Forex markets were subdued in Asian session today, with major pairs showing little movement while regional equities held steady. The muted tone comes despite a disappointing run of Chinese economic data, which showed broad weakness in activity. Investors appeared reluctant to extrapolate too much pessimism from the Chinese numbers. Instead, the data reinforced expectations that Beijing will be forced to accelerate stimulus measures. For traders, the prospect of stronger state support is cushioning risk sentiment, limiting downside pressure on Asian assets.

The policy outlook in China remains closely tied to the Fed. Once the Fed’s rate-cut path is clearly defined, the PBoC will have greater room to ease without triggering destabilizing capital outflows. That dynamic has kept speculation alive of further PBoC cuts in the months ahead, especially as growth signals soften.

While markets are steady for now, volatility is expected to rise sharply this week with four major central bank meetings on deck. The Fed takes center stage, with a widely expected rate cut that carries unusually high risks due to voting splits and fresh economic projections. The BoC, BoE, and BoJ decisions will also be closely watched, alongside a heavy data calendar that includes UK jobs, CPI, and retail sales, Germany’s ZEW survey, Australian employment, and New Zealand GDP.

While monetary policy dominates, geopolitics is also back in play. High-level U.S.–China trade talks kicked off in Madrid on Sunday, bringing together Treasury Secretary Bessent and USTR Greer with Vice Premier He Lifeng and chief negotiator Li Chenggang. The meeting follows July’s Stockholm discussions that extended a 90-day tariff truce and reopened rare-earth exports to the U.S. That extension keeps the pressure on Beijing while limiting near-term escalation.

Still, expectations for a breakthrough remain muted. There is little chance of a major agreement, with another temporary extension the most likely outcome. Markets are particularly focused on whether Washington delays the Sept. 17 deadline for ByteDance to divest TikTok’s U.S. operations, a decision that could otherwise trigger a ban.

In Asia, at the time of writing, Nikkei is up 0.89%. Hong Kong HSI is up 0.19%. China Shanghai SSE is down -0.17%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is flat at 1.602.

NZ services PMI slumps to 47.5, 18th month contraction

New Zealand’s services sector deteriorated further in August, with BusinessNZ Performance of Services Index slipping from 48.9 to 47.5, well below the long-run average of 52.9. The reading also marks the 18th consecutive month of contraction. Both

Activity/Sales (46.2) and New Orders/Business (47.8) weakened, suggesting demand remains fragile. Employment improved slightly to 48.3 but remains in contraction territory, reflecting businesses’ reluctance to expand payrolls in the face of subdued activity.

The survey showed 59.6% of respondents made negative comments in August, an increase from July but still less pessimistic than June’s tally. Firms cited multiple pressures, including high interest rates, sticky inflation, and the cost-of-living squeeze eroding household spending. Rising operating costs, seasonal slowdowns, supply chain disruptions, and uncertainty over government policy also weighed on sentiment.

China industrial output, retail sales miss forecasts, fixed asset investment slumps

China’s economy slowed in August, with key indicators falling short of expectations. Industrial output grew 5.2% yoy, down from 5.7% yoy in July and short of forecasts for 5.8% yoy, marking its weakest pace since August 2024. Retail sales also slowed, rising just 3.4% yoy versus 3.7% yoy previously and expectations of 3.8% yoy, signaling soft household demand despite ongoing government measures to support spending.

Investment activity showed the sharpest loss of momentum. Year-to-date fixed asset investment rose only 0.5%, far weaker than consensus 1.4% and July’s 1.6%. The drag came primarily from the property sector, where real estate investment plunged -12.9% in the first eight months. Excluding real estate, investment rose 4.2%.

The National Bureau of Statistics highlighted “many unstable and uncertain factors” in the global environment and warned that the economy still faces “multiple risks and challenges.” It urged stronger policy implementation to stabilize employment, businesses, and expectations, but the latest figures suggest momentum remains fragile, with property weakness continuing to weigh heavily on growth prospects.

