The forex markets are pretty steady in Asia session today, with major pairs and crosses bounded inside yesterday’s range. Sentiment is mixed as investors are awaiting to see Russia would invade Ukraine on February 16, as media reported. But the rally in Gold suggests that investors are getting nervous on the risks. For now, Swiss Franc and Yen are the stronger ones, while Euro and Sterling are soft together with Kiwi.

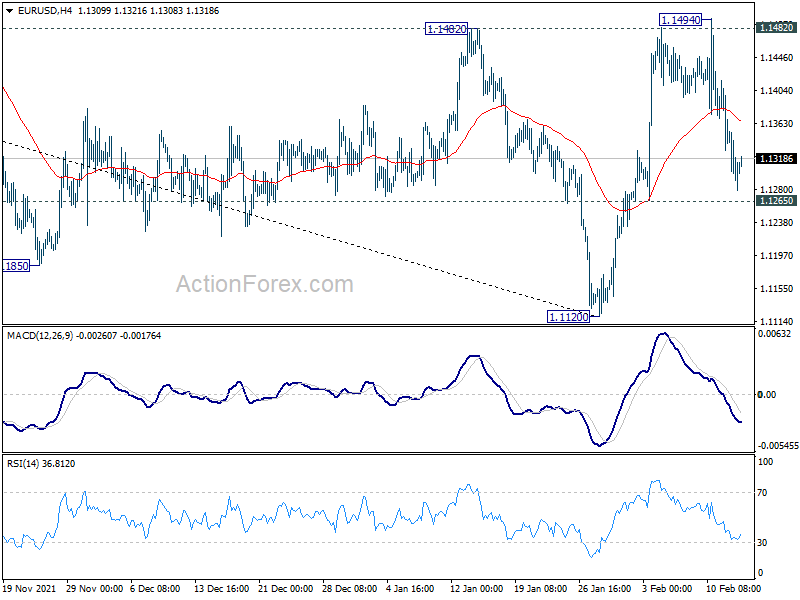

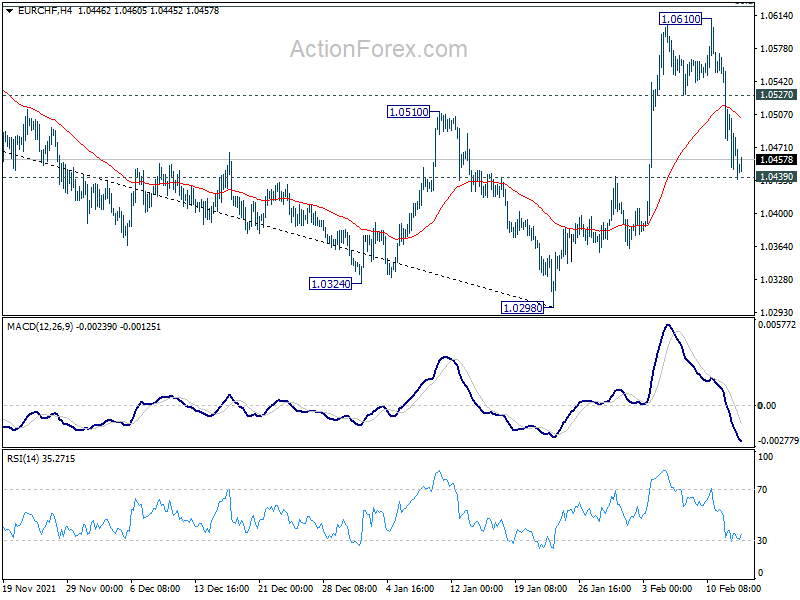

Technically, Euro is starting to look vulnerable as geopolitical risks clearly outweighs prospect of interest rate hike. In particular, we’ll pay attention to EUR/CHF’s reaction to 1.0439 minor support, as well as EUR/USD’s reaction to 1.1265 minor support. Break of these levels will indicate that near term rebound in the two pairs completed. They will then be heading back to 1.0298 and 1.1120 low respectively, with prospects of downside breakout.

