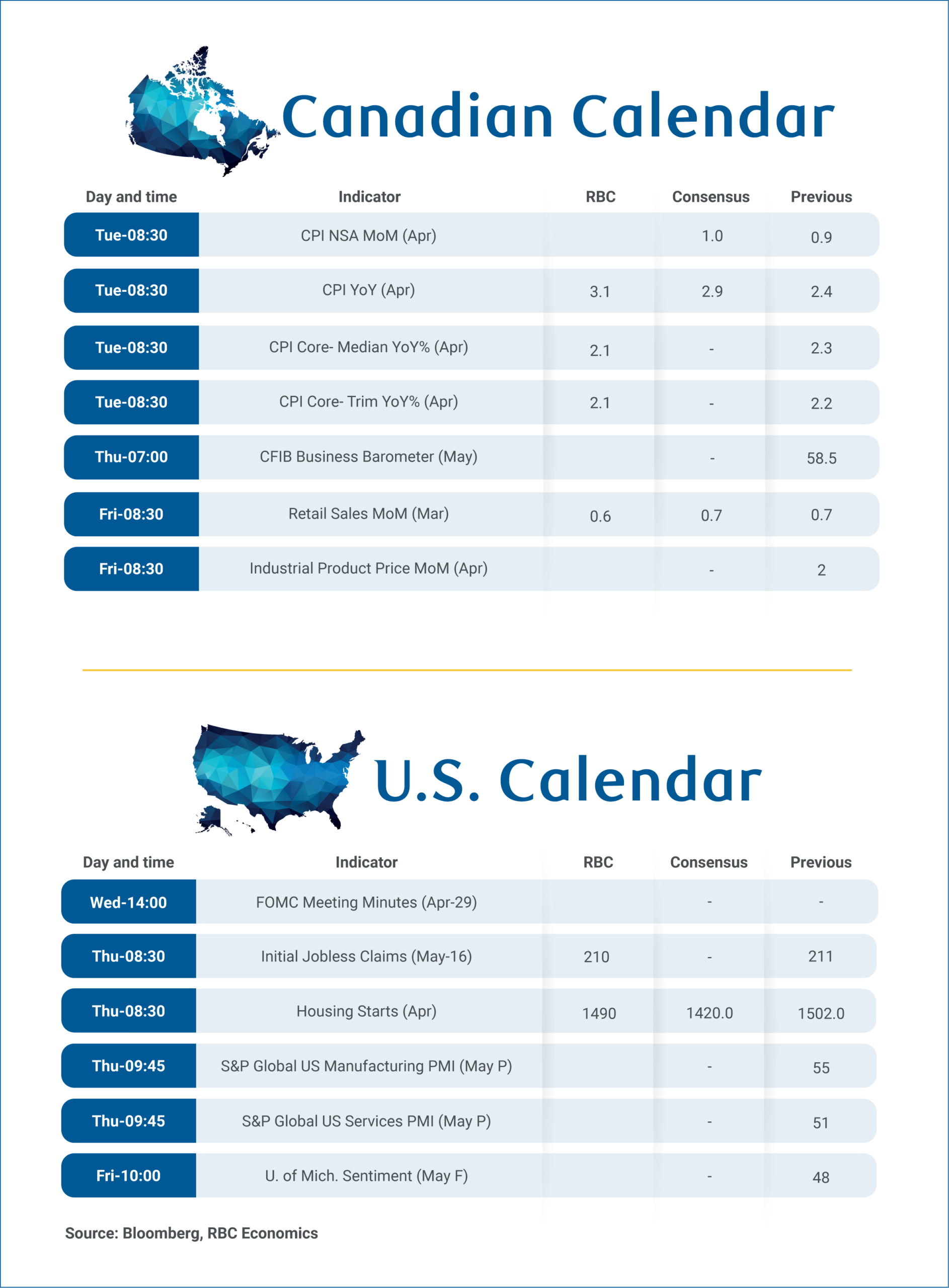

April’s inflation report on Tuesday will be closely watched as the surge in oil prices from conflict in the Middle East continues to drive up gas prices.

We expect headline inflation to rise to 3.1% year-over-year from 2.4% in March, driven primarily by higher fuel costs. Part of it is due to tax distortions. This April is the first month in a year that annual energy price growth won’t be artificially lowered by the removal of the consumer carbon tax in April 2025.

But, gasoline prices also rose another 8% in April after a 21% surge in March, and were up 28% from a year ago. Removal of the 10 cent per litre federal fuel excise tax from April 20 will provide only a small partial offset, and will show up more fully from May onwards. But, after-tax gasoline prices in May are still running more than 30% above a year ago.

The impact of higher oil prices on energy costs are well-known, so focus will be on the extent to which energy price pressures spread to other broader inflation measures.

Will broader inflation pressures reignite?

