Dollar is trying to extend this week’s recovery in Asian session, as focus turns to non-farm payrolls reports. Whether Fed would start tapering asset purchases by the end of the year, or earlier, would very much depend on the job data in Q3. Elsewhere, Aussie is trading a touch softer after dovish comments from RBA governor. Swiss Franc and Yen also turned softer as US stocks made new record high overnight.

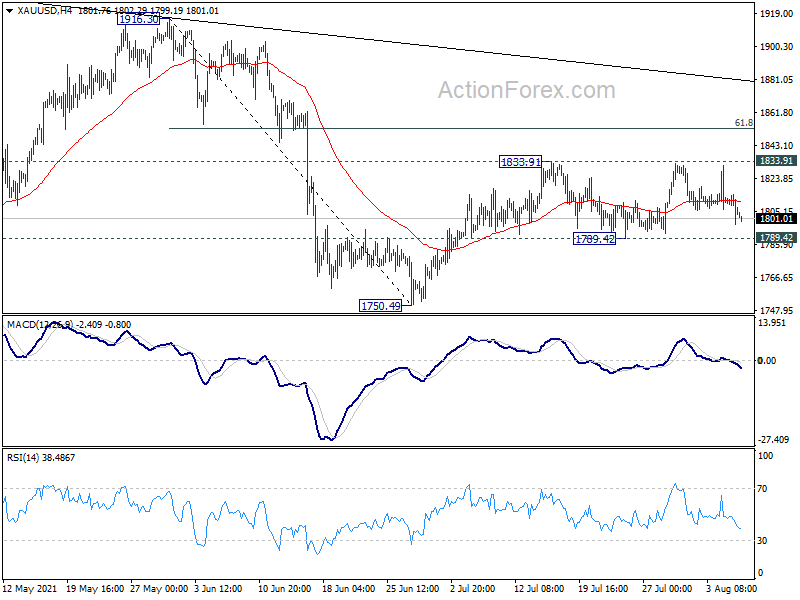

Technically, to judge Dollar’s underlying strength, we’d prefer to see firm break of 110.58 resistance in USD/JPY, 0.9116 resistance in USD/CHF, and to a lesser extent 1.2605 resistance in USD/CAD (which could be affected by Canadian job data too). Additionally, we’d also prefer to see break of 1789.42 support in gold to indicate completion of rebound from 1750.49, to double confirm Dollar buying.

In Asia, at the time of writing, Nikkei is up 0.33%. Hong Kong HSI is down -0.01%. China Shanghai SSE is down -0.48%. Singapore Strait Times is up 0.14%. Japan 10-year JGB yield is up 0.006 at 0.019. Overnight, DOW rose 0.78%. S&P 500 rose 0.60%. NASDAQ rose 0.78%. 10-year yield rose 0.033 to 1.217.

RBA Lowe: Fiscal support more appropriate response to temporary and localized hit to income

RBA Governor Philip Lowe said in a testimony that he didn’t rule out a recession due to restrictions, but still expecting a return to strong growth next year. “Any additional bond purchases would have their maximum effect at that time and only a very small effect right now when the extra support is needed most,” he added. For now, fiscal policy is “the more appropriate instrument for providing support in response to a temporary and localized hit to income.”

Regarding inflation, Lowe said much of this discussion has come out of the US, which was in a “substantially different position to the one we’re in.” In Australia, “the fact that wages growth is likely to remain below 3 per cent for the next couple of years means it’s very difficult for me to see us having an inflation problem.”

