There is not much change in the global investor sentiments today, as stock markets continue to rally on lockdown exit optimism. Much better than expected job data from the US also provide something to cheer. Though, in the currency markets, recent moves appear to have been exhausted. Australian Dollar turns notably weaker on profit taking after a long bull run. But Swiss Franc is the weakest while Canadian Dollar is not far behind ahead of BoC rate decision. On the other hand, New Zealand Dollar and Euro are currently the stronger ones for today. Markets could be turning into mixed consolidative trading.

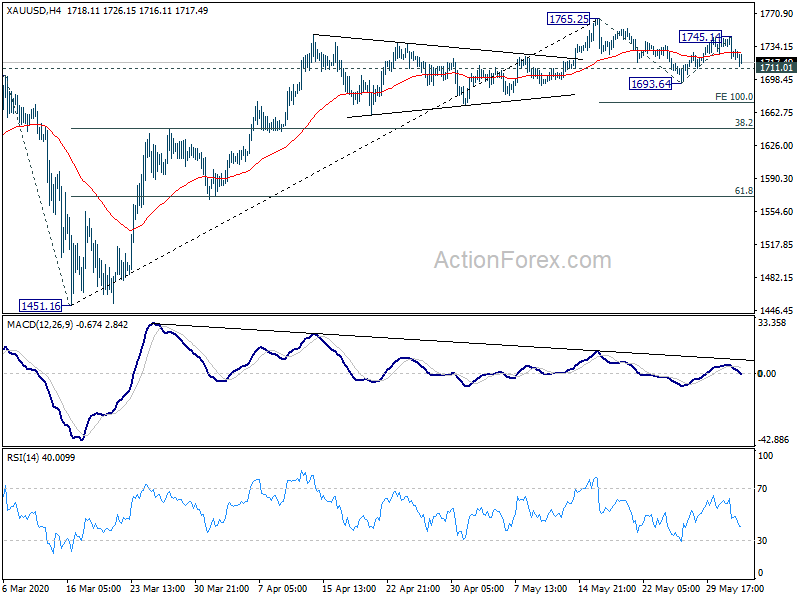

Technically, Gold is back eying 1711.01 minor support with this week’s fall. Break will likely extend the corrective pattern from 1765.25 with another down leg, towards 100% projection of 1765.25 to 1693.54 from 1745.14 at 1673.53. That might be a sign of a rebound in Dollar elsewhere. Meanwhile, AUD/NZD continues to struggle to sustain above 1.0865 near term resistance. Break of 1.0667 minor support will indicate short term topping and bring deeper pull back. If both happens as mentioned, they could together point to a deeper pull back in the powerful AUD/USD.

In Europe, currently, FTSE is up 1.16%. DAX is up 2.37%. CAC is up 2.01%. German 10-year yield is up 0.02277 at -0.384. Earlier in Asia, Nikkei rose 1.29%. Hong Kong HSI rose 1.37%. China Shanghai SSE rose 0.07%. Singapore Strait Times rose 3.40%. Japan 10-year JGB yield rose 0.0022 to 0.013.

US ADP employment dropped -2760k, job loss likely peaked

US ADP report showed only -2760k contraction in private sector jobs in May, well below prior months -19557k. By company size, small businesses lost -435k jobs, medium businesses lost -722k, large businesses lost -1604k. By sector, goods-producing companies lost -794k, service-providing companies lost -1967k.

“The impact of the COVID-19 crisis continues to weigh on businesses of all sizes,” said Ahu Yildirmaz, co-head of the ADP Research Institute. “While the labor market is still reeling from the effects of the pandemic, job loss likely peaked in April, as many states have begun a phased reopening of businesses.”

Eurozone unemployment rate rose to 7.3% in Apr, 11.9m people jobless

Eurozone unemployment rate rose to 7.3% in April, up from March’s 7.1%. EU unemployment rose to 6.6%, up from 6.4%. Eurostat estimates that 14.079 million men and women in the EU, of whom 11.919 million in the euro area, were unemployed in April 2020. Compared with March 2020, the number of persons unemployed increased by 397000 in the EU and by 211000 in the euro area.

