Sample Category Title

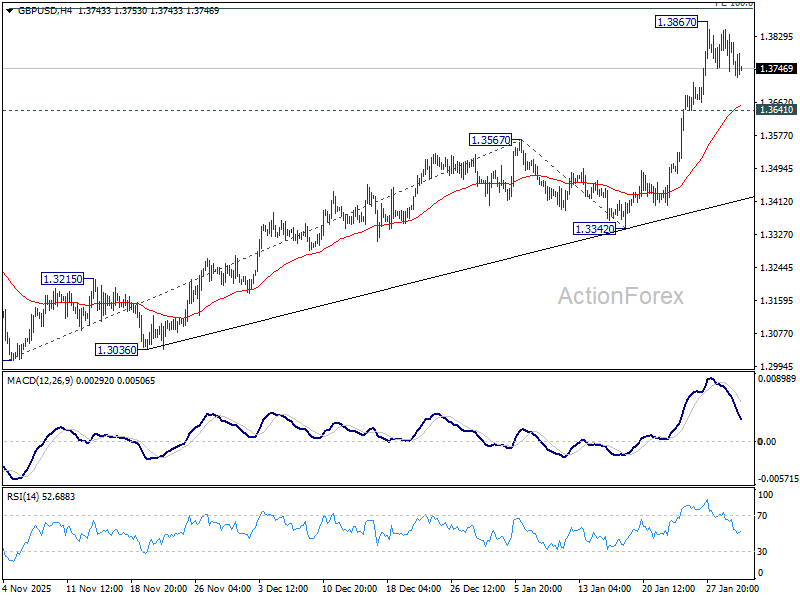

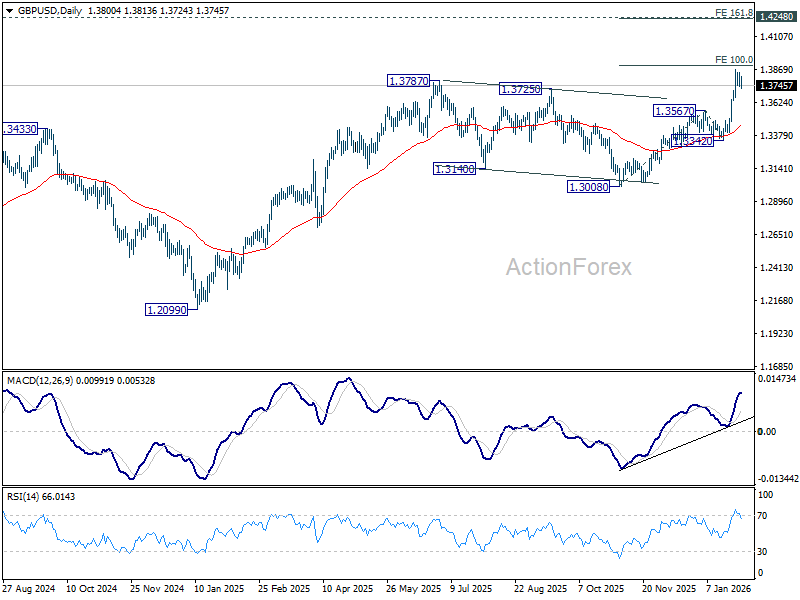

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3753; (P) 1.3801; (R1) 1.3858; More...

No change in GBP/USD's outlook as sideway trading continues below 1.3867. Downside should be contained by 1.3641 to bring another rally. Firm break of 100% projection of 1.3008 to 1.3567 from 1.3342 at 1.3901 will pave the way to 161.8% projection at 1.4246, which is close to 1.4248 key structural resistance. However, break of 1.3641 will turn bias to the downside for deeper pullback.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

