Sample Category Title

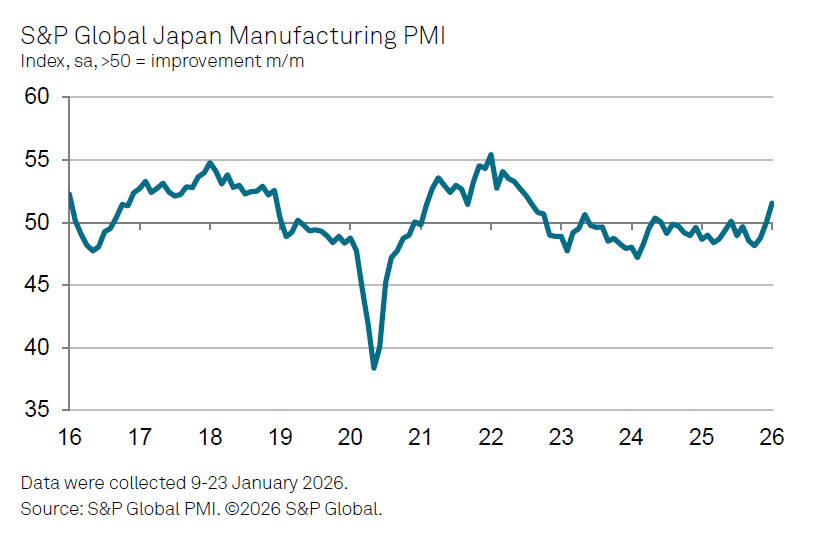

Japan PMI manufacturing finalized at 51.5, growth returns, inflation a risk

Japan’s manufacturing sector returned to expansion in January, with PMI Manufacturing finalized at 51.5. This marks the first improvement in operating conditions since mid-2025 and represents the strongest rate of growth since August 2022, offering early evidence of a cyclical recovery taking hold.

The details were encouraging. S&P Global Market Intelligence noted that output and new orders recorded their sharpest increases in almost four years, while export demand rose for the first time since 2022. Employment growth also accelerated to its fastest pace since September 2022, suggesting the sector is "gearing up for further increases in output in the months ahead."

That said, cost pressures are resurfacing as a potential constraint. Input price inflation climbed to a near one-year high, driven in part by the weaker yen, and firms passed some of those costs on to customers. Whether these price pressures intensify will be key in assessing how durable the recovery proves to be.

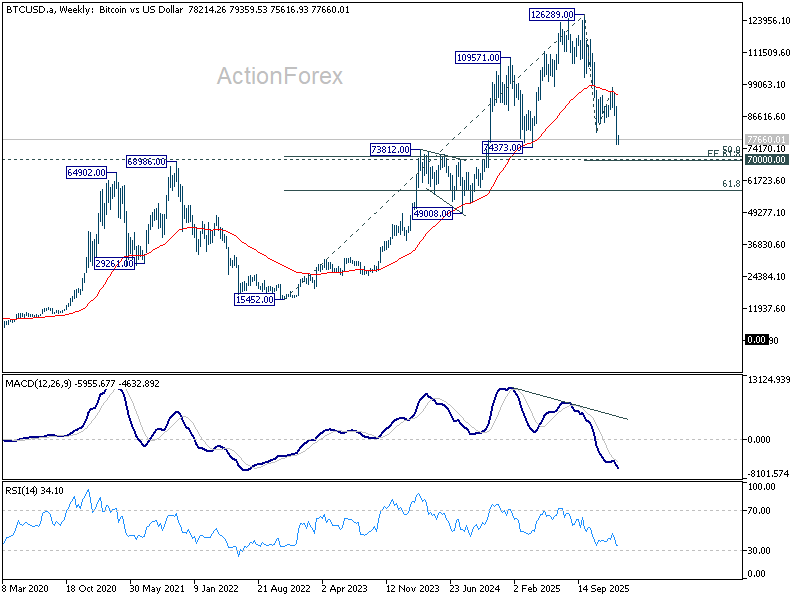

Bitcoin breaks down, 70k becomes critical test for broader market sentiment

Bitcoin remains under heavy pressure after plunging late last week, with prices still struggling to regain 80,000. The selloff closely follows last week’s crash in precious metals, suggesting a shared catalyst of US President Donald Trump’s decision to nominate Kevin Warsh as the next Fed chair.

For now, broader risk assets have so far absorbed the shock. Equity indexes and volatility measures remain relatively calm, indicating that investors are not yet pricing in a wider risk-off regime. That calm, however, may prove misleading. Given Bitcoin’s persistent correlation with tech stocks, sustained weakness in crypto could serve as an early warning signal that underlying sentiment is deteriorating beneath the surface, even as traditional risk gauges remain resilient.

Technically, the damage is already done. The break below 80,492 confirms that Bitcoin's broader downtrend from 126,289 record high has resumed. As long as 84,380 support turned resistance holds, deeper decline should be seen to 61.8% projection of 126,289 to 80,492 from 97,922 at 69,619, which is slightly below 70k psychological level.

This target sits just beneath the key 70,000 psychological level, making that zone a critical battleground between medium-term bulls and bears. It coincides with 50% retracement of the entire 2022–2025 advance. A strong rebound from that zone would keep the post-peak price action in a medium-term sideway consolidation. However, decisive break would open the door to deeper unwind toward 49,008.

Should that bearish scenario unfolds, close monitoring of NASDAQ will be essential, as confirmation from equities would point to broader liquidation across risk markets rather than a crypto-only reset.

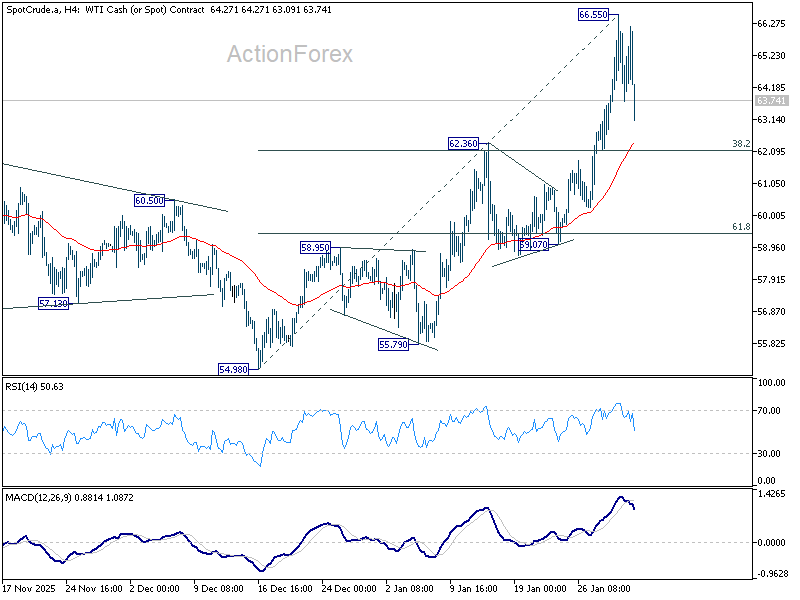

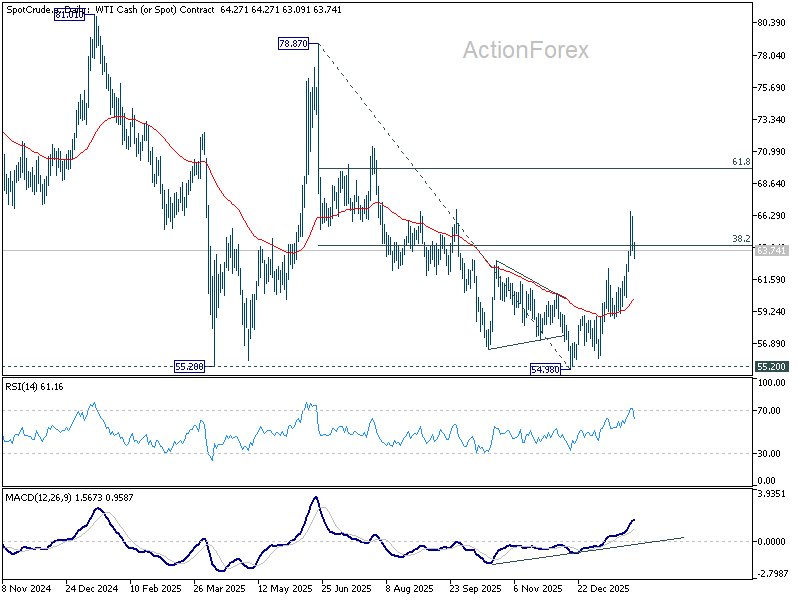

WTI oil rally pauses on OPEC+ hold, bullish trend reversal still intact for 70 later

Oil prices edged lower today after OPEC+ agreed to keep output unchanged for March. Sunday’s brief meeting reaffirmed earlier decisions to freeze planned output increases through the first quarter of 2026.

Those increases—amounting to roughly 2.9 million barrels per day—were scheduled to be phased in from April through December 2025 by eight producers, including Saudi Arabia and Russia, representing about 3% of global demand. With seasonal consumption typically weaker early in the year, the group has opted to stay patient.

