Sample Category Title

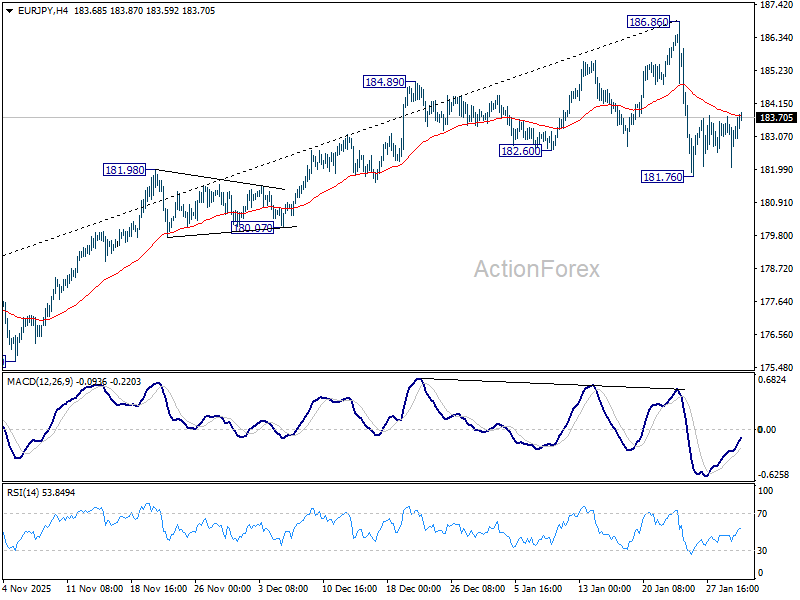

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.34; (P) 183.04; (R1) 184.00; More...

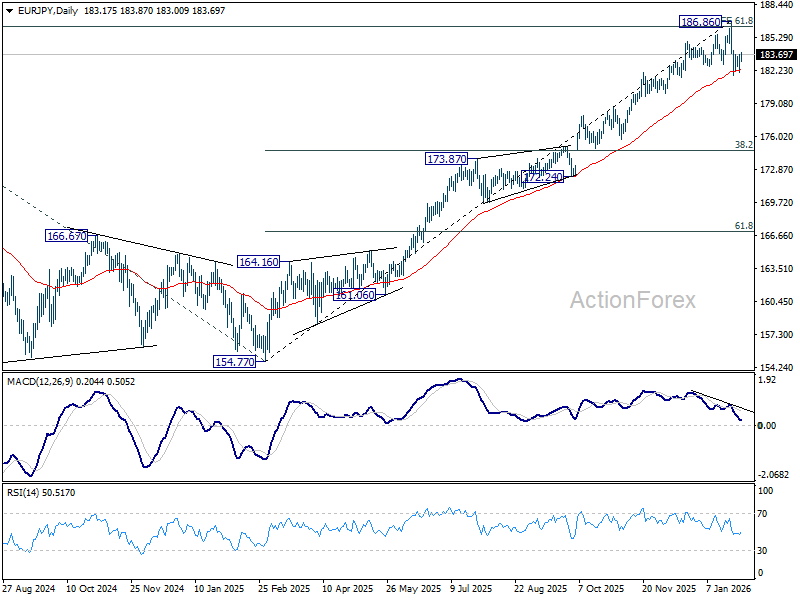

Intraday bias in EUR/JPY remains neutral for the moment. Some consolidations would be seen and risk will stay on the downside as long as 186.86 holds, in case of strong recovery. Break of 181.76 and sustained trading below 55 D EMA (now at 182.28) should solidify the case that fall from 186.86 medium term top is correcting whole rise from 154.77. Deeper decline should then be seen to 38.2% retracement of 154.77 to 186.86 at 174.60.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and and met 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 173.32) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.