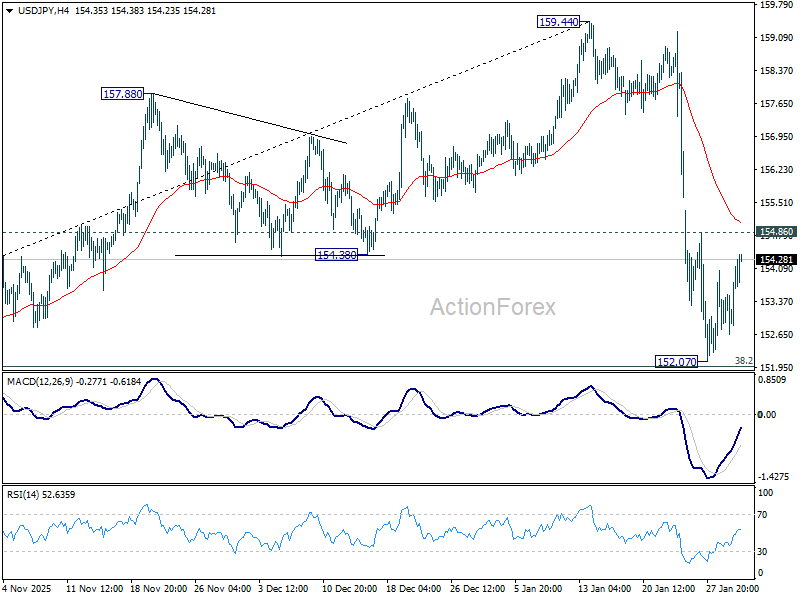

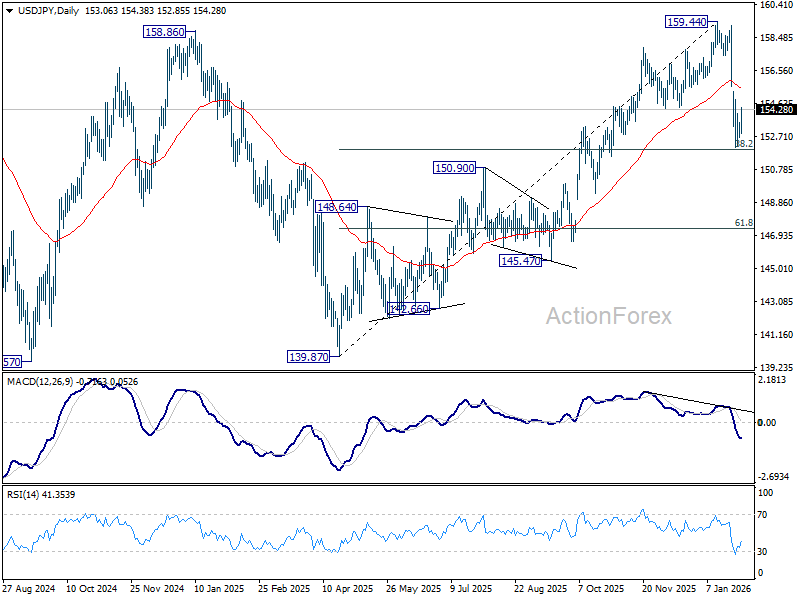

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.69; (P) 153.12; (R1) 153.54; More...

USD/JPY's recovery extends higher today but upside is still limited below 154.86 resistance. Intraday bias stays neutral. As noted before, fall from 159.44 is seen as correcting the rise from 139.87. Strong support should be seen from 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound, at least on first attempt. On the upside above 154.86 minor resistance will turn intraday bias to the upside for recovery. However, decisive break of 151.96 will argue that it is reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.35) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

Canada’s Economy Takes a Step Back in October

Canadian GDP contracted by 0.3% m/m in October, in line with Statistics Canada's advanced guidance and market expectations.

Compositionally, 11 of 20 industries registered a decline on the month. Goods industries (-0.7% m/m) reversed out last month's hefty gain, while the services sector contracted by a smaller 0.2% m/m.

On the goods side, the manufacturing sector (-1.5% m/m) contributed most to the GDP contraction, offsetting last month's expansion. A 0.6% m/m pullback in the mining, oil & gas sectors also contributed to monthly GDP decline. Meanwhile, the construction sector fell for a second consecutive month (-0.4% m/m).

On the services side, the education sector fell by 1.8% weighed down by the teachers strike in Alberta. Meanwhile, the transportation and warehousing sector (-1.1% m/m) reversed out last month's gain. Wholesale and retail trade also fell by 0.9% m/m and 0.6% m/m, respectively.

Advanced guidance calls for a slight uptick in November GDP (0.1% m/m). Increases in the education, construction, and transportation sectors are expected to be partially offset by activity in the manufacturing and mining, oil & gas sector.

Key Implications

After an upside surprise to growth in the third quarter, today's GDP data together with November guidance indicate that fourth-quarter GDP growth is tracking roughly flat. Tariff-impacted industries showed some strain in October after gradually recovering in prior months. The expectation is that overall economic growth will remain subdued over the next quarter or two before gradually recovering over the medium-term.

The Bank of Canada (BoC) doesn't make its next policy decision until January 28th, and we don't think today's data moves them off of their current policy stance. The BoC has acknowledged that trade-related impacts on inflation and economic growth are becoming more clear, though that doesn't lower the level of uncertainty in coming quarters as Canada and the U.S. continue to work on hammering out a trade deal. All told, we maintain our view that the BoC has reached the end of their interest rate easing cycle.