What stood out was not what OPEC+ said, but what it avoided saying. The statement offered no clues on production plans beyond March, effectively keeping all options open. With U.S.–Iran tensions rising and crude prices having pushed to six-month highs last week on fears of potential military escalation, that strategic ambiguity is likely intentional.

Against that backdrop, today’s pullback in WTI looks more corrective than trend-changing. Technically, the dip helps confirm a short-term top at 66.55. WTI now appears to be consolidating the five-wave rally from the 54.98 low. While deeper retracement cannot be ruled out in the near term, downside should be limited. Strong support is expected near the 38.2% retracement of 54.98 to 66.55 at 62.13, where buying interest is likely to re-emerge.

Beyond the short-term noise, the broader technical picture has improved materially. The earlier break above 38.2% retracement of 78.87 to 54.98 at 64.10 argues that the entire sell-off from last year’s highs has likely been completed. In that context, the rise from 54.98 is tentatively viewed as the third leg of the larger pattern that began at 55.20. As long as the 55 D EMA (now at 60.14) holds, the medium-term bias remains to the upside for 61.8% retracement at 69.74 and potentially beyond at a later stage.

Unless geopolitical risks—particularly around Iran—ease decisively, any near-term dips may continue to attract buyers rather than signal a reversal.

Eco Data 2/2/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 00:00 | AUD | TD-MI Inflation Gauge M/M Jan | 0.20% | 1% | ||

| 00:30 | JPY | Manufacturing PMI Jan F | 51.5 | 51.5 | 51.5 | |

| 01:45 | CNY | RatingDog Manufacturing PMI Jan | 50.3 | 50.3 | 50.1 | |

| 07:00 | EUR | Germany Retail Sales M/M Dec | 0.10% | -0.20% | -0.60% | |

| 07:30 | CHF | Real Retail Sales Y/Y Dec | 2.90% | 2.50% | 2.30% | |

| 08:30 | CHF | Manufacturing PMI Jan | 48.8 | 47.9 | 45.8 | |

| 08:50 | EUR | France Manufacturing PMI Jan F | 51.2 | 51 | 51 | |

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 49.1 | 48.7 | 48.7 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 49.5 | 49.4 | 49.4 | |

| 09:30 | GBP | Manufacturing PMI Jan F | 51.8 | 51.6 | 51.6 | |

| 14:30 | CAD | Manufacturing PMI Jan | 50.4 | 48.6 | ||

| 14:45 | USD | Manufacturing PMI Jan F | 52.4 | 51.9 | 51.9 | |

| 15:00 | USD | ISM Manufacturing PMI Jan | 52.6 | 48.3 | 47.9 | |

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | 59.0 | 59.3 | 58.5 | |

| 15:00 | USD | ISM Manufacturing Employment Index Jan | 48.1 | 44.9 |

| 00:00 | AUD |

| TD-MI Inflation Gauge M/M Jan | |

| Actual | 0.20% |

| Consensus | |

| Previous | 1% |

| 00:30 | JPY |

| Manufacturing PMI Jan F | |

| Actual | 51.5 |

| Consensus | 51.5 |

| Previous | 51.5 |

| 01:45 | CNY |

| RatingDog Manufacturing PMI Jan | |

| Actual | 50.3 |

| Consensus | 50.3 |

| Previous | 50.1 |

| 07:00 | EUR |

| Germany Retail Sales M/M Dec | |

| Actual | 0.10% |

| Consensus | -0.20% |

| Previous | -0.60% |

| 07:30 | CHF |

| Real Retail Sales Y/Y Dec | |

| Actual | 2.90% |

| Consensus | 2.50% |

| Previous | 2.30% |

| 08:30 | CHF |

| Manufacturing PMI Jan | |

| Actual | 48.8 |

| Consensus | 47.9 |

| Previous | 45.8 |

| 08:50 | EUR |

| France Manufacturing PMI Jan F | |

| Actual | 51.2 |

| Consensus | 51 |

| Previous | 51 |

| 08:55 | EUR |

| Germany Manufacturing PMI Jan F | |

| Actual | 49.1 |

| Consensus | 48.7 |

| Previous | 48.7 |

| 09:00 | EUR |

| Eurozone Manufacturing PMI Jan F | |

| Actual | 49.5 |

| Consensus | 49.4 |

| Previous | 49.4 |

| 09:30 | GBP |

| Manufacturing PMI Jan F | |

| Actual | 51.8 |

| Consensus | 51.6 |

| Previous | 51.6 |

| 14:30 | CAD |

| Manufacturing PMI Jan | |

| Actual | 50.4 |

| Consensus | |

| Previous | 48.6 |

| 14:45 | USD |

| Manufacturing PMI Jan F | |

| Actual | 52.4 |

| Consensus | 51.9 |

| Previous | 51.9 |

| 15:00 | USD |

| ISM Manufacturing PMI Jan | |

| Actual | 52.6 |

| Consensus | 48.3 |

| Previous | 47.9 |

| 15:00 | USD |

| ISM Manufacturing Prices Paid Jan | |

| Actual | 59.0 |

| Consensus | 59.3 |

| Previous | 58.5 |

| 15:00 | USD |

| ISM Manufacturing Employment Index Jan | |

| Actual | 48.1 |

| Consensus | |

| Previous | 44.9 |

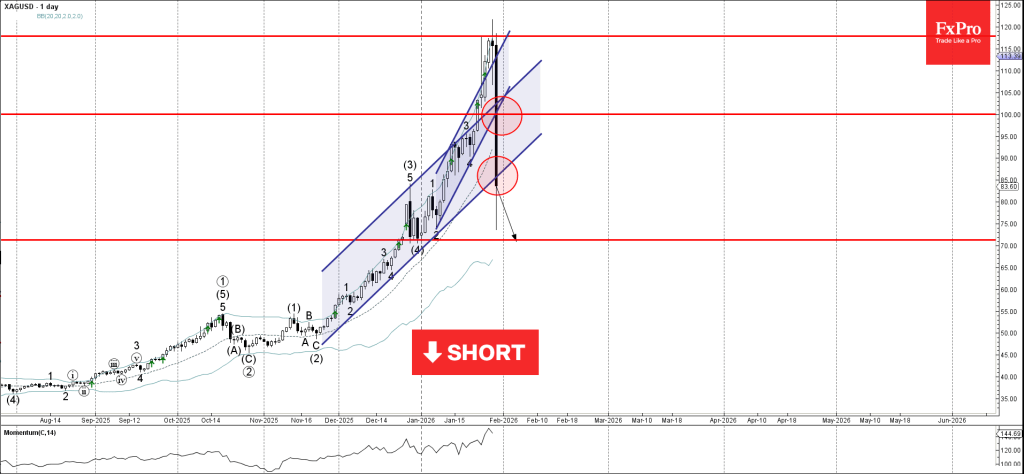

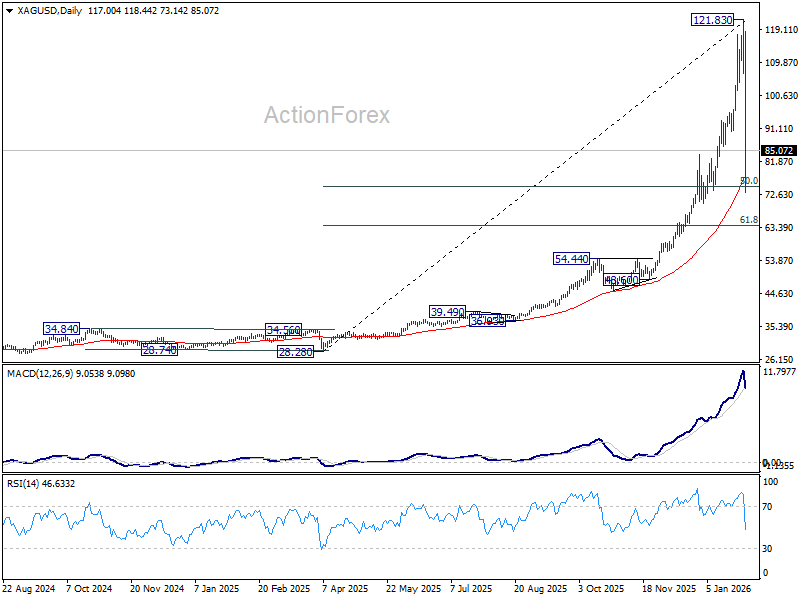

Silver Wave Analysis

Silver: ⬇️ Sell

- Silver broke the round support level 100.00

- Likely to fall to support level 70.00

Silver under strong bearish pressure after the price broke the round support level 100.00, intersecting with two up channels from January and November.

The price just broke the lower trendline of the daily up channel from November – indicating further losses for Silver ahead.

Silver can be expected to fall to the next round support level 70.00, which stopped the previous intermediate correction (4) in December.

