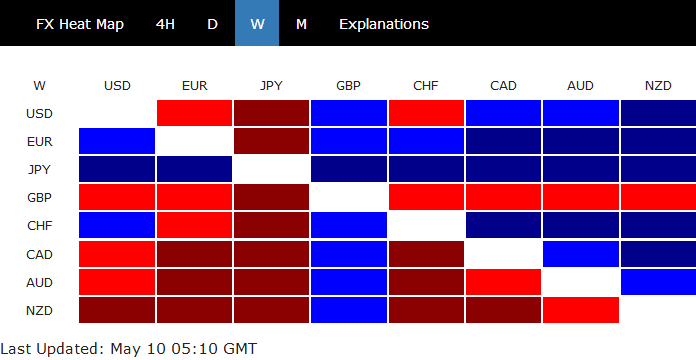

The financial markets are relatively steady today as new round of US-China trade war formally starts. Asian index are just mixed, with gains even seen in Hong Kong and Chinese stocks. In the currency markets, Dollar is currently trading as the weakest for today, followed by Sterling, and New Zealand Dollar. Australian Dollar was given a mild lift by RBA’s Statement of Monetary Policy but the recovery quickly fades. After all, major pairs and crosses are bounded inside Friday’s range and the picture could drastically change before weekly close.

For the week, Yen remains the strongest one on risk aversion. Euro displays a lot of resilience as the second strongest, followed by Swiss Franc on risk aversion. Sterling is the worst performing one on Brexit impasse. But it could have a turn around should GDP and productions surprise on the upside today. New Zealand and Australian Dollars are the weakest.

Technically, Yen is losing some upside momentum against Dollar, Euro and Sterling. Some retreats will be likely but for now, we’ll assume any pull back to be brief first. AUD/USD recovered ahead of 0.6962, with no follow through buying. This support will remain in focus today and break will resume larger fall from 0.7295. EUR/USD, USD/CHF and USD/CAD remain in tight range despite yesterday’s selloff in Dollar. For now, we’d still favor upside breakout in the greenback.

In Asia, currently, Nikkei is down -0.91%. Hong Kong HSI is up 0.17%. China Shanghai SSE is up 0.47%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is down -0.001 at -0.047. Overnight, DOW closed down only -0.54% at 25828.36 after diving to as low as 25517.39. S&P 500 lost -0.30%. NASDAQ dropped -0.41%. 10-year yield dropped -0.025 to 2.457, after diving to 2.425.

It’s formal, new US tariffs on China take effect

It’s formal. The new US tariffs on Chinese imports take effect. Tariffs on USD 200B in Chinese goods are increased from 10% to 25%. Top 10 items affected include telecommunication equipment, computer circuit boards, processing units, metal furniture, computer parts, wooden furniture, static converters, vinyl tile floor coverings, seats with wooden frame and car parts. Paper work for taxing another USD 325B in Chinese goods has also started earlier this week.

In a brief statement China Ministry of Commerce said the country “deeply regrets” US decision. And, MOFCOM said China “will have to take necessary countermeasures”, without elaboration. But it “hoped that the US and the Chinese side will work together and work together to resolve existing problems through cooperation and consultation.”

Chinese VP Liu wrapped first day of negotiation with a smile as new tariffs will start shortly

Yesterday, Chinese Vice Premier Liu He wrapped his first day of meeting with US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin. After 90 minutes meeting in the USTR office, they had a dinner together. Ahead of the meeting, Liu said: “We come here this time, under pressure, which shows China’s greatest sincerity, and want to sincerely, confidently, and rationally resolve certain disagreements or differences facing China and the United States. I think there is hope,”

Trump said he got a “beautiful letter” from Chinese President Xi Jinping and they’ “probably” speak by phone. Trump reiterated his hard line and said “Our alternative is an excellent one, it’s an alternative I’ve spoken about for years. We’ve taken well over $100 billion from China in a year.”

For now, no phone call has been made yet, nor scheduled. White House just noted that the negotiations will continue on Friday morning in Washington.

BoJ opinions: Clarification on forward guidance strengthens confidence in powerful easing

Summary of opinions at the April 24-25 BoJ Monetary Policy Meeting is released today. At the statement of that meeting, BoJ added clarification of forward guidance for policy rates. It noted that BoJ intended to keet current levels of interest rates at least through around spring 2020.

The summary of opinions noted that “in order to strengthen public confidence in continuing with powerful monetary easing, it is appropriate to clarify forward guidance for policy rates, such as through making clear the specific period for which extremely low levels of interest rates will be maintained.” Also, it is appropriate to consider revising forward guidance for policy rates, given, for example, that uncertainties regarding overseas economies have heightened compared to the time of its introduction.

