Dollar trades broadly higher today as talks of trade war heat up again. It’s reported that Trump is considering to impose 25% tariffs on USD 200B in Chinese goods, instead of 10%. The greenback is followed by Canadian Dollar and then Yen. Meanwhile, New Zealand Dollar, Australian Dollar and Swiss Franc are among the weakest for today.

For the week, though, Yen is trading as the weakest one after BoJ sent a loud and clear message that there will be no early stimulus exit. 10 year JGB yield is back at 0.11% at the time of writing, after dropping to as low as 0.045% yesterday. But Yen is apparently indifferent to the rebound in JGB yield. Canadian Dollar is the strongest one as boosted by yesterday’s stronger than expected GDP release. But as yesterday’s volatility showed, the Loonie will be sensitive to any NAFTA news, in both direction.

Technically, Dollar seems to be coming back to live ahead of FOMC rate decision. But more is needed to indicate that it’s finally breaking out of recent correction. The key levels are 1.3070 in GBP/USD, 0.9977 in USD/CHF, 1.1574 in EUR/USD and 0.7309 in AUD/USD.

Trump said to consider slapping 25% tariffs on USD 200B of Chinese imports

Just hours after report that US and China are seeking to re-engage in trade negotiations, there were reports that Trump is planning to slap 25% tariffs on USD 200B in Chinese imports, instead of 10%. The product list could include food, chemicals, steel and aluminum, consumer goods etc. The announcement could be made as soon as on Wednesday, that is today.

Trump defended his try policies in a rally speech in Tampa. And he put the blame on other countries again and said “China and others have targeted our farmers. Not good. Not nice. And you know what our farmers are saying? ‘It’s OK. We can take it.” He also tried to equate the support to his policy to patriotism, in typical authoritarian government way, by hailing the farmers as “true patriots”.

Market reactions to the news were relatively muted though. USD/CNH (offshore Yuan) dipped to as low as 6.770 on news of possible restart in trade talks. But that it’s back above 6.8 on the news of the possible 25% tariffs. It’s clear what is driving the Yuan exchange rate.

UK NIESR urges BoE to stand ready to move in either direction should circumstances change

The UK National Institute of Economic and Social Research release an article “Prospects for the UK Economy” yesterday. It warned that the economy is “facing an unusual level of uncertainty because of Brexit”. Such “uncertainty primarily stems from the yet to be defined relationship between the UK and the EU”, as well as “the economy’s response to the new framework once it emerges.” And it criticized Prime Minister Theresa May’s Brexit white paper for failing to “unite the government or Parliament”, thus ” leaving open an entire spectrum of possible outcomes.”

The NIESR conditioned its economic forecast with a 25bps BoE rate hike this month, that is, tomorrow. That’s also under the assumption of a “soft Brexit”. The economic is expected to grow at potential with GDP up 1.4% this year, and 1.7% next year. But “risks to our GDP growth forecast are wider than before and tilted to the downside.”

NIESR also urged BoE to take account of the uncertainty of Brexit when setting policy and “also weigh the consequences of ‘getting it wrong’.” That is, It urged BoE to “stand ready to move in either direction should circumstances change.” BoE should “emphasise the uncertainty (rather than the certainty) of its future policy stance in its communications and its willingness to reverse its decisions.”

Japan PMI manufacturing finalized at 52.3, export sales stalled for second month

Japan PMI manufacturing was finalized at 52.3, revised up from 51.6. But the reading was still the lowest in 11 months. Joe Hayes, Economist at IHS Markit noted in the release that “latest survey data signalled a slowdown to manufacturing sector growth at the beginning of Q3. Output growth eased and there was a noticeable softening of demand, while export sales failed to record any upswing for a second month running.” “Input price inflation accelerated to an 88-month high, resulting in the strongest rate of increase in selling charges for almost a decade”. But the rise was “primarily cost-pus”. Hence, “further weakness in total new business growth could skew the inflationary outlook to the downside.”

