Sample Category Title

Weekly Economic & Financial Commentary: On Hold

Summary

United States: On Hold

- The FOMC held rates steady at its first meeting of 2026 and signaled it is in no rush to resume policy easing but was careful to preserve flexibility. To cap off a Fed‑heavy week, President Trump named Kevin Warsh as the next Fed chair, succeeding Powell in May.

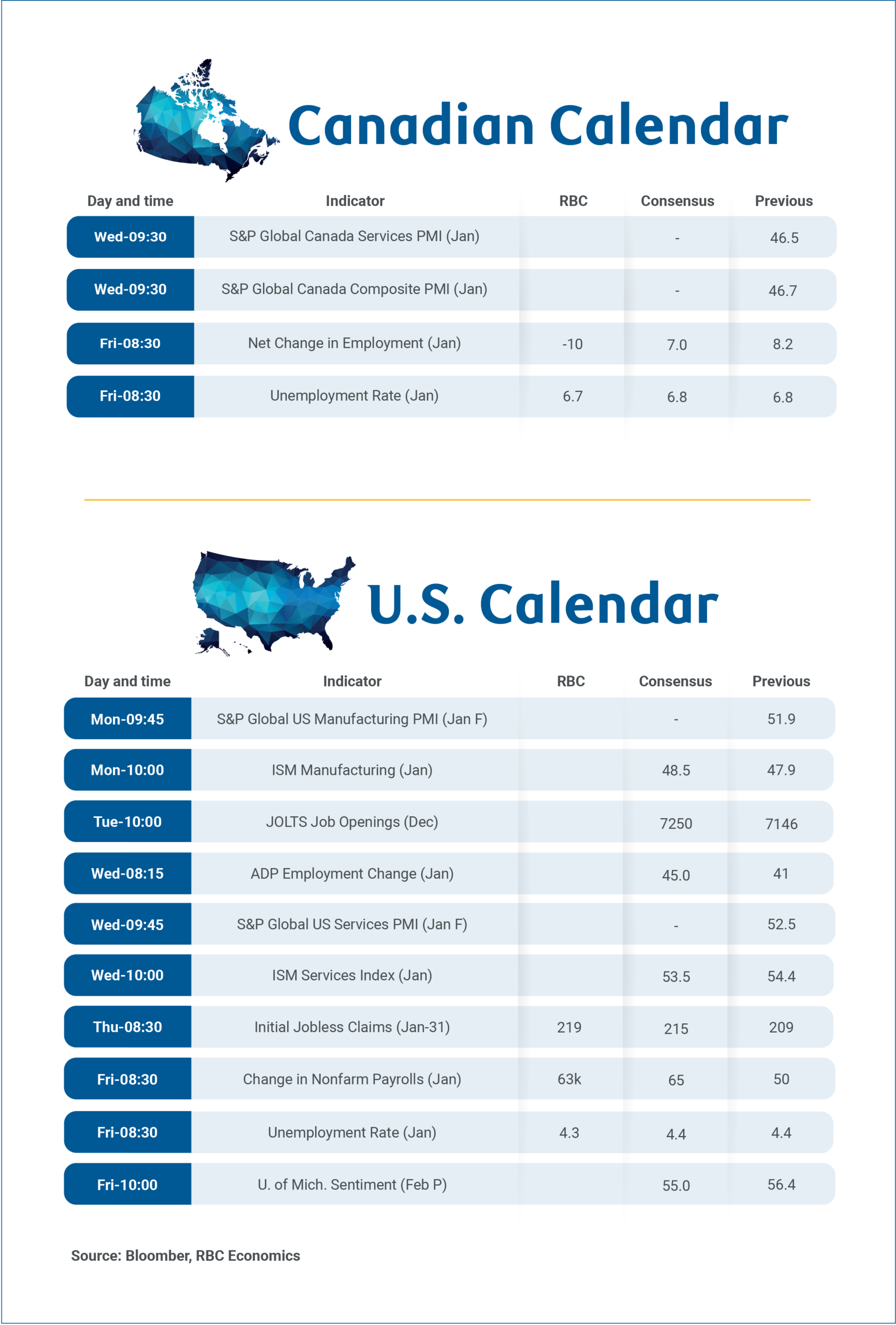

- Next week: ISM Manufacturing & Services (Mon. & Wed.), Employment (Fri.)

International: Global Central Banks Hold Steady as EMs Signal Easing Ahead

- Central banks across both G10 and emerging markets met this week, with most opting to keep policy rates unchanged. Canada, Sweden, Brazil and Chile all held rates steady. Beyond central bank decisions, the Eurozone's solid Q4 GDP growth bolstered the case for the ECB to keep policy rates unchanged next week.

- Next week: Reserve Bank of Australia Cash Rate (Tue.), Bank of England Bank Rate (Thu.), Banxico Policy Rate (Thu.)

Topic of the Week: Government Shutdown Redux

- Heading into this weekend, the probability of a U.S. government shutdown is almost all but certain. Even as the Senate and Trump administration reached a new détente Thursday evening, a shutdown for at least this weekend looks increasingly likely.

More Signs of Stability Expected in Canadian and U.S. Job Market

Next Friday, we expect Canada’s January employment report to show a tick-down in the unemployment rate to 6.7%, after an increase to 6.8% in December that partially reversed an unusually large 0.5 percentage point decline over the prior two months. Employment is expected to have declined by 10,000 in January – after the outsized 189,000 increase between September and December 2025.

Canadian labour market data is notoriously volatile month-to-month, but slower population growth is also sharply reducing the amount of job growth needed to absorb new workers into the workforce. A 9,900 increase in population in December was the smallest gain since the pandemic (December 2020) and the second smallest rise dating back to 1976. We also think a partial reversal of a jump in the December participation rate will result in a pull-back in available labour in January.

We expect these underlying structural trends to persist (on average) this year. Slower population growth, and an aging population means even small declines in job counts in 2026 would be consistent with a steady to declining unemployment rate.

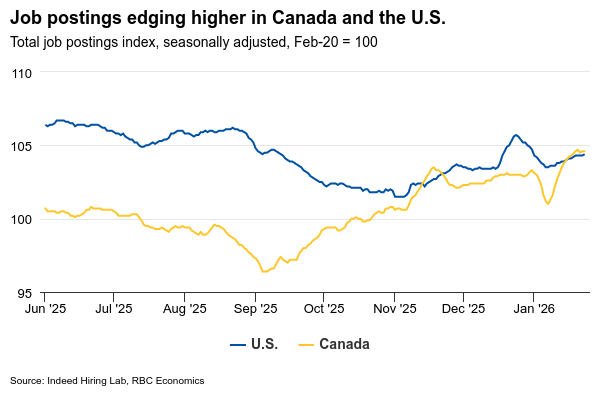

Looking ahead, Canadian firms hiring intentions remained subdued, according to the latest Bank of Canada Business Outlook Survey—and most business survey data is suggesting wage growth will edge lower. Job postings from Indeed.com, however, paint a more optimistic picture with hiring demand rising since September 2025 to levels close to the pre-tariff peak in January 2025.

Sectors heavily exposed to international trade disruptions, like manufacturing, continue to underperform, but we continue to expect a stabilizing trade backdrop and strength in domestic demand will support a rebound in hiring overall. We look for the unemployment rate to edge gradually lower to 6.3% by the end of this year.

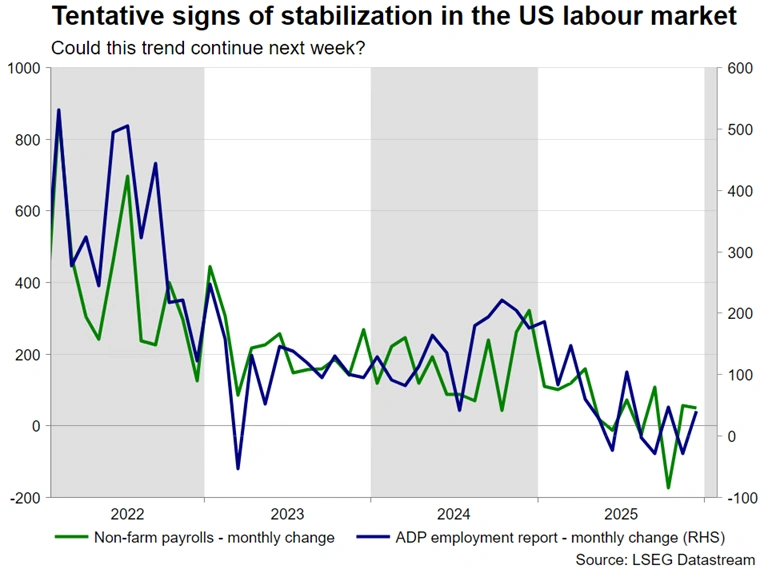

U.S. jobs market to show more signs of stabilizing after cooling

We also expect the U.S. labour market to show more signs of stabilization with the unemployment rate potentially ticking lower in January after falling to 4.4% in December.