Meanwhile BoJ also noted “there is a possibility that a further decline in interest rates will result in a greater risk of inducing side effects on the real economy, rather than positive effects”. But BoJ dismissed the argument that QQE led to deterioration in banks’ profitability. It’s noted monetary easing has “brought about economic improvement, an increase in lending, a decline in credit costs, and an increase in profits stemming from stocks and bonds”.

RBA SoMP: Slight downgrade of inflation, no imminent need to cut rates

In the Statement of Monetary Policy, RBA noted that the economy has “slowed” and inflation “remains “low”. Also, “subdued” growth in household income and “adjustment” in housing markets affected consumer spending and residential construction. Still, labor market is “performing reasonably well”. Underlying inflation came in lower than expected in Q1 and “with pricing pressures subdued across much of the economy”.

Looking at the new economic projections, 2019 growth forecasts was revised down notably from 2.75% to 2.00%. But 2020 growth expectation was unchanged. Unemployment rate will stay longer at 5.00% through Dec 2020. Headline CPI was expected hit 2.00% in Dec 2019 and stay there throughout. Core CPI is revised slightly to 1.75% in Dec 2019 and 2.00% in Dec 2020.

All in all, while 2019 growth is expected to undershoot, it’s expected to pick up quickly. The downward revision in core CPI was just showed a slower pickup back to target, not anything disastrous. Based on this outlook, RBA still has a lot of room to wait and see the developments, before cutting interest rates.

- GDP growth year average: 2019 at 2.00%, revised down from 2.75%; 2020 at 2.75%, unchanged.

- Unemployment rate: Dec 2019 at 5%, unchanged; Dec 2020 at 5%, revised up from 4.75%.

- CPI: Dec 2019 at 2.00%, revised up from 1.75%; Dec 2020 at 2.00%, down from 2.25%.

- Trimmed mean inflation:Dec 2019 at 1.75%, revised down from 2.00%; Dec 2020 at 2.00%, revised down from 2.25%.

RBNZ Bascand: Economy growing below potential, needs to be pumped up

RBNZ Deputy Governor Geoff Bascand said the economy is growing less than potential of 2.8%. And, there’s just not enough pressure to get inflation up. “We think capacity pressures will just become a little less,” he said. “There is pressure there, there’s just not enough pressure to get inflation up. We need growth to be around 3% or more to keep being at or approaching our targets.”

Nevertheless, he added “nobody’s talking gloom here” even though it was “getting a bit harder” to meet the inflation target. He said “the headwinds have become a bit stronger, the global economy has become a bit weaker, the domestic economy seems to have softened.” Hence, “we’re going to be drifting away a little bit, not staying as close, there’s more chance of inflation ebbing than rising”.

And, “because of that, we ended up coming to a view that we needed to help pump it up a bit more.”

On the data front

Japan household spending rose 2.1% yoy in March, above expectation of 1.6% yoy. But labor cash earnings dropped sharply by -1.9% yoy, well below expectation of -0.50%.

UK data will be the major focus in European session today. GDP, productions, trade balance will be featured. Germany will also release trade balance.

Later in the data, US CPI and Canada employment will take center stage.

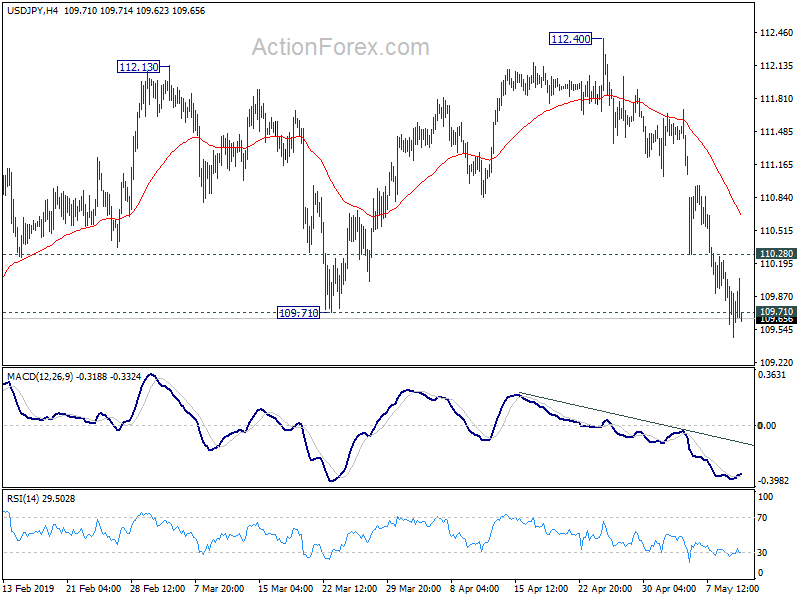

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.45; (P) 109.78; (R1) 110.10; More…

USD/JPY is losing some downside momentum, as seen is 4 hour MACD, as it’s pressing 109.72 key support. Intraday bias stays on the downside as long as 110.28 minor resistance holds. Sustained break of 109.72 key support will confirm completion of rebound from 104.69 at 112.40 on bearish divergence condition in daily MACD. Deeper decline should then be seen back to retest 104.69 low. On the upside, though, rebound from current level and break of 110.28 minor resistance will mix up near term outlook. Intraday bias will be turned neutral in this case first.