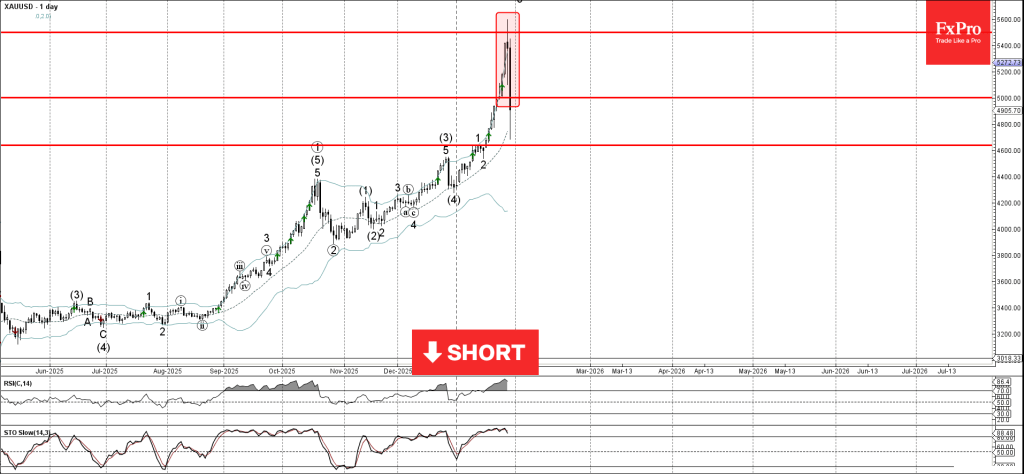

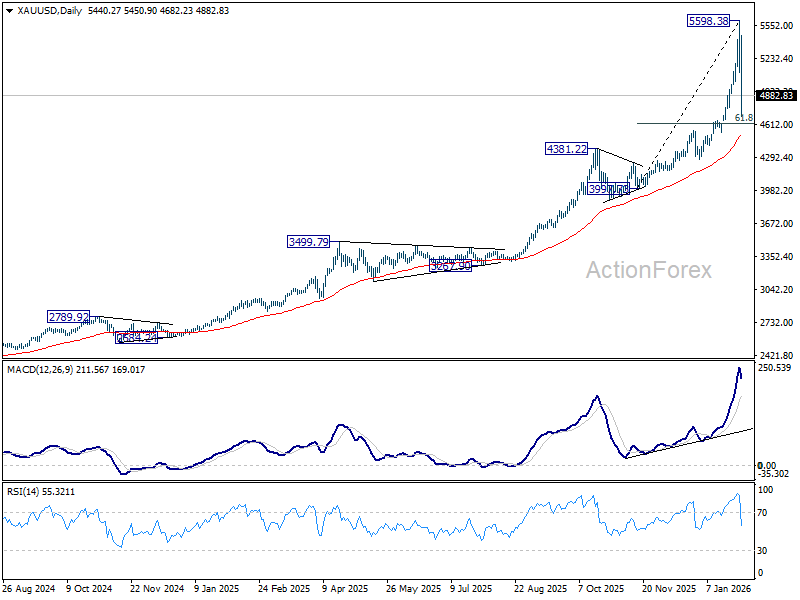

Gold Wave Analysis

Gold: ⬇️ Sell

- Gold formed daily Evening Star

- Likely to fall to support level 4600.00

Gold today fell down sharply after the price failed to close above the major resistance level 5500.00, as can be seen from the daily Gold chart below.

The downward reversal from the resistance level 5500.00 formed the daily Japanese candlesticks reversal pattern long-legged Doji – which is now the middle candle of the daily Evening Star.

Given the overbought Stochastic and RSI, Gold can be expected to fall to the next support level 4600.00 (former top if wave 1 from the start of January).

A Credible Fed Choice Tames Tail Risks, Not the Cycle

Last week delivered yet another reminder that volatility has become a feature this year, rather than an exception. Sudden repricing episodes continue to emerge, often driven by political and institutional developments rather than changes in economic fundamentals.

The latest bout of turbulence was triggered by market repricing around the nomination of former Fed Governor Kevin Warsh as the next Federal Reserve chair. The move forced a rapid reassessment of risks that had built up over monthly weeks, unleashing violent adjustments in select corners of the market.

The intensity of the reaction, however, was far from uniform. While precious metals experienced dramatic swings, other asset classes showed far more restraint. Equities and Treasuries largely stayed within familiar ranges, hinting that the shock was narrowly concentrated rather than systemic.

That divergence mattered. It suggested that markets were not questioning the broader economic outlook or the Fed’s near-term policy path, but instead recalibrating around perceived shifts in institutional risk and long-term credibility.

In currency markets, Dollar staged a late-week rebound but still finished as the worst performer overall, followed by Euro and Sterling. At the other end, Kiwi led gains, with Aussie and Swiss Franc close behind. Yen and Loonie ended the week mixed, reflecting cross-currents rather than a clear directional bias.

Gold and Silver Exodus: When the Party Ends

The most dramatic action unfolded in precious metals. Gold and Silver surged to fresh record highs, only to suffer violent reversals that erased weeks of gains in a matter of house. Gold briefly peaked near 5,598 before collapsing to close the week around 4882, a drawdown of more than 13% from the high. Silver’s reversal was even more brutal, plunging from a record 121.81 to 85.07, a decline of roughly 30%. These are classic signs of terminal momentum, not healthy consolidation.

Such price behavior strongly suggests that major tops have been formed. While this does not invalidate the longer-term bullish trend, it does mark the end of the one-way, momentum-driven phase that had defined the previous rallies.

Technically, both metals have now transitioned into a corrective phase. This distinction is critical. Corrections following blow-off tops are rarely clean or directional. Instead, they tend to be prolonged, erratic, and psychologically punishing.

The problem is not just direction—it is structure. At this stage, price action can morph into any number of patterns: flats, zigzags, triangles, or complex combinations. Early in a correction, it is impossible to know which will dominate, making risk-reward unattractive for all but the most tactical traders.

During such phases, short-term speculators take control. Whipsaws become frequent, false breakouts multiply, and both longs and shorts are routinely punished. Trend-following strategies fail, while mean-reversion trades become increasingly unstable.

Fundamentally, corrections also represent a breakdown in narrative clarity. The dominant bullish story—Fed politicization, institutional erosion, currency debasement—has been partially challenged. New information has arrived, but it remains unclear whether it represents a regime shift or temporary noise.

This ambiguity is toxic for positioning. When conviction dissolves, markets no longer reward holding risk. Instead, they reward speed, flexibility, and capital preservation—qualities that most investors do not associate with Gold and Silver exposure.

For professional traders, opportunity may still exist on very short timeframes. But for investors and medium-term participants, the odds are stacked against clean outcomes. Capital can be deployed more efficiently elsewhere while metals reset.

In short, Gold and Silver are not broken, but they are no longer tradable with confidence, not at least in the near term. Until volatility compresses, structures mature, and sentiment stabilizes, the prudent course is to step aside and wait for clarity to return.

Why Warsh Mattered: Experience, Symbolism, and Institutional Lines

The nomination of Kevin Warsh as the next Fed chair was never just about a personnel change. It carried outsized significance because it arrived after weeks of market anxiety over the future independence and credibility of the US central bank.

Warsh is not a newcomer to monetary policy. He served as a Fed governor from 2006 to 2011, spanning the global financial crisis, where he was deeply involved in emergency liquidity measures, bank rescues, and the early phases of unconventional policy. That experience still carries weight in financial circles.

Before joining the Fed, Warsh built his career on Wall Street and in public service, giving him fluency in both market mechanics and policymaking. That dual background has long made him a familiar and generally respected figure among investors, particularly those concerned with institutional continuity.

In the weeks leading up to the decision, markets had focused on Kevin Hassett, the National Economic Council director, as a frontrunner. Hassett’s perceived dovish leanings mattered, but more importantly, his proximity to the White House raised fears of overt political influence over monetary policy.

Those fears had real market consequences. Investors began to price in a more severe erosion of Fed independence, accelerating flows into hard assets and amplifying volatility in Gold and Silver. The assumption was not just easier policy, but a structural shift in how policy decisions would be made.

Against that backdrop, Warsh’s selection was widely interpreted as a line drawn. While he is not immune to political pressure, he is not seen as an extension of the executive branch either. His appointment suggested that there are still boundaries around how far presidential influence over the Fed can stretch.

The symbolism mattered as much as the individual. Rather than installing a close political ally, US President Donald Trump opted for a figure with established Fed credentials and institutional legitimacy. That choice sent a message that continuity, at least in form, still matters.

For markets, this did not mean a reversal of policy direction or an abrupt shift in rate expectations. But it did mean that the most extreme scenarios around politicization were dialed back, helping to stabilize expectations—even if deeper questions about the Fed’s future remain unresolved.

Relief, Not Repricing: What Warsh Did—and Didn’t—Change

Despite the violent reaction in precious metals, the short answer to whether Kevin Warsh’s appointment materially changed the macro outlook is no. Once the initial shock passed, other parts of the market sent a clear signal: expectations around growth, inflation, and monetary policy remain largely intact.

Most tellingly, Fed rate cut pricing barely moved. Futures continue to imply roughly a 60% chance of a 25bp cut by the end of June, little changed from the prior week. If markets believed Warsh marked a meaningful hawkish turn, that pricing would have shifted decisively.

The Federal Open Market Committee’s own behavior reinforced that message. While Stephen Miran and Christopher Waller dissented in favor of a cut at the last meeting, the majority opted to hold rates at 3.50–3.75%, maintaining a cautious, wait-and-see stance. That internal balance remains unchanged.

After delivering three risk-management cuts last year, policymakers appear content to pause and assess incoming data. Inflation has cooled but remains exposed to upside risks, while employment has stabilized rather than weakened decisively. In that environment, urgency to ease further is limited.

