempt from IEEPA tariffs with product specific section 232 tariffs (not impacted by the ruling) the main source of tariffs on Canada (Issue in Focus for more).

We continue to view maintaining CUSMA-related exemptions more important for Canada than the IEEPA ruling itself.

Canadian GDP growth appears to have stalled in Q4

International trade uncertainty and volatility has been a persistent feature in the growth backdrop over the last year, but we expect a flat Q4 gross domestic product reading for Canada next Friday was in part due to temporary disruptions in the economy with signs of stronger activity late in the quarter.

Following two soft growth prints in October and November, we expect a 0.2% increase in December that would be slightly above Statistics Canada’s 0.1% advance estimate. That would leave Q4 tracking close to our (and the Bank of Canada’s) forecast for no growth after a 2.6% annualized increase in Q3.

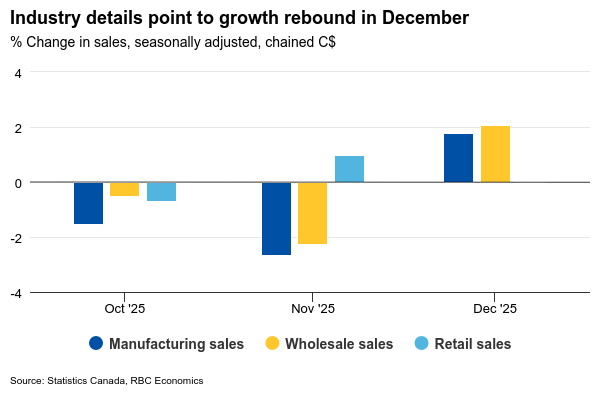

The silver lining to a soft looking quarter is that most of the weakness was concentrated in October and November with industry reports for December mostly positive.

Manufacturing and wholesale sales surged 2.1% and 1.8%, respectively, as auto production bounced back from disruptions related to a semi-conductor shortage in November. Education services in December likely recouped more of the weakness from Alberta’s teachers’ strike in October after a partial bounce back in November.

Those disruptions—along with impact from a postal strike in October—combined to subtract almost three-quarters of 1% from annualized Q4 GDP growth, according to our estimates.

Still, soft spots remain. The manufacturing sector continues to struggle from U.S. tariffs. Home resales pulled back in December (and again in January), and retail sales were unchanged from November.

Rise in business investment but residential likely fell

We expect to see a pick-up in business investment in Q4 as key indicators like electrical equipment and parts’ imports rose.

Moderating trade uncertainty likely helped with stabilizing sentiment and investment intentions. Most companies surveyed in the BoC Q4 Business Outlook Survey didn’t expect further deterioration in the tariff and trade backdrop going forward.

Residential investment likely contracted after bigger increases in Q2 and Q3, given declines in home resales, construction and housing starts in Q4. Elsewhere, household consumption and net trade likely grew modestly although our tracking of RBC card spending data pointed to a drop-off in consumers’ buying momentum (especially among discretionary items) in January.

The BoC already assumed flat Q4 GDP in their January forecasts, and much of the weakness appears to have been due to one-off factors. In the meantime, labour markets continue to show signs of improving with the unemployment rate broadly edging lower.

With interest rates already bordering stimulative levels, we don’t think it’s likely or necessary for the central bank to cut again.

GBP/JPY Marks a Major Top – Will It Revert to 200.00?

GBP/JPY is a historically popular pair in Forex trading, as it is one of the most volatile products to trade and captures geographic dynamics and risk-on/risk-off flows.

The pair once again stands at a key inflection point, right after a historic run back to 2008 levels, and can offer quite interesting setups amid elevated market volatility.

It can be affected by recent tariff developments, as GBP has a historical correlation with Equity markets. Hence, if Markets rally after the tariff cancellation, GBP/JPY can retest recent highs.

However, bearish Stock Markets could bring the pair back to 200.00, a 9,000-pip move from current levels, if geopolitical developments sour sentiment.

