Dollar’s rally extended overnight, following record close in S&P 500 and mild recovery in treasury yields. The greenback is retreating some gains for now. But with near term resistance against European majors broken, further rebound is now mildly in favor. Though, Dollar will still need to survives tests from ISM services and non-farm payroll later in the week.

Australian Dollar is so far the strongest one for today, despite RBA’s rate cut. The move was widely expected and without turning more dovish, traders are turning to the sideline first. On the other hand, New Zealand Dollar is the weakest one, as dragged by rebound in AUD/NZD.

Technically, with 1.1317 support in EUR/USD, 1.2642 support in GBP/USD and 0.9854 resistance in USD/CHF broken, Dollar is likely bottomed out in near term. Though, we’d still prefer to see 108.80 resistance in USD/JP, 1.3151 resistance in USD/CAD and 0.6941 support in AUD/UD taken out too to confirm.

In Asia, Nikkei rose 0.11%. China Shanghai SSE closed down -0.04%. Hong Kong HSI is up 1.29%, back from holiday. Singapore Strait Times is down -0.28%. Japan 10-year JGB yield is flat at -0.145. Overnight, DOW rose 0.44%. S&P 500 rose 0.77% to 2964.33, new record. NASDAQ rose 1.06%. 10-year yield rose 0.034 to 2.034.

RBA cuts interest rate, maintains easing bias, but doesn’t turn more dovish

Australian Dollar recovered earlier today ahead of RBA rate decision. Some knee-jerk reactions were seen after RBA announced the highly anticipated 25 bps rate cut to 1.00%. But AUD/USD quickly found its footing as the accompanying statement revealed nothing special, and doesn’t indicate a drastic dovish turn. While RBA opens the door for more rate cut ahead, upcoming developments, including new economic projections in August, would play an important part in deciding when the next cut would be delivered.

The most important part of the statement is that “the Board will continue to monitor developments in the labour market closely and adjust monetary policy if needed to support sustainable growth in the economy and the achievement of the inflation target over time”. It’s self-explanatory that RBA is open to further easing.

Globally, RBA maintained that outlook “remains reasonable”. Domestically, RBA acknowledged the below trend 1.8% growth in Q1. But it noted that “central scenario for the Australian economy remains reasonable, with growth around trend expected.” Consumption continues to be the main domestic uncertainty”.

Employment growth has “continued to be strong”. But again, ” labour market outcomes suggest that the Australian economy can sustain lower rates of unemployment and underemployment.” Inflation pressures “remain subdued”. But inflation is expected to pick up to “around 2 per cent in 2020 and a little higher after that”. On the positive side, RBA noted “some tentative signs that houses prices are “now stabilizing” in Sydney and Melbourne.

USTR proposes tariffs on additional USD 4B of EU products

Just days after agreeing to stop tariff escalation with China, US is now turning to EU. The US Trade Representative proposed tariffs on additional EU imports, as countermeasures to harm caused by EU aircraft subsidies. A “supplemental list” of 89 subheadings with approximate trade value of USD 4B was proposed. The list includes olives, Italian cheese and Scotch whiskey, etc.

That’s additional to the USD 21B in EU imports published on April 12. A hearing will be held on the proposed additional products on August 5. But US could immediately impose increased duties on the products included in the initial list, if the WTO arbitrator issues a decision before the public comment period ends.

Trump: Trade negotiations with China essentially has already begun

Trump said that trade negotiations with China “essentially has already begun”. And, negotiators were “speaking very much on phone they are also meeting”. He remained optimistic and said “I think we have a good chance of making a deal”. Though, he emphasized that China has had a “big advantage”over the US in trade for “many years”. Hence, “obviously you can’t make a 50-50 deal. It has to be a deal that is somewhat tilted to our advantage.”

China to abolish foreign ownership in finance industry in 2020, a year earlier

Chinese Premier Li Keqiang pledged, in the World Economic Forum in northeastern Chinese port city of Dalian, to further open up the finance and manufacturing industry. Li said, “We will achieve the goal of abolishing ownership limits in securities, futures, life insurance for foreign investors by 2020, a year earlier than the original schedule of 2021.”

Additionally, manufacturing sector, including auto industry, will be opened by further by reduction in negative investment list that restricts foreign investment in some areas. Besides, the government will also reduce restrictions, in 2020, on market access in value-added telecoms services and transport sectors.

Li also noted “global economic risks are rising somewhat, international investment and trade growth is slowing, protectionism is rising and unstable and uncertain factors are increasing”. And, “some countries have taken measures including cutting interest rates, or sent clear signals on quantitative easing.” But he pledged China won’t resort to competitive currency devaluation but keep the exchange rate stable at a reasonable and balanced level.

On the data front

New Zealand building permits rose 13.2% mom in May. Japan monetary base rose 4.0% yoy in June, above expectation of 3.4% yoy. German retail sales dropped -0.6% mom, versus expectation of 0.5% mom. Looking ahead, UK will release construction PMI. Eurozone will release PPI. Canada will release manufacturing PMI.