China Caixin PMI manufacturing dropped to 50.8, export market continued to deteriorate

China Caixin PMI manufacturing dropped -0.2 to 50.8 in July, down from 51.0, slightly below expectation of 50.9. It’s also the lowest since November 2017. The key points in the release are slower increase in output and new orders, fastest decline in new export sales for over two years and solid rise in input costs. Looking at the details, new export orders shrunk at the fastest pace since June 2016, indicating the export market continued to deteriorate. Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group, said in the release that “in general, the survey signaled a weakening manufacturing trend as a grim export market dragged on the sector’s performance. The positive drivers were the increase in stocks of purchases and easing pressure on capital turnover.”

New Zealand employment grew 0.5%, unemployment rate edged higher to 4.5%

New Zealand employment grew 0.5% qoq in Q2, down from prior quarter’s 0.6% qoq, but beat expectation of 0.4% qoq. Unemployment rate rose 0.1% to 4.5%, above expectation of 4.4%. Participation rate rose 0.1% to 70.9%. All sector wage inflation rose 0.5%. From Australia, AiG performance of manufacturing index dropped notable 52 in July, down from 57.4.

FOMC to stand pat today, manufacturing data watched

FOMC rate decision is a major focus today and Fed is widely expected to keep federal funds rate unchanged at 1.75-2.00%. No press conference nor economic projections would follow the announcement. The accompanying statement and minutes to be released later would be the primary too for Fed’s communications and expectations setting. After all, we expect the rate hike path would remain unchanged from the one lain down in June (100 bps increases in both 2018 and 2019). The debate on the change in the “forward guidance” which had been indicating that “the stance of monetary policy remains accommodative” would continue this month with actual change could come later in the year. More in Fed Prepares for Rate Hike in September.

Also on Fed:

- Fed to Hold Rates But Will Trump Criticism Restrain a More hawkish Message?

- Is the FOMC Overly-Optimistic?

- FOMC Preview: Fed on Holiday

Manufacturing data will be the focus other than Fed today. Eurozone will release PMI manufacturing final. UK will release PMI manufacturing. Canada will release PMI manufacturing. US will release ISM manufacturing, construction spending and ADP employment.

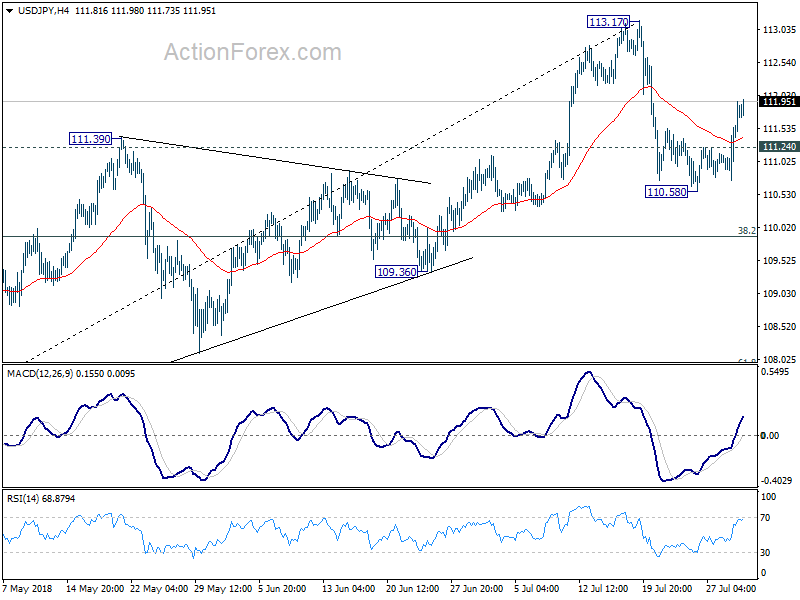

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.11; (P) 111.53; (R1) 112.30; More…

USD/JPY’s rebound from 110.58 is still in progress and intraday bias remains on the upside for retesting 113.17 resistance first. Break there will resume larger rally from 104.62 for 114.73 key resistance next. On the downside, below 111.24 minor support might extend the corrective fall from 113.17 with another decline. But downside should be contained by 38.2% retracement of 104.62 to 113.17 at 109.90 to bring rebound.

