Sample Category Title

US: ISM Services Expansion Improves in August

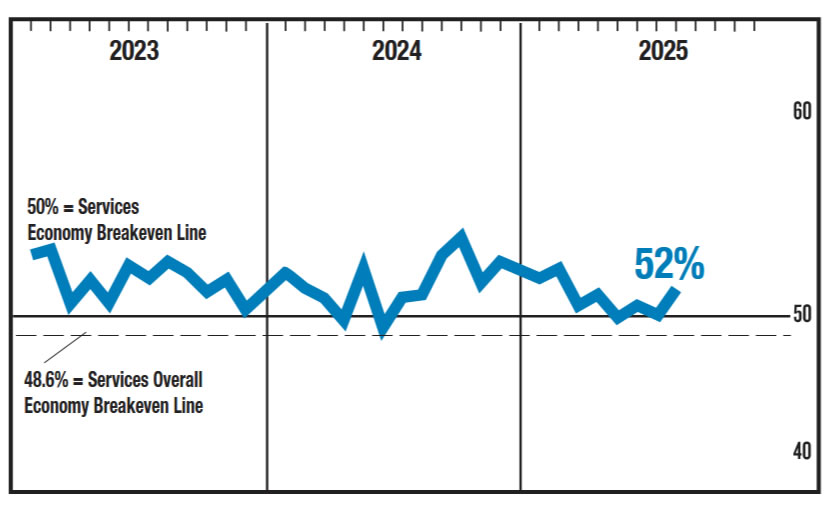

The ISM Services index rose a respectable 1.9 points to 52.0 in August, coming in above the market consensus forecast for only a modest increase. The number of industries reporting growth in August improved to 12 out of 18, compared to 11 in the month prior.

The increase in the headline measure was driven by a 5.7-point gain in new orders (to 56.0). That said, export orders and the backlog of orders continued to trend lower.

A notable 2.4-point improvement in business activity (to 55.0) also helped prop up the headline measure. Gains in other subcomponents were more muted, with the employment index rising only 0.1 points to 46.5 and remaining in contractionary territory for the third consecutive month.

The supplier deliveries index gave back the previous month's gain, falling 0.7 points to 50.3. The prices paid index also fell 0.7 points but remained elevated at 69.2, which is among the highest levels since late 2022.

Key Implications

The improvement in today’s ISM report indicates that activity in the services sector expanded at a slightly better pace in August compared to July, with the headline measure adding a bit more cushion above the 50-point expansionary threshold. The surge in new orders and the improvement in business activity are encouraging. Still, the report wasn't without blemishes, with an employment index that remained in contractionary territory for the third month in a row being the main fly in the ointment.

With the Fed now putting more emphasis on softening labor market conditions, the subdued performance of the employment subcomponent in today's ISM services report lines up with a host of other data favoring a rate cut at next month's FOMC meeting. This morning's ADP report, which indicated that private sector hiring slowed significantly in August, also sings to the same tune. Nonetheless, in judging the health of the labor market, the Fed's attention will be heavily focused on this Friday’s August payrolls report.

US ISM Services PMIs Beat Expectations – Market Overview

US ISM Services PMIs just got released at 52 vs 51 expectations, a positive surprise.

Prices paid are still way too high for a comfortably dovish FED, but it seems like this component isn't accelerating anymore.

For the rest, nothing shocking: The employment component is still in contraction but not disastrous and new orders are increasing again, a positive after the tariff-led decrease.

Next step will be tomorrow's NFP release which will shape up, with the September FOMC Meeting (September 18), the tone for the rest of the year.

Don't forget to stay in touch with the views from NY FED's Williams coming up at 12:05 (holds high influence on the FED and votes at every meeting) and later today Goolsbee's meetings (voter in 2025).

For now the US picture looks like a cooling one (far from catastrophic!).

Except for a major downward surprise tomorrow, there shouldn't be any reason to panic.

