The markets are rather quiet so far today with slow news flow. Major currency pairs and crosses are stuck inside yesterday’s range, in consolidative trading. Other markets are also mixed, with some hope for DOW to hit new records, but other indices are weak. US consumer inflation data provides no special inspiration to traders. Focuses will first turn to BoC rate decision, which is more likely a non-event than not. Then eyes will be on US 10-year bond auctions

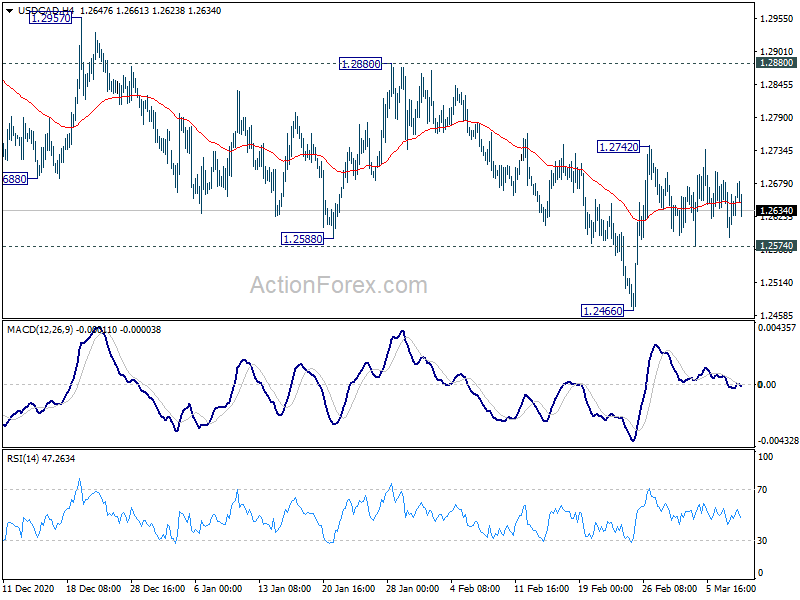

Technically, USD/CAD is one to watch in US session. It’s so far stuck in range of 1.2574/2742. On the upside, break of 1.2742 will resume the rebound form 1.2466 to 1.2880 near term structural resistance. Decisive break there will carry larger bullish implications. Meanwhile, break of 1.2574 support will affirm near term bearishness and bring retest of 1.2466 low next.

In Europe, currently, FTSE is down -0.10%. DAX is up 0.62%. CAC is up 0.89%. German 10-year yield is down -0.0108 at -0.310. Earlier in Asia, Nikkei rose 0.03%. Hong Kong HSI rose 0.47%. China Shanghai SSE dropped -0.05%. Singapore Strait Times dropped -0.93%. Japan 10-year JGB yield dropped -0.0041 to 0.126.

US CPI accelerated to 1.7% yoy, but core CPI slowed to 1.3% yoy in Feb

US CPI rose 0.4% mom in February, matched expectations. CPI core rose 0.1% mom, below expectation of 0.2% mom. Annually, CPI accelerated to 1.7% yoy, up from 1.4% yoy, matched expectations. CPI core slowed to 1.3% yoy, down from 1.4% yoy, missed expectation of 1.4% yoy.

France industrial output rose 3.3% mom in Jan, still -1.7% below pre-pandemic level

France industrial output rose 3.3% mom in January, well above expectation of 0.5% mom. Manufacturing output also rose 3.3% mom. Comparing to February 2020, the last month before first pandemic lockdown, manufacturing output was still -2.6% low, while whole industrial output was -1.7% lower.

Looking at some details, output increased in all industrial activities, except in transport equipment. Machinery and equipment goods rose 8.4% mom. Mining and quarrying, energy, water supply rose 2.9%. Food products and beverages rose 1.6% mom. Coke and refined petroleum rose 7.2% mom. Transport equipment dropped -2.9% mom.

RBA Lowe: Australian economy recovering well, but still a long way to go

RBA Governor Philip Lowe said in a speech that “we received further confirmation that the Australian economy is recovering well”, and “these better-than-expected outcomes are very welcome news”. However, “there is still a long way to go and that the Australian economy is operating well short of full capacity”.

“Over the past couple of weeks market pricing has implied an expectation of possible increases in the cash rate as early as late next year and then again in 2023”, he acknowledged. But, “this is not an expectation that we share”.

“Our judgement is that we are unlikely to see wages growth consistent with the inflation target before 2024,” he reiterated. “This is the basis for our assessment that the cash rate is very likely to remain at its current level until at least 2024.”

In the Q&A session, Lowe also said he’d be more “comfortable” if Australian Dollar’s exchange rate is lower, “because we need to get the unemployment rate down, inflation back to target and a lower currency would help us get there.” But the currency is not overvalued with commodity prices very high and interest rate differentials stable.

Australia Westpac consumer sentiment rose to 111.8 in March, close to 10-year high

Australia Westpac Consumer Sentiment rose 2.6% to 111.8 in March, from February’s 109.1. It’s now just 0.2 pts below the 10-year high recorded in December. “the main factors driving the Index are improving economic conditions and prospects, both domestically and abroad, particularly as they relate to our labour market.”

Westpac said RBA should be “well pleased” with the economic progress. “It is unlikely to make any changes to its current policy settings or signal any likelihood of changes in the near future.”

RBNZ removes some temporary liquidity facilities as financial market conditions improved significantly

RBNZ announced to remove some of the temporary liquidity facilities put in place during the COVID-19 pandemic. Measures include term auction and corporate open market operation (COMO) facilities, which allowed banks to borrow money in exchange for eligible corporate and asset-backed securities.

