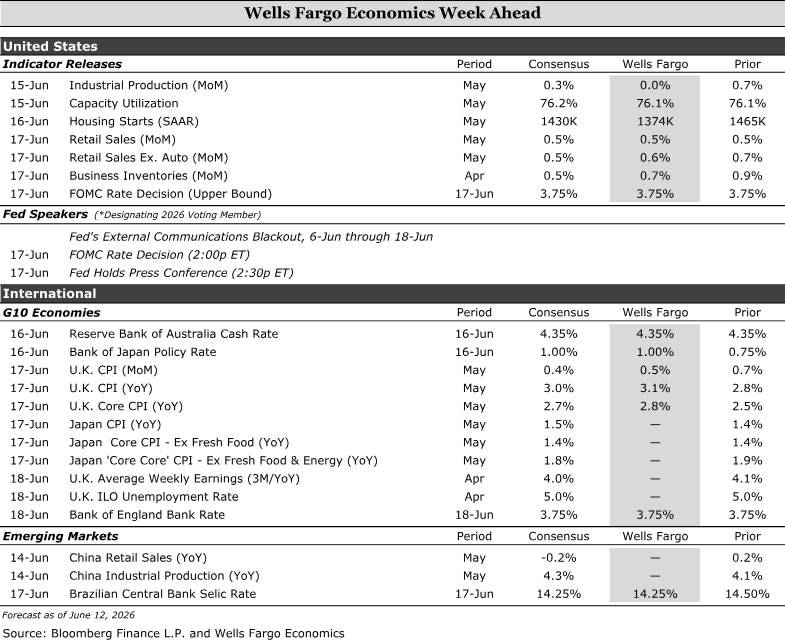

Next week’s calendar is dominated by central bank decisions, with policy paths still shaped by sticky inflation, softer growth and energy-driven uncertainty. We expect the FOMC to strike a neutral tone under Chair Warsh, with easing language likely removed but no clear tightening bias. U.S. retail sales should show consumer spending holding up, though higher gasoline prices are taking a larger share of the consumer wallet. In other advanced economies, the Bank of Japan is likely to hike 25 bps to 1.00%, while the Reserve Bank of Australia and Bank of England should hold for now as they wait for more evidence on inflation pass-through and growth. In emerging markets, we expect the Banco Central do Brasil to cut its Selic Rate by 25 bps to 14.25%, then pause, with easing resuming in Q4.

United States:

- FOMC (Wednesday), Retail Sales (Wednesday)

G10 Economies:

- Bank of Japan (Tuesday), Reserve Bank of Australia (Tuesday), Bank of England (Thursday)

Emerging Markets:

- Brazilian Central Bank (Wednesday)

U.S. Week Ahead

FOMC • Wednesday

We expect the theme of next week’s FOMC meeting will be neutrality. This will be Kevin Warsh’s first meeting as Chair, and we would be surprised if he rocks the boat at a precarious time for U.S. monetary policy. We doubt that Chair Warsh will be full-throated in favor of cutting rates in light of better labor market data and a core PCE deflator that is 130 bps over target. At the May meeting, the Committee debated removing the easing bias from the post-meeting statement, ultimately deciding in a divisive decision to leave it in. We believe that will change at this meeting with the removal of the phrase “the extent and timing of additional adjustments” to be replaced with something more neutral such as “In considering future adjustments to the target range for the federal funds rate, the Committee will….”

That said, we do not think most members of the FOMC, including the Chair, are ready to declare a tightening bias. Yes, the labor market data have been better lately, but there are few signs of overheating in wage growth or job openings, and the current unemployment rate (4.3%) is on the high end of the Committee’s 4.0%–4.3% central tendency range for full employment. Furthermore, given that much of the excess inflation has been driven by supply shocks (tariffs, energy), we believe Chair Warsh will stress a patient and data dependent outlook in the presser.