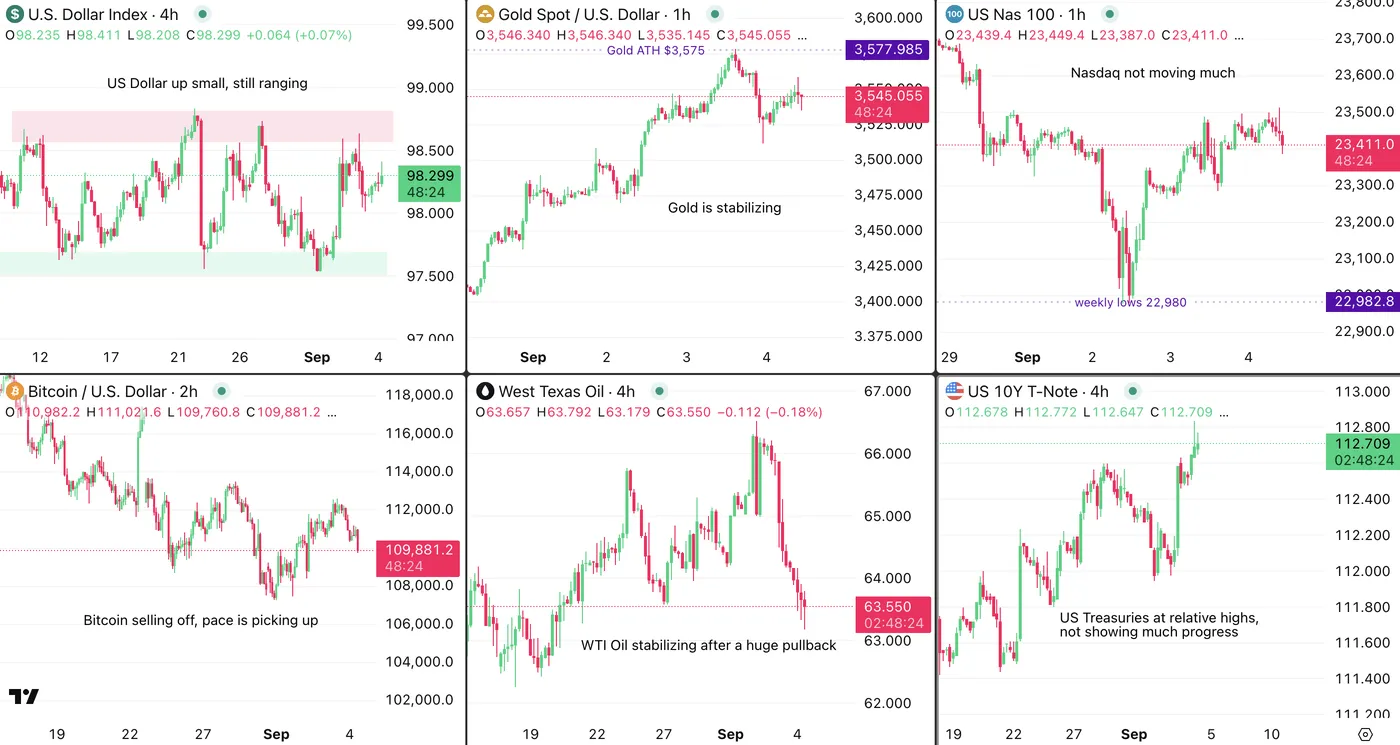

Reactions are small: A global market view

Market Overview, September 4, 2025 – Source: TradingView

Market reactions are very muted as Participants stay put for tomorrow's session – Anxiety is still high.

Only notable move would be Cryptocurrencies still seeing some profit-taking flows.

Safe Trades!