Head of Financial Markets Vanessa Rayner says, “Financial market conditions have improved significantly since March 2020 when these facilities were introduced and the usage of these special facilities has been very low in the last six months. In addition, the Large Scale Asset Purchase, Term Lending Facility, and Funding for Lending programmes have resulted in a significant increase in system liquidity and a lower cost of funding for banks.”

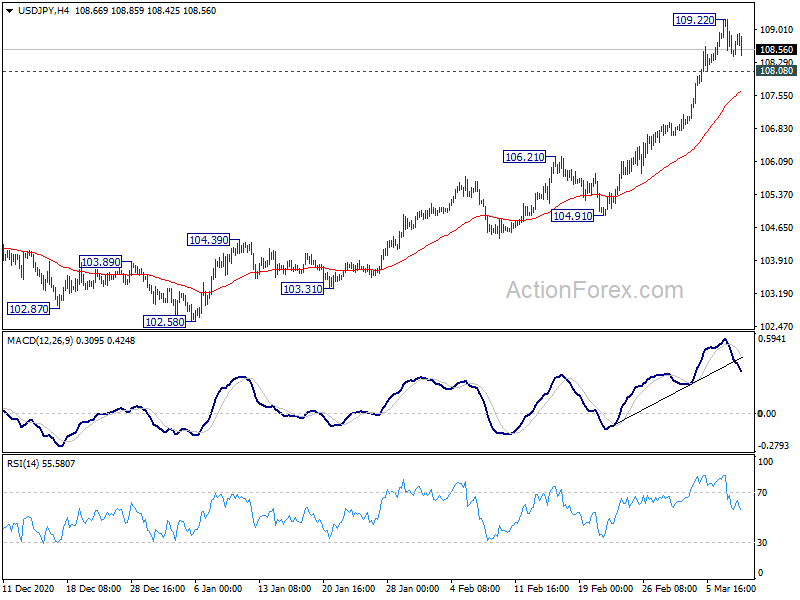

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.20; (P) 108.72; (R1) 109.01; More..

Outlook in USD/JPY is unchanged and intraday bias remains neutral for some sideway trading. With 108.08 minor support intact, consolidation should be relatively brief. On the upside, break of 109.22 will resume recent rally to channel resistance at 110.02 next. Decisive break there will carry larger bullish implications. Break of 108.08 will bring deeper correction. But outlook will stay bullish as long as 106.21 resistance turned support holds.

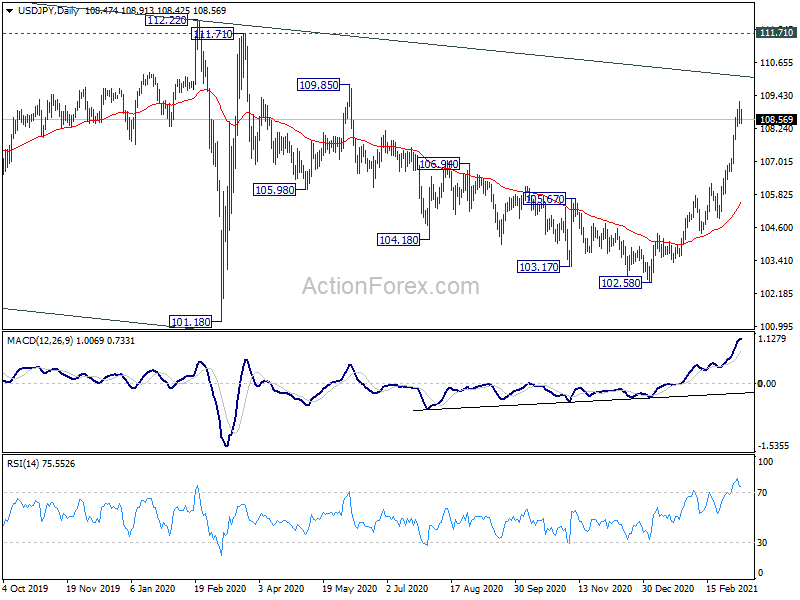

In the bigger picture, focus is now back on long term channel resistance (now at 110.02). Sustained break there will indicate that the down trend from 118.65 (Dec 2016) has completed. Further break of 112.22 resistance will confirm this bullish case and target 118.65 next. However, rejection by the channel resistance will keep medium term outlook bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Mar | 2.60% | 1.90% | ||

| 01:30 | CNY | CPI Y/Y Feb | -0.20% | -0.30% | -0.30% | |

| 01:30 | CNY | PPI Y/Y Feb | 1.70% | 1.50% | 0.30% | |

| 07:45 | EUR | France Industrial Output M/M Jan | 3.30% | 0.50% | -0.80% | -0.70% |

| 12:30 | USD | CPI M/M Feb | 0.40% | 0.40% | 0.30% | |

| 12:30 | USD | CPI Y/Y Feb | 1.70% | 1.70% | 1.40% | |

| 12:30 | USD | CPI Core M/M Feb | 0.10% | 0.20% | 0.00% | |

| 12:30 | USD | CPI Core Y/Y Feb | 1.30% | 1.40% | 1.40% | |

| 15:00 | CAD | BoC Interest Rate Decision | 0.25% | 0.25% | ||

| 15:00 | CAD | BoC Rate Statement | ||||

| 15:30 | USD | Crude Oil Inventories | 3.0M | 21.6M |

{kind=link}