Yen is stealing the spotlight in an otherwise crowded macro day—and it did not take actual intervention to do it. After pushing through the 160 level earlier this week and hitting 160.71, USD/JPY has staged a dramatic reversal, plunging back toward 155 in a move that has caught traders off guard. The speed and scale of the shift point to a powerful repositioning dynamic, driven by a surge in intervention fears, and then amplified by opportunistic buying..

The catalyst was a “final warning” from Finance Minister Satsuki Katayama, who said the timing for “bold steps” is “now nearing.” That phrase, in Japan’s policy language, is widely understood as a direct precursor to intervention. Katayama’s follow-up message—“don’t put your smartphones down”—reinforced the urgency, particularly heading into Golden Week, when thinner liquidity can amplify market moves.

Markets reacted immediately. Short Yen positions were aggressively unwound, triggering a sharp squeeze. At the same time, new longs began to build, with traders betting that authorities will continue to apply pressure until USD/JPY stabilizes at lower levels, potentially closer to 155 or beyond. Whether Japan has intervened or not is almost secondary—the psychological impact alone has been enough to force a major repositioning.

This episode underscores the power of verbal intervention. Without spending a single Yen—at least officially—Japan has managed to engineer a nearly 500-pip move. More importantly, it has broken the one-way momentum that had dominated the currency, restoring uncertainty and two-way risk.

Meanwhile, Oil is providing the other half of today’s volatility story. Brent surged to a four-year high above $126 earlier in the session, reflecting ongoing geopolitical tensions. But the rally proved unstable, with prices reversing sharply back toward $114.

The pullback appears to be driven more by market mechanics than fundamentals. With April 30 marking the expiry of the June Brent contract, position adjustments and rollover flows likely played a role in the sudden reversal. The result is a highly volatile environment where oil is amplifying, rather than stabilizing, broader market dynamics.

In FX, the ripple effects are clear. Yen is by far the strongest performer, while Swiss Franc is benefiting from the unwind of carry trades. As Yen-funded positions are reduced, the Franc gains too.

Dollar, by contrast, is lagging. The retreat in oil prices has undermined its recent strength, and the greenback is largely ignoring macro data releases. Instead, flows are being driven by positioning and cross-market adjustments.

Sterling is finding modest support from a hawkish signal at the Bank of England, where Chief Economist Huw Pill voted for a rate hike. Euro remains steady, with the ECB’s hold offering little surprise and limited market impact.

The bigger picture is that today’s market is being driven less by data and more by positioning and policy signaling. Japan has shown that credible threats alone can move markets. And for now, the Yen’s dramatic comeback is the clearest sign that traders are no longer willing to test authorities without consequence.

US Personal Income Beats, Spending Solid as PCE Inflation Accelerates to 3.5%

US personal income jumps 0.6% and spending rises 0.9% in March, while PCE inflation accelerates to 3.5%, signaling resurging price pressures. Read More.

US GDP Growth Picks Up to 2.0% but Misses Expectations as Inflation Surges

US GDP grows 2.0% in Q1, missing expectations, as PCE inflation surges to 4.5%, signaling rising price pressures despite solid demand. Read More.

ECB Holds Deposit Rate at 2.00% as Energy Shock Lifts Inflation Risks

ECB holds rates, but the real message is rising risk. Energy prices are pushing inflation higher while threatening growth. Read More.

BoE Holds at 3.75% as Pill Dissent for Hike on Second-Round Inflation Risks

BoE holds rates, but a hawkish dissent is the real story. Rising energy costs are raising fears of persistent inflation. Read More.

Eurozone Inflation Jumps to 3.0% in April, But Core CPI Ticks Down to 2.2%

Eurozone inflation is rising again—but it’s all about energy. Core pressures are easing, leaving policymakers with a difficult call. Read More.

Eurozone Economic Growth Slows in Q1 as GDP Misses Expectations at 0.1% qoq

Eurozone growth is slowing again. Germany is holding up, but France is stalling and overall momentum remains fragile. Read More.

Japan Industrial Output Falls -0.5% as Petrochemical Weakness Dominates

Japan’s factory output is slipping as energy-linked sectors are hit by supply disruptions, even as retail sales rebound and consumption holds up. Read More.

NZ ANZ Business Confidence Slumps to -10.6, Inflation Expectations Highest Since Feb 2024

Cost pressures are surging in New Zealand, driving inflation expectations higher and pushing business confidence back into negative territory. Read More.

China PMI Signals Modest Growth as Services Slip and Cost Pressures Build

China’s PMI data shows resilient output but growing divergence and rising inflation pressures within the economy. Read More.

