Sentiments turned sour again after US President Donald Trump’s harsh words on China at UN. But reactions in the forex markets are relatively muted. Dollar is the stronger one for now. New Zealand Dollar is supported after RBNZ stands pat without hinting on another imminent rate cut. On the other hand, Australian Dollar is the weakest so far. Sterling is reversing some of yesterday’s brief and weak rebound.

Technically, most major pairs and crosses are staying in consolidations. Yen crosses’ recoveries yesterday were rather weak. Focuses will stay on 106.68 in USD/JPY, 117.55 in EUR/JPY and 132.17 in GBP/JPY. Break will bring retests of recent low at 104.45, 115.86 and 126.54 respectively. If risk aversion comes back, we might see renewed selling in Australian and Canadian Dollar. That is, AUD/USD would resume the fall from 0.6894 to retest 0.6677 low. USD/CAD would finally rise through 1.3310 temporary top too.

In Asia, currently, Nikkei is down -0.38%. Hong Kong HSI is down -1.07%. China Shanghai SSE is down -0.60%. Singapore Strait Times is down -0.79%. Japan 10-year JGB yield is down -0.0166 at -0.255. Overnight, DOW dropped -0.53%. S&P 500 dropped -0.84%. NASDAQ dropped -1.46%. 10-year yield dropped -0.073 to 1.635.

Trump will not accept a bad trade deal with China

Asian stocks open generally lower today, following weakness in US overnight. Sentiments were somewhat weighed down by US President Donald Trump’s strongly worded rhetoric on China at United Nations General Assembly.

Trump criticized China for now delivering its promises when joining the WTO in 2001. He said “not only has China declined to adopt promised reforms, it has embraced an economic model dependent on massive market barriers, heavy state subsidies, currency manipulation, product dumping, forced technology transfers and the theft of intellectual property and also trade secrets on a grand scale”. And, “as far as America is concerned, those days are over.”

Though, Trump noted that “the American people are absolutely committed to restoring balance in our relationship with China. Hopefully, we can reach an agreement that will be beneficial for both countries.” But he also emphasized “as I have made very clear, I will not accept a bad deal.”

Additionally, Trump reiterated the link between Beijing’s treatment of Hong Kong and the trade deal. He said Washington was “carefully monitoring the situation in Hong Kong”. And, “the world fully expects that the Chinese government will honor its binding treaty made with the British and registered with the United Nations, in which China commits to protect Hong Kong’s freedom, legal system and democratic ways of life”. “How China chooses to handle the situation will say a great deal about its role in the world in the future. We are all counting on President Xi as a great leader,” Trump added.

ADB warns of gloomier prospects for international trade due to US-China tensions

The Asian Development Bank said in a report that growth in the 45 countries of developing Asia would slow from 5.9% in 2018 to 5.4% in 2019, then recover to 5.5% in 2020. The forecasts reflect “gloomier prospects for international trade” partly due to escalation US-China trade tensions, slowdown in advanced economies and the larger economies of developing Asia.

ADB Chief Economist Yasuyuki Sawada warned: “the PRC–US trade conflict could well persist into 2020 while major global economies may struggle even more than we currently anticipate. In Asia, weakening trade momentum and declining investment are the major concerns”.

The report also noted that an escalation and broadening of the US-China trade conflict may reshape supply chains in the region. There is already evidence of trade redirection from China toward other economies in developing Asia such as Vietnam and Bangladesh. Foreign direct investment is following a similar pattern.

RBNZ stands pat, maintains easing bias without hints on imminent rate cut

RBNZ left OCR unchanged at 1.00% as widely expected. The overall statement was balanced with easing bias. However, there is no clear indication of another imminent rate cut. Most importantly, RBNZ noted that “developments since the August Statement had not significantly changed the outlook for monetary policy”. It suggests that the central bank is still on wait-and-see mode, for observing the impact of the -50bps rate cut in August.

Nevertheless, easing bias is maintained as “there remains scope for more fiscal and monetary stimulus, if necessary, to support the economy and maintain our inflation and employment objectives.” But the statement is seen more as urging the government for fiscal stimulus. And the level of monetary stimulus needed might depend on how much the government would do.

Also from New Zealand, trade deficit widened to NZD -1565m, larger than expectation of NZD -100m.

BoJ Minutes: Appropriate to persistently continue with powerful monetary easing

In the minutes of July policy meeting, BoJ maintained that “economy was likely to continue on an “expanding trend” throughout the projection period through fiscal 2021, despite being affected by the slowdown in overseas economies. Exports were projected to “show some weakness” but would stay on a “moderate increasing trend”. The “continued relatively weak developments in prices” was largely affected by “deeply entrenched mindset and behavior based on the assumption that wages and prices would not increase easily”. Members still believed that CPI was “likely to increase gradually toward 2 percent”.

Four risks were outlined on economic outlook: (1) developments in overseas economies; (2) the effects of the scheduled consumption tax hike; (3) firms’ and households’ medium- to long-term growth expectations; and (4) fiscal sustainability in the medium to long term. Also downside risks from overseas were “significant”: (1) the consequences of protectionist moves — including the U.S.-China trade friction — and their effects, as well as (2) developments in the Chinese economy, including the effects of the aforementioned factor and (3) the possibility that the progress in adjustments in the global cycle for IT-related goods might take longer than expected.