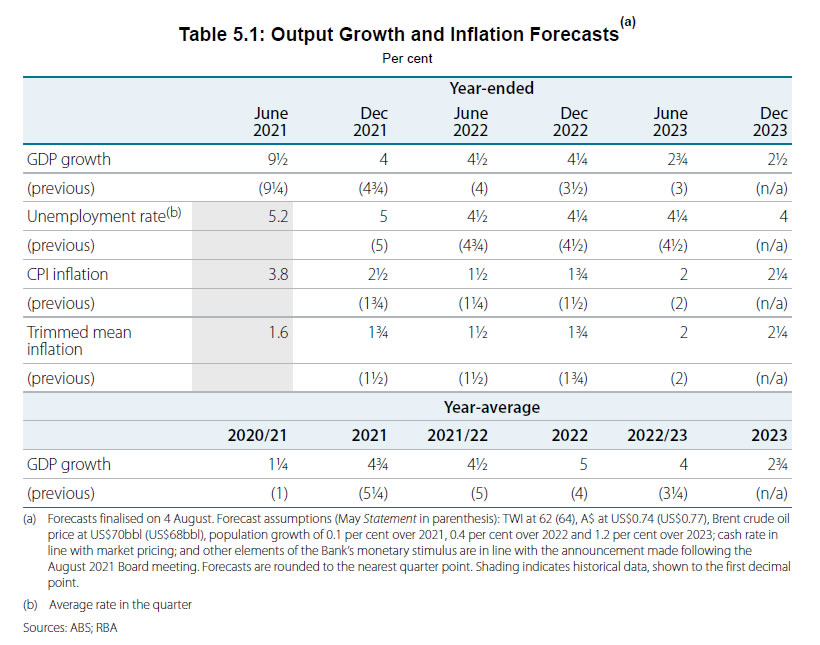

In the Statement on Monetary Policy, RBA downgraded 2021 year-average GDP growth forecast from 5.25% to 4.75%, but upgraded 2022 from 4% to 5%. GDP growth would then slow to 2.75% in 2023. Inflation is projected to be at 2.25% in December 2021 (upgraded from 1.75%), 1.75% in December 2022 (up from 1.50%), and then 2.25% in 2023 year-end. Unemployment rate is projected to be at 5% by 2021 year end, then gradually fall to 4% by 2023 year-end.

Australia AiG services dropped to 51.7, but employment holding up

Australia AiG Performance of Services dropped sharply by -6.1 pts to 51.7 in July. That’s the largest monthly decline since April 2020. Looking at some details, sales dropped -12.9 to 53.2. Employment dropped -3.2 to 51.0. New orders rose 0.1 to 56.7. Supplier deliveries dropped -9.6 to 45.3. Input prices rose 8.7 to 74.1. Selling prices rose 13.2 to 66.7. Average wages rose 2.0 to 68.0.

Ai Group Chief Executive, Innes Willox, said: “The substantial easing in the performance of the Australian services sector in July was mainly driven by the COVID-19 outbreaks and associated restrictions…. There were some encouraging signs with employment and sales holding up and new orders coming in at a faster pace than in June. This provides some grounds to expect the services sector could bounce back quickly if restrictions were able to be lifted. However, with COVID-19 infections and restricted areas on the rise in the early days of August, the chances of an early rebound appear to be fading.”

Fed Waller: Could pull back on accommodation sooner than others think

Fed Governor Christopher Waller said yesterday that his outlook is very much that the economy is “going to recovery”. And, “we will be able to pull back on accommodative monetary policy potentially sooner than others think.”

He repeated his “high hopes” for July and August job numbers, and expected the labor market to recover 85% of pandemic job loss by September. Fed could start to taper asset purchases in October if these two reports show 800k to 1m job growth each.

“My base case is that the inflation we’re seeing is somewhat transitory, that there will be some relief in the fourth quarter of this year on price pressures,” Waller added.

Fed Kashkari: The wrinkle now is Delta

Minneapolis Fed President Neel Kashkari said yesterday, “if we see a very strong labor market this fall, the way I’ve been expecting, then I think we could say we probably have made ‘substantial further progress.'”

However, the “wrinkle, now, is Delta”. He added, “if Delta causes the labor market to heal much more slowly, then that’s going cause me to step back”

“It’s so frustrating for all of us that the Delta variant is surging the way that it is,” Kashkari said. “I was cautiously optimistic a month ago that it seemed like we had the light at the end of the tunnel … and could return to normal.”