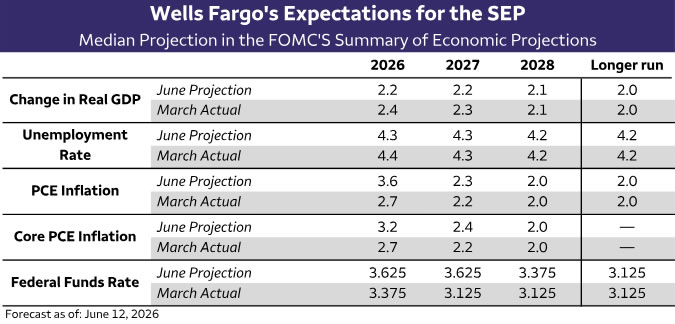

The dot plot looks like a close call. For starters, the dispersion of the dots is likely to tighten with Governor Miran’s low dot dropping out of the picture. The 2026 median dot should shift up to 3.625% thus removing the cut that was in place. Looking to 2027, our sense is this will be the linchpin for how the tone of the dots are perceived overall. If the Fed shows no cuts next year too (and assuming our view on their inflation call is right), they will be signaling a much tighter real rate, which would be an interesting way for the Committee to say they believe the backdrop warrants higher rates without actually hiking. In the end, while we think the dots will offer some interesting nuances, we think ultimately Warsh is likely to be fairly dismissive of the dots on balance.

Retail Sales • Wednesday

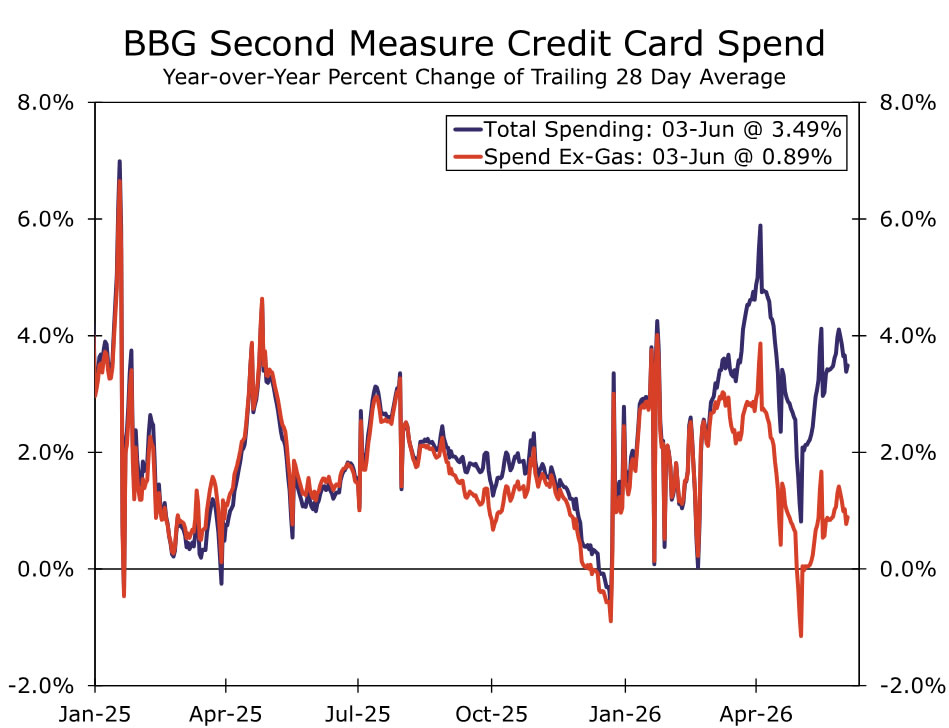

We will get a read on how consumer resilience is holding up in Q2 when the May retail sales report drops Wednesday morning. In April, nominal sales were boosted entirely by higher goods prices—particularly gasoline—while real retail sales slipped about 0.3%. There is little reason to expect a materially different story in May. Motor fuel prices rose another 6.8%, and high-frequency card data point to limited momentum outside of gas stations.

Control group sales (ex-gas, autos, building materials and restaurants) remained modestly positive in real terms, suggesting underlying spending has not rolled over. But the composition continues to do the heavy lifting—higher energy costs are increasingly taking first claim on the consumer wallet.