Leading indicators are starting to point to improvement in the labour market after a year of gradual cooling best characterized as a “low hire, low fire” environment. Similar to Canada, job postings from Indeed.com started to rise in late 2025, although to levels still significantly below where they were at the start of the year. In the meantime, initial and continued jobless claims started to trend lower over the end of 2025 heading into 2026.

A pick-up in the labour market is more in line with GDP data that has surprised consecutively to the upside in the second half of 2025. But, it’s been driven by higher productivity to-date rather than improvement in the labour market. Employment and hours worked were both little changed since April as of December.

Lingering trade uncertainty means the outlook remains cloudy, but we look for the unemployment rate to end 2026 close to its current level at 4.4%.

Will RBA Opt for a Rapid Policy Reversal?

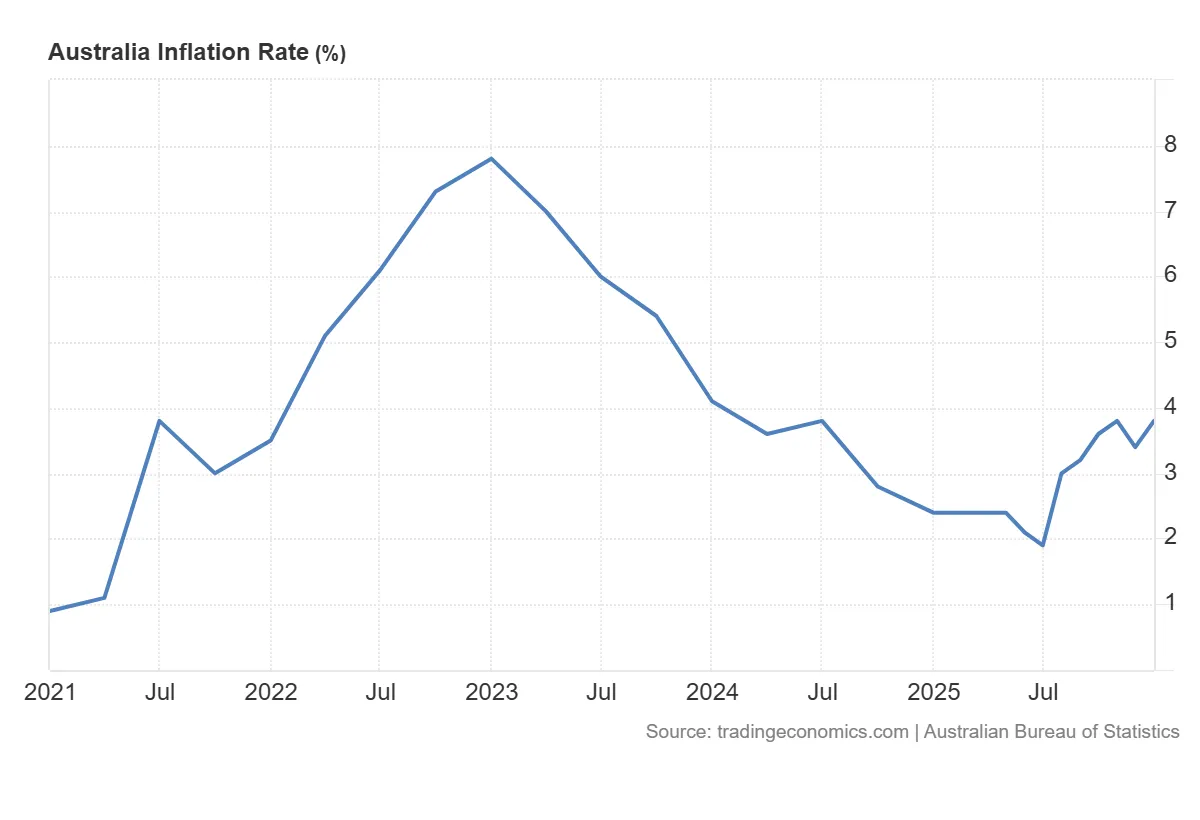

Core inflation in Australia rose to 3.4% y/y, exceeding both forecasts and the Reserve Bank of Australia’s 2–3% target range, increasing pressure on the central bank to act.

Markets are pricing in a high probability (~76%) of a February rate hike, potentially marking a sharp policy reversal less than six months after the last rate cut.

Strong labour market conditions and accelerating services inflation suggest underlying demand pressures remain elevated, testing the RBA’s credibility and policy resolve.

The latest inflation data from Australia has once again raised concerns among monetary policymakers and investors. Core inflation (the trimmed mean) — regarded by the Reserve Bank of Australia (RBA) as the key measure of underlying price pressure — rose in the fourth quarter to 3.4% year on year. This reading not only exceeded market expectations (3.3%), but also moved above the upper bound of the RBA’s inflation target range (2–3%).

On a quarterly basis, core inflation came in at 0.9%, in line with forecasts. However, the annual acceleration suggests that the disinflation process may be less durable than previously assumed.

Headline inflation accelerates – energy and services in focus

Price pressures are also evident in headline inflation. In December, CPI rose to 3.8% y/y, up from 3.4% a month earlier. The largest contributors to the increase were:

- Housing: +5.5%

- Food and non-alcoholic beverages: +3.4%

- Recreation and culture: +4.4%

Australia Inflation Rate, source: TradingEconomics

The composition of inflation deserves particular attention. Services inflation accelerated to 4.1% y/y, from 3.6%, typically signalling strong domestic demand and persistent wage pressures. Goods inflation, meanwhile, stood at 3.4% y/y, with electricity prices surging by 21.5%, further complicating efforts to rein in inflation.

Labour market strength strengthens the case for tighter policy

Elevated inflation is accompanied by a relatively tight labour market. Unemployment has fallen to around 4%, suggesting that demand-side pressures in the economy remain strong. This macroeconomic mix — high inflation and low unemployment — significantly narrows the central bank’s room for manoeuvre and increases the risk that price pressures become entrenched.

It is worth recalling that the RBA cut interest rates as recently as August, but already signalled in December that the next move could be a rate hike if inflation data proved concerning.

Financial markets price in a February rate hike

Market reaction has been swift. OIS contracts now price in around a 76% probability of a rate hike at the 2–3 February meeting. Such a move would represent a sharp pivot in monetary policy — less than six months after the last rate cut. At the same time, three-year government bond yields fell to 4.28%, possibly indicating that some investors view the recent rise in inflation as temporary or expect only a one-off tightening move by the RBA.

Among major financial institutions, consensus is building around the upcoming meeting. Westpac Banking Corp. and ANZ Bank both expect a 25-basis-point rate hike, taking the cash rate to 3.85%. Westpac, however, stresses that such a move does not necessarily mark the start of a sustained tightening cycle. A “wait-and-see” approach remains plausible, particularly if inflationary pressures prove short-lived and begin to ease in the months ahead.

A stronger Australian dollar signals investor confidence

Within the G10 currency universe, the Australian dollar has performed notably well. Since the start of the year, it has appreciated by over 4%, making it the second-best-performing currency in the group. The currency’s strength reflects both expectations of higher interest rates and investor confidence in Australia’s relative resilience amid global economic uncertainty.

Daily Timeframe of AUDUSD, source: TradingView

The RBA decision as a test of credibility

The upcoming RBA meeting in early February will carry significance beyond a single interest-rate decision. Following a recent easing cycle, the central bank now faces a credibility test: whether to pivot decisively in response to rising inflation or treat the latest data as a temporary disturbance. What is clear is that the recent inflation readings have substantially increased pressure on the RBA, and the February decision could set the tone for Australian monetary policy in the quarters ahead.

Silver Down 30%! – Chaos in the Metals Market

Yesterday's flows really did open a breach for a gigantic profit-taking wave in Metals, exploding exponentially since 2026.

Gold and Silver showed a few cracks through yesterday's first crash, but today is something else.

