Markets are finally getting the outcome they have been hoping for. After months of conflict, Washington and Tehran announced a peace agreement that would bring an immediate end to hostilities, setting the stage for the reopening of the Strait of Hormuz and the gradual restoration of normal oil flows. Investors wasted little time responding. The war premium that has dominated markets for much of the past few months is being unwound at remarkable speed.

The reaction was immediate and dramatic. Brent crude gapped lower at the weekly open and plunged below USD 83 as traders priced in a future of fewer supply disruptions and lower energy costs. Equities surged globally, led by a 5% jump in Japan’s Nikkei to a record high. European markets rallied broadly and US futures pointed to strong gains on Wall Street. Even before the agreement receives its formal signature in Switzerland on Friday, investors are already treating peace as the base-case scenario.

Currency markets are sending a similar message. The Dollar is the weakest major currency of the day as defensive positioning is unwound. The Swiss Franc and Euro are leading gains, while the Australian Dollar is benefiting from improving risk sentiment. At the other end of the spectrum, the Yen is under pressure as investors rotate away from safety, while the Canadian Dollar is struggling with the sharp decline in oil prices. The focus has shifted from geopolitical risk to economic normalization.

That shift, however, may only last a few hours. As the Middle East story fades, a wave of central bank meetings is about to take center stage. The Federal Reserve remains the undisputed main event on Wednesday, but the policy cycle begins in Asia with decisions from the Bank of Japan and Reserve Bank of Australia.

The BoJ is expected to deliver a widely anticipated 25 basis point rate hike to 1.00%. Yet the decision itself may matter less than what comes next. With Governor Kazuo Ueda hospitalized, Deputy Governor Shinichi Uchida will front the press conference, and markets are unlikely to receive much clarity on future tightening. Economists broadly expect rates to reach 1.25% later this year and 1.50% next year, but confirmation of that path may have to wait until July’s updated forecasts.

The RBA faces a different challenge. After three consecutive rate increases, policymakers are expected to pause at 4.35% and assess whether enough has already been done. The debate inside the market is far from settled. One camp believes slowing economic activity will eventually bring inflation under control without further action. Another points to persistent inflation pressures and increasingly hawkish rhetoric from RBA officials as evidence that additional tightening may still be required. The split is visible in economist forecasts, with nearly half of those surveyed by Reuters expecting rates to move higher again before the year is out.

For now, investors are enjoying the peace dividend. But the next chapter for markets may be written in Tokyo, Sydney and ultimately Washington, where central banks must decide whether the inflation shock left behind by the conflict is truly beginning to fade.

Gold’s Bullish Reversal Takes Shape After US-Iran Breakthrough, 4366 Key Test Ahead

Gold has a breakout level. Now it has a catalyst too. After surging above 4,300 on the back of a landmark US-Iran agreement, bullion is approaching key resistance at 4,366. A decisive break could confirm that the fall from 4,889 has ended and shift focus back toward the highs. Read More.

Will the Fed Blink? Markets Enter High-Stakes Week of Global Rate Decisions

The war story may be fading, but the inflation story is just beginning. Five major central banks meet this week, yet the real focus is whether the Fed starts preparing markets for a world with future hikes. Kevin Warsh’s first press conference as Fed Chair could set the tone for currencies, yields and equities for months ahead. Read More.

ECB’s Lagarde Sees Broader Inflation Effects Despite Iran Peace Progress

Peace may be approaching, but inflation is proving harder to defeat. ECB President Christine Lagarde welcomed the Washington-Tehran agreement while warning that energy-driven inflation is increasingly spreading across the Eurozone economy. Read More.

Eurozone Industrial Production Edges Up 0.1%, Capital Goods Weaken

Eurozone factories are still growing, but not all parts of the economy are moving together. Consumer goods production strengthened in April, yet weakness in capital goods and energy output left overall industrial growth below expectations. The split may offer an important clue about the region’s economic recovery. Read More.

EU and Eurozone Trade Balances Slip Into Deficit Amid Strong Import Growth

Europe’s trade problem isn’t exports. It’s imports. Eurozone exports grew a healthy 5.0% in April, but imports rose even faster at 9.3%, pushing the region from a sizeable surplus into deficit. The shift offers a different perspective on the strength of domestic demand. Read More.

New Zealand BNZ PSI Falls to 47.5 as Weak Consumer Spending Deepens Services Slump

New Zealand’s services sector is still struggling to regain momentum. The BNZ PSI fell further into contraction territory in May as activity, sales and new orders weakened. Businesses continue to report soft consumer demand and rising costs, suggesting the country’s largest sector is yet to benefit from the broader recovery narrative. Read More.

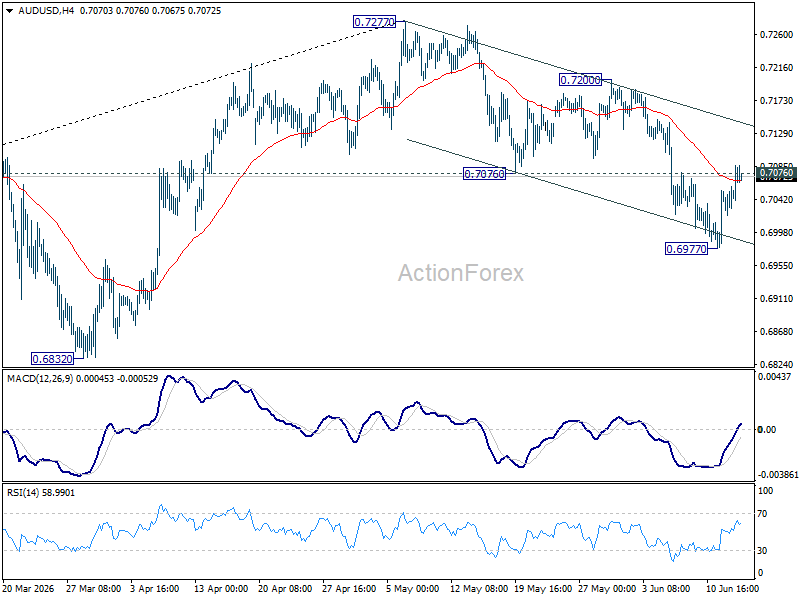

AUD/USD Daily Report

AUD/USD’s break of 0.7076 support turned resistance argues that fall from 0.7277 might have completed as as three wave correction at 0.6977. Intraday bias is back on the upside for 0.7200 resistance. On the downside, though, break of 0.6977 will resume the fall towards 0.6832 support.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206). Deeper fall could be seen to 38.2% retracement of 5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.

{kind=link}