- Middle East developments drive market sentiment as negotiations appear to have stalled.

- An action-packed week ahead, with key GDP prints, central bank meetings and pivotal US earnings.

- US dollar rebound to be tested if ME newsflow improves and/or ECB and BoE turn hawkish.

- BoJ discontent could trigger intervention; equities could suffer on weaker earnings and geopolitical uncertainty.

Middle East conflict continues to dictate market sentiment

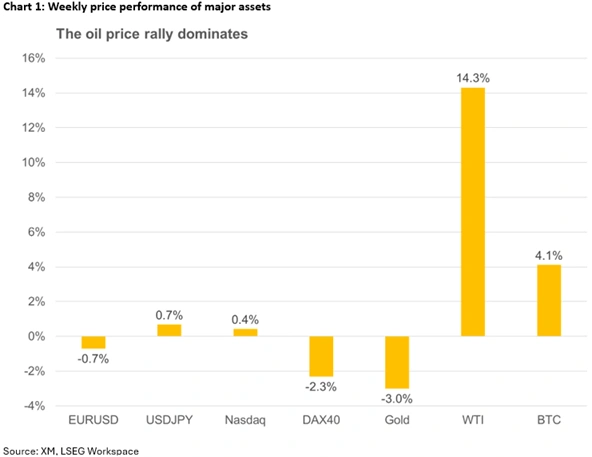

Another week has gone by with investors glued to their screens for developments in the Middle East. Risk appetite has been whipsawed based on the busy newsflow, the lack of a much-talked-about meeting between US and Iranian representatives, and the numerous comments from US President Trump. Notably, major US equity indices managed to record fresh all-time highs and bitcoin climbed to a two-month high, but not everything is shining bright in markets as hostilities could restart at a moment’s notice.

Consequently, oil prices remain in the driving seat, as even the positive scenario of a swift US-Iran agreement pushing oil towards $80 will leave central banks on the edge for second-round effects but obviously quite relieved that the global economy will not come to a standstill due to elevated energy costs.

Amidst this volatile environment, next week brings a rather packed calendar for investors. Key data releases like the preliminary GDP prints for the first quarter of 2026 from both the US and eurozone, and the April PMI surveys from China will complement the five planned central bank meetings and the pivotal US earnings announcements, making next week one of the busiest weeks so far in 2026.

Euro/Dollar rally reverses, Pound/Dollar drops from two-month high

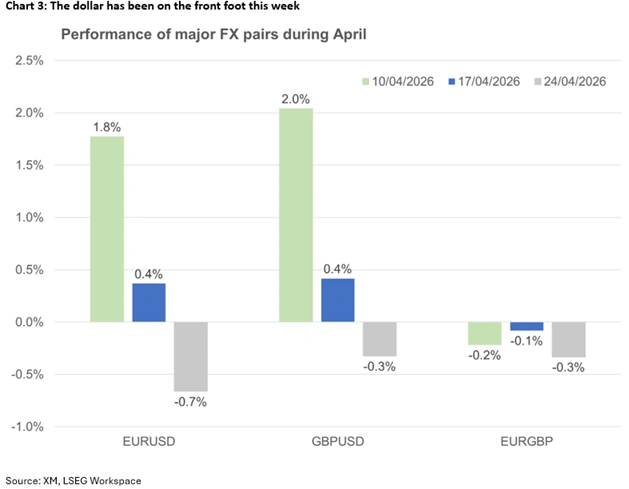

Following a rather difficult first part of April, with the US dollar significantly underperforming against both the euro and the pound, the greenback has been faring much better this week, benefiting from the lack of progress in the Middle East negotiations. At the time of writing, the dollar index is up 0.8% since Monday’s open, reversing last week’s losses.

Understandably, the US will be in the spotlight next week. The preliminary Q1 GDP print, the March durable goods orders report and April’s ISM Manufacturing survey could disappoint on the back of the Middle East conflict, while April’s CB Consumer Confidence index and March’s PCE report could highlight the damage done to spending behaviour as inflation expectations rise and energy costs bite.