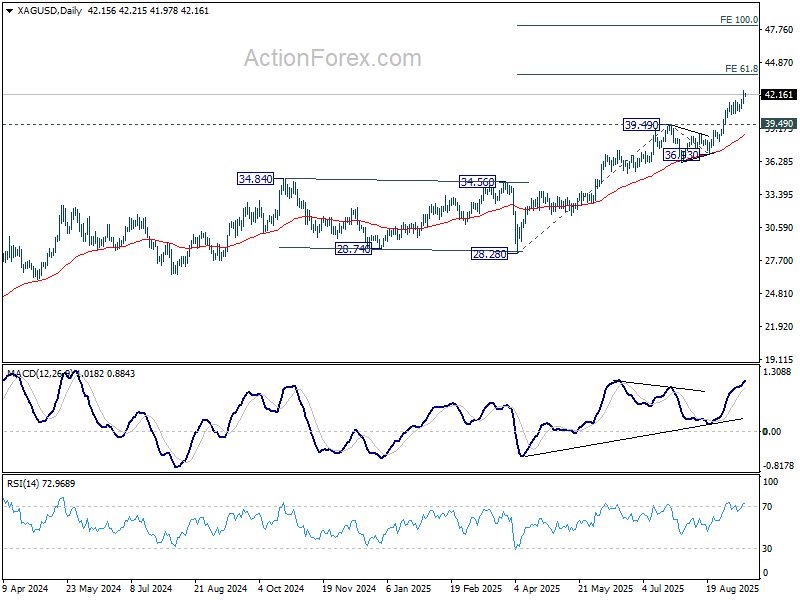

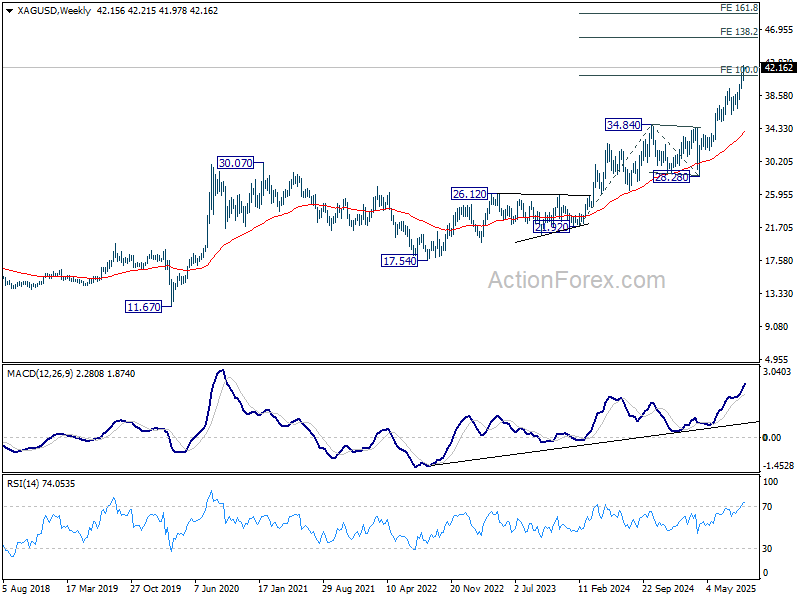

Silver steals spotlight, charging toward 50 while Gold pauses

Precious metals remain firmly bid, but leadership has shifted. Gold’s rally stalled just ahead of a key Fibonacci projection, while Silver broke out to a new 14-year high. Both metals remain supported by a mix of geopolitical risk, policy divergences, and strategic investor demand for hard assets.

Silver’s case is probably more compelling. The market faces a prolonged supply deficit and tightening physical availability, giving its rally deeper structural foundations. This dynamic, coupled with strong investor interest, has pushed prices higher and opened room for further gains on both near-term and medium-term horizons.

Near-term, Silver will remain bullish above former resistance at 39.49, now turned support. Next target is 61.8% projection of 28.28 to 39.49 from 36.93 at 43.85. Decisive break there could prompt upside acceleration to 100% projection at 48.14.