After an insane run on the Yen throughout the latter part of 2025, the landmark victory in Japanese snap elections brought some confidence in the currency and calmed the spikes in long-end yields.

On the other hand, Sterling could be facing some weakness ahead. The UK reported the highest unemployment rate since 2021, and with a relatively cooling Inflation Rate (still too elevated for the Bank of England), the Central Bank might be inclined to cut.

With Rate differentials converging and sentiment souring, GBP/JPY could be facing a significant reversal in the coming times. The challenge for FX traders will be to capture the trade optimally.

Let's dive into a multi-timeframe analysis and technical levels for GBP/JPY, which could soon be subject to intense volatility.

GBP/JPY Multi-timeframe Technical Analysis

Daily Chart

GBP/JPY Daily Chart, February 20, 2026 – Source: TradingView

The pair is consolidating at the lows of its Mid-2025 channel that took the pair back to 2008 highs.

Momentum cool downs are common after such gigantic moves, but with recent Market developments, the action could soon get spicy.

As GBP/JPY tests its Pivot Zone, let's take a look closer at what could tilt the scales.

4H Chart and Technical Levels

GBP/JPY 4H Chart, February 20, 2026 – Source: TradingView

The action recently formed a major intraday resistance (209.50 to 210.00) right at the beginning of its Pivot zone, leaving two potential scenarios:

- With recent rejection of resistance, sellers are attempting to take the upper hand

- Look for a break of the intraday upward trendline.

- Closing below the trendline should see a swift test of February lows at 207.240.

- Breaking this could see acceleration towards the 205.00 Pivotal Support.

- Watch out as these targets are quite far and closer profit-taking could maximize the chance to secure trading profits.

- Any break and session close above 210.00 will give more chances to test the 50-Day MA and top of the Daily Pivot Zone (210.90 to 211.00) – Lower probabilities in the current course of action

Levels to watch for GBP/JPY trading:

Support Levels:

- 208.80 Countertrend micro-support (if break, bears take the hand)

- 208.120 July 2024 highs mini-support

- 207.50 to 208.00 2024 July highs – recent test

- Post-Takaichi Election highs 205.00 – Pivotal Support (breaking this opens the door to 200.00

Main Key Support 199.00 to 200.00

Resistance Levels:

- 209.50 to 210.00 Major Intraday Resistance

- 210.90 50-Day MA

- 212.00 to 213.00 resistance

- Early February 16 year highs 214.834

1H Chart

GBP/JPY 1H Chart, February 20, 2026 – Source: TradingView

With recent rejection of the intraday resistance, a bearish move could appear.

- Watch out for weekend volatility which could lead to spikes at the Sunday Globex open (hence requiring larger stops, make sure to respect your risk-tolerance in that aspect).

To confirm the reversal, traders will want to see a break of the trendline.

- On the other hand, bouncing higher from here and closing above the Intraday resistance would point to higher odds of testing the 50-Day MA.

Safe Trades!

US Supreme Court Strikes Down Trump Tariffs

The U.S. Supreme Court has officially struck down the Trump administration’s global tariffs, ruling that the executive branch exceeded its authority under the IEEPA.

For now, the action remains very muted across FX, Stocks, and Crypto Markets, which are all close to unchanged on the session.

Only Metals are rallying, but that would mainly reflect weekend risk, if anything, and they actually faded their up-move on the Decision.

You can get access to the Full text of the Supreme Court decision right here.

Stocks spiked on the announcement, but the move isn't looking like it will sustain, at least for now.

Overall, Markets are not reacting much for now because the Decision was largely priced in.

What could affect flows going forward is how the Trump Administration responds – they have been prepared for this issue, so what's coming next is still uncharted territory.

Dow Jones 15M Chart – Source: TradingView. February 20, 2026

Safe Trades!