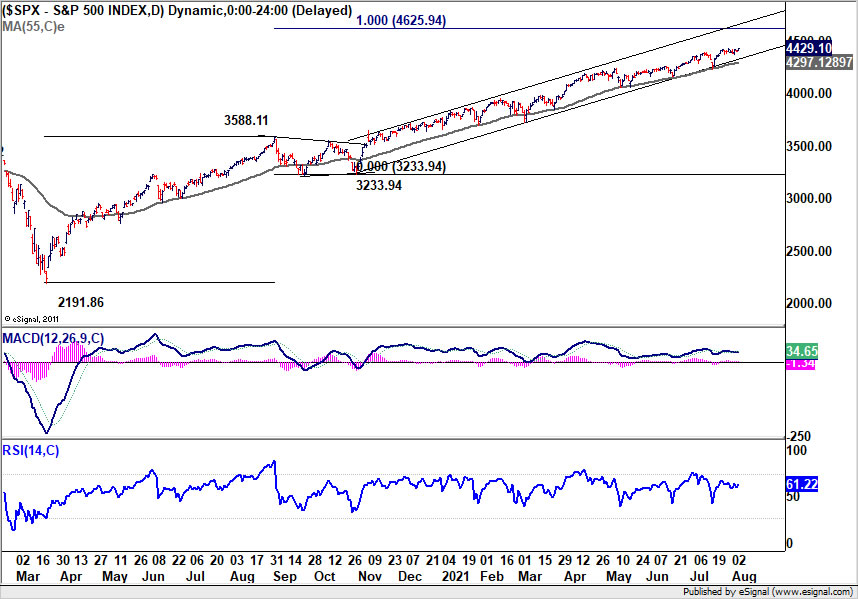

S&P 500 hit new record as focus turns to NFP

S&P 500 and NASDAQ jumped to close at record highs overnight as focuses now turn to non-farm payroll report. Markets are expecting 900k jobs growth in July while unemployment rate would fall from 5.9% to 5.7%.

Looking at related data, ISM manufacturing employment rose 3 pts to 52.9. ISM services employment also rose 4.5 pts to 53.8. Four-week moving average of initial claims was relatively unchanged at 394k. However, ADP private job growth was a big miss at 330k growth only. There is risk of a big surprise in the NFP print.

S&P 500 is losing some upside momentum as seen in daily MACD. But there is little to worry about the medium term up trend. It’s staying well above rising 55 day EMA, inside the rising channel. Some jitters might be seen in response to today’s NFP. But SPX should still be on track to 100% projection of 2191.86 to 3588.11 from 3233.94 at 4625.94, as long as 55 day EMA holds.

Elsewhere

Japan labor cash earnings dropped -1.0% yoy in June versus expectation of 1.2% yoy. Households spending dropped -5.1% yoy versus expectation of 0.1% yoy.

Germany industrial production, France trade balance, Italy industrial output and Swiss foreign currency reserves will be featured in European session.

Later in the day, Canada will also release job data and Ivey PMI, alongside US non-farm payrolls.