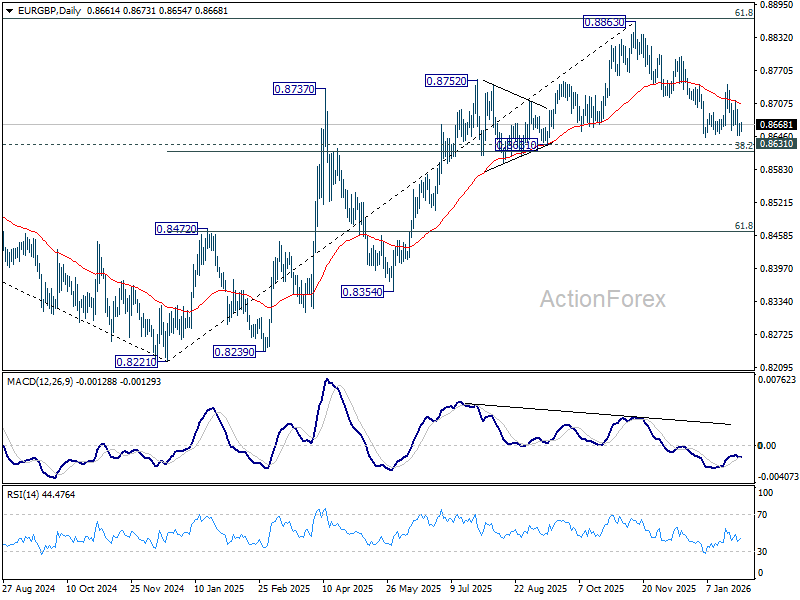

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8655; (P) 0.8663; (R1) 0.8676; More…

No change in EUR/GBP's outlook as range trading continues. Intraday bias remains neutral and risk stays on the downside with 0.8744 resistance intact. Further decline is expected to 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618). Decisive break there will carry larger bearish implications and pave the way to 61.8% retracement at 0.8466.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8625) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

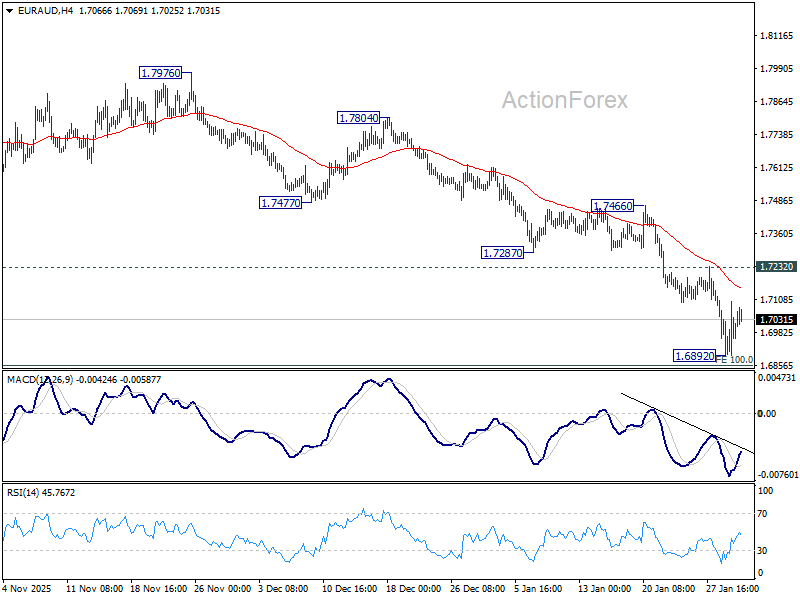

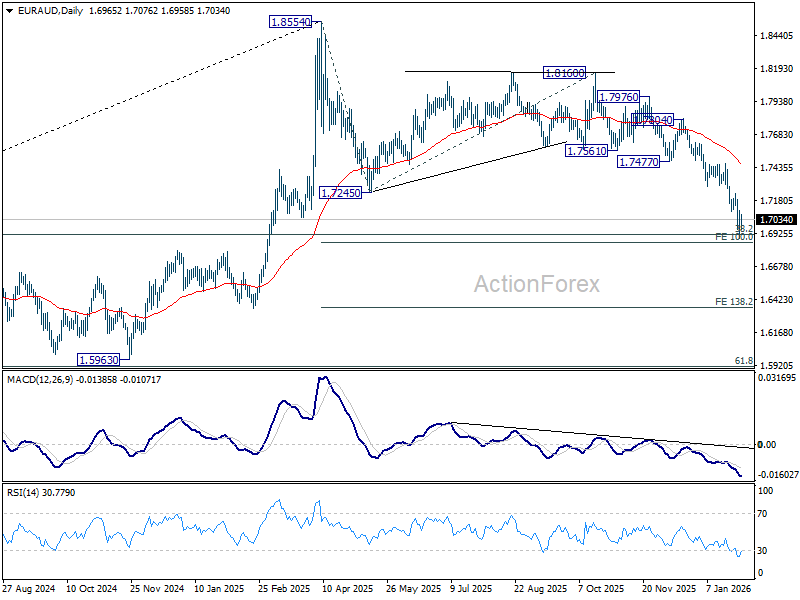

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6882; (P) 1.6992; (R1) 1.7091; More...