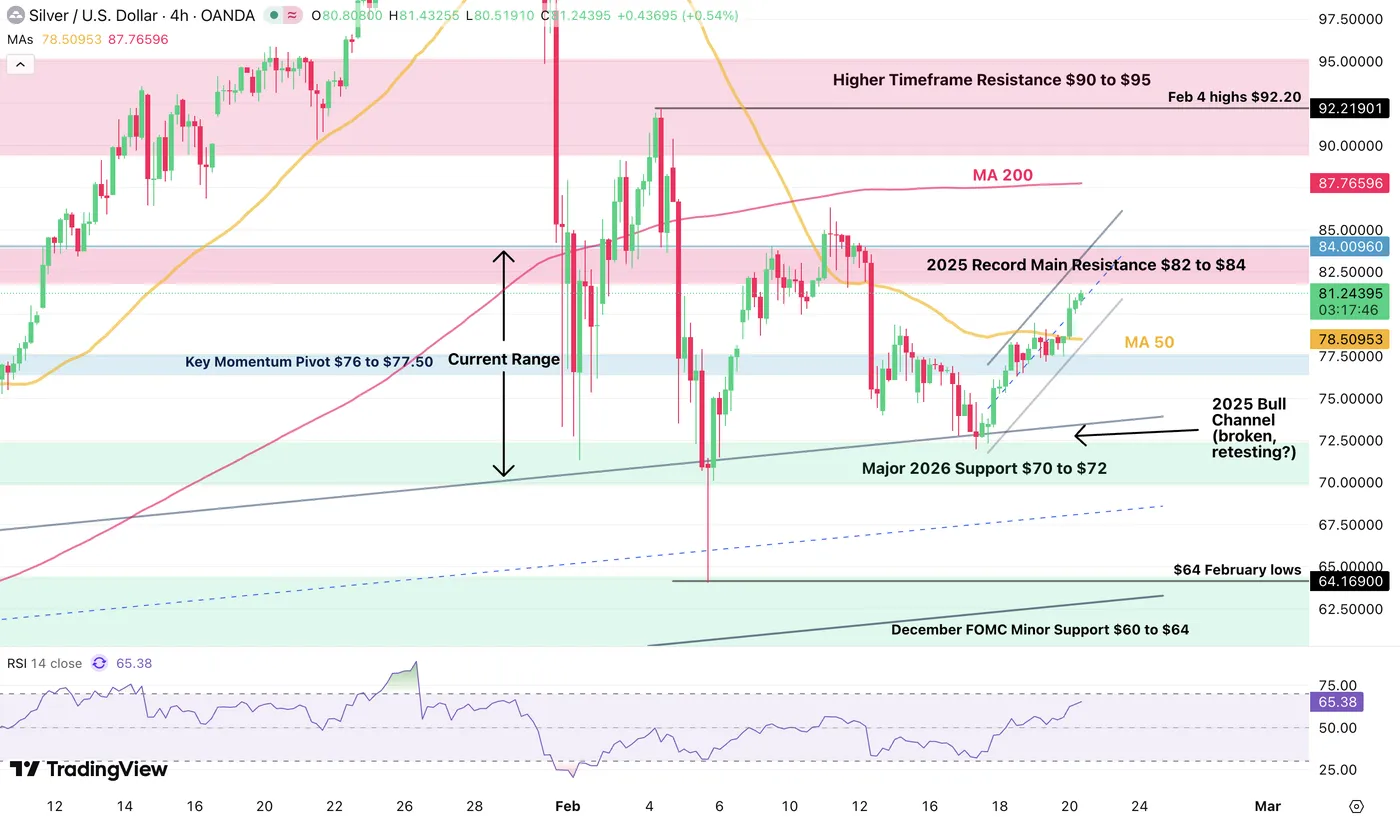

Silver (XAG/USD) Rallies Back Above $80, More Incoming? – Technical Outlook

Metals are slowly recovering after their high-paced deleveraging from late January trading.

Establishing consolidative ranges and holding tight right around their 2026 opening levels, the Precious Commodities are facing key technical tests in their historic runs.

