Rally in Yen and Swiss Franc dominated trading for most of the day, and it stays firm in early US session. Nevertheless, as sentiment of US traders are not too pessimistic, buying in both slows a little bit. On the other hand, Australia, New Zealand and US Dollars are taking turns to be the worst perform. Sterling is somewhat support by strong consumer inflation reading. But Canada CPI is doing little to help the Loonie.

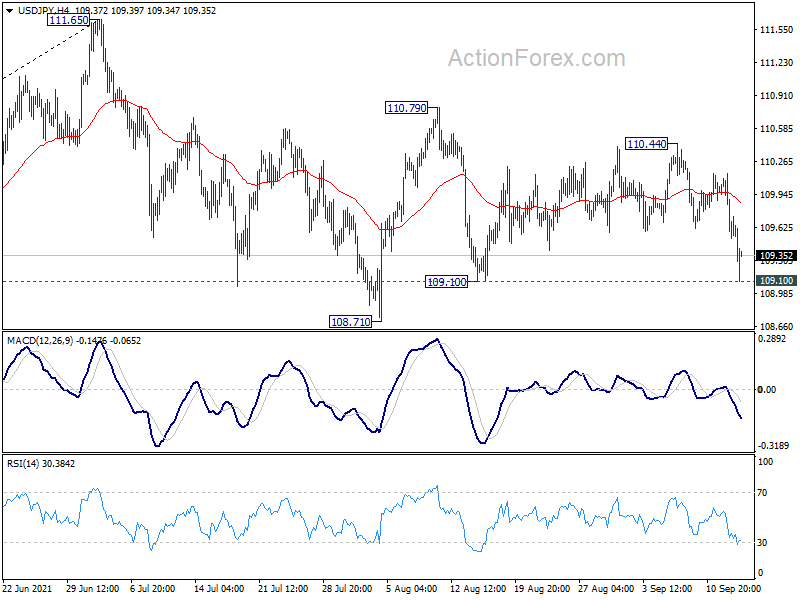

Technically, USD/JPY is now defending 109.10 support. Break there will likely resume whole pattern from 111.65 through 108.71 low. If that happens, we’ll see if it’s accompanied by a break of 1.1850 minor resistance in EUR/USD to signal Dollar weakness. Or it accompanied by steeper fall in EUR/JPY towards 127.91 to indicate upside acceleration in Yen.

In Europe, at the time of writing, FTSE is flat. DAX is down -0.10%. CAC is down -0.64%. German 10-year yield is up 0.012 at -0.326. Earlier in Asia, Nikkei dropped -0.52%. Hong Kong HSI dropped -1.84%. China Shanghai SSE dropped -0.17%. Singapore Strait Times dropped -0.71%. Japan 10-year JGB yield closed flat at 0.036.

Canada CPI jumped to 4.1% yoy in Aug, highest since 2003

Canada CPI accelerated further from 3.7% yoy to 4.1% yoy in August, above expectation of 3.9% yoy. That’s also the fastest pace since March 2003. Statistics Canada said the increase mainly stems from an accumulation of recent price pressures and from lower price levels in 2020.

Looking at some more details, CPI common rose from 1.7% yoy to 1.8% yoy, above expectation of 1.7% yoy. CPI median was unchanged at 2.6% yoy, matched expectations. CPI trimmed rose from 3.1% yoy to 3.3% yoy, above expectation of 3.1% yoy.

Eurozone industrial production rose 1.5% mom in Jul, EU up 1.4% mom

Eurozone industrial production rose 1.5% mom in July, above expectation of 0.5% mom. For the month, production of non-durable consumer goods rose by 3.5%, capital goods by 2.7%, durable consumer goods by 0.6% and intermediate goods by 0.4%, while production of energy fell by 0.6%.

EU industrial production rose 1.4% mom. Among Member States for which data are available, the highest monthly increases were registered in Ireland (+7.8%), Belgium (+5.0%) and Portugal (+3.5%). The largest decreases were observed in Lithuania (-2.0%), Slovenia (-1.8%) and Croatia (-1.6%).

Ifo: Germany inflation to hit 3% this year, fall back to 2-2.5% next

Ifo said inflation in Germany could hit as high as 3% this year. That could be explained by “accelerated increase in prices over the course of 2021” in apparent in energy, food, and some service industries.