The Bullion dropped below $5,000. Platinum, Copper, Silver and Palladium are down between 15% to 30%!!

Silver Daily Chart

Silver (CFD) Daily Chart – January 30, 2026 – Source: TradingView

Gold Daily Chart

Gold (CFD) Daily Chart – January 30, 2026 – Source: TradingView

Morning Session moves in Metal Futures – Courtesy of Finviz

The Metals market lost quite a few trillion dollars of value just today – But despite the panic around Markets, it is essential to take a step back.

Silver had risen 70% in parabolic and unstable moves higher and this can trigger sharp Market conditions. Look at today's move!

Today's selling took out all of the Metals profits in 2026 – XAG/USD is still 185% higher than it was on January 1, 2025!

Even if the run continues from here, odds for metals to return to their prior year levels are low.

Trying to profit from parabolic trend can be dangerous, as was highlighted in our past week Warning – They still offer interesting trade setups but need to be treated with respect.

Nothing is given in Markets and things can change any second.

Stocks are also not liking these flows

Nasdaq (CFD) 1H Chart – January 30, 2026 – Source: TradingView

A Stock Market update is coming up very soon.

Watch out for month-end flows!

The picture in equities isn't looking very bullish across different Benchmarks – Watch out for volatility in upcoming sessions ahead of Weekend risk.

The US Dollar doesn't know where to go

US Dollar (DXY) 1H Chart – Source: TradingView – January 30, 2026

Keep a very close eye on the headlines to monitor Market developments.

Safe Trades!

The Fed Chair Has Been Picked: Who is Kevin Warsh?

- President Trump surprised Markets with an early-morning nomination for a new Fed Chair

- Kevin Warsh will be replacing Chairman Powell in May 2026

- Discover his story, past accomplishments and Market effect

The US President finally gave his answer for who will be the next Federal Reserve Chairman of the Board.

Trump loves a good surprise. Just after announcing he would provide the decision next week, turns out he did so in the early morning through a Truth Social Post.

Kevin Warsh will be serving as the Chairman for the Fed for a first four-year term beginning in May 2026.

The announcement came with swift Market reactions – Gold and other metals are falling off a cliff, Stocks gapped lower in today's open and the Dollar is heading higher.

This definitely looks like "Sell the news" flows – the rest for traders will be to see if this continues or not.

Gold (XAU/USD) 4H Chart, January 30, 2026 – Source: TradingView

We will dive into Mr Warsh's past endeavours, what he represents for the Federal Reserve and our expectations on the effect he should have on Markets.

Who is Kevin Warsh?

His past

Kevin Warsh’s career is a distinguished blend of high-level academia, private sector expertise, and public service.

He holds an A.B. in public policy from Stanford University and a Juris Doctor from Harvard Law School, where he focused on the intersection of law and economics – A clean, classic background for somebody who could run the Fed.

FYI, Powell also held a Law Degree.

Shortly after his completing his studies, Warsh distinguished himself at Morgan Stanley, where he served as Executive Director in the M&A department from 1995.

Warsh quickly became a specialist in structuring complex capital market transactions across diverse industries for the Financial Institution.

His competence for Markets caught the eye of the George W. Bush administration, leading to his appointment as Special Assistant to the President for Economic Policy in 2002 being only 32.

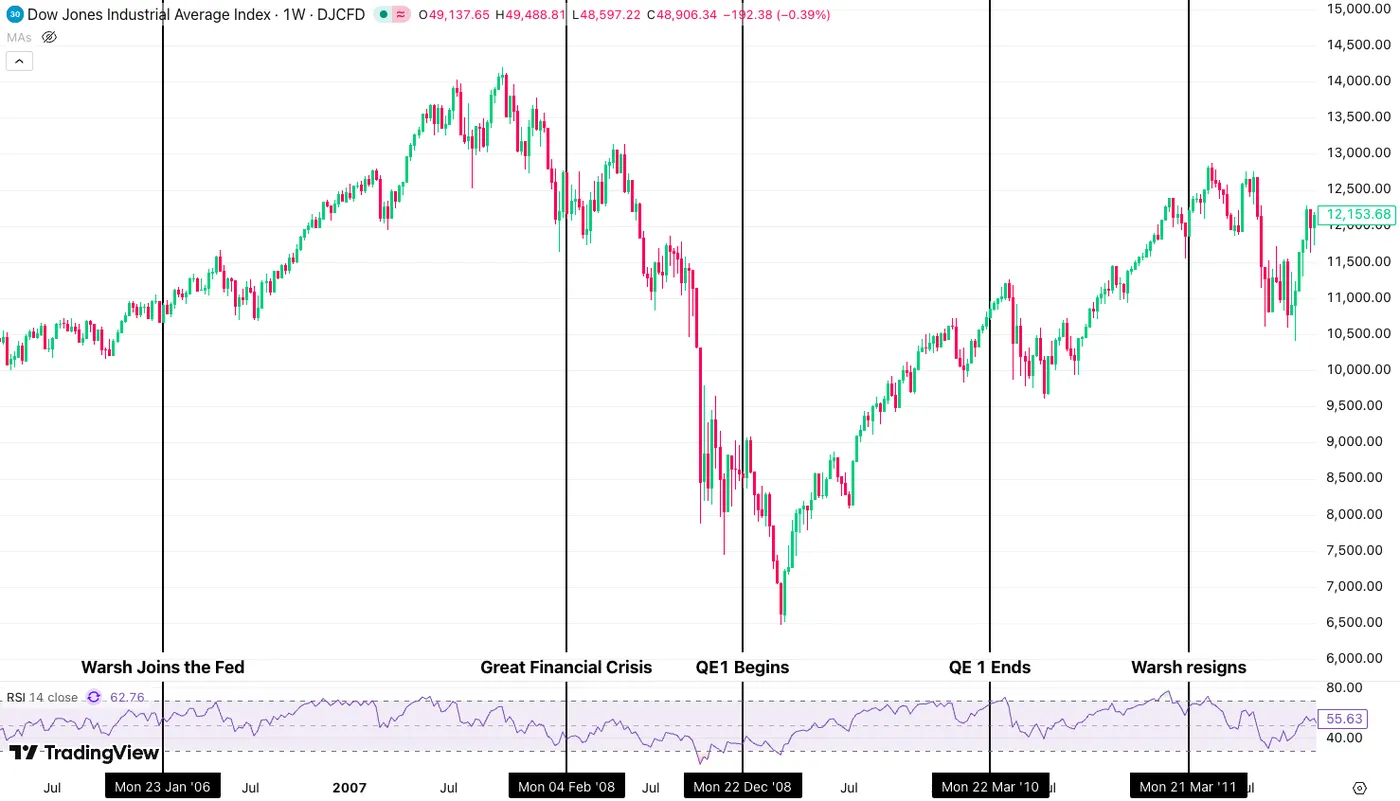

In 2006, Kevin got appointed at the Board of Governors at the Federal Reserve, being the youngest to reach the position, which drew some criticism.

Still, being well connected to Wall Street after his stay at MS, he quickly got accepted as "invaluable" for the Fed.

Warsh became Ben Bernanke’s (Fed Chair during the period) primary "emissary" to the financial world during the 2008 meltdown. His unique ability to speak the "language of the markets" made him the central bank’s most vital conduit to Wall Street CEOs and global regulators.

Just the fact that he remained at the Fed from 2006 to 2011 proves he was well-suited for the Job. It wasn't the easiest period in financial markets.

Dow Jones from 2006 to 2012 and Warsh's first Fed term – Source; TradingView

He also served as the Fed's representative to the G20 and for Emerging and Advanced economies of Asia before resigning in March 2011.

After his first stay at the Fed, Warsh transitioned into heavyweight intellectual roles in many establishments and foundations.

At the Hoover Institution, he became a prominent advocate for regime change in monetary policy, often criticizing the Fed’s long-term reliance on balance sheet expansion.

One of his most notable global achievements was an independent report, the Warsh Review, commissioned by the Bank of England which increased the Central Bank's transparency policy.

Fun fact, Canada's Prime Minister Mark Carney was the Bank of England's Governor during that period.

He also was part of the favorites to be the Fed Chair in 2018, but the first Trump Administration preferred to go towards safety with Jerome Powell (as he was still deemed too young for the position).

The new Fed Chair still kept close ties with the US President, taking us to today.

Let's now see what he represents for Markets and how it can affect the US Dollar and other assets.