Indeed, after their shocking up-and-down performances in the first two months of the year, it is even more astonishing to see that they are mostly back to where they were before year-end, with Gold leading the pack with more modest 16% gains (check out their yearly performance right here).

Metals performance in today's session – Source: Finviz. February 20, 2026

As speculation tones down, up sessions have been much more contained, which bodes well for a more stable price action ahead. Ranging between 2% and 3%, the daily rally in metals changes from the +10% ranges that almost became the new normal throughout January.

Futures Traders are now awaiting deliveries, and the COMEX has sent out notices. Concerns regarding the exchange’s low inventory levels are arising, but the Market hasn’t reacted to such news, so take that with a pinch of salt.

Overall, Metals are still in a rangebound trajectory since their correction, providing non-directional trading opportunities. However, directional traders will have to wait for a further breakout.

What may console Gold and Silver bulls is the heating tone regarding a military intervention in Iran, which would create a spike in Safe-Haven demand. Nevertheless, Gold would be more inclined to rally than the more volatile Silver, and with heavy positioning, any rally could see its potential capped.

Still, flight to quality may push Silver higher.

We will dive into a Silver multi-timeframe analysis to identify where the next breakout could occur and whether anything tilts the scales in favor of the Commodity. Let's get right into it.

Silver (XAG/USD) Multi-timeframe Technical Analysis

Daily Chart

Silver Daily Chart, February 20, 2026 – Source: TradingView

The current price action in Silver is one of hesitant recovery as prices maintain solidly between $70 and $84, a major range.

RSI Momentum is still below neutral territory, indicating a higher potential for correction, particularly as the 50-Day Moving Average is coming at resistance.

Take a close look to reactions if and when trading reaches that price level ($81.65)

4H Chart and Technical Levels

Silver 4H Chart, February 20, 2026 – Source: TradingView

Looking closer, Bulls are attempting to take the advantage, forming a strong rebound after retesting the 2025 broken bull channel and the action is now breaking the 50-Day MA.

If they manage a daily close above the Daily Moving Average (see level above), Silver could see higher chances of an upside breakout. Today's session close and Monday open will be very essential in that aspect.

- Breaking above $84 points to much higher chances to retest the $100 level.

Levels to watch for Silver (XAG) trading:

Resistance Levels:

- Attempting a break above 50-Day MA $81.65 (Watch the close)

- 2025 Record Main Resistance $82 to $84

- 4H 200-MA $87.76

- Higher Timeframe Major Resistance $90 to $95

- Key psychological resistance $100 to $104

Support Levels:

- Key Momentum Pivot $76 to $77.50

- Major 2026 Range Support $70 to $72

- December FOMC Minor Support $60 to $64 (Feb Lows)

- $50 to $54 Major Support

- October FOMC bottom $46.00 to $47.00

1H Chart

Silver 1H Chart, February 10, 2026 – Source: TradingView

Silver is now evolving well within an intraday bull channel which is the indicator to watch for short-term trading.

- Holding it will be essential to provide a more balanced and sustainable rally ahead.

- Breaking the channel would confirm the $70 to $84 Range which should then hold for longer.

Safe Trades!

Week Ahead – Markets Brace for Heightened Volatility as Event Risk Dominates

- Dollar strength dominates markets as risk appetite remains subdued.

- A Supreme Court ruling, geopolitics and Fed developments are in focus.

- Pivotal Nvidia earnings on Wednesday as investors question tech sector weakness.

- Yen and aussie diverge; both pound and euro could recoup their losses.