Intraday bias in EUR/AUD is turned neutral first with current recovery. On the upside, firm break of 1.7232 resistance should confirm strong support from 100% projection of 1.8554 to 1.7245 from 1.8160 at 1.6851. Intraday bias will be back to the upside for 1.7466 support and above. However, decisive break of 1.6851 will likely bring downside acceleration to 138.2% projection at 1.6351 next.

In the bigger picture, fall from 1.8554 is seen as correction to up trend from 1.4281 (2022 low). Strong support should be seen from 38.2% retracement of 1.4281 to 1.8554 at 1.6922 to bring rebound. However, risk will stay on the downside as long as 55 D EMA (now at 1.7473) holds. Sustained break of 1.6922 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.5913.

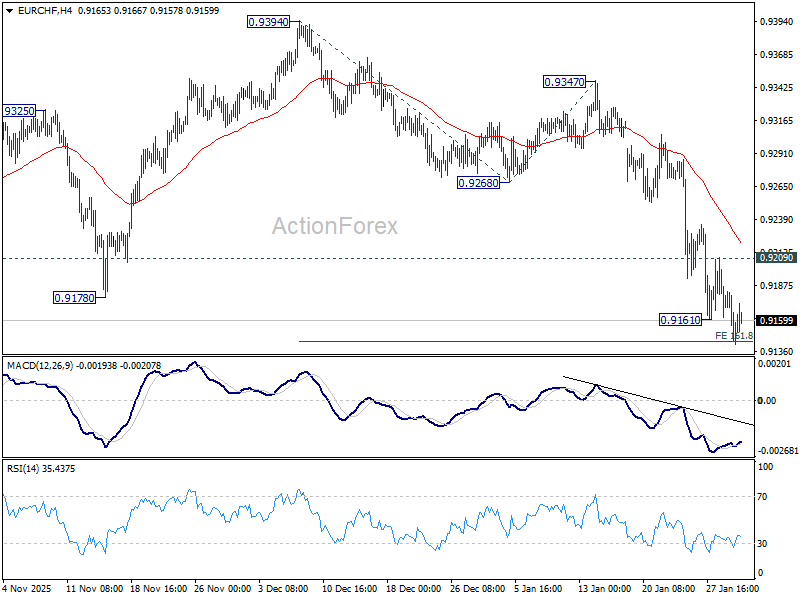

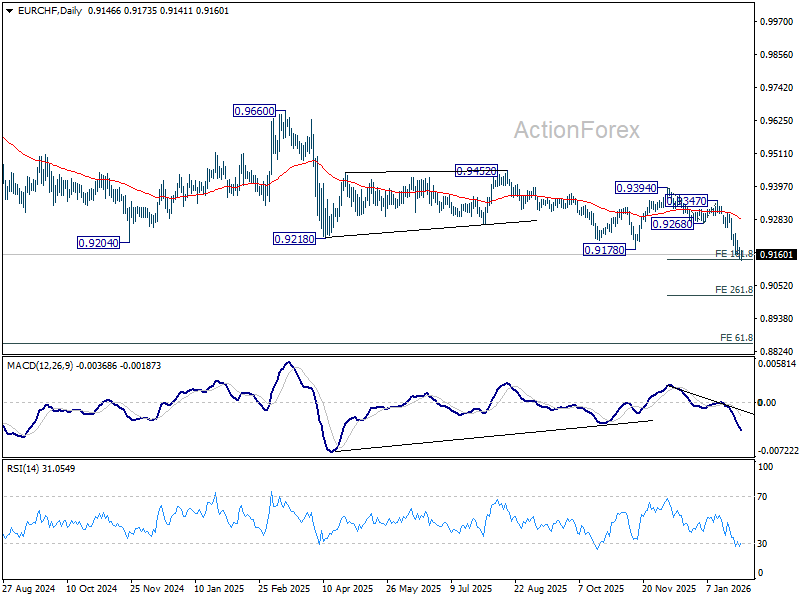

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9132; (P) 0.9164; (R1) 0.9183; More....