Inflation is expected to slow to 2.0-2.5% next year. But Head of Forecasts Timo Wollmershäuser said: “At the beginning of 2022, the special factors that have been driving inflation will peter out: it will be a year since the reduction in VAT was reversed and energy prices reached their pre-crisis levels,”

Separately, ECB Governing Council member Pablo Hernandez de Cos said, “ECB is monitoring the inflation performance closely but we are not seeing any second-round impacts.”

UK CPI surged from 2% to 3.2% yoy in Aug, largest monthly leap on record

UK CPI surged to 3.2% yoy in August, up from 2.0% yoy, above expectation of 2.9% yoy. That sharp 1.2% jump in CPI was the highest leap recorded, but ONS said “this is likely to be a temporary change. CPI core rose to 3.1% yoy, up from 1.8% yoy, above expectation of 2.9% yoy. RPI also rose to 4.8% yoy, up from 3.8% yoy, above expectation of 4.6% yoy.

Also released, PPI input came in at 0.4% mom, 11.0% yoy, versus expectation of 0.2% mom, 10.3% yoy. PPI output was at 0.7% mom, 5.9% yoy, versus expectation of 0.4% mom, 5.4% yoy. PPI core output was at 1.0% mom, 5.4% yoy.

China retail sales grew only 2.8% yoy in Aug, way below expectation

China retail sales growth slowed sharply to 2.8% yoy in August , down from July’s 8.5% yoy, well below expectation of 7.1% yoy. China industrial production growth slowed further to 5.3% yoy, below expectation of 5.8% yoy. Fixed asset investment rose 8.9% ytd yoy, below expectation of 9.1%.

In a released, the National Bureau of Statistics said, “generally speaking, in August, the national economy maintained the trend of recovery. However, we must be aware that the international environment is still complicated and severe. At home, it has been felt that the sporadic outbreak of COVID-19 and natural disasters such as floods had caused impact on the economy, and the foundation for the economic recovery still needs to be consolidated”.

Australia Westpac consumer sentiment rose to 106.2, strong resilient despite lockdown

Australia Westpac-MI consumer sentiment rose 2.0% to 106.2 in September. The index remained comfortably above the levels five years prior to the pandemic. Confidence in New South Wales rose 5.3% while Victoria was steady at 104.1, despite extended lockdown in both states. Queensland jumped 8.4% to 111.6. Overall, the data indicates strong resilience of consumer sentiment and positives reactions to vaccination progresses.

Westpac added that given that RBA has already defer the next review of the asset purchase program to February, it’s highly unlikely that there will be any policy changes before that meeting. Nevertheless, it added, “with the US Federal Reserve likely to have begun its tapering program by then and the economy likely to be bouncing back as high vaccination levels see easing restrictions, we expect the Board to further taper its bond purchases in February.”

OECD downgrades Australia growth forecast, urge broad RBA review

In the latest Economy Survey of Australia, OECD downgraded the country’s GDP growth to 4.0% in 2021 and 3.3% in 2022, from May’s forecast of 5.1% and 3.4% respectively. It said the upcoming post-restriction recovery may be “more gradual than in past episodes”, as it will “occur in an environment of higher virus transmission”. COVID-19 outbreaks in other states than New South Wales and Victoria, could deepen the economic shock. “Any ratcheting up of tensions with China could further weaken trade activity.”

OECD also pointed out that underlying inflation has undershot RBA’s target band for an extended period of time. It suggested that RBA should “conduct a monetary policy framework review that is broad in scope, transparent and involves consultation with a wide variety of relevant stakeholders.”

In response, Treasurer Josh Frydenberg said, “it’s something I will give consideration to in terms of looking at the RBA, looking at the monetary policy settings and learning from the experience through the pandemic. The RBA has performed very well through this crisis, its policy response has been in sync and coordinated with the government’s fiscal response.”

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.42; (P) 109.79; (R1) 110.05; More…

USD/JPY’s decline accelerates today and immediate focus is now on 109.10 support. Firm break there will argue that larger fall from 111.65 is resuming. Intraday bias will be turned back to the downside for 108.71 support first, and then 38.2% retracement of 102.58 to 111.65 at 108.18 next. On the upside, break of 110.44 resistance will turn bias back to the upside for 110.79 first.