Warsh and his impact on Markets

This section can either age like Wine or Milk and will, of course, be subject to extensive reviews as his term commences and his first speeches as Fed Chair get delivered.

Kevin Warsh is not Wall Street's preferred choice (Rick Rieder held that role), but still represents Respect and Credibility for his role.

The Nominee was known for his relatively hawkish views towards the end of his first term at the Fed, notably getting named a "hard money hawk" by CNBC.

But being close to the Trump Administration, particularly today, implies sacrificing some of one's impartial judgment.

Kevin Warsh is an advocate for tax and regulatory reforms, so as long as Trump's fiscal policies aren't too extreme, he should stay mostly in line with the President.

Something positive for the US Dollar and fiat currencies in general is that Warsh tends to be a realist rather than a dove-maximalist. He did express his discontent with the second round of Quantitative Easing.

A good place to look for Market reactions to his credibility regarding the Dollar is the Dollar itself.

The DXY (Dollar Index) has been strengthening again after the pre-FOMC super-tumble. As long as the Index remains below 97.00, it could just be classical mean-reversion. For now, the rebound looks solid.

Dollar Index (DXY) 1H Chart. January 30, 2026 – Source: TradingView

Stock Indexes have opened lower but I wouldn't take this as a red flag.

Stocks did rise after the FOMC meeting and despite yesterday's selling session, benchmarks rebounded and largely remain close to their all-time highs.

What you are seeing today is the result of profit-taking ahead of a high-risk weekend (Iran, or more Trump Admin madness anywhere else).

If Warsh follows Trump's demands, he should help Equities to rise on the long-run. The President loves to base his own performance looking at Markets for those who did not know, so Trump surely will push for his nominee to do the same.

The rest will of course also depend on the US Economy and global risk-appetite (and lack of any major Crisis).

Regarding Fiat currency credibility, it will be tough to say.

Kevin Warsh isn't the favored candidate to reduce the Fed's Balance Sheet – So that's about that for Fiscal reduction concerns.

Still, his realistic views may help with the recent Debasement Trade trends, part of the reason why we saw steep profit-taking around Metals today.

Metas Performance today (11:32 A.M.). January 30, 2026 – Courtesy of Finviz

The yield curve is also steepening further, with the shorter-term yields (3M to 5Y) going lower while the long end (10Y and more) is rising – Implying pricing for more cuts today and more inflation later.

This is a repricing for further dovishness from the Trump-nominee, not seen as such a Yes-Man as Kevin Hassett, but also not a candidate who will stand up to the President like Powell.

Daily US Treasury Yields movement. January 30, 2026 – Source: TradingView

For the rest, time will tell.

Risk-appetite is looking timid amid the past two years of relentless rallies across asset classes and geopolitical instability.

His first address, particularly his first Press Conference as Fed Chair (June 17, 2026), will be quintessential for Markets.

Tribute to Jerome Powell

Jerome Powell will surely go down as one of the most popular Fed Chairs.

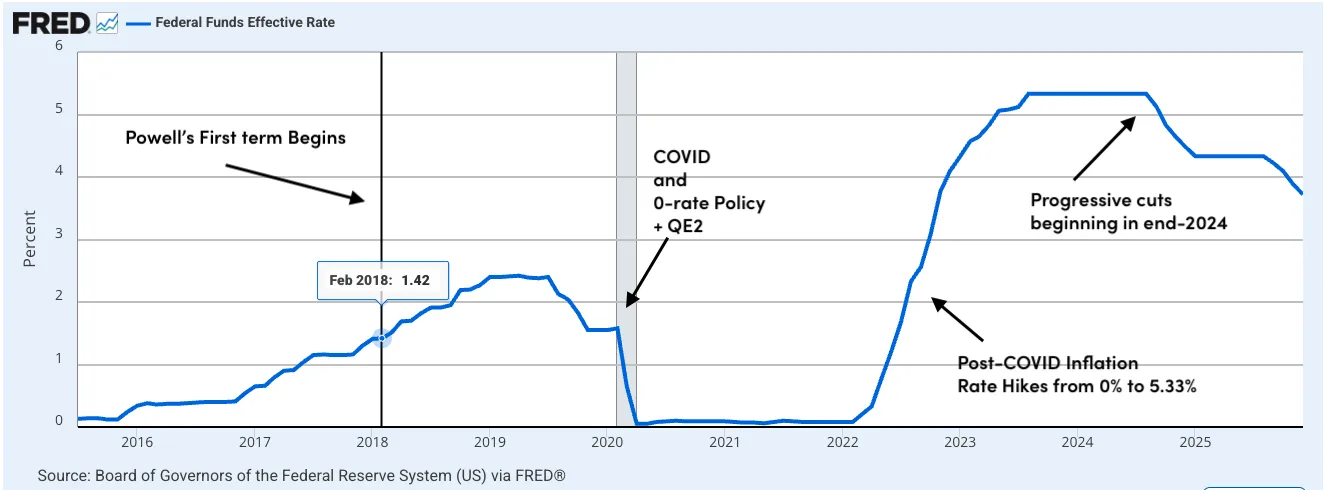

Known as a Market stabilizer, Powell would always push for the lowest volatility outcome over his 8 years as Fed Chair, may it be through the first rounds of post-Great Financial Crisis rate tightening in 2018-2019 or the quick U-turn towards zero-rate policies the year after, as COVID struck hard.

Even when Participants thought he was a dove, he did not hesitate to show his hawkish wings during the 2022 hiking cycle and maintained that tone until inflation abated.

Fed funds Powell

Fed Funds Rate since 2015 – Source: FRED

He was a Swiss Army knife at the head of the most important central bank and held his role with righteousness—a very talented speaker who always knew how to shapeshift curve balls and tricky questions during press conferences. Or even attacks from his President.

Markets will surely miss Jerome Powell as Fed Chair – now we'll see if he wants to stay on the Board of Governors, with his term still valid until January 31, 2028.

He will also be remembered for years of good memes.

I'm part of Generation Z, so this one is a bit more personal.

money printer

zoom_out_map

Money printer go "PRRRRRRRR"

Safe Trades and wishing good luck to Kevin Warsh (and the Financial System)!

Kevin Warsh as Fed Chair

Summary

We know from our many client discussions that there appears to be at least some degree of comfort with a Warsh led Fed vs. the other choices. But, we all should be mindful that there is also some degree of uncertainty associated with this pick if for no other reason than his public remarks on the economic outlook and the appropriate path for the federal funds rate have been fewer and farther between than the other finalists.

We generally expect Chair Warsh to support a more dovish stance on monetary policy driven in part by his optimism over productivity growth as well as his view of the need for lower rates to support "Main Street." And of course, a dovish slant is what President Trump wanted. That said, Warsh has historically been among the most hawkish of the four finalists on President Trump's shortlist. Warsh's reputation as a hawk stems from his time as a Fed Governor and during his post-Fed career.

Although Warsh's comments on the fed funds rate have been infrequent in recent months, he has maintained a belief that the Fed's balance sheet is too large—a belief he has long held and another factor that has contributed to his hawkish reputation.

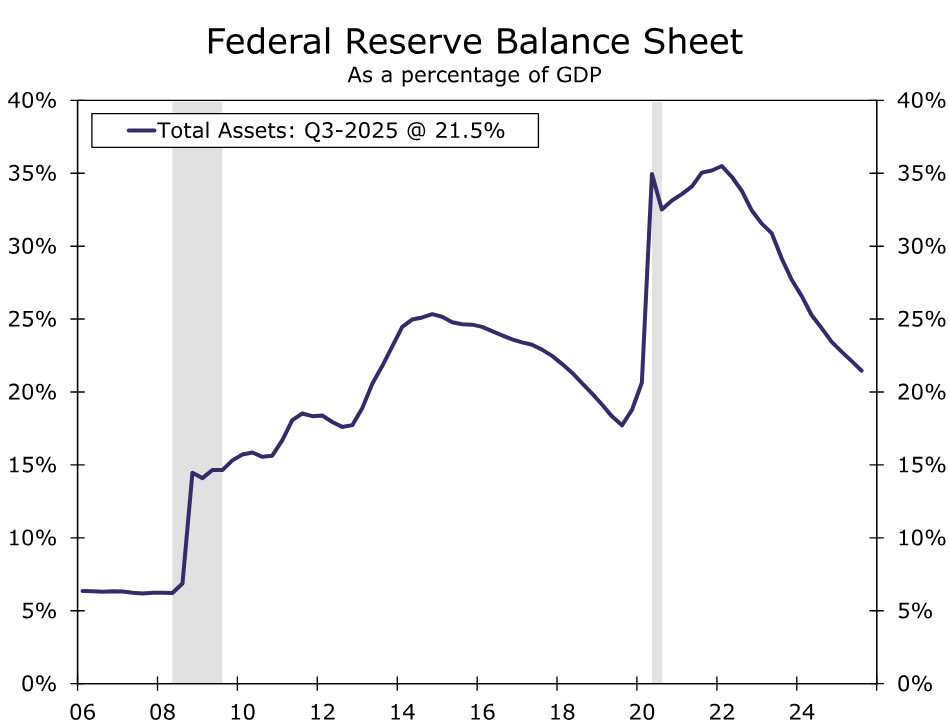

We think it is highly unlikely that the Fed will shrink its balance sheet materially under Chair Warsh given how entrenched the "ample reserve" operating framework is in the financial system. Stated differently, there are no reasonably plausible scenarios where the financial system would comfortably absorb a sharp change to this stance, no matter what the leaning of the new Fed chair may be. There is a high hurdle to altering this framework.