EUR/CHF's fall resumed after brief recovery and intraday bias is back on the downside. Decisive break of 161.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143 extend larger down trend to 261.8% projection at 0.9017. On the upside, though, break of 0.9209 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, another rejection by 55 W EMA (now at 0.9350) keeps outlook bearish. Downtrend from 1.2004 (2018 high) is still in progress. Firm break of 0.9178 will target 61.8% projection of 1.1149 to 0.9407 from 0.9928 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

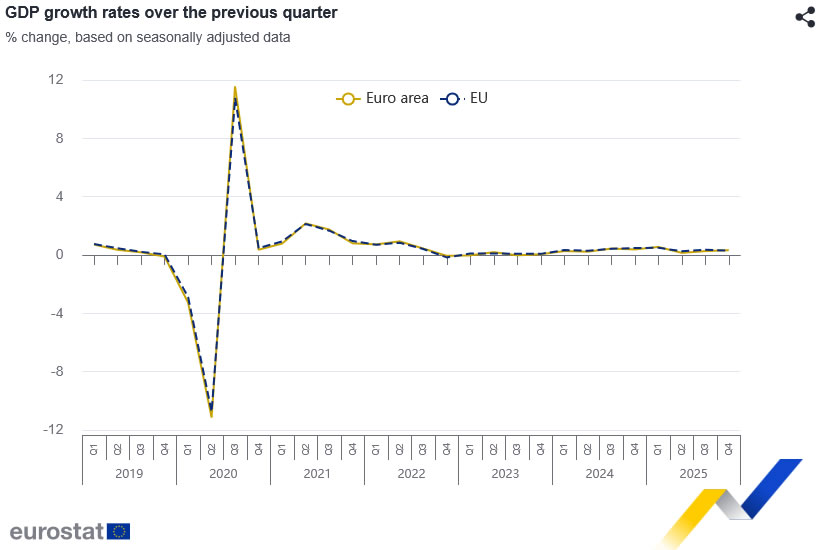

Eurozone GDP beats expectations with 0.3% qoq growth, Q4 ends on firmer note

The Eurozone economy ended 2025 on slightly firmer footing, with GDP rising 0.3% qoq in Q4, modestly above expectations of 0.2%. Growth in the wider European Union matched that pace. On an annual basis, GDP expanded 1.3% yoy in the Eurozone and 1.4% yoy in the EU, easing slightly from Q3 but still consistent with a slow and uneven recovery.

Country-level figures showed a broadly constructive picture. Lithuania (+1.7%) led quarterly gains, followed by Spain and Portugal (both +0.8%), while Ireland (-0.6%) was the only member state to record a contraction. Year-on-year growth was positive in the vast majority of reporting countries, highlighting resilience despite ongoing structural and policy headwinds.

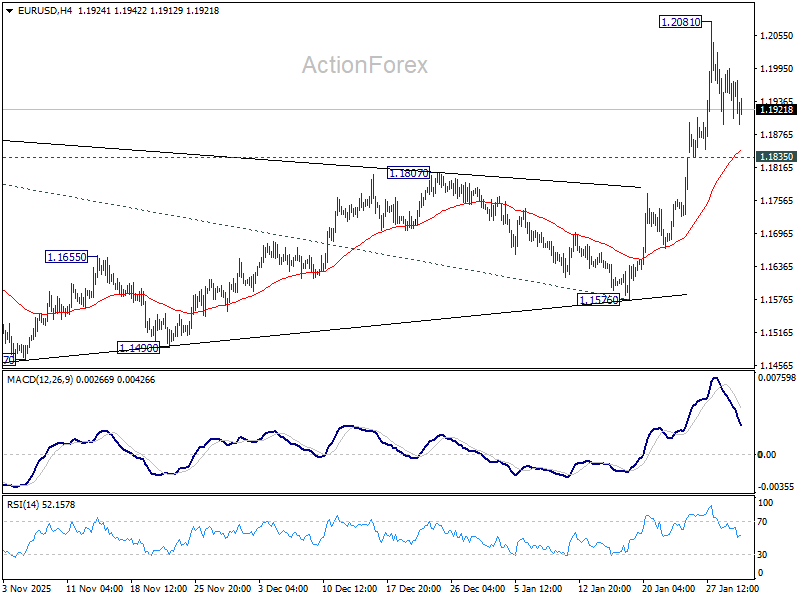

EUR/USD Moves Away from High but Remains Strong

EUR/USD fell to 1.1919 on Friday. Despite this movement, the week ends with the US dollar experiencing its second consecutive decline. Pressure on the USD is driven by heightened geopolitical tensions and uncertainty about economic policy in Washington, which is reducing investor confidence in the dollar.