Crucially, the Warsh appointment does not remove the wild cards facing the Fed. Rising oil prices linked to Iran instability, renewed trade tensions with the EU and Canada, and the broader geopolitical backdrop all complicate the inflation outlook in ways that argue for caution rather than haste.

Equity and bond markets reflected this realism. US stocks did not break out of established ranges, and Treasury yields continued to trade sideways. There was no confirmation of a regime shift—just selective repositioning.

This contrast with precious metals is important. Gold and silver reacted violently because they were pricing institutional decay scenarios that were partially unwound. Other asset classes, which had not embraced those extremes, had far less to reverse.

In that sense, Warsh’s appointment reduced tail risk, but it did not rewrite the base case. The Fed remains data-dependent, the policy path remains conditional, and markets are still operating in a world where uncertainty—not clarity—dominates decision-making.

DOW and 10-Year Yield Stay Caged

US equities continued to trade within established ranges. DOW struggled to sustain upside traction below the 50,000 psychological level, with price action reflecting indecision rather than conviction.

Technically, the picture is mixed. On the supportive side, DOW is still holding comfortably within its medium-term rising channel and above the rising 55 D EMA (now at 48,316.64), which continues to offer dynamic support and argues against an immediate trend reversal.

At the same time, warning signs persist. Bearish divergence in D MACD remains unresolved, suggesting upside momentum is fading. This divergence limits confidence in any clean breakout and keeps the risk of a corrective phase alive.

For now, the path of least resistance still points higher, with a break above 50,000 marginally favored. But even in that scenario, upside is unlikely to be smooth. Technical resistance is expected near 78.6% projection of 41,981.14 to 48,431.57 from 45,728.93 at 50,798.97 to limit upside.

On the other hand, Decisive break below 55 D EMA would shift the balance more clearly toward a medium-term correction. That level remains the key fault line between continuation and consolidation, and it has yet to be tested convincingly.

Treasury markets told a similar story of restraint. US 10-year yield continued to oscillate in a tight range above 4.200, after briefly spiking to 4.311 earlier in January. There was no sustained follow-through in either direction.

For now, outlook is unchanged that rise from 3.947 is reversing whole fall from 4.629. Further rally is expected as long as 55 D EMA (now at 4.168) holds. Another rise should be seen back to 61.8% retracement of 4.629 to 3.947 at 4.368. Firm break there will pave the way back 4.628 resistance.

Dollar’s Problems Run Deeper Than the Fed: Euro Normalization and Yen Asymmetry

Even with the Warsh appointment reducing some tail risks, Dollar remains vulnerable to forces that extend well beyond Fed leadership. Chief among these are developments in the Euro and Yen, both of which continue to exert structural pressure on the greenback.

In Europe, the debate around a stronger Euro has quietly shifted. What once sounded like fringe speculation—EUR/USD pushing decisively above 1.20—is now being discussed more openly by market participants. That change in tone matters. Acceptance often precedes price. Euro’s resilience is not built on rapid growth, but on relative stability. The ECB has little incentive to aggressively lean against currency strength. As long as that remains the case, Euro appreciation becomes a feature rather than a bug.

From a flow perspective, diversification out of US assets continues to favor Euro. Reserve managers, institutional investors, and long-term allocators are reassessing concentration risk after years of Dollar dominance. That process is slow, but persistent—and difficult to reverse with a single personnel change at the Fed.

Japan presents a different, but equally powerful, challenge to Dollar. The upcoming snap election remains a major wild card, even if Prime Minister Sanae Takaichi is still expected to secure a solid result. Markets have learned the hard way that political certainty should never be taken for granted.

Any unfavorable election outcome—or even a weaker-than-expected mandate—could trigger a sharp selloff in Japanese equities. Such a move would likely unwind the crowded “Takaichi trade,” forcing capital back into Yen at speed.

That matters because Yen strength tends to feed on itself. Equity weakness, falling foreign asset exposure, and hedging demand can combine to produce outsized currency moves that are difficult for authorities to counter quickly.

In that context, Dollar faces a pincer movement. Euro appreciation reflects gradual, structural diversification, while Yen strength would arrive through sudden, risk-driven adjustments. Neither dynamic is easily neutralized by modest shifts in US rate expectations.

Technically, Dollar Index reflects this pressure. The break below 96.21 to 95.55 last week signaled renewed downside momentum. As long as 97.74 resistance holds, the long term down trend is seen as resuming.

The key level is 38.2% projection of 110.17 to 96.37 from 100.39 at 95.11. Decisive break there would prompt downside acceleration through 61.8% projection at 91.86. Nevertheless, firm break of 97.74 will tremendously ease immediate downside risk and bring stronger rebound back towards 100.39.

And more importantly, as mentioned many times before, another fall with downside acceleration would push Dollar Index through the multi-decade channel floor decisively. That, if happen, would confirm that Dollar Index is reversing whole uptrend from 70.69 (2008 low). That should open up further down trend to 90 psychological level and below.

Summary 2/2 – 2/6

Monday, Feb 2, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 00:00 | AUD | TD-MI Inflation Gauge M/M Jan | 1% | |

| 00:30 | JPY | Manufacturing PMI Jan F | 51.5 | 51.5 |

| 01:45 | CNY | RatingDog Manufacturing PMI Jan | 50.3 | 50.1 |

| 07:00 | EUR | Germany Retail Sales M/M Dec | -0.20% | -0.60% |

| 07:30 | CHF | Real Retail Sales Y/Y Dec | 2.50% | 2.30% |

| 08:30 | CHF | Manufacturing PMI Jan | 47.9 | 45.8 |

| 08:50 | EUR | France Manufacturing PMI Jan F | 51 | 51 |

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 48.7 | 48.7 |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 49.4 | 49.4 |

| 09:30 | GBP | Manufacturing PMI Jan F | 51.6 | 51.6 |

| 14:30 | CAD | Manufacturing PMI Jan | 48.6 | |

| 14:45 | USD | Manufacturing PMI Jan F | 51.9 | 51.9 |

| 15:00 | USD | ISM Manufacturing PMI Jan | 48.3 | 47.9 |

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | 59.3 | 58.5 |

| 15:00 | USD | ISM Manufacturing Employment Index Jan | 44.9 |

| 00:00 | AUD |

| TD-MI Inflation Gauge M/M Jan | |

| Consensus | |

| Previous | 1% |

| 00:30 | JPY |

| Manufacturing PMI Jan F | |

| Consensus | 51.5 |

| Previous | 51.5 |

| 01:45 | CNY |

| RatingDog Manufacturing PMI Jan | |

| Consensus | 50.3 |

| Previous | 50.1 |

| 07:00 | EUR |

| Germany Retail Sales M/M Dec | |

| Consensus | -0.20% |

| Previous | -0.60% |

| 07:30 | CHF |

| Real Retail Sales Y/Y Dec | |

| Consensus | 2.50% |

| Previous | 2.30% |

| 08:30 | CHF |

| Manufacturing PMI Jan | |

| Consensus | 47.9 |

| Previous | 45.8 |

| 08:50 | EUR |

| France Manufacturing PMI Jan F | |

| Consensus | 51 |

| Previous | 51 |

| 08:55 | EUR |

| Germany Manufacturing PMI Jan F | |

| Consensus | 48.7 |

| Previous | 48.7 |

| 09:00 | EUR |

| Eurozone Manufacturing PMI Jan F | |

| Consensus | 49.4 |

| Previous | 49.4 |

| 09:30 | GBP |

| Manufacturing PMI Jan F | |

| Consensus | 51.6 |

| Previous | 51.6 |

| 14:30 | CAD |

| Manufacturing PMI Jan | |

| Consensus | |

| Previous | 48.6 |

| 14:45 | USD |

| Manufacturing PMI Jan F | |

| Consensus | 51.9 |

| Previous | 51.9 |

| 15:00 | USD |

| ISM Manufacturing PMI Jan | |

| Consensus | 48.3 |

| Previous | 47.9 |

| 15:00 | USD |

| ISM Manufacturing Prices Paid Jan | |

| Consensus | 59.3 |

| Previous | 58.5 |

| 15:00 | USD |

| ISM Manufacturing Employment Index Jan | |

| Consensus | |

| Previous | 44.9 |

Tuesday, Feb 3, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 21:45 | NZD | Building Permits Dec | 2.80% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | -10.20% | -9.80% |

| 00:30 | AUD | Building Permits M/M Dec | -6.00% | 15.20% |

| 03:30 | AUD | RBA Interest Rate Decision | 3.85% | 3.60% |

| 04:30 | AUD | RBA Press Conference |

| 21:45 | NZD |

| Building Permits Dec | |

| Consensus | |

| Previous | 2.80% |

| 23:50 | JPY |

| Monetary Base Y/Y Jan | |

| Consensus | -10.20% |

| Previous | -9.80% |

| 00:30 | AUD |

| Building Permits M/M Dec | |

| Consensus | -6.00% |

| Previous | 15.20% |

| 03:30 | AUD |

| RBA Interest Rate Decision | |

| Consensus | 3.85% |

| Previous | 3.60% |

| 04:30 | AUD |

| RBA Press Conference | |

| Consensus | |

| Previous | |

Wednesday, Feb 4, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 21:45 | NZD | Employment Change Q4 | 0.30% | 0.00% |