In Asia, at the time of writing, Nikkei is down -0.37%. Hong Kong HSI is down -0.67%. China Shanghai SSE is up 0.40%. Singapore Strait Times is down -0.35%. Japan 10-year JGB yield is down -0.0006 at 0.218. Overnight, DOW dropped -0.49%. S&P 500 dropped to 0.38%. NASDAQ dropped -0.00%. 10-year yield rose 0.041 to 1.996, after hitting 2.026.

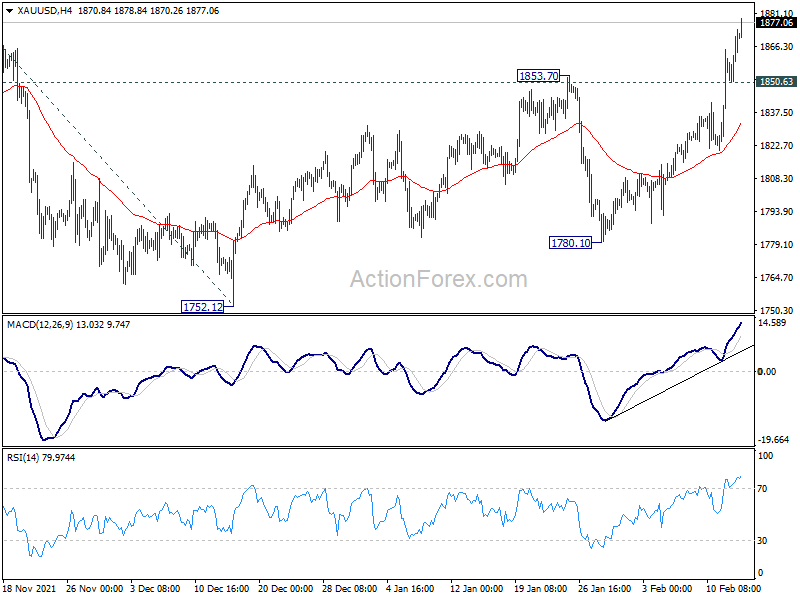

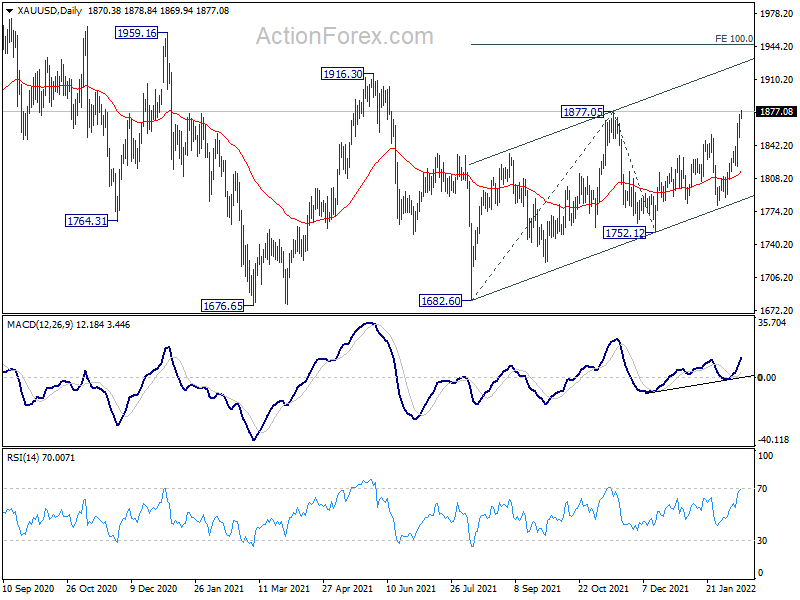

Gold upside breakout, ready for 1916 resistance

Gold rises further to as high as 1878.84 so far today. The break of 1877.05 resistance indicates resumption of whole rally from 1682.60. Further rally will be expected as long as 1850.63 support holds. 1916.30 resistance is the next target and break there will pave the way to 100% projection of 1682.60 to 1877.05 from 1752.12 at 1946.57.