The focus is on recent statements by US President Donald Trump. He threatened tariffs against countries supplying oil to Cuba and also warned Iran of possible military strikes if it refused to sign a nuclear agreement. An additional source of uncertainty was Trump's promise to announce the candidacy of a new Fed chair on Friday morning, following sustained pressure on Jerome Powell to cut rates more aggressively.

In parallel, the White House and Senate Democrats reached a preliminary agreement that avoids a government shutdown. This partially reduced short-term fiscal risks.

Earlier in the week, the dollar fell to levels not seen in almost four years after Trump expressed no concern about its weakening. Later, the US currency was supported by statements from US Treasury Secretary Scott Bessent, who remains committed to a strong dollar policy.

Technical Analysis

On the H4 chart, EUR/USD has formed a wave of growth towards 1.2080. A repeated breakdown of this resistance level may signal a continuation of the uptrend. At this stage, the pair is continuing the correction wave towards the support level of 1.1875. Technically, the correction scenario is confirmed by the MACD indicator, with its histogram and signal line both above zero, forming a downward wave. Upon completion of the correction, we anticipate the uptrend continuing towards 1.2045 and subsequently to 1.2200, with possible corrections along the way.

On the H1 chart, the pair is forming a correction after testing the resistance level. A rebound from the support level of 1.1860 would signal the formation of a new growth wave. The Stochastic oscillator's signal lines are pointing towards level 80, suggesting the uptrend may continue. Subsequently, the target for growth may be 1.2045.

Conclusion

In summary, while the EUR/USD pair has experienced a corrective pullback, the fundamental backdrop of geopolitical tensions and policy uncertainty continues to weigh on the US dollar, underpinning the euro's relative strength. Technically, the correction appears poised to complete near key support levels, with indicators on both the H4 and H1 timeframes suggesting a high probability of resuming the prevailing upward trend. The overall bias remains bullish for a potential test of higher resistance zones.

Bitcoin Breaks Key Support Level

In our 21 January note, titled “Bitcoin Falls Below $90k: Why Does It Matter?”, we confirmed the relevance of a system of two trend channels and highlighted that the price was sitting at the lower boundary of a long-term ascending channel, which had previously acted as strong support in 2025.

In that analysis, we:

→ examined the fundamental drivers behind the price decline;

→ identified a series of bearish signals reflected in BTC/USD price swings;

→ pointed to persistent selling pressure and a growing risk of a support break.

As the Bitcoin price chart shows since then:

→ the lower boundary proved its role as support once more, triggering a rebound (marked by an arrow) on 25–26 January;

→ however, bullish momentum only carried the price up to the psychological $90k level, which acted as resistance on 28 January.

Following this, Bitcoin began to move lower. During the decline, the price successfully broke the key support level, with accelerating downward momentum in BTC/USD confirming that the support had lost its strength.

The lower boundary of the red channel may still act as support, while a potential break below November’s low could trigger panic. In the coming days, a local recovery toward the red channel’s median is possible, especially after signs of oversold conditions.

Overall, the long-term ascending channel on the BTC/USD chart is losing relevance, while the descending trend is becoming increasingly dominant.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service (additional fees may apply). Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