Eurozone PPI came in at -2.0% mom, -4.5% yoy in April, below expectation of -1.8% mom, -.4% yoy. Germany unemployment rose 238k in May, above expectation of 200k. Unemployment rate rose to 6.3%, up from 5.8%, above expectation of 6.2%.

Eurozone PMI composite finalized at 31.9, still point to -9% GDP contraction in 2020

Eurozone PMI Services was finalized at 30.5 in May, up from April’s 12.0. PMI Composite was finalized at 31.9, up from 13.6. Among the member states where data are available, improvement were seen in Italy, Germany, France and Spain. But all PMI composite stayed well below 50, with Italy at 33.9, Germany at 32.3, France at 32.1, Spain at 29.2.

Chris Williamson, Chief Business Economist at IHS Markit said:

Eurozone GDP is consequently set to fall at an unprecedented rate in the second quarter, accompanied by the largest rise in unemployment seen in the history of the euro area.” But ” the downturn has already eased markedly in all countries surveyed.”

“Providing there is no resurgence of infection numbers, the planned lifting of lockdowns will inevitably help boost business activity and sentiment further in coming months. “However, the outlook is scarred by the prospect of demand remaining weak due to household spending being hit by high levels of unemployment and corporate spending being subdued as companies repair balance sheets.”

“We therefore remain cautious with respect to the recovery. Our forecasters expect GDP to slump by almost 9% in 2020 and for a recovery to prepandemic levels of output to take several years.”

UK PMI services finalized at 29.0, deep cuts to corporate spending a major dragging factor

UK PMI Services was finalized at 29.0 in May, up from April’s 13.4. PMI Composite was finalized at 30.0, up from April’s record low of 13.8. Markit said new works slumped amid cutbacks to business and consumer spending. Employment remains on sharp downward trajectory. Business expectations, however, rise again from March’s record low.

Tim Moore, Economics Director at IHS Markit: “The COVID-19 pandemic continued to have a severe impact on UK service sector activity in May, despite a boost in some areas from the gradual easing of lockdown measures. Survey respondents noted that deep cuts to corporate spending had been a major factor dragging down business activity in May, leading to a lack of work to replace completed projects.

Swiss GDP contracted -2.6% in Q1, worse than expectation

Swiss GDP contracted -2.6% qoq in Q1, worse than expectation of -2.2% qoq. “Due to the coronavirus pandemic and the measures to contain it, economic activity in March was severely restricted. The international economic slump also slowed down exports.”

By production approach, manufacturing dropped -1.3% qoq. Construction dropped -4.2% qoq. Trade dropped -4.4%. Accommodation and food dropped -23.4% qoq. Business services dropped -1.9% qoq. Health and social activities dropped -3.9% qoq. Arts, entertainment and recreation dropped -5.4% qoq. On the other hand, finance and insurance rose 1.5% qoq. Public administration rose 0.8% qoq.

By expenditure approach, private consumption dropped -3.5% qoq. Equipment and software investment dropped -4.0% qoq. Construction investment dropped -0.4% qoq. Export of services dropped -4.4% qoq. Import of goods dropped -1.1% qoq while imports of services dropped -1.2% qoq. On the other and, government consumption rose 0.7% qoq. Exports of goods rose 3.4% qoq.

Australia GDP contracted -0.3% in Q1, started first recession in 29 years

Australia GDP contracted -0.3% qoq in Q1, matched expectations. That’s the first contraction in 9 years. Also, the recession should have started in Q1, for the first time in 29 years. Annually, growth slowed to 1.4% yoy, lowest since September 2009 when Australia was in the midst of the global financial crisis.

Treasurer Josh Frydenberg confirmed that the economy is in recession and “that is on the basis of the advice that I have from the Treasury department about where the June quarter is expected to be.” “Based on what we know from Treasury, we’re going to see a contraction in the June quarter, which is going to be a lot more substantial than what we have seen in the March quarter,” he added.

Though, Frydenberg also said “in the face of a one-in-100-year global pandemic, the Australian economy has been remarkably resilient.” “This strength gave us the fiscal firepower to respond as we have done; Around $260 billion in economic support, or the equivalent of more than 13 per cent of GDP.”