On the broader time frame, Silver has already cleared 100% projection of 21.92 to 34.84 from 28.28 at 41.20, setting up to 138.2% projection at 46.13. There is potential of further rally to 161.8% projection at 49.18 before topping, as the fifth wave of the five-wave rally from 17.54.

So in short, for Silver, holding 40 keeps the bullish structure intact, with acceleration toward 50 possible once 44 is cleared.

Gold, meanwhile, looks set to consolidate further in the short term, below 261.8% projection of 3267.90 to 3408.21 from 3311.30 at 3678.63. But pullback should be contained above 3511.49 support to bring rebound. Firm break of 3678.63 will target 323.6% projection at 3765.34 next.

Fed, BoC set to ease as BoE, BoJ hold fire

Global markets face one of the busiest weeks of the year, with four major central bank meetings alongside a heavy slate of data releases. The Fed and BoC are widely expected to resume their rate-cutting cycles, while the BoE and BoJ are set to hold steady but with close attention on forward guidance.

The Fed meeting is the marquee event. Consensus expects policymakers to cut rates by 25bps, bringing the target range to 4.00–4.25%. That would mark the first move since November 2024 with possible signal of re-acceleration of the easing cycle following recent weak labor market data. However, the outcome may not be as straightforward, with the vote split and economic projections likely to carry as much weight as the headline cut.

Several uncertainties cloud the decision. Governors Christopher Waller and Michelle Bowman, both leaning dovish, could press for a 50bps move given the labor market softening. The status of Stephen Miran, nominated as temporary Governor, also looms large—if confirmed in time, his vote could tilt the balance toward a deeper cut. On the other side, Lisa Cook may favor holding steady, introducing the risk of multiple dissents in either direction. This raises the possibility of a fractured committee outcome.

Fresh economic projections will also matter. With job growth stalling and unemployment edging up, the new dot plot may shift from penciling in two cuts this year to three. A Reuters poll showed 60% of economists expect 50bps of easing by year-end, while 37% forecast 75bps. That diverges from market pricing, where traders see over an 80% chance of 25bps moves in both October and December. The outcome will shape expectations not only for 2025 but for how long rates stay restrictive into 2026. Retail sales data later in the week adds another variable for Fed watchers.

The BoC is also set to move. Markets and economists overwhelmingly expect a 25bps cut, lowering the policy rate to 2.50%. A Reuters survey showed 25 of 32 economists anticipate easing this week, aligning with market pricing. Among Canada’s top five banks, RBC stands out in expecting a hold, contingent on the latest inflation release due just before the decision.

Forward guidance will be critical. Over 70% of economists predict the BoC will deliver at least 50bps of cuts by year-end, taking the policy rate to 2.25% or lower, with a minority even expecting 75bps. How Governor Tiff Macklem frames the balance between still-firm wage growth and a weakening consumer sector will guide expectations. Given recent soft Canadian data and rising global risks, markets will be quick to price in more cuts if the BoC leaves the door wide open.

In the UK, the BoE is set to keep Bank Rate unchanged at 4.00% this week. But the outlook is contested. A Reuters poll found 42 of 67 economists expect one final cut in November, while 22 see no further moves this year. Upcoming jobs, CPI, and retail sales data will heavily influence the November call. With inflation expectations edging higher, the BoE is cautious about easing too far, too fast.

The BoJ is also expected to stand pat at 0.50%, preferring more time to assess how new U.S. tariffs and trade deals affect the economy. Policymakers are also monitoring whether food price inflation recedes in coming months, as well as the impact of stronger wage settlements. A Reuters poll showed 55% of economists expect the BoJ to hike to 0.75% by next quarter, leaving risks tilted toward further tightening. Japan’s national CPI release later this week will be a key test of whether inflation pressures are indeed moderating.

Beyond central banks, data releases from Germany’s ZEW survey, Australian employment, and New Zealand GDP will round out a packed week.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; China industrial production, retail sales, fixed asset investment; Swiss PPI; Eurozone trade balance; Canada manufacturing sales, wholesale sales; US Empire state manufacturing.

- Tuesday: Japan tertiary industry index; UK employment; Canada CPI; US retail sales, import prices, industrial production, business inventories, NAHB housing index.