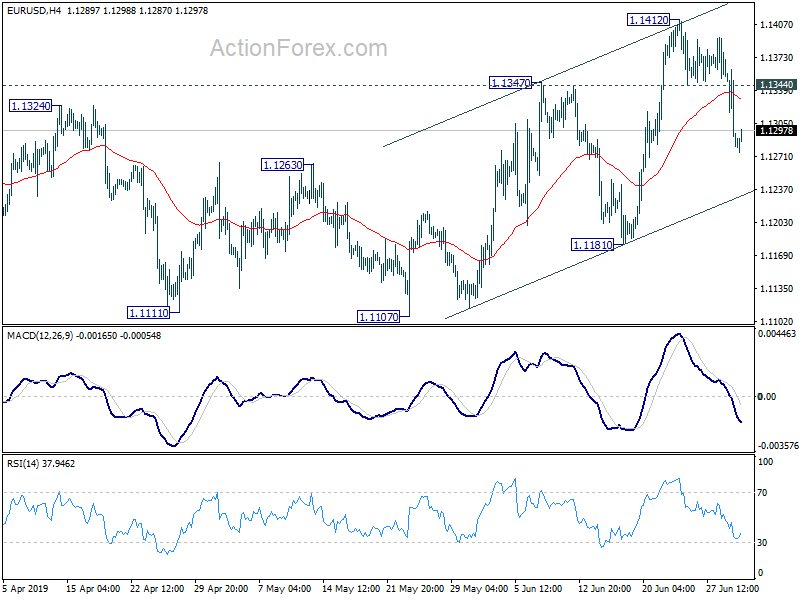

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1254; (P) 1.1312; (R1) 1.1344; More…

EUR/USD’s fall from 1.1412 extends today and broke 1.1317 minor support. Recovery from 1.1107 might have completed earlier than expected at 1.1412. Intraday bias is turned to the downside for 1.1181 support first. Break there will confirm and bring retest of 1.1107 low. Though, above 1.1344 minor resistance will turn bias back to the upside to resume the rebound from 1.1107 through 1.1412 instead.

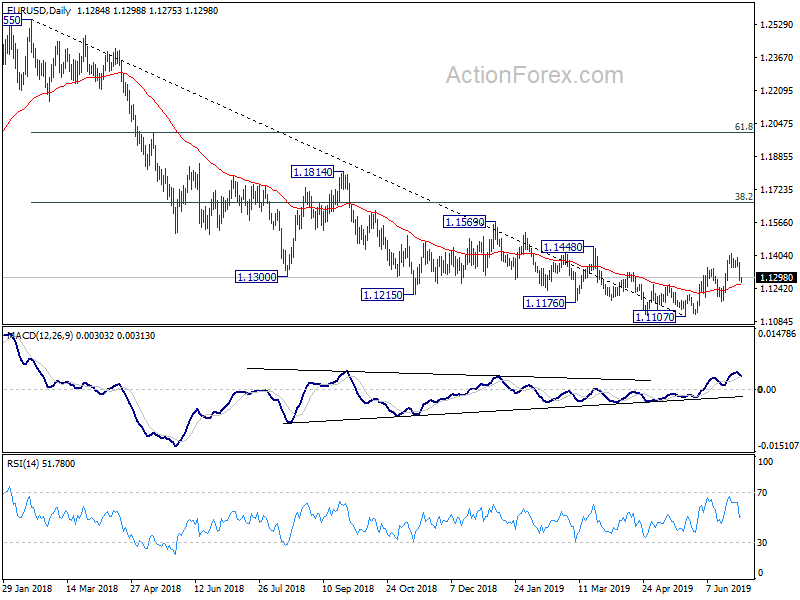

In the bigger picture, considering bullish convergence condition in daily and weekly MACD, a medium term bottom should be in place at 1.1107 after hitting 61.8% retracement of 1.0339 (2016 low) to 1.2555 (2018 high) at 1.1186. Further rise should be seen to 38.2% retracement of 1.2555 to 1.1107 at 1.1660. Reactions from there could indicate whether rebound from 1.1107 is a corrective rise or reversing medium term trend. In any case, risk will stay mildly on the upside as long as 1.1107 low remains intact.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | 13.20% | -7.90% | ||

| 23:50 | JPY | Monetary Base Y/Y Jun | 4.00% | 3.40% | 3.60% | |

| 4:30 | AUD | RBA Rate Decision | 1.00% | 1.00% | 1.25% | |

| 6:00 | EUR | German Retail Sales M/M May | -0.60% | 0.50% | -2.00% | -1.00% |

| 8:30 | GBP | Construction PMI Jun | 49.2 | 48.6 | ||

| 9:00 | EUR | Eurozone PPI M/M May | 0.10% | -0.30% | ||

| 9:00 | EUR | Eurozone PPI Y/Y May | 1.80% | 2.60% | ||

| 13:30 | CAD | Manufacturing PMI Jun | 49.1 |

{kind=link}