Also from Australia, AiG Performance of Construction Index rose to 24.9 in May, up from 21.6. Building permits dropped -1.8% mom in April, better than expectation of -15.0% mom.

Japan PMI composite rose to 27.8 in May, indicative of -10% annualized GDP contraction

Japan PMI Services improved to 26.5 in May, up from April’s record low of 21.5. PMI Composite also rose slightly to 27.8, up from April’s record low of 25.8. The data signed “historically unparalleled” decline in output.

Joe Hayes, Economist at IHS Markit, said: “While the month of May has seen the Japanese government reduce the stringency of its lockdown, latest survey data indicated that economic activity continued to sink at a rate which had previously been unrivalled before the coronavirus crisis began… Looking at May’s survey data in isolation, the reading of the Composite PMI is indicative of GDP falling by around 10% on an annual basis. Taking into consideration the April reading, which was even worse, it is clear that the impact on second quarter GDP is going to be enormous.”

China Caixin PMI composite rose to 54.5, more time still needed to return to normal

China Caixin PMI Services rose to 55.0 in May, up from April’s 44.4. PMI Composite rose to 54.5, up from 47.6, back in expansion territory. Markit said that business activity and new work rose at quickest pace since late 2010. Pandemic continued to weigh heavily on export orders. Employment fell slightly as firms look to raise efficiency.

Wang Zhe, Senior Economist at Caixin Insight Group said: “In general, the improvement in supply and demand was still not able to fully offset the fallout from the pandemic, and more time is needed for the economy to get back to normal. The composite employment gauge stayed in negative territory as companies were cautious about increasing headcounts. But they were relatively optimistic about the economy’s forward momentum, and look forward to implementation of the policies announced during the annual session of China’s top legislature.”

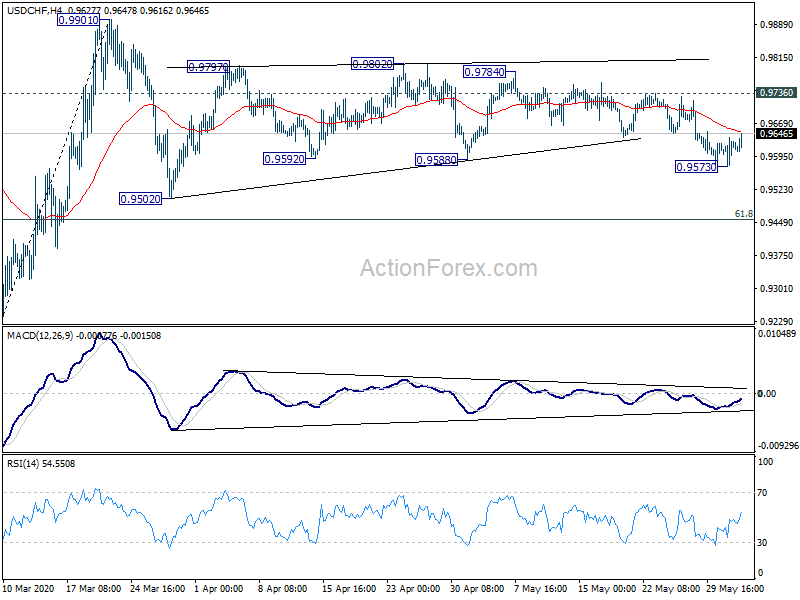

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9586; (P) 0.9612; (R1) 0.9650; More…

USD/CHF’s recovery form 0.9573 continues in early US session, but upside is held well below 0.9736 resistance. Intraday bias stays neutral and another fall remains in favor. Break of 0.9573 will extend the corrective pattern form 0.9901 to 0.9502 support. But downside should be contained by 61.8% retracement of 0.9181 to 0.9901 at 0.9456 to rebound. On the upside, break of 0.9736 resistance will turn bias back to the upside instead.