Dollar rally persists

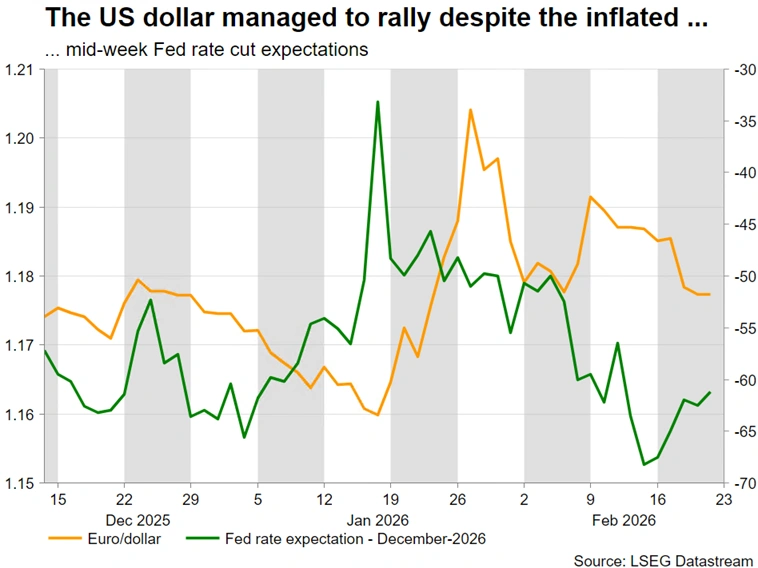

Despite markets pricing in additional easing from the Fed mid-week, the US dollar continues to perform strongly, posting gains across the FX spectrum, partly due to the geopolitical newsflow. Barring a major surprise on Friday with the announcement of the Supreme Court’s ruling on tariffs, this trend is likely to persist into the weekend if Friday’s key US data confirm the US economic strength and the lower inflationary pressures.

At the same, investors are trying to figure out the lingering weakness in US technology stocks. Is this a rotational shift into defensive and value stocks in anticipation of gradual US growth moderation, or just a temporary pause as companies adjust to the AI revolution? This dilemma will be partly answered on Wednesday, when Nvidia reports earnings after the US market closes. Unsatisfactory results and, more importantly, more conservative forward guidance could amplify the current weakness.

Fed in the spotlight, light data calendar

The Fed is unable to support risk appetite as it appears to be stuck in limbo. The chances of a rate cut under Chair Powell have diminished, predominantly due to the recently strong US data releases, and the continued attacks from the US President essentially limiting Powell’s willingness to meet Trump’s demand. This probably means that Fed meetings may lose some of their market-moving potential until June, with investors focusing instead on Kevin Warsh’s nomination hearings.

The process is currently stalled at the Senate Banking Committee, where senators are frustrated about the Fed probe against Powell over the Fed HQ renovation costs. Despite Treasury secretary Bessent’s optimism, no date for Warsh’s hearing has been set, gradually raising the probability of Powell remaining in position beyond May 15, and upsetting the robust rate cut expectations. This may sound far-fetched, but concerns appear credible given that Powell testified at the Senate Committee on Banking three months before taking office in February 2018.

Meanwhile, Fedspeak continues at full throttle. Investors tend to react more favourably to dovish rhetoric, limiting the dollar’s upside momentum. Next week’s data calendar is rather light, with Tuesday’s CB Consumer Confidence and Friday’s Producer Price Index report providing further insight into the economic trends. Interestingly, two-, five- and seven-year US Treasury auctions will take place next week. Investors are focusing on the level of foreign demand, with this week’s moves in US yields suggesting interest in Treasuries.

Wildcards could dent risk sentiment

If the Supreme Court judges refrain from publishing their tariff ruling on Friday, there are two additional ‘decision’ dates next week, Tuesday and Wednesday, February 24 and 25, respectively. The focus here is not just on the fate of tariffs, which if needed will be reimposed using different legislation, but on whether Trump will be allowed to act independently on such issues, ignoring Congress. This is key, since a loss of majority in either chamber at the November midterm elections would complicate Trump’s ability to govern.

Additionally, should the ruling strike down tariffs, the Trump administration might have to return some tariff revenue that has already been collected, which would blow a fresh fiscal hole into an already big federal deficit. Hence, a ruling announcement could prove extraordinarily market-moving across asset classes.

