Both Sterling and Euro trade firmer after UK Prime Minister Theresa May got Cabinet support for her Brexit deal. But no significant technical development is seen with these two currencies yet. Instead, Australian Dollar steals the show with strong employment data. Additional support to Aussie was given by news that China has already sent response to US demand regarding trade, even though there’s no detail yet. On the other hand, Dollar is leading the way down as consolidation continues, followed by Swiss France and Yen.

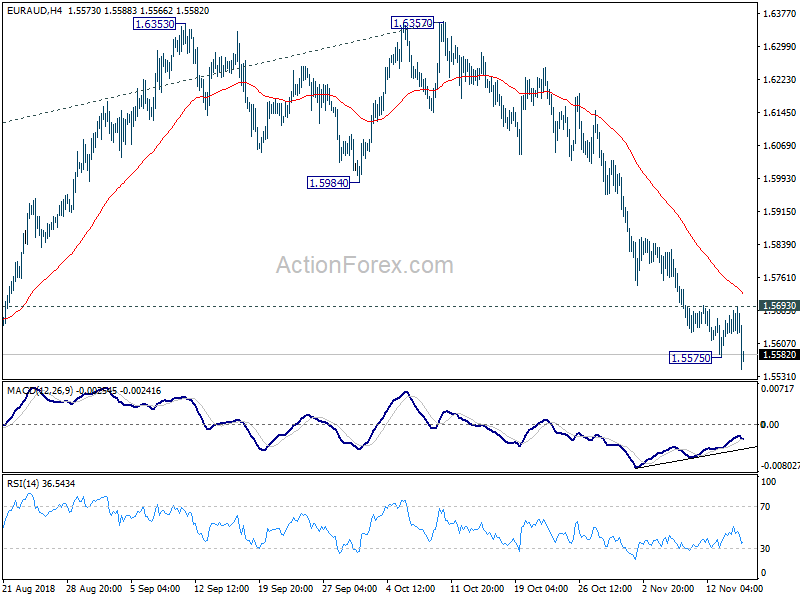

Technically, EUR/AUD takes the lead by breaking through 1.5575 temporary low today, resuming recent decline from 1.6357. AUD/USD might follow and challenge 0.7314 key structure support. Decisive break there will solidify the case of medium term bullish reversal. For Dollar-Europeans, despite this week’s pull back, near term levels are holding well. That is, 1.1499 resistance in EUR/USD and 0.9952 support in USD/CHF are intact. Hence, Dollar remains bullish against the two. However, USD/JPY is risking near term bearish reversal ahead of 114.54/73 resistance zone. And focus is back on 112.94 minor support today.

In other markets, DOW dropped notably by -0.81% to 25080.50 overnight. S&P 500 lost -0.76% and NASDAQ fell -0.90%. Treasury yields also turned weaker with 10 year yield closed down -0.025 at 3.120. That’s a major factor for Dollar’s softness this week. In Asian, Nikkei trades in opposite direction with others again today, down -0.45%. Hong Kong HSI, China Shanghai SSE and Singapore Strait Times are up 0.38%, 0.72% and 0.06% respectively. WTI crude oil’s recovery is losing some steam and is back below 56 handle.

May secured cabinet support for Brexit deal, Sterling reactions volatile yet muted

After some last minute dramas, UK Prime Minister Theresa May finally secured the backing from her Cabinet, on the Brexit draft agreement. As a more positive sign, there is no resignation of ministers so far. May said after a five-hour marathon meeting that “the collective decision of cabinet was that the government should agree the draft withdrawal agreement and the outline political declaration.” She added, “when you strip away the detail, the choice before us was clear: this deal, which delivers on the vote of the referendum, which brings back control of our money laws and borders, ends free movement, protects jobs security and our Union; or leave with no deal; or no Brexit at all.”