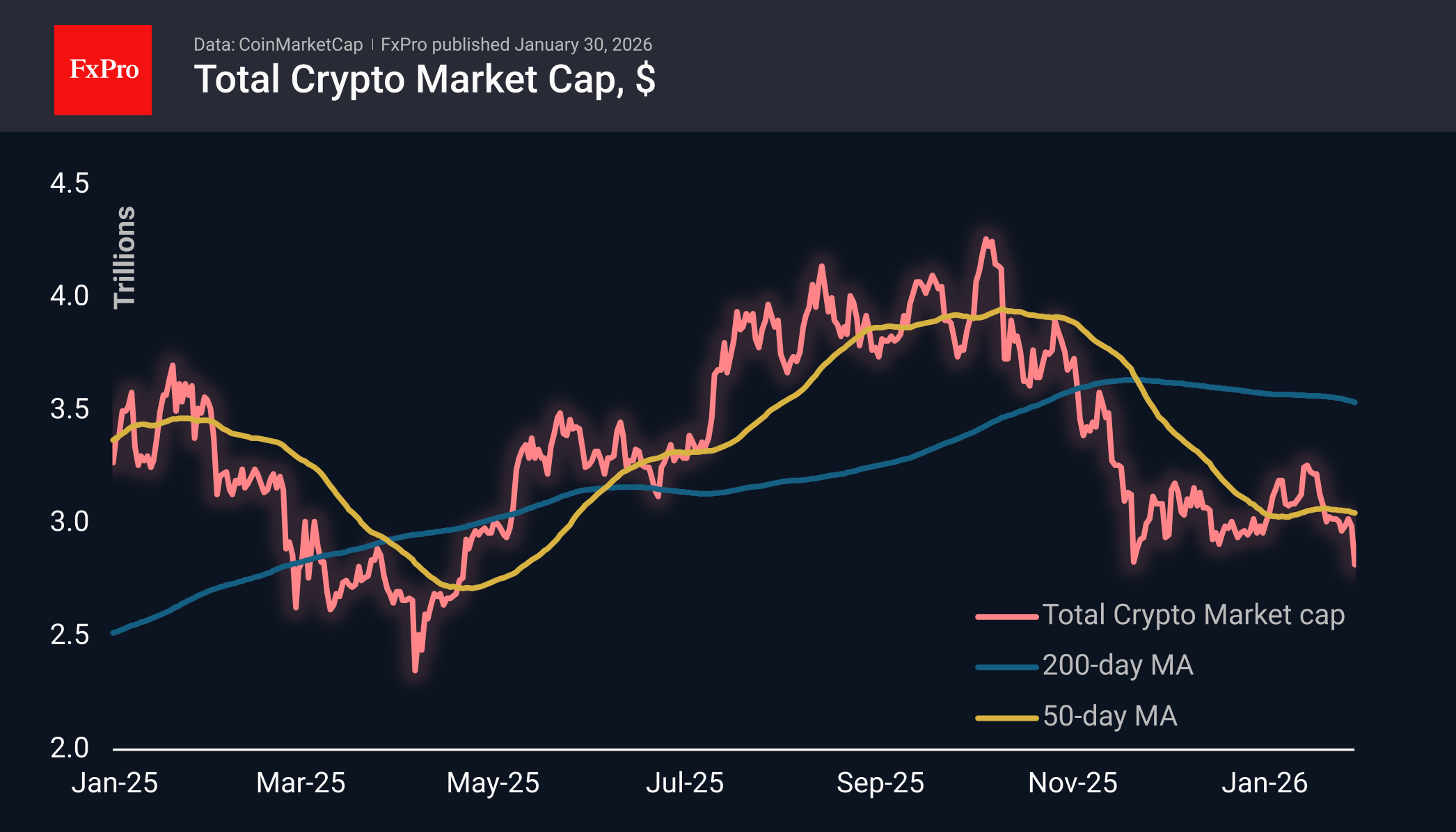

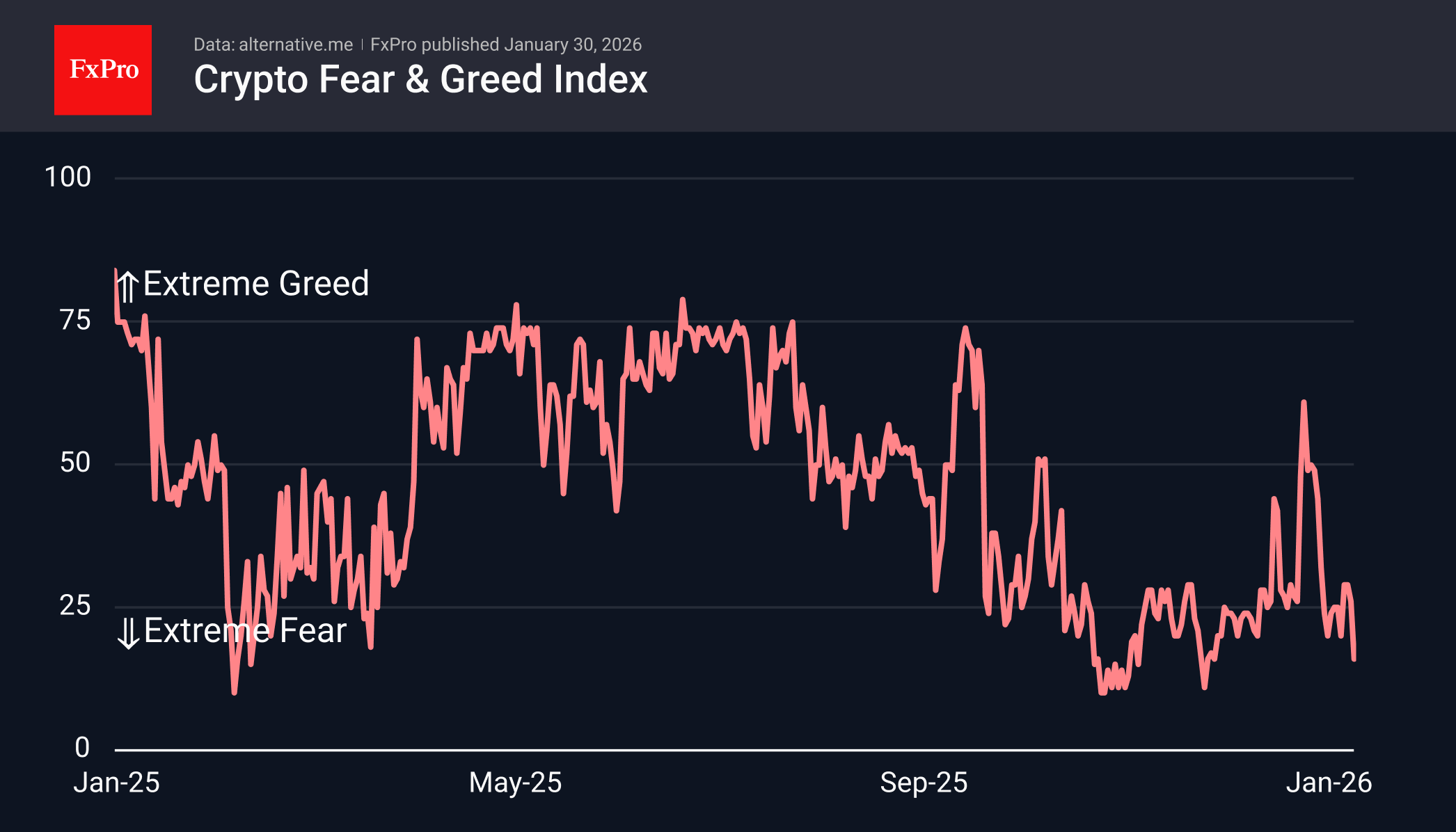

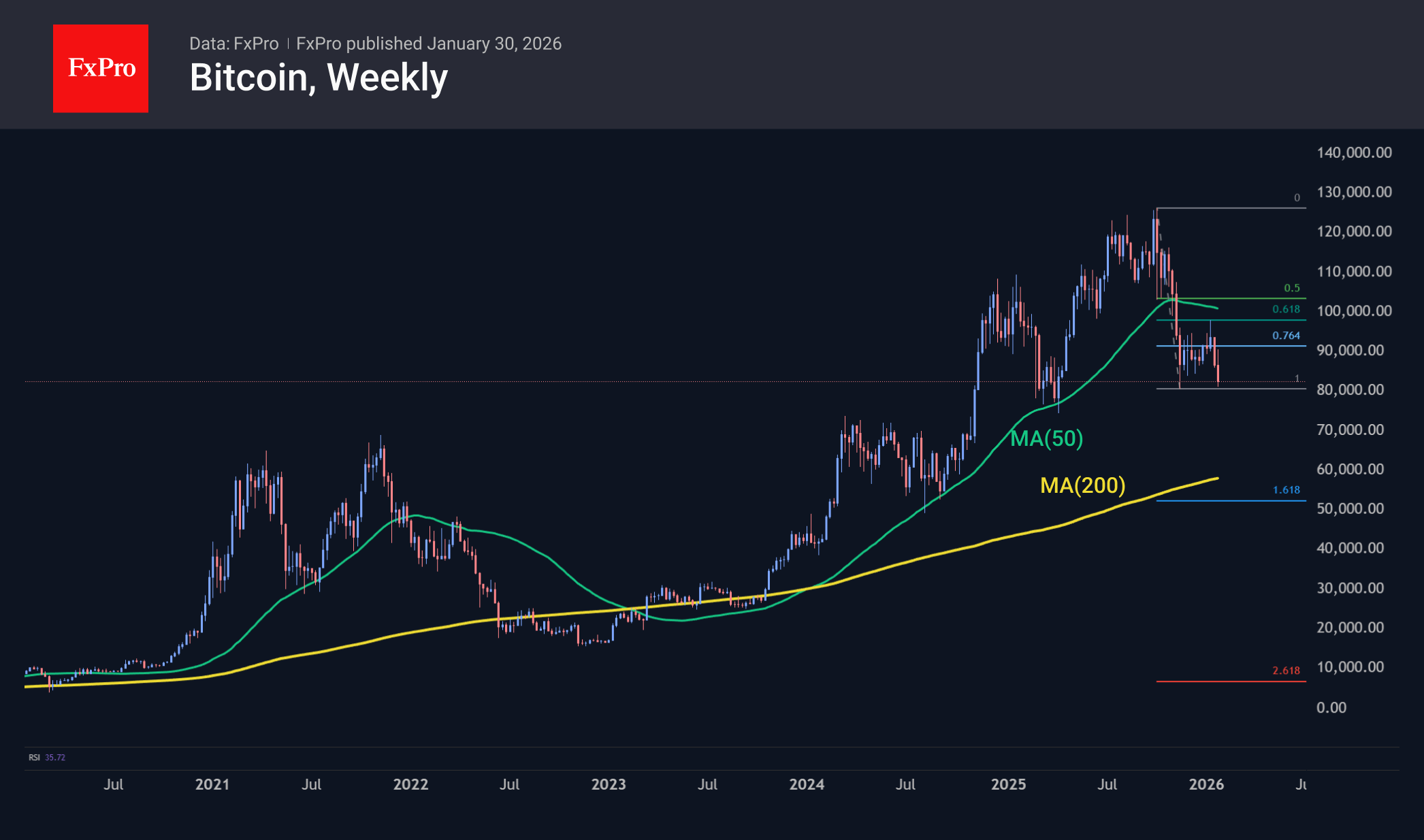

Crypto Looking for Support

Market Overview

The crypto market cap fell by around 5% to $2.82 trillion over the last 24 hours, and it twice touched $2.78 trillion, the lowest level since April last year. As we expected, the downward momentum in the commodity and stock markets only increased pressure on the cryptocurrency market, and the sell-off occurred at elevated volumes as market participants tightened their stop orders during the prolonged consolidation. Our worst-case scenario assumes a decline to the $1.8-2T range, with an extension to 161.8% of the initial downward momentum in October-November.

The Crypto Sentiment index fell to 16 by Friday. This is the lowest level in the last six weeks and a return to extreme fear, from which it was only possible to escape for two days during this week. We never tire of reminding you that although such sentiment values are perceived as a buying opportunity, a more cautious approach suggests buying when exiting the territory of extreme fear, to avoid the risks of sharp downward slippage.

Bitcoin has lost 6% in the last 24 hours, at one point falling to $81K and repeating the lows of late November. Now the market is testing the strength of the support that withstood the onslaught of sellers last year. Another 10K below is the area where the peak values for 2021–2022 and the first half of 2024 are concentrated. If it fails to hold, catch BTC at $52-60K. However, in the coming days, it is still worth focusing on BTC’s dynamics near $80K, which may not be so easy to break through and which many see as a buying opportunity.

News Background