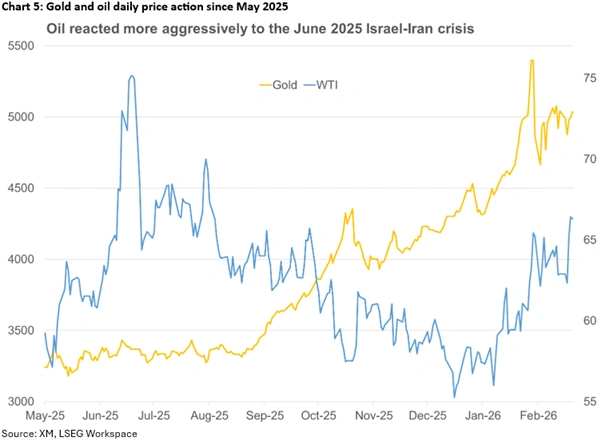

At the same time, there are numerous reports about an imminent US strike on Iran, despite the positive newsflow regarding the ongoing negotiations. Gold and oil are poised to further benefit from an escalation but the aftermath matters. Should Iran retaliate, potentially drawing Israel into the crisis, market reaction could resemble the June 2025 price action, when both the dollar and gold got a sizeable boost, but oil was the clear protagonist, skyrocketing to $80. Interestingly, gold has been struggling to reclaim the $5,000 level, potentially suffering from the Chinese holiday and the persistent strength of the US dollar.

The Yen and the Aussie are under close market scrutiny

Certain currencies could be in the spotlight next week. In particular, the yen continues to attract market interest, as the post-election rally appears to be reversing after testing the 152 zone.

Japanese PM Takaichi is preparing for her second term, with investors gradually questioning the implementation of her pre-election promises and their impact on the debt burden. The leader of Ishin, the junior coalition partner, has touted the idea of using the vast foreign exchange reserves to cover funding needs without tapping the bond market, but the implementation of this idea might not be so straightforward.

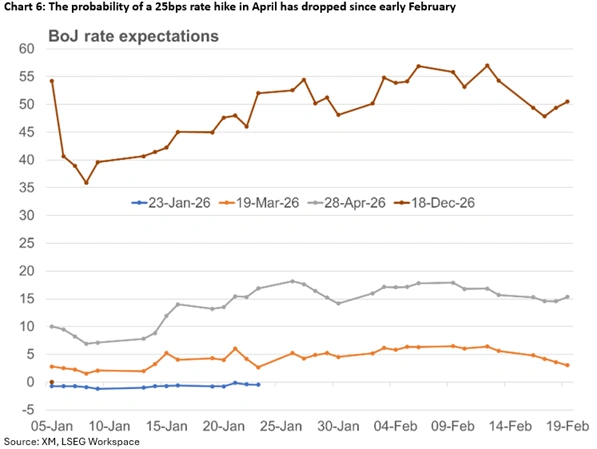

In the meantime, speculation is rife about the timing of the BoJ’s next rate hike. With the data softening lately, a weaker-than-forecast Tokyo CPI on Friday may further dent the chances of a rate move at the April meeting. Notably, it will be interesting to see whether the recent Takaichi-Ueda meeting could alter the BoJ’s current stance going forward. Should this occur, coupled with concerns about the planned aggressive fiscal spending, the door for a dollar/yen rally would be wide open.

Similarly, the aussie remains in the headlines due to the RBA’s hawkish stance and for successfully resisting the current US dollar strength. Following a robust set of labour market prints, the focus shifts to next week’s monthly inflation figures. The last CPI report before the March 17 meeting could go a long way into sealing expectations for a May rate hike, potentially even prompting the RBA to indirectly ‘announce’ this move at the next gathering, and helping aussie/dollar break above the early February 2022 high of 0.7157.

Both the pound and Euro could see increased volatility

Despite the potent retail sales figures, the pound has had a difficult week. Soft data have been added to the recent dovish BoE meeting and last week’s short-term political unrest, pushing the probability of a March rate cut to 78%. That said, despite the myriad of issues, the pound has not fallen off a cliff, partly benefiting from positioning. A potential drop below the 1.3400 zone in pound/dollar, though, could mark the beginning of a sizeable correction.