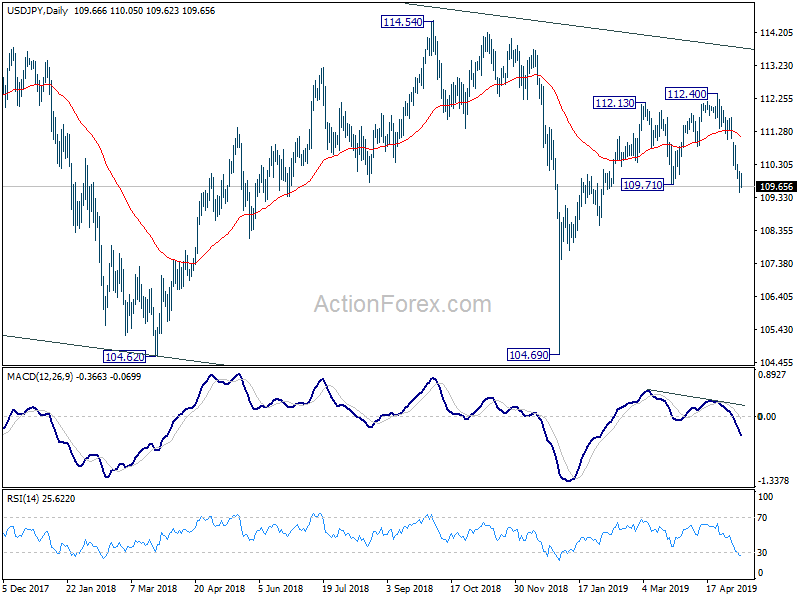

In the bigger picture, USD/JPY is staying inside falling channel from 118.65. Thus, there is no confirmation of trend reversal yet. Sustained break of 109.71 will argue that rebound from 104.69 is completed. And the down trend from 118.65 is still in progress. But at this stage, in case of break of 104.69, we’d expect strong support above 98.9 (2016 low) to contain downside an bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Mar | 2.10% | 1.60% | 1.70% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | -1.90% | -0.50% | -0.80% | -0.70% |

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 1:30 | AUD | RBA Statement on Monetary Policy May | ||||

| 6:00 | EUR | German Trade Balance (EUR) Mar | 19.4B | 18.7B | ||

| 8:30 | GBP | GDP M/M Mar | 0.00% | 0.20% | ||

| 8:30 | GBP | GDP Q/Q Q1 P | 0.50% | 0.20% | ||

| 8:30 | GBP | Total Business Investment Q/Q Q1 P | -0.70% | -0.90% | ||

| 8:30 | GBP | Industrial Production M/M Mar | 0.10% | 0.60% | ||

| 8:30 | GBP | Industrial Production Y/Y Mar | 0.40% | 0.10% | ||

| 8:30 | GBP | Manufacturing Production M/M Mar | 0.00% | 0.90% | ||

| 8:30 | GBP | Manufacturing Production Y/Y Mar | 1.10% | 0.60% | ||

| 8:30 | GBP | Construction Output M/M Mar | -0.90% | 0.40% | ||

| 8:30 | GBP | Visible Trade Balance (GBP) Mar | -13.7B | -14.1B | ||

| 8:30 | GBP | Index of Services 3M/3M Mar | 0.40% | 0.40% | ||

| 12:30 | CAD | Building Permits M/M Mar | 2.30% | -5.70% | ||

| 12:30 | CAD | Net Change in Employment Apr | 15.0K | -7.2K | ||

| 12:30 | CAD | Unemployment Rate Apr | 5.80% | 5.80% | ||

| 12:30 | USD | CPI M/M Apr | 0.40% | 0.40% | ||

| 12:30 | USD | CPI Y/Y Apr | 2.10% | 1.90% | ||

| 12:30 | USD | CPI Core M/M Apr | 0.20% | 0.10% | ||

| 12:30 | USD | CPI Core Y/Y Apr | 2.10% | 2.00% |

{kind=link}