Dollar dives sharply in early US session after huge employment data miss. Canadian Dollar is slightly weaker, also on job data disappointment. Euro and Swiss Franc are quick to jump on assaulting the greenback. But Yen is not too far behind, as stocks could be under some pressure after the data. As for the week, Dollar is set to end as the worst performing one without little doubt. Kiwi and Aussie are currently strongest, but Euro has the potential to overtake them.

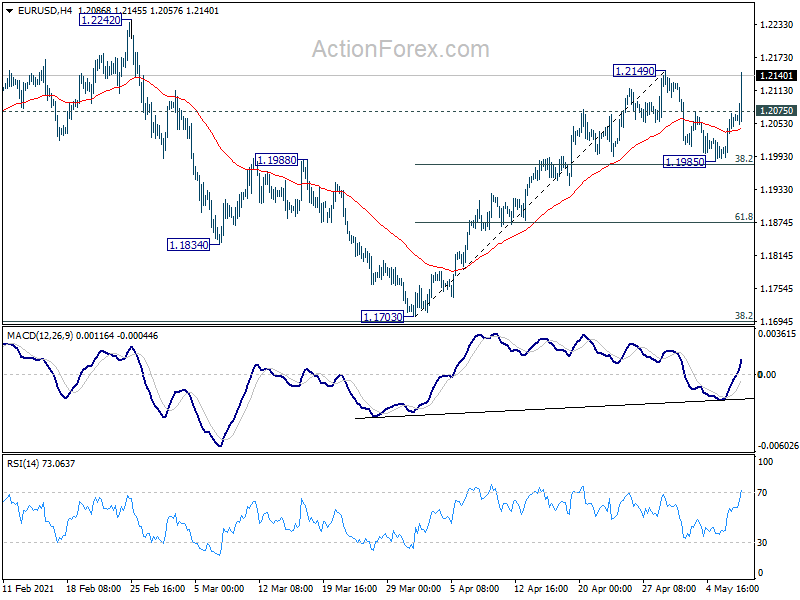

Technically, with the current surge, EUR/USD is likely ready to resume the rise from 1.1703. Firm break of 1.2149 will confirm and target 1.2242/2348 resistance zone. USD/JPY’s break of 108.70 minor support also suggests that recovery from 107.47 has completed, and retest of this low could be seen soon. Eyes will now be on 1.4008 resistance in GBP/USD and 0.7815 resistance in AUD/USD to confirm more dollar bearishness.

In Europe, at the time of writing, DAX FTSE is up 0.35%. DAX is up 0.89%. CAC is down -0.13%. Germany 10-year yield is down -0.024 at -0.244. Earlier in Asia, Nikkei rose 0.09%. Hong Kong HSI dropped -0.09%. China Shanghai SSE dropped -0.65%. Singapore Strait Times rose 0.86%. Japan 10-year JGB yield dropped -0.0045 to 0.085.

US NFP grew just 266k, well below expectation

US non-farm payroll employment grew just 266k in April, well below expectation of 950k. Prior month’s figure was also revised down from 916k to 770k. Total non-farm employment was still down -8.2m, or -5.4%, comparing to pre-pandemic level in February 2020. Unemployment rate edged up to 6.1%, above expectation of 5.7%. Labor force participation rate rose 0.2% to 61.7%. Wage growth, however, was strong, with average hourly earnings up 0.7% mom, versus expectation of 0.1% mom.

Canada employment dropped -207k, unemployment rate rose to 8.1%

Canada employment dropped -207k, or -1.1% in April, larger than expectation of -160.5k decline. Full times jobs dropped -129k, or -0.8%. Part-time jobs dropped -78k, or -2.3%. Unemployment rate jumped sharply by 0.6% to 8.1%, above expectation of 7.8%.

ECB Kazaks: The size of PEPP package is not an absolute truth

ECB Governing Council member Martins Kazaks said that “flexibility is at the very core of PEPP”, referring to the central bank’s Pandemic Emergency Purchase Program. “If financial conditions remain favorable, in June we can decide to buy less.”

He added that there is not reason to believe that PEPP program will extend beyond the March 2022. ECB might even complete the program without using up the entire envelop of EUR 1.85T, depending on economic developments. “The size of the package is not an absolute truth,” he said. “If the economy performs nicely, it’s quite likely that we will not need to spend everything.”

Still,he emphasized that it’s “premature” to talk about stimulus exit due to high uncertainty. “If the inflation outlook remains like the current forecast when PEPP ends, I think we would certainly discuss increasing APP,” Kazaks said.” Monetary policy will remain very accommodative. If necessary we can also devise new instruments.”