Positioning appears to be a major issue in euro/dollar as there is an exceptionally large short position against the dollar. This could explain the euro’s recent difficulty in taking advantage of the inflated Fed rate cut expectations.

It has been a quieter period for the eurozone, with data prints unable to materially challenge current ECB rate expectations, keeping the doves quiet. The highlight of next week’s calendar is Friday’s German preliminary CPI report. A very weak print could rejuvenate the ECB doves, mostly to no avail, thereby denting the euro’s appeal.

However, the burning issue appears to be rumours about Lagarde stepping down before November 2027. Could a German finally take the ECB helm, or could a less hawkish option could be explored, ensuring a smooth transition into the new era, and avoiding a rally in the euro? Notably, an early departure by Lagarde would mean that, for the first time ever, both the Fed and ECB heads will be selected/replaced in the same period, adding a rare level of uncertainty to markets.

Weekly Focus – Geopolitics Steals the Spotlight Again

Geopolitical developments in Middle East took centre stage in the markets this week. Despite the slightly optimistic tones of voices after the US-Iran talks ended in Geneva early this week, the US military buildup in the region has continued and the risk of a conflict is hanging in the air. Based on media reports, President Trump has not yet decided whether to attack, but if so, the attack could come soon.

Oil market has started to react to developments in Middle East. This week, Brent broke through USD 70 per barrel level. Unlike in early February, this time around higher oil prices are not driven by a weaker USD. On the contrary, the DXY index rose 1% this week. The fact that implied oil volatility is also up, suggests that this time the price move is primarily driven by a geopolitical risk premium.

In our view, the current market pricing broadly reflects a scenario where Iran's response to any US intervention would remain carefully calibrated - similar to what we saw last June. Thanks to excess supply, the oil market has some buffer against geopolitical shocks for as long as the shocks would be limited in scale and duration. Even limited disruptions in the Strait of Hormuz (SOH) would not devastate markets for as long as oil and gas flows would continue. And for now, tanker traffic seems to have returned to normal levels. That said, in the worst case, a complete closure of the SOH for several days could drive oil price above USD 100 per barrel.

The higher oil price has been one of the factors weighing on euro lately, as Europe's energy imports dependence remains one of its key vulnerabilities. This week, EUR/USD fell below the 1.18 mark. We still think the downside is temporary and now target EUR/USD at 1.25 in 12M.

On data front, focus was on euro area sentiment surveys this week. The German PMIs surprised on the upside, corroborating the story that the German industry is finally recovering. The manufacturing PMI exceeded the watershed 50 level for the first time since June 2022. The French PMI also topped expectations on the composite level, but manufacturing index disappointed by falling back below 50.

The speculation that ECB's President Lagarde would leave office before her term expires also received media attention this week. The rumours have not been confirmed, and in any case, we do not see this as a key market driver.

In the US, we have adjusted our Fed call. We still foresee terminal rate at 3.00-3.25% but have pushed the rate cuts further out, see RtM USD - The Fed will cut in June and September, 17 February. Recent data from the US has again painted a picture of a resilient economy, but while consensus has continued to upgrade GDP projections for this year, we are a bit cautious about whether private consumption can maintain its current strength. This week, we also saw how the economy is starting to rebalance with trade balance re-widening in December as imports volumes are starting to recover from abnormally low levels.

Next week's calendar looks rather empty with the main events being Trump's state of the union speech on Tuesday and EA flash HICP on Friday. Hence, it is more than likely that geopolitics will remain the main market driver.

US: Consumer Spending and Income End 2025 on Softer Footing

Personal income rose 0.3% month-over-month (m/m) in December, in line with market expectations. All gains were in nominal terms, with personal income remaining flat after adjusting for inflation.