More than 22% of the market supply of Bitcoin is in the red. Critical support for BTC is located at $83,400, according to Glassnode. Losing this level threatens a decline to the ‘true average market price’ of $80,700. With a further decline, long-term holders may begin to take losses, which will accelerate the decline.

This year, the speculative hype around cryptocurrencies will subside, and they will become the basic financial and settlement layer for the entire internet, according to Wintermute Ventures. Stablecoins will be the main means of payment in the digital economy.

Ethereum’s market supply on exchanges has been declining for the sixth consecutive month due to the hype around staking, Santiment notes. Since July last year, the figure has fallen by a third to 8.15 million ETH.

In 2025, the total volume of illegal cryptocurrency transactions reached a record $158 billion, increasing by 145% over the year, according to TRM Labs. Over the course of the year, hackers stole $2.87 billion in nearly 150 incidents.

The USD1 stablecoin, issued by US President Donald Trump’s company World Liberty Financial, reached a market capitalisation of $5 billion in less than a year since its launch, becoming the fifth largest stablecoin in the world.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7620; (P) 0.7663; (R1) 0.7686; More….

USD/CHF is still bounded in tight range above 0.7603 and intraday bias remains neutral. With 0.7792 resistance intact, outlook remains bearish. On the downside, break of 0.7603 will resume the larger down trend to 0.7382 projection level next. However, firm break of 0.7792 will turn bias back to the upside, for stronger rebound to 0.7860 support turned resistance and above.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

Warsh Pick Calms Fed Fears But No Dollar Turnaround

US President Donald Trump today finally named former Fed Governor Kevin Warsh to succeed Jerome Powell as Fed Chair, bringing an end to a prolonged and unusually turbulent succession process. Trump praised Warsh publicly, calling him a future “great” Fed chairman and signaling confidence in his leadership.