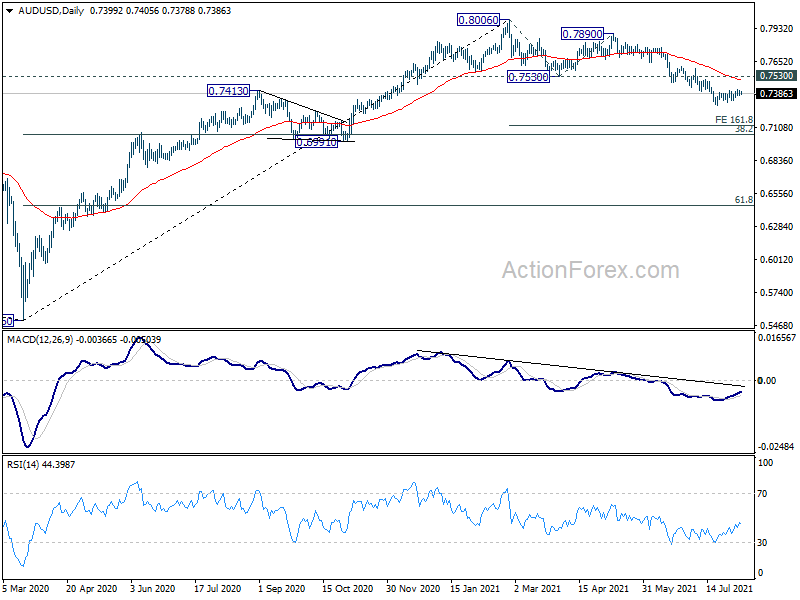

AUD/USD Daily Report

Daily Pivots: (S1) 0.7380; (P) 0.7398; (R1) 0.7420; More…

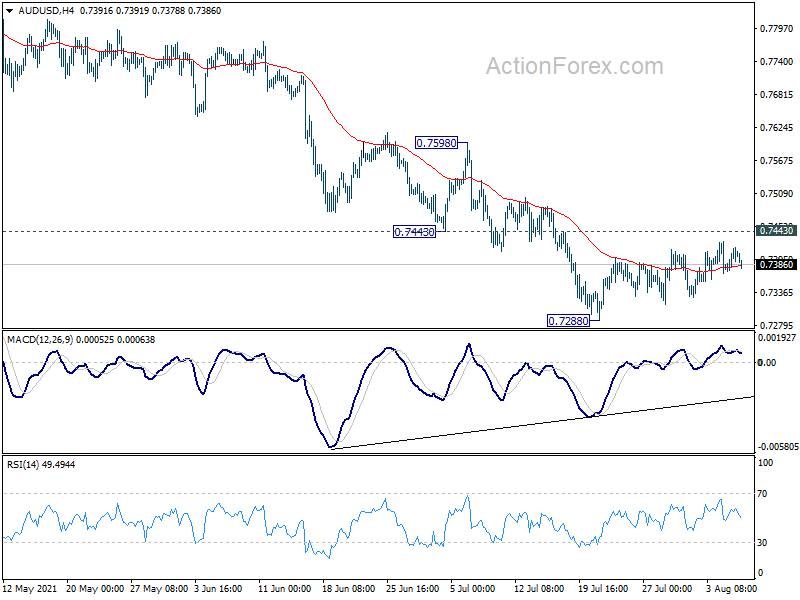

Intraday bias in AUD/USD remains neutral as consolidation from 0.7288 is in progress. Near term outlook stays bearish with 0.7443 support turned resistance intact, and further decline is in favor. On the downside, break of 0.7288 will resume the whole fall from 0.8006 and target 161.8% projection of 0.8006 to 0.7530 from 0.7890 at 0.7120 next. On the upside, break of 0.7443 will bring stronger rebound to 0.7530 support turned resistance instead.

In the bigger picture, rise from 0.5506 medium term bottom could have completed at 0.8006, after failing 0.8135 key resistance. Correction from there could target 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051). We’d look for strong support from there to bring rebound. However, sustained break of this level would argue that the whole medium term trend has indeed reversed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Jul | 51.7 | 57.8 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jun | -0.10% | 1.20% | 1.90% | |

| 23:30 | JPY | Household Spending Y/Y Jun | -5.10% | 0.10% | 11.60% | |

| 01:30 | AUD | RBA Monetary Policy Statement | ||||

| 05:00 | JPY | Leading Economic Index Jun P | 104.2 | 102.6 | ||

| 06:00 | EUR | Germany Industrial Production M/M Jun | 0.50% | -0.30% | ||

| 06:45 | EUR | France Trade Balance (EUR) Jun | -6.1B | -6.8B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jul | 941B | |||

| 08:00 | EUR | Italy Industrial Output M/M Jun | 0.80% | -1.50% | ||

| 12:30 | USD | Nonfarm Payrolls Jul | 900K | 850K | ||

| 12:30 | USD | Unemployment Rate Jul | 5.70% | 5.90% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jul | 0.30% | 0.30% | ||

| 12:30 | CAD | Net Change in Employment Jul | 148.5K | 230.7K | ||

| 12:30 | CAD | Unemployment Rate Jul | 7.70% | 7.80% | ||

| 14:00 | USD | Wholesale Inventories Jun F | 0.80% | 0.80% | ||

| 14:00 | CAD | Ivey PMI Jul | 67.3 | 71.9 |

{kind=link}