International Week Ahead

- Eurozone CPI: Disinflation to Keep ECB Asymmetry for Rate Cuts

- Australia GDP: Q4 Growth Recovery Expected, Driven by Consumption

- China PMIs: Contraction, but IEEPA Ruling May Cloud Takeaways

- China Inflation: Deflation Pressures to Remain Present

- China NPC and 15th Five-Year Plan: Significance Has Dwindled

G10

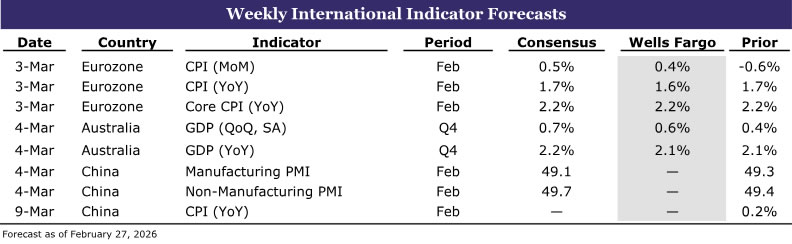

Eurozone February CPI • (03/03)

Broader Disinflation to Keep ECB Asymmetry for Rate Cuts

We expect preliminary readings for February CPI to come in at 0.4% month-over-month, below consensus at 0.5% (per Bloomberg). In terms of the year-over-year numbers, we expect headline inflation to decline to 1.6% from 1.7% and core to hold at 2.2%. Disinflationary pressures have broadened in recent months beyond energy prices and have encompassed both non-energy industrial goods (NEIG) and services. A stronger EUR, goods diversion from China and weak global demand has helped drive the softness in NEIG price inflation, whereas easing wage momentum has helped push services inflation lower. Although our baseline remains for the European Central Bank (ECB) to remain on hold, the asymmetry remains firmly tilted towards easing, in our view. The ECB appears comfortable with a slight undershoot of inflation vs. its target (ECB forecast of 1.9% and 1.8% for 2026 and 2027, respectively), however larger shortfalls are likely to bring rate cuts back on the table. Moreover, the ECB is likely to be sensitive to signs of weakness in growth and/or tightness in credit conditions. We continue to believe meaningful support from fiscal policy is not likely until 2027. On the flip side, upside risks to inflation have dissipated significantly absent a meaningful rebound in oil/gas prices.

Australia GDP • (03/04)

Q4 Growth Recovery Expected, Driven by Consumption

Australia’s growth likely strengthened at year-end after a softer Q3 print. While we and consensus expect a Q4 rebound, we see less upside, with GDP rising 0.6% quarter-over-quarter on a seasonally adjusted basis and 2.1% year-over-year (versus consensus expectations of 0.7% and 2.2%, respectively). Q3 GDP grew 0.4% quarter-over-quarter and 2.1% year-over-year, driven mainly by a 0.8% increase in private business investment led by a 7.6% rebound in machinery and equipment. That momentum appears to have faded, as recent capital expenditure data show machinery and equipment spending slowing, and while non-residential construction remained firm, overall business investment momentum likely softened. Consumption, which accounts for roughly half of GDP, was more resilient in Q4, with monthly household spending indicators pointing to stronger activity despite a weaker December, and should be the main growth driver as Reserve Bank of Australia (RBA) rate cuts continued to filter through the economy. As in Q3, net exports and inventories are likely to weigh on growth, with imports continuing to outpace exports and monthly trade data pointing to another drag. In terms of monetary policy implications, we remain comfortable with our base case of one additional rate hike in May, taking the Cash Rate to 4.10%, given still-elevated inflation. However, a weaker-than-expected Q4 growth outcome could likely cap the tightening cycle at a single hike and reduce the risk of further increases later this year.

EM

China Manufacturing & Non-Manufacturing PMI • (03/04)

Contraction Territory, but IEEPA Tariff Ruling May Cloud Takeaways

With most hard activity data delayed due to Lunar New Year celebrations, PMIs will be closely watched to gauge underlying economic sentiment in China. As of January, both the manufacturing and non-manufacturing PMIs are in contraction territory and expectations are for both sentiment indices to remain below 50 when February data are released. Historically, PMI data have been useful to gauge trend direction of China’s economy. Below 50 prints are consistent with decelerating activity, and vice versa. But keep in mind, while February data may show both sectors in contraction, they both may not fully capture a lower effective tariff rate applied to Chinese exports headed for the U.S. after the U.S. Supreme Court’s IEEPA tariff ruling. So while we will be paying attention to both, we will take each with a modest grain of salt. March PMIs next month will likely be more reflective of whether U.S. importers will rush to place orders in China as tariff rates are lower, especially with the Trump administration set to raise the baseline tariff to 15% in the coming weeks and possibly explore new country-specific tariffs through another legal avenues in the coming months. While we remain steadfast in our view that China’s economy is riddled with structural imbalances that will pressure long-term growth rates, short-term growth prospects are holding up on exports with risks to our 4.7% 2026 GDP forecast tilted to the upside.

China Inflation • (03/09)

Weak Consumer Spending and Subdued Export Prices Keep Deflation Pressures Present

Deflation pressures are one of the structural deficiencies within China’s economy, a challenge for short and long-term growth that should be on display when February CPI and PPI data are released next week. On the consumer side, subdued inflation is a product of weak consumer confidence and subdued domestic demand. We can point to a myriad of issues that contribute to soft consumer spending, but an unwillingness by Chinese policymakers to reflate the economy via monetary policy accommodation and fiscal support should mean soft consumer activity likely remains a theme for the foreseeable future. For producers, exporters are still trying to clear our excess inventory and still keeping export prices low. Export prices have come up a bit as authorities have pursued an anti-involution agenda, but we would not expect any significant changes to export prices nor PPI next month. Thematically, exporters may also look to keep prices permanently lower in an effort to maintain market share won last year. China now has ~22% of the global export market, up from ~17% at the end of 2024. How does China maintain market share? Pull-forward of external demand and front-running tariff hikes will help, but keeping prices low doesn’t hurt either.

China National People’s Congress and 15th Five-Year Plan • (03/05 – ~03/19)

Significance Has Dwindled and We Do Not Expect Anything Groundbreaking

The annual gathering of the National People’s Congress (NPC) will start next week, yet will run over the course of the next two weeks. Typically, the NPC is a forum for implementing policy already decided and does not generate much in terms of surprises. We expect a similar result this year. But at least this year’s NPC will be marked by the Chinese Communist Party (CCP) releasing its updated and 15th “Five-Year Plan” designed to offer insight into economic priorities, how the economy will be managed and economic goals for the next five years. In the past, Five-Year Plans were significant—especially during the Great Leap Forward years and the subsequent recovery and pursuit of a more market-driven economy under Deng. But more recently, Five-Year Plans have not offered much in terms of detail nor significant adjustments to how the CCP wants to evolve China’s economy. For the 15th Plan, CCP members have already released a tentative summary of what the final Five-Year Plan will address. Long document, but skimming through suggests little in terms of surprises or significance. While we will pay attention, we anticipate headlines that sound material and economy-altering, particularly in the current tariff and trade backdrop, to amount to more of the same recent trends. We expect market participants to ultimately shrug off the Five-Year Plan and focus elsewhere going forward.

. In terms of the year-over-year numbers, we expect headline inflation to decline to 1.6% from 1.7% and core to hold at 2.2%. Disinflationary pressures have broadened in recent months beyond energy prices and have encompassed both non-energy industrial goods (NEIG) and services.){kind=link}