The announcement removed a major overhang for markets that had been grappling with rising concern over institutional credibility and political interference at the central bank. Warsh, a former Fed governor, is widely viewed as an orthodox and experienced policymaker, which has helped restore a degree of confidence in the Fed’s longer-term independence.

In policy terms, the appointment is not expected to derail the Fed’s existing outlook. The latest dot plot already signals scope for at least one rate cut later this year, and Warsh is not seen as an obstacle to that path. Instead, his selection is interpreted as favoring continuity rather than confrontation.

That partial restoration of institutional confidence showed up quickly in precious metals. After surging to record highs above 5500 earlier in the week, gold slipped back below the 5,000 psychological level, as traders locked in profits following an extreme rally fueled by policy and political risk. Silver also saw a sharp reversal, dropping back below 100 after briefly trading above 120. The pullback suggests that some of the most aggressive hedging and speculative positioning tied to institutional fears has eased, at least temporarily.

Despite these developments, Dollar has failed to mount a convincing rebound. While downside momentum has slowed, the greenback remains the worst performer of the week so far. In relative terms, Kiwi leads the FX board, followed by Aussie and Swiss Franc, while Yen and Loonie sit in the middle. The Dollar’s inability to capitalize on the Fed succession news suggests markets see the development as stabilizing—but not yet sufficient to reverse the longer-running diversification away from US assets.