| 21:45 | NZD | Unemployment Rate Q4 | 5.30% | 5.30% |

| 00:30 | JPY | Services PMI Jan F | 53.4 | 53.4 |

| 01:45 | CNY | RatingDog Services PMI Jan | 52 | 52 |

| 08:50 | EUR | France Services PMI Jan F | 47.9 | 47.9 |

| 08:55 | EUR | Germany Services PMI Jan F | 53.3 | 53.3 |

| 09:00 | EUR | Eurozone Services PMI Jan F | 51.9 | 51.9 |

| 09:30 | GBP | Services PMI Jan F | 54.3 | 54.3 |

| 10:00 | EUR | Eurozone CPI Y/Y Jan P | 1.70% | 1.90% |

| 10:00 | EUR | Eurozone Core CPI Y/Y Jan P | 2.20% | 2.30% |

| 10:00 | EUR | Eurozone PPI M/M Dec | 0.30% | 0.50% |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | -2.30% | -1.70% |

| 13:15 | USD | ADP Employment Change Jan | 48K | 41K |

| 14:45 | USD | Services PMI Jan F | 52.5 | 52.5 |

| 15:00 | USD | ISM Services PMI Jan | 53.8 | 54.4 |

| 15:30 | USD | Crude Oil Inventories (Jan 30) | -2.0M | -2.3M |

| 21:45 | NZD |

| Employment Change Q4 | |

| Consensus | 0.30% |

| Previous | 0.00% |

| 21:45 | NZD |

| Unemployment Rate Q4 | |

| Consensus | 5.30% |

| Previous | 5.30% |

| 00:30 | JPY |

| Services PMI Jan F | |

| Consensus | 53.4 |

| Previous | 53.4 |

| 01:45 | CNY |

| RatingDog Services PMI Jan | |

| Consensus | 52 |

| Previous | 52 |

| 08:50 | EUR |

| France Services PMI Jan F | |

| Consensus | 47.9 |

| Previous | 47.9 |

| 08:55 | EUR |

| Germany Services PMI Jan F | |

| Consensus | 53.3 |

| Previous | 53.3 |

| 09:00 | EUR |

| Eurozone Services PMI Jan F | |

| Consensus | 51.9 |

| Previous | 51.9 |

| 09:30 | GBP |

| Services PMI Jan F | |

| Consensus | 54.3 |

| Previous | 54.3 |

| 10:00 | EUR |

| Eurozone CPI Y/Y Jan P | |

| Consensus | 1.70% |

| Previous | 1.90% |

| 10:00 | EUR |

| Eurozone Core CPI Y/Y Jan P | |

| Consensus | 2.20% |

| Previous | 2.30% |

| 10:00 | EUR |

| Eurozone PPI M/M Dec | |

| Consensus | 0.30% |

| Previous | 0.50% |

| 10:00 | EUR |

| Eurozone PPI Y/Y Dec | |

| Consensus | -2.30% |

| Previous | -1.70% |

| 13:15 | USD |

| ADP Employment Change Jan | |

| Consensus | 48K |

| Previous | 41K |

| 14:45 | USD |

| Services PMI Jan F | |

| Consensus | 52.5 |

| Previous | 52.5 |

| 15:00 | USD |

| ISM Services PMI Jan | |

| Consensus | 53.8 |

| Previous | 54.4 |

| 15:30 | USD |

| Crude Oil Inventories (Jan 30) | |

| Consensus | -2.0M |

| Previous | -2.3M |

Thursday, Feb 5, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Dec | 3.45B | 2.94B |

| 07:00 | EUR | Germany Factory Orders M/M Dec | -1.30% | 5.60% |

| 07:45 | EUR | France Industrial Output M/M Dec | 0.10% | -0.10% |

| 09:30 | GBP | Construction PMI Jan | 42 | 40.1 |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -0.20% | 0.20% |

| 12:00 | GBP | BoE Interest Rate Decision | 3.75% | 3.75% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--2--7 | 0--5--4 |

| 13:15 | EUR | ECB Main Refinancing Rate | 2.15% | 2.15% |

| 13:15 | EUR | ECB Rate On Deposit Facility | 2.00% | 2.00% |

| 13:30 | USD | Initial Jobless Claims (Jan 30) | 210K | 209K |

| 13:45 | EUR | ECB Press Conference | ||

| 15:30 | USD | Natural Gas Storage (Jan 30) | -379B | -242B |

| 00:30 | AUD |

| Trade Balance (AUD) Dec | |

| Consensus | 3.45B |

| Previous | 2.94B |

| 07:00 | EUR |

| Germany Factory Orders M/M Dec | |

| Consensus | -1.30% |

| Previous | 5.60% |

| 07:45 | EUR |

| France Industrial Output M/M Dec | |

| Consensus | 0.10% |

| Previous | -0.10% |

| 09:30 | GBP |

| Construction PMI Jan | |

| Consensus | 42 |

| Previous | 40.1 |

| 10:00 | EUR |

| Eurozone Retail Sales M/M Dec | |

| Consensus | -0.20% |

| Previous | 0.20% |

| 12:00 | GBP |

| BoE Interest Rate Decision | |

| Consensus | 3.75% |

| Previous | 3.75% |

| 12:00 | GBP |

| MPC Official Bank Rate Votes | |

| Consensus | 0--2--7 |

| Previous | 0--5--4 |

| 13:15 | EUR |

| ECB Main Refinancing Rate | |

| Consensus | 2.15% |

| Previous | 2.15% |

| 13:15 | EUR |

| ECB Rate On Deposit Facility | |

| Consensus | 2.00% |

| Previous | 2.00% |

| 13:30 | USD |

| Initial Jobless Claims (Jan 30) | |

| Consensus | 210K |

| Previous | 209K |

| 13:45 | EUR |

| ECB Press Conference | |

| Consensus | |

| Previous | |

| 15:30 | USD |

| Natural Gas Storage (Jan 30) | |

| Consensus | -379B |

| Previous | -242B |

Friday, Feb 6, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Dec | -0.30% | 2.90% |

| 05:00 | JPY | Leading Economic Index Dec P | 109.8 | 109.9 |

| 07:00 | EUR | Germany Industrial Production M/M Dec | -0.30% | 0.80% |

| 07:00 | EUR | Germany Trade Balance (EUR)Dec | 14.5B | 13.1B |

| 08:00 | CHF | Unemployment Rate M/M Jan | 3.00% | 3.00% |

| 08:00 | CHF | Foreign Currency Reserves Jan | 725B | |

| 13:30 | CAD | Net Change in Employment Jan | 7.3K | 8.2K |

| 13:30 | CAD | Unemployment Rate Jan | 6.80% | 6.80% |

| 15:00 | CAD | Ivey PMI Jan | 49.7 | 51.9 |

| 15:00 | USD | UoM Consumer Sentiment Feb P | 55.8 | 56.4 |

| 15:00 | USD | UoM 1-Yr Inflation Expectations Feb P | 4% |

| 23:30 | JPY |

| Overall Household Spending Y/Y Dec | |

| Consensus | -0.30% |

| Previous | 2.90% |

| 05:00 | JPY |

| Leading Economic Index Dec P | |

| Consensus | 109.8 |

| Previous | 109.9 |

| 07:00 | EUR |

| Germany Industrial Production M/M Dec | |

| Consensus | -0.30% |

| Previous | 0.80% |

| 07:00 | EUR |

| Germany Trade Balance (EUR)Dec | |

| Consensus | 14.5B |

| Previous | 13.1B |

| 08:00 | CHF |

| Unemployment Rate M/M Jan | |

| Consensus | 3.00% |

| Previous | 3.00% |

| 08:00 | CHF |

| Foreign Currency Reserves Jan | |

| Consensus | |

| Previous | 725B |

| 13:30 | CAD |

| Net Change in Employment Jan | |

| Consensus | 7.3K |

| Previous | 8.2K |

| 13:30 | CAD |

| Unemployment Rate Jan | |

| Consensus | 6.80% |

| Previous | 6.80% |

| 15:00 | CAD |

| Ivey PMI Jan | |

| Consensus | 49.7 |

| Previous | 51.9 |

| 15:00 | USD |

| UoM Consumer Sentiment Feb P | |

| Consensus | 55.8 |

| Previous | 56.4 |

| 15:00 | USD |

| UoM 1-Yr Inflation Expectations Feb P | |

| Consensus | |

| Previous | 4% |

Markets Weekly Outlook – NFP forecast, Fed’s New Direction, RBA Rate Hike Risk, BoE/ECB Pause and Big Tech Earnings

Week in review

- Kevin Warsh nominated as the next US Federal Reserve Chair.

- Commodity markets saw a sharp reversal, with silver down 27%.

- Key focus for the week ahead: Alphabet and Amazon earnings.

- Central Banks (RBA, BoE, ECB) meet ahead of the January NFP report.

A blockbuster week for global markets with wild price swings, geopolitical risk, Central Bank meetings and a new Fed Chair nominated.