Where we think Chair Warsh could affect more change is by de-emphasizing short-term data dependence in favor of "trend dependence", which we believe would lead to fewer, but more seismic, inflection points in U.S. monetary policy. We can also see him making a case for diminishing or even completely doing away with the Summary of Economic Projections and the Dots. We would not be surprised if he makes a case for less "Fed-speak".

When it comes to Fed independence, Warsh has been outspoken about the need for the Fed to revisit some of its current governance policies and processes, but he has publicly maintained a belief in the importance of central bank monetary policy independence.

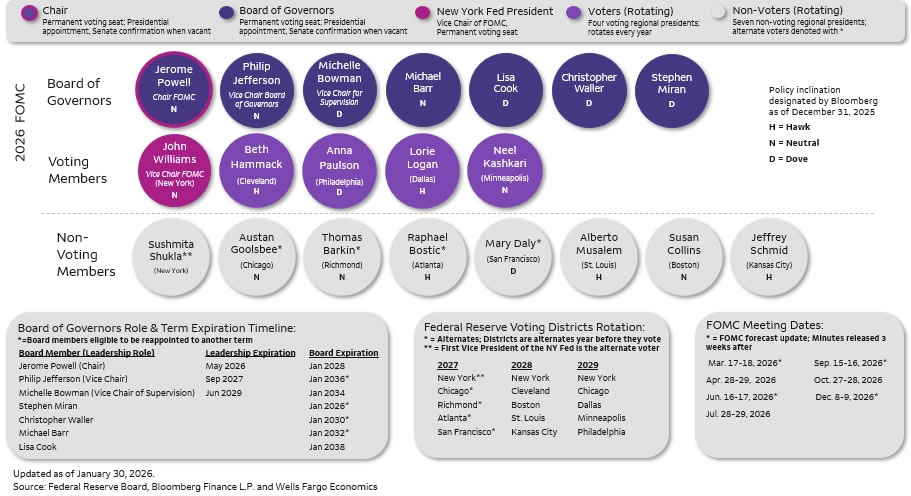

It is also important to remember that monetary policy decisions are a Committee decision. Seven governors vote at each meeting in addition to five of the 12 regional Fed presidents. This ensures some continuity in the makeup of the FOMC as it transitions. Accordingly, we do not anticipate making any changes to our fed funds forecast, although as we have stressed elsewhere, we continue to see risks to our call.

We would give you just two more things to consider. Warsh has some challenges that start almost right away. First, does he act as a shadow Fed chair? If he is going to second guess Powell at every turn or forcibly disagree with him, he may appease his new boss, but he runs the risk of alienating himself to the rest of the Committee. We think Warsh knows this and will tread carefully around that, but it’s a risk. And second, what kind of consensus builder will he be? Criticize Powell as much as you like (and yes, we have been critical of him at times), but he is one heck of a consensus builder, carefully crafting and selling his message to members ahead of meetings. This will be critical for Warsh. The expectation is he wants to cut, perhaps even more aggressively than market pricing. If that is indeed the case, he has his work cut out for him in building a consensus toward that when the expectation of the Committee at large is just for one more cut per the dots (where we think the hurdle is growing higher even for that).

For those that want to read on, below you’ll find more detail about his background and our analysis of his direct quotes over the years…

Warsh's Windy Path Back to the FOMC

Like current Fed Chair Jerome Powell, Kevin Warsh does not hold a PhD in economics but has prior experience in the financial industry and public policy. After obtaining a law degree from Harvard in the mid-1990s, Warsh went on to work on Wall Street before holding several positions in the George W. Bush administration, including executive secretary to the National Economic Council. From 2006 to 2011, he served on the Federal Reserve Board of Governors. Although Ben Bernanke, Janet Yellen and Jerome Powell also served on the Board prior to their appointments as Fed Chair, Warsh's tenure is not as recent as his predecessors' was when they assumed the Chair (Figure 1). Warsh has not served in government since his time at the Fed, although he has remained active in public policy circles. He currently serves as a distinguished visiting fellow at the Hoover Institution.

A Hawk Dressed in Dove's Clothing?

Public comments by Warsh last summer revealed he was in favor of reducing rates prior to the Committee cutting the fed funds rate at its three final meetings of 2025, noting simply in an interview on July 8, that "interest rates should be lower." Driving his rationale for a lower fed funds rate at the time was the sluggish state of the housing market but, more predominantly, optimism that the economy was on the verge of a productivity boom. Such a resurgence, traced to AI and other "pro-growth policies" adopted by the Trump administration, would act as a disinflationary force, in his view.

We have significantly less conviction about how far Warsh would aim to reduce the fed funds rate compared to other candidates that were on President Trump's short list. Warsh's lack of recent remarks on the policy rate as well as his historic reputation as a hawk inject more uncertainty into the monetary policy outlook than a Chair Hassett or Chair Waller would have generated, in our view. Warsh's hawkish reputation was earned due to his focus on upside risks to inflation during his time as a Fed governor from 2006-2011, including in the spring of 2008 when inflation was a little over 2% but the economy, as we now know in hindsight, was already in recession (Figure 2). He was also an outspoken critic of the Fed engaging in multiple rounds of large-scale asset purchases (i.e., quantitative easing) in the early 2010s when the fed funds rate was constrained by the zero-lower bound. In short, there are more questions than answers about a Chair Warsh, in our view, and we expect the market to be sensitive to his public remarks in the coming months as everyone assesses his outlook on monetary policy.

While less concerned about inflation today, Warsh has remained critical of the size of the Fed's balance sheet. In a November Wall Street Journal op-ed, he said that "the Fed's bloated balance sheet...can be reduced significantly." With the Fed owning 14% of Treasury securities and 25% of agency MBS, reducing the balance sheet significantly would, all else equal, put upward pressure on longer-term borrowing costs. Warsh believes that these upward effects could be offset by cutting the fed funds rate further. He views the size of the Fed's balance sheet as having disproportionately benefited large companies and "Wall Street" in lieu of "Main Street" and the broader economy.

We would not expect Warsh to meaningfully shrink the balance sheet in his tenure as Fed Chair. The Fed's shift to an "ample reserve" operating framework makes reducing the balance sheet to pre-2008 levels as a share of GDP very unlikely (Figure 3). As recently as the FOMC's meeting in December, the Committee voted to initiate purchases of shorter-term Treasury securities to maintain an ample supply of reserves and ensure effective short-term interest rate control. Furthermore, a smaller balance sheet could be at odds with President Trump's preference for lower longer-term borrowing rates generally and lower mortgage rates specifically, leading us to question how ardently Warsh would push for a smaller balance sheet as Fed Chair.

One other view from Warsh that struck us as important in his history of public remarks is his disdain for near-term forecasting, forward guidance and data dependence. These themes have come up repeatedly in his public remarks, such as in his G30 speech at the IMF Spring Meetings last April.1 The following remarks from a 2017 op-ed in the WSJ capture the sentiment well: "The Fed should adjust monetary policy only when deviations from its employment and inflation objectives are readily observable and significant. The Fed should stop indulging in a policy of trying to fine-tune the economy. When the central bank acts in response to a monthly payroll report, it confuses the immediate with the important." Under Chair Warsh, individual data points and Fed speak may move markets less than they did under Chair Powell if Warsh adopts a more medium-term and less near-term perspective on monetary policy. The "insurance cuts" taken out at various times under Chair Powell might become less common, for example. That said, under this framework, inflection points may become less frequent but more seismic at times when the Chair attempts to change course.