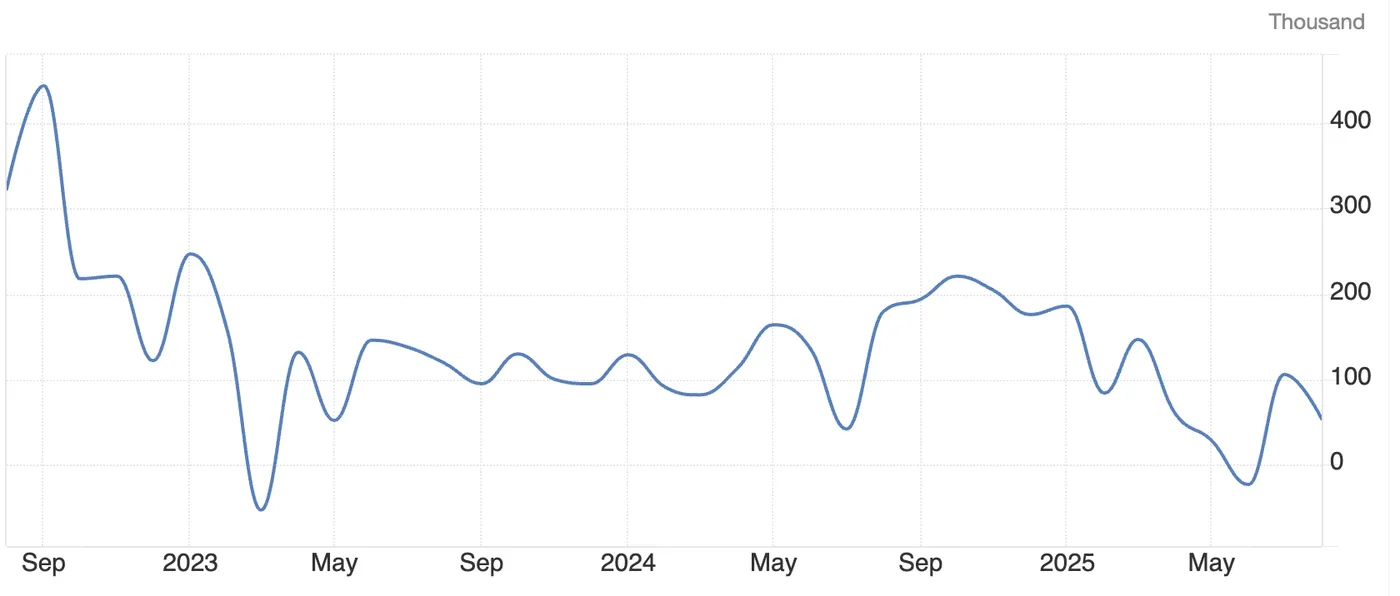

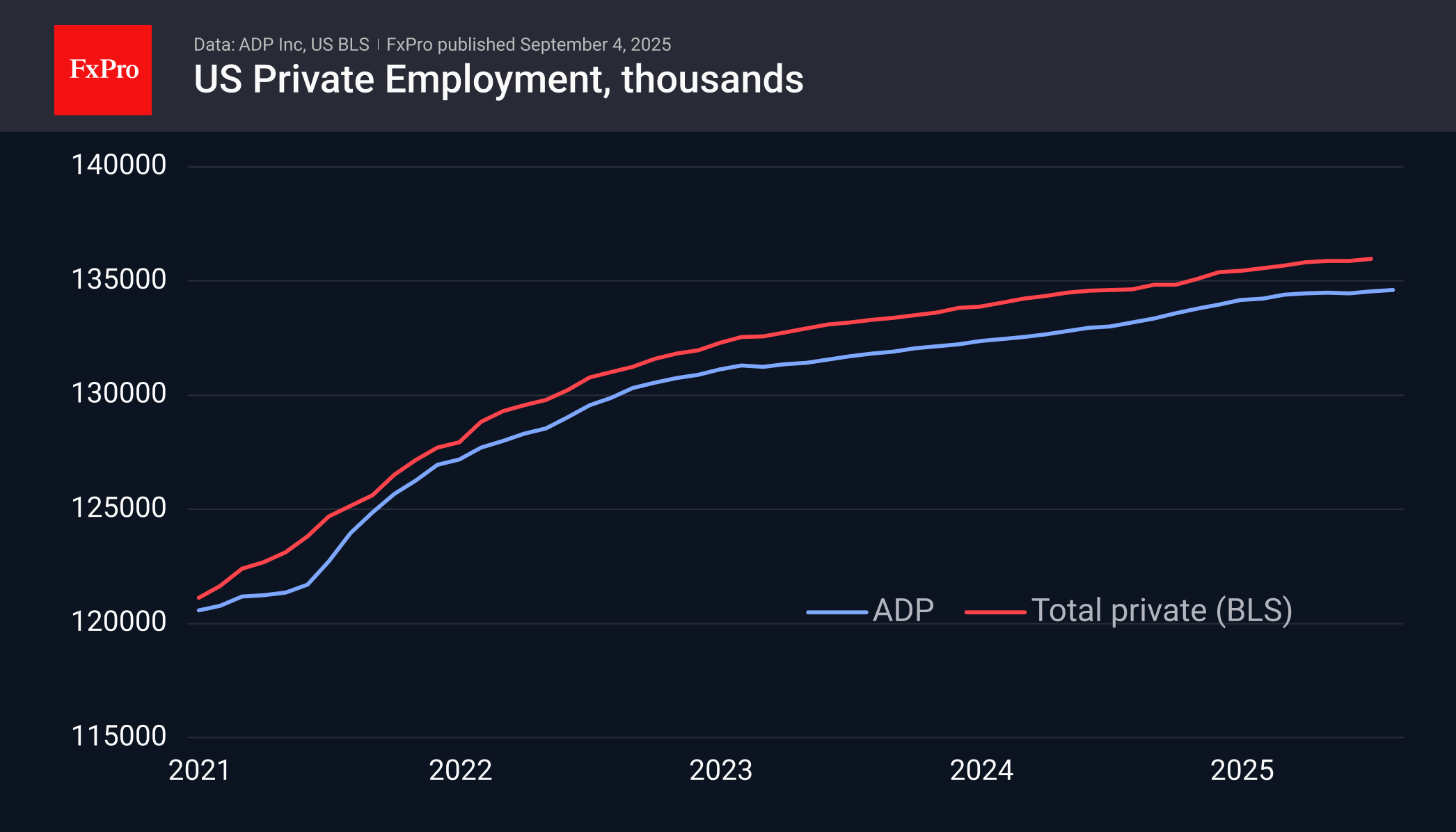

ADP Private Employment Misses on Expectations and Jobless Claims Rise Again – a Preview for Tomorrow’s Release?

ADP Private Employment data

In the long awaiting for tomorrow's Non-Farm Payrolls release, Participants can't get enough of more labor data, particularly as ADP employment recently turned out to be a more accurate preview of the US Employment trends (as large revisions to NFP later confirmed.

The report came at 54K vs 65K expectations a relatively small miss, but miss nonetheless – and this report reiterates the ongoing downtrend in private employment.