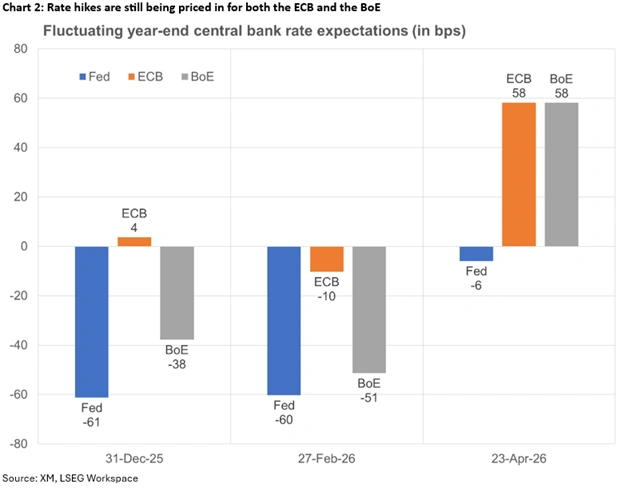

On Wednesday, the Fed meeting is not expected to announce a rate change, given the lack of the usual dot plot and projections, and the fact that Powell might be less inclined for a major tilt in his (most likely) final meeting as Chairman. That said, overall rhetoric and the Q&A session at the usual press conference, along with the possibility of more FOMC members voting with Miran for a rate cut, are pivotal in gauging the sentiment within the committee. Hawkish dissenters are not expected following balanced commentary from Cleveland Fed President Hammack.

On the other side of the pond, the ECB will meet on Thursday. Courtesy of the Middle East developments and surging energy prices, the eurozone is going through a rough patch as per the PMI and ZEW surveys. However, there are no thoughts about rate cuts since inflation has been accelerating and remains the ECB’s only mandate.

Similar to the Fed, the ECB is expected to stand pat. The scenarios presented in the previous meeting will be the main topic of discussion in the council, but most members are expected to support another pause until the picture is completely clear, postponing any decision to June, when the new staff projections will be published. That said, there is a non-negligible risk of President Lagarde sounding more hawkish to please the uber hawks, especially if Thursday‘s preliminary eurozone inflation report shows further inflation pressures and the preliminary Q1 GDP figure surprises on the upside.

Meanwhile, amidst continued pressure on PM Starmer regarding the Mandelson case, the Bank of England will also meet on Thursday. Despite the lack of a sizeable acceleration in March inflation, the jump in the preliminary PMI surveys for April and the impressive March retail sales report have refueled rate hike expectations. To be fair, while the rhetoric from MPC hawks has been quite strong, the doves seem to still be in control of the committee. Therefore, the voting result can tilt either way, with a 5-4 outcome proving extremely market-moving.

Putting everything together, the US dollar will mostly remain whipsawed by developments in the Middle East. However, if there is positive sentiment from the region, even without a peace deal being agreed, the greenback might find itself on the back foot against both the euro and the pound. A successful bounce off the busy 1.1636-1.1671 range in euro/dollar would open the door to a rally towards 1.1830, reversing this week’s move. Similarly, a climb for pound/dollar above the recent local peak of 1.3599 could act as a basis for a more protracted advance, especially if the BoE doves avoid voting for a rate cut.

Could BoJ’s inaction trigger an intervention in Dollar/Yen?