Would Monetary Policy Independence Be Maintained Under a Warsh Fed?

We are of the view that Kevin Warsh as Fed Chair would not be a major threat to U.S. monetary policy independence. Warsh has argued for a "strategic reset" at the Federal Reserve after "institutional drift" and, in his view, a loss of credibility. But when it comes to monetary policy, Warsh believes Fed independence is "essential", provided that when "monetary policy outcomes are poor, the Fed should be subjected to serious questioning, strong oversight, and when they err, opprobrium".

While Warsh would likely be apt to revisit current governance and processes at the Fed, we do not think his chairmanship would greatly alter the near-term path of monetary policy. It is important to remember that monetary policy decisions are a Committee decision. There are seven governors voting at each meeting in addition to five of the 12 regional Fed presidents (Figure 4). This ensures some continuity in the makeup of the Committee as it transitions from one led by Jerome Powell to one led by Kevin Warsh. It is our view that if an incoming Chair were to propose monetary policy that is significantly out of line with what economic conditions warrant, then there would be major push back by most of the FOMC.

Of more importance to Fed independence, in our view, are the multiple legal challenges the Trump administration has brought to current Board members. The case regarding the dismissal of Fed Governor Lisa Cook is currently pending with the Supreme Court. If the court rules in favor of the administration, it could grant presidents sweeping authority to dismiss Fed governors for cause. This would set a precedent for future administrations to take advantage of and allow the executive branch to adjust the composition of the FOMC in a more material way. The Department of Justice investigation of Chair Powell's Congressional testimony similarly holds higher stakes than the appointment of a new Chair in our view. If criminal charges can be brought against FOMC members, they are more likely to bend to the president's will. Our base case is that the Supreme Court will establish a relatively high bar for dismissing a Fed governor for cause and the DOJ will not pursue charges against Powell. But if we are wrong on either front, we view such legal developments as a significantly bigger threat to Fed independence in 2026 than the appointment of Kevin Warsh as Fed Chair.

Week Ahead – Could Strong US Data Shift Focus from Trump’s Rhetoric?

- Significant market moves keep investors on their toes.

- Trump has been the primary source of volatility, mainly when targeting the Fed.

- Pivotal US data releases next week as markets adjust to potential Warsh Fed nomination.

- RBA, BoE and ECB meet next week; decent chances of surprises across the board.

- Dollar/Yen prepares for February 8 elections; gold experiences its first substantial correction.

Dollar’s outlook remains bleak

The final week of January can be safely characterized as tumultuous, given the significant market moves and the plethora of issues troubling investors’ minds. The dollar has been in the spotlight due to persistent weakness, commodities, led by gold and silver, have been making strides in uncharted waters, and the major US stock indices have been tentatively trying to post fresh all-time highs.

The root of these moves is the uncertainty stemming from US President Trump’s actions and rhetoric. Since the start of the year, he has authorized the transfer of the Venezuelan President to the US, threatened his closest European NATO allies with additional tariffs over Greenland, and is also ready to raise the punitive tariffs on imports from both Canada and South Korea.

But the dollar is mostly hurt by Trump’s strategy towards the Fed. The mid-month judicial probe targeting Fed Chair Powell, the Supreme Court case about Lisa Cook’s firing, and speculation regarding the new Fed Chair are casting a shadow over the future of one of the most respected institutions in the US. Particularly, the nomination of a ‘soft’ candidate for the Fed top spot – with the latest information pointing to Kevin Warsh being the chosen one – could put the final nail in the dollar’s coffin.

US economy is solid footing

Despite Trump’s shenanigans, the US economy is progressing well, with the Fed keeping rates constant, as widely expected. Notably, Chair Powell commented after the FOMC meeting that “the outlook for economic activity has clearly improved since the last meeting”, and “upside risks to inflation and downside risks to employment have diminished”. That said, as noted by Powell, there are some tentative signs of consumer spending fatigue, keeping expectations for two rate cuts in 2026 alive.

In the meantime, corporate America is progressing well also, with the current earnings round proving satisfactory, fueling a muted rally in risk assets, particularly on sessions during which US sovereign yields retreat. Interestingly, the S&P 500 index has never finished January in negative territory with Trump in office.

Further good news from the US labour market?

With investors being alert to Trump’s commentary and geopolitics, the focus next week will shift to the usual early-month US data releases and Fedspeak. The calendar includes the key ISM Manufacturing and Services PMI surveys, and Wednesday’s ADP employment report, but the highlight of the week is Friday’s January nonfarm payroll report. A solid 70k increase is currently forecast for the latter, maintaining the recent trend of positive prints and weakening the Fed doves’ arguments for a ‘fragile job market’.

A strong set of US data, confirming current indications for a stabilizing labour market, along with another small pullback in inflationary pressures, could offer some significant respite to the dollar. However, hawkish Fedspeak is critical for the durability of such a move. Despite the upbeat Fed meeting, and the fact that Miran voted for a 25bps cut this time, hawkish Fedspeak is not the baseline scenario at this stage.

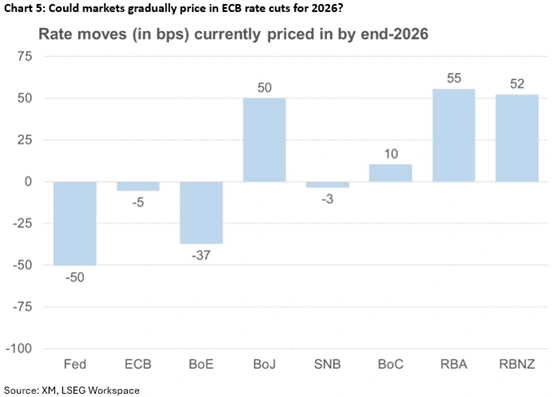

The hawkish (RBA), the boring (ECB) and the anxious (BoE)?

The dollar has been faring very poorly against most major currencies, particularly against the Antipodeans. Interestingly, the RBA, the BoE and the ECB will hold their respective rate-setting meetings next week.

After a short easing cycle, there are strong expectations of the RBA changing its course next week due to January’s robust data releases: the January S&P Global PMI surveys posted impressive jumps, the unemployment rate dropped unexpectedly to 4.1%, and, more importantly, the Q4 inflation print climbed to 3.6%.

At the December meeting, the RBA highlighted the upside risk to inflation and the tight labour market conditions, with Governor Bullock stating that “if inflation does not slow, then it will be considered at the February meeting”. Being true to her words, a 25bps rate hike will be discussed on Tuesday, with the market assigning a 72% probability to such a move.

Aussie/Dollar has climbed to the highest level since February 2023, fully taking advantage of the US dollar’s troubles and some positive momentum from China. The announcement of a rate hike will most likely result in a short-term rally, but this might prove short-lived if the accompanying statement is not hawkish enough.

Do doves still hold the upper hand at the BoE?

With developments elsewhere shifting the focus away from the UK, the pound has been benefiting from dollar troubles. Pound/dollar is up 2.3% in January – its strongest start to the year since 2019 – after an impressive 7.7% rally in 2025.

Most data prints during January produced upside surprises – particularly the robust December retail sales and the January PMI surveys – with the market currently pricing just a 5% probability of a rate cut on Thursday. Crucially, the small pickup in CPI and the sustainably elevated average earnings growth have been keeping a lid on MPC doves.

A rate cut next week would be a massive surprise, denting the pound’s recent strength against both the euro and the dollar. Similarly, a possible 5-4 voting result in favour of a pause – with Governor Baily siding with the hawks – would also threaten the pound’s current gains. On the other hand, acknowledgment of the persistent inflationary pressure might boost the pound, particularly if the quarterly inflation projections point to less steady decline over the forecast horizon.

Therefore, the pound stands to gain from a possible lack of dovish tilt and a stronger vote in support for the expected rate pause. That said, the innate dovishness of the BoE cannot be underestimated, with Bailey once again keeping both doves and hawks happy by voting for a pause and keeping rate cuts firmly on the table.

Could the ECB sound alarmed by Euro’s appreciation?

The ECB policy meeting is probably going to be the least exciting one, as no rate cut or noticeable shift in the rhetoric is expected, with President Lagarde et al. most likely remaining content with the underlying growth and inflation dynamics. However, behind-closed-doors discussions and the Q&A will focus on tariffs and the euro strength.