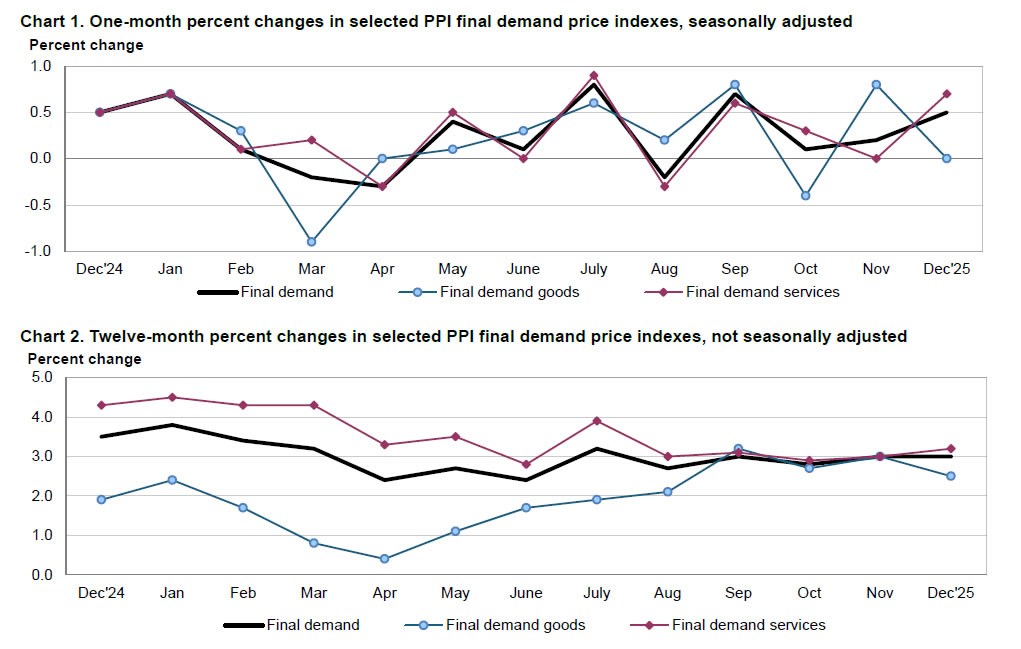

US PPI jumps 0.5% mom in December as services drive cost pressures

US producer prices rose sharply in December, with PPI up 0.5% mom, well above expectations of 0.2% mom. The increase was driven almost entirely by services, where prices climbed 0.7% mom on the month. In contrast, goods were flat.

Excluding food, energy, and trade services, core PPI rose 0.4%, marking the eighth consecutive monthly increase.

On an annual basis, PPI held at 3.0% yoy, above expectations of slowing to 2.7% yoy.

Canada GDP stalls in November as manufacturing drag offsets modest service growth

Canada’s economy stalled in November, with GDP flat at 0.0% mom and undershooting expectations for a modest 0.1% mom increase. The drag came from goods-producing industries, which fell -0.3% mom, marking the third decline in four months. Manufacturing and agriculture, forestry, fishing and hunting were the main contributors to the contraction.

By contrast, services-producing industries edged up 0.1% mom, supported by gains in retail trade, education, and transportation and warehousing. Overall, 10 of 20 sectors expanded.

Early indications point to a 0.1% mom rise in December GDP, with manufacturing and wholesale trade offsetting weakness in mining and energy—suggesting growth remains fragile but not rolling over.

Eurozone GDP beats expectations with 0.3% qoq growth, Q4 ends on firmer note

The Eurozone economy ended 2025 on slightly firmer footing, with GDP rising 0.3% qoq in Q4, modestly above expectations of 0.2%. Growth in the wider European Union matched that pace. On an annual basis, GDP expanded 1.3% yoy in the Eurozone and 1.4% yoy in the EU, easing slightly from Q3 but still consistent with a slow and uneven recovery.

Country-level figures showed a broadly constructive picture. Lithuania (+1.7%) led quarterly gains, followed by Spain and Portugal (both +0.8%), while Ireland (-0.6%) was the only member state to record a contraction. Year-on-year growth was positive in the vast majority of reporting countries, highlighting resilience despite ongoing structural and policy headwinds.

Swiss KOF falls to 102.5, but outlook remains above average

Switzerland’s KOF Swiss Economic Institute Economic Barometer eased from 103.6 to 102.5 in January, undershooting expectations of 103.2. Despite the pullback, the index remains comfortably above its medium-term average, suggesting the outlook has softened but is far from weak.

The decline was driven mainly by deterioration in hospitality and construction, where confidence faded at the start of the year. By contrast, sentiment improved in manufacturing as well as financial and insurance services, helping to cushion the overall slowdown.

Within the producing sector, signals were mixed. Employment prospects, profit expectations, exports, and assessments of production constraints came under pressure. However, brighter readings for order backlogs, general business conditions, and competitive positioning point to underlying resilience, reinforcing the view of moderation rather than a sharp downturn.