- Wednesday: Japan trade balance; UK CPI; Eurozone CPI final; US housing starts and building permits, FOMC rate decision; BoC rate decision.

- Thursday: New Zealand GDP; Australia employment; Swiss trade balance; ; Eurozone current account; BoE rate decision; US jobless claims, Philly Fed manufacturing.

- Friday: Japan CPI, BoJ rate decision; Germany PPI; UK retail sales, public sector net borrowing; Canada retail sales.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1709; (P) 1.1728; (R1) 1.1756; More…

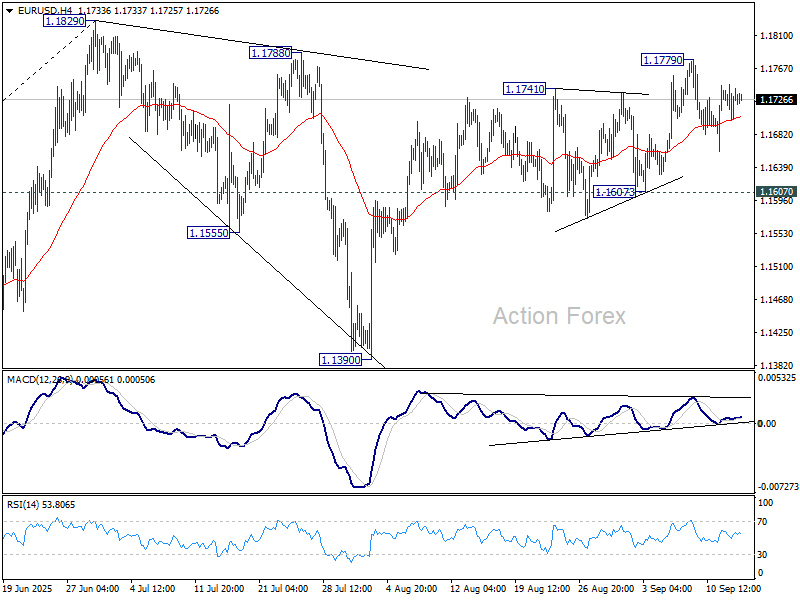

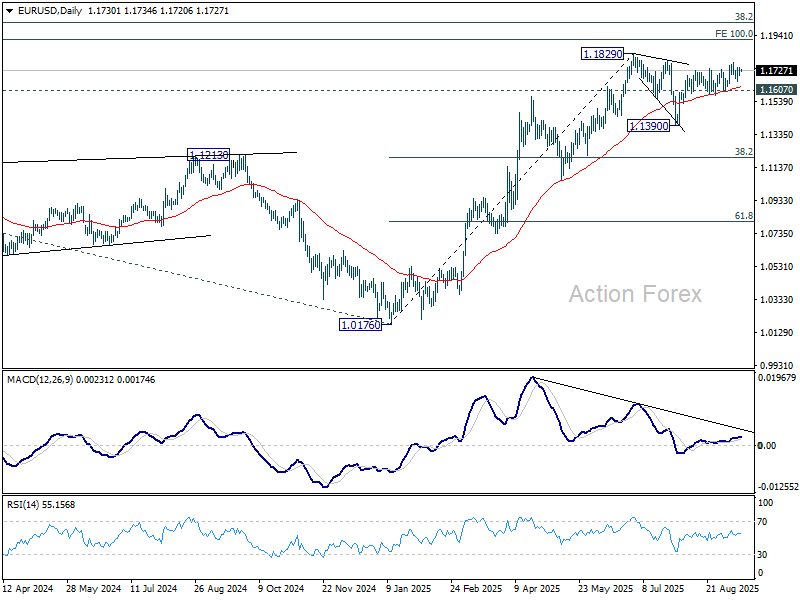

Range trading continues in EUR/USD and intraday bias remains neutral. With 1.1607 support intact, further rise is expected. On the upside, above 1.1779 will target a retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level next.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 55 W EMA (now at 1.1174) holds.

{kind=link}