ADP Employment in the past 3 years, September 4, 2025 – Source: TradingEconomics

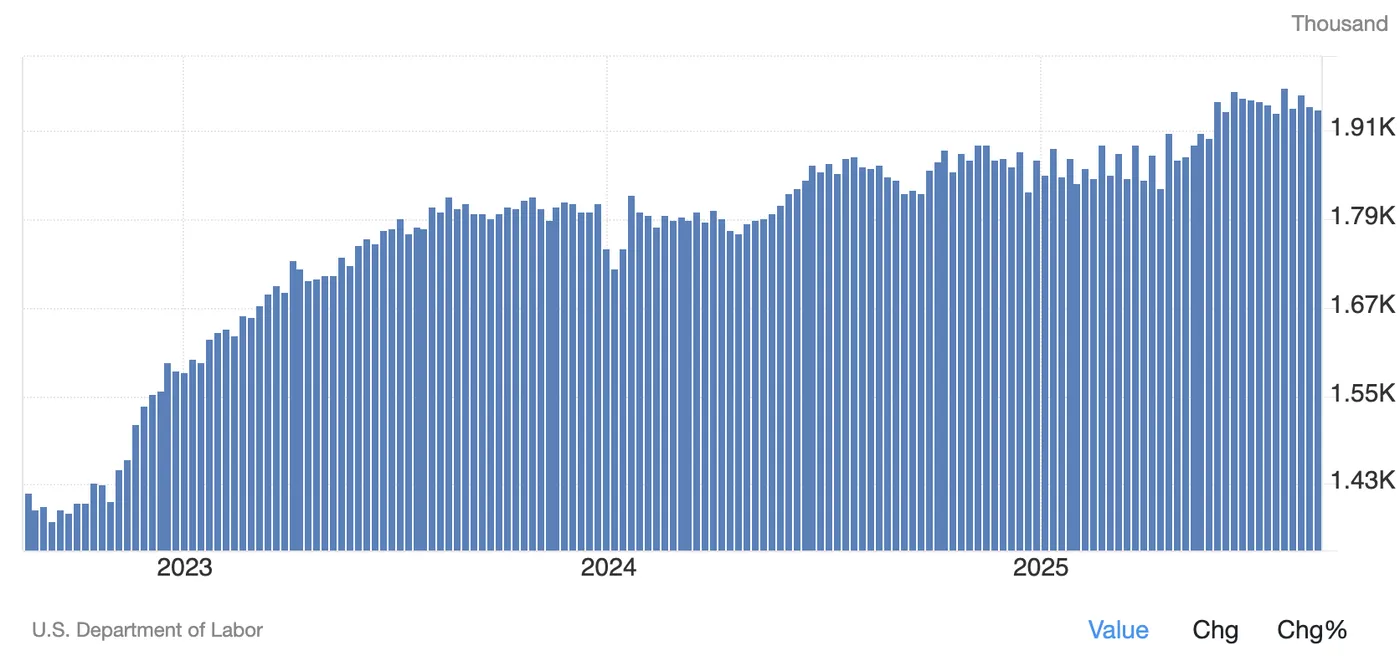

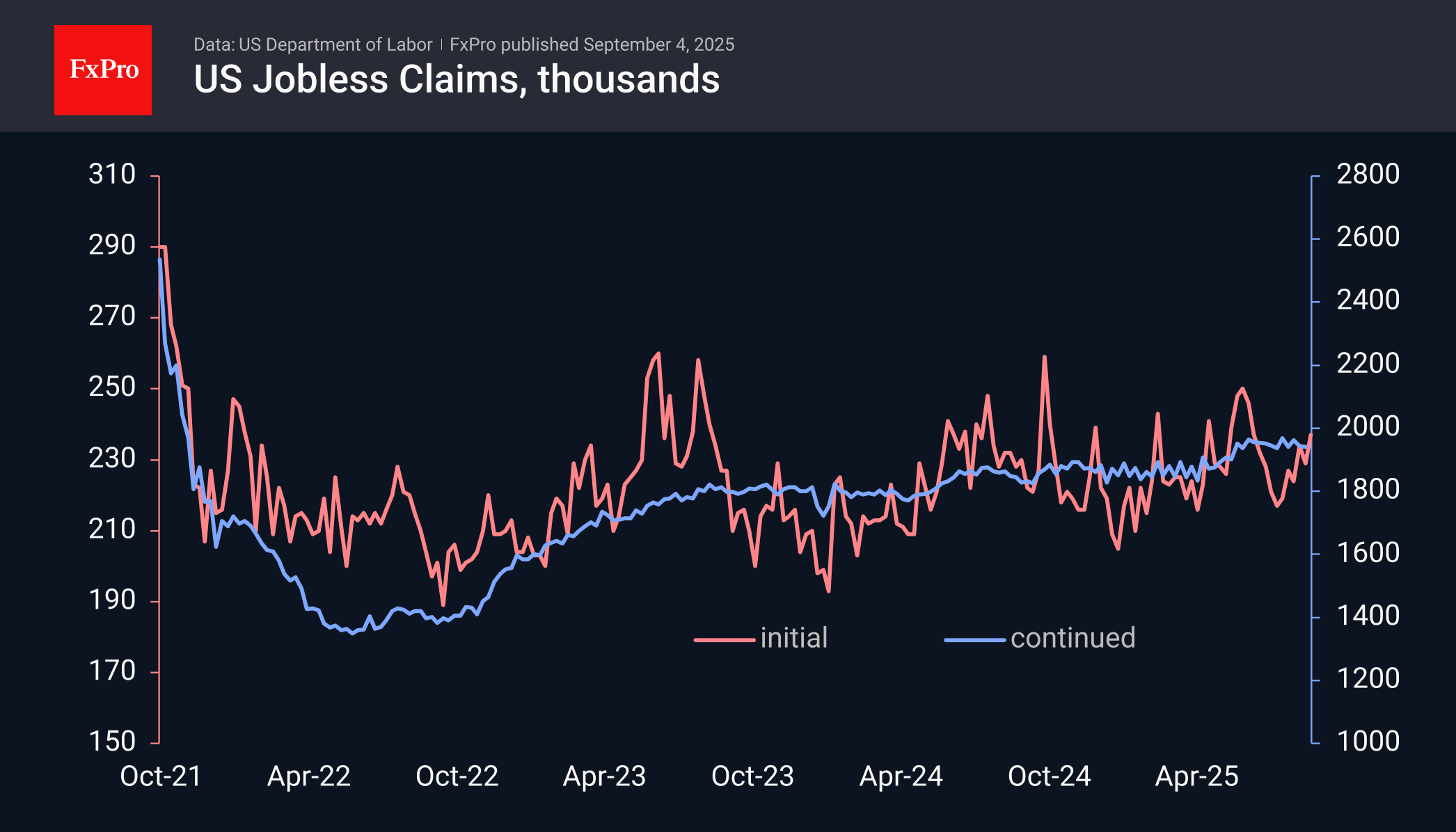

Jobless Claims and Unit Labor Costs

The Jobless claims rose to 237K from 230K, with the continuing claims still hanging around November 2021 levels.

Continuing Claims since 2023 – A steep rise – Source: TradingEconomics

The FED will still be appreciating the Unit Labor Cost data which came at 1% instead of 1.6%, which will help with inflationary pressures.

In case you didn’t know, Unit Labor Costs measure how much businesses pay workers to produce one unit of output. Rising costs signal wage pressures and potential inflation, while falling costs suggest easing price pressures.

Market reactions are very slow as Markets seem to not exaggerate tomorrow's NFP release which may still differentiate largely from this morning's reports.

Safe Trades!

Ahead of NFP: Slowdown, But Still Growth in US Jobs Market

On the eve of the monthly labour market report, alternative indicators point to a deterioration, albeit not too dramatic.