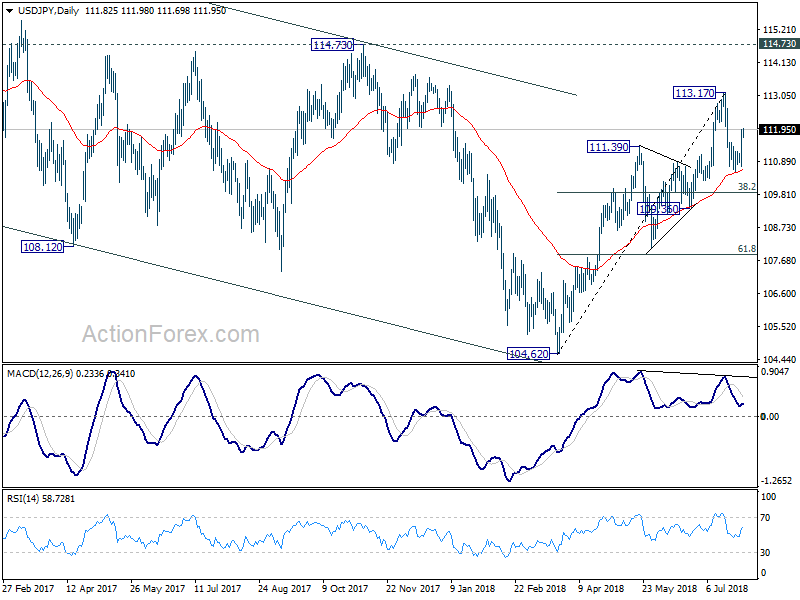

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.36 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Jul | 52 | 57.4 | ||

| 22:45 | NZD | Unemployment Rate Q2 | 4.50% | 4.40% | 4.40% | |

| 22:45 | NZD | Employment Change Q/Q Q2 | 0.50% | 0.40% | 0.60% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Jul | -0.30% | -0.50% | ||

| 0:30 | JPY | PMI Manufacturing Jul F | 52.3 | 51.6 | 51.6 | |

| 1:45 | CNY | Caixin China PMI Mfg Jul | 50.8 | 50.9 | 51 | |

| 6:30 | AUD | RBA Commodity Index SDR Y/Y Jul | 6.60% | |||

| 7:45 | EUR | Italy Manufacturing PMI Jul | 53 | 53.3 | ||

| 7:50 | EUR | France Manufacturing PMI Jul F | 53.1 | 53.1 | ||

| 7:55 | EUR | Germany Manufacturing PMI Jul F | 57.3 | 57.3 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Jul F | 55.1 | 55.1 | ||

| 8:30 | GBP | PMI Manufacturing Jul | 54.2 | 54.4 | ||

| 12:15 | USD | ADP Employment Change Jul | 186K | 177K | ||

| 13:30 | CAD | Manufacturing PMI Jul | 57.1 | |||

| 13:45 | USD | US Manufacturing PMI Jul F | 55.5 | 55.5 | ||

| 14:00 | USD | Construction Spending M/M Jun | 0.30% | 0.40% | ||

| 14:00 | USD | ISM Manufacturing Jul | 59.3 | 60.2 | ||

| 14:00 | USD | ISM Employment Jul | 56 | |||

| 14:00 | USD | ISM Prices Paid Jul | 75.5 | 76.8 | ||

| 14:30 | USD | Crude Oil Inventories | -6.1M | |||

| 18:00 | USD | FOMC Rate Decision (Upper Bound) | 2.00% | 2.00% | ||

| 18:00 | USD | FOMC Rate Decision (Lower Bound) | 1.75% | 1.75% |

{kind=link}