Yen strengthened modestly in quiet Asian trading, with many regional centers closed for Lunar New Year. Liquidity remains thin, keeping most major pairs confined within last week’s ranges. Despite limited volatility, Japanese assets offered a subtle signal of resilience.

Japan’s government bonds extended gains after the first JGB auction since the snap election passed without disruption. Demand at the five-year debt sale improved slightly, with the bid-to-cover ratio rising to 3.10 from 3.08 previously — the first increase since September.

While the improvement does not signal a full recovery in investor confidence, it suggests markets are stabilizing following the election uncertainty. Importantly, the auction cleared without disorderly selling, passing what many viewed as a near-term litmus test.

Attention now turns to the 20-year auction scheduled for February 19, which will provide a clearer read on longer-end demand. Sustained strength in JGBs could lend additional support to Yen.

Elsewhere, Aussie remains steady after RBA minutes reaffirmed tightening bias. Markets continue to price a high probability of a May rate hike, limiting downside in AUD. However, the next leg higher will likely require confirmation from incoming data. Thursday’s employment report stands as the immediate catalyst.

In commodities, Gold and Silver edged lower, partly tracking Dollar’s modest recovery. Easing geopolitical tensions also weighed on safe-haven demand. US President Donald Trump said he would be involved “indirectly” in renewed talks with Iran over its nuclear program in Geneva, expressing belief that Tehran seeks a deal. Separately, US-mediated discussions between Ukraine and Russia resume in Geneva, focusing on territorial issues.

Reduced geopolitical risk premium has contributed to mild pullback in precious metals, aligning with technical vulnerability highlighted previously here.

So far this week, Dollar leads performance, followed by Kiwi and Aussie. Sterling is the weakest, trailed by Yen and Euro, while Swiss Franc and Loonie sit in middle. Yet with major pairs still trapped within last week’s ranges, conviction remains low and broader direction awaits stronger catalysts.

RBA minutes sees risks tilting toward tighter policy

Minutes of RBA’s February 3 meeting revealed that while the case for holding rates was considered, members ultimately saw a stronger argument for raising the cash rate by 25 bps to 3.85%. The decision reflected growing concern that inflation pressures may prove more persistent than previously anticipated.

The Board judged that part of the recent rise in inflation likely reflects sustained “capacity pressure”, and that financial conditions were “currently not restrictive enough ” to return inflation to target within a reasonable timeframe. Data received since the previous meeting strengthened the view that, “without a policy response, inflation could remain persistently above target for too long.”

Members also acknowledged that risks to both price stability and full employment objectives had “shifted materially”. Staff forecasts show inflation staying above the midpoint of the target range for at least two more years, based on a market-implied path that assumes two additional hikes in 2026. If realized, that would extend the already prolonged period during which underlying inflation has exceeded target. At the same time, downside risks to the labor market were seen as having diminished.

Still, policymakers stressed “prevailing uncertainties meant it was not possible to have a high degree of confidence in any particular path for the cash rate.” The minutes suggest the tightening bias remains intact, but future moves will hinge squarely on incoming data, particularly inflation and labor market developments.

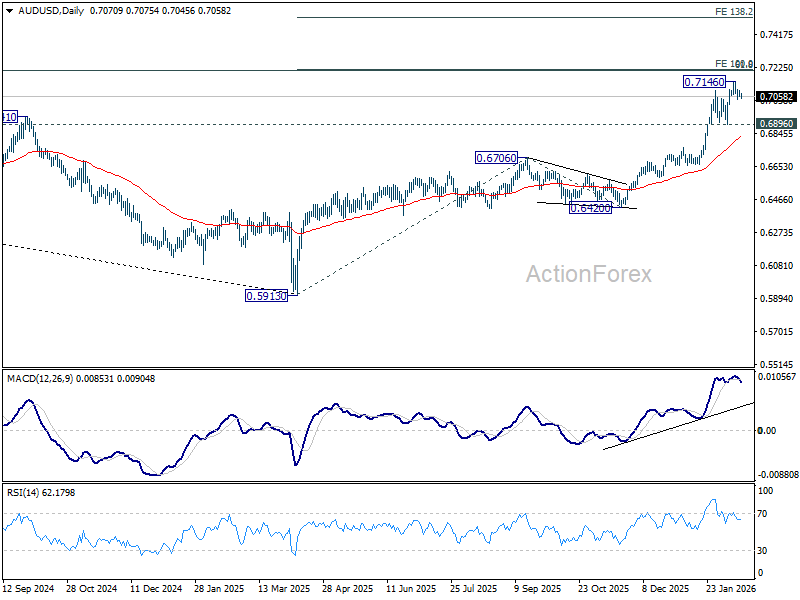

AUD/USD steady after RBA minutes, momentum tempered but uptrend intact

AUD/USD is steady after RBA minutes reinforced tightening bias, though policymakers emphasized low confidence in outlining the next move. That cautious messaging capped immediate upside follow-through. Still, markets continue to price a solid chance of a May rate hike, despite growing talk that the currency’s recent surge could lessen the need for further tightening. As long as those expectations remain intact, any pullback in AUD/USD should be contained, leaving the broader uptrend undisturbed.