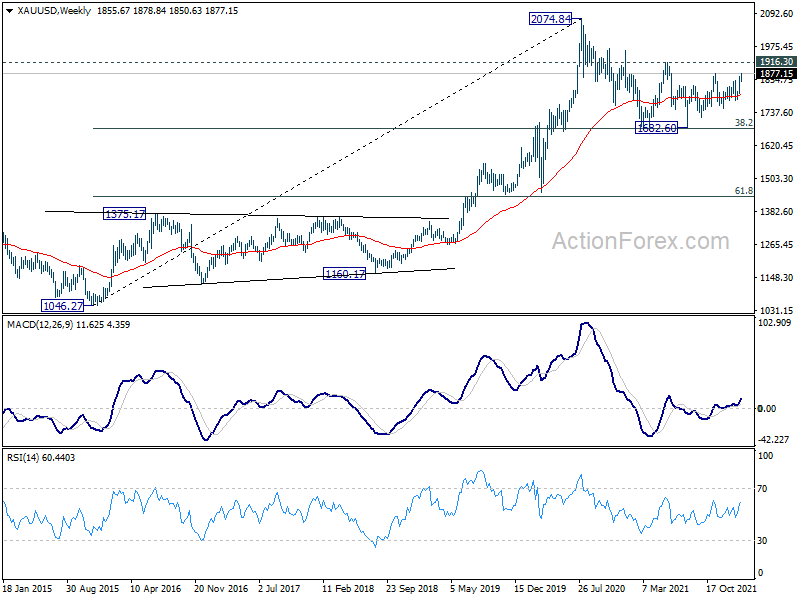

More importantly, sustained break of 1946.57 will affirm the case that whole medium term correction from 2074.84 has completed at 1682.60, after hitting 38.2% retracement of 1046.27 to 2074.84. That is, retest of 2074.84 should be seen next with prospect of resuming the long term up trend at a later stage.

BoJ Kuroda: Baseline for economy and prices to gradually pick up

BoJ Governor Haruhiko Kuroda reiterated that the baseline forecast is for Japan’s economy and prices to gradually pick up as rising real household income underpins consumption. Nevertheless, the “economic and price conditions warrant maintaining our easy monetary policy.”

He acknowledged that the market operation of an offer to buy unlimited amount of bonds on Monday successfully pushed 10-year JGB yield from near 0.25% to 0.22%. But he emphasized it’s a “last resort” and a “powerful means not used explicitly by other central banks.” “We don’t expect to conduct such operation frequently. We’ll do this as needed,” he added.

Japan GDP grew 1.3% qoq in Q4, remains slightly be pre-pandemic level

Japan GDP grew 1.3% qoq in Q4, slightly below expectation of 1.4% qoq. In annualized term, GDP grew 5.4%, below expectation of 5.8%.

Private consumption grew 2.7% qoq, accounting for much of the growth. Capital expenditure rose 0.4% qoq. External demand rose 0.2% qoq.

For 2021 as a whole, GDP grew 1.7%, marking the first expansion in three years. The seasonally-adjusted real GDP size at JPY 541T remains slightly below pre-pandemic level of late 2019.

RBA minutes: Prepared to be patient on interest rate

In the minutes of February 1 meeting, RBA reiterated that it “will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target band.” It’s “too early to conclude that it was sustainably within the target band”. There were uncertainties about “how persistent the pick-up in inflation would be as supply-side problems were resolved” and “wages growth also remained modest”. The central bank is “prepared to be patient”.

Omicron outbreak “had affected the economy, but had not derailed the recovery”. The economy was “resilient” and was expected to “pick up as case numbers trended lower”. Job market had “recovered strongly” with central forecasts seeing unemployment to fall to “levels not seen since early 1970s”. Wages growth was expected to pick-up, buy only gradually.

Inflation had “picked up more quickly than the Bank had expected”, but was still “lower than in many other countries”. “Some moderation” in inflation was expected as “supply problems were resolved.” Stronger growth in labour costs was expected to become the “more important driver of inflation”. The central forecast was for underlying inflation to be within the target band over both 2022 and 2023.

A decision about reinvestment of asset purchases would be made at the May meeting, with the key considerations being the “state of the economy and the outlook for inflation and unemployment.”