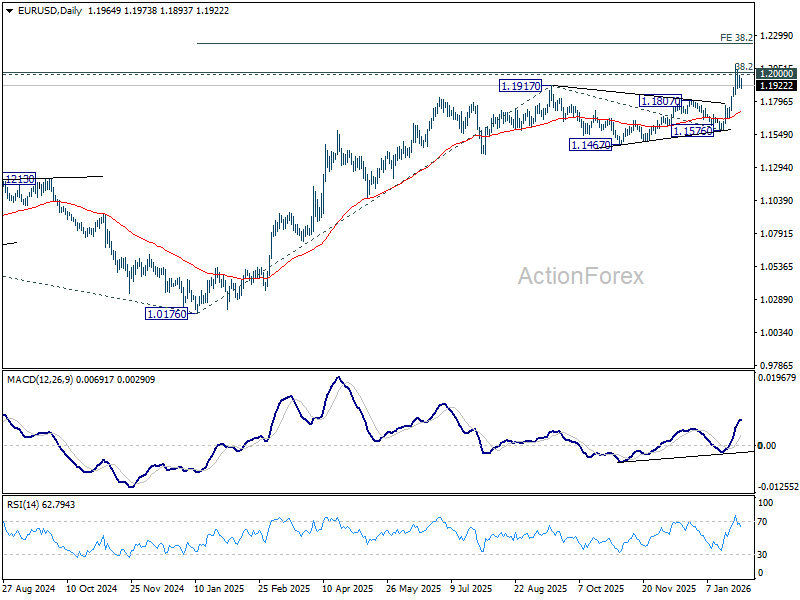

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1920; (P) 1.1958; (R1) 1.2010; More….

Intraday bias in EUR/USD remains neutral and more consolidations could be seen below 1.2081. But downside of retreat should be contained by 1.1835 support. Decisive break above 1.2 will carry larger bullish implications. Next near term target will be 38.2% projection of 1.0176 to 1.1917 from 1.1576 at 1.3434. However, break of 1.1835 will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, as long as 55 W EMA (now at 1.1443) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

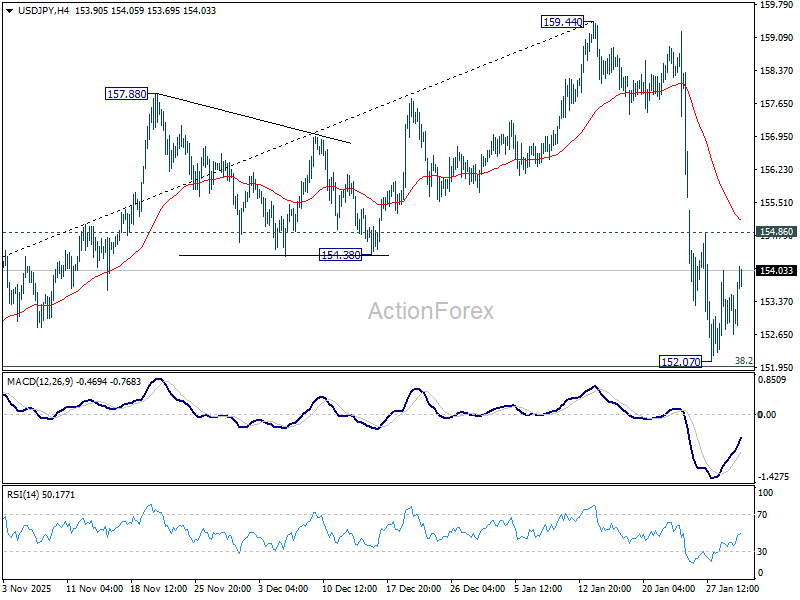

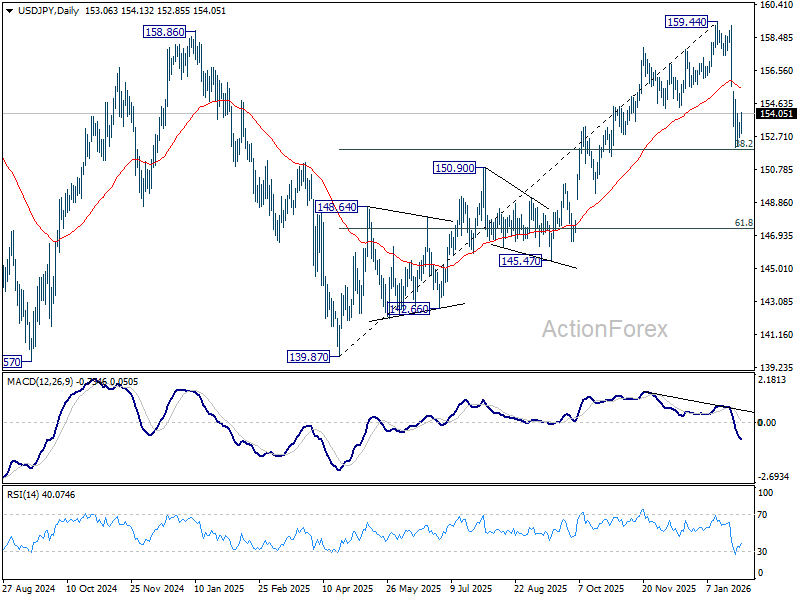

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.69; (P) 153.12; (R1) 153.54; More...