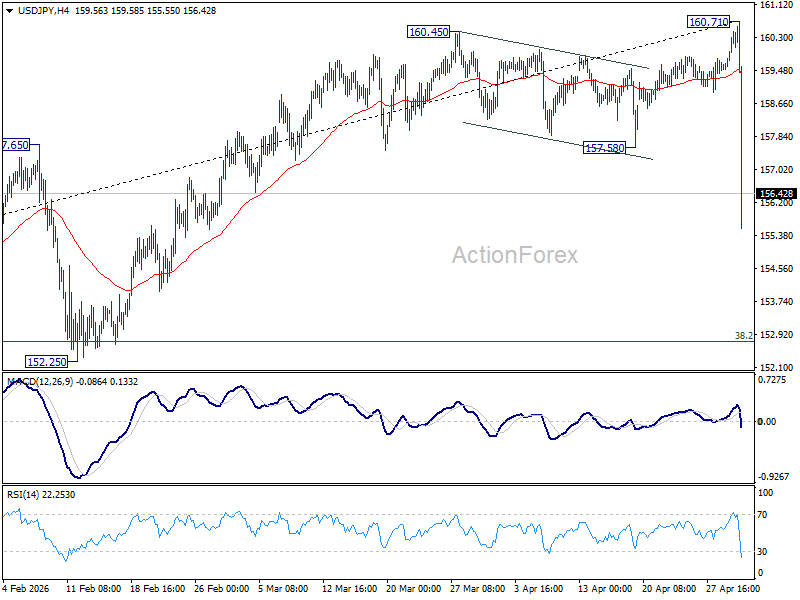

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.79; (P) 160.14; (R1) 160.79; More…

USD/JPY steep decline today suggests medium term topping at 160.71, on bearish divergence condition in D MACD. Deeper fall should be seen to 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). Strong support should emerge there to bring rebound, at least on first attempt. However, decisive break of 152.25/75 will confirm rejection by 161.94 high. That would pave the way back to 61.8% retracement at 147.83 next.

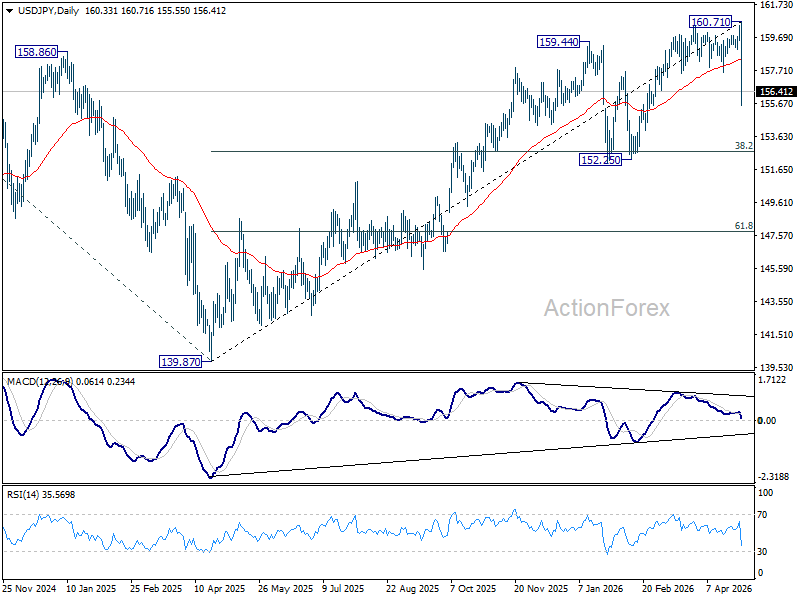

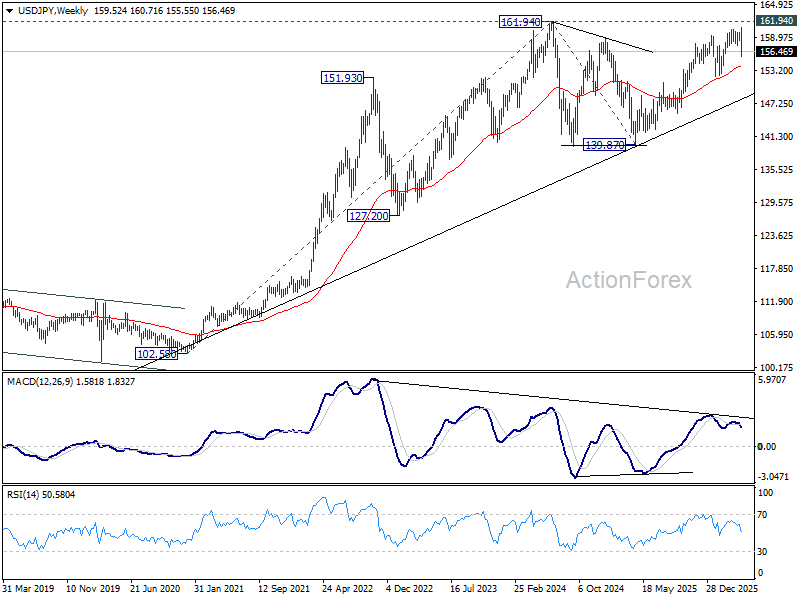

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 153.90) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

{kind=link}