EU chief Brexit negotiator Michel Barnier hailed the UK for making a “decisive, crucial step” towards orderly Brexit. Referring to the draft, he said “this is a precise, detailed document… which provides legal certainty for everyone and on all the issues where we have to deal with the consequences of Brexit.” While it ” may be hard to guarantee an orderly withdrawal”, he pledged that UK will remain “our friend, our partner, and our ally.” Barnier had also passed his recommendation to EU27 leaders that “decisive progress” had been made for an extra EU summit, probably on November 25, to sign off.

EU’s statement here, with link to the withdrawal agreement.

More on the deal: Brexit Update – EU and UK Agree on Draft Deal, Still More Challenge Ahead

EU Malmstromg: Scope of trade negotiation with US cannot be defined until early 2019

EU Trade Commissioner Cecilia Malmstrom met US Trade Representative Robert Lighthizer yesterday. Malmstrom said the meeting focused on regulatory cooperations issues, plus ways for EU to import more soybeans and LNG from the US. She also told Lighthizer the EU’s willingness to negotiation a trade deal, but that would be limited to industrial goods, excluding agriculture. However, Malmstrom noted that the scope of the talks cannot be defined until early 2019. USTR will have to complete its consultation with Congress. EU will also need to receive negotiating mandate from member states.

On US auto tariff threats, Malmstrom said EU already has a list of retaliation targets ready. She said “it could be cars, it could be agriculture, it could be industrial products – it could be everything. And we will do that, but hope we don’t have to get to that situation.”

Fed Powell: From now on, Fed can and will move at any meeting

Fed Chair Jerome Powell had an hour long exchange with Dallas Fed President Robert Kaplan, titled “Global Perspectives with Jerome H. Powell“. Powell reiterated his upbeat comments on the US economy. He said “I’m very happy about the state of the economy now”. He also hailed the Fed collectively and said “our policy is part of the reason why our economy is in such a good place right now.”

A key take away is his comments regarding the arrangement of having press conference after all eight FOMC meetings during the year, starting next. He said “certainly all meetings are live now, there’s no question about it now.” And he added, “over time, folks will get used to the idea that we can and will move at any meeting.”

On interest rates, Powell acknowledged the need to thing about “how much further to raise rates and the pace at which we will raise rates.” And, “the way we will be approaching that is to be looking really carefully at how the markets and the economy and business contacts will be reacting to our policy.” He emphasized that “our goals will be to extend the recovery … and to keep unemployment low and inflation low. So that’s how we’re going to think about it.”

On headwinds, Powell noted slowing growth abroad, waning effect of the administration’s tax cuts and spending increases are some that the economy might face. Also, he noted that there are a lot of factors weighing on home building too.

Australia employment jumped 32.8k, with strong growth in full-time jobs

Australia employment rose 32.8k in October, much better than expectation of 20.3k. Full-time employment jumped 42.3k to 8.70M. Part-time jobs dropped -9.5k to 3.97M. Unemployment rate was unchanged at 5.0%, below expectation of 5.1%. Participation rate rose 0.1% to 65.6%. Monthly worked hours in all jobs also rose 0.3%. Released yesterday, wages grew 2.3% in Q3, fastest annual pace in three years. The overall set of employment data released this week is pretty encouraging.

The set of data should be very welcomed by the RBA. However, they kind of just confirmed RBA’s outlook, without too much out-performance. Wage growth remains the key for lifting inflation. And there’s still much more work to do. Nevertheless, it’s a step in the right direction and affirmed that the next move is a hike rather than a cut. But, that leaves RBA with no urgency to move any time soon.

Looking ahead

UK retial sales and Eurozone trade balance are the main feature in European session. US data will take center stage later in the data. Retail sales, Empire State manufacturing, Philly Fed survey, import price index, business inventories and jobless claims will be released.