Consumer spending was also aligned with market expectations, advancing by 0.4% month-over-month in nominal terms and matching November's pace. Most of the gain, however, was due to higher prices: real spending rose by just 0.1% m/m.

Examining the broad categories, spending on goods declined by 0.5% in real terms, weighed by reduced spending on cars and parts and furniture, while spending on services rose by 0.3% m/m.

With spending slightly outpacing income, the personal saving rate edged lower to 3.6% (down from 3.7% in November and 4.3% a year ago). This marks the lowest level of the saving rate since October 2022.

Inflation remains persistently above the Fed's 2% target. Core PCE – the Fed's preferred inflation gauge – rose by 0.4% in December, a notable uptick from 0.2% pace in November. In annual terms, core PCE inflation was up 3.0% year-over-year, up slightly from 2.8% pace seen in November.

Key Implications

Today's release shows that consumers had a bit less spring in their step in the final quarter of 2025 that previously reported. This tells us that while the government shutdown didn't detail consumer spending, it still weighed on activity, with real consumer spending advancing by 2.4% (annualized) in Q4, down from the 3.5% pace seen in Q3. Looking back at 2025, growth in consumer spending averaged 2.7%, down slightly from a 3% pace in 2024, suggesting consumer spending has remained resilient, despite heightened economic uncertainty and slowing labour market.

Looking ahead, we expect consumer spending to remain relatively robust at the start of 2026. Consumers should benefit from past interest rate cuts, some stabilization in the labour market, and wealth gains. The fiscal boost from higher OBBBA-related tax refunds—which could be on average $800–$1,000 higher than last fiscal year—will provide another tailwind to household income and spending (report).

US: Q4 GDP Weaker Than Expected, But Underlying Fundamentals Remain Solid

The U.S. economy expanded by 1.4% quarter-on-quarter (q/q, annualized) in the fourth quarter – below the consensus forecast of 3.0% – and a notable deceleration from Q3's 4.4%.

- The annual average rate of growth for 2025 was 2.2% – down from 2024's 2.8%.

Consumer spending rose by 2.4% q/q, following a stronger gain of 3.5% in Q3. Goods spending was essentially flat on the quarter, while services rose by a healthy 3.4%.

Business investment was up 3.7% q/q, a slight uptick from Q3. In terms of the breakdown, both equipment (+3.2%) and intellectual property products (+7.4%) were higher, while spending on structures (-2.4% q/q) declined for an eighth consecutive quarter. Residential investment (-1.5%) also declined.

Government spending (-5.1%) fell sharply, entirely driven by a pullback in federal outlays (-16.6%) due to the 43-day long government shutdown. Meanwhile, state & local spending rose 2.4%.

International trade had a negligible impact on growth, as a very modest pullback in exports (-0.9%) was largely offset by a similar decline in imports (-1.3%). Inventory investment added a modest 0.2 percentage points to Q4 GDP.

Final sales to private domestic purchasers, a better gauge of underlying demand as it includes only household consumption and fixed investment rose by a healthy 2.4%, following a gain of 2.9% in Q3.

Core PCE inflation – the Fed's preferred gauge – rose 2.7% q/q annualized, down slightly from Q3's 2.9%.

Key Implications

Following a very strong third quarter, economic growth softened by more than expected through the final three months of last year, largely due to a sharp contraction in federal outlays. However, this was a temporary impact related to the government shutdown, and we should see a reversal of those effects in the first quarter. Encouragingly, final sales to private domestic purchasers – a better gauge of underlying demand – still expanded by a healthy 2.4%.

All told, even after accounting for this morning's miss on growth, we still feel that the U.S. economy has entered 2026 with considerable momentum. While headwinds from tariffs and trade policy uncertainty remain, its effects are likely to be eclipsed by fiscal tailwinds from the One Big Beautiful Bill Act, easier financial conditions, and continued investments in AI. Growth is expected to accelerate to 2.7% Q4/Q4 this year – up from 2025's 2.2%.