The threat of additional tariffs, potentially forcing eurozone governments to retaliate, and the strong Euro, which is not favoured by most eurozone countries as they are unable to compete with China and other manufacturing powerhouses, could force the ECB to reconsider its stance, putting rate cuts back in the spotlight.

All in all, the eurozone is not dazzling with its growth momentum, but stability appears to pay off. That said, it would be interesting to see if euro/dollar manages to consistently remain above 1.1908, without eurozone-based bullish catalysts.

Dollar/yen bounces higher after drop – Focus shifts to snap elections

Last week’s rate check from the New York Fed, which resulted in a significant sell-off, has probably changed the momentum in dollar/yen. Investors are wondering whether this move proves short-lived, like in April 2024, when it dropped from 160.20 to 151.85, but in just a handful of sessions it climbed, eventually reaching the 161 level. Another scenario is that it might resembles the July - September 2024 move, when actual intervention resulted in a 14% decline, which left yen bears badly bruised.

With intervention risk remaining high, the focus shifts to the February 8 snap elections. Following PM Takaichi’s comment that she will step down if her LDP party does not gain a majority in the Lower House, the stakes are exceptionally high. Based on current polls, the majority looks secure, but the yen would be under severe pressure if Takaichi’s election ‘gamble’ fails, forcing the BoJ to be activated once again in Dollar/Yen.

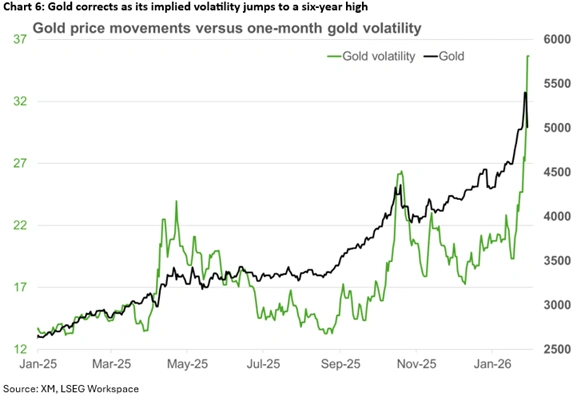

Gold and Silver correction takes place

Following the unrelenting rally since early 2025, partly due to the dollar’s persistent weakness, gold and silver investors are experiencing an overdue correction, partly signalled by the metals’ skyrocketing implied volatility. With their recent price gains being parabolic, this decline feels like a healthy reaction. That said, the bullish case for these precious metals remains intact, with geopolitics potentially in the foreground if Trump continues with his warmongering against Iran.

Weekly Focus – USD Slide Continues

The USD has continued to weaken this week with broad dollar trading at its weakest levels since 2022. This constitutes a continuous boost to the global economy, which is also linked to the surge we see in both oil and copper prices. While we think stronger global demand is the key explanation, the focus on Iran also adds a potential oil supply shock to the mix.

The FOMC kept rates on hold in an undramatic meeting. Fed chair Powell struck a balanced but positive tone as the Fed sees both reduced downside risks to the labour market and upside risks to inflation. He refrained from commenting on the recent USD weakness, and whether the move could fuel additional inflation. With a cooling labour market weighing on wage growth and the full tariff impact still ahead, we pencil in two rate cuts in March and June, ahead of investors, which are keener on July.

President Trump has pointed to Kevin Warsh as Powel's successor. Having served five years on the board during the GFC, he would be an uncontroversial choice, likely representing a balanced view on monetary policies, markets can relate to.

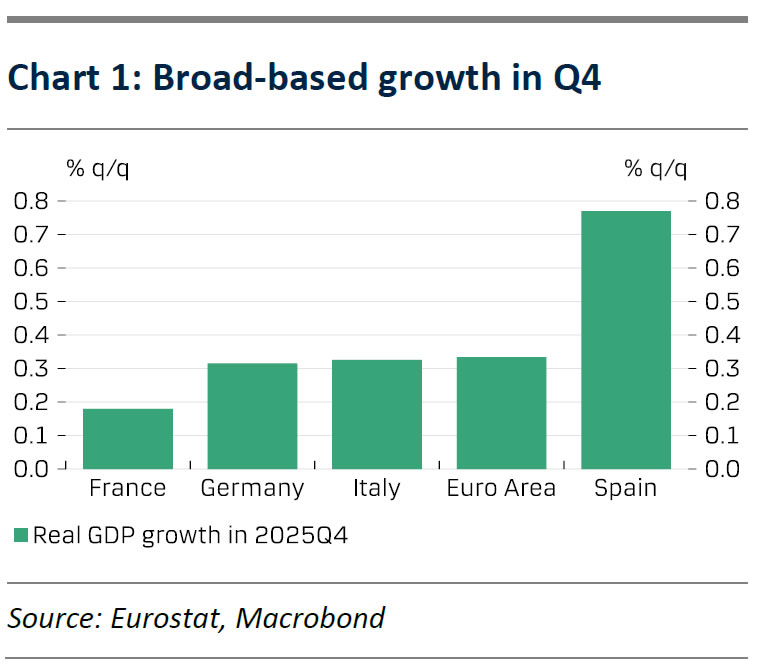

Conference Board consumer confidence unexpectedly declined as the "jobs plentiful" index fell to its lowest level since early 2021. Inflation expectations declined and thus the souring mood looks more related to the real economy than tariff concerns. US data is quite mixed these days, though. The euro area finished off 2025 with a bit more speed than expected, with q/q growth at 0.3%. With both Spain and France highlighting private spending as a growth driver, this serves as a hawkish surprise. The unemployment rate also edged back to all-time lows at 6.2% in December.

It was also the week when the EU and the world's most populous country, India landed a trade agreement that has been 20 years in the making. It will remove tariffs on over 90% of the goods traded over a period of seven years. India makes up just 2.4% of total EU exports today, so we should not expect any big short-term impact on the economy but of course, the long-term potential is significant for the EU. Next week, we expect energy prices to drag euro area inflation significantly below the inflation target in January. This supports the potential for a gradual private spending pick-up. The ECB should look through this, though, as core inflation will remain above 2%.

Both the ECB and the Bank of England (BoE) will meet to discuss monetary policy. Neither should be very eventful. We do not expect any new policy signals from president Lagarde. Data highlights how the ECB remains "in a good place". After the rate cut in December, the BoE is waiting for further disinflationary signs before we expect the final rate cut in April. We do however expect a 25bp rate hike in Australia.

We will also look out for a flood of labour market releases from the US. The most important of them being the January jobs report where we expect 60K new jobs. We also expect a downward annual benchmark revision of 1.1 million jobs. In China, we will look for PMI releases. The manufacturing PMI rebounded above the 50-threshold in December, and we expect it to be broadly flat in January held up by robust exports.

ECB Preview: Stronger Euro? No Problem

- We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday 5 February in line with consensus and market pricing.

- Lagarde is likely to face questions on the recent strengthening of the euro but provide a neutral answer, not highlighting any target level.

- We expect a muted market reaction as Lagarde refrains from giving new policy signals since the ECB awaits new staff projections in March.

We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday in line with consensus and as priced by markets. There has been a lot of geopolitical turbulence since the December meeting but in the end, it has not changed the outlook for the ECB in our view. While uncertainty and trade barriers hurt economic activity in the long run, demand is much more important for the short-term outlook. Demand is decent as the economy grew more than expected by 0.3% q/q (consensus: 0.2%, ECB staff: 0.2% q/q) in Q4 2025 and the unemployment rate fell to 6.2%. The surprise was driven by stronger-than-expected growth in Germany, Spain, and Italy while France grew as expected – still at a modest pace (see chart 1). As growth in Q4 also seemed to be driven by private consumption and it was broad-based in the eurozone this supports the “good place” assessment of the ECB.