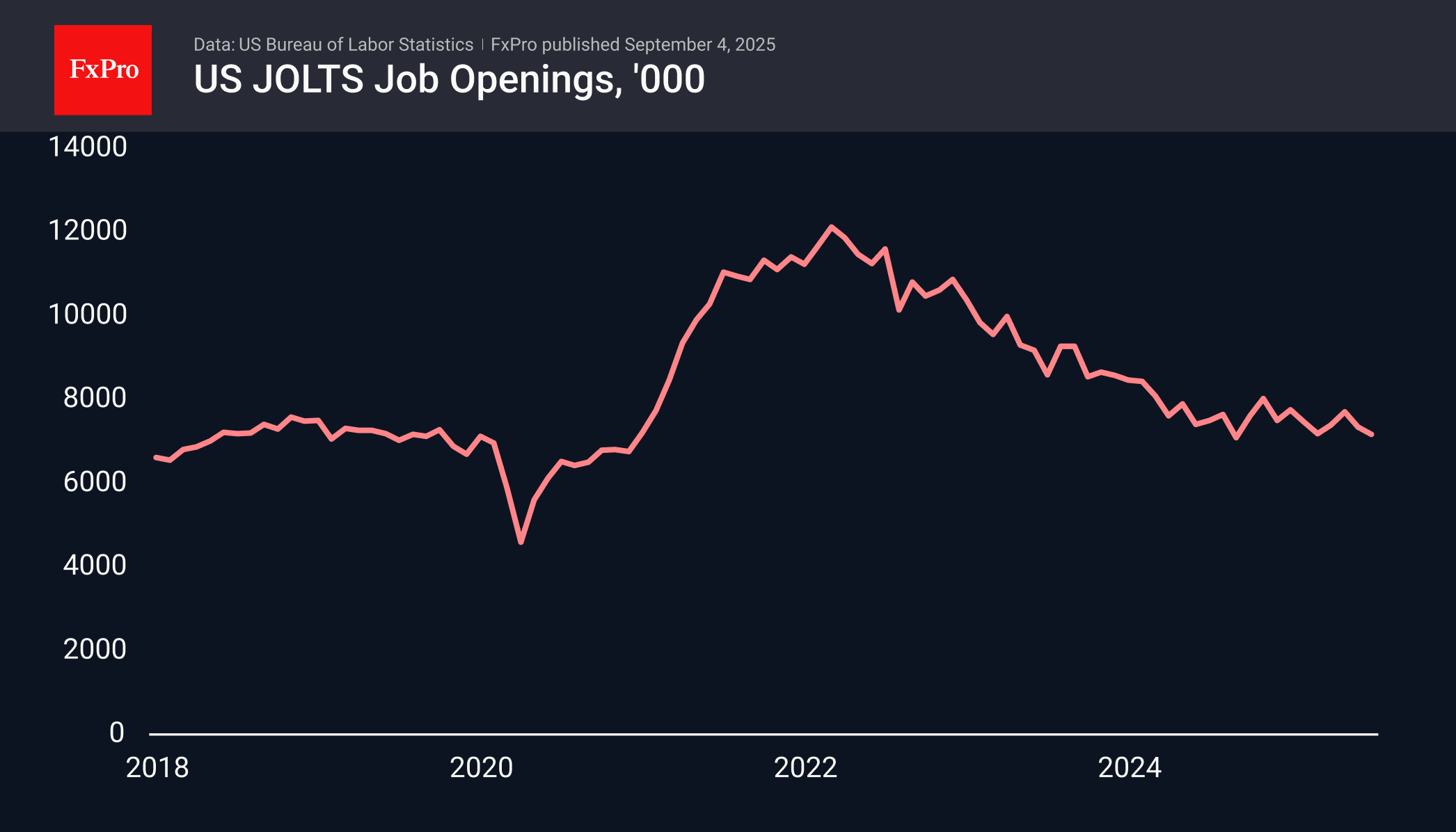

Data released on Wednesday showed job vacancies falling to a ten-month low. Looking at the bigger picture, this is a return to pre-pandemic levels, during which the number of vacancies jumped due to the spread of remote working. In fact, this is a signal that employers are now looking for staff less than before the pandemic, but there is no point in talking about a dramatic collapse.

