Australian Dollar remains the strongest one for the week as stronger than expected CPI data prompted another round of buying in Asia. Other commodity currencies are also firm, but the Japanese Yen is not too far away. Dollar, on the other hand, is the worst performing one for the week so far. The greenback will turn to US GDP and Fed for savior. European majors are generally mixed.

Technically, USD/JPY remains on track to 104.58 near term projection level. It seems to be finally dragging down EUR/JPY, which is pressing 115.54 temporary low. Break will target near term projection level at 114.19.

Aussie pairs are worth a lot of attention before the weekend, as they’re pressing key resistance levels now. AUD/JPY is close to medium term cluster at around 69.95 (61.8% retracement of 76.54 to 59.89 at 70.17). AUD/CAD breached 0.9105 (38.2% retracement of 1.0784 to 0.8066 at 0.9104. EUR/AUD is pressing 1.6597 (2015 high, which is close to 55 week EMA at 1.6512. We’ll see if Aussie could power through these important levels.

In Asia, currently, Nikkei is down -0.06%. Hong Kong HSI is up 0.27%. China Shanghai SSE is up 0.39%. Singapore Strait Times is up 0.42%. Japan 10-year JGB yield is down -0.0075 to -0.045. Overnight, DOW dropped -0.13%. S&P 500 dropped -0.52%. NASDAQ dropped -1.40%. 10-year yield dropped -0.046 to 0.610.

Australia CPI jumped to 2.2% in Q1, highest since 2014

Australia CPI rose 0.3% qoq in Q1, above expectation of 0.2% qoq. Annually, CPI accelerated to 2.2% yoy, up from 1.8% yoy, beat expectation of 2.0% yoy. The annual rate was also the highest level since Q3 of 2014. RBA trimmed mean CPI rose 0.5% qoq, slightly above expectation of 0.4% qoq. Annual rate also accelerated to 1.8% yoy, up from 1.6% yoy and beat expectation of 1.6% yoy.

ABS Chief Economist, Bruce Hockman said: “There were some price effects of COVID-19 apparent in the March quarter due to higher purchasing of certain products towards the end of the quarter, as restrictions came into effect… More evident effects of COVID-19 are expected in the June quarter CPI.”

New Zealand imports and exports surged in March, but trade with China shrank

New Zealand’s imports rose 7.7% yoy to NZD 5.1B in March while exports rose 3.8% yoy to NZD 5.8B. Trade surplus came in at NZD 672m, smaller than expectation of NZD 700m.

Trade with its largest partner, China, continued to drop. Imports from China dropped -10% yoy to NZD 714m. Exports to China dropped -5.8% yoy to NZD 1.4B. Meanwhile, exports to Australia also dropped -8.9% yoy to NZD 738m. But exports to US rose 9.4% to NZD 623m. Exports to EU rose 8.2% yoy to NZD 595m. Exports to Japan also rose 22% yoy to NZD 352m.

Fitch downgrades Italy rating to BBB-, significant impact of coronavirus on economy and fiscal position

Fitch downgraded Italy’s credit rating to BBB- yesterday, down from BBB, with a stable outlook. The rating is now just a single notch above “junk level”. The agency said “the downgrade reflects the significant impact of the global Covid-19 pandemic on Italy’s economy and the sovereign’s fiscal position…. According to our baseline debt dynamics scenario, the [debt] to GDP ratio will only stabilise at this very high level over the medium term, underlining debt sustainability risks.”

Fitch also warned “downward pressure on the rating could resume if the government does not implement a credible economic growth and fiscal strategy that enhances confidence that general government debt/GDP will be placed on a downward path over time.”

Italian Finance Minister Roberto Gualtieri responded and said “the fundamentals of Italy’s economy and public finances are solid”.He added that Fitch’s move didn’t take into account the measures by EU. “In particular, the strategic orientation of the European Central Bank does not seem to be adequately valued.”

Dollar index range bound as US GDP and Fed awaited

Two heavy weight events are scheduled for the US today. Firstly. Q1 GDP is expected to show -4.0% annualized contraction. That would be the steepest contraction since the Great Recession in 2009. Consumer spending has definitely suffered a big hit from the coronavirus lockdowns. Some focuses would be on business investments. Optimism was lifted just for a brief while by US-China trade agreement phase one, but then nose-dived on the pandemic.

Fed is generally expected to keep monetary policies unchanged today. There will be no formal economic projections until June, which is agreeable as everything ties to how the coronavirus pandemic is contained. Nevertheless, Fed chair Jerome Powell could still offer a glimpse of what he expected in the second half, and he view on the shape of the recovery. Guidance on interest rates would be something to watch too. Powell has ruled out negative rates for now and we’ll see if he sticks to the same position.

Suggested readings:

- FOMC to Highlight Weakness in Economy and Reinforce Dovish Stance in April Meeting

- Fed Meeting: Taking A Breather

While Dollar is performing rather poorly this week, the development in Dollar index isn’t that bad. That’s primarily due to indecisiveness in Euro, though. Technically, we’re seeing price actions from 102.99 as a corrective pattern, with the sideway pattern from 98.27 as the second leg. Firm break of 55 day EMA will confirm the start of the third leg towards 98.27 support. But in that case, we’d expect strong support from 61.8% retracement of 94.65 to 102.99 at 97.83 to contain downside and bring rebound.