The upshot: spending is holding up for now, but the longer elevated energy prices persist alongside softer income growth, the greater the risk to broader demand. Next week’s report should show goods PCE started Q2 on a decent, but unspectacular, footing.

G10 Week Ahead

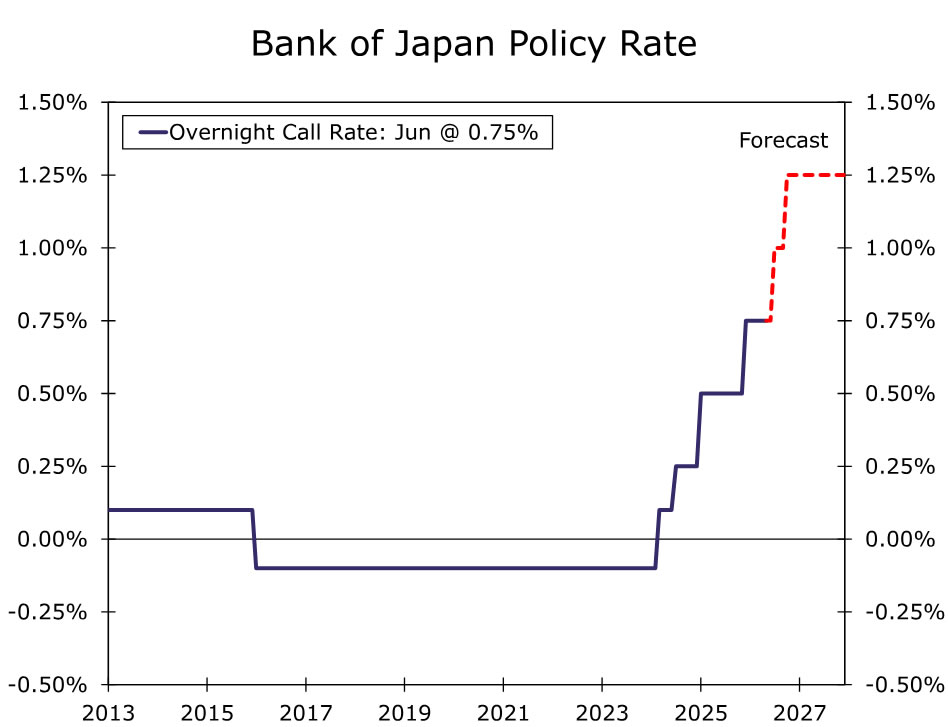

Bank of Japan • Tuesday

The Bank of Japan (BoJ) looks set to hike rates next week, with markets pricing a 97% probability of a 25 bps move to 1.00%. While the meeting is clearly “live” in our view, we see a non-trivial risk that the BoJ opts to hold. Easing geopolitical tensions around a potential US–Iran deal, alongside Governor Ueda’s recent hospitalization, could tilt the balance toward preserving optionality. That said, a near-term hike remains our base case. Abstracting from the highly uncertain outlook for commodity prices and global supply chains, which remain tightly linked to developments in the Middle East, domestic inflation dynamics are firming. Wage gains and fiscal support are set to push inflation higher with core-core measures (ex- food, energy and institutional factors) already at 2.8% year-over-year.

Whether the move comes in June or July, we expect the policy rate to reach 1.00% by end-Q3. Beyond that, we continue to see further tightening through year-end, taking rates to 1.25%, with additional hikes likely in 2027. Even then, policy would remain at the lower end of our estimated 1.0–2.5% neutral range. In the near term, we expect limited FX impact from a BoJ hike, with global drivers, particularly energy prices and Fed policy, continuing to dominate. However, this dynamic should shift over the medium-term. As the BoJ’s tightening cycle progresses and the global backdrop becomes more supportive, we see scope for a meaningful correction in the yen’s pronounced real trade-weighted undervaluation.