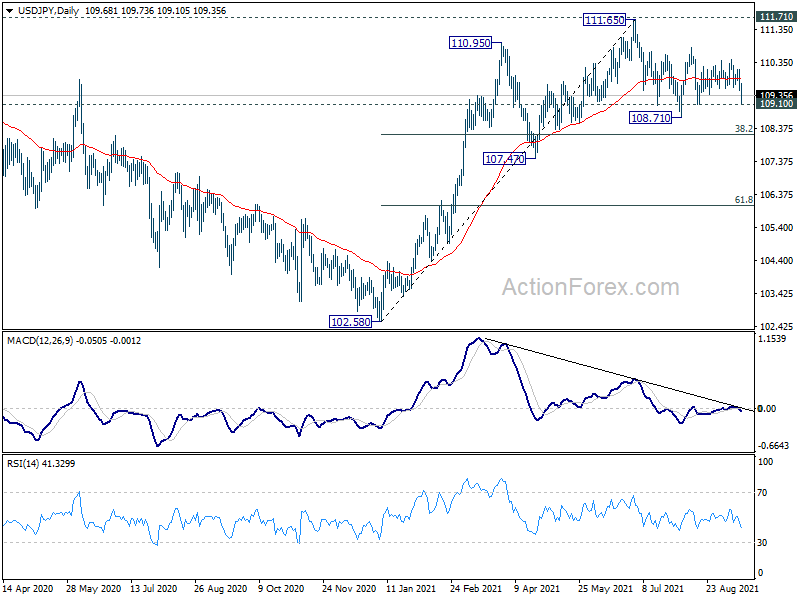

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. The pattern from 101.18 could still extend with another falling leg. Sustained trading below 55 day EMA will bring deeper fall to 107.47 support and below. Nevertheless, strong break of 111.71 resistance will confirm completion of the corrective decline from 118.65 (2016 high). Further rise should then be seen to 114.54 and then 118.65 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q2 | -1.40B | -2.15B | -2.90B | -3.19B |

| 23:50 | JPY | Machinery Orders M/M Jul | 0.90% | 3.10% | -1.50% | |

| 00:30 | AUD | Westpac Consumer Confidence Sep | 2.00% | -4.40% | ||

| 02:00 | CNY | Retail Sales Y/Y Aug | 2.50% | 7.10% | 8.50% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Aug | 8.90% | 9.10% | 10.30% | |

| 02:00 | CNY | Industrial Production Y/Y Aug | 5.30% | 5.80% | 6.40% | |

| 06:00 | GBP | CPI M/M Aug | 0.70% | 0.50% | 0.00% | |

| 06:00 | GBP | CPI Y/Y Aug | 3.20% | 2.90% | 2.00% | |

| 06:00 | GBP | Core CPI Y/Y Aug | 3.10% | 2.90% | 1.80% | |

| 06:00 | GBP | RPI M/M Aug | 0.60% | 0.30% | 0.50% | |

| 06:00 | GBP | RPI Y/Y Aug | 4.80% | 4.60% | 3.80% | |

| 06:00 | GBP | PPI Input M/M Aug | 0.40% | 0.20% | 0.80% | 1.30% |

| 06:00 | GBP | PPI Input Y/Y Aug | 11.00% | 10.30% | 9.90% | |

| 06:00 | GBP | PPI Output M/M Aug | 0.70% | 0.40% | 0.60% | 0.80% |

| 06:00 | GBP | PPI Output Y/Y Aug | 5.90% | 5.40% | 4.90% | |

| 06:00 | GBP | PPI Core Output M/M Aug | 1.00% | 0.70% | ||

| 06:00 | GBP | PPI Core Output Y/Y Aug | 5.30% | 3.90% | ||

| 08:30 | GBP | DCLG House Price Index Y/Y Jul | 8.00% | 12.40% | 13.20% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Jul | 1.50% | 0.50% | -0.30% | |

| 12:30 | CAD | CPI M/M Aug | 0.20% | 0.10% | 0.60% | |

| 12:30 | CAD | CPI Y/Y Aug | 4.10% | 3.90% | 3.70% | |

| 12:30 | CAD | CPI Common Y/Y Aug | 1.80% | 1.70% | 1.70% | |

| 12:30 | CAD | CPI Median Y/Y Aug | 2.60% | 2.60% | 2.60% | |

| 12:30 | CAD | CPI Trimmed Y/Y Aug | 3.30% | 3.10% | 3.10% | |

| 12:30 | USD | Empire State Manufacturing Index Sep | 34.3 | 17.1 | 18.3 | |

| 12:30 | USD | Import Price Index M/M Aug | -0.30% | 0.30% | 0.30% | |

| 13:15 | USD | Industrial Production M/M Aug | 0.4% | 0.40% | 0.90% | |

| 13:15 | USD | Capacity Utilization Aug | 76.4% | 76.30% | 76.10% | |

| 14:30 | USD | Crude Oil Inventories | -3.6M | -1.5M |

{kind=link}