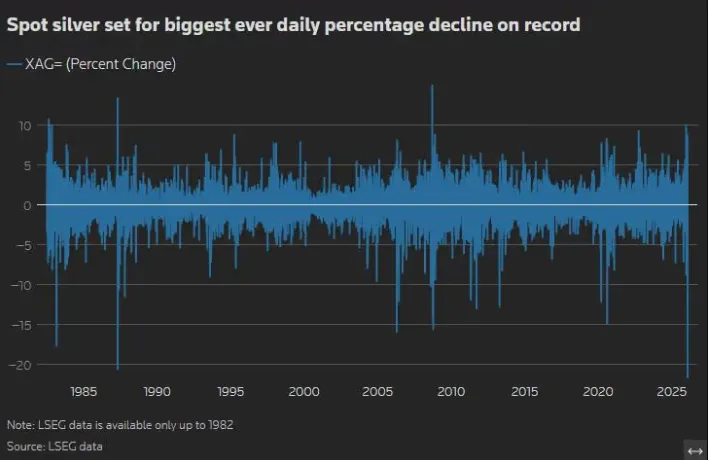

The starting point though has to be the stark reversal in commodity markets on Thursday and Friday which sent markets into a tailspin. At the time of writing, spot silver is down around 27% on the day, on track for their biggest daily drop on record, based on LSEG data available through 1982.

Source: LSEG

Gold on the other hand was down as much as 12%.

The selloff in commodities was driven largely by profit taking as well as a late renaissance for the US Dollar following the announcement by President Trump that Kevin Warsh has been tapped as the next chair of the US Federal Reserve.

Donald Trump mentioned he won’t ask Kevin Warsh (a candidate to lead the central bank) directly if he plans to cut interest rates. However, Trump believes Warsh naturally favors making it cheaper for people and businesses to borrow money.

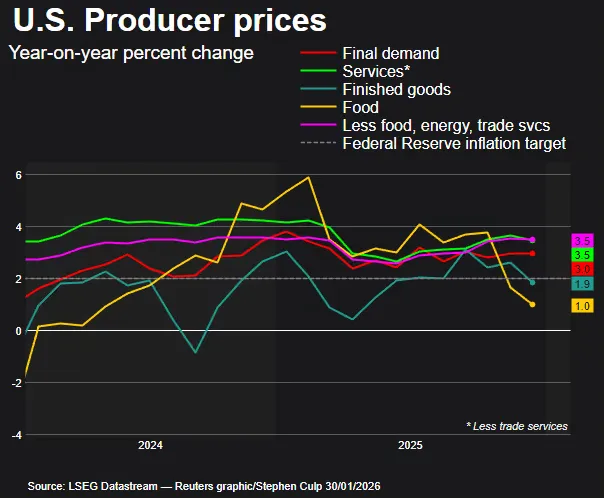

Adding to markets' late week malaise was a strong US PPI print which came in above the 0.2% estimate of economists polled by Reuters, after an unrevised 0.2% gain in November. Businesses appeared to be passing on higher costs from import tariffs.

Source: LSEG

The stock market saw some mixed results today. Apple’s stock price dropped by nearly 1% after the company shared its latest financial report, which put some downward pressure on the US market.

Despite this drop, the S&P 500 index is still heading toward its first winning week in nearly a month. On a global scale, MSCI's gauge of stocks that tracks stocks worldwide fell slightly today, but it is still on track to finish the week in the green and have its best month since September.

In Europe, stocks actually performed well with the pan-European STOXX 600 index closing up 0.64%. Strong earnings have helped propel the index to its biggest monthly gain since May. The index registered its seventh straight monthly gain, its longest streak since 2021.

On the FX front, the US dollar got stronger today continuing to show signs of stabilizing after recent weakness. The dollar index which measures the greenback against a basket of currencies, rose 0.57% to 96.73, with the euro down 0.54% at $1.1904.

The dollar was still on track for a second straight weekly decline and third straight monthly drop.

Source: LSEG

The Week Ahead

For the week starting February 2, 2026, markets face a critical junction as the "Magnificent Seven" earnings season continues alongside pivotal central bank decisions and the January US jobs report.

Big Tech Earnings: Alphabet and Amazon

Investors are laser-focused on whether AI investments are beginning to yield significant returns or if capital expenditure (capex) is rising too quickly.

- Alphabet (Wednesday, Feb 4):

- Expectations: Analysts expect Q4 earnings to grow 22.4% to $2.63 per share, with revenue rising 15.5% to $111.4bn.

- The Big Question: Capex is expected to have surged by over 90% to $27.3bn. Markets will look for guidance on 2026 spending; if it exceeds the projected $89.8bn without clear revenue growth, the stock could face pressure.

- Market Sentiment: Options markets imply a potential 5.5% post-earnings swing. Resistance is seen at $350.

- Amazon (Thursday, Feb 5):

- Expectations: Forecasts suggest revenue of $211.3bn (up 12.5%). The key metric will be AWS (Cloud) revenue, projected to grow 21.1% to $34.9bn.

- Market Sentiment: Shares are currently in a "symmetrical triangle" consolidation. A break above $250 would signal a bullish trend, while disappointing AWS growth could send the stock toward support at $220.

US Labor Market: The January Jobs Report

The headline event of the week arrives on Friday, Feb 6 (Saturday morning AEDT).

- Non-Farm Payrolls (NFP): After a soft December (+50k jobs), January is expected to see a slight improvement with 70,000 jobs added.

- Unemployment Rate: Expected to hold steady at 4.4%.

- Market Impact: A stronger-than-expected report could bolster the US Dollar, especially following the nomination of Kevin Warsh as the next Fed Chair, who is perceived as less "dovish" than his predecessors.

Central Bank Decisions (The "Thursday Double-Header")

Both the Bank of England (BoE) and the European Central Bank (ECB) meet on Thursday, Feb 5.

- BoE: Markets expect rates to stay on hold at 3.75%. However, with UK unemployment at a multi-year high (5.1%), traders will hunt for signals of a rate cut later in Q1 or Q2.

- ECB: Also expected to pause. The focus remains on whether the Euro (EUR/USD) can sustain its breakout above the $1.19 level.

Asia-Pacific: RBA Interest Rate Decision

Closer to home, the Reserve Bank of Australia (RBA) meets on Tuesday, Feb 3.

- The Outlook: Following higher-than-expected trimmed mean inflation (3.4%) and a falling unemployment rate (4.1%), the market has aggressively priced in a 75% chance of a 25bp rate hike.

- The ASX 200: The local index is hovering just 2% below its all-time high (9115.2). A hawkish RBA could create headwinds for the index, though materials and energy sectors remain a source of strength.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index (DXY)

From a technical perspective, the US Dollar Index (DXY) has made a late week recovery printing a bullish engulfing daily candle close on Friday.

The index has closed above a key resistance level at 96.90 which does bode well for further upside.

The question now is whether the rally is sustainable?

The US dollar is facing several other problems. Conflicts around the world (geopolitics), concerns about how much money the US government is spending (fiscal risks), and the possibility that different countries might work together to lower the dollar’s value (FX intervention) have all been weighing on the Dollar.

If the US DOllar is able to overcome these in the short-term, immediate resistance rests at 97.70 before the 200-day MA comes into focus at 98.62.

A move lower from current prices faces support at 96.37 before this weeks lows around 95.50 comes into focus.

US Dollar Index (DXY) Chart, January 30, 2026

Source:TradingView.Com (click to enlarge)

The Weekly Bottom Line: Kevin Warsh Nominated as Next Fed Chair

Canadian Highlights

- Despite a busy week of Canadian economic updates, not much has changed for the economic outlook.

- Declines in non-precious metal exports to the U.S. are only being partly offset by gains elsewhere. This aligns with recent GDP and trade data pointing to effectively flat fourth quarter output.

- An increase in the GST/HST tax credit will provide modest relief to lower income households but is expected to have a limited macroeconomic impact.

U.S. Highlights

- President Trump has nominated former Fed governor Kevin Warsh as the next Fed Chair.

- The Federal Reserve elected to hold rates steady at the target range of 3.50-3.75%.

- The White House and Senate have reached a deal that would avert another government shutdown. The appropriations bill still needs to be confirmed by the House of Representatives on Monday.