Looking ahead

UK employment data will be a main feature in European session. Eurozone GDP and Germany ZEW economic sentiment will also be closely watched. Later in the day, US will release PPI and Empire state manufacturing index. Canada will release housing starts.

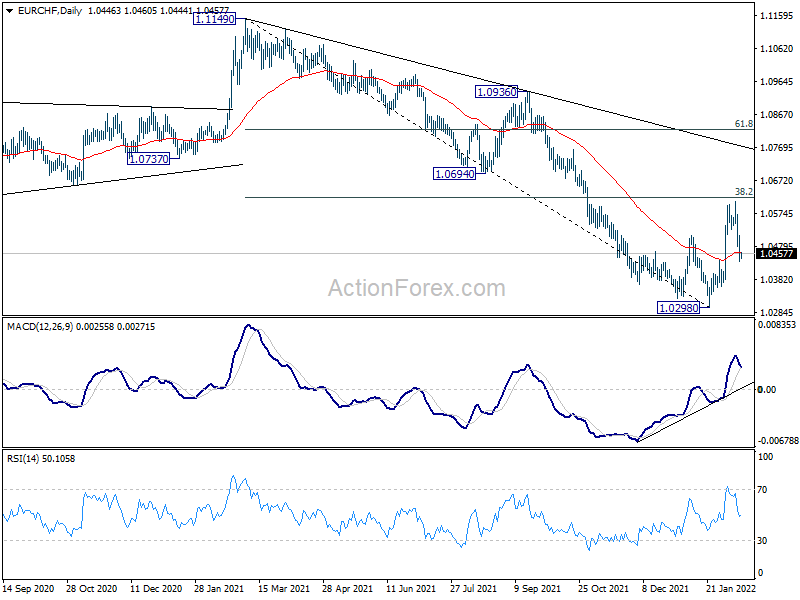

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0423; (P) 1.0469; (R1) 1.0499; More….

Immediate focus is now on 1.0439 support in EUR/CHF. Firm break there should confirm that rebound from 1.0298 has completed, ahead of 38.2% retracement of 1.1149 to 1.0298 at 1.0623. Deeper fall will then be seen back to retest 1.0298 low. On the upside, break of 1.0527 minor resistance will clear near term downside risk and bring stronger rebound back to 1.0623 fibonacci resistance instead.

In the bigger picture, a medium term bottom was formed at 1.0298 on bullish convergence condition in daily MACD. Rebound from there is still tentatively viewed part of a corrective pattern. That is, larger down trend from 1.2004 (2018) could still extend through 1.0298 to 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223. However, sustained trading above 55 week EMA (now at 1.0673) will argue that the down trend is over, and bring stronger rise back to 1.1149 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q4 P | 1.30% | 1.40% | -0.90% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | -1.30% | -1.20% | -1.20% | |

| 00:30 | AUD | RBA Minutes | ||||

| 04:30 | JPY | Industrial Production M/M Dec F | -1.00% | -1.00% | ||

| 07:00 | GBP | Claimant Count Change Jan | -43.3K | |||

| 07:00 | GBP | ILO Unemployment Rate (3M) Dec | 4.10% | 4.10% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Dec | 3.60% | 3.80% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Dec | 3.90% | 4.20% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | -2.5B | -1.3B | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.30% | 0.30% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 P | 0.40% | 0.90% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Feb | 53.5 | 51.7 | ||

| 10:00 | EUR | Germany ZEW Current Situation Feb | -7 | -10.2 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Feb | 52.3 | 49.4 | ||

| 13:15 | CAD | Housing Starts Jan | 270.0K | 236.1K | ||

| 13:30 | USD | Empire State Manufacturing Index Feb | 10 | -0.7 | ||

| 13:30 | USD | PPI M/M Jan | 0.60% | 0.20% | ||

| 13:30 | USD | PPI Y/Y Jan | 9.20% | 9.70% | ||

| 13:30 | USD | PPI Core M/M Jan | 0.50% | 0.50% | ||

| 13:30 | USD | PPI Core Y/Y Jan | 8.10% | 8.30% |

{kind=link}