Selloff in New Zealand and Australian Dollar is the main theme in Asian session today. Kiwi plummets after RBNZ stands pat and indicates that the next move is a cut. After that, a full RBZN cut in priced in November but there are speculations on as early as a May cut. At the same time, RBNZ’s dovish seems to be adding to the case for RBA to cut twice this year too. For now, more downside are expected in both currencies for the near term.

Meanwhile, Yen and Dollar are the strongest ones, followed by Euro. The greenback is partly helped by weakness in other major currencies, and rebound in stocks overnight. But upside of Dollar is capped by yield curve inversion so far. 10-year yield dropped for another day to 2.414 overnight and 2.4 handle now looks vulnerable. Inversion with 3-month yield (now at 2.464) will only get worse before getting better.

Technically, EUR/USD’s fall from 1.1448 resumed by breaking 1.1273 temporary low and it should be heading to 1.1176 key support level. EUR/CHF also resumed fall from 1.1444 but it’s trying to draw support from key support zone at 1.1154/98. Sterling will be a key so focus today and Brexit alternative votes loom in Commons. It’s so far stuck in range against Dollar, Euro and Yen. 0.8474 support in EUR/GBP is the level to watch for Sterling strength. 1.2960 in GBP/USD and 143.72 in GBP/JPY are the levels to watch for Sterling weakness.

In Asia, Nikkei closed down -0.23%. Hong Kong HSI is up 0.62%. China Shanghai SSE is up 0.59%, back above 3000 handle. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is down -0.027 at -0.068. Overnight in US, DOW rose 0.55%. S&P 500 rose 0.72%. NASDAQ rose 0.71%. 10-year yield dropped -0.006 to 2.414.

NZD dives as RBNZ turns dovish, next move is rate cut

New Zealand Dollar dives sharply after RBNZ kept OCR unchanged at 1.75% and shifted to a clear dovish stance. It now expected that “the more likely direction of our next OCR move is down”.

In the statement, it also noted that balance of risks to the outlook has “shifted to the downside”. At the same time, risk of a “more pronounced global downturn has increased”, and ‘low business sentiment continues to weigh on domestic spending.” Though, on the upside, “inflation could rise faster if firms pass on cost increases to prices to a greater extent.”

Markets are raising bets of an RBNZ rate cut this year. A cut it full priced in for November and there speculations that it might happen as soon as in May.

More in

- RBNZ Review – Next Move would be Rate Cut as Risks…

- First impressions of the RBNZ’s March OCR Review

Fed Daly: Patient until data suggests we go one way or another

San Francisco Federal Reserve President Mary Daly said yesterday that “patience is where I’m at right now,” regarding monetary policy. She added the US economy is in “a good place”. And interest rates should be left unchanged “”until the data suggests we go one way or another way.”

Though, she predicts that unemployment rate at 3.8% will eventually push wages and prices upward. And “it’s just taking a longer time than it typically does”. She noted “that’s part of what feeds into my patient strategy.”

Daly supported Decembers rate hike when the economy was growing at a faster rate. Now, she noted interest rates are at “neutral” and thus, patience is “the way to go, because you don’t want to guess that you need to do more, or guess that we need to do less, you just want to be patient and look at the data.”

China industrial profits dropped -14%. Autos, oil processing, steel and chemicals dragged

China’s industrial profits in January-February period slumped -14.0% yoy to CNY 708B. It’s the biggest contraction since 2011. National Bureau of Statistics (NBS) said the contract was mainly due to distortions caused by the timing of Lunar New Year.

Meanwhile, there were notable declines in profits in auto, oil processing, steel and chemical industries. Ex-factory prices of Auto, oil processing, steel and chemicals dropped -0.4%, -1.3%, -2.5% and -2.3% respectively. Profits dropped CNY 37B, CNY 32B, CNY, 29B and CNY 19B respectively. Combined the contributed to -14.2% contraction in profits. Excluding them, industrial profits rose 0.2%.

While the set of data is largely ignored by the stock markets, it’s putting some more weight to the upcoming round of trade talks. US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin will visit Beijing on March 28-29. Even though an eventual trade might might not help reverse the slowdown in China, at least, the drag on exports will likely be eased.

Looking ahead

The economic calendar is not too busy today. ECB President Mario Draghi’s speech will catch some attention. UK will release CBI realized sales. Canada will release trade balance. US will release trade balance and current account.