No change in USD/JPY's outlook and intraday bias stays neutral. As noted before, fall from 159.44 is seen as correcting the rise from 139.87. Strong support should be seen from 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound, at least on first attempt. On the upside above 154.86 minor resistance will turn intraday bias to the upside for recovery. However, decisive break of 151.96 will argue that it is reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.35) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

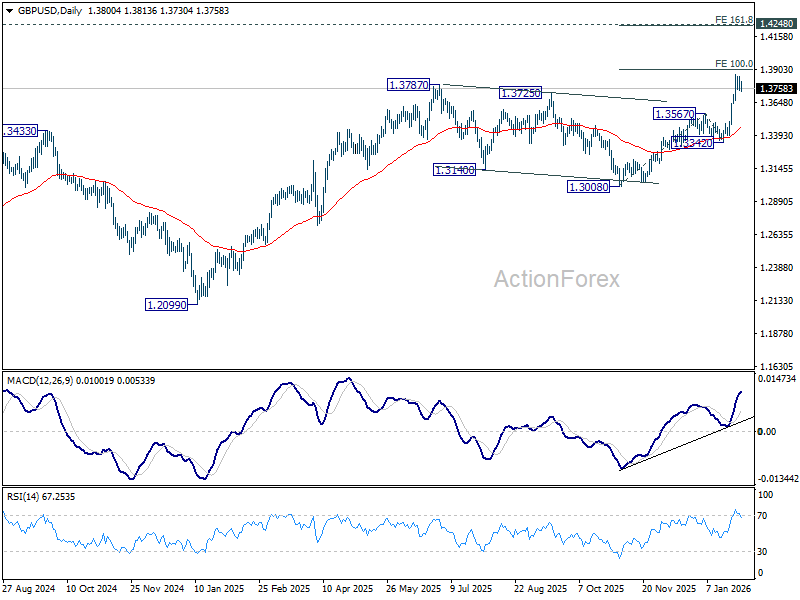

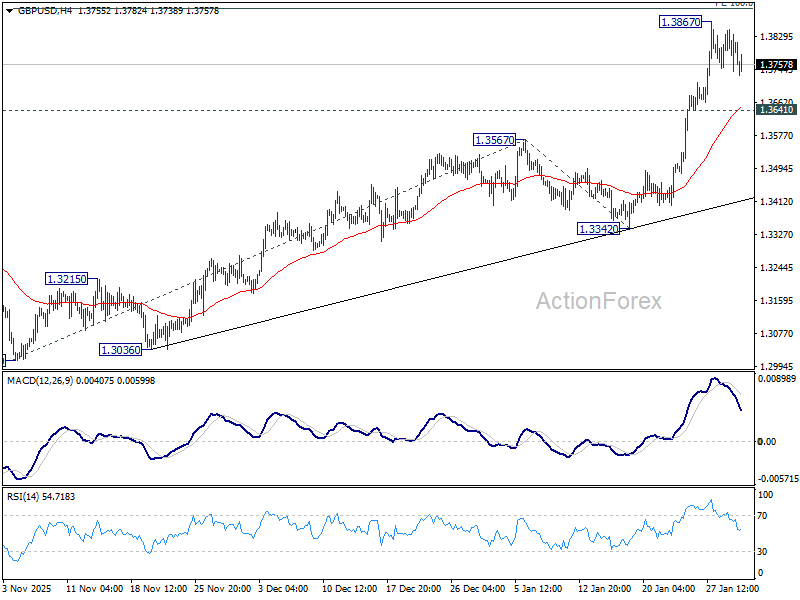

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3753; (P) 1.3801; (R1) 1.3858; More...

Intraday bias in GBP/USD remains neutral as consolidations continue below 1.3867 temporary top. Downside should be contained by 1.3641 to bring another rally. Firm break of 100% projection of 1.3008 to 1.3567 from 1.3342 at 1.3901 will pave the way to 161.8% projection at 1.4246, which is close to 1.4248 key structural resistance. However, break of 1.3641 will turn bias to the downside for deeper pullback.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.