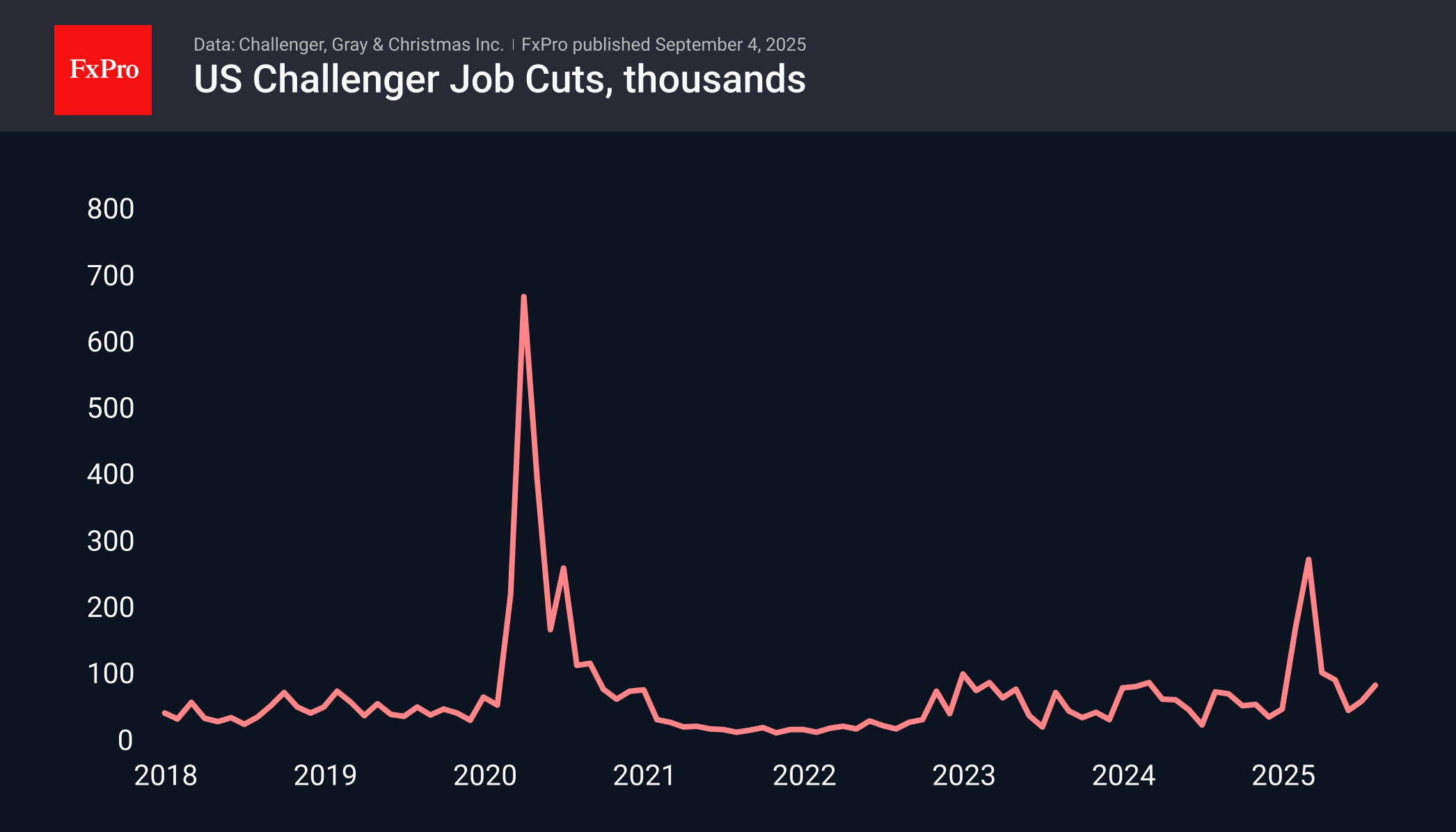

Earlier on Thursday, statistics on planned layoffs were also released. In August, their number approached 86,000, compared to 62,000 a month ago and 76,000 a year earlier. This indicator, more than any other, points to a deterioration, with nearly 900,000 layoffs since the beginning of the year. Only in 2009 and 2020 were the figures higher. At that time, there were severe recessions, but now, the consequences of optimisation in healthcare and finance are as follows. The report also mentions the lowest number of planned expansions since records began in 2009 – 1,494.

According to ADP, the number of private-sector jobs grew by 54,000 in August, compared to 106,000 a month earlier. This is slightly worse than the expected 74,000. The leisure (+50,000) and construction (+16,000) sectors fared better than others. Trade (-17,000), healthcare and education (-12,000), and manufacturing (-7,000) made a negative contribution.

The number of initial claims for unemployment benefits rose to 237,000, the highest since the end of June. Overall, the figure is roughly in the middle of the range for the past year and a half.

The indicators do not suggest any dramatic deviation in tomorrow’s official data from the average values of recent months. Market analysts predict an average value of around 75,000, but we would not be surprised to see a value of 130,000, which would correspond to the average values of the last year and a half. Strong figures are also unlikely to stop the Fed from returning to a cycle of rate cuts, and the main subject of speculation is the number of cuts before the end of the year, two or three. The latest data is more on the side of the ‘two’-camp, but it is important to consider the political pressure on the Fed.

Swiss CPI Declines, Will SNB Revert to Negative Rates?

The Swiss franc has edged lower on Thursday. In the North American session, USD/CHF is trading at 0.8052, down 0.13% on the day.

Swiss CPI declines in August

Swiss inflation declined in August for the first time since January. CPI slipped 0.1%, following the July reading of zero and the market estimate of zero. Yearly, CPI rose 0.2%, unchanged from July and in line with the market estimate.

The soft inflation report could support the case for the Swiss National Bank to return to negative interest rates. The SNB had a negative rate policy in effect for eight consecutive years until 2022, when high inflation forced the bank to sharply tighten policy. The markets widely expect the SNB to hold rates at this month's meeting, but if inflation continues to sag, there will be pressure on the central bank to lower rates.

SNB President Martin Schlegel has stressed in the past that the central bank could revert back to negative rates if necessary but would try to avoid doing so since it causes difficulties for businesses and consumers.

The SNB is also keeping a close eye on the value of the Swiss franc. The Swiss currency has soared against the US dollar, gaining 11.3% since the start of the year. In June, USD/CHF fell below the psychologically significant 0.80 level for the first time 2011. The central bank does not want the franc to continue appreciating, since it means that Swiss exports are more expensive and thus less competitive.

US tariffs have dealt a blow to the export-reliant Swiss economy. Switzerland has had to absorb US tariffs of 39% on most goods, which has put the country at a serious disadvantage against the neighboring European Union, which faces tariffs of only 15% on most goods.

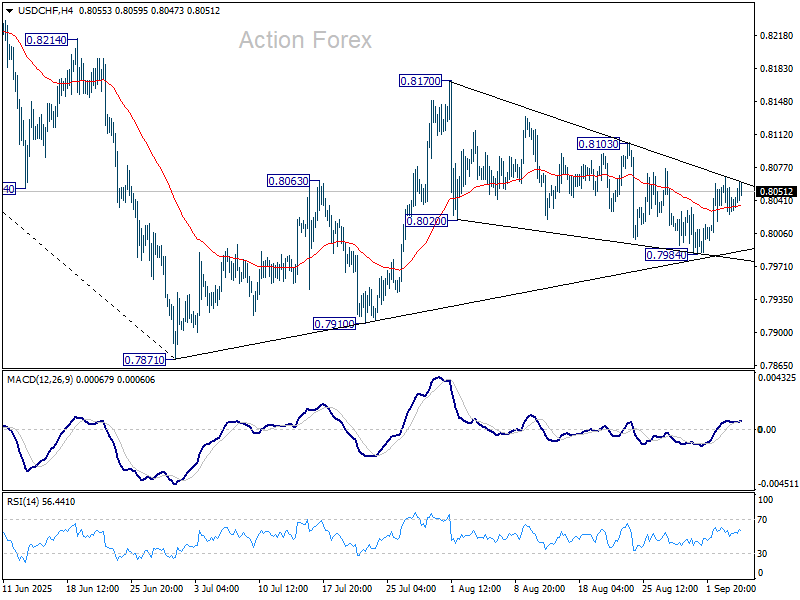

USD/CHF Technical

- USD/CHF is testing resistance at 0.8045. Next, there is resistance at 0.8054 and 0.8064

- 0.8035 and 0.8026 are providing support

USDCHF 4-Hour Chart, September 4, 2025

US ISM services rises to 52.0, new orders surge despite jobs weakness

US services activity picked up in August, with ISM Services PMI rising to 52.0 from 50.1, comfortably above expectations of 50.9. The headline gain was supported by stronger demand conditions, highlighting resilience in the sector despite lingering economic uncertainty. ISM noted the reading corresponds to a 1.1% annualized rise in GDP.