Canada – Trade Uncertainty Lingers Over Economy

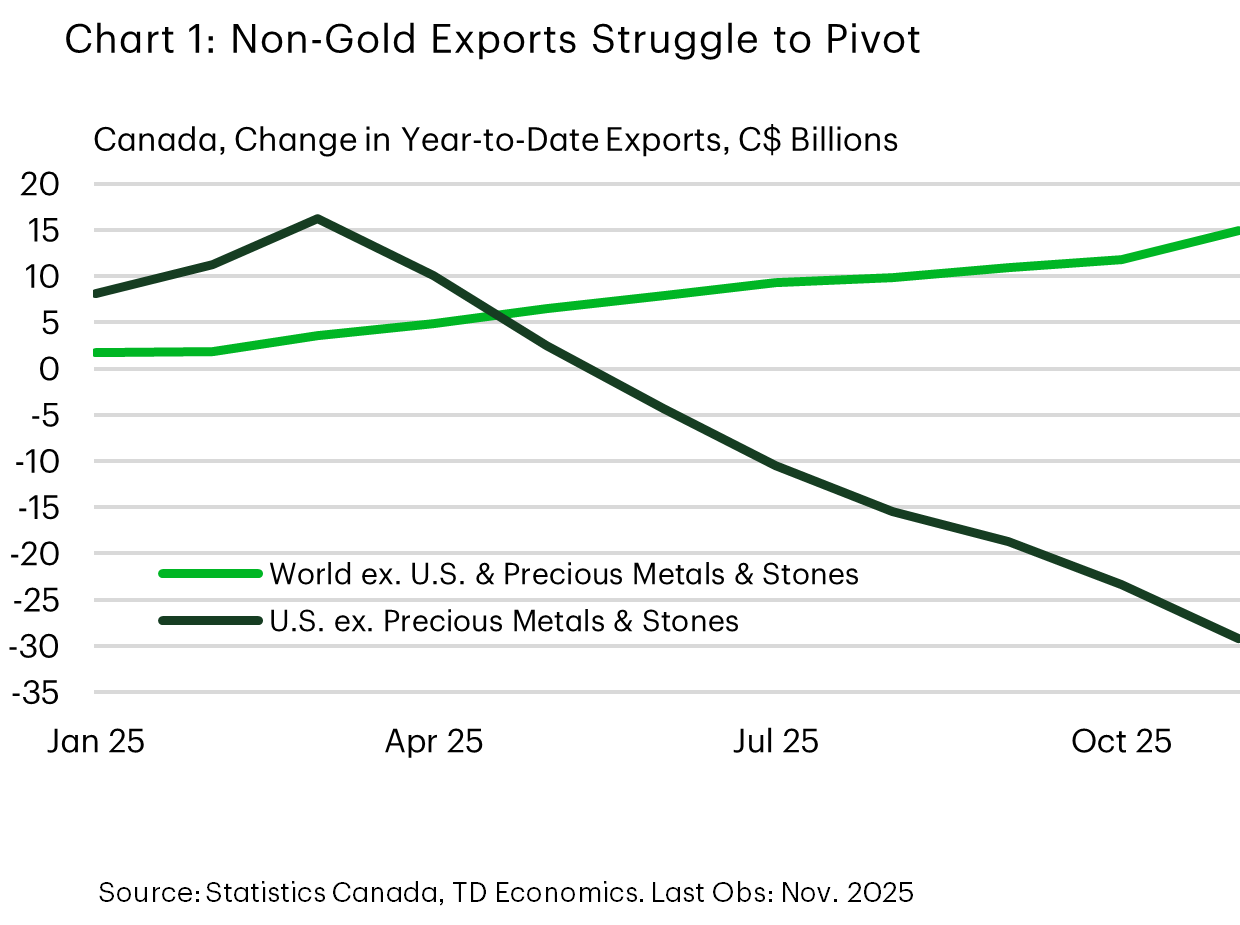

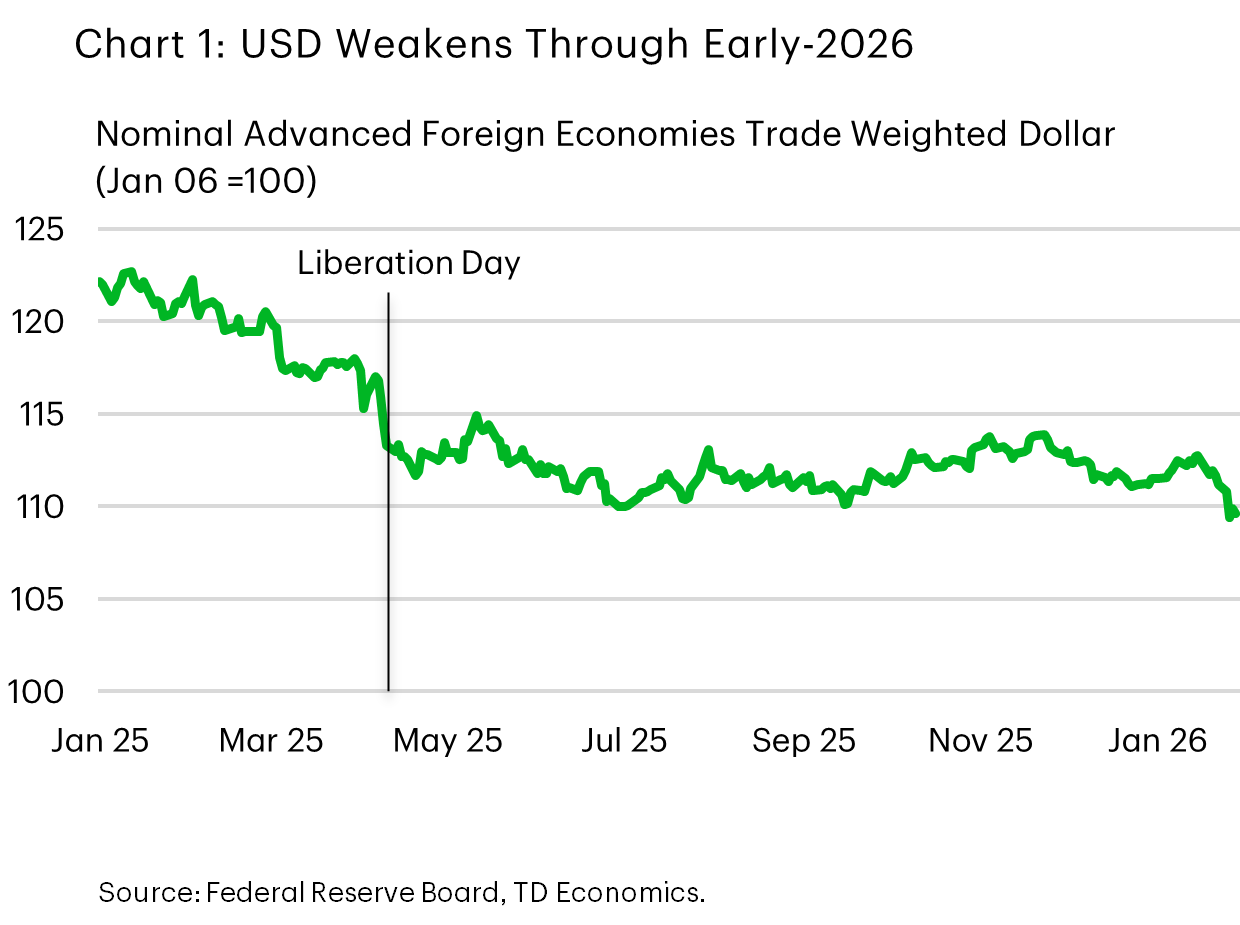

It was a busy week of updates on the Canadian economy, on top of an announcement of expanded support for modest income Canadians and a widely expected rate hold from the Bank of Canada. Yet, after all the news, Canadian bond yields are roughly in line with last Friday’s close. Currency markets made headlines this week (see commentary) with the U.S. dollar’s (USD) slide since mid-January – lifting the CAD roughly 2.7% against USD over that span. Overall, the economy is still tracking with our prior forecasts, with relatively weak growth expected in 2026.

The trade picture remains challenging with the non-precious metal exports to the U.S. down $29 billion year-to-date (-5.5%), while exports to the rest of the world are up a smaller $14.9 billion (+10.9%). The picture highlights the challenge for Canadian exporters in finding or developing new markets.