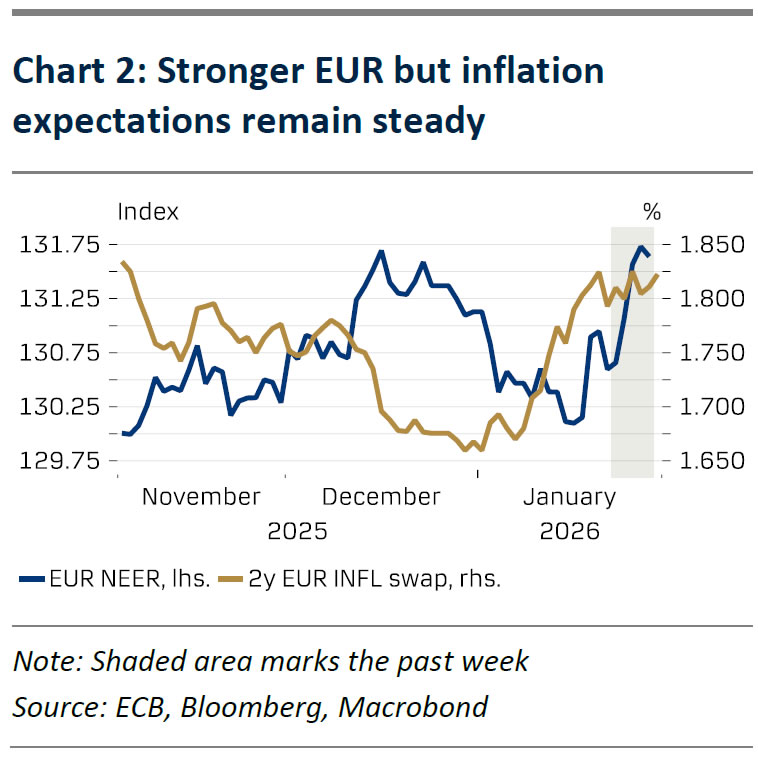

Over the past week, EUR/USD has risen above the 1.19 mark breaking out of the narrow trading range of 1.15-1.17 in H2 2025. This has reignited discussions as to whether a significant strengthening of the euro would meaningfully impact imported inflation and hence become an issue for the ECB. Yet, we note that the broad euro NEER is only 0.2% stronger compared to the December meeting and 1.0% stronger compared to the cut-off date for the latest staff projections as the recent strengthening comes after a weakening over New Year (see chart 2). A paper published by the ECB shows that a 10% appreciation of the nominal effective exchange rate reduces euro area core goods inflation by 0.25ppafter one year and headline HICP by 0.06 p.p. Importantly, we also note that inflation expectations remain steady despite the strengthening (see the shaded area in chart 2) and that a broad weakening of the USD constitutes an easing of global financial conditions (see more in RtM EUR, 30 January). Against this backdrop we do not see the magnitude of the recent EUR appreciation as a cause of concern for the ECB. Lagarde will likely face question about the euro, but we expect her to provide a neutral answer saying it is one of several variables they monitor and have no target level.

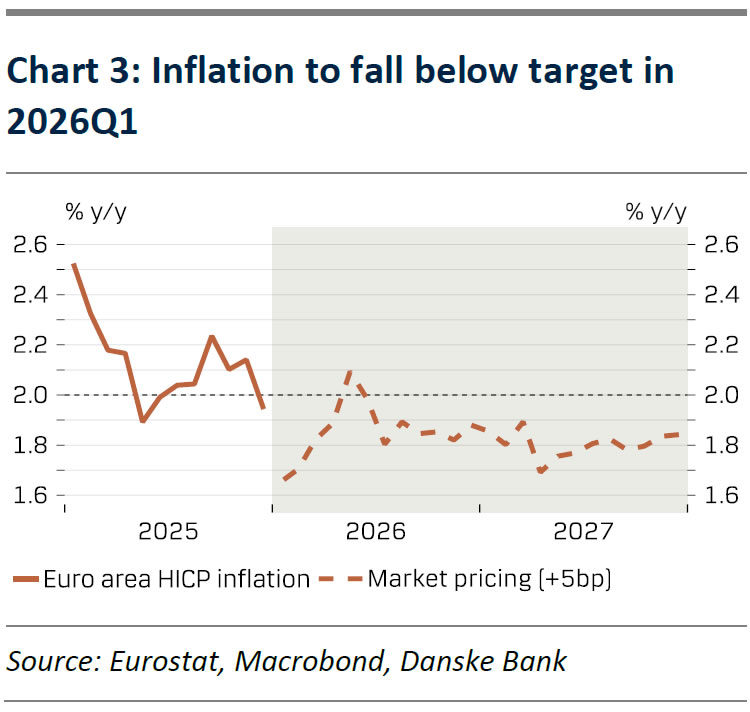

Communication since the last meeting has been supporting the “good place” assessment and indicated no near-term discussions of rate changes in the GC. Inflation in December was softer than expected particularly on core goods while the initial data from Spain and German regions suggests slightly higher than expected inflation in January. Energy base effects are expected to pull headline inflation significantly down to 1.7% y/y in 2026Q1. Yet, with growth still holding up, services inflation being sticky, and as inflation expectations anchored, we do think the bar for new rate cuts from the ECB is high. We therefore expect a muted market reaction as Lagarde refrains from giving new policy signals while the ECB awaits new staff projections in March. We keep our call of 2.00% deposit rate in 2026 and 2027.

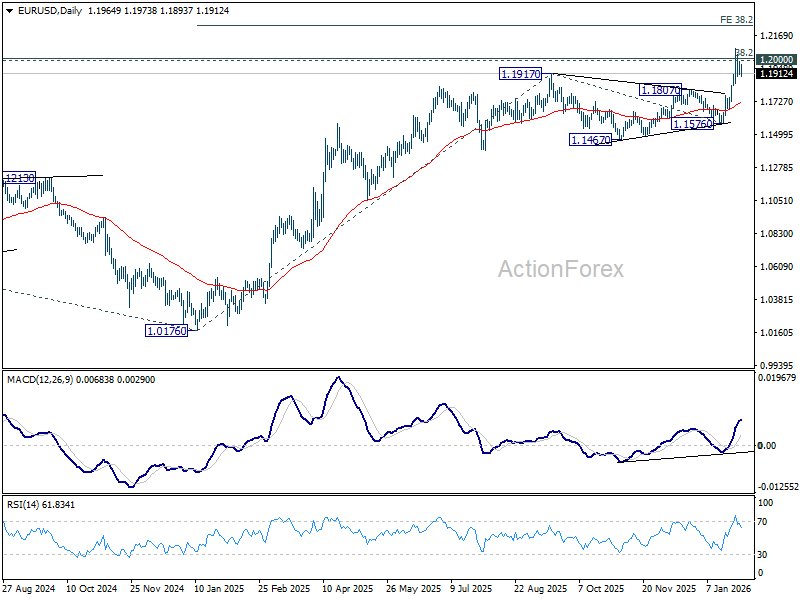

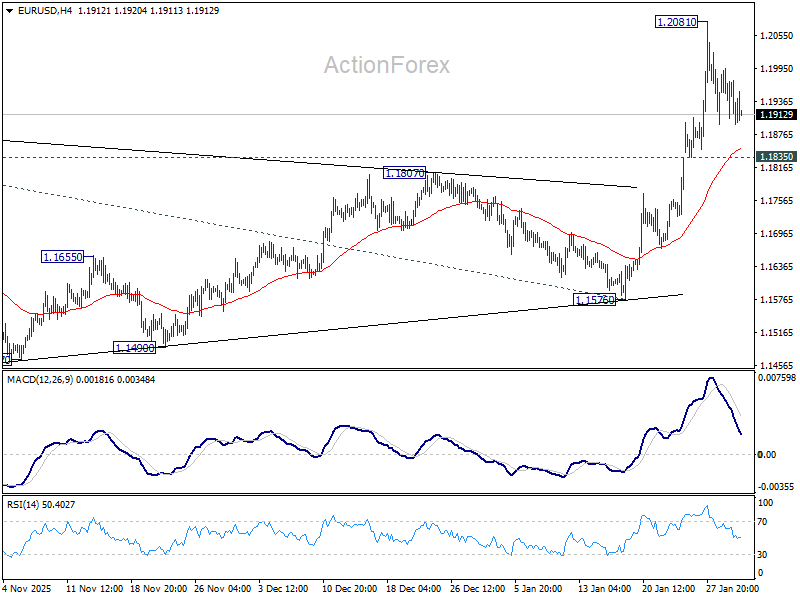

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1920; (P) 1.1958; (R1) 1.2010; More….

Outlook in EUR/USD is unchanged as consolidations continue below 1.2081. Intraday bias stays neutral, and downside of retreat should be contained by 1.1835 support. Decisive break above 1.2 will carry larger bullish implications. Next near term target will be 38.2% projection of 1.0176 to 1.1917 from 1.1576 at 1.3434. However, break of 1.1835 will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, as long as 55 W EMA (now at 1.1443) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.