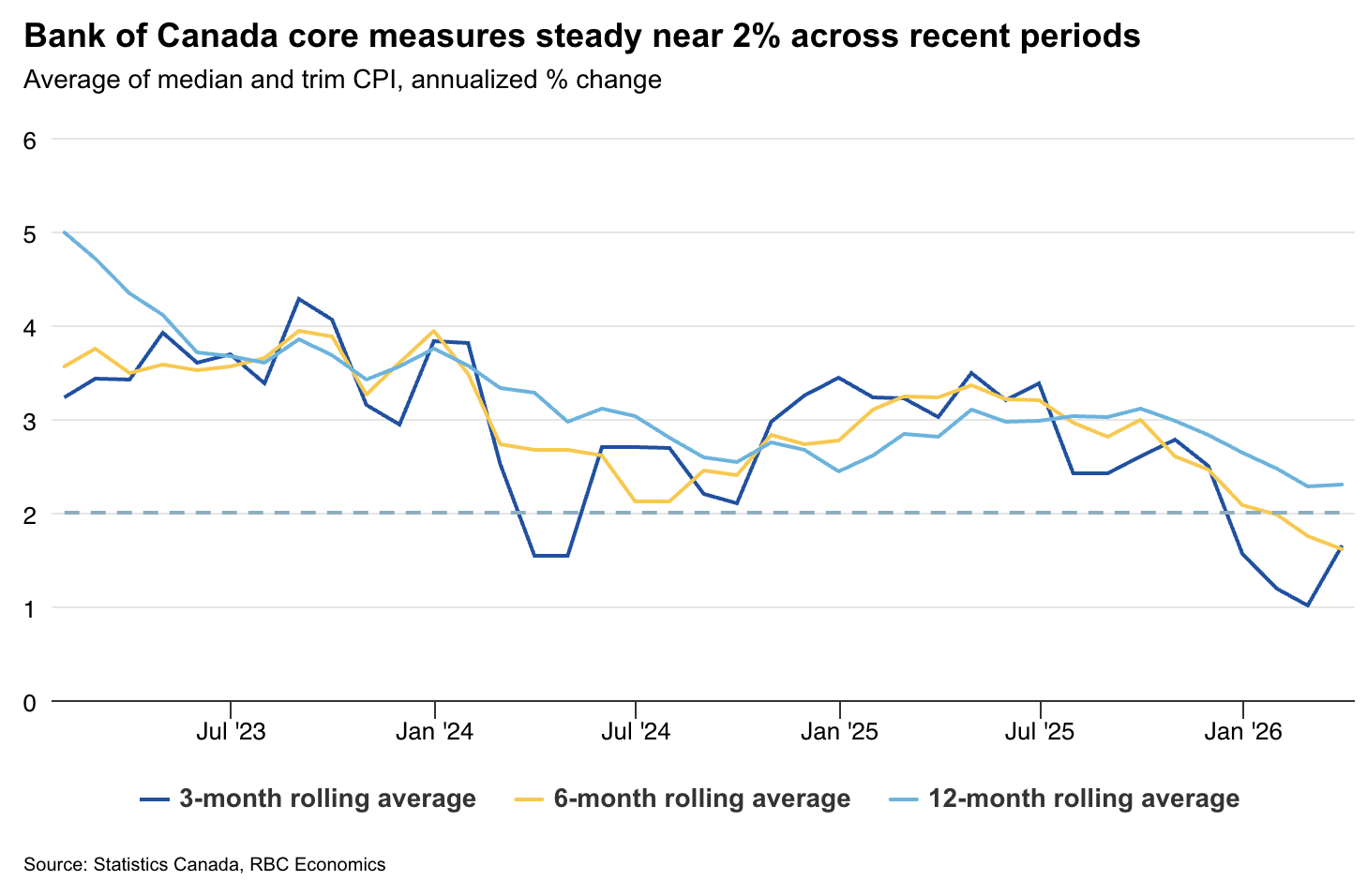

Food price growth remains higher, but we expect it will stay around 4% in April. Broader inflation measures have been consistent recently with cooling underlying price momentum so far. We look for the Bank of Canada’s preferred median and trim measures of broader inflation pressures to tick lower (year-over-year) as a large monthly increase a year ago falls out of the annual calculation.

We don’t expect higher oil prices to re-ignite broader inflation pressures, but that also will depend on the magnitude and duration of the oil price shock. The BoC will continue to watch for any evidence that pressures are spreading.

Business surveys show short-term inflation expectations have risen in recent months alongside energy price spikes, but longer-term expectations remain anchored around target.

This suggests the BoC has room to look through near-term headline volatility, particularly given slower core price growth, and what is still a soft economic backdrop with the unemployment rate elevated at 6.9%. Against this backdrop, our base case forecast for the BoC remains unchanged: We expect rates to hold steady through 2026.

Building on the momentum from February’s retail sales increase, Statistics Canada’s advance estimate suggests retail sales rose 0.6% in March. Household spending has remained a steady engine of growth with RBC cardholder transactions indicating resilience extended into Q1 2026 even as a significant new oil shock hit the economy.

{kind=link}