In recent days, arguments have surfaced that Aussie’s recent surge may act as a “shadow hike,” reducing need for additional tightening. Since early January, AUD has rallied roughly 5.8% against Dollar and 4.8% against Yuan. A stronger exchange rate lowers import prices, theoretically easing inflation pressure without further rate increases.

Given that China accounts for roughly 25–30% of Australia’s total trade and US around 11% of goods imports, the appreciation looks meaningful. Standard models suggest that a sustained 10% appreciation trims headline inflation by about 0.5–1.0% over a year.

However, relying on currency strength alone to anchor inflation is a risky strategy. The recent 5% move is helpful but limited, and its impact is concentrated in goods prices. Yet goods inflation is no longer the primary problem. December CPI showed headline at 3.8%, driven by domestic pressures. Rent inflation persists amid structural housing constraints. Services costs remain elevated due to wage dynamics. In short, exchange-rate strength does little to address core domestic drivers.

The logic for further tightening rests on three pillars a stronger AUD cannot directly weaken. First, labor market remains tight, and wage growth continues to support services inflation. Second, productivity gains remain modest. Without stronger output per worker, higher wages feed directly into higher prices. Third, fiscal policy still provides tailwinds, offsetting some monetary restraint.

Market pricing continues to assign high probability to another 25bps hike in May, pending Q1 CPI confirmation. Unless data show abrupt cooling in labor market or services pricing, the “shadow hike” narrative is unlikely to displace tightening bias.

Technically, some more consolidations would likely be seen in AUD/USD below 0.7146 short term top. But downside should be contained above 0.6896 support to bring up trend resumption. The real test lies in 0.72 zone, with 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213. Decisive break there will pave the way to 138.2% projection at 0.7516. But that break through 0.72 might need either a shift in expectations for more than one RBA hike this year, or more Fed rate cuts.

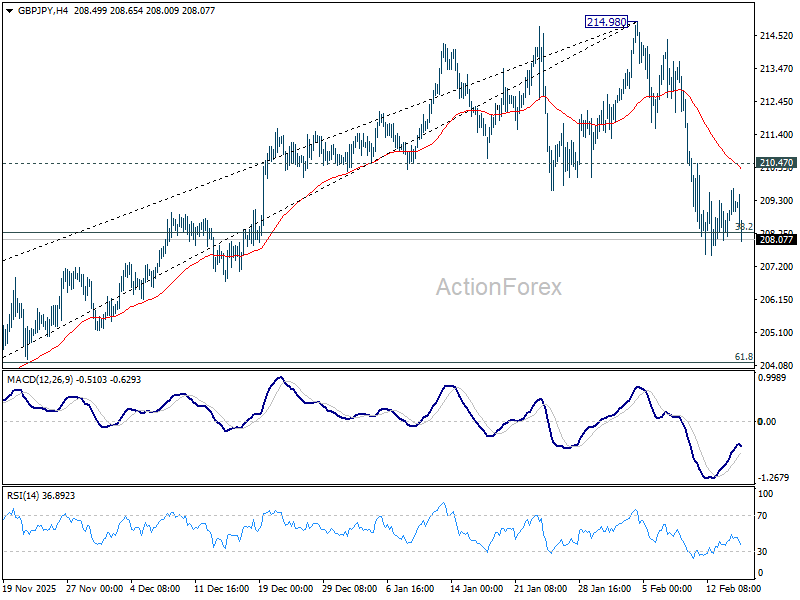

GBP/JPY Daily Outlook

Daily Pivots: (S1) 207.82; (P) 208.58; (R1) 209.28; More…

Outlook in GBP/JPY is unchanged. Intraday bias stays neutral with immediate focus on 38.2% retracement of 197.47 to 214.98 at 208.29. Sustained break of 208.29 will suggest that larger scale correction is already underway and target 203.27 fibonacci level. Nevertheless, strong rebound from current level, followed by break of 210.47 minor resistance will retain near term bullishness, and bring retest of 214.83/98 resistance zone.

In the bigger picture, considering the break of 55 D EMA (now at 209.88), a medium term top could be formed at 214.98. Deeper correction would be seen, but downside should be contained by 38.2% retracement of 184.35 to 214.98 at 203.27. On the upside, break of 214.98 will resume larger up trend from from 123.94 (2020 low), and target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90.

{kind=link}