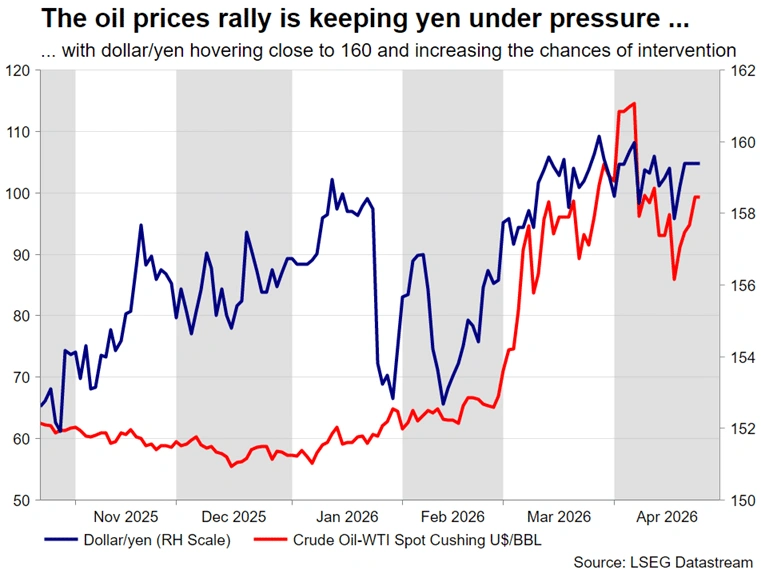

On Tuesday, the Bank of Japan kicks off this round of central bank meetings. Despite a buildup of hawkish expectations ahead of the US-Israel-Iran conflict for the April gathering, a rate hike is out of the picture, which, along with concerns about the Japanese economy due to the blockade of the Strait of Hormuz, can explain the yen’s inability to benefit from the recent dollar weakness.

The focus will mostly be on the overall rhetoric of the BoJ meeting, but yen hawks looking for a clear signal that the BoJ is primed to deliver the much-discussed hike in June might be disappointed again. Dollar/yen trades just below 160 at the time of writing and developments could quickly force BoJ officials to decide if they will continue to tolerate the current high dollar/yen level, which helps exports and inflation, or intervene, reducing pressure on the BoJ to hike rates?

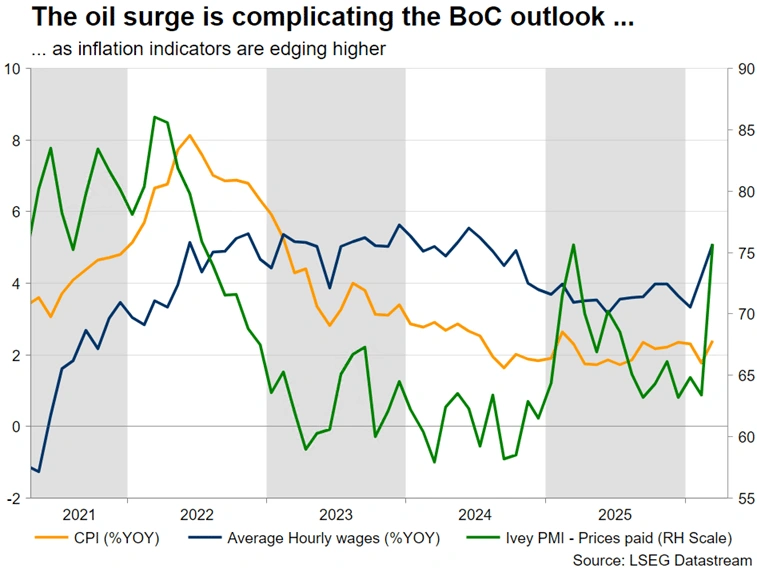

Loonie’s performance rests on BoC’s rhetoric

Commodity currencies have been outperforming the US dollar due to the improved risk appetite and, in the case of the loonie, higher oil prices. However, in the case of the Bank of Canada, which meets on Wednesday ahead of the Fed, growth concerns could still outweigh the inflation surge. No rate change is expected, although the weak March Ivey PMIs might force BoC members to refrain from sounding hawkish. In this case, coupled with negative newsflow from the Middle East, the current upward move in dollar/loonie could extend further, with the 1.3800 being the next key resistance area.

Gold remains directionless while equities appear too optimistic

Gold has been confusing most investors. While in the first part of the US-Israel-Iran conflict, dollar strength was the key factor for gold’s underperformance, the precious metal has failed to rally since early April when the dollar was on the backfoot. And while demand from central banks remains strong, with surveys pointing to further gold buying ahead, and real yields are not rising, gold continues to weaken, which can only mean that certain countries, most likely in the Middle East, are selling gold to raise cash.

On the other hand, US equities are faring much better, ignoring the Middle East developments and the reduced probability of Fed rate cuts in 2026. The current earnings season has been contributing to the sentiment change, but this upbeat sentiment will be put to the test next week as Alphabet, Microsoft, Amazon and Meta will announce their results on Wednesday, followed by Apple on Thursday. Other key earnings announcements include oil giants ExxonMobil and Chevron.

Provided that the situation in the Middle East does not escalate further, a positive set of figures would fuel another move higher, negating concerns about the recent movement being too aggressive – even groundless. Growth and technology stocks are expected to lead such a rally, pushing the usual suspects – the Nasdaq 100 and the S&P 500 indices – to post new all-time highs.

{kind=link}