Details showed business activity rising to 55.0 from 52.6, while new orders jumped sharply to 56.0 from 50.3, marking the strongest pace since early this year. The improvement highlighted a rebound in demand momentum as companies prepared for the holiday season, with some firms reportedly advancing purchases to get ahead of tariff-related price increases.

The employment index, however, remained in contraction at 46.5, signaling persistent softness in hiring within the services sector. Meanwhile, the backlog of orders fell to a 16-year low, tempering optimism about the durability of demand. Prices stayed elevated at 69.2, marking a ninth consecutive month above 60—a sign of ongoing cost pressures across the industry.

ISM said commentary from respondents was dominated by tariff concerns, with firms highlighting both higher input costs and evidence of import demand being pulled forward.

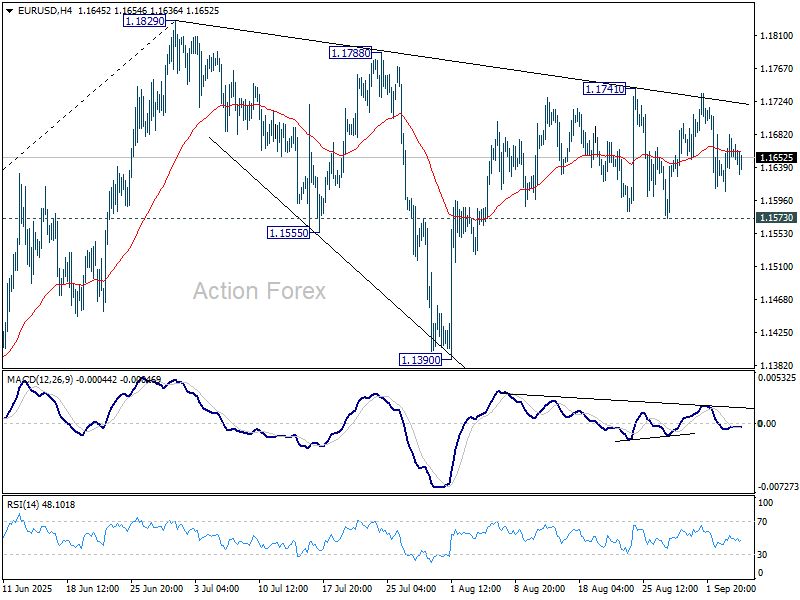

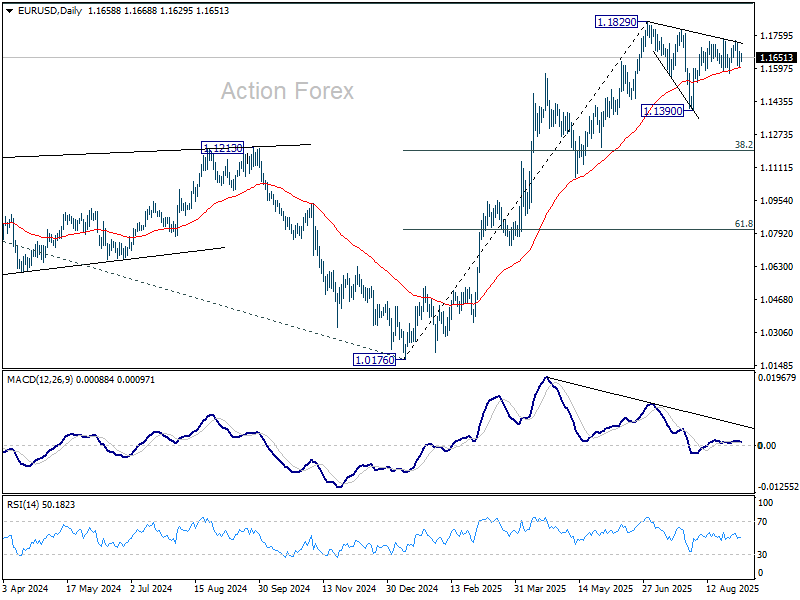

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1619; (P) 1.1650; (R1) 1.1693; More...

EUR/USD is bounded in sideway trading and intraday bias stays neutral. Further rise is in favor as long as 1.1573 support holds. Corrective fall from 1.1829 should have completed with three waves down to 1.1390. On the upside, above 1.1741 will bring retest of 1.1829 high first. Firm break there will resume larger up trend. However, sustained break of 1.1573 will dampen this view, and indicate that corrective pattern from 1.1829 is extending with another falling leg towards 1.1390 again.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