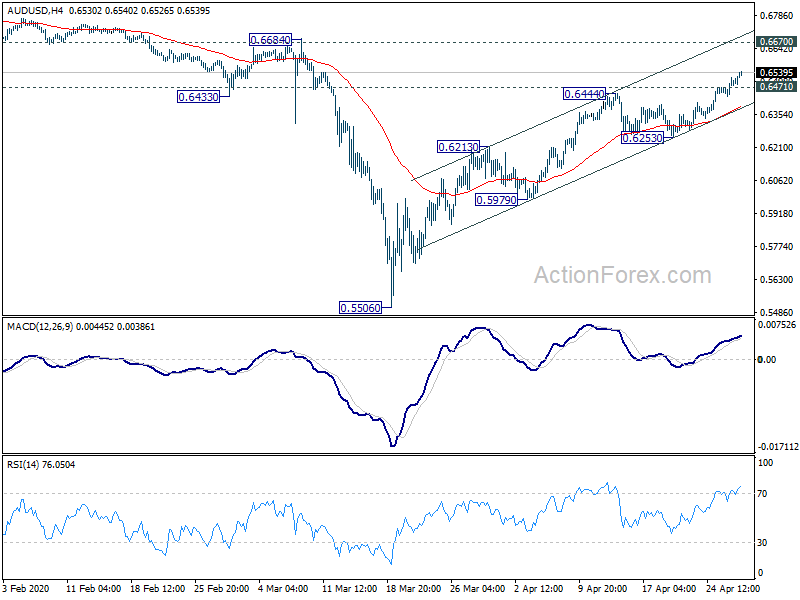

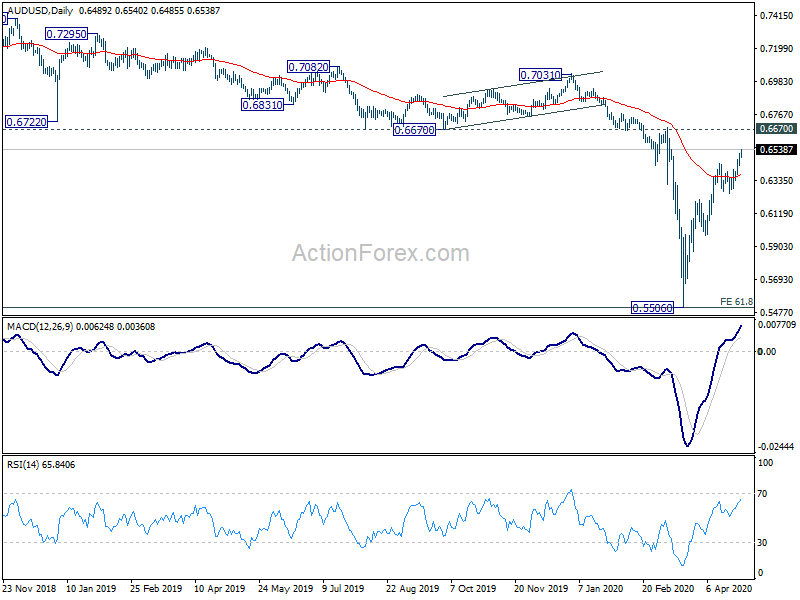

AUD/USD Daily Report

Daily Pivots: (S1) 0.6406; (P) 0.6439; (R1) 0.6495; More…

AUD/USD’s rise from 0.5506 continues today and intraday bias remains on the upside. Next target is 0.6670 key resistance. On the downside, below 0.6471 minor support will turn intraday bias neutral first. Further break of 0.6253 support will argue that rebound from 0.5506 has completed.

In the bigger picture, there is no clear sign of trend reversal yet. The larger down trend from 1.1079 (2011 high) is still in favor to extend. 61.8% projection of 1.1079 to 0.6826 from 0.8135 at 0.5507 is already met. Sustained break there will pave the way to 0.4773 (2001 low). On the upside, however, sustained break of 0.6607 will suggest medium term bottoming and turn focus to 0.7031 resistance next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | 672M | 700M | 594M | 531M |

| 23:01 | GBP | BRC Shop Price Index Y/Y Mar | -0.70% | -0.80% | ||

| 1:30 | AUD | CPI Q/Q Q1 | 0.30% | 0.20% | 0.70% | |

| 1:30 | AUD | CPI Y/Y Q1 | 2.20% | 2.00% | 1.80% | |

| 1:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 0.50% | 0.40% | 0.40% | 0.50% |

| 1:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 1.80% | 1.60% | 1.60% | |

| 6:00 | EUR | Germany Import Price Index M/M Mar | -2.30% | -0.90% | ||

| 8:00 | CHF | ZEW Survey – Expectations Apr | -45.8 | |||

| 9:00 | EUR | Eurozone Economic Sentiment Apr | 75 | 94.5 | ||

| 9:00 | EUR | Eurozone Services Sentiment Apr | -2.2 | |||

| 9:00 | EUR | Eurozone Consumer Confidence Apr F | -22.7 | -22.7 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Apr | -25 | -10.8 | ||

| 9:00 | EUR | Eurozone Business Climate Apr | -0.28 | |||

| 9:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 5.50% | 5.50% | ||

| 12:00 | EUR | Germany CPI M/M Apr P | 0.00% | 0.10% | ||

| 12:00 | EUR | Germany CPI Y/Y Apr P | 0.60% | 1.40% | ||

| 12:30 | USD | GDP Annualized Q1 P | -4.00% | 2.10% | ||

| 12:30 | USD | GDP Price Index Q1 P | 1.00% | 1.40% | ||

| 14:00 | USD | Pending Home Sales M/M Mar | -10.00% | 2.40% | ||

| 14:30 | USD | Crude Oil Inventories | 15.0M | |||

| 18:00 | USD | Fed Interest Rate Decision | 0.25% | 0.25% | ||

| 18:30 | USD | FOMC Press Conference |

{kind=link}