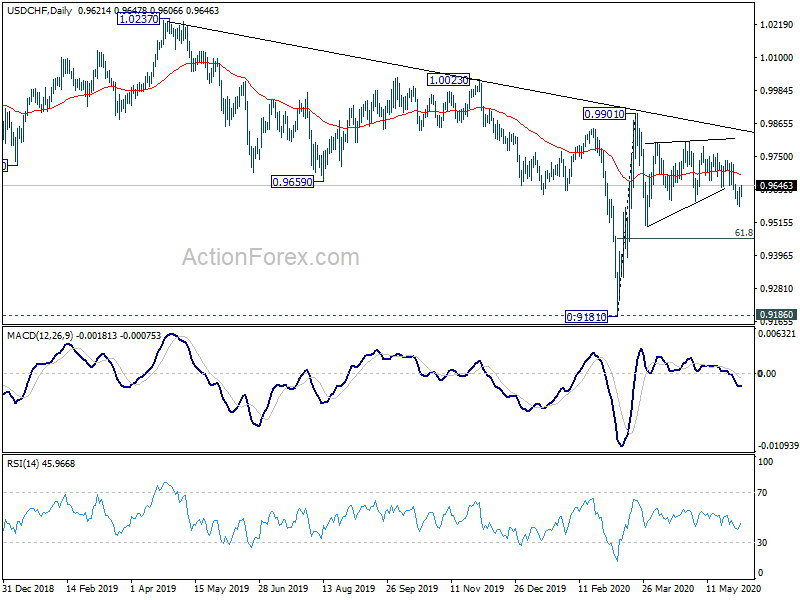

In the bigger picture, decline from 1.0237 is seen as the third leg of the pattern from 1.0342 (2016 low). It could have completed at 0.9181 after hitting 0.9186 key support (2018 low). Break of 0.9901 will extend the rebound form 0.9181 through 1.0023 resistance. After all, medium term range trading will likely continue between 0.9181/1.0237 for some more time.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index May | 24.9 | 21.6 | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Apr | -2.40% | -1.70% | ||

| 01:30 | AUD | GDP Q/Q Q1 | -0.30% | -0.30% | 0.50% | |

| 01:30 | AUD | Building Permits M/M Apr | -1.80% | -15.00% | -4.00% | -2.50% |

| 01:45 | CNY | Caixin Services PMI May | 55 | 47.4 | 44.4 | |

| 05:45 | CHF | GDP Q/Q Q1 | -2.60% | -2.20% | 0.30% | |

| 07:45 | EUR | Italy Services PMI May | 28.9 | 27 | 10.8 | |

| 07:50 | EUR | France Services PMI May F | 31.1 | 29.4 | 29.4 | |

| 07:55 | EUR | Germany Services PMI May F | 32.6 | 31.4 | 31.4 | |

| 07:55 | EUR | Germany Unemployment Rate May | 6.30% | 6.20% | 5.80% | |

| 07:55 | EUR | Germany Unemployment Change May | 238K | 200K | 373K | 372K |

| 08:00 | EUR | Italy Unemployment Apr | 6.30% | 9.20% | 8.40% | 8.00% |

| 08:00 | EUR | Eurozone Services PMI May F | 30.5 | 28.7 | 28.7 | |

| 08:30 | GBP | Services PMI May | 29 | 27.9 | 27.8 | |

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 7.30% | 8.20% | 7.40% | 7.10% |

| 09:00 | EUR | Eurozone PPI M/M Apr | -2.00% | -1.70% | -1.50% | |

| 09:00 | EUR | Eurozone PPI Y/Y Apr | -4.50% | -4.00% | -2.80% | |

| 12:15 | USD | ADP Employment Change May | -2760K | -9500K | -20236K | -19557K |

| 12:30 | CAD | Labor Productivity Q/Q Q1 | 3.40% | -0.10% | ||

| 13:45 | USD | Services PMI May F | 36.9 | 36.9 | ||

| 14:00 | USD | ISM Non-Manufacturing PMI Apr | 43 | 41.8 | ||

| 14:00 | USD | ISM Non-Manufacturing Employment Apr | 35.8 | 30 | ||

| 14:00 | USD | Factory Orders M/M Apr | -12.40% | -10.40% | ||

| 14:00 | CAD | BoC Interest Rate Decision | 0.25% | 0.25% | ||

| 14:30 | USD | Crude Oil Inventories | 3.0M | 7.9M |

{kind=link}