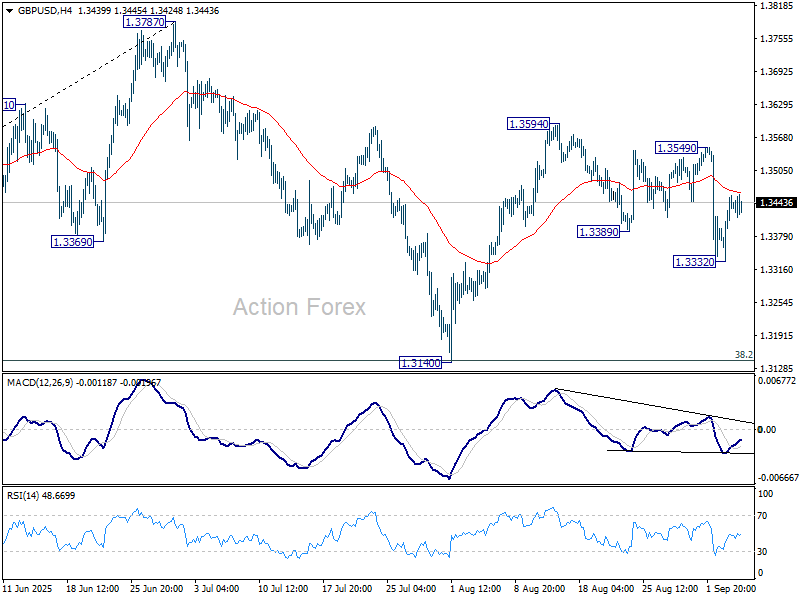

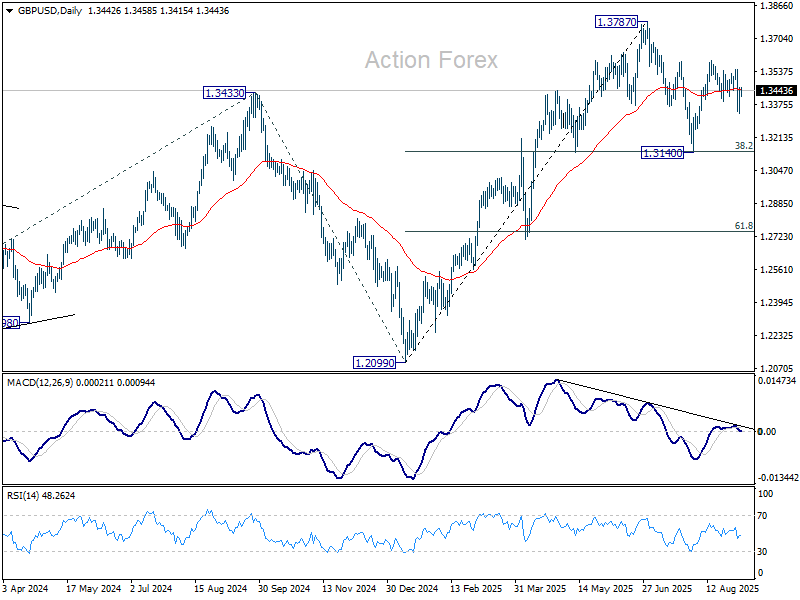

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3365; (P) 1.3412; (R1) 1.3489; More...

Intraday bias in GBP/USD stays neutral at this point. Overall outlook is unchanged that corrective pattern from 1.3787 is extending. Below 1.3332 will bring deeper pullback. But downside should be contained by 38.2% retracement of 1.2099 to 1.3787 at 1.3142. On the upside, break of 1.3549 resistance should resume the rebound from 1.3140 towards 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3104) holds, even in case of deep pullback.

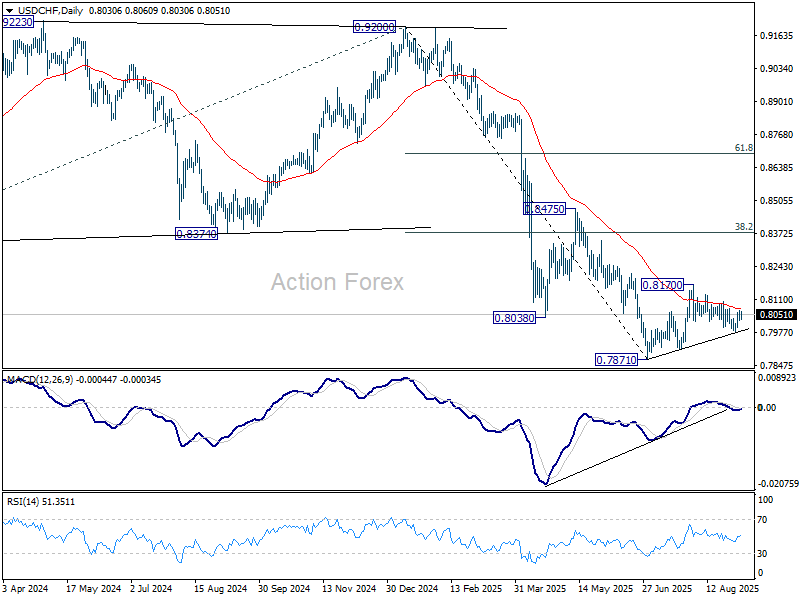

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8025; (P) 0.8046; (R1) 0.8066; More….

Intraday bias in USD/CHF stays neutral for the moment. On the downside, break of 0.7984 will resume the fall from 0.8170 to 0.7910 support first, and then retest of 0.7871 low. However, break of 0.8103 resistance will turn bias to the upside to resume the rebound from 0.7871 through 0.8170.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

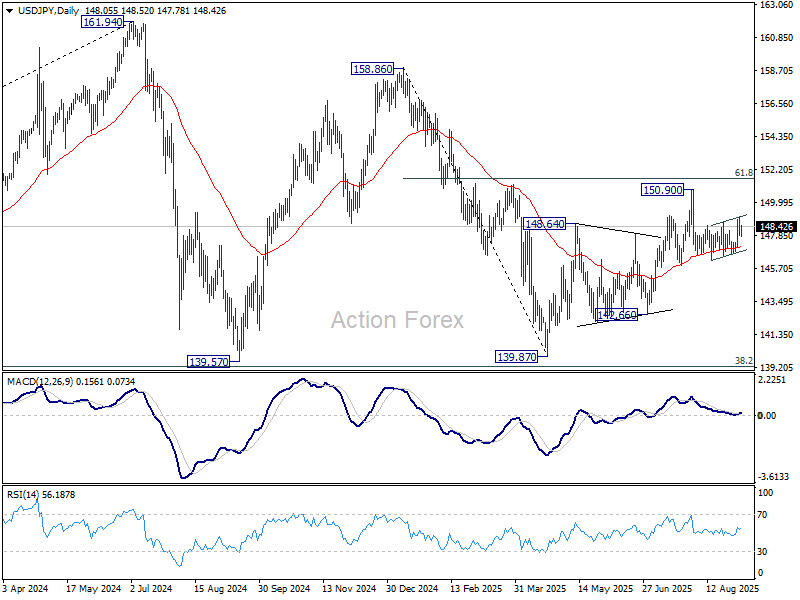

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.61; (P) 148.38; (R1) 148.87; More...

Intraday bias in USD/JPY remains neutral at this point. On the upside, above 149.12 will resume the rebound from 146.20 to retest 150.90 high. Break there will resume the rise from 139.87 to 151.22 fibonacci level. However, on the downside, break of 146.65 support will resume the decline from 150.90 through 146.20 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.