German industrial production rose 2.5% in March, France industrial output up 0.8% mom

Germany industrial production rose 2.5% mom in March, versus expectation of 2.0% mom. Compared with February 2020, the month before the pandemic, production was still -4.3% lower in seasonally and calendar adjusted terms. Exports rose 6.5% mom while exports rose 1.2% mom. Trade surplus came in at EUR 14.3B.

France industrial output rose 0.8% mom in March, below expectation of 2.0% mom. manufacturing output rose 0.4% mom. Compared to pre-pandemic February 2020, industrial output remained -5.9% down, manufacturing -6.8% down. France trade deficit came in at ER -6.1B, larger than expectation of -5.4B.

Swiss unemployment rate dropped to 3.1% in April, down from 3.3%, better than expectation of 3.6%. Foreign currency reserves dropped to CHF 915B in April, down from CHF 930B.

RBA discussed upside and downside scenarios in SoMP

In the Statement on Monetary Policy, RBA reiterated that it’s “committed to maintaining highly supportive monetary conditions to support a return to full employment in Australia and inflation consistent with the target”. The conditions for raising the cast rate is unlikely to be met “until 2024 at the earliest”.

RBA also discussed both an upside and a downside scenario. In the upside scenario, stronger household consumption and reduced uncertainty about the outlook would “underpin faster growth in business investment and employment” and “puts additional downward pressure on the unemployment rate”. Unemployment would fall below 4%, and inflation back within target range by mid-2023.

On the other hand, in the downside scenario, household prefer to continue strengthening their balance sheets. Lower consumption growth would weigh on business income, and prompting delay in investment, as well as slower employment growth. Unemployment rate will remain at around 5.25-5.50%, while underlying inflation will remain below 2%.

Also from Australia, AiG Performance of Services index rose 2.3 pts to 61.0 in April. That’s the highest reading since October 2003. All five of the services sectors available in the Australian PSI in April indicated expansion, with results above 50 points (trend). All five activity indicators – sales, new orders, employment, stocks and deliveries – showed positive and improving results in the month (results above 50 points and rising from last month, seasonally adjusted).

China Caixin PMI services rose to 56.3, composite rose to 54.7

China Caixin PMI Services rose to 56.3 in April, up from 54.3, above expectation of 54.2. There was steeper increase in activity amid strongest upturn in sales for five months. Quicker rise in employment helped easing capacity pressures. Optimism towards the year ahead remained historically sharp. PMI Composite rose to 54.7, up from 53.1.

Wang Zhe, Senior Economist at Caixin Insight Group said: “To sum up, the post-epidemic manufacturing and services recovery accelerated as both supply and demand expanded. Business confidence was high amid strong overseas demand and improved employment. Services recovered faster than manufacturing. Inflation will be a focus in the future. Inflationary pressure was evident as input costs and output prices in manufacturing and services have continued to increase for several months.”

China exports rose 32.3% yoy in Apr, imports up 43.1% yoy, surplus swelled to USD 42.9B

In USD term, in April, China’s total trade rose 37.0% yoy to USD 485B. Exports rose 32.3% yoy to USD 264B. Imports rose 43.1% yoy to USD 221B. Trade surplus came in at USD 42.9B, up from March’s 13.8B, well above expectation of USD 28.0B.

Year to date in April, total trade rose 38.2% yoy to USD 1789B. Exports rose 44.0% yoy to 974B. Imports rose 31.9% yoy to 816B. Trade surplus came in at USD 158B.

- YTD with EU, total trade rose 38.2% yoy to USD 250B. Exports rose 46.6% to USD 150B. Imports rose 35.7% to USD 100B.

- YTD with US, total trade rose 61.8% yoy to USD 222B. Exports rose 60.8% yoy to USD 161B. Imports rose 64.7% yoy to USD 60B.

- YTD with Australia, total trade rose 32.0% yoy to USD 68.1B. Exports rose 40.9% yoy to USD 19.3B. Imports rose 28.7% yoy to USD 48.8B.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2015; (P) 1.2043; (R1) 1.2093; More….

EUR/USD’s strong break of 1.2075 minor resistance suggests that pull back from 1.2149 has completed at 1.1985. Rise from 1.1703 is likely ready to resume. Intraday bias is back on the upside. Break of 1.2149 will confirm and target 1.2242/2348 resistance zone. In case of another fall, we’d continue to expect strong support from 38.2% retracement of 1.1703 to 1.2149 at 1.1979 to bring rebound.