Tokyo CPI slows to 2% on fuel subsidies, BoJ normalization path intact

Japan’s January Tokyo core CPI (excluding fresh food) eased from 2.3% to 2.0% yoy, undershooting expectations of 2.2% and marking a 15-month low. Core-core CPI (excluding fresh food and energy) also eased from 2.3% to 2.0% yoy. Headline inflation slowed more sharply from 2.0% to 1.5%.

The slowdown was driven largely by one-off factors. Food inflation excluding fresh food decelerated for a fifth straight month, while energy prices fell -4.2% yoy after gasoline subsidies and the abolition of a provisional fuel tax surcharge. Gasoline prices dropped -14.8%, with electricity and city gas bills also declining. Base effects from last year’s food price surge further weighed on the data.

Despite the softer print, the figures are unlikely to derail the BoJ’s normalization. While fuel subsidies may push core inflation below target in coming months, policymakers are expected to focus on whether firms continue to pass through higher import costs from a weak yen—an outcome that would keep underlying inflation pressures alive.

Japan's industrial production fall -0.1% mom in December, consumption falters

Japan’s industrial production edged down -0.1% mom in December, a milder decline than expected -0.4% mom and consistent with a sector struggling for direction rather than deteriorating sharply. The Ministry of Economy, Trade and Industry maintained its assessment that output “fluctuates indecisively,” reflecting uneven momentum across industries.

Forward-looking guidance from manufacturers remains volatile. Firms surveyed expect output to jump 9.3% in January, followed by a 4.3% decline in February, highlighting stop-start dynamics rather than a clear recovery trend.

Sector performance was split, with declines in production machinery, chemicals, and paper products offset by gains in general machinery, electronics, and motor vehicles. Supply-side indicators pointed to some imbalance. Industrial shipments fell -1.7%, while inventories rose 1.0%, suggesting demand has not kept pace with production and raising the risk of further output adjustments if sales do not improve.

That concern was reinforced by a sharp disappointment in consumption. Retail sales fell -0.9% yoy in December, far below expectations for a 0.7% increase.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7620; (P) 0.7663; (R1) 0.7686; More….

USD/CHF is still bounded in tight range above 0.7603 and intraday bias remains neutral. With 0.7792 resistance intact, outlook remains bearish. On the downside, break of 0.7603 will resume the larger down trend to 0.7382 projection level next. However, firm break of 0.7792 will turn bias back to the upside, for stronger rebound to 0.7860 support turned resistance and above.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

US PPI jumps 0.5% mom in December as services drive cost pressures

US producer prices rose sharply in December, with PPI up 0.5% mom, well above expectations of 0.2% mom. The increase was driven almost entirely by services, where prices climbed 0.7% mom on the month. In contrast, goods were flat.

Excluding food, energy, and trade services, core PPI rose 0.4%, marking the eighth consecutive monthly increase.

On an annual basis, PPI held at 3.0% yoy, above expectations of slowing to 2.7% yoy.

Canada GDP stalls in November as manufacturing drag offsets modest service growth

Canada’s economy stalled in November, with GDP flat at 0.0% mom and undershooting expectations for a modest 0.1% mom increase. The drag came from goods-producing industries, which fell -0.3% mom, marking the third decline in four months. Manufacturing and agriculture, forestry, fishing and hunting were the main contributors to the contraction.

By contrast, services-producing industries edged up 0.1% mom, supported by gains in retail trade, education, and transportation and warehousing. Overall, 10 of 20 sectors expanded.

Early indications point to a 0.1% mom rise in December GDP, with manufacturing and wholesale trade offsetting weakness in mining and energy—suggesting growth remains fragile but not rolling over.

Chart Alert: Gold Has Formed a Medium-Term Blow-Off Top Below $5,600

Key takeaways

- Gold likely formed a medium-term blow-off top: After surging to a record high of US$5,602, Gold reversed sharply with a 12% drop, signalling that the recent bullish acceleration phase has been damaged and may have peaked.

- Pullback driven by positioning and hawkish expectations: The sell-off appears driven more by stop-outs of leveraged long positions below US$5,238, amplified by speculation over a hawkish Fed Chair nominee, rather than any hard fundamental shock.

- Short-term bias turns corrective unless US$5,240 is reclaimed: Gold is now in a short-term corrective decline within a broader uptrend, with downside risks toward US$4,888–4,550 unless prices regain and hold above US$5,240, which would reopen upside squeeze risk

Since the start of this week, Gold (XAU/USD) continued to extend its bullish acceleration and hit the intermediate resistance zone at US$5,049/5,149, as highlighted.

The precious yellow metal printed a fresh all-time high of US$5,602 on Thursday, 29 January, and then staged a swift 11.8% decline to an intraday low of US$4,941 on Friday, 30 January, at the time of writing.

The volatile movement seen in Gold (XAU/USD) in the past 24 hours has not been triggered by any concrete fundamental catalysts.

Media reports suggesting that former US Federal Reserve Governor Kevin Walsh may be nominated as the next Fed Chair, an announcement expected later today by President Trump, have been cited as the catalyst behind the ongoing pullback in precious metals.

Walsh is widely viewed as hawkish, raising concerns over tighter monetary policy and higher-for-longer interest rates, which have weighed on gold and broader precious metals prices.