Reserve Bank of Australia • Tuesday

Reserve Bank of Australia (RBA) policymakers meet next week, and we expect them to keep the Cash Rate on hold at 4.35%. A hold would not necessarily signal the end of the tightening cycle. After three rate hikes this year, which addressed inflation pressures that were already elevated before the Middle East conflict, the RBA has room to wait for more evidence on monetary policy transmission.

April headline inflation eased to 4.2% year-over-year, helped by the government’s temporary fuel excise reduction. Still, automotive fuel prices were 23.5% above February levels, before the impact of the Middle East conflict, and the fuel relief measures are set to expire at the end of June. Underlying price pressures also remained firm, with trimmed mean inflation at 3.4% year-over-year. Wage risks have also moved back into focus. As part of the Annual Wage Review, the Fair Work Commission approved increases in modern award minimum wages and the National Minimum Wage, effective July 1. Although the increase was contained to some degree, it could still keep labor costs elevated and add to inflation persistence.

As such, we still see room for another rate hike in August, when policymakers should have more clarity on the economy, the Middle East conflict and the extent of pass-through to prices. That would bring the Cash Rate to a terminal rate of 4.60%, though risks are tilted to the downside if growth weakens sharply or pass-through remains contained.

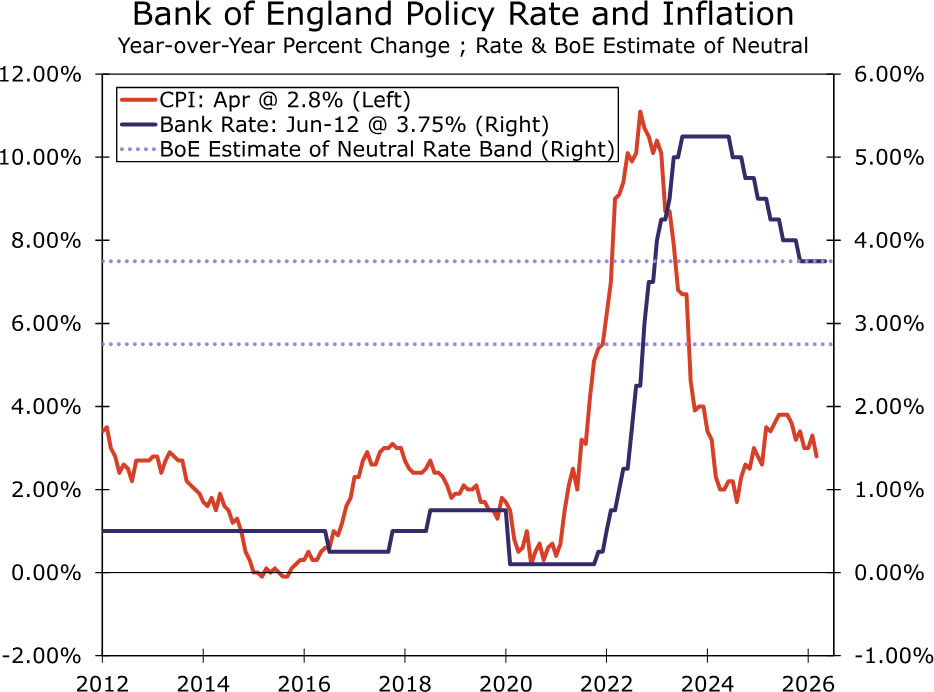

Bank of England • Thursday

When Bank of England (BoE) policymakers meet next week, we expect them to leave Bank Rate on hold at 3.75%. The economy was subdued before the Middle East conflict, and policymakers had been expected to cut rates this year to support growth. That should keep the BoE cautious next week, even as some members may lean more hawkish and emphasize that they remain “ready to act.”

Recent data have been mixed enough to justify a hold for now. Q1 GDP surprised to the upside at 0.6% quarter-over-quarter, but much of that strength reflected pre-conflict conditions. April GDP then fell 0.1% month-over-month, which suggests momentum may already be softening. While April inflation remained contained at 2.8% year-over-year, higher energy prices should start to reverse the disinflation trend in the coming months. The BoE’s Inflation Attitudes Survey also showed a sharp rise in year-ahead household inflation expectations to 4.0%. At the same time, the labor market has weakened, with unemployment at 5.0% and forward-looking surveys pointing to softer labor demand.