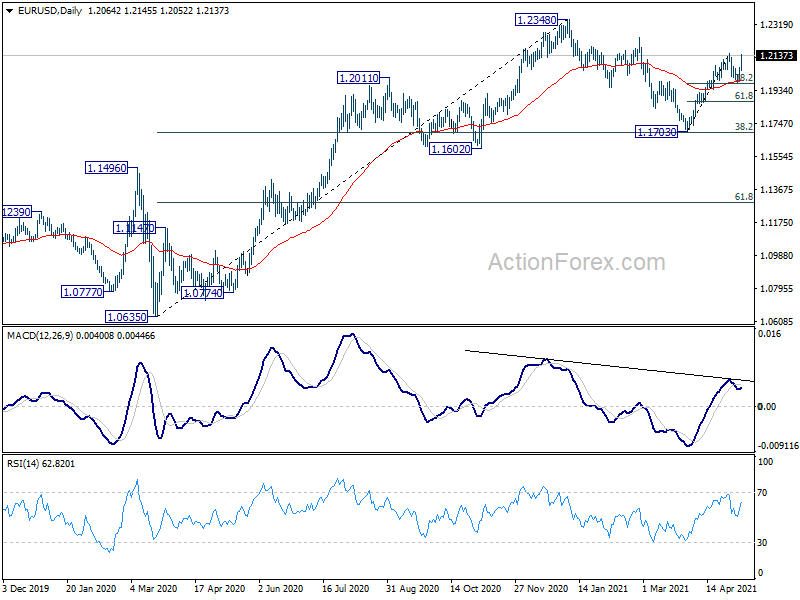

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. However, sustained break of 1.1602 will argue that whole rise from 1.10635 has completed. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Apr | 61 | 58.7 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | 0.20% | -0.50% | -0.40% | |

| 23:50 | JPY | Monetary Base Y/Y Apr | 24.30% | 21.90% | 20.80% | |

| 01:30 | AUD | RBA Monetary Policy Statement | ||||

| 01:45 | CNY | Caixin Services PMI Apr | 56.3 | 54.2 | 54.3 | |

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q2 | 2.05% | 1.89% | ||

| 03:03 | CNY | Trade Balance (USD) Apr | 42.9B | 28.0B | 13.8B | |

| 03:03 | CNY | Imports (USD) Y/Y Apr | 43.10% | 23.30% | 38.10% | |

| 03:03 | CNY | Exports (USD) Y/Y Apr | 32.30% | 35.50% | 30.60% | |

| 03:03 | CNY | Trade Balance (CNY) Apr | 276.5B | 88B | ||

| 03:03 | CNY | Imports (CNY) Y/Y Apr | 32.20% | 12.60% | 27.70% | |

| 03:03 | CNY | Exports (CNY) Y/Y Apr | 22.20% | 30.70% | 20.70% | |

| 05:45 | CHF | Unemployment Rate M/M Apr | 3.10% | 3.60% | 3.30% | |

| 06:00 | EUR | Germany Industrial Production M/M Mar | 2.50% | 2.00% | -1.60% | -1.90% |

| 06:00 | EUR | Germany Trade Balance (EUR) Mar | 14.3B | 22.3B | 19.1B | 18.9B |

| 06:45 | EUR | France Trade Balance (EUR) Mar | -6.1B | -5.4B | -5.2B | -5.1B |

| 06:45 | EUR | France Industrial Output M/M Mar | 0.80% | 2.00% | -4.70% | |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Apr | 914B | 930B | ||

| 08:00 | EUR | Italy Retail Sales M/M Mar | -0.10% | -1.50% | 6.60% | |

| 08:30 | GBP | Construction PMI Apr | 61.6 | 62.5 | 61.7 | |

| 12:30 | CAD | Net Change in Employment Apr | ‘-207.1K | -160.5K | 303.1K | |

| 12:30 | CAD | Unemployment Rate Apr | 8.10% | 7.80% | 7.50% | |

| 12:30 | USD | Nonfarm Payrolls Apr | 266K | 950K | 916K | 770K |

| 12:30 | USD | Unemployment Rate Apr | 6.10% | 5.70% | 6.00% | |

| 12:30 | USD | Average Hourly Earnings M/M Apr | 0.70% | 0.10% | -0.10% | |

| 14:00 | USD | Wholesale Inventories Mar F | 1.40% | 1.40% | ||

| 14:00 | CAD | Ivey PMI Apr | 67 | 72.9 |

{kind=link}