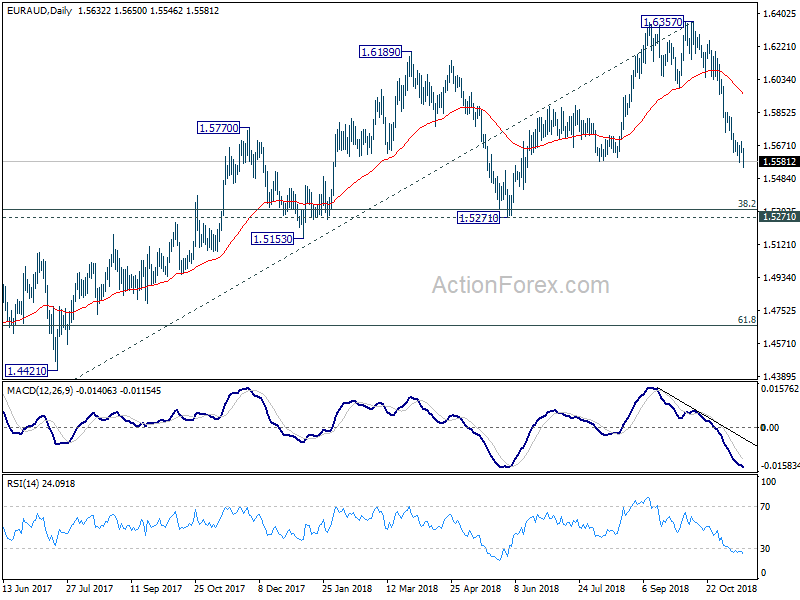

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5611; (P) 1.5653; (R1) 1.5676; More….

EUR/AUD’s decline resumed after consolidation from 1.5575 entered rather quickly, dropping to as low as 1.5546 so far. Intraday bias is back on the downside. Current fall from 1.6357 should target 1.5271/5313 cluster support zone next. On the upside, though, break of 1.5693 resistance will now indicate short term bottoming. In that case, lengthier consolidation would be seen first before staging another decline.

In the bigger picture, current development argues that up trend from 1.3624 (2017 low) is possibly completed at 1.6357, ahead of 1.6587 (2015 high). This is supported by bearish divergence condition in weekly MACD. Deeper decline is now in favor to 1.5271 cluster support (38.2% retracement of 1.3624 to 1.6357 at 1.5313). Break will target 61.8% retracement at 1.4668. On the upside, break of 1.5984 support turned resistance is now needed to revive the prior medium term up trend. Otherwise, further decline will be in favor even in case of strong interim rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectation Nov | 3.60% | 4.00% | ||

| 00:30 | AUD | Employment Change Oct | 32.8K | 20.3K | 5.6K | 7.8K |

| 00:30 | AUD | Unemployment Rate Oct | 5.00% | 5.10% | 5.00% | |

| 09:30 | GBP | Retail Sales Inc Auto Fuel M/M Oct | 0.20% | -0.80% | ||

| 09:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Oct | 2.80% | 3.00% | ||

| 09:30 | GBP | Retail Sales Ex Auto Fuel M/M Oct | 0.20% | -0.80% | ||

| 09:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Oct | 3.30% | 3.20% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 16.7B | 16.6B | ||

| 13:30 | CAD | ADP Non-Farm Employment Change Oct | 28.8K | |||

| 13:30 | USD | Empire State Manufacturing Nov | 19.3 | 21.1 | ||

| 13:30 | USD | Retail Sales Advance M/M Oct | 0.50% | 0.10% | ||

| 13:30 | USD | Retail Sales Ex Auto M/M Oct | 0.50% | -0.10% | ||

| 13:30 | USD | Philadelphia Fed Business Outlook Nov | 20.7 | 22.2 | ||

| 13:30 | USD | Import Price Index M/M Oct | 0.10% | 0.50% | ||

| 13:30 | USD | Initial Jobless Claims (NOV 13) | 213K | 214K | ||

| 15:00 | USD | Business Inventories Sep | 0.30% | 0.50% | ||

| 15:30 | USD | Natural Gas Storage | 35B | 65B | ||

| 16:00 | USD | Crude Oil Inventories | 2.9M | 5.8M |

{kind=link}