As such, while we expect the BoE to stay on hold next week, we still see scope for tightening in H2 as second-round effects become more visible. We look for an initial 25 bps rate hike in Q3, potentially in July alongside the updated Monetary Policy Report, followed by another hike in Q4. That would bring Bank Rate to a terminal rate of 4.25%. Risks are tilted toward a more limited tightening cycle if growth weakens more sharply or the labor market loosens faster than expected.

EM Week Ahead

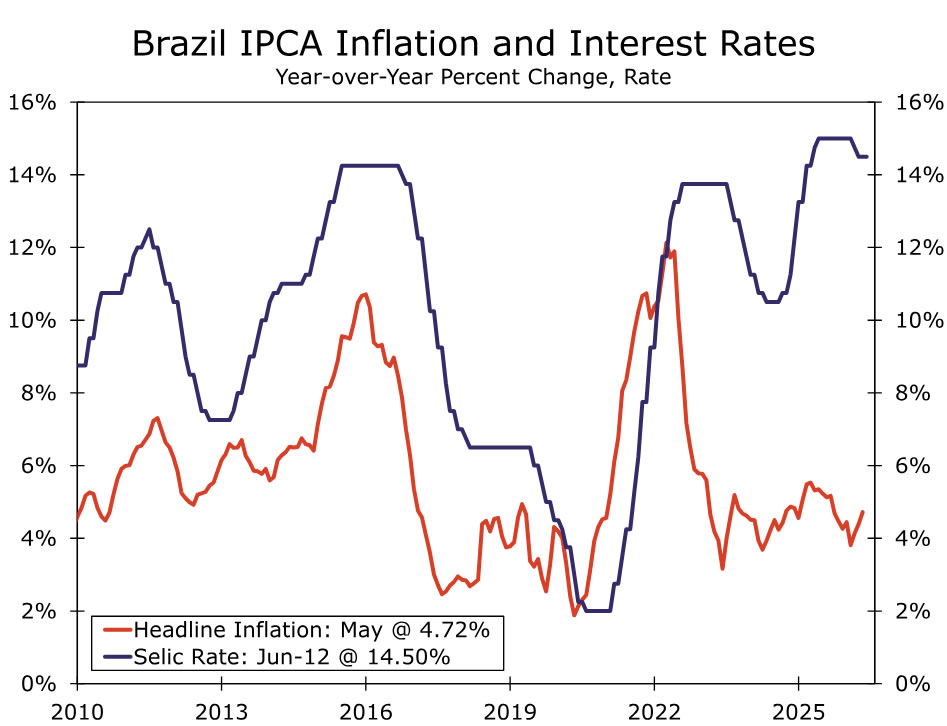

Brazilian Central Bank • Wednesday

We expect the Banco Central do Brasil (BCB) to cut rates by 25 bps next week to 14.25%. Economic activity and domestic consumption have remained resilient despite high real interest rates, supported by directed credit programs, a strong labor market, rising real minimum wages and higher household incomes following tax reform. Inflation has picked up, rising to 4.72% in May, above the BCB’s 1.5–4.5% target range, while 12-month ahead inflation expectations remain stubbornly above 4%. The external backdrop of higher commodity prices is likely to be both inflationary and growth-supportive for Brazil, reflecting its net export position in energy, food and agricultural products.

On the political front, Lula continues to lead in the polls ahead of the October elections, with pre-election policy easing to address cost-of-living pressures posing upside risks to inflation. These dynamics are evident in inflation breakevens, which are at or above 6% across the curve from 1-year through 10-year tenors. Taken together, elevated inflation, political uncertainty and fiscal risks argue for a cautious approach beyond the June meeting. We expect the BCB to pause after this cut, with easing resuming in Q4. While our base case still incorporates further rate cuts in 2027, the market-implied policy path is likely to remain highly sensitive to both domestic developments and shifts in the global backdrop over the coming months.

{kind=link}