Based on technical analysis and order flows, it seems like short-term speculative leveraged long positions got stopped when Gold (XAU/USD) crossed below a short-term pivotal support at US$5,238.

Overall, the short-term bullish acceleration phase for Gold has been damaged.

Let’s now look at the latest short-term technical elements to decipher the yellow metal’s potential trajectory for the next 1 to 3 days.

Short-term trend (1 to 3 days): Corrective decline within a medium-term uptrend

Fig. 1: Gold (XAU/USD) minor trend as of 30 Jan 2026 (Source: TradingView)

Fig. 2: Gold (XAU/USD) medium-term trend as of 30 Jan 2026 (Source: TradingView)

Watch the US$5,240 short-term pivotal resistance on Gold (XAU/USD) to maintain the ongoing minor corrective decline sequence to expose the next intermediate supports at US$4,888, US$4,757, and US$4,630/4,550 (see Fig. 1).

On the flip side, clearance and an hourly close above US$5,240 invalidates the bearish scenario for a squeeze up towards US$5,473 and a retest of the current all-time high area of US$5,600

Key elements to support the short-term bearish bias

- The price actions of Gold (XAU/USD) have formed an impending daily bearish “Evening Star” candlestick pattern, which suggests this week’s bullish acceleration has transformed into a potential medium-term “blow-off” top (see Fig. 2).

- There is still further room for the current price actions to stage a further retracement towards the 20-day and 50-day moving averages.

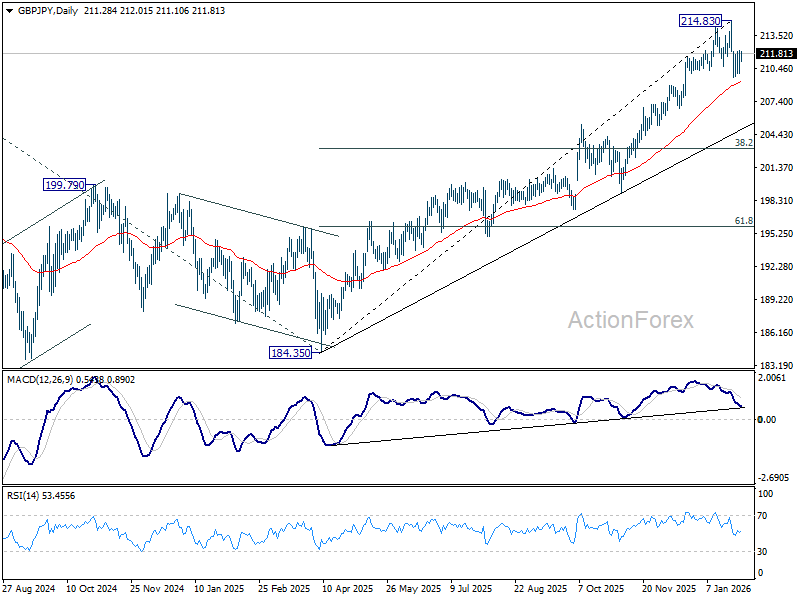

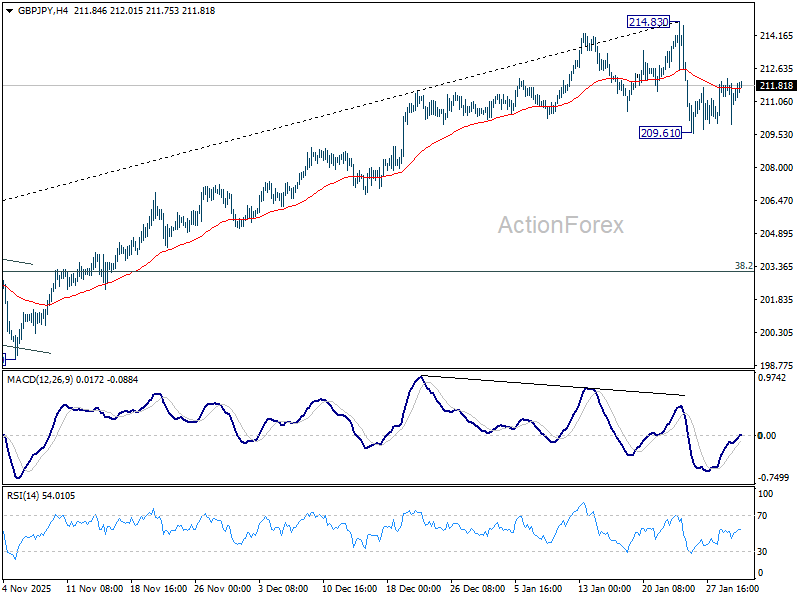

GBP/JPY Daily Outlook

Daily Pivots: (S1) 210.28; (P) 211.23; (R1) 212.40; More...

Intraday bias in GBP/JPY remains neutral for consolidations. Risk will stay on the downside as long as 214.83 holds, even in case of strong recovery. Below 209.61, and sustained break of 55 D EMA (now at 209.27) will argue that it's correcting whole rise from 184.35 and target 38.2% retracement of 184.35 to 214.83 at 203.18.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.