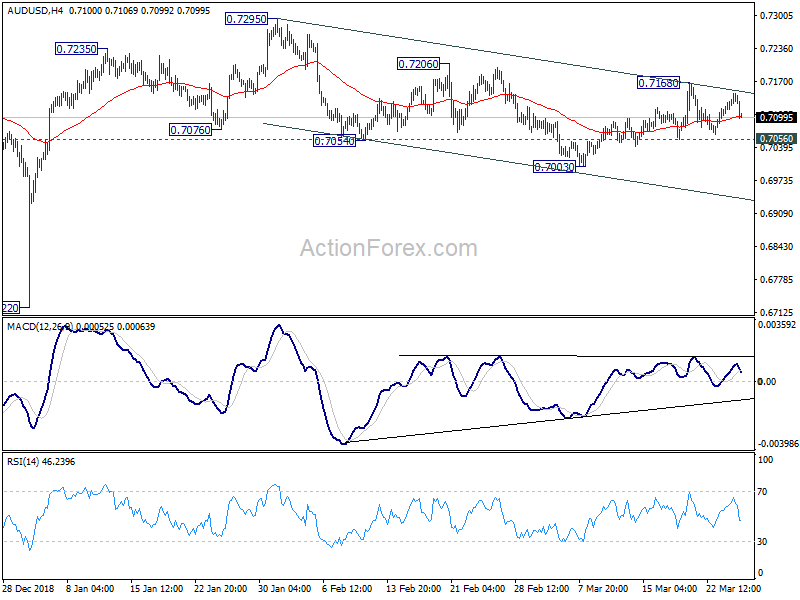

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7111; (P) 0.7130; (R1) 0.7152; More…

AUD/USD’s rebound was limited below 0.7168 resistance and drops sharply today. But it’s staying above 0.7056 minor support so far. Intraday bias remains neutral at this point. On the downside, break of 0.7056 minor support will turn bias to the downside for 0.7003 first. Break will resume the whole decline from 0.7295. On the upside above 0.7168 will resume the rebound from 0.7003 towards 0.7295 high instead.

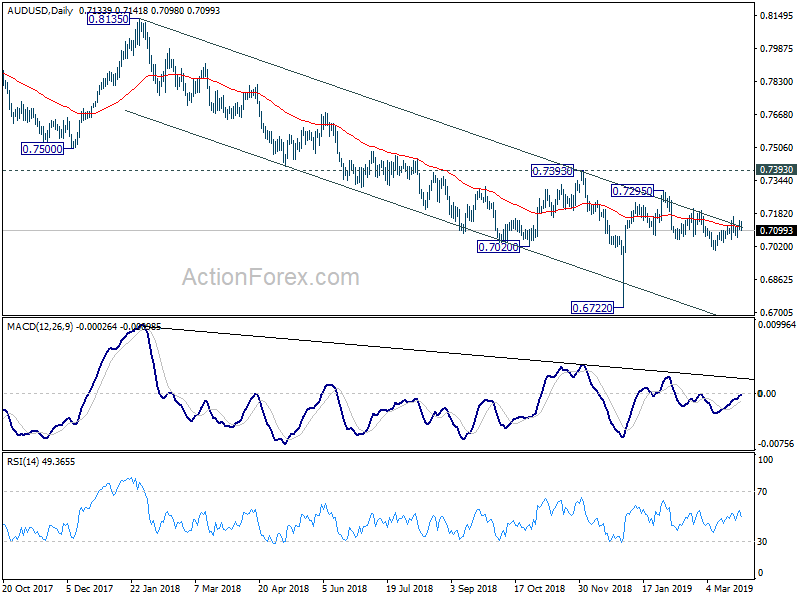

In the bigger picture, as long as 0.7393 resistance holds, we’d treat fall from 0.8135 as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | NZD | RBNZ Official Cash Rate | 1.75% | 1.75% | 1.75% | |

| 11:00 | GBP | CBI Reported Sales Mar | 5 | 0 | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Jan | -2.3B | -4.6B | ||

| 12:30 | USD | Trade Balance (USD) Jan | -57.5B | -59.8B | ||

| 14:00 | USD | Current Account Balance (USD) Q4 | -130B | -125B | ||

| 14:30 | USD | Crude Oil Inventories | -9.6M |

{kind=link}