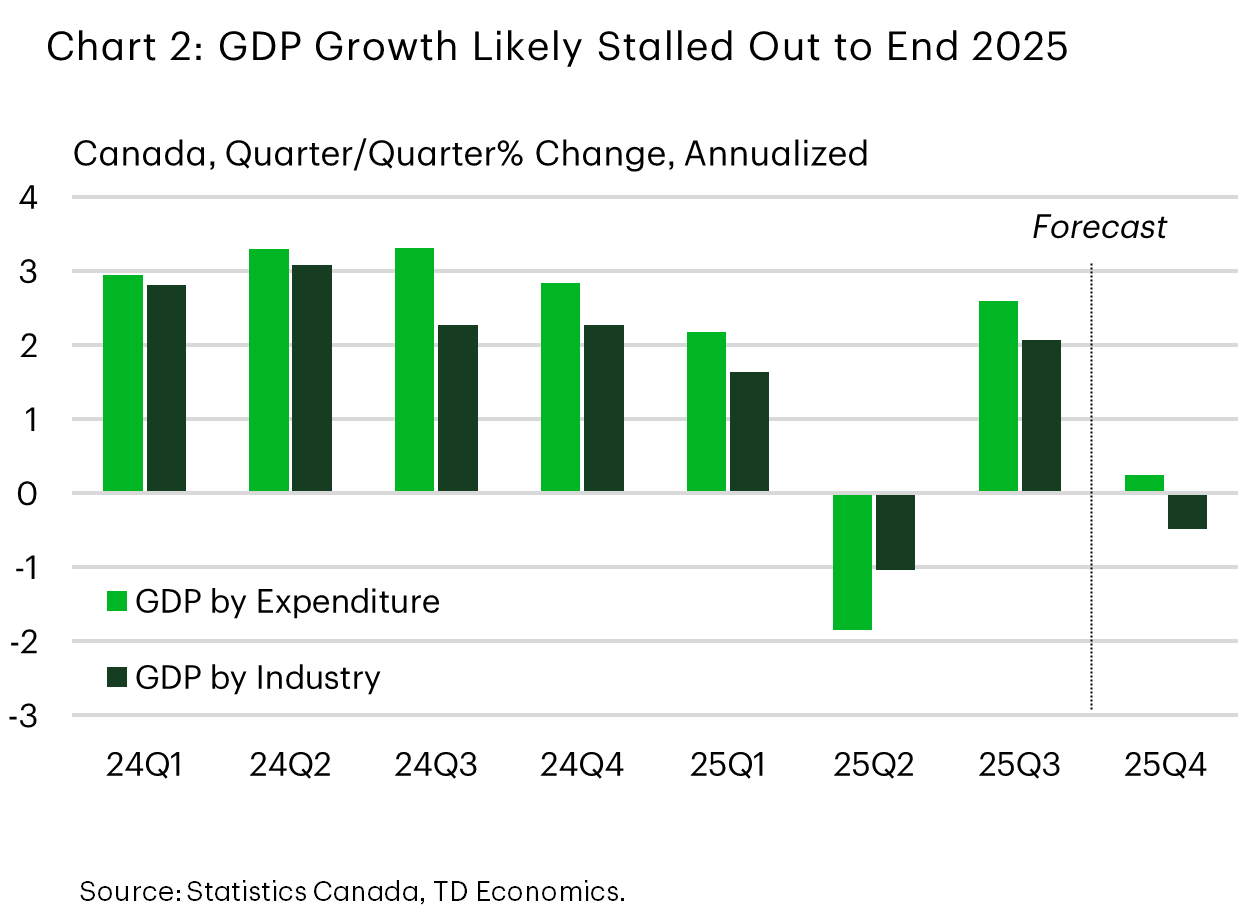

The difficult trade picture squares with the recent data flow from industry. Monthly GDP figures in the fourth quarter suggest a 0.5% (quarter-on-quarter annualized, q/q ann.) contraction to end the year. Now, there’s been a healthy wedge between the monthly and quarterly GDP figures of late (Chart 2), but it is a signal that is hard to ignore. Together with the updated trade figures, we now expect virtually no growth (+0.3%, q/q ann.) in the fourth quarter of the year – a touch above the Bank of Canada’s flat projection. The fourth quarter is a slight mark-down from prior projections but still conforms to the general picture of an economy that is going to struggle to gain traction over 2026. The picture, supported by the November trade data, is one of firms and consumers working under a cloud of uncertainty as they work to adjust to the new trade landscape. Circumstances are not expected to materially change in the coming months as the review of CUSMA picks up.

On the consumer front, the government announced an increase in the GST/HST tax credit, which it has rebranded the “Canada Groceries and Essentials Benefit”. The program is targeted towards lower income Canadians (about 12 million people receive the benefit), with payments expected to increase 25% for the next five years, along with a one-time payment of “a 50% increase” around mid-2026. The impact on the economy is expected to be relatively small (~0.1% of GDP), but could help to alleviate some of the challenges lower-income households have been facing, especially with regards to food costs.

We don’t expect this program to materially affect the outlook and, therefore, inflation. It is relatively small and the currents carrying the economy over the coming months are far more powerful forces. Uncertainty remains very high, so possible outcomes around the baseline are wide, but we expect 2026 to be a year where growth gradually stabilizes as a new normal is established.

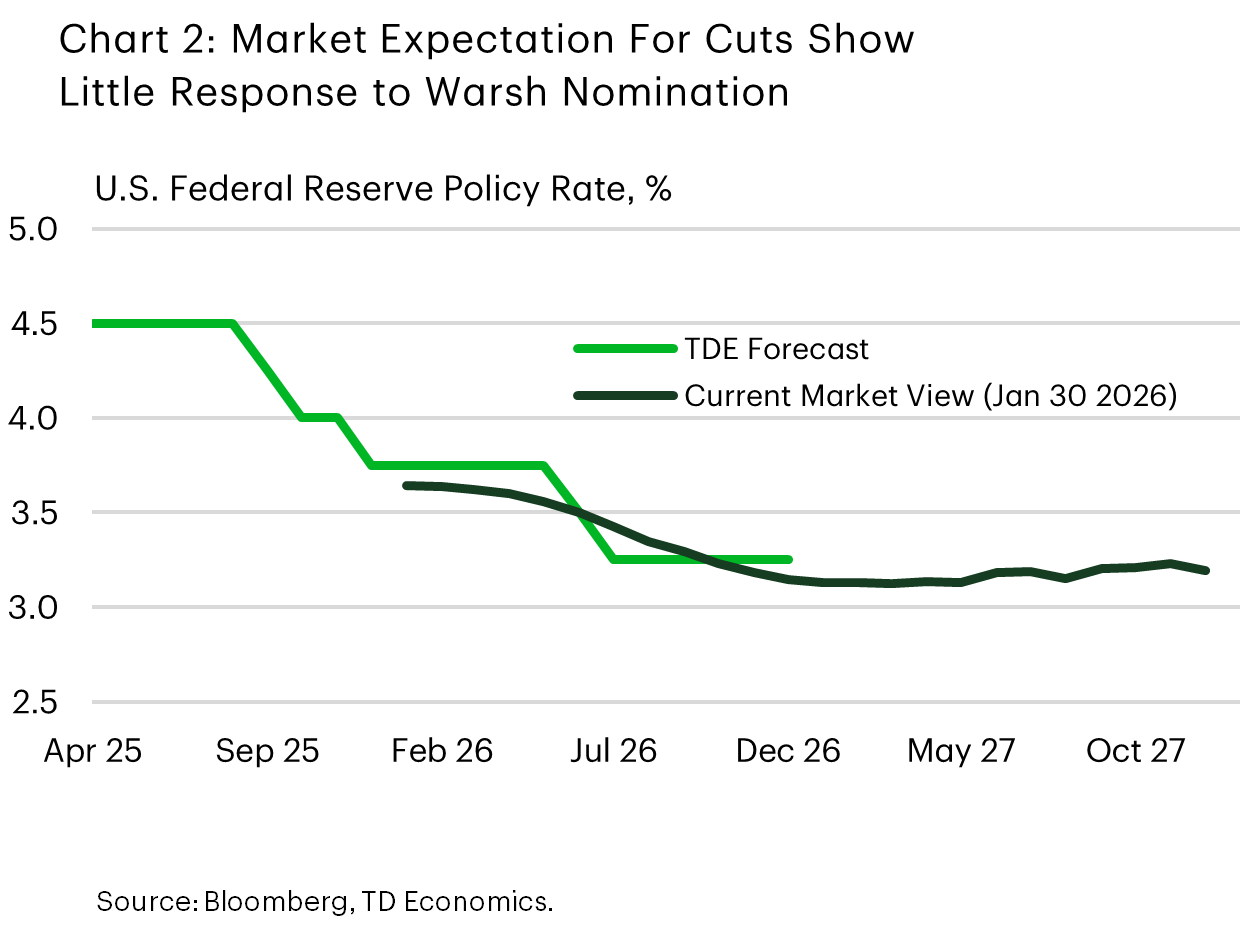

U.S. – Kevin Warsh Nominated as Next Fed Chair

It was a quiet week on the economic data calendar, giving financial markets an opportunity to digest a torrent of developments on the earnings, political and policy front. The Fed interest rate announcement took a backseat, with the FOMC predictably holding the policy rate steady, while maintaining its cutting bias. But the bigger news was President Trump’s nominating Kevin Warsh to be the new Fed Chair (see commentary). More recently, Warsh has struck a relatively dovish tone, but historically he has leaned more hawkish. Financial market reaction is somewhat mixed. Equities have turned modestly lower – and look to the end the week in the red – while the yield curve has steepened by several basis points. Meanwhile, gold gave back most of its gains from earlier in the week, while the greenback suffered a second straight week of declines and has now slipped by 2.7% since mid-January (Chart 1).

As of writing, it looks like the White House and Senate leaders have reached a deal to avert another government shutdown… well, sort of. The “deal” will extend funding for five of the six agencies through September 30th. Funding for the Department of Homeland Security, which includes Immigration and Customs Enforcement (ICE), will be split off from the larger appropriations package and will only extend through February 13th. This will allow Congress more time to negotiate new policy measures on the current ICE deployment.

However, the funding bill will need to return to the House for another vote, which won’t happen until Monday, so there will be a brief lapse in appropriations over the weekend. Provided the revised bill passes without issue, the disruptions will be small. However, should passage in the House be delayed, and the shutdown drags on for even a few days, then it’s very likely that the January employment report – scheduled for release on Friday February 6th – will be delayed.

Turning to the Fed announcement, there was little doubt that the FOMC would hold the policy rate steady. For investors, the focus was more on tweaks to the statement and the press conference to get a better sense of forward guidance. Changes to the statement largely reflected a “mark-to-market” on current conditions. The assessment on economic activity was upgraded to “solid” (previously “moderate”), while the reference to the downside risks to the labor market were removed. During the press conference, Powell characterized the current policy stance as “roughly appropriate and not significantly restrictive”. Translation: the FOMC sees reduced risks to both sides of its dual mandate, suggesting less need for further policy action.

Importantly, Fed futures barely budged following President Trump’s announcement that he is nominating Warsh to be the new Fed chair – with two cuts still priced by year-end (Chart 2). For the time being, concerns surrounding Fed independence have been tempered. But rest assured – if confirmed by the Senate – market participants will parse every word over the coming months as Warsh shadows Chair Powell.