On monetary policy, most members recognized that downside risks warranted attention. And, “it was appropriate to persistently continue with the current powerful monetary easing as the momentum toward achieving 2 percent inflation was being maintained with the output gap remaining positive”.

Also from Japan, corporate services price index rose 0.6% yoy in August, above expectation of 0.5% yoy.

Looking ahead

Germany will release Gfk consumer sentiment. Swiss will release ZEW expectations. UK will release CBI distributive trades. US will release new home sales later in the day.

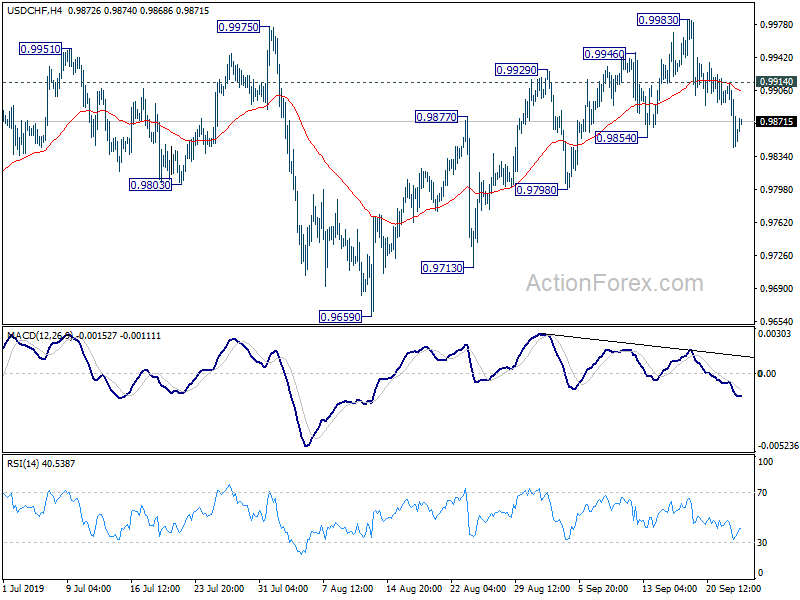

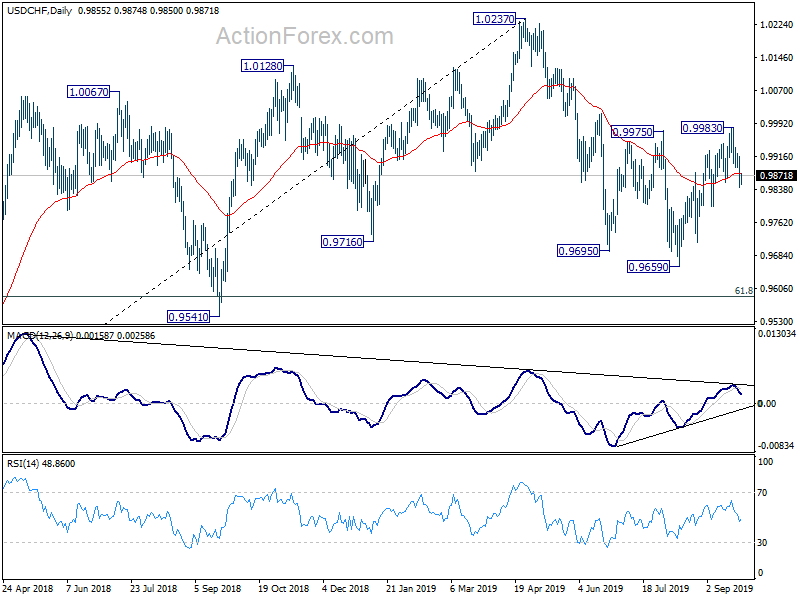

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9829; (P) 0.9872; (R1) 0.9899; More…

USD/CHF’s break of 0.9854 support argues that corrective rebound from 0.9659 has completed at 0.9983, after failing to sustain above 0.9975 resistance. Intraday bias is turned back to the downside for 0.9798 support first. Break will bring retest of 0.9659 low. On the upside, break of 0.9914 minor resistance will turn intraday bias neutral first. But risk will now stay on the downside as long as 0.9983 resistance holds.

In the bigger picture, the structure of the fall from 1.0237 suggests that it’s a corrective move. Sustained break of 0.9975 will argue that such correction has completed at 0.9659, ahead of 61.8% retracement of 0.9186 to 1.0237 at 0.9587. But decisive break of 1.0237 is needed to indicate up trend resumption. Otherwise, medium term outlook will stay neutral first. Meanwhile, break of 0.9695 support will extend the correction to 0.9541 support instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) M/M | -1565M | -100M | -685M | -700M |

| 23:50 | JPY | Corporate Services Price Index Y/Y Aug | 0.60% | 0.50% | 0.50% | 0.60% |

| 23:50 | JPY | BoJ Minutes | ||||

| 02:00 | NZD | RBNZ Rate Decision | 1.00% | 1.00% | 1.00% | |

| 06:00 | EUR | German GfK Consumer Climate Oct | 9.7 | 9.7 | ||

| 08:00 | CHF | ZEW Expectations Sep | -37.5 | |||

| 10:00 | GBP | CBI Distributive Trades Survey Sep | -26 | -49 | ||

| 14:00 | USD | New Home Sales Aug | 660K | 635K | ||

| 14:30 | USD | Crude Oil Inventories | 1.1M |

{kind=link}